Understanding the mortgage broker cost before starting your home financing journey helps you make informed decisions and avoid surprises at closing. For Seattle-area homebuyers-particularly tech professionals at Amazon, Microsoft, and other major employers-knowing what to expect from broker fees creates clarity during an already complex process. While many borrowers assume working with a mortgage broker adds significant expense, the reality often differs substantially from this perception, especially when you factor in the value of expert guidance through competitive markets like Bellevue, Redmond, and Kirkland.

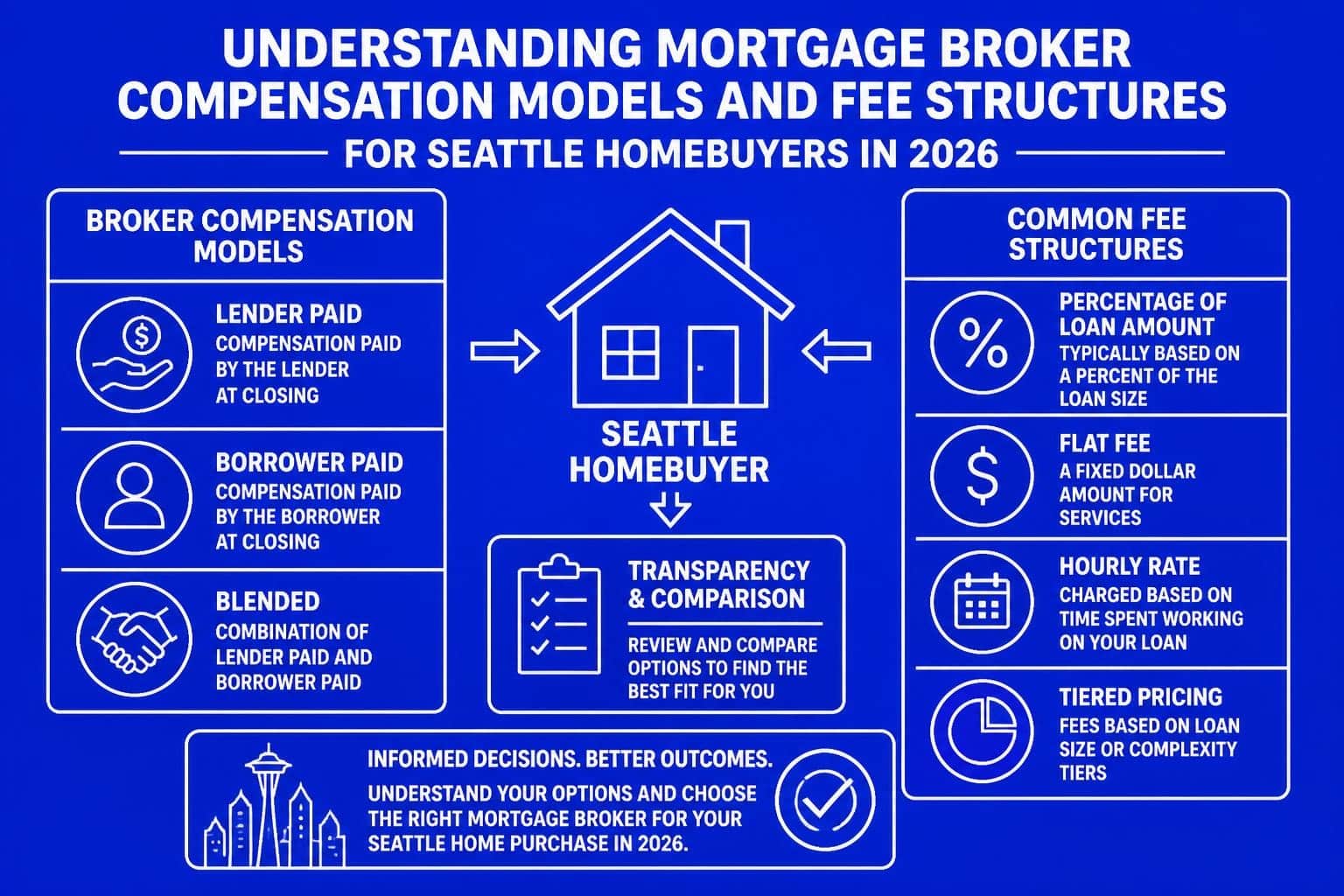

How Mortgage Brokers Earn Compensation

Mortgage brokers operate differently from direct lenders, and their compensation structure reflects this distinction. Rather than earning a salary from a single institution, brokers receive payment through origination fees and commissions tied to the loans they facilitate.

