Buying your first home in the Greater Seattle area can feel overwhelming, especially with median prices in neighborhoods from Shoreline to Everett continuing to challenge budgets. Fortunately, 1st time home buyer programs exist specifically to reduce financial barriers and make homeownership achievable. These programs offer down payment assistance, reduced interest rates, flexible credit requirements, and educational resources designed to give new buyers a competitive edge. Understanding which options align with your financial situation and homeownership goals is essential, particularly in markets like Seattle, Bellevue, and Redmond where inventory moves quickly and prices remain elevated.

Understanding 1st Time Home Buyer Programs

First-time homebuyer programs encompass a range of federal, state, and local initiatives designed to assist individuals purchasing their first property. The definition of a "first-time buyer" is more flexible than many people realize. Generally, you qualify if you haven't owned a home in the past three years, making these programs accessible even to those who previously owned property.

Federal Programs Available Nationwide

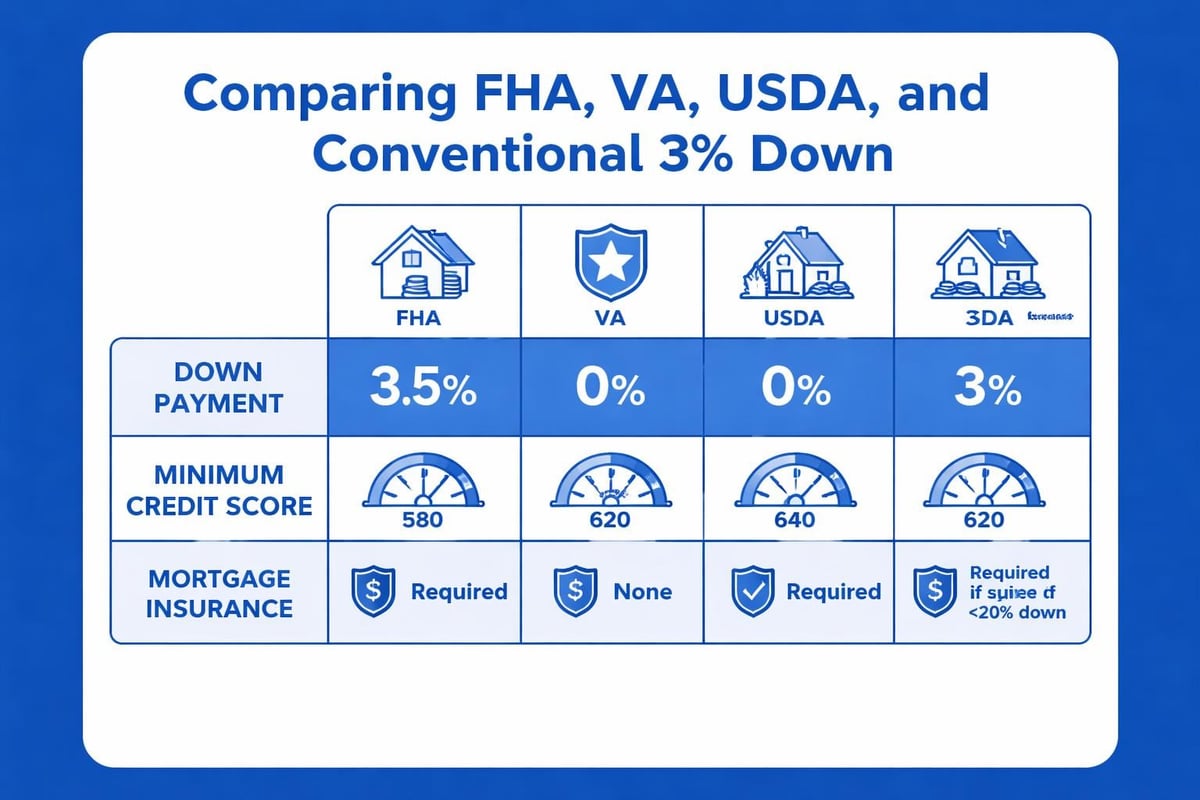

Several federal programs provide foundational support for new buyers across the country. FHA loans remain one of the most popular options, requiring as little as 3.5% down with credit scores as low as 580. These government-backed mortgages allow buyers to finance their purchase with minimal cash reserves while benefiting from competitive interest rates.

