Understanding jumbo mortgage loan rates is essential for homebuyers in Seattle and surrounding communities where property values frequently exceed conforming loan limits. With median home prices in neighborhoods across Seattle, Bellevue, and Kirkland consistently pushing into jumbo territory, knowing how these specialized mortgages work can mean the difference between securing your dream home and missing out. Whether you're a tech professional at Amazon or Microsoft looking to use stock compensation for a larger purchase, or a move-up buyer exploring luxury properties in Shoreline or Mill Creek, jumbo financing offers unique opportunities and considerations that differ significantly from conventional loans.

What Makes Jumbo Mortgage Loan Rates Different

Jumbo mortgages exceed the conforming loan limits set annually by the Federal Housing Finance Agency. In 2026, the baseline conforming limit stands at $806,500 for most single-family homes, though this threshold varies by county. Any loan amount above this threshold requires jumbo financing, which operates under different underwriting standards and pricing structures.

Key differences in jumbo lending include:

- Higher credit score requirements (typically 700 minimum, 740+ for best rates)

- Lower maximum debt-to-income ratios (usually 43% or less)

- Larger down payment expectations (often 10-20% minimum)

- More extensive documentation of income and assets

- Stricter appraisal requirements and property condition standards

The interest rates on jumbo loans historically carried a premium over conforming rates due to increased lender risk. However, market dynamics have shifted considerably. In many cases throughout 2025 and into 2026, jumbo mortgage rates have actually dropped below conforming rates, creating advantageous opportunities for qualified borrowers in high-cost markets like Seattle.

Why Jumbo Rates Sometimes Beat Conforming Rates

This rate inversion happens for several reasons. Jumbo borrowers typically present stronger financial profiles with substantial assets, higher incomes, and excellent credit histories. Lenders recognize this reduced risk profile. Additionally, portfolio lenders who hold jumbo loans rather than selling them to government-sponsored enterprises can price more competitively based on the borrower's complete financial picture.

Current Jumbo Mortgage Loan Rates Landscape in 2026

Interest rate trends for jumbo mortgages reflect broader economic conditions, Federal Reserve policy, and investor appetite for mortgage-backed securities. Throughout early 2026, rates have remained influenced by inflation concerns, employment data, and geopolitical factors that affect treasury yields.

