Are you ready to navigate Seattle’s fast-changing real estate landscape in 2026? For first time homebuyers, understanding the latest trends in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett is essential.

This guide equips first time homebuyers with the tools and confidence to make informed decisions. You’ll discover up-to-date market data, budgeting strategies, mortgage options, and proven steps to secure your dream home.

We’ll highlight success stories and offer actionable tips, ensuring your path to homeownership in the Seattle area is both achievable and rewarding.

Understanding the 2026 Seattle Housing Market

Navigating the Seattle housing market in 2026 requires first time homebuyers to stay informed and adaptable. Market conditions are evolving quickly, with new opportunities and challenges emerging across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

Key Market Trends for First-Time Buyers

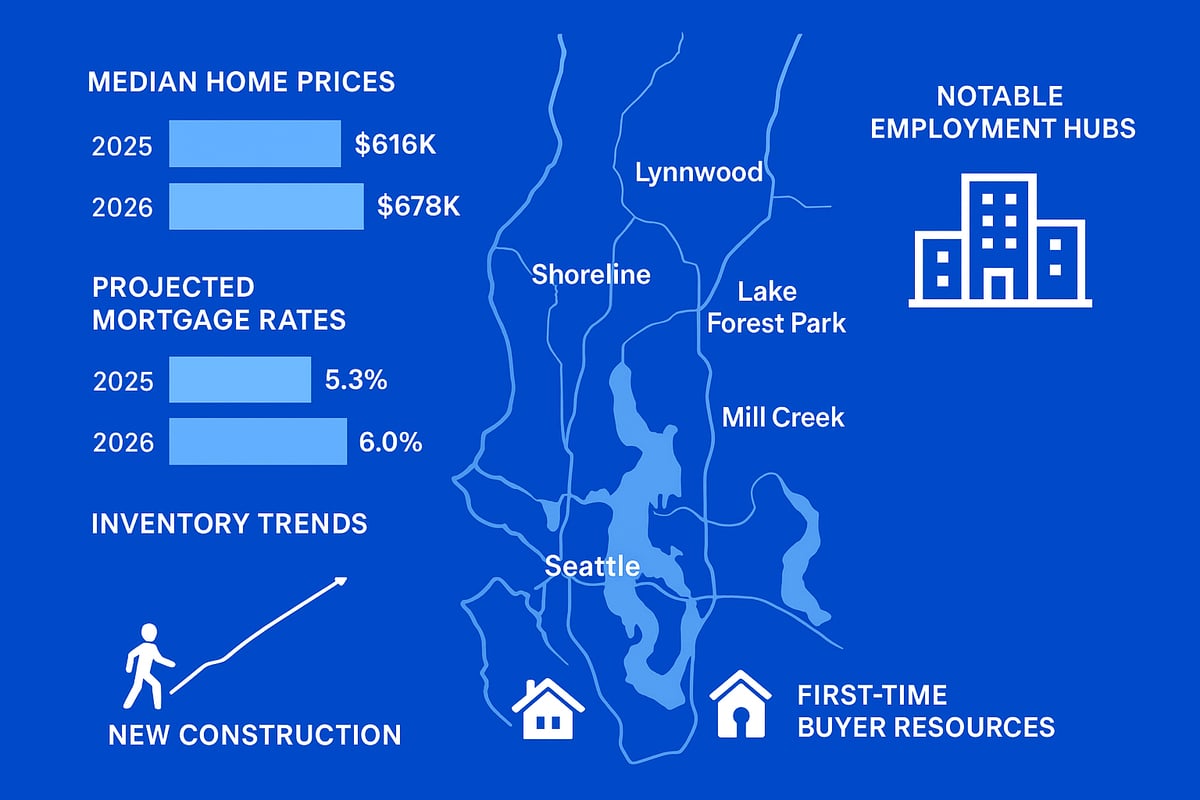

In 2026, the Seattle housing market is seeing notable shifts that directly impact first time homebuyers. Median home prices in Seattle are forecasted to reach $845,000, while nearby cities like Shoreline, Lynnwood, and Everett offer more accessible options, with averages ranging from $650,000 to $725,000.