VA loans serve military members, veterans, and eligible spouses with zero down payment requirements and no private mortgage insurance. For Seattle-area buyers working at Joint Base Lewis-McChord or with military service history, this represents substantial savings over conventional financing.

USDA loans offer another zero-down option for properties in eligible rural and suburban areas. While Seattle proper doesn't qualify, portions of Mill Creek, Lynnwood, and areas around Everett may meet USDA criteria depending on population density and location.

The U.S. Department of Housing and Urban Development provides comprehensive details on these federal programs and eligibility requirements for buyers nationwide.

Washington State Housing Finance Commission Programs

Washington State offers some of the most robust 1st time home buyer programs in the country through the Washington State Housing Finance Commission (WSHFC). These programs combine competitive interest rates with down payment assistance to maximize affordability.

Home Advantage Program

The Home Advantage loan provides conventional financing with down payment options as low as 3%. This program doesn't include additional assistance but offers competitive rates and accepts various income sources, making it ideal for tech professionals in Seattle with stock compensation or RSUs from employers like Amazon, Microsoft, or Google.

Income limits apply based on county and household size, but these thresholds are generous enough to accommodate many middle-income buyers in King and Snohomish counties.

House Key Program

House Key combines a first mortgage with down payment and closing cost assistance. Eligible buyers can receive grants or deferred-payment junior loans to cover upfront expenses, significantly reducing the cash needed at closing.

This program works particularly well for buyers in Shoreline or Lake Forest Park who have stable income but limited savings for down payment. The assistance doesn't require monthly payments and is forgiven after meeting occupancy requirements.

| Program | Down Payment | Income Limits | Best For |

|---|---|---|---|

| Home Advantage | 3% minimum | County-specific | Stable income, limited savings |

| House Key | 3% + assistance | County-specific | Low savings, need grant help |

| Home Choice | 1% down | Lower thresholds | Moderate income households |

Home Choice Program

Home Choice reduces the down payment requirement to just 1% for qualified buyers, with WSHFC contributing an additional 2%. This program targets low- to moderate-income households and includes income limits below those of Home Advantage.

Buyers purchasing in Lynnwood or Everett often find Home Choice particularly valuable when competing against cash offers, as it minimizes upfront costs while maintaining strong purchasing power.

Down Payment Assistance Programs

Down payment assistance represents one of the most significant benefits available through 1st time home buyer programs. These funds come in various forms, each with distinct repayment terms and eligibility criteria.