| Loan Type | Typical Rate Range | Credit Score Requirement | Down Payment |

|---|---|---|---|

| 30-Year Fixed Jumbo | 6.25% – 7.00% | 740+ | 20% |

| 15-Year Fixed Jumbo | 5.75% – 6.50% | 740+ | 20% |

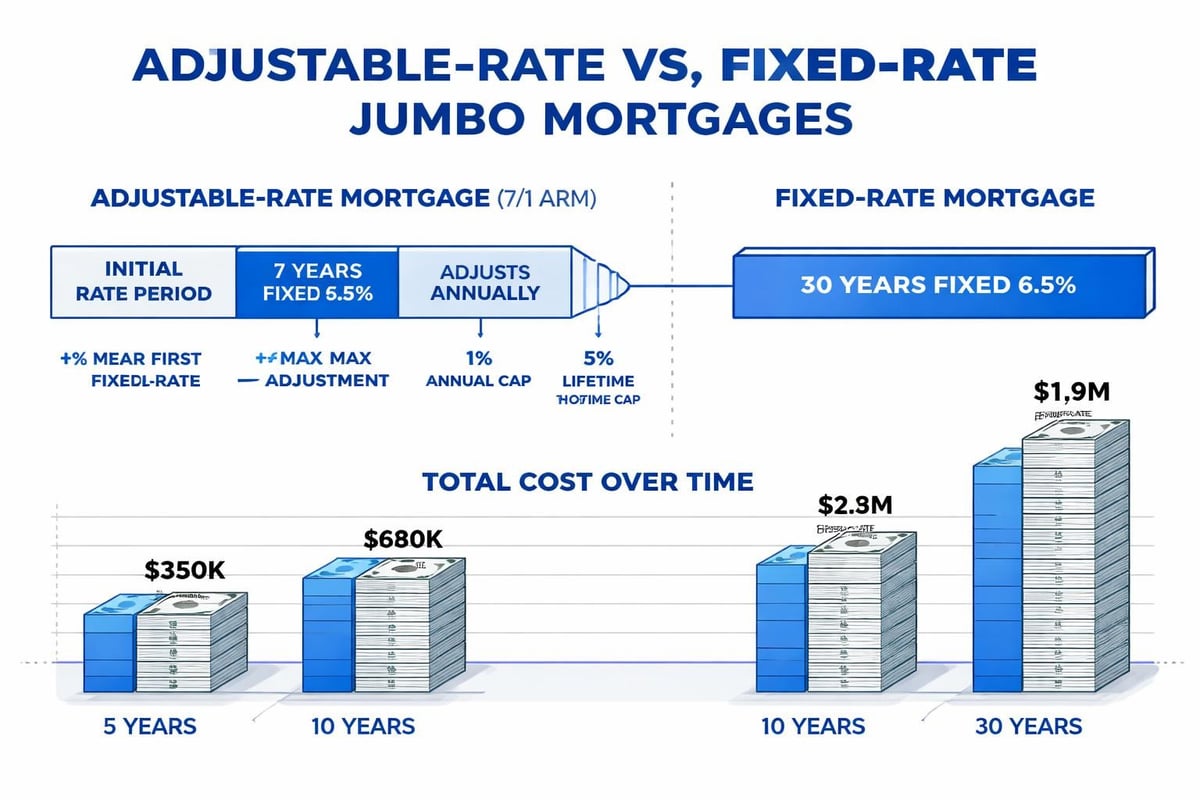

| 7/1 ARM Jumbo | 5.50% – 6.25% | 720+ | 15-20% |

| 5/1 ARM Jumbo | 5.25% – 6.00% | 720+ | 15-20% |

These ranges represent general market conditions and vary significantly based on individual borrower profiles. A Microsoft engineer in Redmond with a 780 credit score, 30% down payment, and substantial RSU holdings will receive dramatically better pricing than a borrower at minimum qualification thresholds.

Current jumbo mortgage rate data shows considerable variation among lenders, making rate shopping particularly valuable. Even a quarter-point difference on a $1.2 million loan translates to substantial savings over the life of the mortgage.