Inventory levels are expected to rise modestly, providing more choices but keeping competition high, especially in desirable neighborhoods. Projected mortgage rates hover around 6.2 percent, which influences monthly affordability for first time homebuyers.

Local employment remains strong, especially in the tech sector, fueling demand and supporting price stability. Remote work trends continue to affect housing preferences, with many buyers seeking homes in Lake Forest Park and Mill Creek for added space.

For a detailed look at projected home values and sales trends, see the Seattle housing market forecast 2026.

| City | 2025 Median Price | 2026 Median Price (Projected) | Inventory Trend |

|---|---|---|---|

| Seattle | $810,000 | $845,000 | Up 7 percent |

| Shoreline | $690,000 | $710,000 | Up 5 percent |

| Lynnwood | $650,000 | $675,000 | Up 6 percent |

| Everett | $620,000 | $655,000 | Up 6 percent |

Challenges and Opportunities in the Greater Seattle Area

First time homebuyers in Seattle and surrounding cities face continued competition, often encountering bidding wars in popular areas. However, first time homebuyers have unique advantages, such as fewer contingencies and eligibility for special programs.

New construction is becoming more available in Lynnwood and Mill Creek, offering modern amenities but sometimes higher prices and longer timelines. Resale homes in established neighborhoods like Lake Forest Park may require updates but can be more affordable.

Local policies and new housing initiatives are increasing inventory and creating more pathways for first time homebuyers. For instance, Everett has seen successful pilot programs that helped several first time homebuyers secure homes with minimal contingencies.

Staying informed about zoning changes and city incentives is essential for maximizing your search and finding the best fit for your needs as a first time homebuyer.

Timing Your Purchase in 2026

Timing is crucial for first time homebuyers aiming to enter the Seattle market. Historically, late spring and early summer see the most listings, but also heightened competition. Fall and winter may present better opportunities, with fewer buyers and more motivated sellers.

Interest rates are expected to fluctuate throughout 2026, so monitoring market conditions can help first time homebuyers lock in a favorable rate. Using online tools and real-time market alerts can make the difference between missing out and making a successful offer.

Acting quickly when the right home appears is key, especially in fast-moving markets like Shoreline and Everett. Collaborate with your agent to track trends and respond strategically, balancing timing with your personal readiness as a first time homebuyer.

Local Resources and Support for Buyers

Seattle and its neighboring cities offer robust support for first time homebuyers. City and county programs provide down payment assistance, grants, and access to affordable housing.

Free workshops and homebuyer education classes are available through organizations like the Washington State Housing Finance Commission, equipping first time homebuyers with essential knowledge. Many local lenders also offer counseling services to guide you through budgeting and the application process.

Accessing up-to-date data and local market reports will empower your search, helping you compare neighborhoods and make informed decisions. Leveraging these resources is vital for building confidence and success as a first time homebuyer in Seattle or any of its vibrant suburbs.