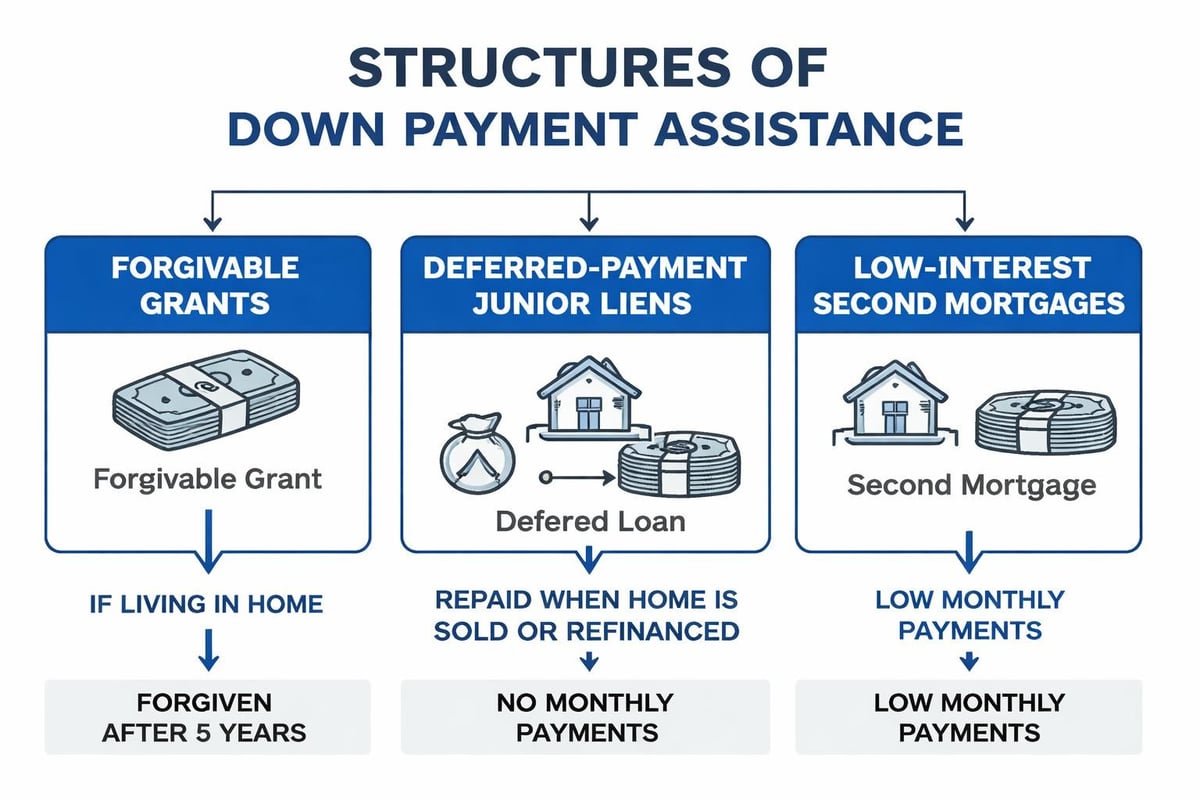

Grant programs provide money that doesn't require repayment, assuming you meet occupancy and ownership requirements for a specified period. These represent the most valuable assistance type but often have stricter income and purchase price limits.

Deferred-payment loans create a junior lien on your property with no monthly payment required. The loan becomes due when you sell, refinance, or no longer occupy the home as your primary residence. Many programs forgive these loans entirely after 10-15 years of continuous occupancy.

Low-interest second mortgages require monthly payments but offer rates significantly below market. These work well for buyers who can afford slightly higher monthly costs in exchange for immediate purchasing power.

Freddie Mac’s homebuyer resources outline additional conventional options that may include reduced down payment requirements and built-in affordability features.

Conventional 3% Down Options

Beyond government-backed programs, conventional mortgages now offer 3% down payment options through programs like HomeReady and Home Possible. These 1st time home buyer programs provide flexibility without FHA mortgage insurance requirements that persist for the loan's life.

HomeReady Advantages

Fannie Mae's HomeReady program accepts income from non-borrower household members, making it valuable for multi-generational households common in Seattle's diverse communities. The program also offers reduced mortgage insurance costs and accepts non-traditional credit when traditional credit history is limited.

Buyers working in tech industries can benefit from HomeReady's ability to use stock vesting schedules and bonus income projections when calculating qualifying income, particularly relevant for Amazon and Microsoft employees with substantial equity compensation.

Home Possible Benefits

Freddie Mac's Home Possible offers similar 3% down financing with income limits based on area median income. The program requires homebuyer education, ensuring you understand the mortgage process and long-term obligations before closing.

For buyers in Redmond or Kirkland working for tech companies, Home Possible can accommodate complex income documentation while maintaining competitive rates and reasonable mortgage insurance costs.

