Navigating Seattle's competitive housing market requires more than just finding the right property. Understanding how to evaluate and select from the mortgage lenders available in the Pacific Northwest directly impacts your purchasing power, closing timeline, and long-term financial success. With housing prices in Seattle, Bellevue, and Redmond remaining elevated throughout 2026, the choice between different lending options has never been more consequential for tech professionals, first-time buyers, and real estate investors alike.

Understanding the Landscape of Mortgage Lenders in 2026

The mortgage lending industry has evolved significantly over the past decade. According to The Motley Fool’s analysis of the largest mortgage providers, non-bank financial institutions now dominate the market, accounting for a substantial portion of mortgage originations. This shift has created a more diverse lending environment with varied service models, technology platforms, and approval processes.

Types of Mortgage Lenders Serving Seattle Homebuyers

When evaluating the mortgage lenders in your market, understanding the fundamental differences between lender types helps you make an informed decision:

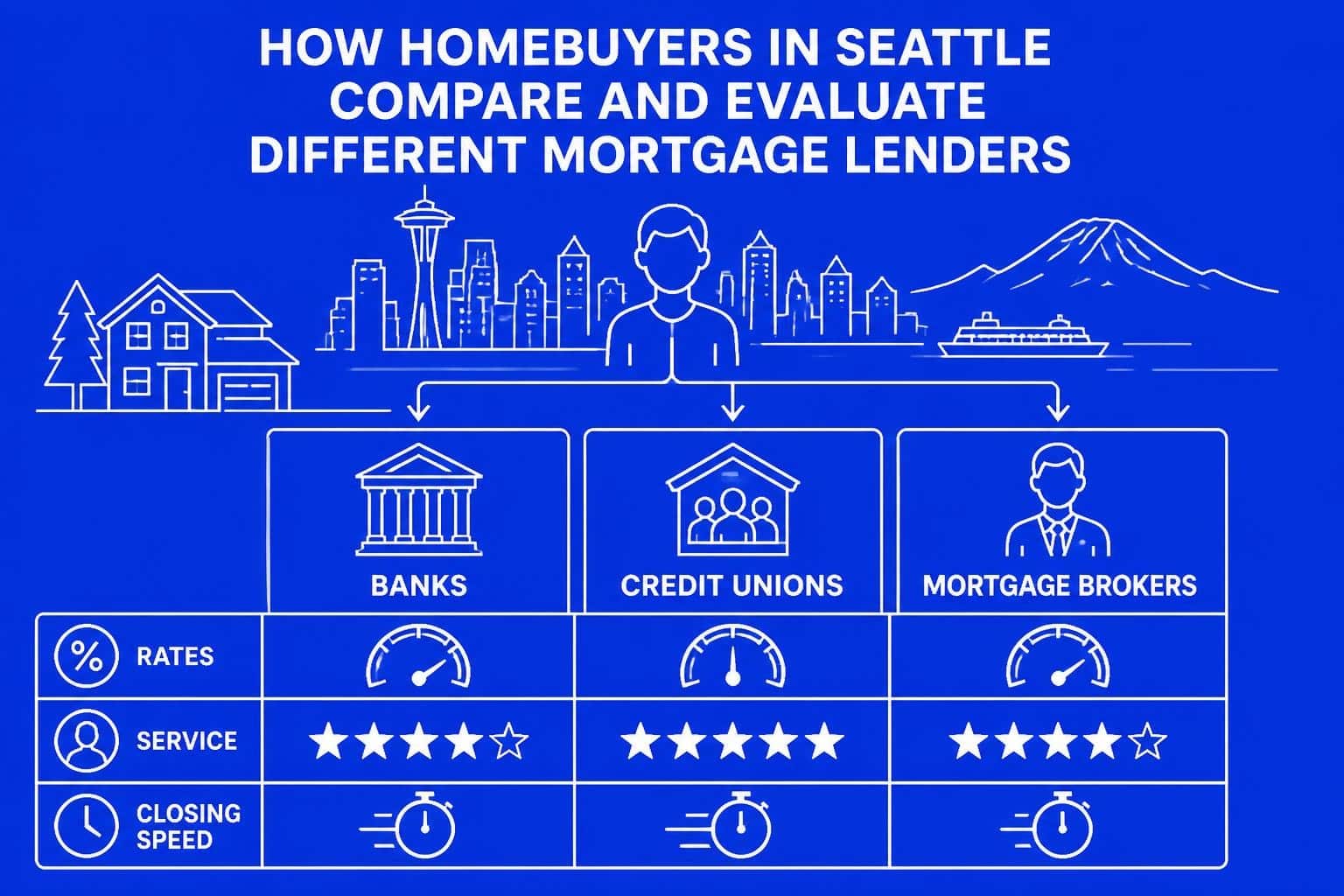

