Searching for a "home loan broker near me" is often the first step many Seattle-area homebuyers take when preparing to purchase or refinance a property. While online searches deliver hundreds of results, finding the right mortgage professional requires more than clicking the top listing. The best home loan broker near me combines local market knowledge, transparent communication, and access to competitive loan programs tailored to your financial situation. In the Greater Seattle area-from Shoreline to Everett-working with an experienced broker can mean the difference between a stressful transaction and a smooth, well-coordinated closing.

What a Home Loan Broker Actually Does

A home loan broker serves as an intermediary between borrowers and lenders, shopping your application across multiple wholesale lending partners to find the best rates and terms. Unlike a bank loan officer who works for a single institution, a broker has access to dozens of lenders, including national banks, credit unions, and specialized wholesale channels. This expanded network often leads to better pricing, more flexible underwriting, and loan products you might not find on your own.

Access to Multiple Lenders and Loan Products

When you search for a home loan broker near me, you gain immediate access to a broader marketplace. Brokers maintain relationships with lenders that offer:

- Conventional loans with varying down payment requirements

- FHA and VA loans for eligible borrowers

- Jumbo loans for high-balance properties common in Seattle, Bellevue, and Redmond

- Non-QM products for self-employed borrowers or unique income scenarios

- Portfolio loans that offer flexibility beyond standard guidelines

This variety becomes especially valuable in competitive markets like Lake Forest Park or Mill Creek, where buyers need creative financing solutions to win contracts. A broker can match your profile to the lender most likely to approve your loan quickly and at the lowest cost.

Expert Guidance Through the Mortgage Process

Beyond rate shopping, a skilled broker educates you on loan structure, closing costs, and timing strategies. They review your credit report, calculate debt-to-income ratios, and recommend steps to strengthen your application before submission. For tech professionals with stock compensation, a broker experienced in qualifying RSUs and bonuses can maximize your purchasing power without requiring you to liquidate investments prematurely.

Why Local Expertise Matters in Seattle

Searching "home loan broker near me" emphasizes proximity, but the real value lies in understanding regional real estate dynamics. Seattle's housing market operates differently than Phoenix or Atlanta-appreciation patterns, inventory levels, and buyer competition all influence loan strategy.

A broker familiar with Seattle, Lynnwood, and Shoreline knows how to structure offers that appeal to sellers in multiple-offer scenarios. They understand local appraisal challenges, property tax considerations, and HOA requirements that can impact loan approval. This knowledge translates into faster closings and fewer surprises during underwriting.

Understanding Competitive Offer Strategies

In neighborhoods like Bellevue and Redmond, where homes often receive five or more offers, your financing terms become part of your negotiating power. A local broker can:

- Provide pre-approval letters that carry weight with listing agents

- Recommend appraisal waiver strategies when appropriate

- Structure earnest money deposits and contingencies to strengthen your position

- Coordinate closing timelines to match seller preferences

These tactics require familiarity with local market norms and relationships with real estate professionals who recognize your broker's track record.

Navigating Regional Property Types and Values

Seattle's diverse housing stock-from Capitol Hill condos to Everett single-family homes-requires lenders comfortable with various property types. A home loan broker near me should understand:

| Property Type | Common Challenges | Broker Solutions |

|---|---|---|

| High-rise condos | Warrantability reviews, HOA approval | Pre-screen condo projects, expedite documentation |

| Townhomes with HOAs | Reserve fund requirements, rental caps | Connect with HOA-friendly lenders |

| Older homes (pre-1940) | Appraisal condition issues, renovation needs | Offer renovation loan options, condition waivers |

| New construction | Builder requirements, phased closings | Coordinate with builder reps, lock rates strategically |

This level of detail ensures your loan matches the property you're purchasing, avoiding last-minute complications that delay closing.

How to Evaluate a Home Loan Broker Near Me

Not all brokers offer the same service quality or expertise. Choosing a mortgage broker requires research beyond a simple Google search. Consider these factors when narrowing your options.

Licensing and Credentials

Every mortgage broker must hold a valid license through the Nationwide Mortgage Licensing System (NMLS). Verify their license number, check for disciplinary actions, and review public records. The Better Business Bureau’s mortgage broker directory provides additional credibility indicators, including complaint history and accreditation status.

Ask about professional designations like Certified Mortgage Advisor (CMA) or membership in local industry organizations. These credentials signal ongoing education and commitment to ethical practices.

