Understanding how brokers finance works is essential for anyone navigating the Seattle housing market in 2026. Whether you're a first-time homebuyer in Shoreline, a tech professional relocating to Bellevue, or a real estate investor expanding your portfolio in Mill Creek, working with a mortgage broker offers distinct advantages over going directly to a single bank. Brokers finance relationships differently than traditional lenders because they act as intermediaries, accessing multiple lending sources to find competitive rates and loan programs tailored to your unique financial situation. This comprehensive guide explains the mechanics, regulatory framework, and strategic benefits of brokers finance for Greater Seattle homebuyers.

What Brokers Finance Actually Means

Brokers finance refers to the process where licensed mortgage professionals facilitate loan transactions between borrowers and lenders. Unlike retail banks that only offer their own loan products, mortgage brokers maintain relationships with dozens of wholesale lenders, credit unions, and specialized financing institutions.

The core function involves:

- Evaluating your financial profile and homeownership goals

- Identifying lenders whose guidelines align with your situation

- Submitting your application to multiple sources simultaneously

- Negotiating terms and pricing on your behalf

- Managing the entire transaction from application to closing

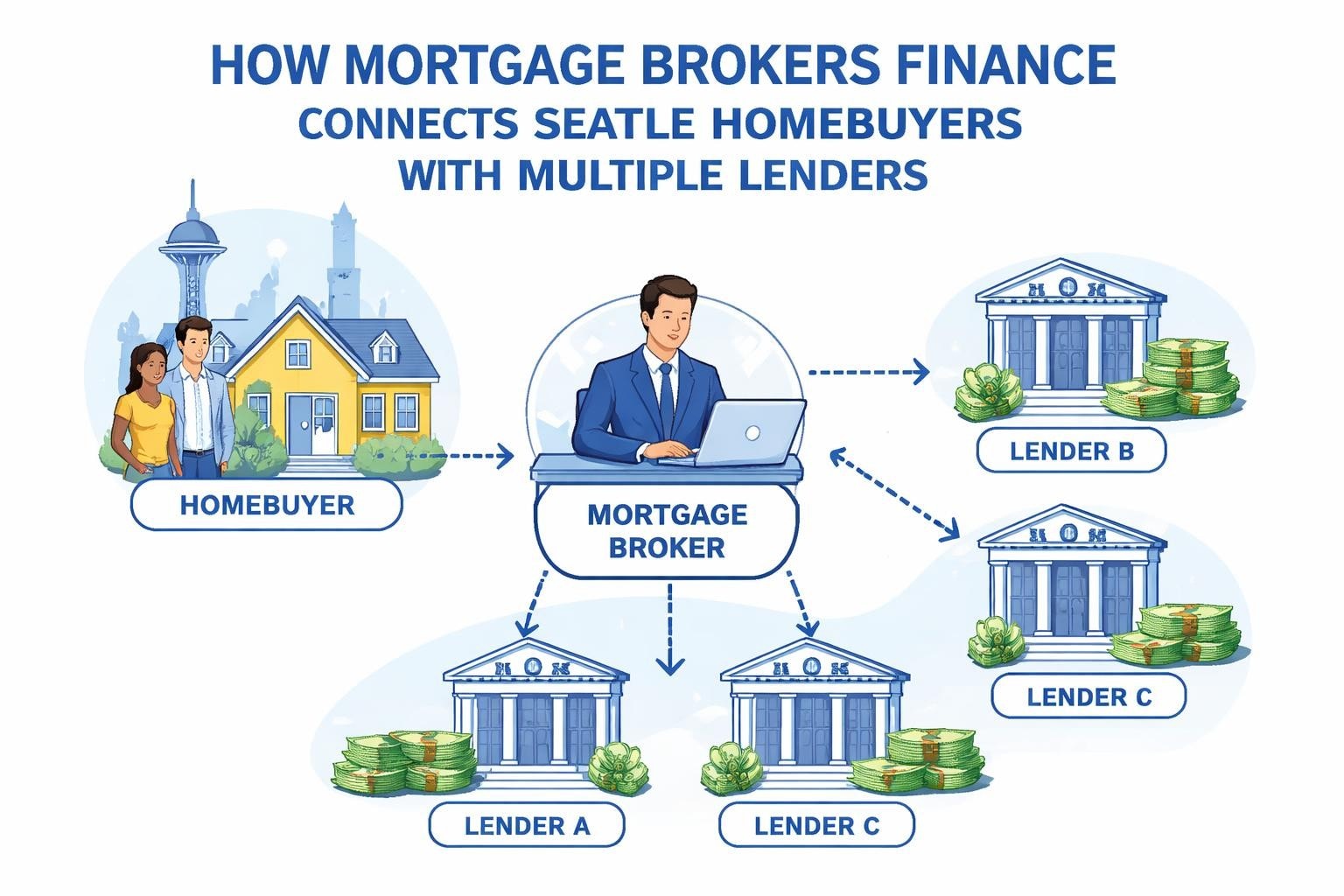