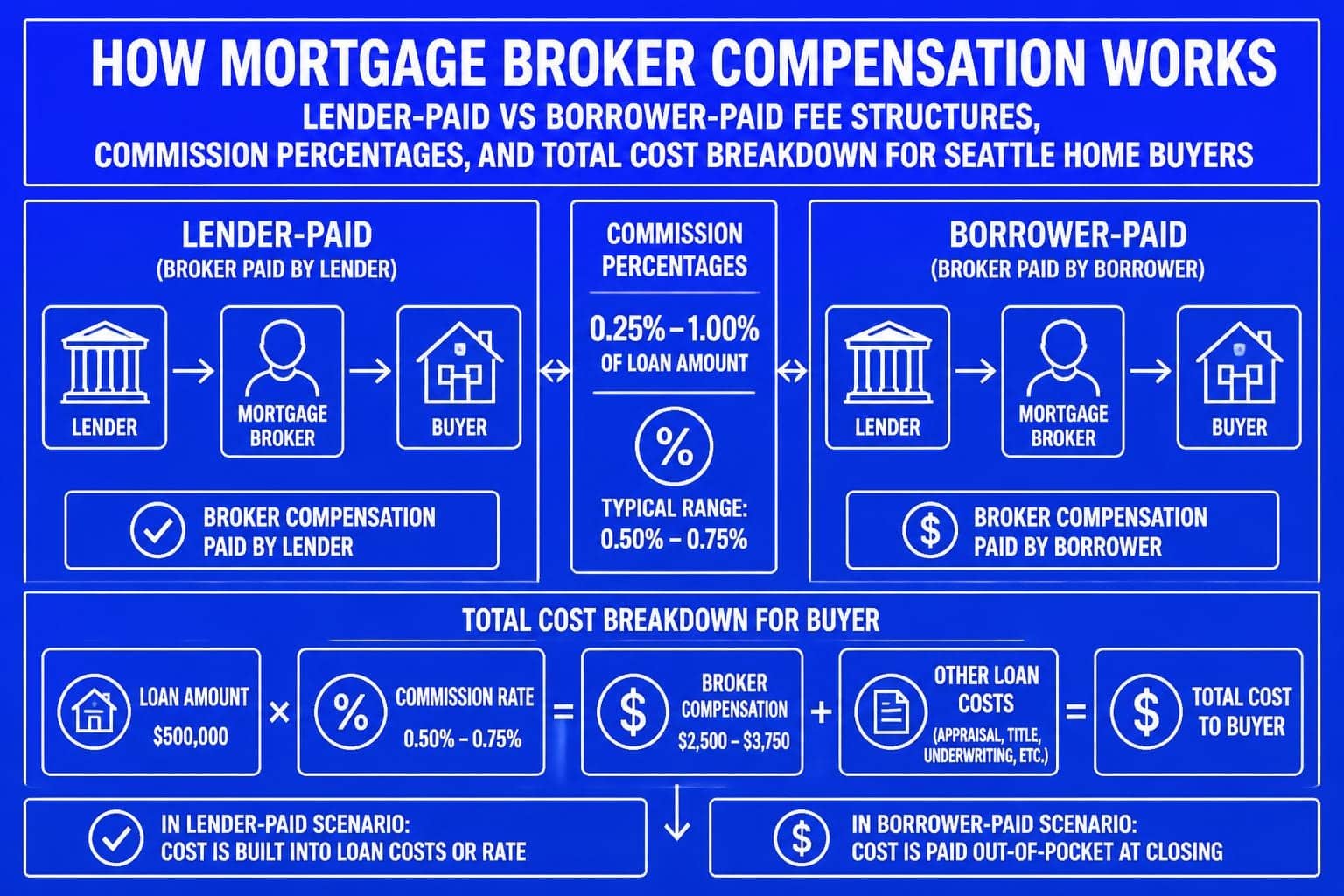

The typical mortgage broker cost ranges between 0.5% and 2.75% of the total loan amount, though most transactions fall within the 1% to 2% range. For a $750,000 home purchase in Seattle-close to the median price point in many neighborhoods-this translates to approximately $7,500 to $15,000 in broker compensation.