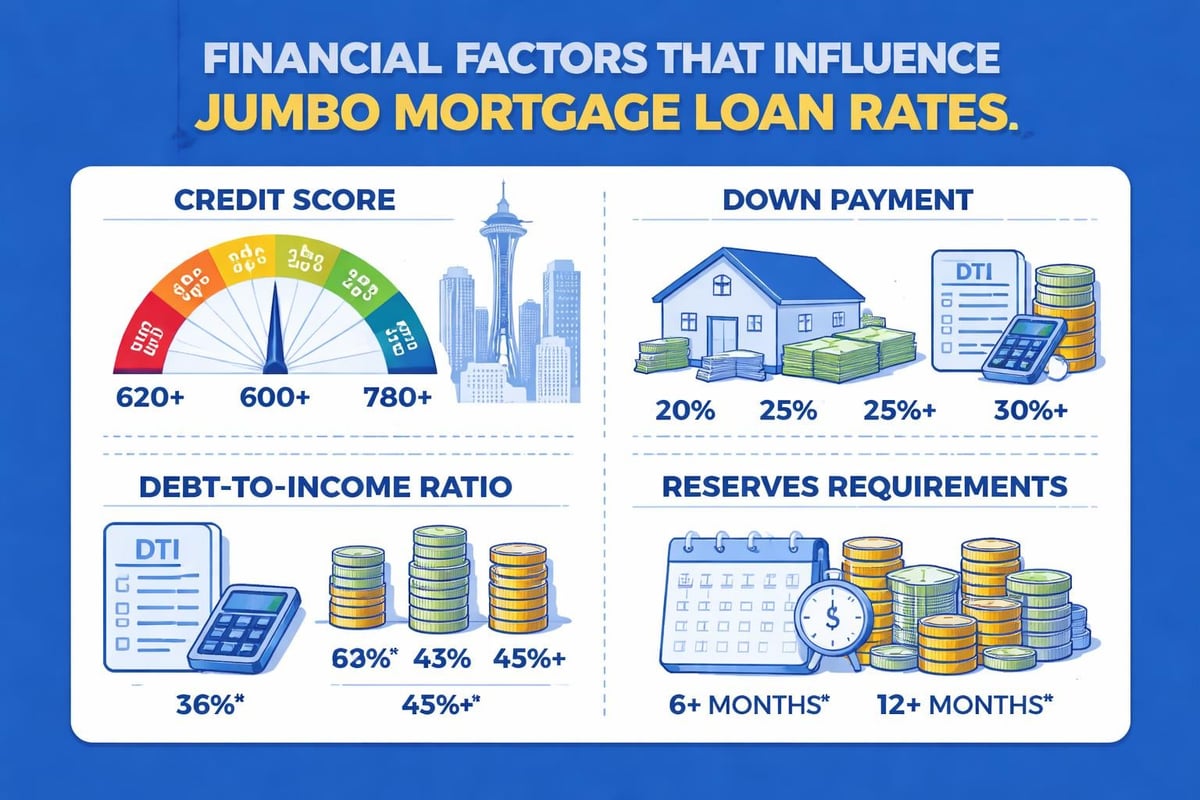

Qualification Requirements for Jumbo Mortgages

Meeting jumbo loan criteria requires careful financial preparation. Lenders scrutinize every aspect of your financial profile because they're taking on loans that cannot be sold to Fannie Mae or Freddie Mac, meaning they often hold more risk on their own balance sheets.

Credit Score and History Standards

Most jumbo lenders establish a 700 credit score floor, but competitive rates require scores of 740 or higher. Beyond the number itself, underwriters examine:

- Payment history across all credit accounts over the past 24 months

- Credit utilization ratios (preferably below 30% on revolving accounts)

- Recent credit inquiries and new account openings

- Any derogatory marks, collections, or public records

- Length of established credit history

For buyers in Lake Forest Park or Lynnwood purchasing homes in the $900,000 to $1.3 million range, maintaining pristine credit for at least 12 months before applying yields the best rate outcomes.

Down Payment and Reserve Requirements

While some jumbo programs allow as little as 10% down, putting down 20% or more significantly improves your rate and eliminates private mortgage insurance. Many lenders prefer seeing 25-30% down on properties exceeding $1.5 million.

Reserve requirements typically include:

- Six to twelve months of mortgage payments (principal, interest, taxes, insurance)

- Additional reserves for other financed properties you own

- Documentation showing liquid, seasoned assets (not recent deposits)