When you work with a Seattle mortgage broker, you're essentially gaining access to a lending network that would otherwise require you to apply separately with each institution. This is particularly valuable in competitive markets like Seattle, Lynnwood, and Lake Forest Park, where timing and execution matter significantly.

How Mortgage Brokers Generate Revenue

Brokers finance their operations through lender-paid compensation and, in some cases, borrower-paid origination fees. The compensation structure is tightly regulated to ensure transparency and prevent conflicts of interest that could harm consumers.

Most wholesale lenders pay brokers a yield spread premium or lender credit when a loan closes. This commission typically ranges from 0.50% to 2.75% of the loan amount, depending on the loan type, rate, and lender policies. Importantly, federal regulations require full disclosure of all compensation on your Loan Estimate, which you receive within three business days of application.

Regulatory Framework Governing Brokers Finance

The mortgage industry operates under extensive federal and state oversight designed to protect consumers and maintain market integrity. Understanding this regulatory framework helps you recognize legitimate professionals from unlicensed operators.

Federal Oversight and Licensing Requirements

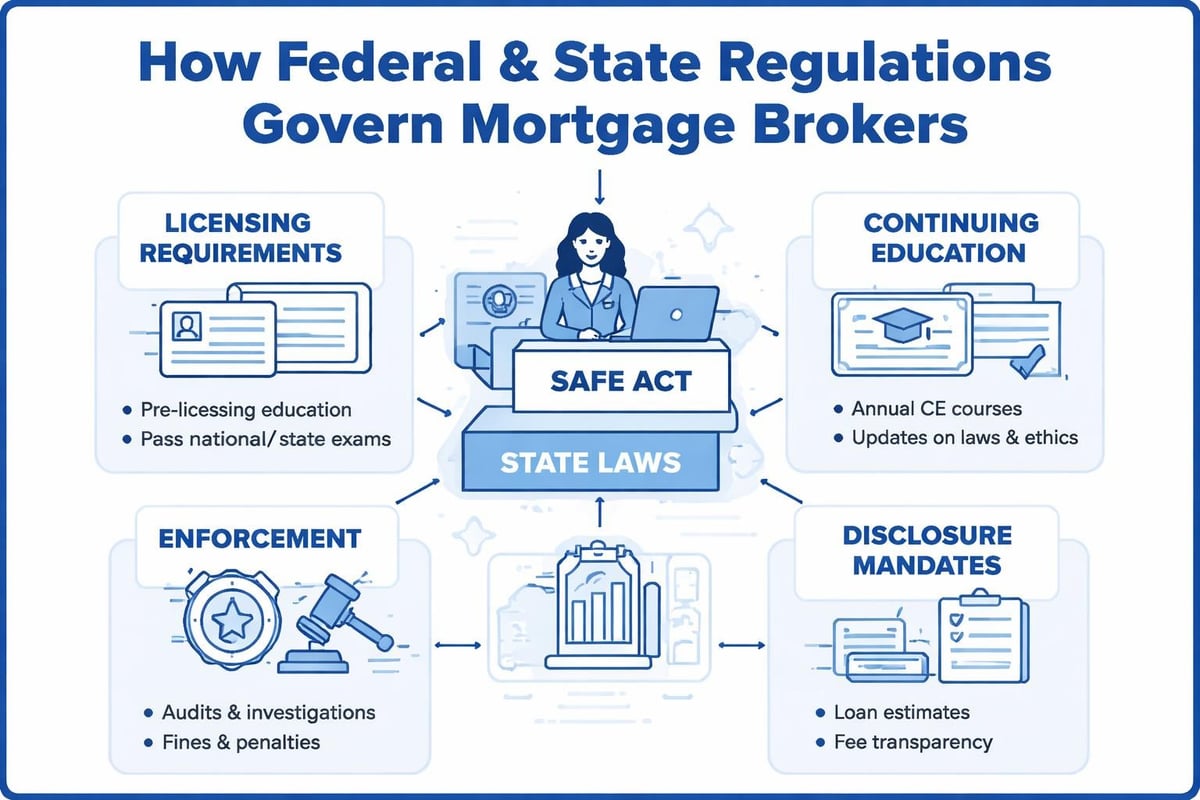

The Secure and Fair Enforcement for Mortgage Licensing Act (SAFE Act) established nationwide standards for mortgage broker licensing. Every mortgage loan originator must:

- Complete 20 hours of pre-licensing education

- Pass the National SAFE MLO Test with a score of 75% or higher

- Submit fingerprints for FBI criminal background checks

- Obtain a unique NMLS (Nationwide Multistate Licensing System) number

- Complete 8 hours of continuing education annually

Washington State enforces additional requirements through the Department of Financial Institutions, including state-specific law courses and minimum net worth standards for brokerage firms. These regulations ensure that brokers finance transactions are handled by qualified professionals who understand lending guidelines, fair lending laws, and ethical obligations.

Restrictions on Business Practices

Brokers finance operations are subject to strict rules regarding borrowing, fee structures, and disclosure requirements. The Federal Reserve Board regulations outline specific restrictions that prevent conflicts of interest and protect consumer interests.

Key regulatory prohibitions include:

- Steering borrowers toward higher-rate loans for increased compensation

- Receiving undisclosed payments from lenders or third parties

- Charging excessive or hidden fees beyond disclosed origination costs

- Misrepresenting loan terms, rates, or approval likelihood

- Conducting business without proper state licensure

For Seattle-area homebuyers, these protections mean you can trust that licensed brokers are legally obligated to present suitable loan options based on your financial profile, not their commission structure.

Advantages of Brokers Finance for Seattle Homebuyers

The competitive Seattle real estate market demands efficiency, speed, and strategic financing. Brokers finance provides distinct benefits that can make the difference between securing your dream home in Everett or losing out to cash buyers.