Lender-Paid Compensation

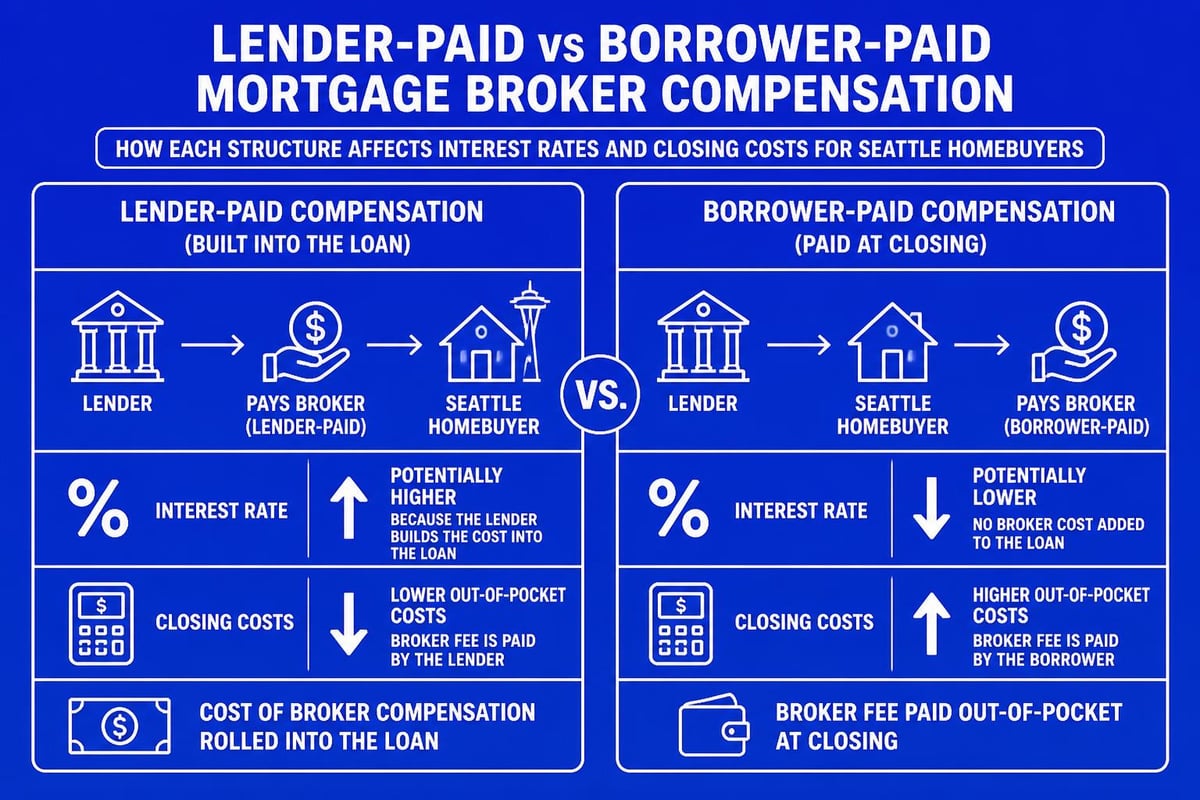

Many borrowers experience no direct out-of-pocket mortgage broker cost because lenders often pay the broker's commission directly. This lender-paid compensation model has become increasingly common since the 2008 financial crisis and subsequent regulatory reforms.