Preparing Financially for Your First Home

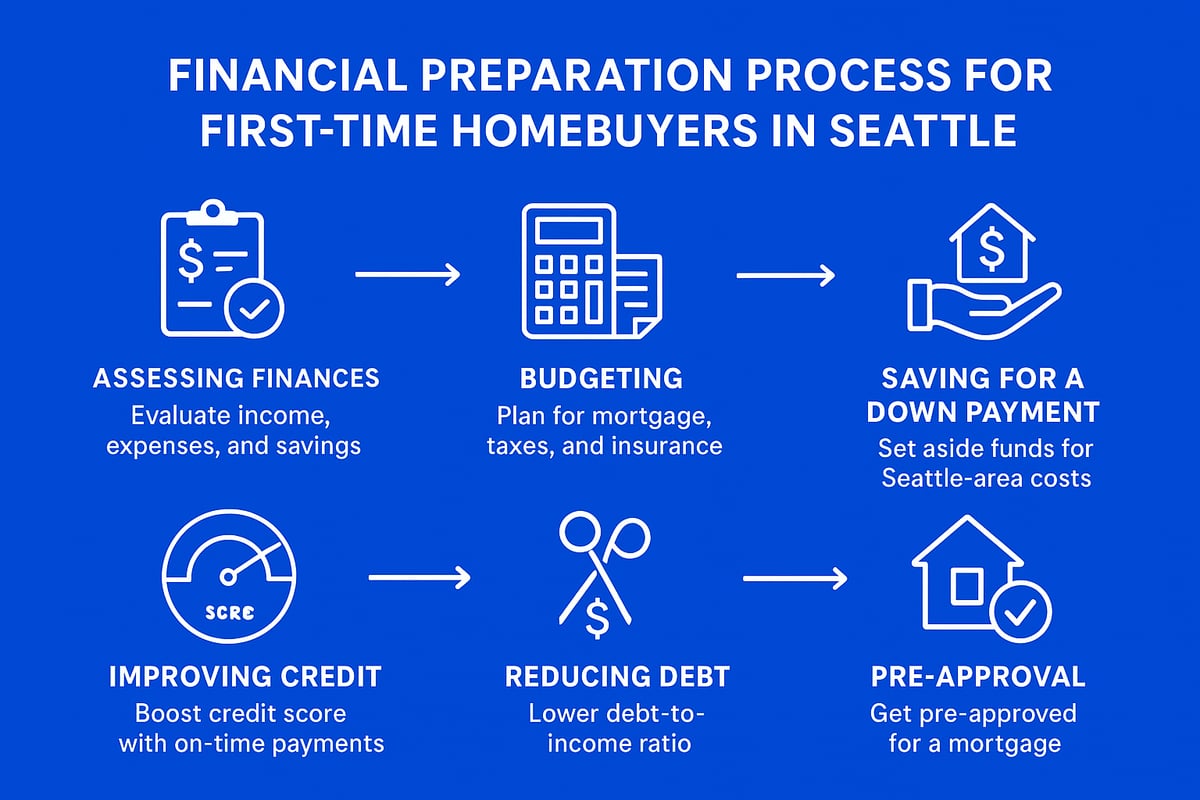

Getting financially prepared is the first and most important step for first time homebuyers in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. With local prices rising and lending criteria changing, understanding your finances will help you shop confidently and avoid surprises. Let’s walk through what you need to know to make your first purchase a success.

Budgeting and Calculating Affordability

Before you start touring homes, evaluate your financial health. First time homebuyers should review income, debts, and credit scores. This helps you set a realistic budget. Use the 28/36 rule: keep your monthly housing costs under 28 percent of gross income, and total debt below 36 percent.

In Seattle, Everett, and nearby cities, factor in property taxes, insurance, and HOA dues. For example, a $700,000 home in Everett might require $7,000 annually in taxes and $1,200 for insurance. Many online calculators let you input Seattle-area costs for accurate estimates.

- Review your paystubs, debts, and monthly expenses

- Estimate total monthly payment, including taxes and insurance

- Adjust your price range based on comfort, not just lender limits

Planning ahead helps first time homebuyers avoid financial stress and make informed decisions.

Saving for a Down Payment and Closing Costs

Most first time homebuyers in Seattle put down 3 to 5 percent, but larger down payments can lower monthly costs. Closing costs, typically 2 to 5 percent of the purchase price, include lender fees, escrow, and title insurance.

Boost your savings with high-yield accounts or side gigs. Some buyers use gift funds from family or employer assistance programs. Explore local grants and down payment assistance, especially in Shoreline and Lynnwood. For a detailed breakdown of available options and requirements, see Down payment options Washington State.

- Set up automatic transfers to a savings account

- Research grants and forgivable loans in your city

- Track closing costs with a Seattle-focused worksheet

By being proactive, first time homebuyers can secure their dream home with confidence.

Understanding and Improving Your Credit Score

Your credit score directly impacts your mortgage options and interest rates. Most lenders require a minimum score of 620 for conventional loans, while FHA loans may accept 580 or above. VA loans have flexible criteria, helpful for first time homebuyers with military backgrounds in Mill Creek or Everett.

To improve your score, pay all bills on time, reduce credit card balances, and avoid new debt. Review your credit report for errors and dispute any inaccuracies. Even a small increase in your score can save thousands over the life of your mortgage.

- Check your score at least six months before applying

- Avoid major purchases or new credit cards

- Use free credit monitoring tools

A strong credit profile gives first time homebuyers more choices and better rates.

