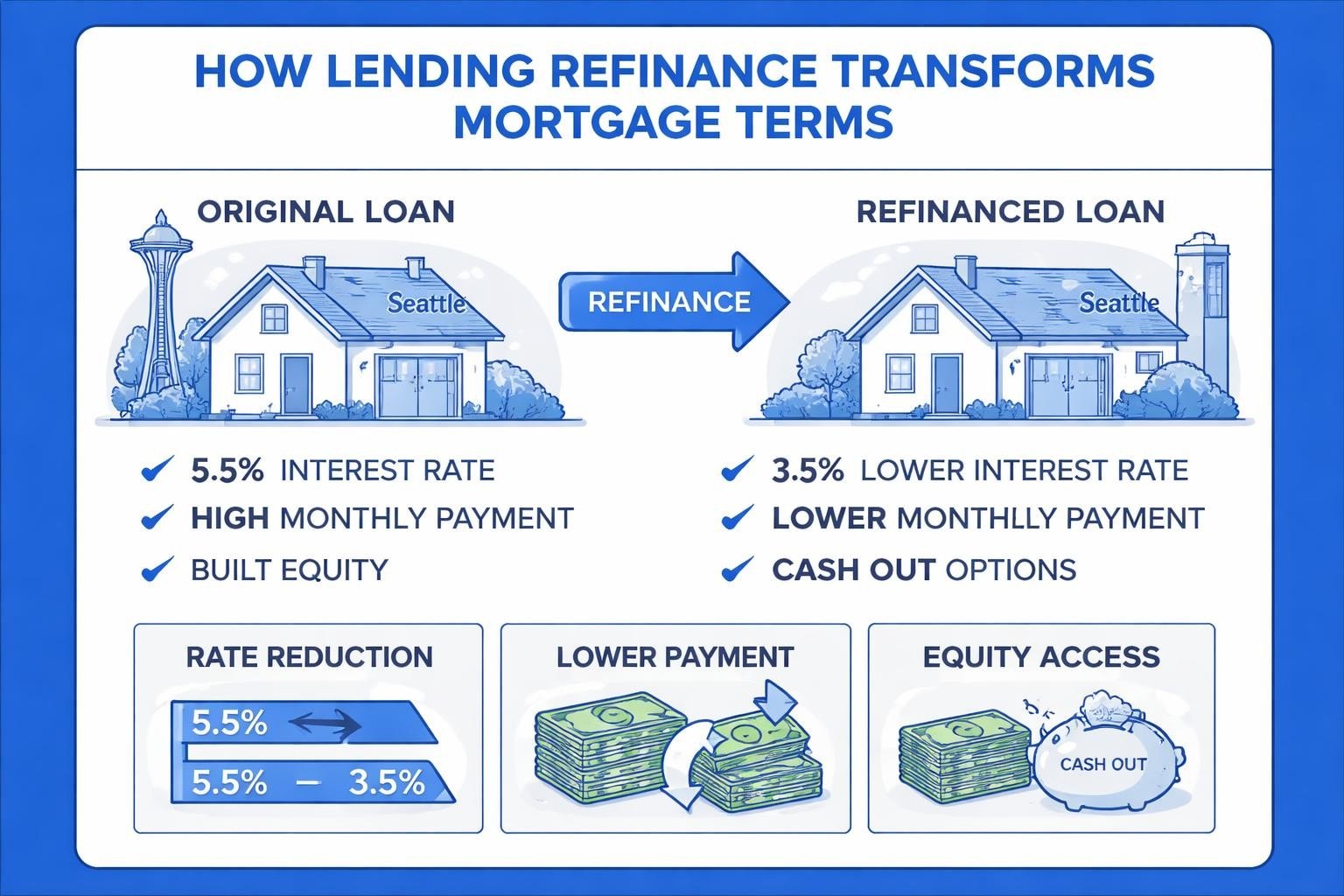

Refinancing your mortgage can be one of the most powerful financial tools available to homeowners in Seattle and surrounding areas. Whether you're looking to reduce your monthly payment, access your home's equity, or shift to a more favorable loan structure, understanding lending refinance is essential to making informed decisions. With interest rates fluctuating and home values continuing to evolve across the Greater Seattle area, now is an opportune time to explore whether a refinance makes sense for your situation. This guide breaks down the fundamentals of lending refinance, helping you navigate the process with confidence and clarity.