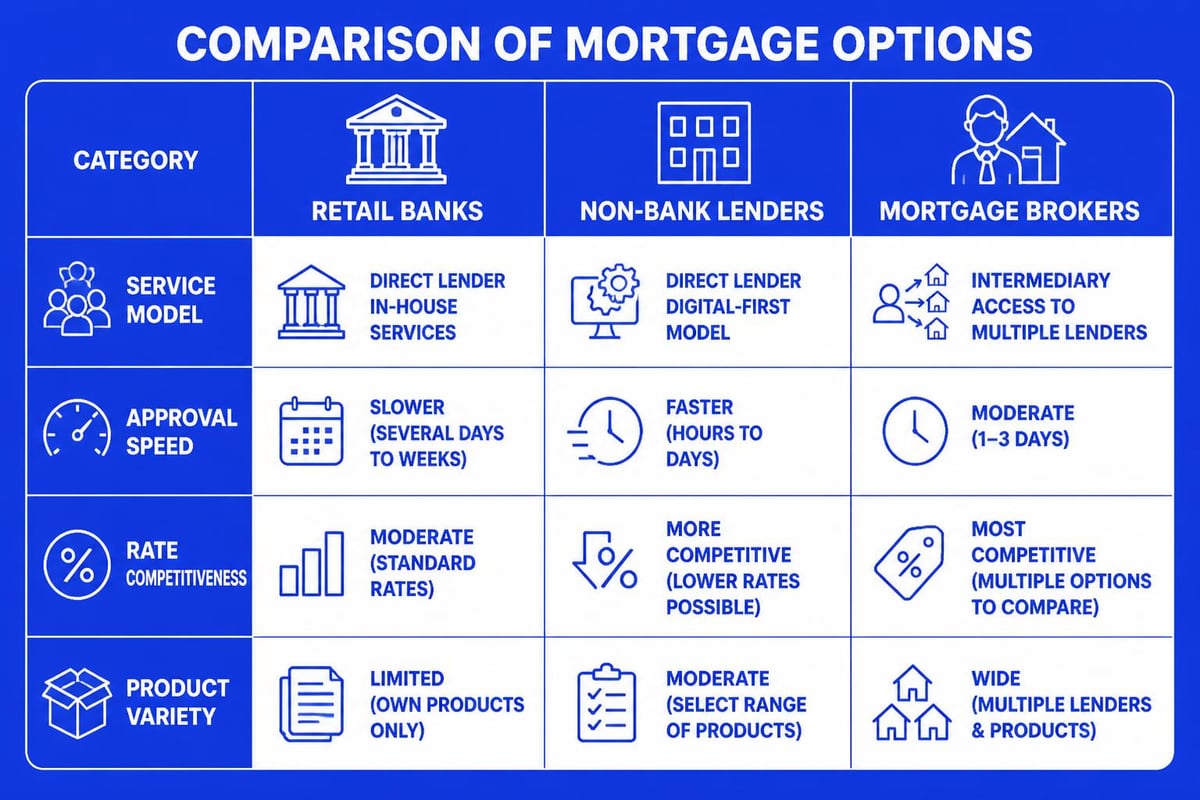

Retail Banks and Credit Unions

- Traditional banking relationships

- Portfolio lending capabilities

- In-person branch access

- Often slower processing times

- Limited product flexibility

Non-Bank Mortgage Companies

- Specialized mortgage focus

- Advanced technology platforms

- Competitive pricing structures

- Streamlined processes

- Diverse loan product offerings

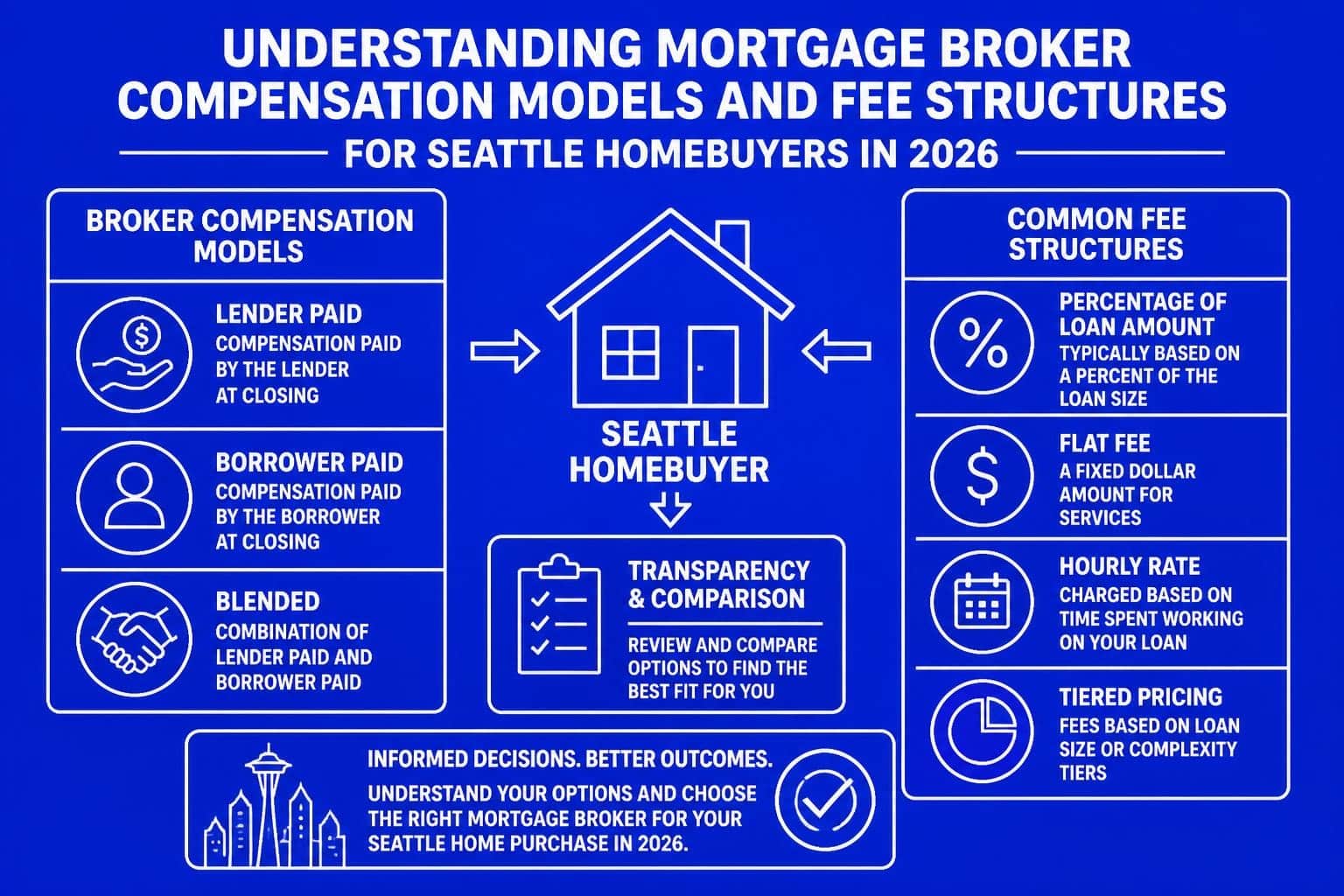

Mortgage Brokers

- Access to multiple lenders

- Competitive rate shopping

- Personalized guidance

- Local market expertise

- Flexible underwriting solutions

For Seattle-area buyers, particularly those working at Amazon, Microsoft, or Google, understanding mortgage broker advantages becomes essential when dealing with complex compensation structures involving RSUs and stock options.

What Distinguishes the Mortgage Lenders in Competitive Markets

The mortgage lenders operating in high-cost areas like Seattle, Shoreline, and Bellevue must navigate unique challenges. Rising interest rates and market volatility, as discussed in HousingWire’s Q2 2026 mortgage earnings outlook, have forced lenders to differentiate through service quality, specialized programs, and technological innovation.

Key Differentiators Among Seattle Lenders

| Factor | Why It Matters | What to Look For |

|---|---|---|

| Closing Speed | Competitive offers require fast execution | 9-21 day capabilities |

| Stock Compensation Expertise | Tech income qualification | RSU and equity handling |

| Jumbo Loan Experience | Seattle median prices exceed conforming limits | Portfolio and agency jumbo options |

| Communication Style | Complex transactions need clarity | Proactive updates, education focus |

| Local Market Knowledge | Neighborhood-specific insights | Experience in your target area |

When you're purchasing in neighborhoods like Capitol Hill, Montlake, or Portage Bay, the mortgage lenders who understand local appraisal challenges, condo warrantability issues, and competitive bidding dynamics provide measurable advantages.

Evaluating Lender Qualifications and Compliance

All mortgage lenders must adhere to strict federal regulations. The FDIC’s mortgage lending compliance requirements ensure consumer protections through the Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA). These regulations standardize disclosure requirements and prohibit predatory practices.