When lenders pay the broker fee, they typically build this cost into the interest rate or loan terms. You won't see a separate line item on your loan estimate for broker compensation, but the cost is incorporated into your overall loan structure. Understanding who pays mortgage broker fees helps you evaluate different loan offers more effectively.

Benefits of lender-paid compensation:

- No upfront cash required for broker services

- Simplified closing cost calculations

- Potentially higher interest rate to offset the lender's expense

- Uniform compensation across different loan products

Borrower-Paid Fees

In some scenarios, particularly with specialized loan products like jumbo home loans, borrowers pay the mortgage broker cost directly. This arrangement often results in lower interest rates since the lender isn't building broker compensation into the rate.

Direct payment to your broker appears as an origination fee on your loan estimate and closing disclosure. This transparency allows you to see exactly what you're paying for professional mortgage services.

Breaking Down Mortgage Broker Cost Components

The total mortgage broker cost encompasses several potential fees, though not all apply to every transaction. Understanding each component helps you evaluate loan estimates and compare offers across different brokers and lenders.

| Fee Type | Typical Range | Who Pays | Purpose |

|---|---|---|---|

| Origination Fee | 0.5% – 1.5% | Borrower or Lender | Processing and underwriting coordination |

| Broker Commission | 1% – 2.75% | Lender | Compensation for loan placement |

| Application Fee | $300 – $500 | Borrower | Credit reports and initial processing |

| Processing Fee | $400 – $800 | Borrower | Document collection and verification |

Origination Fees Explained

The origination fee represents the primary mortgage broker cost for services rendered throughout your loan process. This fee covers the broker's time spent analyzing your financial situation, comparing loan products, negotiating with lenders, and coordinating your application through closing.

In Seattle's competitive market, where closing can happen in as few as 9 business days, experienced brokers invest significant resources in expediting your transaction. The origination fee compensates this intensive work.

Additional Processing Charges

Some brokers charge separate processing or administrative fees beyond the standard origination fee. These charges typically range from $300 to $800 and cover specific operational costs like credit reports, appraisal coordination, and document preparation.

Washington State law requires full disclosure of all broker fees, and federal regulations mandate that these fees appear on your loan estimate within three business days of application. This transparency protects borrowers from unexpected charges and allows for meaningful comparison shopping.

Factors That Influence Mortgage Broker Cost

Several variables affect the total mortgage broker cost you'll encounter. Understanding these factors helps you anticipate expenses and negotiate effectively.

Loan size matters significantly. Larger loans naturally generate higher percentage-based fees. A 1% origination fee on a $500,000 conventional loan equals $5,000, while the same percentage on a $1.2 million jumbo loan totals $12,000.

Loan complexity increases costs. Standard conforming loans for primary residences typically carry lower broker fees than specialized products. Tech professionals using RSU income or stock compensation for qualification often work with brokers who charge premium fees reflecting the additional expertise required to structure these transactions properly.

Geographic location plays a role. Mortgage broker cost in Seattle, Bellevue, and Redmond tends to run higher than in smaller markets like Lynnwood or Mill Creek, reflecting the higher cost of doing business and more competitive housing markets.

Credit Profile Impact

Your credit score and financial strength influence the mortgage broker cost indirectly. Borrowers with excellent credit accessing straightforward loan products generally pay lower fees than those requiring extensive documentation or specialized underwriting.

Strong credit profiles also provide negotiating leverage. When brokers compete for your business in markets like Shoreline or Lake Forest Park, they may reduce fees to secure qualified borrowers.

- Review your credit reports from all three bureaus

- Address any errors or discrepancies before applying

- Understand how your credit score affects available loan products

- Use your strong profile to negotiate better broker terms

Comparing Broker Costs to Direct Lender Fees

Many borrowers wonder whether working directly with a bank or credit union eliminates mortgage-related fees. The reality is more nuanced than simple cost comparison suggests.

Direct lenders charge origination fees comparable to mortgage broker costs, typically ranging from 0.5% to 1.5% of the loan amount. However, direct lenders offer access to only their own loan products, while brokers provide options from multiple lenders.