What Is Lending Refinance and How Does It Work

Lending refinance is the process of replacing your existing mortgage with a new loan, typically to achieve better terms, lower interest rates, or access equity built up in your home. When you refinance, your new lender pays off your original mortgage, and you begin making payments on the new loan according to its terms.

The refinancing process shares many similarities with your original mortgage application. You'll submit financial documentation, undergo credit checks, and complete a home appraisal to determine current property value. However, because you already own the home, the process often moves faster than a purchase loan.

Types of Refinance Products Available

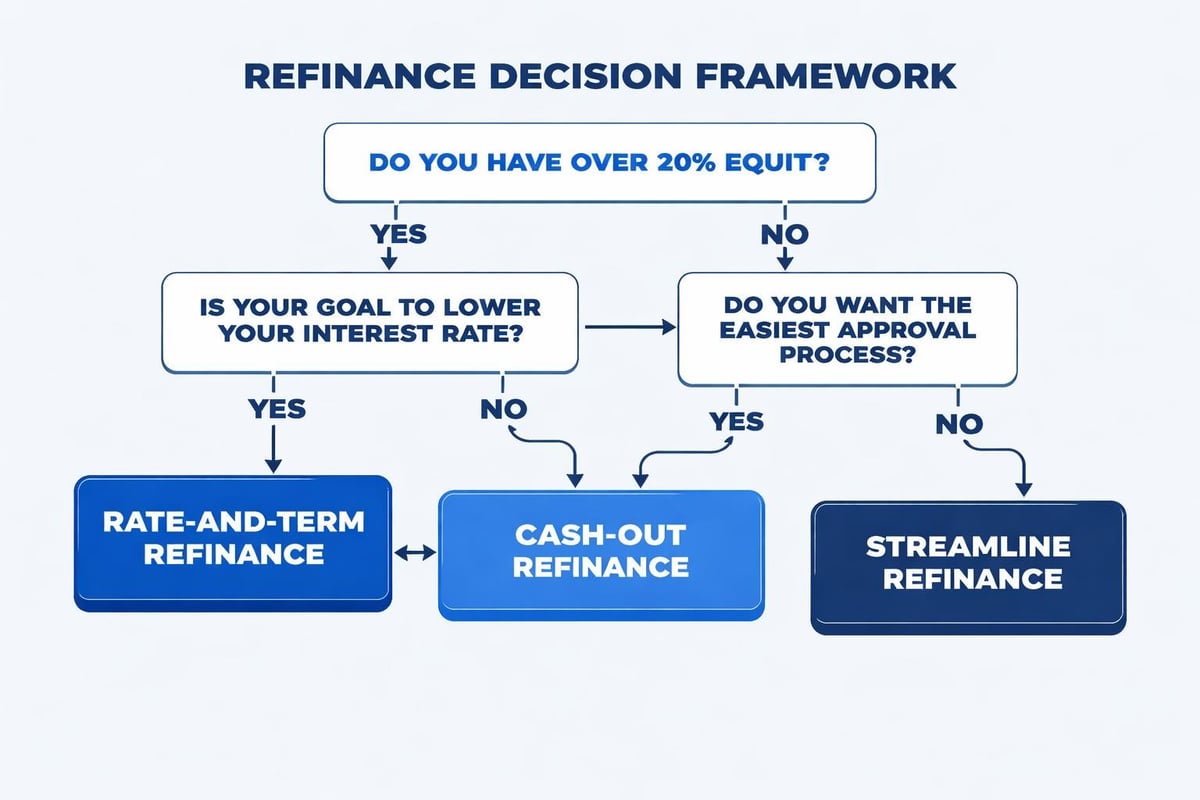

Several lending refinance options exist, each designed to address different financial goals:

- Rate-and-term refinance: Changes your interest rate, loan term, or both without taking cash out

- Cash-out refinance: Allows you to borrow against your home equity and receive the difference in cash

- Cash-in refinance: You bring money to closing to reduce your principal balance and potentially eliminate private mortgage insurance

- Streamline refinance: Simplified process for FHA, VA, or USDA loans with reduced documentation requirements

The right refinance type depends on your current financial situation and long-term objectives. For homeowners in Shoreline or Lynnwood with substantial equity, a cash-out refinance might fund home improvements or debt consolidation. Tech professionals in Seattle working at Amazon or Microsoft might prioritize a rate-and-term refinance to lower monthly obligations while maintaining their current equity position.