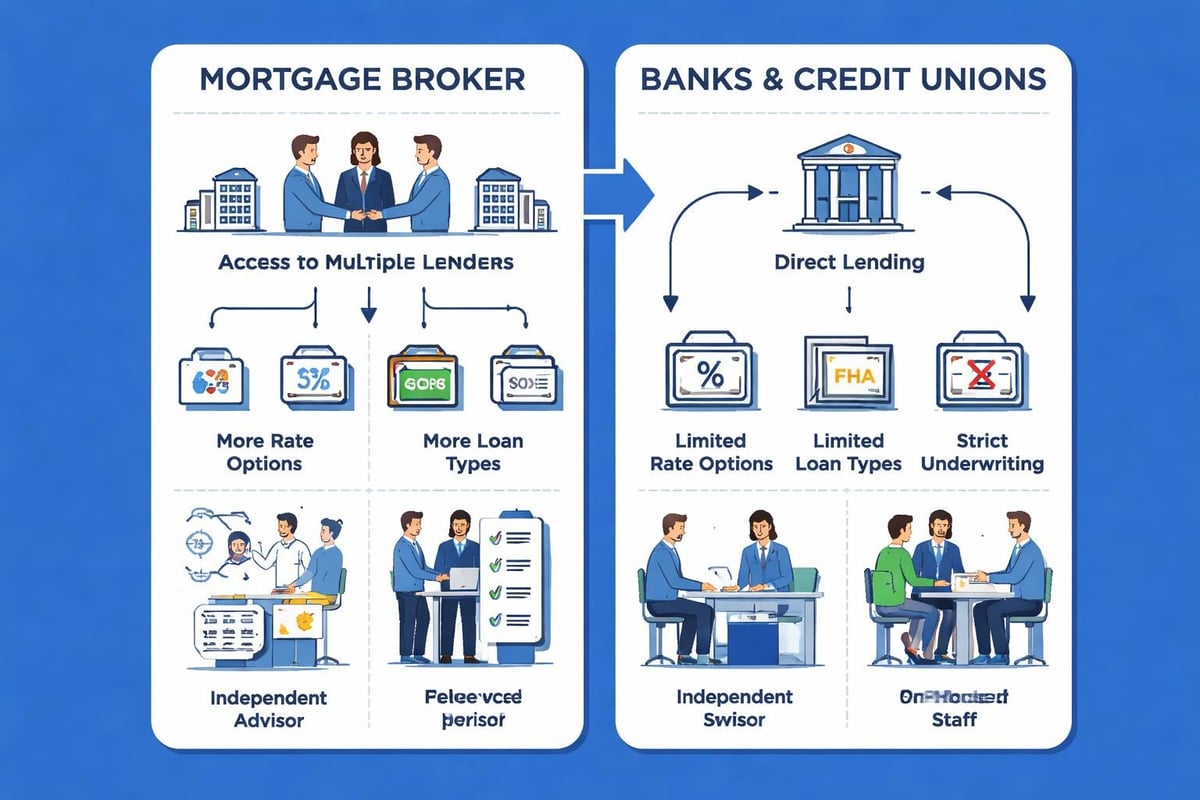

Access to Multiple Lenders and Loan Programs

When you apply through a mortgage broker, your single application gets shopped to numerous lenders simultaneously. This access is particularly valuable for borrowers with unique circumstances that traditional banks might decline.

| Borrower Profile | Traditional Bank Limitation | Broker Solution |

|---|---|---|

| Tech professional with RSU income | May not count unvested equity | Specialized lenders that qualify 50-100% of stock compensation |

| Self-employed consultant | Requires two years tax returns | Bank statement programs using 12-24 months deposits |

| Investment property buyer | Limited to 4-10 financed properties | Portfolio lenders offering programs for unlimited properties |

| Recent credit event | Rigid waiting periods post-bankruptcy | Alternative lenders with reduced seasoning requirements |

For Amazon, Microsoft, or Google employees in Seattle and Redmond, brokers finance expertise in qualifying complex compensation packages can increase purchasing power by $100,000 or more compared to traditional income calculations.

Competitive Rate Shopping Without Multiple Credit Inquiries

One of the most misunderstood aspects of brokers finance is credit impact. When multiple lenders pull your credit within a 45-day window for mortgage purposes, credit scoring models count these as a single inquiry. However, applying separately with three or four banks yourself creates unnecessary complexity.

A broker submits your complete application package to multiple lenders simultaneously, allowing you to compare actual Loan Estimates rather than vague rate quotes. This process typically takes 24-48 hours and provides concrete numbers you can evaluate side-by-side.

Faster Closing Timelines

Experienced brokers finance closings more efficiently because they know each lender's underwriting preferences, documentation requirements, and processing speed. This institutional knowledge prevents common delays that occur when borrowers apply directly.

In the Seattle market, where sellers often receive multiple offers, the ability to close in 15-21 days (or even 9 business days with premium programs) strengthens your offer significantly. Brokers maintain direct relationships with underwriters and processors, enabling them to troubleshoot issues proactively rather than waiting for automated responses.

Industry Trends Shaping Brokers Finance in 2026

The mortgage brokerage industry continues evolving in response to technological innovation, regulatory changes, and shifting consumer preferences. According to recent market research on finance brokers, the sector demonstrates strong growth potential despite economic headwinds.

Technology Integration and Digital Processing

Modern brokers finance operations leverage sophisticated loan origination systems that streamline documentation collection, income verification, and status updates. Borrowers in Shoreline or Lynnwood can upload documents via secure portals, receive automated task reminders, and track their file progress in real-time.

Current technology capabilities include:

- Automated asset verification connecting directly to bank accounts

- Digital income verification through IRS transcripts and payroll systems

- Electronic appraisal alternatives for eligible transactions

- Remote online notarization for purchase and refinance closings

These innovations reduce closing timelines by 3-7 days compared to traditional paper-based processes while improving accuracy and transparency.

State-Level Regulatory Changes

Recent state-level regulations affecting brokers finance emphasize increased transparency and consumer protection. Washington State continues enhancing its oversight through more stringent disclosure requirements and enforcement actions against non-compliant operators.

These regulatory improvements benefit consumers by ensuring that brokers finance transactions adhere to the highest ethical standards. Licensed professionals must now provide more detailed explanations of loan options, compensation structures, and potential conflicts of interest.

Comparing Brokers Finance to Direct Lending Options

Understanding the differences between mortgage brokers and direct lenders helps you make informed decisions about which channel best serves your needs.

Wholesale Versus Retail Rate Structures

Wholesale lenders that work exclusively with brokers often offer better pricing than their retail counterparts because they eliminate branch overhead, advertising costs, and commissioned loan officers. The savings pass directly to borrowers through lower rates or reduced fees.