- Retirement accounts may count at 70% of value

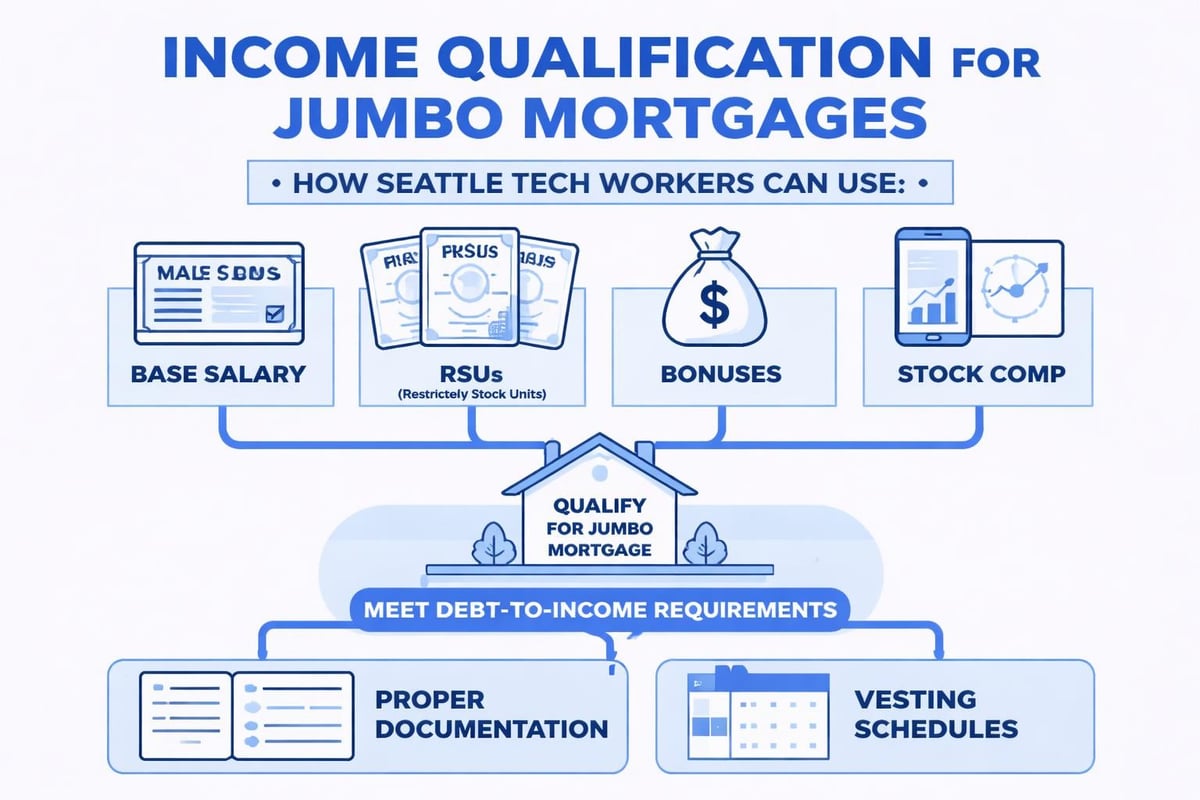

Tech professionals often leverage vested RSUs and stock holdings to satisfy reserve requirements, though underwriters apply discounts to equity compensation based on volatility and liquidity restrictions.

Income Documentation and Debt-to-Income Ratios

Jumbo lenders maintain conservative debt-to-income (DTI) standards, typically capping total DTI at 43% and preferring front-end ratios (housing expense only) below 35%. This means a borrower needs substantial documented income to support larger loan amounts.

Qualifying Complex Compensation Structures

For Amazon, Google, and Microsoft employees throughout Seattle and Redmond, stock-based compensation forms a significant portion of total earnings. Qualifying this income for jumbo mortgages requires understanding specific guidelines:

- RSUs and Stock Awards: Typically require two-year history of receipt and vesting documentation

- Bonuses: Need two-year history showing consistency and likelihood of continuance

- Stock Options: Usually only exercised, sold options count as income

- Base Salary: W-2 wages form the foundation of qualification

Working with a mortgage broker experienced in tech compensation helps maximize qualifying income. Many Seattle-area borrowers discover they can afford significantly more than initially expected once all compensation elements are properly documented and calculated.

The recent Federal Housing Finance Agency increase in conforming loan limits to $806,500 means some borrowers who previously required jumbo financing now qualify for conventional loans. However, with median home prices in desirable Seattle neighborhoods ranging from $900,000 to well over $2 million, jumbo mortgages remain essential for most move-up buyers and luxury purchases.

Strategies for Securing the Best Jumbo Mortgage Loan Rates

Rate optimization for jumbo mortgages involves more than just shopping lenders. Strategic timing, financial positioning, and negotiation all contribute to securing favorable terms.

Improve Your Rate Position Before Applying

Taking 3-6 months to strengthen your financial profile before formally applying can save tens of thousands over the loan term:

- Pay down credit card balances to below 10% utilization

- Avoid opening new credit accounts or making large purchases

- Accumulate additional reserves beyond minimum requirements

- Increase your planned down payment if possible

- Address any credit report errors or discrepancies

Lender shopping best practices:

- Compare at least three to five lenders specializing in jumbo products

- Request loan estimates on the same day for accurate comparison

- Look beyond rate to fees, points, and closing costs

- Evaluate ARM products if you plan to move or refinance within seven years

- Consider portfolio lenders who may offer more flexibility

Rate Lock Timing and Float Strategies

Once you've selected a lender, deciding when to lock your rate requires understanding market trends and your purchase timeline. In volatile rate environments, locking early provides certainty. When rates show downward momentum, floating with a lock option preserves flexibility.