When Lending Refinance Makes Financial Sense

Timing plays a critical role in maximizing the benefits of a refinance. Understanding when to refinance requires analyzing multiple factors beyond just current interest rates.

Interest Rate Considerations

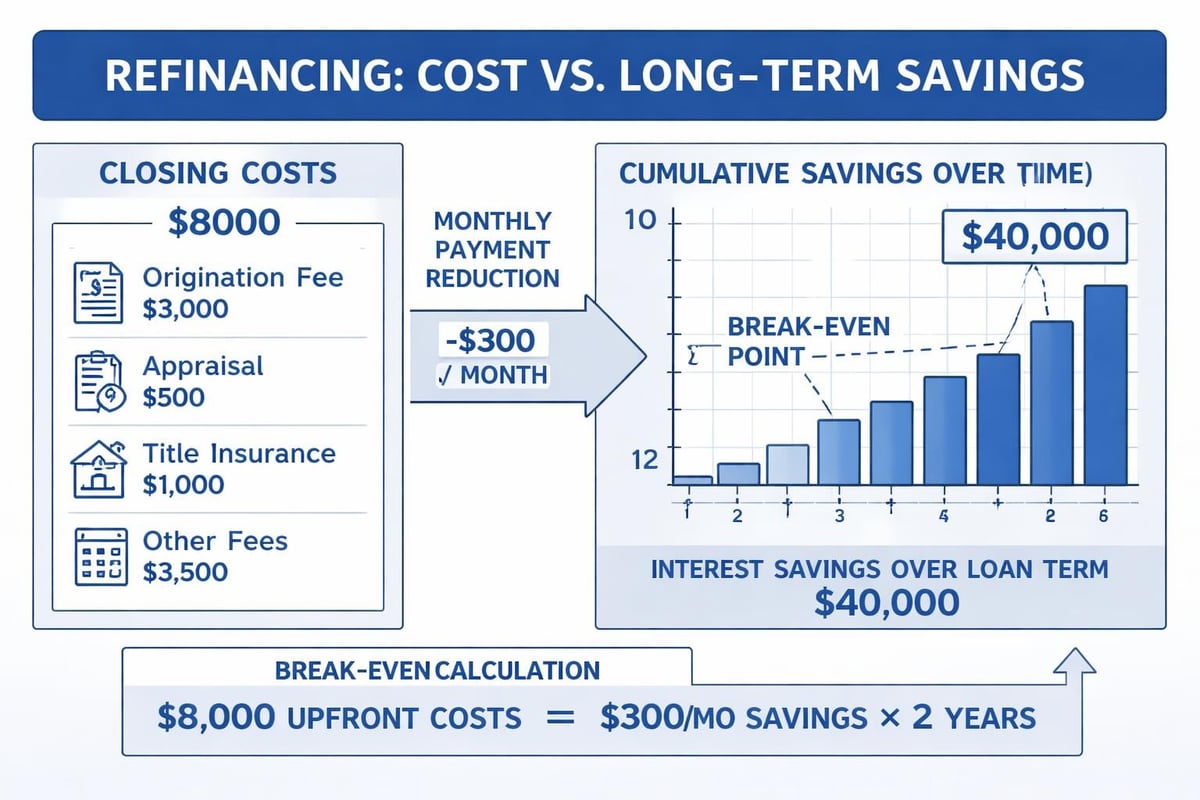

The traditional guideline suggests refinancing when you can reduce your rate by at least 0.75% to 1%. However, this threshold isn't absolute. With today's loan products and closing cost structures, even smaller rate reductions can generate meaningful savings depending on your loan amount and how long you plan to stay in the home.