For example, a Seattle homebuyer financing a $800,000 purchase might see these differences:

| Loan Source | Interest Rate | Monthly Payment | Total Interest (30 years) |

|---|---|---|---|

| National bank retail division | 6.875% | $5,258 | $1,092,800 |

| Wholesale lender through broker | 6.625% | $5,119 | $1,042,840 |

| Difference | -0.250% | -$139/month | -$49,960 |

This quarter-point difference saves nearly $50,000 over the loan term while reducing monthly housing costs by $139.

Loan Program Variety and Specialization

Direct lenders typically offer 5-15 core loan programs designed for mainstream borrowers. Brokers finance arrangements provide access to hundreds of specialized programs including:

- Non-QM loans for self-employed borrowers

- Portfolio products for investment properties

- Construction-to-permanent financing

- Bridge loans for simultaneous purchase-sale transactions

- Foreign national programs for international buyers

For Lake Forest Park buyers with unconventional income sources or Mill Creek investors managing multiple properties, this variety proves essential when traditional banks decline applications.

Evaluating Brokers Finance Professionals in Seattle

Not all mortgage brokers deliver the same level of service, expertise, or results. Selecting the right professional requires evaluating specific credentials and performance indicators.

Essential Qualifications and Experience Markers

When interviewing potential brokers finance partners, verify these fundamental qualifications:

- Active NMLS license with clean disciplinary history

- Minimum 5 years experience in your local market

- Lender network breadth (at least 15-20 active wholesale relationships)

- Specialization alignment with your borrower profile

- Verifiable client reviews across multiple platforms

For first-time homebuyers in Seattle, working with a broker who offers comprehensive education and transparent guidance makes the process significantly less stressful. The first-time homebuyer guide provides detailed information about navigating your first purchase.

Questions to Ask Before Committing

Before submitting an application, ask these critical questions:

- How many wholesale lenders do you currently work with?

- What percentage of your business comes from my borrower profile?

- Will you run my scenario through multiple lenders before selecting one?

- How do you get compensated, and will that appear on my Loan Estimate?

- What's your average closing timeline for purchase transactions?

- Can you provide references from recent clients with similar situations?

Professional brokers finance practitioners welcome these questions and provide clear, detailed answers. Evasiveness or pressure tactics indicate you should continue your search.

Common Misconceptions About Brokers Finance

Several persistent myths about mortgage brokers create unnecessary confusion for Seattle-area homebuyers.

"Brokers Add Extra Costs to Your Loan"

This misconception stems from outdated industry practices that ended with the Dodd-Frank Act reforms in 2010. Modern brokers finance compensation comes primarily from lenders, not borrowers, and total costs often run lower than direct lending channels.

When comparing Loan Estimates, focus on the bottom-line numbers in Section A (total loan costs) and Section J (total closing costs). The source of broker compensation doesn't increase what you pay; it's already factored into the lender's rate sheets.

"Banks Offer Better Rates Than Brokers"

Wholesale lending rates typically beat retail bank pricing because brokers finance operations have lower overhead than branch networks. Additionally, brokers can shop among multiple lenders to find promotional rates or investor appetite for specific loan profiles.

According to industry analysis of loan brokers, mortgage brokers consistently deliver competitive pricing while offering superior service and loan variety compared to direct lenders.

"You Can Only Use Brokers for Complicated Loans"

While brokers finance expertise proves invaluable for complex scenarios, even straightforward purchases benefit from broker involvement. The ability to compare multiple lender options simultaneously ensures you receive optimal pricing regardless of loan complexity.

For Everett buyers with strong credit and standard W-2 income, a broker might identify a credit union offering exceptional rates or a wholesale lender with reduced fees, creating savings that direct applicants never discover.

Strategic Applications of Brokers Finance

Understanding when and how to leverage broker relationships maximizes your financial outcomes across different real estate transactions.

Maximizing Purchasing Power for Tech Professionals

Seattle's concentration of major technology employers creates unique financing opportunities and challenges. Brokers finance specialists who understand equity compensation can structure loans that traditional banks decline.

Stock-based compensation qualifying strategies include:

- Averaging RSU vesting over 12-24 months for income calculation

- Using prior-year equity grants to demonstrate income stability

- Structuring down payments to preserve liquid stock holdings

- Qualifying bonuses and commissions with shorter history requirements

These approaches can increase pre-approval amounts by $150,000-$300,000 for Microsoft, Amazon, or Google employees, particularly when combined with jumbo loan programs designed for high-income borrowers.