Reducing Debt and Strengthening Your Application

Lenders assess your debt-to-income (DTI) ratio to determine loan eligibility. In Seattle, where home prices are high, keeping a lower DTI can make your application more attractive. Pay down student loans, car payments, and credit cards to improve your ratio.

Not all debt is viewed equally. Installment loans (like student loans) are less risky than high credit card balances. If possible, consolidate or pay off high-interest debt before applying. Document any recent debt reductions for your lender.

- Calculate your DTI using a local mortgage calculator

- Prioritize paying off high-interest accounts

- Avoid taking on new debt during the buying process

First time homebuyers with strong applications stand out in Seattle’s competitive market.

Getting Pre-Approved: The First Step

Pre-approval is essential for first time homebuyers in fast-paced markets like Seattle, Shoreline, or Everett. It shows sellers you’re serious and ready to close. Gather recent paystubs, W-2s, bank statements, and ID before meeting with a lender.

The process typically takes a few days. Your lender will review your financials and issue a pre-approval letter, which strengthens your offer. Stay responsive and keep your documents updated for a smooth experience.

With pre-approval, first time homebuyers can confidently search for homes, knowing exactly what they can afford.

Exploring Mortgage Options for Seattle First-Time Buyers

Choosing the right mortgage is one of the most important steps for first time homebuyers in Seattle and nearby cities like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Understanding the available loan types, local programs, and the true costs can help first time homebuyers make confident, informed decisions in 2026.

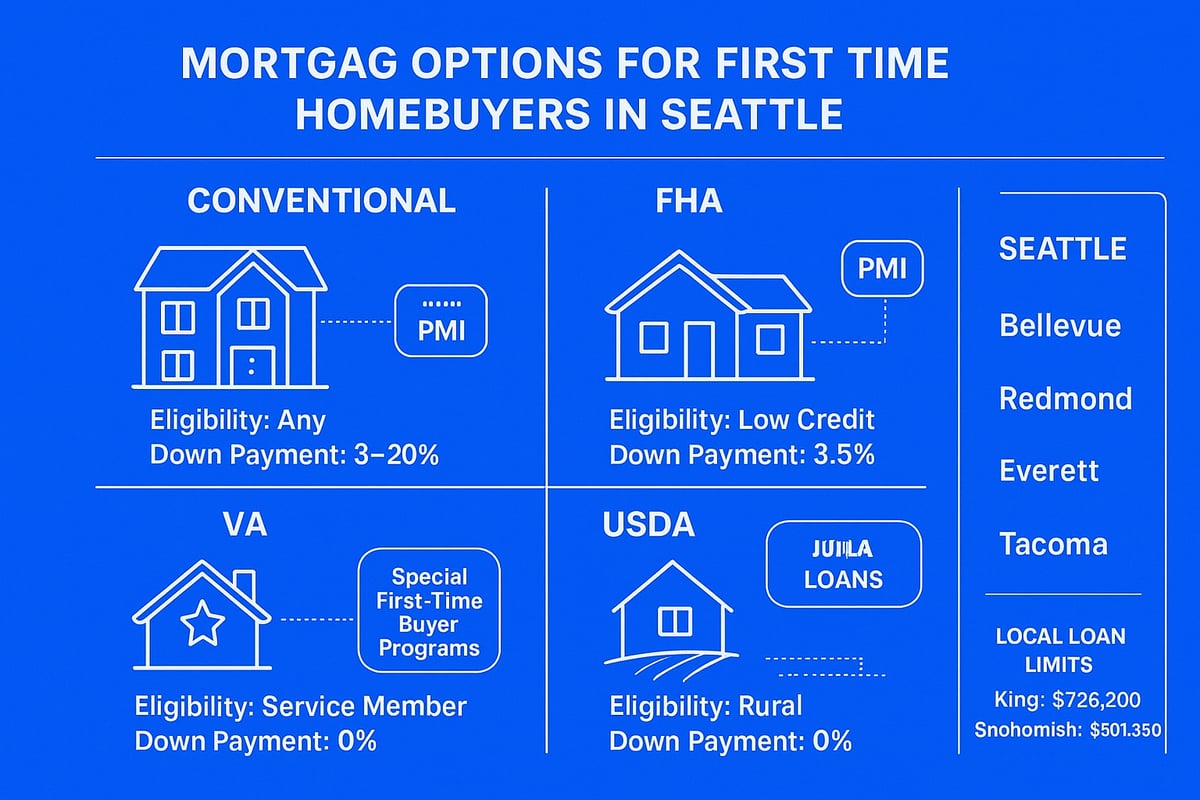

Conventional, FHA, VA, and USDA Loans Explained

For first time homebuyers, the four main mortgage types are Conventional, FHA, VA, and USDA loans. Each comes with unique benefits and requirements, making it crucial to compare options based on your financial profile and homebuying goals.

