Thinking about a va mortgage loan refinance in Seattle for 2026? You are not alone. Many veterans and military families across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett are exploring their options as interest rates and home values shift.

VA loan refinances offer unique advantages compared to conventional loans. These include lower monthly payments, no private mortgage insurance, and flexible qualification standards. For local homeowners, the right refinancing strategy can unlock significant savings, provide access to home equity, or create a more stable financial future.

This comprehensive guide will walk you step by step through every aspect of va mortgage loan refinance in 2026. You will learn about VA refinance basics, eligibility, the full process, local market trends, pros and cons, and expert strategies tailored to Seattle and surrounding areas.

Understanding VA Mortgage Loan Refinance in 2026

Navigating a va mortgage loan refinance in Seattle in 2026 offers unique advantages for veterans, active duty, and military families. This process helps homeowners lower monthly payments, access home equity, or secure a more stable financial future. Understanding the essentials of va mortgage loan refinance is key for making informed decisions, especially with evolving guidelines and Seattle’s dynamic real estate market.

What is a VA Mortgage Loan Refinance?

A va mortgage loan refinance allows eligible Seattle-area veterans and service members to replace their existing VA loan with a new one, often at a lower interest rate or with different terms. Unlike conventional refinancing, this program features no private mortgage insurance, lower credit barriers, and unique benefits tied to military service.

There are two main types: the Interest Rate Reduction Refinance Loan (IRRRL), also known as the “streamline” option, and the cash-out refinance. The IRRRL is used primarily to lower your rate or payment with minimal paperwork, while cash-out lets you access equity for renovations or debt payoff. In 2026, recent VA guideline updates may impact fees, documentation, and eligibility.

For example, a Seattle veteran who refinanced with an IRRRL in early 2026 saw their monthly payment drop by $200, thanks to falling rates and the streamlined approval process. To learn more about these benefits, see the Seattle VA home loan benefits page.

Types of VA Refinance Options

When considering a va mortgage loan refinance, Seattle homeowners can choose between two primary options:

- VA IRRRL (Interest Rate Reduction Refinance Loan): Designed for current VA loan holders, this option provides a fast, low-cost way to reduce interest rates or switch from an ARM to a fixed-rate mortgage. Minimal documentation and no appraisal are often required.

- VA Cash-Out Refinance: This option allows borrowers to access home equity for major expenses like renovations, debt consolidation, or education costs. It does require a full appraisal and more paperwork, but offers greater flexibility.

| Feature | VA IRRRL | VA Cash-Out Refinance |

|---|---|---|

| Documentation | Minimal | Full income/asset review |

| Appraisal | Often not required | Required |

| Purpose | Lower rate/payment | Access equity |

| Occupancy | Previous or current | Must occupy as primary |

| 2026 Updates | Possible lower fees | Updated loan limits, fees |

For example, a Lynnwood homeowner used a cash-out refinance in 2026 to fund major kitchen upgrades, leveraging increased home value. Each va mortgage loan refinance type aligns with different financial goals and, with anticipated program changes in 2026, eligibility and costs may shift for Seattle-area borrowers.

Seattle-Area Market Context for VA Refinancing

The Seattle region, including Shoreline, Everett, and Mill Creek, has seen steady home value growth, providing more equity for potential va mortgage loan refinance opportunities. Rising property values in King and Snohomish counties increase both IRRRL and cash-out refinance options for veterans.

Local statistics show that VA loan usage rates remain high, as many military families choose to refinance for lower payments, fixed rates, or to access cash for life events. For instance, a Mill Creek family recently leveraged rising equity through a cash-out refinance, funding a home addition while maintaining affordable payments.

Seattle’s competitive real estate market means timing, lender selection, and understanding current guidelines are crucial for maximizing the benefits of a va mortgage loan refinance.

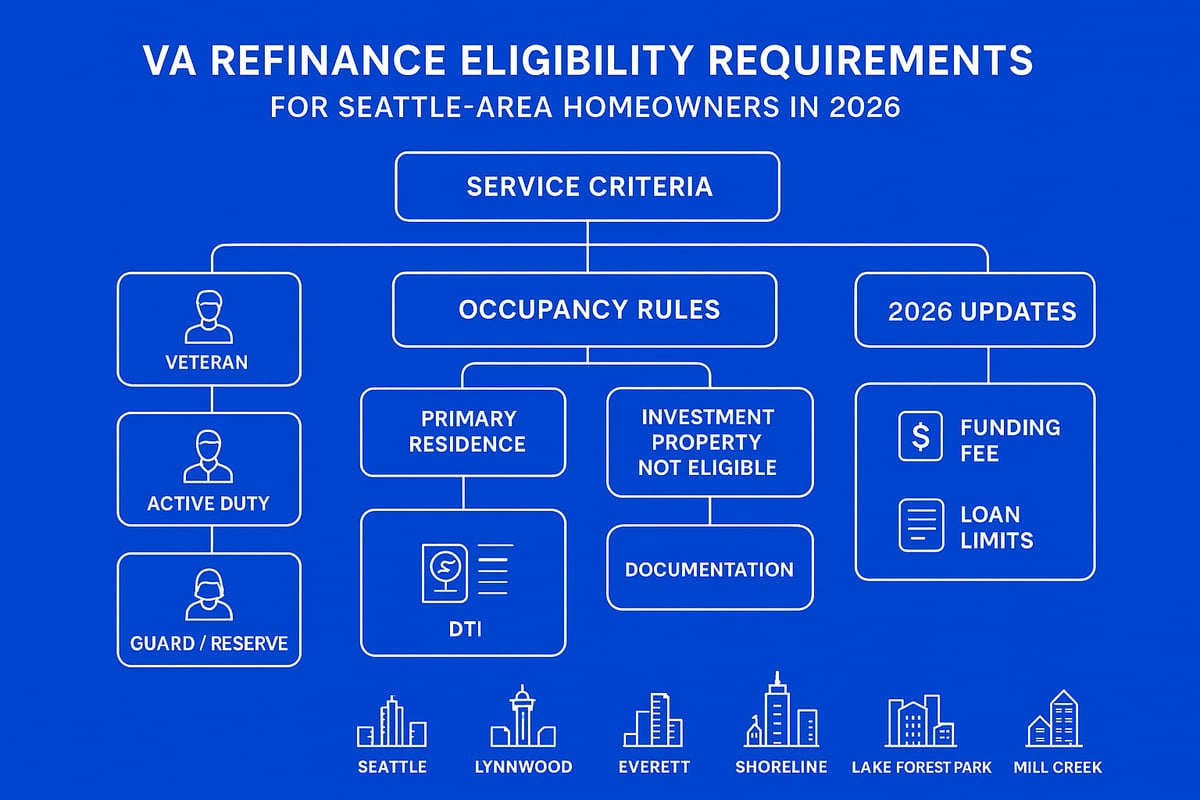

VA Refinance Eligibility Requirements in 2026

Understanding if you qualify for a va mortgage loan refinance is the first step toward unlocking better rates or cash access in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. With updated VA guidelines for 2026, it is crucial to know what lenders look for and how to prepare.