Investment Property Financing Strategies

Real estate investors in Seattle and surrounding markets benefit significantly from brokers finance access to portfolio lenders and non-QM programs. Conventional financing through Fannie Mae and Freddie Mac caps investors at 10 financed properties, but portfolio lenders offer unlimited property financing.

Brokers maintain relationships with specialized lenders offering:

- DSCR (Debt Service Coverage Ratio) loans requiring no income verification

- Portfolio loans for properties 11+ with competitive terms

- Cross-collateralization options for leveraging existing equity

- Short-term rental property programs for Airbnb investments

For investors scaling beyond conventional limits, brokers finance expertise becomes essential for continued portfolio growth.

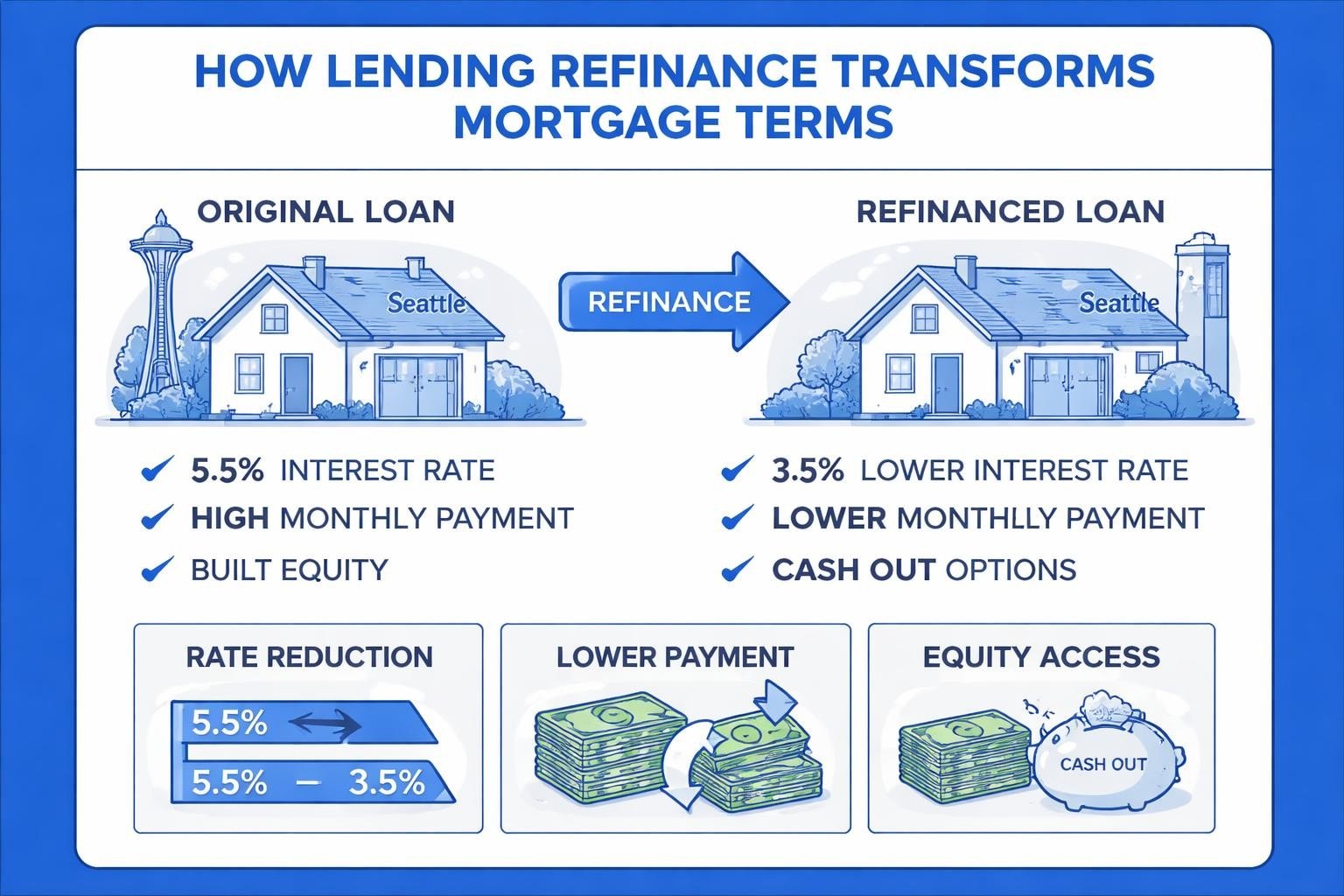

Refinancing Optimization and Rate Monitoring

Effective brokers finance relationships extend beyond the initial purchase. Experienced brokers monitor rate environments and proactively contact clients when refinancing opportunities emerge.