Reviews and Client Testimonials

Online reviews across Google, Zillow, Redfin, and Yelp offer insight into a broker's communication style, responsiveness, and ability to close loans on time. Look for patterns in feedback:

- Consistent praise for transparency and education

- Specific examples of problem-solving during difficult transactions

- Recent reviews that reflect current market conditions

- Volume of reviews indicating experience level

A broker with 750+ five-star reviews demonstrates a proven track record across diverse scenarios and client types.

Questions to Ask Before Committing

Before choosing a home loan broker near me, schedule consultations with at least two or three candidates. Ten essential questions should guide your conversations:

- How many lenders do you work with, and which are your primary partners?

- What loan programs do you specialize in for my borrower profile?

- How do you get compensated-lender-paid, borrower-paid, or both?

- What is your average time to close, and can you meet my timeline?

- Do you handle underwriting in-house or through third parties?

- How do you communicate updates during the loan process?

- Can you provide references from recent clients in my neighborhood?

- What documentation will I need to gather upfront?

- How do you help clients improve their approval odds?

- What happens if my loan doesn't close on time?

Their answers reveal not only competence but also whether their working style matches your expectations.

The Home Loan Broker Process: What to Expect

Understanding the workflow helps you prepare and reduces anxiety during what can be a complex transaction. Here's how working with a home loan broker near me typically unfolds.

Initial Consultation and Pre-Approval

Your first meeting focuses on assessing your financial readiness. The broker reviews:

- Credit reports from all three bureaus

- Income documentation including pay stubs, tax returns, and bonus letters

- Asset statements showing down payment funds and reserves

- Debt obligations such as student loans, auto payments, and credit cards

For Seattle tech professionals, this stage includes analyzing RSU vesting schedules, stock option exercises, and how to document equity compensation for underwriting purposes. A skilled broker can often qualify income sources that less experienced loan officers might overlook.

Once your profile is complete, you receive a pre-approval letter stating your maximum loan amount and purchase price. This document becomes essential when making offers in competitive neighborhoods.

Loan Application and Documentation

After identifying a property, you submit a formal loan application. The broker coordinates:

- Purchase contract review with contingency timelines

- Appraisal ordering to confirm property value

- Title and escrow coordination with your closing agent

- Homeowners insurance verification

- Final income and asset updates to satisfy underwriting conditions

Expect regular communication throughout this phase. A responsive broker provides status updates without requiring you to chase them down.

Underwriting and Closing Coordination

Once documentation is complete, the underwriter reviews your file to ensure compliance with lending guidelines. This stage often generates conditions-additional documents or explanations needed before final approval. Common requests include:

- Letters of explanation for credit inquiries or deposits

- Updated pay stubs or asset statements

- HOA documents and condo questionnaires

- Gift letter documentation for down payment assistance

Your broker manages these conditions, translating underwriter requirements into plain language and helping you gather the necessary items quickly. In Seattle's fast-paced market, this efficiency can mean closing in as few as nine business days when conditions align.

Specialized Services for Seattle-Area Buyers

The Greater Seattle region attracts diverse buyer types, each with unique financing needs. A home loan broker near me should offer specialized expertise for your situation.

First-Time Homebuyers in Shoreline and Lynnwood

First-time buyers often benefit from programs requiring lower down payments and offering flexible qualifying criteria. First-time buyer strategies include:

- Conventional loans with 3% down through Fannie Mae or Freddie Mac

- FHA loans with 3.5% down and flexible credit requirements

- Down payment assistance programs available in King and Snohomish counties

- Closing cost credits negotiated from sellers

A broker experienced with first-time buyers provides education on escrow accounts, mortgage insurance, and budgeting for homeownership costs beyond the monthly payment.

Tech Professionals with Complex Compensation

Amazon, Microsoft, and Google employees in Seattle, Bellevue, and Redmond often receive significant portions of their income through stock grants. Traditional lenders may struggle to qualify RSUs or bonus income, limiting purchasing power. A specialized broker understands:

- How to calculate average stock compensation over two years

- When to include unvested RSUs in qualifying income

- Documentation requirements for stock option exercises

- Strategies for jumbo loans above conforming limits

This expertise allows tech professionals to maximize their buying power without unnecessary down payment requirements or PMI costs.

Real Estate Investors in Mill Creek and Everett

Investment property financing follows different guidelines than primary residence loans. Investors need:

- Rental income analysis that satisfies underwriting standards

- DSCR loans that qualify based on property cash flow rather than personal income

- Portfolio lending for borrowers with multiple investment properties

- 1031 exchange coordination for tax-deferred property swaps

A broker with investor experience can structure loans that support your acquisition strategy while minimizing tax liability and preserving liquidity.