Service and Occupancy Criteria

To be eligible for a va mortgage loan refinance in Seattle or surrounding cities, veterans, active duty members, National Guard, and Reservists must meet specific service requirements. Typically, you need at least 90 days of active wartime service or 181 days during peacetime. Surviving spouses may also qualify if the veteran died in service or due to a service-connected condition.

Occupancy rules differ by refinance type. For an IRRRL, you must certify prior occupancy as your primary residence. For a cash-out refinance, you must live in the home as your primary residence at closing. For example, an Everett veteran separating from service in 2025 can use their Certificate of Eligibility to refinance if they still meet occupancy and service standards.

Always double-check your service record and occupancy plans before applying for a va mortgage loan refinance. This will help avoid delays and ensure you meet all VA and lender requirements.

Credit, Income, and Property Standards

Seattle-area lenders look for strong credit and stable income when evaluating a va mortgage loan refinance. For IRRRLs, the minimum credit score is often around 550. Cash-out refinances generally require at least 570. Debt-to-income (DTI) ratios should typically be below 50 percent, calculated by dividing total monthly debts by gross monthly income.

Eligible properties include single-family homes, VA-approved condos, and some townhomes within Seattle, Lynnwood, and nearby areas. You will need documentation such as pay stubs, W-2s, tax returns, and your Certificate of Eligibility (COE). For instance, a Shoreline tech worker with restricted stock units (RSUs) can use employment and asset documents to support their cash-out application.

Gathering paperwork early and understanding these standards will streamline your va mortgage loan refinance. Consult with local experts if you have non-traditional income or unique property types.

2026-Specific VA Guidelines and Updates

For 2026, the VA has introduced updates affecting va mortgage loan refinance eligibility. Funding fee rates may be reduced for certain veterans, making refinancing more affordable. Seasoning requirements still apply: you must have made at least six payments and 210 days must have passed since your last loan closing.

Loan limits and appraisal standards have been adjusted for King and Snohomish counties, reflecting Seattle’s rising home values. For example, a Lynnwood homeowner might see a lower funding fee and higher allowable loan amount when refinancing this year. For the latest on these changes and how they impact you locally, consult the Seattle mortgage refinance insights page.

Staying updated with 2026 guidelines ensures you maximize the benefits of your va mortgage loan refinance and avoid surprises during the process.

Common Eligibility Pitfalls and Solutions

Many Seattle-area homeowners encounter obstacles when applying for a va mortgage loan refinance. Common issues include not meeting occupancy requirements, recent late mortgage payments, or properties that do not meet VA standards. High DTI or borderline credit can also pose challenges.

Solutions include:

- Requesting a rapid rescore for recent credit improvements

- Paying down debts to lower DTI

- Working with VA-approved contractors for minor property repairs

- Using VA resources to obtain or correct your COE

A Lake Forest Park family recently overcame lost service paperwork by contacting the local VA office for assistance, enabling a successful refinance. Addressing potential pitfalls early will help ensure your va mortgage loan refinance moves forward smoothly.