Verification Steps for Borrower Protection

- License verification through NMLS Consumer Access database

- Review history across multiple platforms (Google, Zillow, Yelp)

- Regulatory compliance with TILA and RESPA disclosures

- Company stability and funding capacity

- Technology security for sensitive financial data

The mortgage lenders with established track records and transparent processes reduce risk during your home purchase. In Seattle's fast-moving market, working with properly licensed professionals prevents costly delays and protects your earnest money deposits.

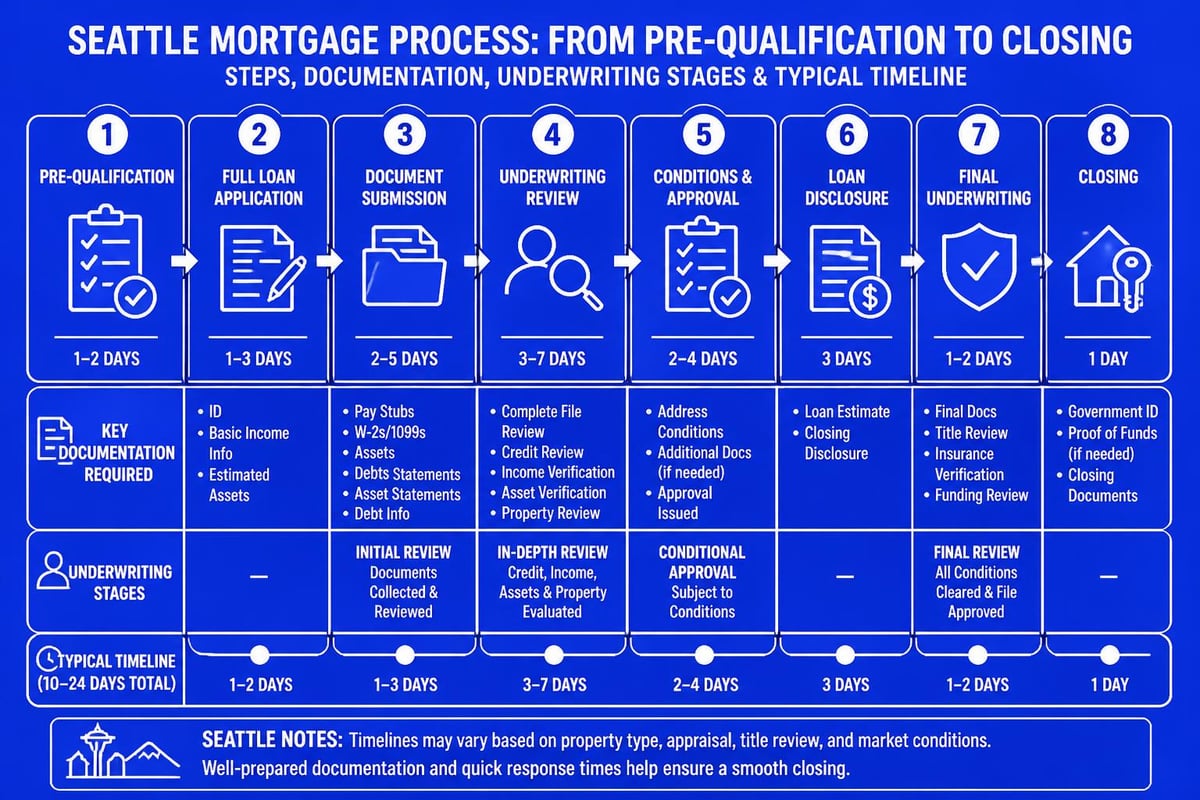

How the Mortgage Lenders Process Your Application

Understanding the application workflow helps you prepare documentation efficiently and set realistic timeline expectations. Kiplinger’s mortgage application process guide outlines standard steps that the mortgage lenders follow from initial application through closing.

The Complete Qualification Journey

Initial Consultation Phase

- Financial assessment and pre-qualification

- Program recommendations based on goals

- Documentation requirements overview

- Rate lock strategy discussion

Formal Application and Processing

- Completed loan application submission

- Credit report and verification ordering

- Property appraisal coordination

- Income and asset documentation review

Underwriting and Approval

- Automated underwriting system evaluation

- Manual underwriting for complex income

- Conditional approval issuance

- Final documentation clearing

Closing Preparation

- Clear to close confirmation

- Final disclosure review

- Funding authorization

- Settlement coordination with title company

For tech professionals in Bellevue and Redmond, qualifying RSU income requires the mortgage lenders to document vesting schedules, continuity of income, and stock value calculations according to specific Fannie Mae and Freddie Mac guidelines.