The current refinancing landscape in Seattle shows potential savings for borrowers who financed at rates above 6.50% in 2023-2024. A broker can quickly evaluate whether rate-term refinancing, cash-out refinancing, or equity repositioning makes financial sense based on your long-term goals.

Selecting the Right Broker Finance Partner in Greater Seattle

Your mortgage broker relationship significantly impacts your homeownership journey, from initial pre-approval through long-term portfolio management. Making an informed selection requires evaluating both technical competence and service quality.

Local Market Expertise Matters

Greater Seattle's diverse submarkets have distinct characteristics that influence lending approaches. A broker with deep Shoreline, Lynnwood, and Lake Forest Park experience understands:

- Typical property values and how they affect conforming versus jumbo loan thresholds

- Common title issues in older neighborhoods requiring specialized handling

- Local appraisal markets and typical timelines

- Homeowners association requirements that impact loan eligibility

- New construction processes with builders in emerging developments

This localized knowledge prevents delays and surprises that can jeopardize time-sensitive transactions.

Communication Style and Availability

The best brokers finance transactions through proactive communication and accessibility during business hours, evenings, and weekends. In Seattle's competitive market, delays of even a few hours can mean losing a property to another buyer.

Evaluate communication preferences during initial conversations:

- Response time to emails and calls

- Willingness to explain complex concepts in accessible terms

- Proactive updates versus reactive responses

- Weekend and evening availability during active house hunting

- Use of technology for document sharing and status updates

Your broker should function as a strategic advisor, not just a transaction processor. This partnership approach proves especially valuable for Seattle home financing decisions that impact your long-term financial position.

Track Record and Verifiable Results

Modern technology makes verifying broker performance easier than ever. Beyond online reviews, request specific performance metrics:

- Average days from application to closing

- Percentage of pre-approvals that successfully close

- Denial rate and common reasons

- Client retention and referral percentages

- Lender relationships and pricing competitiveness

Top-performing brokers finance hundreds of transactions annually with denial rates below 5% and closing timelines that consistently beat industry averages. These metrics demonstrate operational excellence and strategic capability.

Future Outlook for Brokers Finance Industry

The mortgage brokerage sector continues adapting to technological innovation, demographic shifts, and regulatory evolution. Understanding these trends helps you work effectively with brokers in 2026 and beyond.

Artificial Intelligence and Automated Underwriting

Machine learning algorithms now handle preliminary underwriting decisions in seconds, analyzing income documentation, credit profiles, and property characteristics faster than human underwriters. Brokers finance operations increasingly leverage these tools to provide instant pre-qualification and accurate approval timelines.

However, artificial intelligence supplements rather than replaces broker expertise. Complex scenarios involving non-traditional income, unique properties, or borrowers with credit events still require professional judgment and strategic lender selection that technology cannot provide.

Demographic Changes Driving Demand

Millennial and Gen Z homebuyers demonstrate different preferences than previous generations, favoring digital communication, transparent pricing, and educational resources. Successful brokers finance their operations around these expectations through enhanced technology platforms and content-driven marketing.

The Greater Seattle market's continuing population growth, driven by technology sector expansion and lifestyle migration, ensures sustained demand for professional mortgage guidance through 2026 and beyond.

Understanding how brokers finance works empowers you to make confident decisions in Seattle's competitive real estate market. Whether you're purchasing your first home in Mill Creek, refinancing in Lynnwood, or building an investment portfolio across Greater Seattle, working with an experienced mortgage broker provides access to better rates, more loan options, and faster execution. Keith Akada at Mortgage Reel brings over 25 years of experience serving Seattle-area homebuyers with transparent guidance, competitive pricing through Fairway's wholesale lender network, and specialized expertise in qualifying complex compensation for tech professionals. With 750+ five-star reviews and the ability to close in as few as 9 business days, we're ready to help you navigate your next purchase or refinance with confidence.