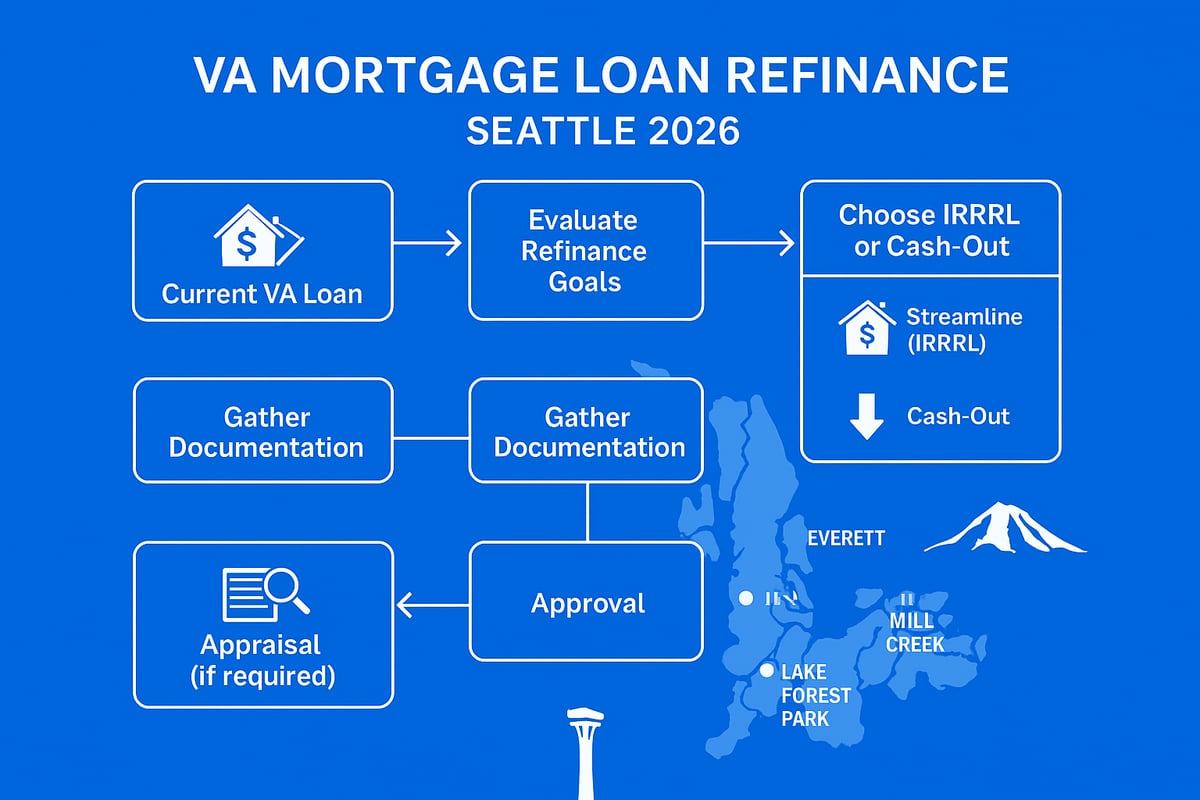

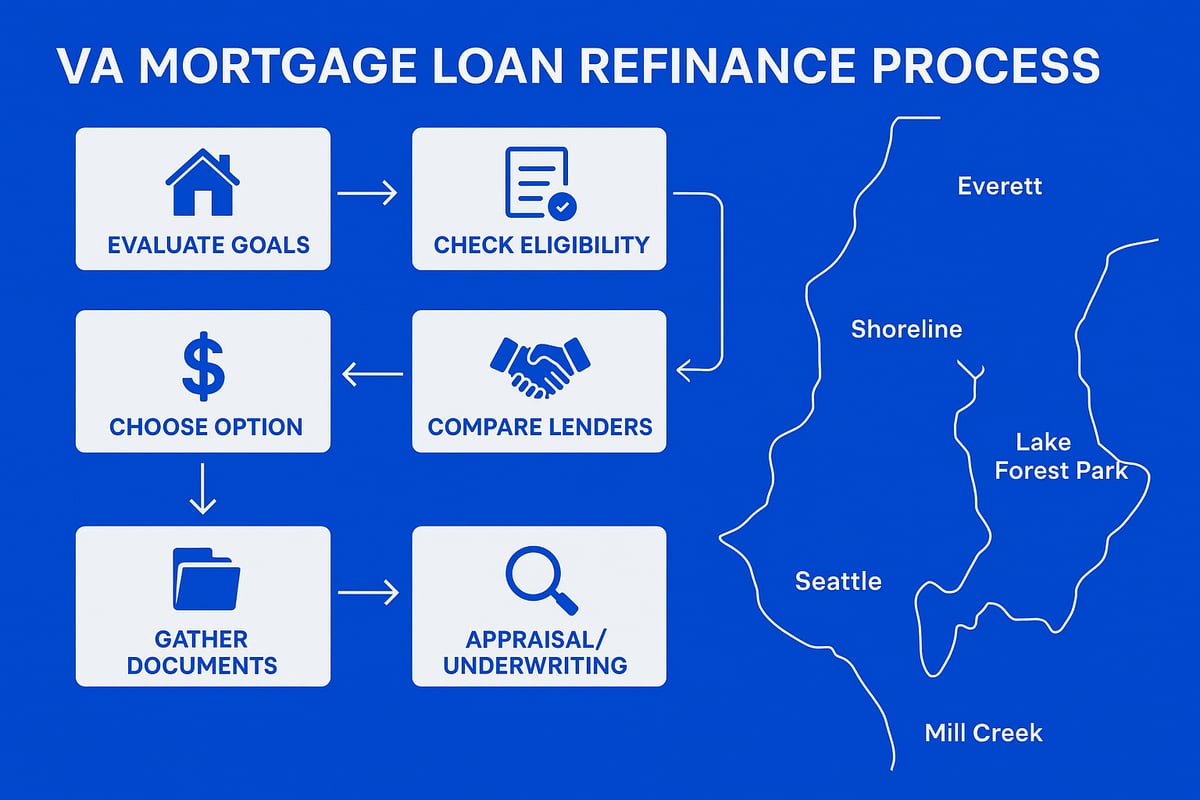

Step-by-Step Guide to Refinancing Your VA Mortgage in Seattle

Refinancing your VA mortgage loan in Seattle requires a thoughtful, step-by-step approach to ensure you maximize your benefits and avoid costly missteps. As a licensed mortgage broker serving Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett, I will walk you through the process, highlighting local strategies and pitfalls to avoid. Here is your comprehensive guide to a successful va mortgage loan refinance.

Step 1: Evaluate Your Current Mortgage and Goals

Begin your va mortgage loan refinance by reviewing your current mortgage details. Examine your interest rate, remaining loan balance, and monthly payment. This information is crucial for understanding whether refinancing will deliver the financial benefits you seek.

Next, clarify your objectives. Are you looking to lower your monthly payment, shorten your loan term, switch from an ARM to a fixed rate, or access cash from your home’s equity? Seattle’s recent home appreciation means many homeowners now have more equity, creating opportunities for both payment reduction and cash-out.

For instance, a Mill Creek homeowner compared several scenarios and found that refinancing into a lower rate could save hundreds monthly. If your primary goal is to reduce your payment, explore actionable strategies in this How to lower your mortgage payment guide.

List of common refinance goals:

- Lowering interest rate and payment

- Accessing cash for renovations or debt payoff

- Shortening loan term for faster payoff

- Switching loan type for stability

Evaluating your current mortgage and future needs sets the foundation for a successful va mortgage loan refinance.

Step 2: Confirm Your VA Refinance Eligibility

Before proceeding, confirm your eligibility for a va mortgage loan refinance. Use this checklist to evaluate your qualifications:

- Sufficient VA service history (active, veteran, or certain spouses)

- Minimum credit score (typically 550+ for IRRRL, 570+ for cash-out)

- Acceptable debt-to-income ratio (DTI), usually under 50%

- Eligible property type (single-family, some condos, townhomes)

- Occupancy requirements: must have lived in the home, though IRRRL is flexible

Obtain your Certificate of Eligibility (COE) through the VA or your lender. Seattle-area veterans can visit local VA offices for help or use online portals for faster processing.

For example, an Everett veteran recently separated from service was able to secure a COE and confirm eligibility in less than a week, thanks to proactive documentation.

Gather the following documents:

- COE

- Recent pay stubs or benefit statements

- Last two years’ tax returns

- Current mortgage statement

- Government-issued ID

Completing this eligibility review ensures your va mortgage loan refinance proceeds smoothly.

Step 3: Choose the Right VA Refinance Option

Selecting the best va mortgage loan refinance product depends on your financial goals and current situation. There are two main VA refinance paths:

| Option | Best For | Key Features |

|---|---|---|

| IRRRL (Streamline) | Lowering rate/payment | Minimal docs, no appraisal, fast process |

| Cash-Out | Tapping home equity | Full appraisal, higher docs, access to cash |

Consider these questions:

- Do you want a quick rate reduction with minimal hassle? IRRRL is ideal.

- Need cash for home improvements or debt? Cash-out is the way to go.

A Shoreline couple recently used the IRRRL option to lower their payment by $200 monthly, with no new appraisal needed. In contrast, a Lynnwood homeowner chose cash-out to fund a kitchen remodel.