Local City and County Programs

King and Snohomish counties offer additional 1st time home buyer programs that layer with state and federal options to maximize assistance.

Seattle Office of Housing

Seattle provides down payment assistance loans up to $115,000 for income-qualified buyers purchasing within city limits. These deferred loans carry zero interest and no monthly payment, becoming due only upon sale or refinance.

Income limits adjust annually based on area median income, with separate thresholds for different household sizes. The program prioritizes buyers purchasing in designated opportunity areas and may offer additional assistance for these targeted neighborhoods.

Snohomish County HOME Program

Snohomish County administers federal HOME Investment Partnerships Program funds to assist buyers in Lynnwood, Mill Creek, Everett, and other county areas. Assistance amounts vary based on available funding and property location, with forgivable loans available for qualified applicants.

These programs often have application deadlines and limited annual funding, making early preparation and quick action essential when funds become available.

Credit and Income Requirements

Understanding qualification criteria for 1st time home buyer programs helps you prepare effectively and choose the right option for your financial profile.

Minimum Credit Scores

Most programs require minimum credit scores between 580 and 640, though specific requirements vary by program and lender. FHA loans accept scores as low as 580 with 3.5% down or 500 with 10% down. Conventional programs typically require 620 or higher, with better rates available above 680.

Building credit before applying improves both program eligibility and interest rate pricing. Focus on these priorities:

- Pay all bills on time for at least 12 months before applying

- Reduce credit card balances below 30% of limits

- Avoid opening new credit accounts in the six months before purchase

- Dispute any credit report errors well in advance

Income Documentation Standards

1st time home buyer programs generally require two years of employment history and income documentation, though exceptions exist for recent graduates and those changing careers. Acceptable documentation includes:

- W-2 forms and recent pay stubs for salaried employees

- Tax returns and profit/loss statements for self-employed buyers

- RSU vesting schedules and stock compensation statements

- Offer letters and employment verification for new positions

Tech professionals in Seattle often have complex income structures combining base salary, bonuses, stock grants, and equity compensation. Working with a mortgage broker experienced in documenting these income sources ensures maximum qualifying power and program eligibility.

The Consumer Financial Protection Bureau’s guide to owning a home explains documentation requirements and mortgage qualification standards in detail.

Homebuyer Education Requirements

Many 1st time home buyer programs require completion of an approved homebuyer education course before closing. These courses cover essential topics including budgeting, mortgage types, the purchase process, and homeownership responsibilities.

Course Benefits

Education requirements provide genuine value beyond program qualification. You'll learn to:

- Calculate realistic budgets including taxes, insurance, and maintenance

- Compare loan programs and understand rate locks and points

- Navigate inspection, appraisal, and closing processes confidently

- Identify predatory lending practices and avoid common mistakes

- Plan for long-term homeownership costs and equity building

Available Formats

Courses are available online and in-person through HUD-approved counseling agencies. Online courses offer flexibility for busy professionals, while in-person sessions provide opportunities to ask specific questions about Seattle-area market conditions.

Most courses cost $50-$100 and take 6-8 hours to complete. Certificates are typically valid for two years, allowing you to complete education early while saving for down payment.

Tax Benefits and Additional Incentives

First-time homebuyers gain access to tax advantages that improve overall affordability beyond program assistance.

Mortgage Interest Deduction

Interest paid on mortgages up to $750,000 is generally tax-deductible, providing substantial savings for buyers in Seattle's higher-priced market. This deduction reduces your effective mortgage cost, particularly in the early years when interest comprises most of your payment.

Mortgage Credit Certificate Program

Washington State offers a Mortgage Credit Certificate (MCC) that converts a portion of your mortgage interest into a dollar-for-dollar tax credit. The MCC provides up to $2,000 annually in federal tax credits, effectively reducing your tax liability and increasing take-home pay.

This program layers with other 1st time home buyer programs, allowing you to combine down payment assistance with ongoing tax savings. Income limits apply, and you must use the MCC with your initial purchase loan.