Common Mistakes When Searching for a Home Loan Broker Near Me

Even informed borrowers make missteps that complicate the mortgage process. Avoid these pitfalls to ensure a smooth transaction.

Choosing Based on Rate Alone

While competitive rates matter, the lowest advertised rate often comes with costly tradeoffs. Some brokers:

- Quote rates with high points that inflate closing costs

- Advertise rates requiring perfect credit and large down payments

- Fail to lock rates promptly, exposing you to market volatility

- Neglect to explain APR, which reflects total borrowing costs

Instead, compare total cost scenarios across multiple loan structures. A slightly higher rate with lower fees may save you thousands over the loan's first five years, especially if you plan to refinance or relocate.

Neglecting Communication Preferences

Mortgage transactions require frequent communication during a compressed timeline. If your broker:

- Takes 24+ hours to respond to questions

- Communicates only via email when you prefer phone calls

- Delegates to unresponsive assistants

- Provides vague updates without specific next steps

…you'll experience unnecessary stress during an already demanding process. Establish communication expectations upfront and confirm your broker's availability during critical phases like inspection periods and appraisal reviews.

Failing to Verify Local Market Knowledge

National online lenders advertise convenience but often lack understanding of Seattle-specific challenges. Issues that require local expertise include:

| Challenge | Impact | Local Broker Solution |

|---|---|---|

| Condo warrantability | Loan denial after contract signing | Pre-screen projects, identify approved buildings |

| Appraisal gaps | Purchase price exceeds appraised value | Recommend comps, coordinate reconsideration of value |

| Title issues | Delayed closing due to lien resolution | Work with trusted local title companies |

| HOA documentation delays | Missing closing deadlines | Proactively request documents, follow up directly |

These situations demand relationships with local appraisers, title companies, and HOA management firms that national lenders simply don't maintain.