| Loan Type | Minimum Down Payment | Key Eligibility | Local Loan Limits (2026) | Pros & Cons |

|---|---|---|---|---|

| Conventional | 3% | Good credit, stable income | King: $850K, Snohomish: $800K | Lower PMI, flexible terms |

| FHA | 3.5% | 580+ credit, moderate income | Same as above | Easier to qualify, higher PMI |

| VA | 0% | Veterans/military only | Up to $1M+ | No PMI, competitive rates |

| USDA | 0% | Rural areas, income limits | Area-specific | No down payment, limited areas |

Local buyers in Shoreline or Everett may find FHA appealing for lower credit, while tech professionals in Seattle might benefit from conventional or VA options. For further details on each loan type, see this guide on home loans for first-time buyers.

Special First-Time Homebuyer Programs in Seattle

Seattle and its neighboring areas offer a range of programs designed to help first time homebuyers succeed. The Washington State Housing Finance Commission (WSHFC) provides initiatives like Home Advantage and House Key Opportunity, which offer down payment assistance and below-market rates.

Local programs in Shoreline, Lynnwood, and Everett may provide grants or forgivable loans for eligible buyers. These often require:

- Income below set limits (varies by city and program)

- Completion of a homebuyer education class

- Use of an approved lender

For example, a Mill Creek buyer might qualify for a city-specific grant, while a Lake Forest Park resident could access county-level assistance. Check eligibility early, as program funds can be limited in 2026.

Choosing the Right Loan for Your Needs

Fixed-rate mortgages offer predictable payments, which many first time homebuyers prefer in a changing interest rate environment. Adjustable-rate mortgages (ARMs) can start with lower rates but may rise after a few years.

When comparing loans, review both the interest rate and the annual percentage rate (APR), which includes fees. Request loan estimates from several Seattle-area lenders to find the best fit for your budget and long-term plans. Local mortgage brokers can explain how options differ in Everett versus Seattle.

Understanding Private Mortgage Insurance (PMI) and Other Costs

First time homebuyers putting less than 20% down generally pay Private Mortgage Insurance (PMI) on conventional loans. In Seattle, this can add $100–$300 per month, depending on your loan amount and credit.

Ways to avoid PMI include:

- Increasing your down payment

- Using lender-paid PMI options

- Choosing a VA loan if eligible

Other common fees include origination, appraisal, title, and escrow. These costs vary by city but are typically disclosed up front during the loan process.

Jumbo Loans and Financing High-Cost Seattle Homes

Home prices in Seattle and the Eastside often exceed conforming loan limits, especially for tech professionals with higher incomes. In 2026, the conforming limit is $850,000 for King County and $800,000 for Snohomish County.

Jumbo loans cover amounts above these limits but have stricter requirements, such as higher credit scores, larger down payments, and thorough documentation of assets, including RSUs or stock bonuses. First time homebuyers in Mill Creek or Lake Forest Park considering jumbo loans should consult with a local expert to navigate these complexities.

Step-by-Step Homebuying Process in Seattle

Buying a home in Seattle can feel overwhelming, especially for first time homebuyers. Understanding each step in the process helps reduce stress and builds your confidence. Whether you are searching in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, following a clear roadmap gives you an edge in the 2026 market.

Finding the Right Real Estate Agent

For first time homebuyers, partnering with a knowledgeable real estate agent is crucial. A great agent in Seattle or nearby cities should have deep local market knowledge, strong negotiation skills, and a history of helping first time homebuyers succeed.