For a $600,000 mortgage common in the Seattle market, reducing your rate from 6.5% to 5.75% could save approximately $300 monthly. Over a 30-year term, that represents substantial savings, even after accounting for closing costs typically ranging from 2% to 5% of the loan amount.

| Current Rate | New Rate | Monthly Savings* | Break-Even Period** |

|---|---|---|---|

| 7.0% | 6.0% | $370 | 16 months |

| 6.5% | 5.75% | $295 | 20 months |

| 6.0% | 5.5% | $185 | 27 months |

*Based on $500,000 loan amount

**Assuming $5,000 in closing costs

Equity Growth and Home Value Appreciation

Seattle-area home values have experienced significant appreciation over recent years. If your property in Lake Forest Park or Mill Creek has increased substantially in value, refinancing can help you eliminate private mortgage insurance requirements or access equity for strategic purposes.

Reaching 20% equity removes PMI obligations, which typically cost between 0.5% and 1% of the loan amount annually. For a $500,000 loan, that's $2,500 to $5,000 in annual savings. The Fannie Mae refinance guidelines provide detailed information on equity requirements and lending standards.

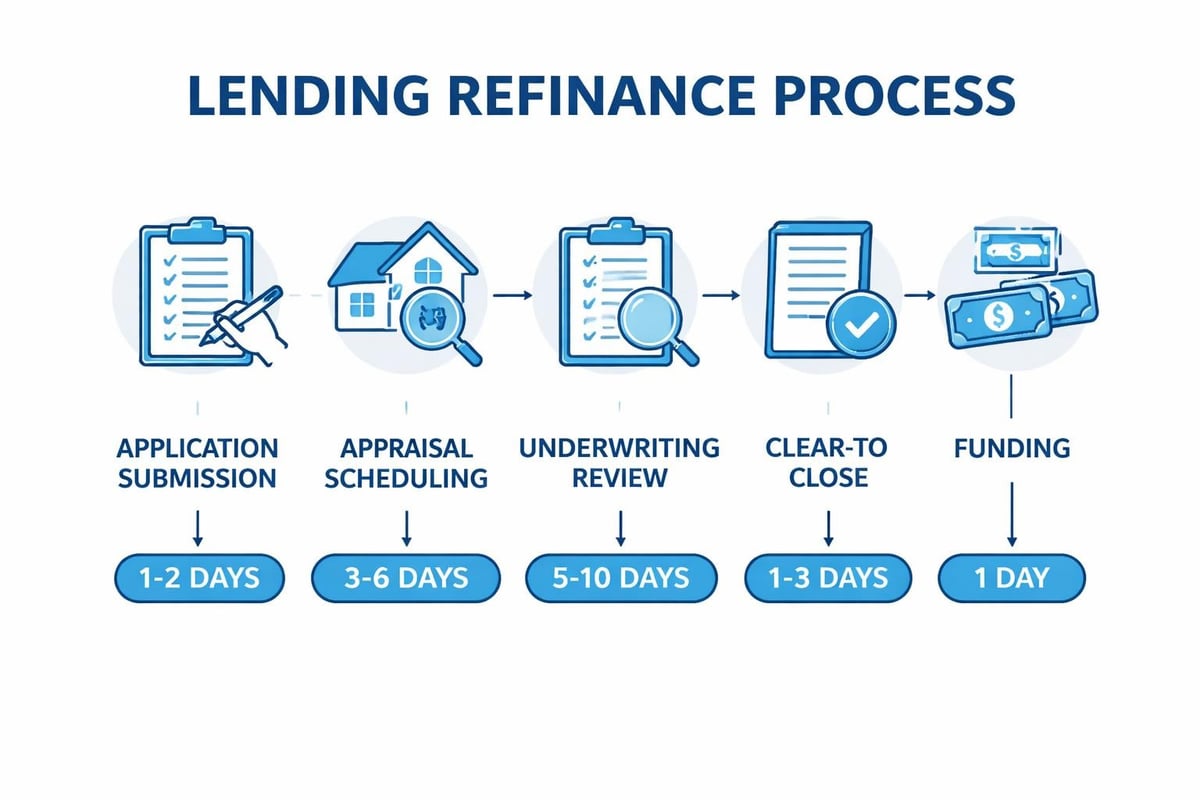

The Lending Refinance Process Step by Step

Understanding the refinance timeline helps you prepare documentation and set realistic expectations. Working with an experienced mortgage broker streamlines this process significantly.