Value Beyond Cost

The mortgage broker cost discussion must account for value delivered, not just fees charged. Experienced brokers like those serving the Seattle market provide several advantages that offset their compensation:

- Access to wholesale rates often unavailable to retail borrowers

- Expertise in complex income structures critical for tech professionals with RSUs and stock compensation

- Negotiating power with multiple lenders competing for your business

- Time savings through streamlined processes and expert guidance

- Problem-solving ability when unique situations arise

For first-time homebuyers in Seattle, the educational value and hand-holding throughout the process often justifies any incremental mortgage broker cost compared to navigating a direct lender relationship independently.

Regulatory Protections and Fee Limitations

Federal regulations protect borrowers from excessive mortgage broker costs through several mechanisms. The Dodd-Frank Wall Street Reform Act established important safeguards that remain in effect in 2026.

Federal compensation rules for mortgage brokers prohibit certain practices that previously led to inflated fees. Brokers cannot receive compensation based on loan terms other than the principal amount, eliminating incentives to steer borrowers toward higher-rate products.

Key regulatory protections include:

- Prohibition on dual compensation (receiving fees from both borrower and lender)

- Required disclosure of all broker compensation on loan estimates

- Caps on total origination charges in certain loan programs

- Mandatory three-day review period for loan estimates

- Protection against last-minute fee increases

Washington State Requirements

Washington State imposes additional regulations beyond federal requirements. Mortgage brokers must maintain licensing through the Department of Financial Institutions and comply with state-specific disclosure requirements.

These protections ensure that the mortgage broker cost you see on your initial loan estimate remains consistent through closing, barring significant changes to your loan application or property value.