Weigh the pros and cons of each option:

- IRRRL: Faster, lower fees, but no cash out

- Cash-Out: Access equity, but higher costs and documentation

Identifying the right va mortgage loan refinance strategy will help you meet your objectives efficiently.

Step 4: Compare Seattle Lenders and Rates

Not all lenders are created equal—especially when it comes to va mortgage loan refinance expertise in Seattle and nearby cities. Take time to shop for the best rates, closing costs, and customer service.

Follow these steps:

- Contact at least three local lenders in Seattle, Bellevue, or Redmond.

- Request detailed Loan Estimates for the same refinance type.

- Compare rates, fees, and turnaround times.

- Check online reviews and ask about VA experience.

Factors influencing your rate:

- Credit score

- Loan amount

- Property type and location

- Chosen refinance option (IRRRL or cash-out)

For example, a Lynnwood veteran saved over $3,000 in closing costs by comparing three lenders and choosing the one with the most VA experience.

Use online calculators and review current Seattle mortgage rates and trends (if desired) to benchmark offers. This diligence ensures your va mortgage loan refinance delivers maximum value.

Step 5: Gather Documentation and Apply

Once you have chosen a lender, collect the necessary paperwork to begin your va mortgage loan refinance application. Requirements vary by option:

- IRRRL: Driver’s license, current mortgage statement, COE, recent pay stub (if required)

- Cash-Out: All above, plus two years’ tax returns, bank statements, homeowner’s insurance, and full appraisal

Tips for a smooth process in Seattle’s competitive market:

- Use digital uploads for speed and accuracy

- Double-check all forms for completeness

- Respond quickly to lender requests

A Lake Forest Park applicant recently streamlined their process by organizing all documents before applying, leading to a hassle-free experience.

Be proactive with your documentation to avoid delays and keep your va mortgage loan refinance on track.

Step 6: Appraisal, Underwriting, and Approval

The next stage in your va mortgage loan refinance is appraisal (for cash-out) and underwriting. Here is what to expect:

- Appraisal: For cash-out refis, a local appraiser will assess your home’s value. In Seattle and Everett, rising values can boost your equity and loan options.

- Underwriting: Lender reviews your credit, income, assets, property, and occupancy.

- Timeline: IRRRLs often close in 30–45 days, while cash-out can take 45–60 days due to the appraisal.

Common challenges include appraisal delays (especially in busy markets) or document requests for further income verification.

Recently, an Everett homeowner faced an unexpectedly low appraisal. By providing recent comparable sales data, they successfully appealed and secured a higher value—demonstrating the importance of preparation.

Stay in close contact with your lender during this stage to ensure your va mortgage loan refinance stays on schedule.

Step 7: Closing and Funding Your New VA Loan

The final step in your va mortgage loan refinance is closing and funding. Your lender will provide a Closing Disclosure outlining all costs. You will sign documents at a local title office or via secure e-signature.

Expect these typical Seattle-area closing costs:

- 2–6% of the loan amount for cash-out

- 1–3% for IRRRL

After signing, your new VA loan will fund within a few days. If you opted for cash-out, funds will be disbursed by direct deposit or check.

A Mill Creek family recently closed their va mortgage loan refinance and received funds within three business days, allowing them to start their home renovation immediately.

After closing, your new payment schedule begins the following month. Congratulations—you have successfully navigated the va mortgage loan refinance process in Seattle.

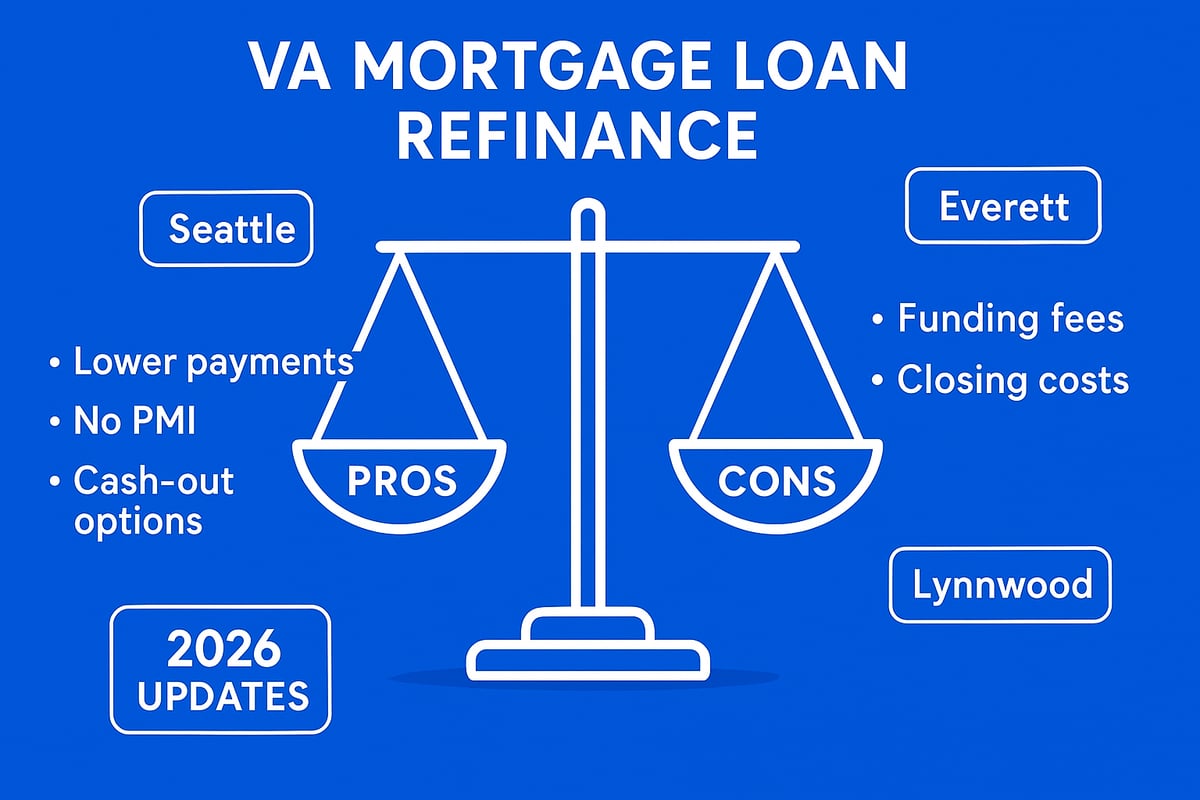

Pros and Cons of VA Mortgage Loan Refinance in 2026

Refinancing with a va mortgage loan refinance in the Seattle area can unlock powerful financial benefits for veterans, active-duty personnel, and their families. Understanding the pros and cons is essential for homeowners in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett as they consider their options for 2026.