Property Tax Exemptions

Some Washington jurisdictions offer property tax exemptions for new construction or designated development areas. While not specifically first-time buyer programs, these exemptions can significantly reduce ownership costs during the initial years.

Common Mistakes to Avoid

New buyers often encounter preventable obstacles when pursuing 1st time home buyer programs. Awareness helps you navigate the process smoothly and maintain program eligibility.

Timing and Application Errors

Applying too late represents a critical mistake. Many assistance programs have application deadlines or limited funding that depletes quickly. Research and apply for programs before starting your home search, ensuring funds are reserved when you find the right property.

Changing employment during the mortgage process can jeopardize approval. Lenders verify employment immediately before closing, and job changes may require restarting qualification with new income documentation.

Making large purchases on credit before closing affects your debt-to-income ratio and potentially disqualifies you from the loan. Avoid financing cars, furniture, or other items until after your mortgage funds.

Program Compliance Issues

Each program includes specific occupancy requirements, typically mandating you occupy the home as your primary residence for a minimum period. Renting the property or purchasing it as an investment violates program terms and may trigger full repayment of assistance.

Understanding recapture provisions prevents surprises. Some programs require repaying assistance if you sell within specific timeframes or if your income increases substantially. Read all program documentation carefully and ask questions about any unclear terms.

Combining Multiple Programs

Strategic buyers often layer multiple 1st time home buyer programs to maximize assistance and minimize out-of-pocket costs. This approach requires careful coordination but can significantly improve affordability.

A common combination uses a WSHFC first mortgage with down payment assistance, layers in a city or county assistance program, and incorporates a Mortgage Credit Certificate for ongoing tax savings. This structure might provide:

- 3% down payment conventional loan through WSHFC

- $30,000 down payment assistance from Seattle Office of Housing

- $2,000 annual tax credit through MCC program

The result dramatically reduces both upfront costs and monthly payment burden compared to conventional financing without assistance.

Program stacking requires understanding how different assistance sources interact and ensuring you meet all eligibility requirements simultaneously. Some programs explicitly allow combining while others prohibit it, making expert guidance valuable.

Special Considerations for Tech Professionals

Seattle-area tech employees face unique opportunities and challenges when accessing 1st time home buyer programs. Stock compensation, restricted stock units, and performance bonuses create substantial income but require specialized documentation.

RSU and Stock Income Qualification

Most 1st time home buyer programs allow using RSU income for qualification once you have a two-year history of receiving equity compensation. Lenders average the past two years' vested amounts and project future income based on current vesting schedules.

For Amazon employees with substantial RSU packages, this often means qualifying for significantly higher loan amounts than base salary alone would support. However, program income limits sometimes create complications, as total compensation including stock may exceed thresholds while base salary remains under limits.

Bonus and Variable Income

Annual bonuses and variable compensation generally require a two-year history for qualification purposes. Lenders average the amounts received and may discount inconsistent bonuses or declining trends.

Microsoft employees with predictable bonus structures find qualification straightforward, while those in sales roles or with highly variable compensation may need additional documentation explaining income sources and sustainability.

Navigating Seattle's Competitive Market

Using 1st time home buyer programs effectively in Seattle's fast-moving market requires strategy and preparation. Multiple offers remain common in desirable neighborhoods, and sellers may favor conventional financing over government-backed loans.

Strengthening Your Offer

Despite using assistance programs, you can compete effectively by:

- Getting fully underwritten pre-approval before making offers

- Offering shorter inspection periods when confident in property condition

- Including escalation clauses with competitive caps

- Writing personal letters explaining your connection to the area

- Demonstrating financial strength through substantial reserves

Conventional 3% down programs often compete more effectively than FHA financing because they don't require FHA appraisal standards that sometimes challenge older Seattle homes.