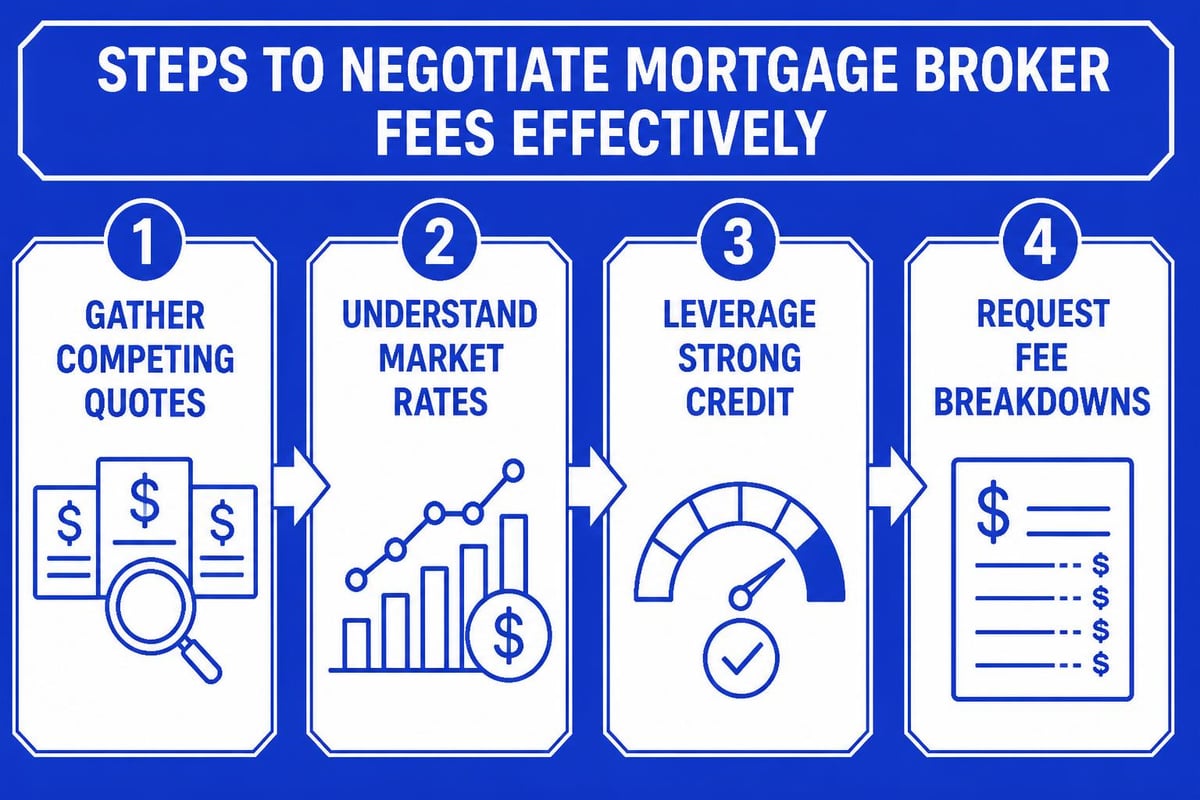

Negotiating Mortgage Broker Fees

While many borrowers accept quoted fees without question, negotiation is often possible, particularly in competitive markets like Everett, Mill Creek, or Shoreline. Your negotiating leverage depends on several factors.

Strong negotiating positions include:

- Excellent credit scores (typically 740+)

- Substantial down payments (20% or more)

- Simple loan structures without complications

- Pre-existing relationships with the broker or referrals

- Multiple competing offers from different brokers

Start negotiations by requesting detailed breakdowns of all fees. Understanding exactly what you're paying for enables targeted discussions about specific charges rather than vague requests for discounts.

What's Negotiable vs. Fixed

Certain costs remain fixed regardless of negotiation, while others offer flexibility. The mortgage broker cost associated with third-party services like appraisals, title insurance, and credit reports cannot be negotiated with your broker since these vendors set their own prices.

However, broker origination fees, processing charges, and administrative fees are typically negotiable. In the Seattle market, where competition among experienced brokers is significant, many professionals offer flexibility on fees to secure your business.

| Fee Category | Negotiable? | Strategy |

|---|---|---|

| Origination Fee | Yes | Compare multiple broker quotes |

| Processing Fee | Sometimes | Request itemized justification |

| Application Fee | Rarely | Often waived for strong borrowers |

| Third-Party Costs | No | Broker has no control over these |

Hidden Value in Broker Services

Focusing exclusively on mortgage broker cost overlooks substantial value that experienced professionals deliver throughout your transaction. This value becomes particularly apparent in complex scenarios common among Seattle-area tech professionals.

Qualifying Complex Income Streams

How brokers structure loans for borrowers with RSU income, stock options, and performance bonuses requires specialized knowledge that most direct lenders lack. The mortgage broker cost for this expertise often proves minimal compared to the increased borrowing power it unlocks.

Brokers familiar with major Seattle employers understand how underwriters evaluate equity compensation differently across companies. They know which documentation strengthens your application and how to present variable income streams in the most favorable light.

Market Access and Rate Shopping

A single mortgage broker provides access to dozens of lenders, effectively conducting rate shopping across multiple institutions simultaneously. This access often results in better terms than borrowers could secure independently, even after accounting for the mortgage broker cost.

In rapidly changing markets, brokers monitor rate movements throughout each day and can lock your rate at optimal times. This timing expertise alone can save thousands of dollars over your loan term.

Cost Comparison Across Loan Types

Different loan products carry varying mortgage broker cost structures. Understanding these variations helps you budget appropriately based on your financing needs.

Conventional Loans

Standard conventional loans typically feature the most competitive broker fees, often ranging from 0.5% to 1.5%. The standardized nature of these products and high volume makes them efficient for brokers to process.

For properties in Seattle neighborhoods like Capitol Hill or Montlake, conventional financing often provides the best combination of rates and fees when working with a broker.

Jumbo Loans

Jumbo financing for properties exceeding conforming loan limits carries higher mortgage broker costs, typically 1% to 2.75%. The additional complexity, documentation requirements, and lender risk justify these increased fees.

Seattle's high property values mean many transactions require jumbo loan expertise, making the broker's specialized knowledge particularly valuable. The cost premium often pays for itself through better rates and terms than borrowers could negotiate independently.

Government-Backed Loans

FHA, VA, and USDA loans feature regulated fee structures that limit total origination charges. The mortgage broker cost for these products typically falls at the lower end of the spectrum, usually under 1%.