Key Benefits for Seattle-Area Borrowers

A va mortgage loan refinance offers unique advantages for local veterans and military families. First, most borrowers enjoy lower interest rates, leading to substantial monthly savings. For example, a Shoreline homeowner recently reduced their payment by $250 per month. VA loans do not require private mortgage insurance, which can save hundreds each year.

Flexible credit and documentation standards make the process accessible, especially for those using the Interest Rate Reduction Refinance Loan. Homeowners can also tap equity for renovations or debt consolidation, supporting financial goals. In 2026, possible updates may include lower funding fees and more streamlined processes, making refinancing even more attractive. For a detailed breakdown of IRRRL benefits and eligibility, visit the VA IRRRL guidelines.

| Benefit | Description |

|---|---|

| Lower Interest Rates | Reduce payments and total interest |

| No PMI | No private mortgage insurance required |

| Flexible Qualification | Easier credit and documentation standards |

| Tap Home Equity | Fund renovations, pay off debt, or major expenses |

Potential Drawbacks and Costs

While a va mortgage loan refinance offers many benefits, there are important costs to consider. The VA funding fee is typically 0.5% for IRRRLs and higher for cash-out refinances. Closing costs in Seattle, Lynnwood, and Everett generally run 2% to 6% of the loan amount.

Resetting your loan term could increase the total interest paid over time. Not all properties or borrowers qualify, and cash-out limits depend on your home’s appraised value and equity. For example, a Lynnwood borrower who chose a shorter term faced higher payments despite a lower rate. To understand cash-out requirements and potential costs, review the VA cash-out refinance program.

| Drawback | Impact |

|---|---|

| VA Funding Fee | 0.5%-3.6% of loan (varies by type and exemption) |

| Closing Costs | 2%-6% of loan amount |

| Loan Term Reset | Possible increase in total interest |

| Equity & Appraisal | Limited by property value and equity |

When VA Refinance Makes Sense (and When It Doesn’t)

A va mortgage loan refinance is ideal when interest rates drop, your current loan has high payments, or you need cash for renovations or debt. It is also a strong choice for switching from an adjustable-rate to a fixed-rate mortgage, especially in Seattle’s fluctuating market.

However, it may not be the right move if you recently purchased your home, see minimal rate improvement, or face high closing costs. Local appreciation and property taxes in Mill Creek and Lake Forest Park can also influence timing. One Everett veteran decided to wait for better rates before refinancing, avoiding unnecessary fees.

Common Mistakes and How to Avoid Them

Mistakes with va mortgage loan refinance often stem from lack of research or incomplete paperwork. To avoid missing out on savings:

- Compare offers from at least three Seattle-area lenders.

- Review all costs, including the funding fee and closing expenses.

- Verify eligibility and gather documentation early.

- Use local resources to clarify requirements.

A Lake Forest Park homeowner once lost out on savings due to missing documents, underscoring the value of preparation and expert guidance.

Why Does It Matter?

The VA requires every va mortgage loan refinance to deliver a net tangible benefit for the borrower. This means your new loan must improve your financial situation, such as by lowering your interest rate, reducing your monthly payment, or switching from an adjustable to a fixed rate.

Seattle lenders will review your application to ensure the refinance provides a clear and measurable benefit. For example, a Mill Creek veteran who moves from a 30-year fixed at 6.25 percent to a new VA IRRRL at 5.25 percent would see lower payments and long-term savings.

How Soon Can You Refinance a VA Loan After Purchase?

You can pursue a va mortgage loan refinance in Seattle once you have made at least six consecutive monthly payments and at least 210 days have passed since your first payment. These seasoning requirements help ensure borrowers are established in their current loan before refinancing.

If rates drop or your needs change, plan your refinance timing accordingly. For instance, a recent Shoreline homebuyer may want to watch market trends and start preparing paperwork as soon as the waiting period ends.

What Are the Typical Costs and Fees for VA Refinancing?

Typical costs for va mortgage loan refinance in the Seattle area include a VA funding fee (0.5 percent for IRRRL, higher for cash-out) and closing costs, which usually range from 2 percent to 6 percent of the loan amount. Disabled veterans may be exempt from the funding fee.

Local closing costs can vary by city and lender, so it’s wise to compare estimates. You can also check the latest VA loan limits 2026 for King and Snohomish counties, as higher limits may impact available loan amounts and closing costs for Lynnwood or Everett homeowners.

How Long Does the VA Refinance Process Take in Seattle?

The average timeline for a va mortgage loan refinance in Seattle is 30 to 45 days for an IRRRL, and 45 to 60 days for a cash-out refinance. The process may move faster if your documentation is ready and your lender is experienced with VA loans.

Factors like appraisal scheduling and underwriting review can affect timing. For example, a Lake Forest Park family with a straightforward IRRRL and digital paperwork could close in just over a month, while a cash-out in Everett may take longer due to appraisal or title work.

Can You Refinance Multiple Times with a VA Loan?

Yes, you can complete a va mortgage loan refinance more than once, provided you meet eligibility and seasoning requirements each time. There’s no set limit on the number of refinances.

Each time you refinance, the new loan must meet the VA’s benefit criteria. For example, a Seattle homeowner who refinanced in 2023 could refinance again in 2026 if rates fall or they want to tap additional equity.

Can You Get Cash from a VA IRRRL?

The VA IRRRL program is designed strictly for lowering your interest rate or payment on an existing VA loan. It does not allow you to take cash out at closing. If you need funds for renovations or debt consolidation in Lynnwood or Mill Creek, you’ll need to apply for a VA cash-out refinance instead.

A Shoreline family, for example, chose a cash-out option to pay for college expenses, while another in Everett used IRRRL to quickly reduce their monthly mortgage cost.

Now that you have a clear picture of what it takes to refinance a VA mortgage loan in Seattle for 2026, you might still have questions about your unique situation or want to explore what’s possible based on your goals. Whether you’re hoping to lower your monthly payment, tap into your home’s equity, or simply get clarity on the latest VA guidelines, I’m here to help guide you every step of the way. Let’s review your options together and build a plan that fits your needs—Let’s have a conversation.

Thinking about a va mortgage loan refinance in Seattle for 2026? You are not alone. Many veterans and military families across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett are exploring their options as interest rates and home values shift.

VA loan refinances offer unique advantages compared to conventional loans. These include lower monthly payments, no private mortgage insurance, and flexible qualification standards. For local homeowners, the right refinancing strategy can unlock significant savings, provide access to home equity, or create a more stable financial future.