Ask about their experience in neighborhoods like Mill Creek or Everett. Compare agents by reviewing online testimonials and recent sales. Important qualities include:

- Expertise in first time homebuyers’ needs

- Familiarity with Seattle-area programs and incentives

- Proactive communication and availability

A trusted agent will guide you from the first viewing to closing, making the complex process manageable for first time homebuyers.

House Hunting in Seattle and Surrounding Cities

Once you have chosen an agent, you will begin house hunting. Use MLS, Redfin, and local listing services to search for homes in Seattle, Shoreline, or Lake Forest Park. Touring homes in person or through virtual tours is essential for first time homebuyers to assess property conditions and layouts.

When comparing homes in Lynnwood versus Lake Forest Park, consider age, amenities, and commute times. Open houses and private showings reveal details not visible online. For more practical advice and strategies, check out Seattle first-time buyer tips.

Create a checklist of must-haves and nice-to-haves. This step helps first time homebuyers focus their search and make informed decisions.

Making a Competitive Offer

Seattle’s 2026 market is competitive, so first time homebuyers must move quickly when making an offer. Your agent will help you analyze comparable sales and determine a fair price. In multiple-offer situations, consider strengthening your offer with a larger earnest money deposit or fewer contingencies.

Common contingencies include:

- Home inspection

- Financing approval

- Appraisal

Understanding earnest money is important. In Seattle, this deposit shows your commitment and is applied toward your purchase if the deal closes. For first time homebuyers, a strong offer often makes the difference.

Navigating the Inspection and Appraisal Process

After your offer is accepted, the inspection and appraisal begin. In Seattle’s climate, inspections often reveal foundation, roof, or drainage issues, especially in older homes. First time homebuyers should attend the inspection to ask questions and understand potential repairs.

The appraisal determines if the home’s value matches your offer. If the appraisal is low, you may need to renegotiate or bring extra funds to closing. Your agent will help you navigate these steps, ensuring first time homebuyers are protected and informed.

Securing Financing and Finalizing the Loan

Once the inspection and appraisal are complete, your lender begins finalizing your mortgage. First time homebuyers must submit updated financial documents and respond quickly to lender requests.

The underwriting process involves:

- Verifying income, assets, and employment

- Reviewing credit and debt-to-income ratios

- Ensuring the property meets lender guidelines

Address any lender conditions promptly. Staying organized helps first time homebuyers avoid delays and keeps the process on track.

Closing on Your Home: What to Expect

Closing is the final step for first time homebuyers in Seattle. You will receive a closing disclosure outlining all costs. A final walk-through ensures the home is in agreed-upon condition.

Typical closing costs include:

- Loan origination and processing fees

- Title insurance and escrow charges

- Homeowners insurance premiums

Sign documents either in person or remotely, depending on what is offered in King and Snohomish counties. After funds are transferred, first time homebuyers receive the keys to their new home.

Moving In and Next Steps

Congratulations, you are now a homeowner. As first time homebuyers, your next steps include setting up utilities, changing your address, and reviewing a move-in checklist.

Key tasks to remember:

- Schedule utility connections for electricity, water, and internet

- Update your address with the post office and financial institutions

- Review home maintenance tips for Seattle’s climate

Connect with local resources and neighborhood groups to make your transition smooth. First time homebuyers who plan ahead enjoy a seamless move and peace of mind.

Navigating Down Payment Assistance and Grants in Seattle

Overview of Available Assistance Programs

Seattle and its surrounding cities offer several robust down payment assistance programs designed specifically for first time homebuyers. The Washington State Housing Finance Commission (WSHFC) provides popular options like the Home Advantage and House Key Opportunity programs. These initiatives often combine low-interest loans with down payment grants.

Local governments, including the City of Seattle, Shoreline, and King County, also provide targeted grants that can be layered with state resources. Eligibility usually depends on factors such as income, credit score, and the intended home’s purchase price. Many programs require buyers to complete a homebuyer education class, which is conveniently available through the Washington State Housing Finance Commission programs.

Applying for Down Payment Assistance

The application process for down payment assistance is straightforward but requires careful attention to details. First time homebuyers should start by consulting with an approved lender who is familiar with Seattle-area programs. Next, gather essential documentation, including proof of income, recent tax returns, and a credit report.