Most lenders offer lock periods from 30 to 60 days, with longer locks carrying higher costs. For new construction purchases in Everett or Mill Creek where closing dates remain uncertain, extended locks or float-down provisions become valuable tools.

Jumbo Loan Products and Term Options

Beyond standard 30-year fixed mortgages, jumbo borrowers access various product structures designed for different financial situations and goals.

| Product Type | Best For | Key Advantage | Primary Consideration |

|---|---|---|---|

| 30-Year Fixed | Long-term homeownership, stability | Predictable payment, locked rate | Higher rate than shorter terms |

| 15-Year Fixed | Equity building, lower total interest | Significant interest savings | Higher monthly payment |

| 7/1 ARM | 5-7 year ownership horizon | Lower initial rate | Rate adjusts after fixed period |

| 10/1 ARM | Medium-term ownership | Balance of rate and stability | Less predictable long-term |

| Interest-Only | Cash flow management, investment properties | Lower initial payments | No principal reduction, higher refinance risk |

Adjustable-rate jumbo mortgages deserve particular attention in 2026's rate environment. With initial rates sometimes 50-75 basis points below fixed options, ARMs provide compelling value for borrowers with shorter time horizons or those anticipating income growth.

Interest-Only Jumbo Mortgages

Interest-only products allow payment flexibility by requiring only interest payments for an initial period (typically 5-10 years) before converting to fully amortizing payments. These work well for borrowers with variable income, bonus-heavy compensation, or investment strategies.

A Shoreline buyer purchasing a $1.4 million property with substantial year-end bonuses might use interest-only payments to minimize monthly obligations, then make large principal payments annually. This strategy requires discipline and clear financial planning to avoid payment shock when the loan converts to principal and interest.

Property Types and Jumbo Mortgage Considerations

Not all properties qualify equally for jumbo financing. Lenders apply varying standards based on property type, location, and characteristics that affect marketability and risk.

Single-Family Homes and Condominiums

Detached single-family residences receive the most favorable jumbo mortgage loan rates and terms. Condominiums face additional scrutiny including HOA financial health reviews, percentage of owner-occupied units, and litigation history. Some lenders limit jumbo condo financing or add rate premiums.

Vacation homes and second homes typically require:

- Minimum 20-30% down payment

- Higher credit scores (750+)

- Additional reserves (12+ months)

- Clear explanation of intended use

- Distance requirements from primary residence

Investment properties using jumbo financing carry the strictest requirements with 25-30% down payments, higher rates, and more extensive documentation proving rental income potential.

Tax Implications and Financial Planning

Understanding the tax treatment of jumbo mortgages helps optimize your overall financial strategy. The 2026 tax code maintains the mortgage interest deduction with specific limitations affecting jumbo borrowers.

Interest on mortgage debt up to $750,000 remains deductible for married couples filing jointly (half that for single filers). For a $1.2 million mortgage, only the interest on $750,000 of principal qualifies for deduction. This limitation makes running the numbers with a tax professional valuable before finalizing your loan amount.

High earners in Seattle's tech sector may find that maximizing retirement contributions, optimizing equity compensation timing, and strategic property ownership structures provide more tax efficiency than relying solely on mortgage interest deductions.

Common Pitfalls to Avoid When Seeking Jumbo Financing

Even sophisticated borrowers make mistakes that cost them better rates or delay closings. Awareness of common issues helps you navigate the jumbo loan process smoothly.