This comprehensive guide will walk you step by step through every aspect of va mortgage loan refinance in 2026. You will learn about VA refinance basics, eligibility, the full process, local market trends, pros and cons, and expert strategies tailored to Seattle and surrounding areas.

Understanding VA Mortgage Loan Refinance in 2026

Navigating a va mortgage loan refinance in Seattle in 2026 offers unique advantages for veterans, active duty, and military families. This process helps homeowners lower monthly payments, access home equity, or secure a more stable financial future. Understanding the essentials of va mortgage loan refinance is key for making informed decisions, especially with evolving guidelines and Seattle’s dynamic real estate market.

What is a VA Mortgage Loan Refinance?

A va mortgage loan refinance allows eligible Seattle-area veterans and service members to replace their existing VA loan with a new one, often at a lower interest rate or with different terms. Unlike conventional refinancing, this program features no private mortgage insurance, lower credit barriers, and unique benefits tied to military service.

There are two main types: the Interest Rate Reduction Refinance Loan (IRRRL), also known as the “streamline” option, and the cash-out refinance. The IRRRL is used primarily to lower your rate or payment with minimal paperwork, while cash-out lets you access equity for renovations or debt payoff. In 2026, recent VA guideline updates may impact fees, documentation, and eligibility.

For example, a Seattle veteran who refinanced with an IRRRL in early 2026 saw their monthly payment drop by $200, thanks to falling rates and the streamlined approval process. To learn more about these benefits, see the Seattle VA home loan benefits page.

Types of VA Refinance Options

When considering a va mortgage loan refinance, Seattle homeowners can choose between two primary options:

- VA IRRRL (Interest Rate Reduction Refinance Loan): Designed for current VA loan holders, this option provides a fast, low-cost way to reduce interest rates or switch from an ARM to a fixed-rate mortgage. Minimal documentation and no appraisal are often required.

- VA Cash-Out Refinance: This option allows borrowers to access home equity for major expenses like renovations, debt consolidation, or education costs. It does require a full appraisal and more paperwork, but offers greater flexibility.

| Feature | VA IRRRL | VA Cash-Out Refinance |

|---|---|---|

| Documentation | Minimal | Full income/asset review |

| Appraisal | Often not required | Required |

| Purpose | Lower rate/payment | Access equity |

| Occupancy | Previous or current | Must occupy as primary |

| 2026 Updates | Possible lower fees | Updated loan limits, fees |

For example, a Lynnwood homeowner used a cash-out refinance in 2026 to fund major kitchen upgrades, leveraging increased home value. Each va mortgage loan refinance type aligns with different financial goals and, with anticipated program changes in 2026, eligibility and costs may shift for Seattle-area borrowers.

Seattle-Area Market Context for VA Refinancing

The Seattle region, including Shoreline, Everett, and Mill Creek, has seen steady home value growth, providing more equity for potential va mortgage loan refinance opportunities. Rising property values in King and Snohomish counties increase both IRRRL and cash-out refinance options for veterans.

Local statistics show that VA loan usage rates remain high, as many military families choose to refinance for lower payments, fixed rates, or to access cash for life events. For instance, a Mill Creek family recently leveraged rising equity through a cash-out refinance, funding a home addition while maintaining affordable payments.

Seattle’s competitive real estate market means timing, lender selection, and understanding current guidelines are crucial for maximizing the benefits of a va mortgage loan refinance.

VA Refinance Eligibility Requirements in 2026

Understanding if you qualify for a va mortgage loan refinance is the first step toward unlocking better rates or cash access in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. With updated VA guidelines for 2026, it is crucial to know what lenders look for and how to prepare.

Service and Occupancy Criteria

To be eligible for a va mortgage loan refinance in Seattle or surrounding cities, veterans, active duty members, National Guard, and Reservists must meet specific service requirements. Typically, you need at least 90 days of active wartime service or 181 days during peacetime. Surviving spouses may also qualify if the veteran died in service or due to a service-connected condition.

Occupancy rules differ by refinance type. For an IRRRL, you must certify prior occupancy as your primary residence. For a cash-out refinance, you must live in the home as your primary residence at closing. For example, an Everett veteran separating from service in 2025 can use their Certificate of Eligibility to refinance if they still meet occupancy and service standards.

Always double-check your service record and occupancy plans before applying for a va mortgage loan refinance. This will help avoid delays and ensure you meet all VA and lender requirements.

Credit, Income, and Property Standards

Seattle-area lenders look for strong credit and stable income when evaluating a va mortgage loan refinance. For IRRRLs, the minimum credit score is often around 550. Cash-out refinances generally require at least 570. Debt-to-income (DTI) ratios should typically be below 50 percent, calculated by dividing total monthly debts by gross monthly income.

Eligible properties include single-family homes, VA-approved condos, and some townhomes within Seattle, Lynnwood, and nearby areas. You will need documentation such as pay stubs, W-2s, tax returns, and your Certificate of Eligibility (COE). For instance, a Shoreline tech worker with restricted stock units (RSUs) can use employment and asset documents to support their cash-out application.

Gathering paperwork early and understanding these standards will streamline your va mortgage loan refinance. Consult with local experts if you have non-traditional income or unique property types.

2026-Specific VA Guidelines and Updates

For 2026, the VA has introduced updates affecting va mortgage loan refinance eligibility. Funding fee rates may be reduced for certain veterans, making refinancing more affordable. Seasoning requirements still apply: you must have made at least six payments and 210 days must have passed since your last loan closing.

Loan limits and appraisal standards have been adjusted for King and Snohomish counties, reflecting Seattle’s rising home values. For example, a Lynnwood homeowner might see a lower funding fee and higher allowable loan amount when refinancing this year. For the latest on these changes and how they impact you locally, consult the Seattle mortgage refinance insights page.

Staying updated with 2026 guidelines ensures you maximize the benefits of your va mortgage loan refinance and avoid surprises during the process.

Common Eligibility Pitfalls and Solutions

Many Seattle-area homeowners encounter obstacles when applying for a va mortgage loan refinance. Common issues include not meeting occupancy requirements, recent late mortgage payments, or properties that do not meet VA standards. High DTI or borderline credit can also pose challenges.

Solutions include:

- Requesting a rapid rescore for recent credit improvements

- Paying down debts to lower DTI

- Working with VA-approved contractors for minor property repairs

- Using VA resources to obtain or correct your COE

A Lake Forest Park family recently overcame lost service paperwork by contacting the local VA office for assistance, enabling a successful refinance. Addressing potential pitfalls early will help ensure your va mortgage loan refinance moves forward smoothly.