After verifying eligibility, submit your application along with the supporting documents. Most assistance programs review applications within a few weeks. It is crucial to work with a housing counselor or mortgage broker who understands the unique requirements for Seattle, Shoreline, and Everett buyers. Completing a homebuyer education course is often required prior to final approval.

Pros and Cons of Using Assistance Programs

Leveraging down payment assistance offers clear advantages, especially for first time homebuyers navigating Seattle’s competitive market. These programs reduce upfront costs and can help buyers secure homes sooner. However, some assistance comes as a second loan that must eventually be repaid, and certain grants have restrictions on how long you must live in the property.

Consider the loan type you plan to use, as some assistance programs pair only with FHA, VA, or specific conventional loans. For example, a Lynnwood buyer may use a forgivable grant to lower their down payment but must remain in the home for a set number of years to avoid repayment. Always review the program’s terms carefully and consult with your lender before committing.

Tips for Maximizing Your Homebuying Budget

First time homebuyers can maximize their budget by stacking multiple assistance programs when allowed. For instance, combining a city grant with a state-sponsored loan can significantly reduce the cash needed at closing. Negotiating for seller credits or concessions can further offset closing costs.

Plan for future equity by choosing homes in growing neighborhoods like Mill Creek or Everett, where property values are projected to rise. Staying informed and using local resources ensures you make the most of every dollar, helping first time homebuyers move confidently toward long-term financial stability.

Frequently Asked Questions for Seattle First-Time Homebuyers

Navigating the Seattle real estate landscape as first time homebuyers can be overwhelming. Below, I answer the most common questions I receive from clients in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. These responses will help you make informed, confident decisions at every stage.

Common Mortgage and Homebuying Questions

For first time homebuyers, understanding down payment requirements is key. In Seattle, the minimum down payment ranges from 3% for conventional loans to 3.5% for FHA loans, and 0% for eligible VA or USDA buyers. Many buyers ask if they can use gift funds—yes, most loan types allow gifts from family or approved sources, provided documentation is clear.

The average time to close on a home in Seattle, Shoreline, or Everett is 30 to 45 days, depending on the loan type and market conditions. Closing can be quicker if you are fully pre approved and have your documents ready.

If you want to explore specialized programs or incentives, review the latest first-time homebuyer programs Seattle for updated options and eligibility details.

Local Market and Process FAQs

Is it better to buy in Seattle or a nearby city like Everett in 2026? The answer depends on your priorities. Seattle offers proximity to tech jobs and amenities, but nearby cities like Lynnwood and Mill Creek often provide more affordable options and less competition for first time homebuyers.

Property taxes also vary by location. King County (Seattle, Shoreline) tends to have higher rates than Snohomish County (Everett, Lynnwood, Mill Creek). For a $700,000 home, expect roughly $7,000 to $8,500 annually in taxes, but always check the local assessor’s site for specifics.

Typical closing costs for first time homebuyers in the Seattle area range from 2% to 4% of the purchase price. These include lender fees, title, escrow, and prepaid taxes or insurance. Some buyers negotiate for seller credits to offset these costs. For more on affordability trends, see this overview of Seattle housing affordability challenges.

Credit, Income, and Qualification FAQs

What credit score is needed? For most first time homebuyers, a conventional loan requires a minimum score of 620, while FHA loans allow scores as low as 580. Higher scores can secure better interest rates.

If you work in tech or have RSUs and bonuses, lenders may count a portion of your vested equity as qualifying income, especially if you have a two year history. Be prepared to provide documentation of your compensation structure.

Yes, you can buy a home with student loan debt. Lenders will look at your debt to income (DTI) ratio, which compares your monthly debts to your gross income. Keeping your DTI below 45% is ideal for most loan programs in Seattle and surrounding cities.

Post-Purchase and Homeownership FAQs

First time homebuyers often wonder what to expect after moving in. You will need to set up utilities, update your address, and review your homeowners insurance. Many cities, like Lake Forest Park and Everett, offer welcome packets and community resources for new residents.

If you think your property tax assessment is too high, you can appeal through the county assessor’s office. The process typically involves submitting comparable sales and a formal appeal within a set timeframe.

For ongoing support, look for local home maintenance workshops or neighborhood associations. These resources help first time homebuyers manage repairs, connect with service providers, and build long term value in their new home.