Initial Assessment and Planning

Begin by evaluating your current mortgage terms, remaining balance, and credit profile. Review your most recent mortgage statement and credit report to identify any issues requiring attention before application.

Calculate your break-even point by dividing estimated closing costs by monthly savings. If you plan to move within the break-even period, refinancing may not make financial sense. Homeowners in Everett or other suburban Seattle markets should consider local market conditions and their likelihood of staying in the property long-term.

Documentation and Application

- Gather required financial documents including pay stubs, W-2s, tax returns, and bank statements

- For tech professionals with stock compensation, prepare RSU vesting schedules and equity statements

- Complete the loan application with detailed income and asset information

- Authorize credit checks and employment verification

- Submit any additional documentation requested by your lender

For those working with complex income structures common among Seattle's tech workforce, having a mortgage broker who specializes in qualifying RSUs and bonus income becomes invaluable. These compensation elements require specific documentation and underwriting expertise.

Appraisal and Underwriting

The appraisal determines your home's current market value, which directly impacts your loan-to-value ratio and available refinance options. In competitive Seattle neighborhoods, appraisals generally reflect strong appreciation trends, though specific property conditions and recent comparable sales influence final valuations.

During underwriting, lenders verify all documentation and ensure you meet program guidelines. This stage typically takes 1-3 weeks, though streamlined processes with experienced lenders can reduce this timeframe significantly. Some lenders offer closing timelines as short as 9 business days for well-qualified borrowers with complete documentation.

Strategic Considerations for Seattle Homeowners

Local market dynamics influence refinance decisions. Seattle's unique housing market presents both opportunities and challenges that require tailored strategies.

Jumbo Loan Refinancing

Many Seattle-area homes exceed conforming loan limits, requiring jumbo financing. Jumbo lending refinance typically demands stronger credit profiles, larger down payments or equity positions, and more extensive documentation. However, competitive jumbo rates remain available for qualified borrowers.

Working with lenders who specialize in jumbo products ensures access to the best available terms. For properties in Bellevue or Redmond valued above $1.5 million, specialized jumbo refinance programs offer flexibility unavailable through standard conforming products.

Tax Implications and Deductibility

Understanding the tax treatment of refinancing helps you make fully informed decisions. Mortgage interest remains deductible on loans up to $750,000 for married couples filing jointly, though specific circumstances vary. The Truth in Lending requirements for refinancing govern disclosure obligations and protect borrowers throughout the process.

Cash-out refinance proceeds used for home improvements may offer different tax advantages compared to funds used for other purposes. Consult with tax professionals to understand how your specific refinance scenario impacts your tax situation.

Common Lending Refinance Mistakes to Avoid

Even experienced homeowners can make costly errors during refinancing. Awareness of common pitfalls helps you navigate the process successfully.

Focusing Solely on Interest Rates

While obtaining a lower rate represents a primary refinance goal, other factors deserve equal attention:

- Total closing costs and how they're financed

- Loan term and total interest paid over the life of the loan

- Prepayment penalties on your existing mortgage

- Whether you're restarting the amortization clock on a loan you've been paying for years

A slightly higher rate with lower closing costs might provide better value if you plan to sell or refinance again within a few years. Running detailed scenarios comparing different loan structures reveals the most advantageous option for your situation. Resources like those from NOLA Lending Group offer helpful calculators and tools for comparison.

Neglecting Credit Preparation

Your credit score directly impacts available rates and terms. Small improvements to your credit profile before applying can generate significant savings. Pay down credit card balances to below 30% utilization, avoid opening new credit accounts, and dispute any errors on your credit report.

For borrowers near credit tier thresholds (680, 700, 740, 760, 780), even modest score improvements can unlock substantially better pricing. The difference between a 739 and 740 credit score might save you 0.25% on your interest rate, translating to meaningful monthly savings on larger Seattle-area loan amounts.

Special Programs and Streamline Options

Several refinance programs offer simplified processes with reduced documentation and faster timelines. These specialized lending refinance products benefit eligible homeowners significantly.