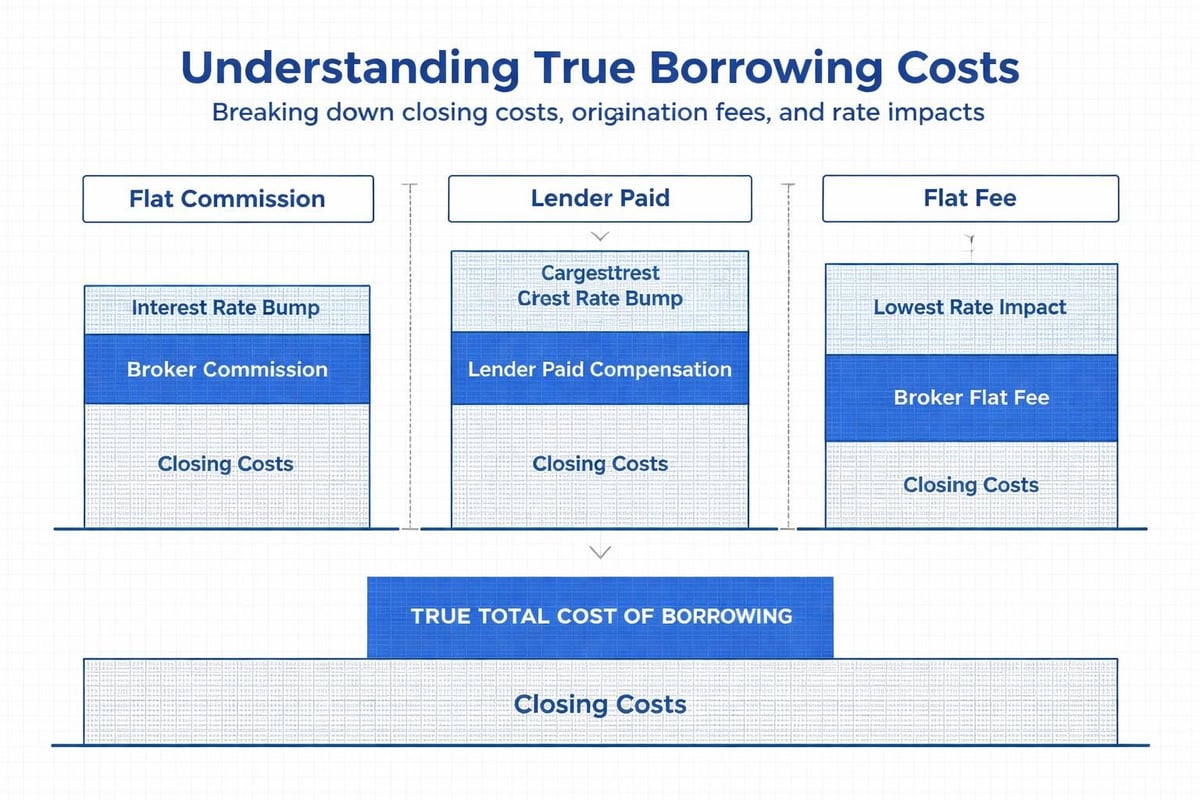

Cost Considerations and Transparency

Understanding how your broker is compensated helps you evaluate whether their recommendations serve your best interests. Tips for choosing a mortgage lender emphasize the importance of fee transparency.

Broker Compensation Models

Mortgage brokers earn compensation in three primary ways:

-

Lender-paid compensation: The wholesale lender pays the broker a percentage of the loan amount, typically 1.5% to 2.5%. This cost is built into your interest rate but doesn't appear as a separate fee on your closing disclosure.

-

Borrower-paid compensation: You pay the broker directly through an origination fee, usually 0.5% to 1.5% of the loan amount. This model often results in lower interest rates since the lender isn't covering broker fees.

-

Combination: Some scenarios blend both methods, particularly for complex loan structures or when rate buydowns are involved.

Ask your broker to disclose their compensation structure upfront. Ethical brokers provide this information willingly and explain how it impacts your rate and closing costs.

Comparing Fee Structures

When evaluating multiple brokers, request Loan Estimates for identical scenarios. Federal law requires lenders to provide this standardized form within three business days of application. Compare:

- Origination charges in Section A

- Third-party services in Section B (title, appraisal, credit reports)

- Prepaid items like property taxes and insurance

- Interest rate and monthly payment in Section 1

Focus on the total cash to close figure, which accounts for all costs minus your earnest money deposit. A broker offering a slightly higher rate but $3,000 less in fees may provide better value depending on how long you keep the loan.

Technology and the Modern Mortgage Experience

While the core mortgage process remains document-intensive, technology has streamlined many aspects of working with a home loan broker near me.

Digital Application and Document Upload

Modern brokers offer secure portals where you can:

- Complete application forms electronically

- Upload bank statements, tax returns, and pay stubs

- Sign disclosures with e-signature tools

- Track loan status in real time

These platforms reduce paperwork hassles while maintaining security standards required by federal regulations. For busy tech professionals in Seattle, the ability to upload documents from a smartphone during lunch breaks significantly simplifies the process.

Automated Underwriting and Faster Approvals

Many brokers utilize Desktop Underwriter (DU) or Loan Prospector (LP) systems that provide instant preliminary approval based on your data. These automated systems:

- Validate income and asset information through third-party verification services

- Check credit reports and identify potential issues before manual underwriting

- Recommend optimal loan programs based on your profile

- Generate condition lists that guide documentation requirements

While automated approvals don't guarantee final loan approval, they significantly reduce processing time and allow experienced brokers to close loans in as few as nine business days when circumstances permit.

Market Conditions and Timing Your Home Loan

Interest rates, inventory levels, and seasonal patterns all influence your mortgage strategy. A knowledgeable home loan broker near me monitors these factors and advises on timing.

Rate Lock Strategies

Mortgage rates fluctuate daily based on bond market activity. When you apply for a loan, you'll choose when to lock your rate. Options include:

- Immediate lock: Secure today's rate regardless of future market movement

- Float strategy: Wait for rates to improve before locking, accepting downside risk

- Float-down option: Lock with the ability to reduce your rate once if markets improve (usually requires a fee)

Your broker should explain current rate trends and recommend a strategy aligned with your risk tolerance and closing timeline. For purchase transactions in competitive Seattle neighborhoods, immediate locks provide certainty that helps you budget accurately.

Seasonal Buying Patterns in the Greater Seattle Area

Real estate activity varies throughout the year, impacting your experience when searching for a home loan broker near me:

| Season | Market Characteristics | Financing Considerations |

|---|---|---|

| Spring (Mar-May) | High inventory, maximum competition | Secure pre-approval early, expect faster timelines |

| Summer (Jun-Aug) | Peak activity, multiple offers common | Emphasize strong financing terms in offers |

| Fall (Sep-Nov) | Moderate activity, motivated sellers | Negotiate seller-paid closing costs more easily |

| Winter (Dec-Feb) | Low inventory, less competition | Take time to strengthen credit, save additional funds |

Understanding these patterns helps you time your home search and loan application for optimal results.