Selecting from the Mortgage Lenders: Five Critical Factors

Kiplinger’s five-step lender selection process provides a framework for comparison, but Seattle's unique market conditions require additional considerations.

Strategic Selection Criteria for Seattle Buyers

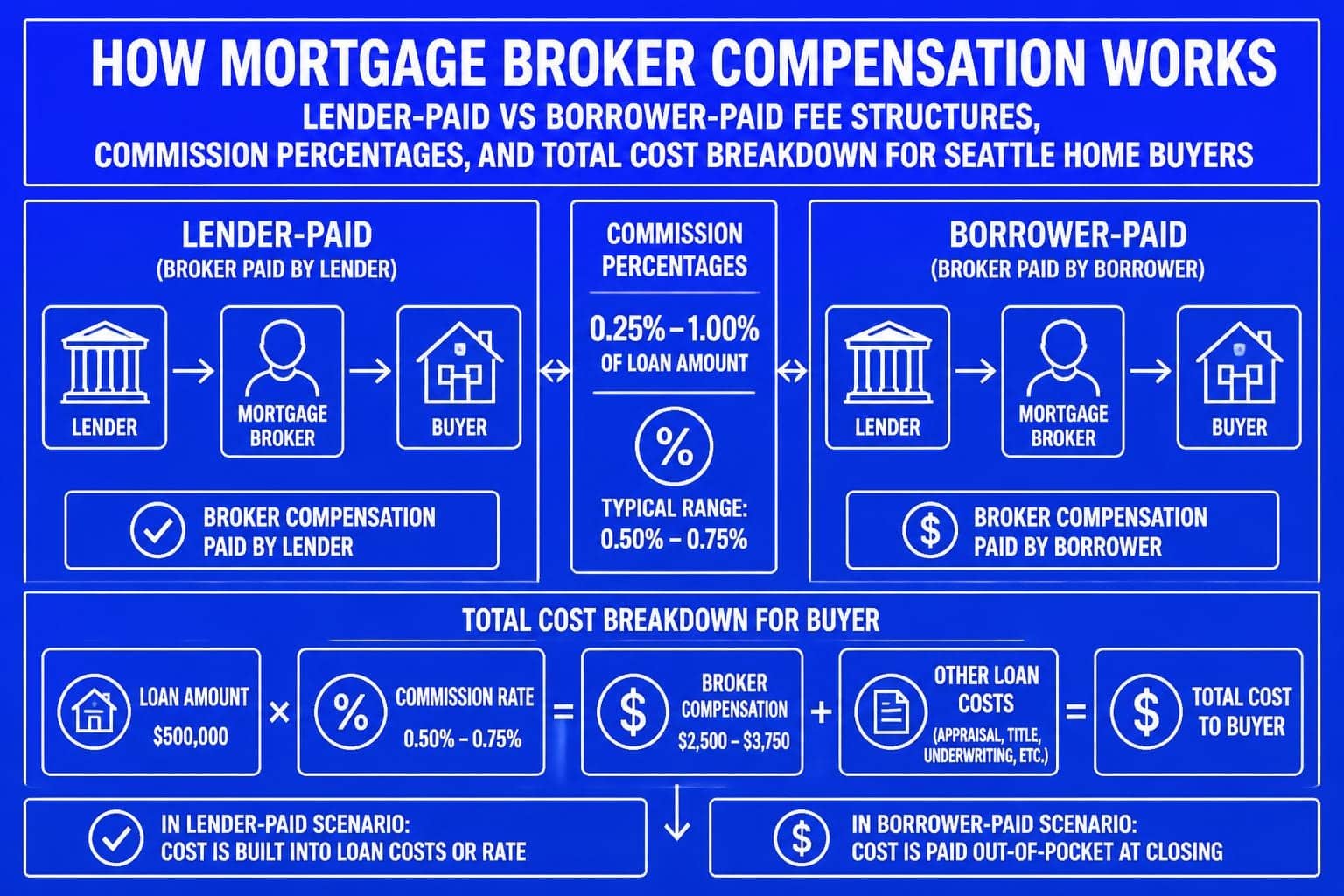

Rate and Fee Transparency

The mortgage lenders should provide itemized fee breakdowns without hidden charges. Request Loan Estimates from multiple sources and compare:

- Base interest rate and APR

- Origination fees and points

- Third-party service costs

- Lender credits or rebates

- Rate lock policies and extension fees

Program Availability and Expertise

Match lender specialization to your situation. First-time buyers in Shoreline benefit from specialized first-time buyer programs, while investors purchasing in Lake Forest Park need access to investment property financing with competitive terms.