Documentation and Timeline Mistakes

- Large unexplained deposits: Any deposit over $1,000 requires documentation; gift funds need proper paperwork

- Job changes during underwriting: Switching employers, even for promotions, can derail approval

- Major purchases before closing: Buying cars, furniture, or taking on new debt alters your qualification

- Inadequate appraisal preparation: Property condition issues or comparable sales gaps create valuation problems

Rate Shopping Errors

Comparing jumbo mortgage loan rates requires understanding that advertised rates rarely reflect what you'll actually receive. Rates depend on your specific credit profile, down payment, property type, and loan amount. A quote for one borrower means nothing for another with different qualifications.

Comparing jumbo rates across multiple lenders on the same day, with identical scenarios, provides the only valid comparison. Request detailed loan estimates showing all fees, not just interest rates.

The Appraisal Process for Jumbo Properties

Jumbo mortgages require more rigorous appraisals than conforming loans. Lenders often mandate two appraisals for loans exceeding $1.5 million, particularly in areas with limited comparable sales data.

Appraisers must find recent sales (within 6-12 months) of similar properties within reasonable proximity. In neighborhoods like Bellevue or Kirkland where luxury homes vary widely in features and finishes, establishing accurate valuations becomes complex. Understanding how appraisers work helps you set realistic expectations and avoid overpriced purchases.

Supporting a strong appraisal:

- Provide the appraiser with recent comparable sales data

- Complete any deferred maintenance before the appraisal

- Document recent upgrades or improvements with receipts

- Ensure the property is clean and presentable during inspection

If the appraisal comes in low, options include renegotiating the purchase price, increasing your down payment to maintain the loan-to-value ratio, or challenging the appraisal with additional comparable sales data.

Working with Specialized Jumbo Lenders

Not all mortgage lenders offer competitive jumbo programs. Banks and credit unions with portfolio lending capabilities often provide the most flexibility and competitive pricing because they hold loans rather than selling them to secondary markets.

Portfolio lenders evaluate your complete financial profile rather than relying solely on automated underwriting. This human element benefits borrowers with complex income structures, multiple properties, or unique situations that don't fit standard guidelines perfectly.

Finding a mortgage broker with deep jumbo lending experience and relationships with multiple portfolio lenders expands your options significantly. A broker can match your specific situation to the lender most likely to offer favorable terms based on your strengths.

Refinancing Jumbo Mortgages

Market conditions change, and refinancing your jumbo mortgage can provide substantial savings when rates drop or your financial situation improves. The same qualification standards apply, though you'll benefit from any principal paydown and property appreciation since your original purchase.

Refinancing makes sense when:

- Current rates are at least 0.50-0.75% below your existing rate

- You can recover closing costs through savings within 2-3 years

- You're converting from an ARM to fixed before adjustment

- You're consolidating higher-interest debt or removing PMI

- You need to access equity for improvements or investments

The jumbo mortgage rate environment in 2026 has created opportunities for borrowers who financed in 2024-2025 at higher rates. Even small rate reductions on million-dollar-plus loans generate meaningful monthly and lifetime savings.

Regional Market Factors Affecting Seattle Jumbo Rates

Local market conditions influence jumbo mortgage availability and pricing. Seattle's strong employment market, limited housing inventory, and consistent population growth create competitive dynamics that affect lending.

Property values in Seattle proper have appreciated steadily, with neighborhoods like Queen Anne, Capitol Hill, and Madison Park seeing median prices well into jumbo territory. Suburbs including Lynnwood and Everett offer more affordable entry points, though desirable areas in these communities also frequently exceed conforming limits.

Understanding neighborhood-specific trends helps you time purchases strategically and negotiate effectively. Working with professionals who specialize in Seattle-area lending ensures you're getting guidance based on current local conditions rather than national averages that may not apply to this unique market.

Securing favorable jumbo mortgage loan rates in Seattle's competitive market requires understanding qualification requirements, comparing lender options strategically, and optimizing your financial profile before applying. Whether you're purchasing a luxury home in Seattle or a growing family residence in Mill Creek, working with an experienced professional makes all the difference. Keith Akada at Mortgage Reel brings 25+ years of expertise helping Seattle-area homebuyers navigate jumbo financing, with specialized knowledge in qualifying complex tech compensation and closing loans efficiently in competitive markets.