Working with Experienced Professionals

Real estate agents familiar with 1st time home buyer programs understand how to position your offer competitively while using assistance. They can identify sellers likely to accept program financing and negotiate terms that protect your interests while appealing to seller priorities.

USA.gov’s home buying guide provides general information about the purchase process and federal resources available to new buyers.

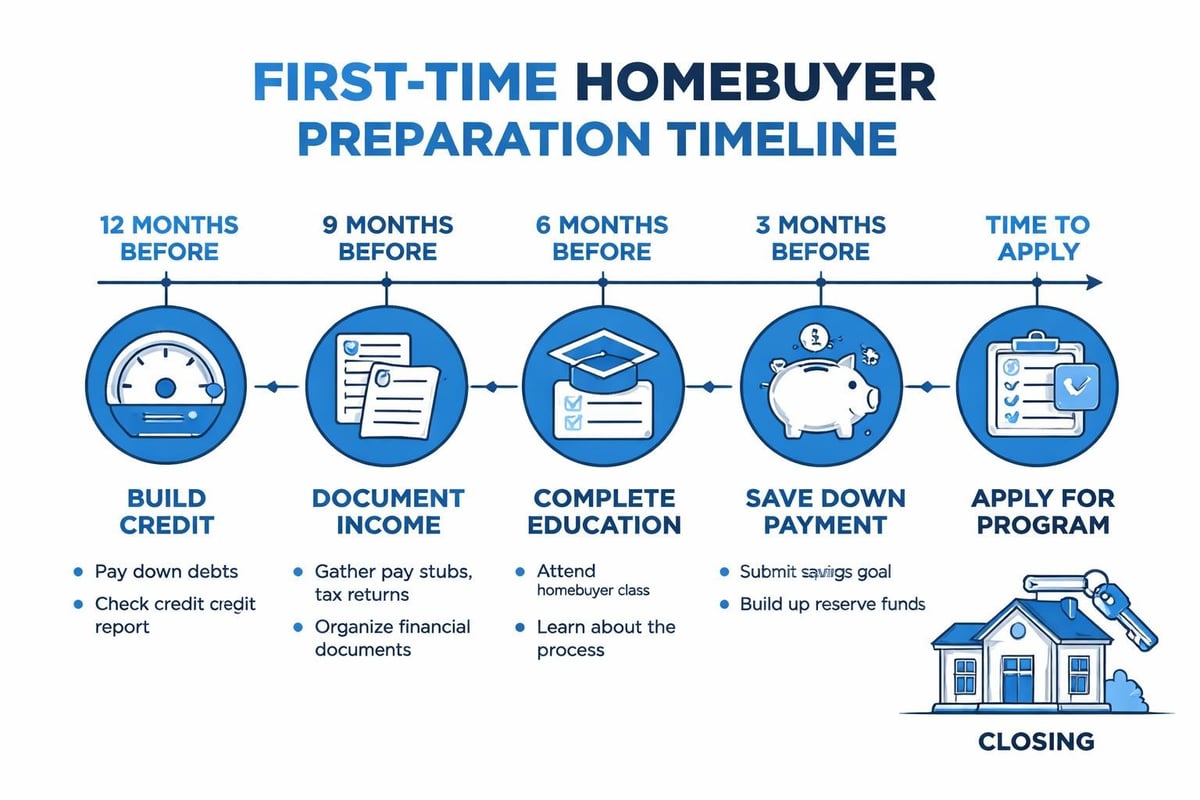

Application Process and Timeline

Understanding the application timeline for 1st time home buyer programs helps you plan effectively and avoid delays that could cost you a desired property.