Step-by-Step Guide to Refinancing Your VA Mortgage in Seattle

Refinancing your VA mortgage loan in Seattle requires a thoughtful, step-by-step approach to ensure you maximize your benefits and avoid costly missteps. As a licensed mortgage broker serving Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett, I will walk you through the process, highlighting local strategies and pitfalls to avoid. Here is your comprehensive guide to a successful va mortgage loan refinance.

Step 1: Evaluate Your Current Mortgage and Goals

Begin your va mortgage loan refinance by reviewing your current mortgage details. Examine your interest rate, remaining loan balance, and monthly payment. This information is crucial for understanding whether refinancing will deliver the financial benefits you seek.

Next, clarify your objectives. Are you looking to lower your monthly payment, shorten your loan term, switch from an ARM to a fixed rate, or access cash from your home’s equity? Seattle’s recent home appreciation means many homeowners now have more equity, creating opportunities for both payment reduction and cash-out.

For instance, a Mill Creek homeowner compared several scenarios and found that refinancing into a lower rate could save hundreds monthly. If your primary goal is to reduce your payment, explore actionable strategies in this How to lower your mortgage payment guide.

List of common refinance goals:

- Lowering interest rate and payment

- Accessing cash for renovations or debt payoff

- Shortening loan term for faster payoff

- Switching loan type for stability

Evaluating your current mortgage and future needs sets the foundation for a successful va mortgage loan refinance.

Step 2: Confirm Your VA Refinance Eligibility

Before proceeding, confirm your eligibility for a va mortgage loan refinance. Use this checklist to evaluate your qualifications:

- Sufficient VA service history (active, veteran, or certain spouses)

- Minimum credit score (typically 550+ for IRRRL, 570+ for cash-out)

- Acceptable debt-to-income ratio (DTI), usually under 50%

- Eligible property type (single-family, some condos, townhomes)

- Occupancy requirements: must have lived in the home, though IRRRL is flexible

Obtain your Certificate of Eligibility (COE) through the VA or your lender. Seattle-area veterans can visit local VA offices for help or use online portals for faster processing.

For example, an Everett veteran recently separated from service was able to secure a COE and confirm eligibility in less than a week, thanks to proactive documentation.

Gather the following documents:

- COE

- Recent pay stubs or benefit statements

- Last two years’ tax returns

- Current mortgage statement

- Government-issued ID

Completing this eligibility review ensures your va mortgage loan refinance proceeds smoothly.

Step 3: Choose the Right VA Refinance Option

Selecting the best va mortgage loan refinance product depends on your financial goals and current situation. There are two main VA refinance paths:

| Option | Best For | Key Features |

|---|---|---|

| IRRRL (Streamline) | Lowering rate/payment | Minimal docs, no appraisal, fast process |

| Cash-Out | Tapping home equity | Full appraisal, higher docs, access to cash |

Consider these questions:

- Do you want a quick rate reduction with minimal hassle? IRRRL is ideal.

- Need cash for home improvements or debt? Cash-out is the way to go.

A Shoreline couple recently used the IRRRL option to lower their payment by $200 monthly, with no new appraisal needed. In contrast, a Lynnwood homeowner chose cash-out to fund a kitchen remodel.

Weigh the pros and cons of each option:

- IRRRL: Faster, lower fees, but no cash out

- Cash-Out: Access equity, but higher costs and documentation

Identifying the right va mortgage loan refinance strategy will help you meet your objectives efficiently.

Step 4: Compare Seattle Lenders and Rates

Not all lenders are created equal—especially when it comes to va mortgage loan refinance expertise in Seattle and nearby cities. Take time to shop for the best rates, closing costs, and customer service.

Follow these steps:

- Contact at least three local lenders in Seattle, Bellevue, or Redmond.

- Request detailed Loan Estimates for the same refinance type.

- Compare rates, fees, and turnaround times.

- Check online reviews and ask about VA experience.

Factors influencing your rate:

- Credit score

- Loan amount

- Property type and location

- Chosen refinance option (IRRRL or cash-out)

For example, a Lynnwood veteran saved over $3,000 in closing costs by comparing three lenders and choosing the one with the most VA experience.

Use online calculators and review current Seattle mortgage rates and trends (if desired) to benchmark offers. This diligence ensures your va mortgage loan refinance delivers maximum value.

Step 5: Gather Documentation and Apply

Once you have chosen a lender, collect the necessary paperwork to begin your va mortgage loan refinance application. Requirements vary by option:

- IRRRL: Driver’s license, current mortgage statement, COE, recent pay stub (if required)

- Cash-Out: All above, plus two years’ tax returns, bank statements, homeowner’s insurance, and full appraisal

Tips for a smooth process in Seattle’s competitive market:

- Use digital uploads for speed and accuracy

- Double-check all forms for completeness

- Respond quickly to lender requests

A Lake Forest Park applicant recently streamlined their process by organizing all documents before applying, leading to a hassle-free experience.

Be proactive with your documentation to avoid delays and keep your va mortgage loan refinance on track.

Step 6: Appraisal, Underwriting, and Approval

The next stage in your va mortgage loan refinance is appraisal (for cash-out) and underwriting. Here is what to expect:

- Appraisal: For cash-out refis, a local appraiser will assess your home’s value. In Seattle and Everett, rising values can boost your equity and loan options.

- Underwriting: Lender reviews your credit, income, assets, property, and occupancy.

- Timeline: IRRRLs often close in 30–45 days, while cash-out can take 45–60 days due to the appraisal.

Common challenges include appraisal delays (especially in busy markets) or document requests for further income verification.

Recently, an Everett homeowner faced an unexpectedly low appraisal. By providing recent comparable sales data, they successfully appealed and secured a higher value—demonstrating the importance of preparation.

Stay in close contact with your lender during this stage to ensure your va mortgage loan refinance stays on schedule.

Step 7: Closing and Funding Your New VA Loan

The final step in your va mortgage loan refinance is closing and funding. Your lender will provide a Closing Disclosure outlining all costs. You will sign documents at a local title office or via secure e-signature.

Expect these typical Seattle-area closing costs:

- 2–6% of the loan amount for cash-out

- 1–3% for IRRRL

After signing, your new VA loan will fund within a few days. If you opted for cash-out, funds will be disbursed by direct deposit or check.

A Mill Creek family recently closed their va mortgage loan refinance and received funds within three business days, allowing them to start their home renovation immediately.