Pro Tips for Success in the 2026 Seattle Market

Navigating the Seattle real estate landscape as first time homebuyers in 2026 demands a competitive edge, a clear strategy, and local market savvy. Whether you are searching in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, these expert-backed tips will help you achieve your homeownership goals with confidence.

Winning Strategies for First-Time Buyers

In Seattle’s fast-paced market, first time homebuyers benefit from being prepared and decisive. Start by securing a strong pre-approval letter from a reputable local lender, which signals to sellers that you are a serious contender.

Work closely with your agent to identify properties in competitive neighborhoods like Mill Creek and Everett, and be ready to act quickly. Consider flexible closing dates or higher earnest money deposits to make your offer stand out. In multiple-offer situations, review your contingencies carefully; waiving low-risk contingencies, after consultation with your agent, can strengthen your position without unnecessary exposure.

- Obtain a full pre-approval, not just pre-qualification

- Set clear priorities for must-haves vs. nice-to-haves

- Prepare for swift decision-making on new listings

With the right approach, first time homebuyers can successfully compete, even in bidding wars.

Avoiding Common Pitfalls and Mistakes

Seattle’s market is exciting, but it is easy for first time homebuyers to make avoidable errors. Overbidding can lead to appraisal gaps, especially in hot areas like Shoreline or Lake Forest Park. Always consult your agent about the risk of offering more than the appraised value and have a plan if the appraisal comes in low.

Never skip a professional inspection, especially with older homes common in Seattle and Everett. Unnoticed issues with foundations, roofs, or drainage can result in costly repairs. Remember to budget for ongoing maintenance and unexpected expenses, not just the purchase price.

- Avoid emotional overbidding

- Prioritize thorough inspections

- Account for post-purchase expenses in your budget

By staying cautious and informed, first time homebuyers can avoid costly surprises.

Leveraging Technology and Local Expertise

Modern tools offer first time homebuyers a significant advantage. Use MLS alerts, Redfin, and local listing sites to monitor new properties in Shoreline, Lynnwood, and beyond. Virtual tours and e-signature platforms make it easier to tour homes and submit offers efficiently, even with a busy schedule.

Partnering with a local mortgage broker or agent who knows the nuances of the Seattle area is invaluable. They can provide neighborhood-specific advice, recommend trusted inspectors, and help you navigate local lending programs.

- Sign up for real-time listing alerts

- Utilize virtual walkthroughs and remote document signing

- Rely on local experts for negotiation and guidance

Tech tools and local professionals together empower first time homebuyers to move quickly and make informed choices.

Building Long-Term Wealth Through Homeownership

For first time homebuyers, owning a home in Seattle or nearby cities can be a powerful wealth-building tool. Home values in the region are projected to appreciate steadily, according to Seattle housing market trends 2026, making your purchase a smart long-term investment.

As the market evolves, consider refinancing if rates decrease, especially in areas like Lynnwood or Mill Creek where equity can build rapidly. Regular home maintenance not only protects your investment but can also boost your home’s value over time.

- Monitor market trends and refinance when advantageous

- Invest in annual maintenance and improvements

- Plan for future upgrades to maximize appreciation

With the right mindset, first time homebuyers can turn homeownership in the Seattle area into lasting financial security.

As you look ahead to buying your first home in Seattle in 2026, remember that the journey is about making informed choices that fit your goals and lifestyle. Whether you have questions about navigating local market trends, want clarity on mortgage options, or need guidance on qualifying with RSUs and bonuses, you don’t have to figure it out alone. I’m here to help you chart the best path forward, backed by years of experience and a commitment to your success. If you’re ready to talk through your next steps or simply want expert advice tailored to your situation, Let’s have a conversation.

Key Takeaways

- The article provides an Essential Guide for First Time Homebuyers in 2026, covering trends in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

- Key market trends include rising home prices, increasing inventory, and projected mortgage rates around 6.2%.

- First time homebuyers can navigate challenges through local programs, down payment assistance, and budgeting strategies.

- The homebuying process involves securing pre-approval, making competitive offers, and understanding mortgage options.

- Technological tools and local expertise empower first time homebuyers to maximize their budget and build long-term wealth.

Estimated reading time: 21 minutes