Government-Backed Streamline Refinances

If you currently have an FHA, VA, or USDA loan, streamline refinance programs provide expedited processing:

- FHA Streamline: No appraisal or income verification required in many cases, designed to reduce your rate or payment

- VA Interest Rate Reduction Refinance Loan (IRRRL): Minimal documentation for eligible veterans and service members

- USDA Streamline Assist: Simplified refinancing for existing USDA borrowers in eligible rural areas

These programs typically feature lower closing costs and faster approval timelines compared to conventional refinancing. The streamlined nature makes them attractive for homeowners seeking straightforward rate reductions without extensive documentation requirements.

Portfolio and Non-Conforming Options

Some lenders offer portfolio refinance products that don't conform to Fannie Mae or Freddie Mac guidelines. These loans provide flexibility for unique situations such as:

- Properties with non-traditional features or conditions

- Borrowers with complex income documentation

- Debt-to-income ratios exceeding conventional limits

- Recent credit events requiring alternative qualification approaches

Portfolio products typically carry slightly higher rates but offer approval pathways unavailable through standard channels. For self-employed borrowers or real estate investors in Seattle with multiple properties, portfolio refinancing can provide essential flexibility. If you're also considering purchasing additional investment properties, working with professionals who understand both refinancing and purchase transactions-like experienced realtors who specialize in investment properties-can provide comprehensive guidance across your real estate portfolio.

Refinance Costs and Fee Structures

Understanding the complete cost picture ensures you evaluate refinance offers accurately. Lending refinance costs vary by lender, loan amount, and program type.

Typical Closing Cost Components

Refinance closing costs generally include:

- Application and origination fees: Lender charges for processing your loan, typically 0.5% to 1% of loan amount

- Appraisal fee: Property valuation cost, usually $500 to $800 in the Seattle area

- Title insurance and settlement fees: Protects lenders and covers closing services, varying by property value

- Recording fees: Government charges for recording the new mortgage, set by local jurisdictions

- Prepaid items: Property taxes, homeowners insurance, and interest adjustments

Total costs typically range from 2% to 5% of the loan amount. On a $600,000 refinance, expect closing costs between $12,000 and $30,000, though specific amounts vary based on your situation and chosen lender.

No-Closing-Cost Refinance Options

Some lenders offer no-closing-cost refinances where fees are rolled into the loan balance or covered through a slightly higher interest rate. This approach makes sense when you want to preserve cash or plan to sell or refinance again within a few years.

Carefully evaluate whether paying closing costs upfront or accepting a higher rate provides better long-term value. For a homeowner in Kirkland planning to stay in their property for 10+ years, paying costs upfront and securing the lowest possible rate typically proves most economical.

Market Timing and Rate Lock Strategies

Interest rates fluctuate daily based on economic conditions, Federal Reserve policy, and market demand. Strategic rate lock timing can save thousands over your loan term.

Understanding Rate Volatility

Mortgage rates respond to Treasury yields, inflation expectations, employment data, and broader economic indicators. While timing the absolute bottom of the market proves nearly impossible, understanding rate trends helps you make informed decisions.

Monitor rate movements over several weeks before committing. If rates trend downward, waiting might benefit you. Conversely, when rates begin rising from recent lows, locking quickly preserves favorable terms. The research on FinTech lending and refinancing patterns provides insights into market dynamics and borrower behavior.

Rate Lock Periods and Float Options

Standard rate locks range from 30 to 60 days, protecting you from rate increases during processing. Extended lock periods may cost extra but provide security during complex transactions.

Some lenders offer float-down provisions allowing you to capture lower rates if they drop during your lock period. These options typically require specific criteria to be met, such as rates falling by a minimum threshold. Discuss available rate lock strategies with your mortgage broker to determine the best approach for your timeline and risk tolerance.

Refinance Alternatives Worth Considering

Before committing to a full refinance, explore whether other options might better serve your goals.

Loan Modification

If you're experiencing financial hardship, loan modification through your existing lender might provide relief without the costs and effort of refinancing. Modifications can reduce your interest rate, extend your term, or adjust payment structures without creating a new loan.

However, modifications typically require demonstrated financial hardship and may not offer terms as favorable as refinancing in a competitive market. They serve best as solutions for borrowers facing payment difficulties rather than those seeking optimal financial positioning.