- Conventional conforming loans

- Jumbo financing for high-balance properties

- FHA and VA government programs

- Portfolio products for unique situations

- Down payment assistance options

Technology and Communication Systems

Modern platforms enable document upload, milestone tracking, and secure messaging. The mortgage lenders who invest in technology reduce processing time and improve borrower experience through:

- Mobile application capabilities

- Real-time status updates

- Electronic document signing

- Automated verification systems

- Responsive communication channels

Service Model and Accessibility

Determine your preferred interaction style. Some borrowers value face-to-face meetings in Seattle or Kirkland offices, while others prioritize digital convenience. The mortgage lenders with hybrid service models accommodate both preferences without compromising service quality.

Track Record and Reviews

Quantifiable performance metrics reveal operational excellence. Look for:

- Verified customer reviews across platforms

- On-time closing percentages

- Volume and experience levels

- Industry recognition and awards

- Professional credentials and continuing education

Specialized Lending for Seattle's Tech Economy

Seattle's concentration of technology employers creates unique qualification opportunities. The mortgage lenders familiar with stock compensation income qualification can maximize your purchasing power by properly documenting equity compensation.

Tech Income Qualification Framework

Restricted Stock Units (RSUs)

- Two-year vesting history requirement

- Continuity likelihood analysis

- Share value calculation methodology

- Tax impact considerations

Stock Options and ESPP

- Exercise price evaluation

- Vesting schedule documentation

- Market volatility assessments

- Income stability projections

Performance Bonuses

- Historical bonus patterns

- Employer verification letters

- Averaging calculations

- Qualification percentage applications

For professionals relocating to Mill Creek or Everett from other tech hubs, the mortgage lenders experienced with these income types eliminate confusion and expedite approvals. Understanding jumbo loan qualification requirements becomes particularly important when Seattle's median home prices push buyers into jumbo territory.