Pre-Qualification Phase

Start by gathering financial documentation and researching available programs 6-12 months before your target purchase date. This allows time to:

- Complete required homebuyer education courses

- Build or repair credit to meet minimum score requirements

- Save additional funds for down payment and reserves

- Research neighborhoods and price ranges within your budget

- Apply for assistance programs with application deadlines

Formal Application Steps

Once you're ready to purchase, the formal process typically follows this sequence:

- Submit assistance program applications and receive conditional approval or funding reservation

- Obtain pre-approval from a lender who participates in your chosen programs

- Search for homes within program price limits and eligible areas

- Make an offer and enter into a purchase agreement

- Finalize assistance program approval with property-specific information

- Complete underwriting and satisfy all loan conditions

- Close on your home and fulfill occupancy requirements

The entire process from application to closing typically takes 30-45 days for straightforward transactions, though complex income documentation or program coordination may extend this timeline.

Income and Price Limits by County

Understanding county-specific limits for 1st time home buyer programs helps you identify which options align with your situation and target neighborhoods.

| County | Area Median Income | Typical Buyer Limit | Max Purchase Price |

|---|---|---|---|

| King (Seattle) | $129,300 | $155,160 (120% AMI) | $1,149,825 |

| Snohomish | $113,600 | $136,320 (120% AMI) | $1,020,200 |

These limits update annually and vary by household size. Programs using 120% of area median income accommodate many moderate-income buyers, while those limited to 80% serve primarily lower-income households.