Home Equity Lines of Credit (HELOCs)

When your primary goal involves accessing equity rather than reducing your mortgage rate, a HELOC provides an alternative to cash-out refinancing. HELOCs offer revolving credit secured by your home equity, typically with variable interest rates.

HELOCs work well for ongoing expenses like home renovations or college tuition where you need flexibility to draw funds as needed. However, variable rates and smaller credit lines compared to cash-out refinancing limit their utility for large, one-time expenses or when rate certainty matters.

Frequently Asked Questions About Lending Refinance

How Often Can You Refinance Your Mortgage?

No specific limit restricts how frequently you can refinance, though practical considerations apply. Most lenders require at least six months of payment history on your current mortgage before refinancing. Additionally, frequent refinancing rarely makes financial sense due to closing costs and the break-even period required to recoup expenses.

Homeowners in competitive markets like Seattle might refinance every few years when rate environments shift significantly or when equity growth opens new opportunities. The key involves ensuring each refinance delivers clear financial benefits exceeding its costs.

Does Refinancing Hurt Your Credit Score?

Refinancing causes a temporary, modest credit score decrease due to the hard inquiry on your credit report and the new account opening. Typically, scores drop 5-10 points initially but recover within several months as you establish a positive payment history.

The long-term credit impact is generally neutral or positive. Successfully managing a new mortgage demonstrates creditworthiness, and reducing your debt-to-income ratio through lower payments can improve your overall credit profile.

What Credit Score Do You Need to Refinance?

Minimum credit score requirements vary by loan program and lender. Conventional refinances typically require scores of at least 620, though the best rates and terms go to borrowers with scores above 740. FHA streamline refinances may accept scores as low as 580, while VA and USDA programs show flexibility for qualifying veterans and rural homeowners.

For jumbo lending refinance common in Seattle's higher-priced neighborhoods, lenders typically require scores of 700 or higher, with the most competitive programs demanding 740+. Understanding where you stand and how different score levels impact available terms helps you time your application optimally. More information about managing refinance risk can help you prepare effectively.

Should You Refinance If You Plan to Move Soon?

Generally, refinancing makes sense only if you'll stay in the home long enough to recoup closing costs through monthly savings. Calculate your break-even point and compare it to your expected occupancy timeline.

If you plan to sell your Seattle home within two years to relocate to Mill Creek or another area, refinancing probably doesn't make financial sense unless you're eliminating PMI or addressing another urgent concern. However, if you're uncertain about your timeline or plan to convert the property to a rental, the long-term benefits might justify proceeding.

Working With the Right Lending Partner

The lender you choose significantly impacts your refinance experience and outcomes. Differences in rates, fees, service quality, and expertise vary substantially across lenders.

What to Look for in a Refinance Lender

Evaluate potential lenders based on several critical factors:

- Rate competitiveness and fee transparency: Compare complete offers including both rate and closing costs

- Experience with your loan type: Jumbo, portfolio, or specialized programs require specific expertise

- Customer service and communication: Responsive, proactive guidance prevents delays and confusion

- Processing speed and efficiency: Faster closings save you money and provide flexibility

- Reviews and reputation: Verified customer feedback reveals actual service quality

For Seattle homeowners with stock compensation or complex financial profiles, working with a mortgage broker experienced in qualifying non-traditional income proves essential. The ability to navigate underwriting requirements for RSUs, bonuses, and equity awards can mean the difference between approval and denial.

Questions to Ask Before Committing

Before selecting your refinance lender, ask:

- What is your total loan estimate including all fees and costs?

- How long will the process take from application to closing?

- What rate lock options do you offer?

- Do you service loans in-house or sell them after closing?

- What documentation will you need from me, and when?

- How do you handle complications or issues that arise during underwriting?

Clear answers to these questions reveal whether a lender will deliver the experience and results you expect. Don't hesitate to interview multiple lenders before making your decision.

Lending refinance represents a powerful financial tool when executed strategically with clear objectives and thorough analysis. Whether you're reducing your monthly obligations, accessing home equity, or optimizing your loan structure, understanding the process and available options ensures you make confident, informed decisions. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle homeowners navigate refinance decisions with transparency, expertise, and personalized guidance tailored to your unique financial situation.