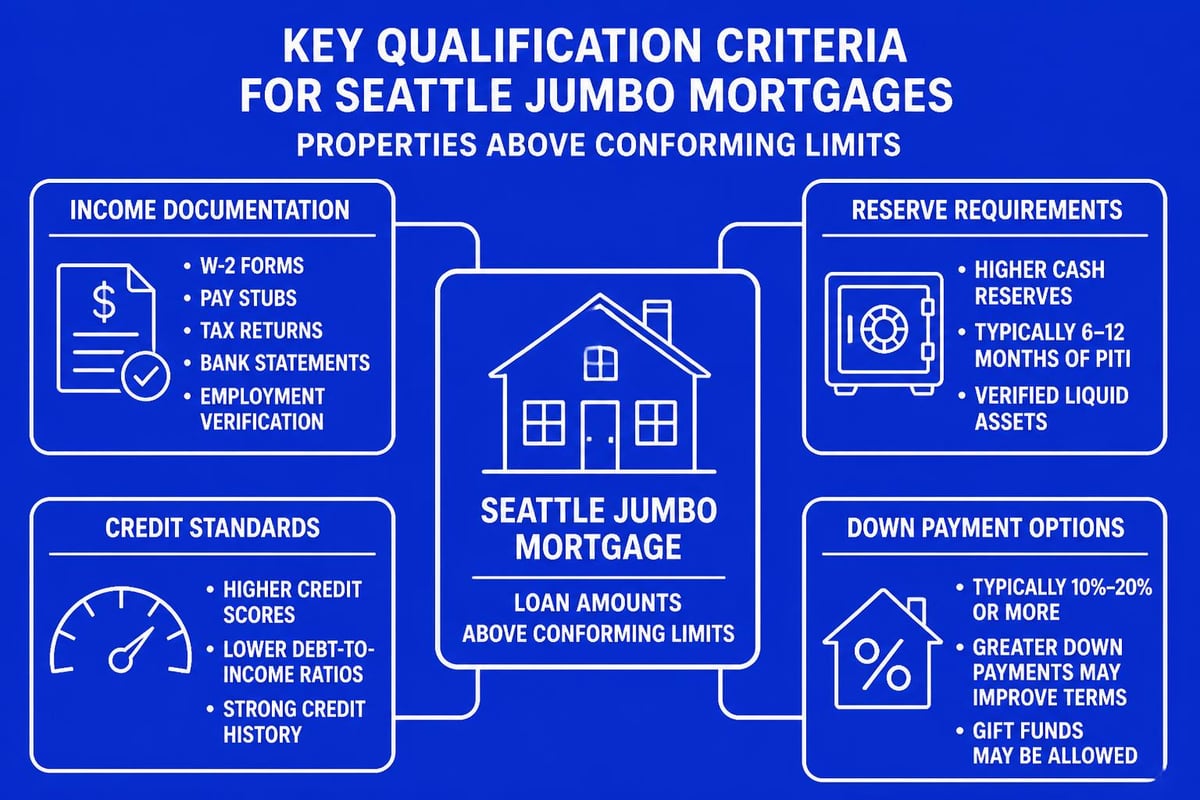

Jumbo Lending Expertise in High-Cost Markets

With conforming loan limits at $806,500 for 2026 in King County, many Seattle-area purchases require jumbo financing. The mortgage lenders offering competitive jumbo programs provide critical advantages in neighborhoods where starter homes exceed $1 million.

Jumbo Loan Comparison Matrix

| Program Feature | Traditional Jumbo | Portfolio Jumbo | Agency High-Balance |

|---|---|---|---|

| Loan Amounts | $806,501+ | $806,501+ | Up to $806,500 |

| Down Payment | 10-20% typical | Flexible options | 5-20% range |

| Credit Requirements | 700+ preferred | 680+ considered | 660+ possible |

| Reserve Requirements | 6-12 months | 3-12 months | 2-6 months |

| Rate Competitiveness | Moderate | Variable | Most competitive |

Understanding jumbo loan down payment strategies helps you balance liquidity preservation with rate optimization. The mortgage lenders who offer 10% down jumbo options without mortgage insurance provide significant flexibility for well-qualified borrowers.

Regional Lending Considerations Across King and Snohomish Counties

The mortgage lenders operating across the Greater Seattle region must understand micro-market differences. Property types, appraisal challenges, and buyer demographics vary significantly between urban Seattle and suburban communities.

Neighborhood-Specific Lending Factors

Urban Seattle (Capitol Hill, Montlake, Pike-Pine)

- Condominium warrantability reviews

- HOA financial health assessments

- Limited parking and storage considerations

- Historic property challenges

- Competitive multiple offer scenarios

Eastside Communities (Bellevue, Redmond, Kirkland)

- Higher price points requiring jumbo expertise

- Tech employee concentration

- New construction opportunities

- Strong appreciation trends

- Excellent school district premiums

North End Suburbs (Shoreline, Lake Forest Park, Mill Creek)

- Diverse property types and price ranges

- First-time buyer program availability

- Family-oriented communities

- Commute accessibility factors

- Shoreline School District appeal

Snohomish County (Lynnwood, Everett)

- More affordable entry points

- Snohomish County specific programs

- Growing employment centers

- Development and appreciation potential

Working with the mortgage lenders who maintain active relationships with appraisers, title companies, and real estate professionals throughout your target area accelerates transaction timelines and reduces complications.

Advanced Strategies: Mortgage Recasting and Refinancing

Beyond initial purchase financing, the mortgage lenders who offer portfolio servicing provide ongoing optimization opportunities. Mortgage recasting represents an underutilized strategy for borrowers receiving windfalls from stock vesting, bonuses, or inheritances.

Recast vs. Refinance Comparison

Mortgage Recasting Benefits

- Minimal processing fees ($200-500 typical)

- Maintains existing interest rate

- No credit check or income verification

- Reduces monthly payment through re-amortization

- Preserves low-rate mortgages from previous years

When Refinancing Makes More Sense

- Current rates significantly lower than existing rate

- Desire to shorten loan term

- Equity extraction needs

- ARM conversion to fixed rate

- Debt consolidation objectives

Understanding why to recast a Seattle mortgage helps homeowners optimize cash flow without the costs and complications of full refinancing. The mortgage lenders who service loans in-house rather than selling them to secondary market investors provide more flexible servicing options.

Addressing Equity and Access in Mortgage Lending

Research documented in academic analysis of HMDA data reveals persistent disparities in mortgage access and pricing across demographic groups. The mortgage lenders committed to fair lending implement policies ensuring equal treatment regardless of race, ethnicity, or other protected characteristics.

Fair Lending Best Practices

- Transparent rate and fee structures

- Consistent underwriting standards

- Diverse product offerings

- Financial education resources

- Alternative credit evaluation methods

- Community partnership programs

Seattle's diverse communities deserve equitable access to homeownership opportunities. The mortgage lenders who prioritize inclusion through expanded documentation acceptance, non-traditional income qualification, and first-time buyer education contribute to more balanced housing markets.

Technology Integration and Processing Speed

Competitive offer scenarios in Seattle, Bellevue, and Redmond demand rapid processing capabilities. The mortgage lenders leveraging automated underwriting systems, digital verification platforms, and integrated workflow management close transactions faster without sacrificing quality.