These programs serve specific borrower segments, and brokers specializing in government-backed financing often process high volumes that allow for competitive pricing.

When Mortgage Broker Cost Delivers Maximum Value

Certain situations magnify the value delivered relative to mortgage broker cost. Recognizing these scenarios helps you decide whether broker services justify the expense.

High-value broker situations:

- First-time homebuyers navigating unfamiliar processes benefit enormously from expert guidance

- Complex income situations requiring creative underwriting approaches

- Tight timelines where speed and efficiency are critical

- Competitive markets where pre-approval strength determines success

- Credit challenges requiring strategic lender selection

- Refinancing decisions needing break-even analysis and product comparison

For tech professionals relocating to Seattle from other markets, the local expertise provided by experienced brokers proves invaluable in understanding neighborhood nuances, competitive offer strategies, and market timing.

Cost-Benefit Analysis

Calculate whether mortgage broker cost justifies the expense by considering both tangible and intangible benefits. A broker who secures a rate just 0.125% lower than you could obtain independently saves $234 monthly on a $750,000 loan-$2,808 annually and over $84,000 across a 30-year term.

This savings typically far exceeds any origination fee difference between broker and direct lender paths. Add the time saved, stress reduced, and expertise applied, and the value proposition becomes clear for most borrowers.

Transparency and Disclosure Requirements

Modern regulations ensure mortgage broker cost transparency from your first interaction through closing. Understanding required disclosures helps you evaluate offers and identify any irregularities.

Loan Estimate Timeline

Within three business days of your loan application, brokers must provide a standardized loan estimate detailing all costs, including their compensation. This document allows meaningful comparison between different broker offers and direct lender proposals.

The loan estimate breaks down every fee into specific categories, showing which charges the broker controls and which come from third parties. Understanding how brokers make money through these disclosures helps you evaluate the fairness of quoted fees.

Closing Disclosure Review

At least three business days before closing, you'll receive a closing disclosure showing final costs. The mortgage broker cost shown here must align closely with your loan estimate unless specific circumstances changed during processing.

Compare these documents carefully. Significant unexplained increases warrant discussion with your broker before proceeding to closing. Federal law protects you from surprise fee increases except in limited circumstances like property value changes or loan program switches you requested.

Questions to Ask About Mortgage Broker Cost

Informed borrowers ask specific questions about fees before committing to a broker relationship. These inquiries establish transparency and set appropriate expectations.

Essential questions include:

- What is your total origination fee as a percentage and dollar amount?

- Will I pay this fee directly, or does the lender compensate you?

- Are there any additional processing, application, or administrative fees?

- How does your compensation change if I select different loan products?

- Can you provide references from recent clients with similar loan profiles?

- What services are included in your origination fee?

- Do you offer any fee discounts for referrals or repeat clients?

For borrowers in Bellevue or Redmond considering multiple broker options, asking these questions of each candidate enables true apples-to-apples comparison beyond just the quoted mortgage broker cost.

The True Cost of Choosing Wrong

While focusing on mortgage broker cost is natural, the expense of working with the wrong professional-regardless of their fees-often exceeds any savings from choosing the lowest-cost option.

Inexperienced brokers may miss opportunities to strengthen your application, fail to identify optimal loan products for your situation, or lack relationships with underwriters that expedite processing. In competitive Seattle markets, these deficiencies can mean losing your dream home to better-prepared buyers.

The opportunity cost of delayed closings, denied applications, or suboptimal loan terms typically dwarfs the few hundred dollars you might save by selecting a discount broker over an experienced professional charging fair market rates.

Understanding mortgage broker cost empowers you to make confident decisions about your home financing while recognizing the value experienced professionals deliver. Whether you're a first-time buyer navigating Seattle's competitive market or a tech professional leveraging complex compensation for a jumbo loan, transparent fee structures and expert guidance make all the difference. Keith Akada at Mortgage Reel brings 25+ years of experience and over 750 five-star reviews to clients throughout Seattle, Bellevue, Redmond, and Kirkland, delivering clear communication and strategic counsel that consistently exceeds expectations.