After closing, your new payment schedule begins the following month. Congratulations—you have successfully navigated the va mortgage loan refinance process in Seattle.

Pros and Cons of VA Mortgage Loan Refinance in 2026

Refinancing with a va mortgage loan refinance in the Seattle area can unlock powerful financial benefits for veterans, active-duty personnel, and their families. Understanding the pros and cons is essential for homeowners in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett as they consider their options for 2026.

Key Benefits for Seattle-Area Borrowers

A va mortgage loan refinance offers unique advantages for local veterans and military families. First, most borrowers enjoy lower interest rates, leading to substantial monthly savings. For example, a Shoreline homeowner recently reduced their payment by $250 per month. VA loans do not require private mortgage insurance, which can save hundreds each year.

Flexible credit and documentation standards make the process accessible, especially for those using the Interest Rate Reduction Refinance Loan. Homeowners can also tap equity for renovations or debt consolidation, supporting financial goals. In 2026, possible updates may include lower funding fees and more streamlined processes, making refinancing even more attractive. For a detailed breakdown of IRRRL benefits and eligibility, visit the VA IRRRL guidelines.

| Benefit | Description |

|---|---|

| Lower Interest Rates | Reduce payments and total interest |

| No PMI | No private mortgage insurance required |

| Flexible Qualification | Easier credit and documentation standards |

| Tap Home Equity | Fund renovations, pay off debt, or major expenses |

Potential Drawbacks and Costs

While a va mortgage loan refinance offers many benefits, there are important costs to consider. The VA funding fee is typically 0.5% for IRRRLs and higher for cash-out refinances. Closing costs in Seattle, Lynnwood, and Everett generally run 2% to 6% of the loan amount.

Resetting your loan term could increase the total interest paid over time. Not all properties or borrowers qualify, and cash-out limits depend on your home’s appraised value and equity. For example, a Lynnwood borrower who chose a shorter term faced higher payments despite a lower rate. To understand cash-out requirements and potential costs, review the VA cash-out refinance program.

| Drawback | Impact |

|---|---|

| VA Funding Fee | 0.5%-3.6% of loan (varies by type and exemption) |

| Closing Costs | 2%-6% of loan amount |

| Loan Term Reset | Possible increase in total interest |

| Equity & Appraisal | Limited by property value and equity |

When VA Refinance Makes Sense (and When It Doesn’t)

A va mortgage loan refinance is ideal when interest rates drop, your current loan has high payments, or you need cash for renovations or debt. It is also a strong choice for switching from an adjustable-rate to a fixed-rate mortgage, especially in Seattle’s fluctuating market.

However, it may not be the right move if you recently purchased your home, see minimal rate improvement, or face high closing costs. Local appreciation and property taxes in Mill Creek and Lake Forest Park can also influence timing. One Everett veteran decided to wait for better rates before refinancing, avoiding unnecessary fees.

Common Mistakes and How to Avoid Them

Mistakes with va mortgage loan refinance often stem from lack of research or incomplete paperwork. To avoid missing out on savings:

- Compare offers from at least three Seattle-area lenders.

- Review all costs, including the funding fee and closing expenses.

- Verify eligibility and gather documentation early.

- Use local resources to clarify requirements.

A Lake Forest Park homeowner once lost out on savings due to missing documents, underscoring the value of preparation and expert guidance.

What is a Net Tangible Benefit and Why Does It Matter?

The VA requires every va mortgage loan refinance to deliver a net tangible benefit for the borrower. This means your new loan must improve your financial situation, such as by lowering your interest rate, reducing your monthly payment, or switching from an adjustable to a fixed rate.

Seattle lenders will review your application to ensure the refinance provides a clear and measurable benefit. For example, a Mill Creek veteran who moves from a 30-year fixed at 6.25 percent to a new VA IRRRL at 5.25 percent would see lower payments and long-term savings.

How Soon Can You Refinance a VA Loan After Purchase?

You can pursue a va mortgage loan refinance in Seattle once you have made at least six consecutive monthly payments and at least 210 days have passed since your first payment. These seasoning requirements help ensure borrowers are established in their current loan before refinancing.

If rates drop or your needs change, plan your refinance timing accordingly. For instance, a recent Shoreline homebuyer may want to watch market trends and start preparing paperwork as soon as the waiting period ends.

What Are the Typical Costs and Fees for VA Refinancing?

Typical costs for va mortgage loan refinance in the Seattle area include a VA funding fee (0.5 percent for IRRRL, higher for cash-out) and closing costs, which usually range from 2 percent to 6 percent of the loan amount. Disabled veterans may be exempt from the funding fee.

Local closing costs can vary by city and lender, so it’s wise to compare estimates. You can also check the latest VA loan limits 2026 for King and Snohomish counties, as higher limits may impact available loan amounts and closing costs for Lynnwood or Everett homeowners.

How Long Does the VA Refinance Process Take in Seattle?

The average timeline for a va mortgage loan refinance in Seattle is 30 to 45 days for an IRRRL, and 45 to 60 days for a cash-out refinance. The process may move faster if your documentation is ready and your lender is experienced with VA loans.

Factors like appraisal scheduling and underwriting review can affect timing. For example, a Lake Forest Park family with a straightforward IRRRL and digital paperwork could close in just over a month, while a cash-out in Everett may take longer due to appraisal or title work.

Can You Refinance Multiple Times with a VA Loan?

Yes, you can complete a va mortgage loan refinance more than once, provided you meet eligibility and seasoning requirements each time. There’s no set limit on the number of refinances.

Each time you refinance, the new loan must meet the VA’s benefit criteria. For example, a Seattle homeowner who refinanced in 2023 could refinance again in 2026 if rates fall or they want to tap additional equity.

Can You Get Cash from a VA IRRRL?

The VA IRRRL program is designed strictly for lowering your interest rate or payment on an existing VA loan. It does not allow you to take cash out at closing. If you need funds for renovations or debt consolidation in Lynnwood or Mill Creek, you’ll need to apply for a VA cash-out refinance instead.

A Shoreline family, for example, chose a cash-out option to pay for college expenses, while another in Everett used IRRRL to quickly reduce their monthly mortgage cost.

Now that you have a clear picture of what it takes to refinance a VA mortgage loan in Seattle for 2026, you might still have questions about your unique situation or want to explore what’s possible based on your goals. Whether you’re hoping to lower your monthly payment, tap into your home’s equity, or simply get clarity on the latest VA guidelines, I’m here to help guide you every step of the way. Let’s review your options together and build a plan that fits your needs—Let’s have a conversation.