Processing Timeline Benchmarks

Standard Processing (21-30 days)

- Traditional documentation methods

- Manual verification processes

- Standard appraisal timelines

- Conventional underwriting queues

Accelerated Processing (14-20 days)

- Digital document submission

- Electronic verification systems

- Rush appraisal ordering

- Dedicated processing teams

Expedited Processing (9-13 days)

- Same-day underwriting capability

- Automated valuation acceptance

- Pre-approved documentation packages

- Premium service tier access

When competing in Seattle’s bidding wars, financing contingency periods influence seller selection. The mortgage lenders who consistently close within contracted timelines strengthen offer competitiveness without requiring waived contingencies.

Portfolio Products and Non-QM Solutions

Beyond agency-conforming programs, the mortgage lenders offering portfolio and non-qualified mortgage (non-QM) products serve borrowers with unique situations. Self-employed professionals, real estate investors with multiple properties, and recent credit event recoveries benefit from expanded qualification criteria.

Portfolio Lending Advantages

- Income documentation flexibility

- Higher debt-to-income ratio acceptance

- Recent self-employment consideration

- Multiple financed property allowances

- Unique property type approvals

- Customized underwriting approaches

These specialized products typically carry higher rates reflecting increased lender risk, but they provide access when traditional programs decline applications. The mortgage lenders maintaining active portfolio lending divisions offer solutions unavailable through standard channels.

Local Market Knowledge and Strategic Guidance

Beyond transaction processing, the mortgage lenders who function as trusted advisors provide market insights, timing recommendations, and long-term financial planning guidance. Understanding Seattle mortgage rate trends, neighborhood appreciation patterns, and economic indicators helps buyers make informed decisions.

Strategic Advisory Services

Market Timing Consultation

- Interest rate trend analysis

- Seasonal market pattern recognition

- Economic indicator interpretation

- Rate lock timing recommendations

Financial Planning Integration

- Total cost of homeownership projections

- Tax implication discussions

- Equity building strategies

- Portfolio diversification considerations

Ongoing Relationship Management

- Annual loan review consultations

- Refinance opportunity notifications

- Home equity optimization strategies

- Future purchase pre-planning

The mortgage lenders viewing client relationships as long-term partnerships rather than one-time transactions deliver sustained value throughout your homeownership journey. This approach proves particularly valuable for growing families planning moves within the region or real estate investors building rental portfolios.

Due Diligence: Researching Lender Performance

Before committing to one of the mortgage lenders you're considering, thorough research validates their claims and reveals potential concerns. Multiple verification sources provide comprehensive performance pictures.

Research Methodology

Online Review Platforms

- Google Business reviews for service feedback

- Zillow lender ratings and borrower testimonials

- Yelp experiences and response patterns

- Better Business Bureau complaint history

- NMLS Consumer Access license verification

Professional References

- Real estate agent recommendations

- Title company experiences

- Certified public accountant referrals

- Attorney working relationships

- Past client testimonials

Regulatory Verification

- State licensing confirmation

- Disciplinary action searches

- Complaint history review

- Company stability assessment

- Funding capacity verification

The mortgage lenders with consistently positive feedback across platforms, strong professional networks, and clean regulatory histories minimize transaction risk and enhance confidence throughout your home purchase process.

Preparing for Your Lender Interviews

Approaching initial consultations with the mortgage lenders prepared with questions and documentation accelerates the qualification process and reveals lender capabilities.

Essential Questions to Ask

- What is your average closing timeline for my transaction type?

- How do you handle rate locks and extension scenarios?

- What documentation do you require for my income type?

- Which underwriting system and overlays apply to my situation?

- How do you communicate throughout the process?

- What are your complete fees and third-party cost estimates?

- Do you sell loans or service them in-house?

- What happens if appraisal comes in low?

- How do you handle last-minute complications?

- Can you provide recent client references in my situation?

The mortgage lenders who answer questions directly, explain processes clearly, and set realistic expectations demonstrate the professionalism essential for successful transactions in competitive markets.

Selecting from the mortgage lenders available in Seattle's diverse marketplace requires balancing rate competitiveness with service quality, processing speed, and specialized expertise. Understanding lender types, qualification processes, and strategic options positions you for successful home purchases in one of America's most competitive housing markets. Whether you're a first-time buyer in Lake Forest Park, a tech professional purchasing in Bellevue, or an investor expanding your Seattle portfolio, Keith Akada at Mortgage Reel brings 25+ years of experience, 750+ five-star reviews, and the specialized knowledge to guide you through every aspect of your mortgage journey with transparency, education, and proven results.