Red Flags to Watch for When Choosing a Broker

While most mortgage professionals operate ethically, some practices should prompt you to look elsewhere.

Pressure Tactics and Unrealistic Promises

Be cautious of brokers who:

- Guarantee approval without reviewing your finances

- Pressure you to apply immediately before reviewing options

- Discourage you from shopping with competitors

- Promise rates significantly below market averages

- Rush you through disclosures without explaining terms

How to find a mortgage broker emphasizes taking time to evaluate multiple professionals before committing.

Lack of Transparency About Costs

Red flags include:

- Refusing to disclose compensation structure

- Providing vague estimates instead of detailed fee breakdowns

- Adding unexpected charges at closing

- Switching loan programs at the last minute without clear explanation

Reputable brokers welcome questions about costs and provide clear, written explanations of all fees before you proceed.

Poor Communication and Missed Deadlines

If your broker consistently:

- Misses promised callback times

- Fails to submit documents by agreed deadlines

- Doesn't inform you of application status changes

- Blames lenders or underwriters for delays caused by incomplete submissions

…these patterns suggest disorganization that could jeopardize your closing. Don't hesitate to switch brokers if communication problems persist after you've raised concerns.

How Seattle's Competitive Market Influences Broker Selection

Seattle consistently ranks among the nation's most competitive housing markets, with median home prices exceeding $800,000 in many neighborhoods. This environment demands a home loan broker near me who understands what sellers and listing agents expect.

Pre-Approval Strength and Offer Acceptance

In multiple-offer scenarios common throughout Bellevue, Redmond, and Seattle proper, your pre-approval letter's credibility directly impacts offer acceptance. Strong pre-approvals include:

- Verified asset statements confirming you have funds for down payment and reserves

- Credit report review documenting your credit score and debt ratios

- Income documentation proving stable employment and sufficient earnings

- Property type flexibility showing you can qualify for various property types

Listing agents in competitive markets often request this backup documentation before presenting offers to sellers. A broker who thoroughly underwrites your pre-approval upfront positions you as a serious, qualified buyer.

Reputation Among Real Estate Professionals

Seattle's real estate community is interconnected. Agents, title companies, and escrow officers recognize brokers with track records of successful closings. When your agent can vouch for your broker's reliability, sellers view your offer more favorably.

This reputation stems from:

- Consistent on-time closings

- Proactive communication with all transaction parties

- Accurate initial disclosures that don't change at closing

- Problem-solving ability when challenges arise

Building relationships with trusted Seattle mortgage brokers creates competitive advantages that help you win contracts in desirable neighborhoods.

Long-Term Value of Choosing the Right Broker

Your relationship with a home loan broker near me shouldn't end at closing. The best brokers provide ongoing value through:

Periodic Rate Reviews and Refinance Opportunities

Market conditions change, and your financial situation evolves. A proactive broker monitors rates and contacts you when refinancing could:

- Lower your monthly payment by 1% or more

- Eliminate mortgage insurance once you reach 20% equity

- Convert an adjustable-rate mortgage before rates increase

- Consolidate high-interest debt through cash-out refinancing

This ongoing relationship ensures you continually optimize your housing costs rather than settling for rates that made sense years ago but no longer serve your best interests.

Future Purchase Planning

Whether you're upgrading to a larger home, purchasing investment property, or relocating within the Greater Seattle area, maintaining broker relationships simplifies future transactions. Your broker already understands:

- Your income documentation and credit profile

- Your borrowing preferences and risk tolerance

- Property types you prefer and neighborhoods you target

- Communication styles that work best for you

This familiarity accelerates future loan processes and provides consistency across multiple real estate transactions throughout your homeownership journey.

Finding the right home loan broker near me requires research, questions, and attention to both technical expertise and communication style. In Seattle's competitive market-spanning from Shoreline through Lynnwood, Lake Forest Park, Mill Creek, and Everett-local knowledge and lender relationships make measurable differences in rates, approval odds, and closing timelines. Whether you're a first-time buyer, tech professional with complex compensation, or seasoned investor, working with an experienced broker simplifies what can otherwise feel overwhelming. Keith Akada brings 25+ years of mortgage expertise and 750+ five-star reviews to every transaction, helping clients across the Greater Seattle area secure competitive financing with clear communication and reliable execution. Explore how Mortgage Reel can guide your home purchase or refinance with transparency and proven results.