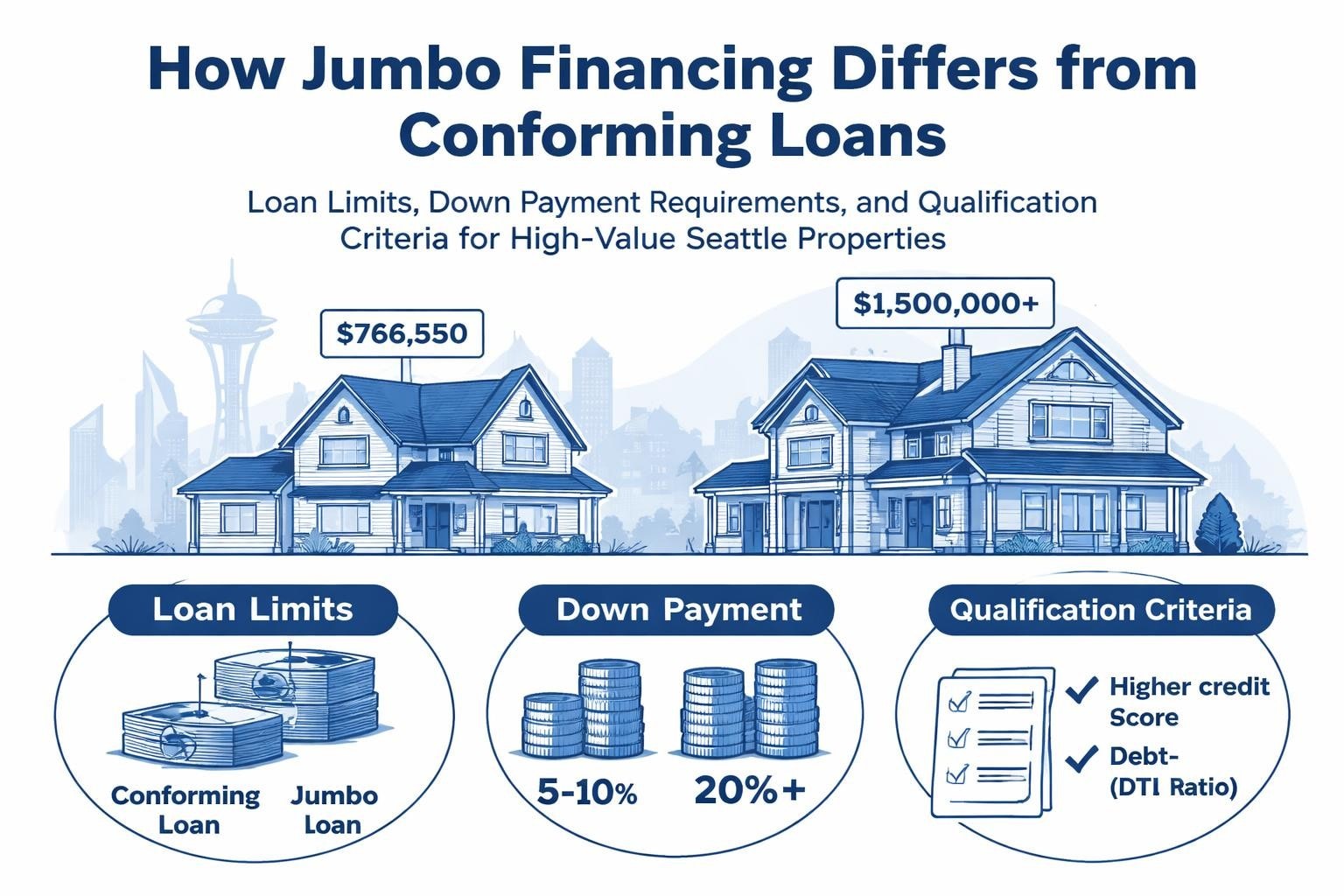

Purchase price limits often align with conforming loan limits but may be lower for specific programs. The 2026 conforming limit of $806,500 applies to most of King and Snohomish counties, with higher limits in designated high-cost areas.

Alternative Paths to Homeownership

When traditional 1st time home buyer programs don't align with your situation, alternative approaches can still make homeownership achievable.

Gift Funds and Family Assistance

Many programs allow using gift funds from family members for down payment and closing costs. Gifts must be properly documented with gift letters confirming the funds require no repayment, but they can supplement your savings significantly.

This approach works particularly well when combined with programs requiring minimal personal down payment, allowing you to use gifted funds for closing costs and reserves while program assistance covers the majority of the down payment.

Individual Development Accounts

Some nonprofit organizations offer Individual Development Account (IDA) programs that match your savings toward homeownership goals. You contribute regularly to a dedicated account, and the organization matches your deposits at rates from 1:1 to 4:1.

These programs typically require financial education and have income eligibility requirements, but they can dramatically accelerate your savings timeline while building financial management skills.

Program Resources and Next Steps

Multiple resources help you identify and access 1st time home buyer programs effectively:

- Washington State Housing Finance Commission maintains current program details, income limits, and participating lender lists

- HUD-approved housing counseling agencies provide free guidance on program eligibility and application processes

- Local housing authorities in Seattle, Shoreline, Lynnwood, and other cities offer city-specific assistance information

- Experienced mortgage brokers who specialize in first-time buyer programs can navigate complex qualification and coordinate multiple assistance sources

Bankrate’s comprehensive guide to first-time homebuyer programs offers state-specific information including Washington programs and eligibility criteria.

Begin your preparation by assessing your current financial position, researching programs that match your income and target purchase price, and completing required education courses. This foundation positions you to act quickly when you find the right property and ensures you maximize available assistance.

The competitive Seattle market rewards prepared buyers who understand their options and can move decisively. By combining appropriate 1st time home buyer programs with strategic offer presentation and experienced professional guidance, you can successfully navigate the purchase process and achieve your homeownership goals, even in challenging market conditions like those in Seattle, Bellevue, Redmond, and surrounding communities.

Understanding and accessing 1st time home buyer programs transforms homeownership from aspirational to achievable, particularly in competitive markets throughout the Greater Seattle area. Whether you're considering properties in Shoreline, evaluating options in Lynnwood, or searching in Everett, the right combination of programs and expert guidance makes the difference. Keith Akada brings 25+ years of experience helping first-time buyers navigate complex assistance programs, qualify stock compensation and variable income, and compete effectively in Seattle's challenging market. Ready to explore which programs fit your situation and start your path to homeownership? Connect with Mortgage Reel today for personalized guidance backed by 750+ five-star reviews and a proven track record of successful first-time buyer closings.