Navigating mortgage financing in today's Seattle housing market requires a strategic approach, particularly for tech professionals and first-time buyers facing competitive conditions in neighborhoods across Bellevue, Redmond, and Kirkland. Understanding the fundamentals of mortgage financing-from loan structures to qualification requirements-empowers buyers to make confident decisions whether purchasing a starter home in Lake Forest Park or securing a jumbo loan for a property in Shoreline. This comprehensive guide breaks down the essential elements of mortgage financing and provides actionable insights for maximizing buying power in the Greater Seattle area.

Understanding the Foundation of Mortgage Financing

Mortgage financing represents the process of obtaining capital to purchase real estate through a loan secured by the property itself. The Consumer Financial Protection Bureau provides comprehensive guidance on exploring mortgage options and understanding loan costs, which proves essential for prospective homeowners navigating this complex landscape.

The basic structure involves a borrower, a lender, and the property serving as collateral. When you engage in mortgage financing, you're essentially entering a long-term agreement where the lender provides funds upfront, and you repay that amount plus interest over a predetermined period-typically 15 or 30 years.

Key components of mortgage financing include:

- Principal amount (the actual loan size)

- Interest rate (the cost of borrowing)

- Loan term (repayment timeline)

- Down payment (upfront equity contribution)

- Closing costs (fees for processing and securing the loan)

How Lenders Evaluate Mortgage Applications

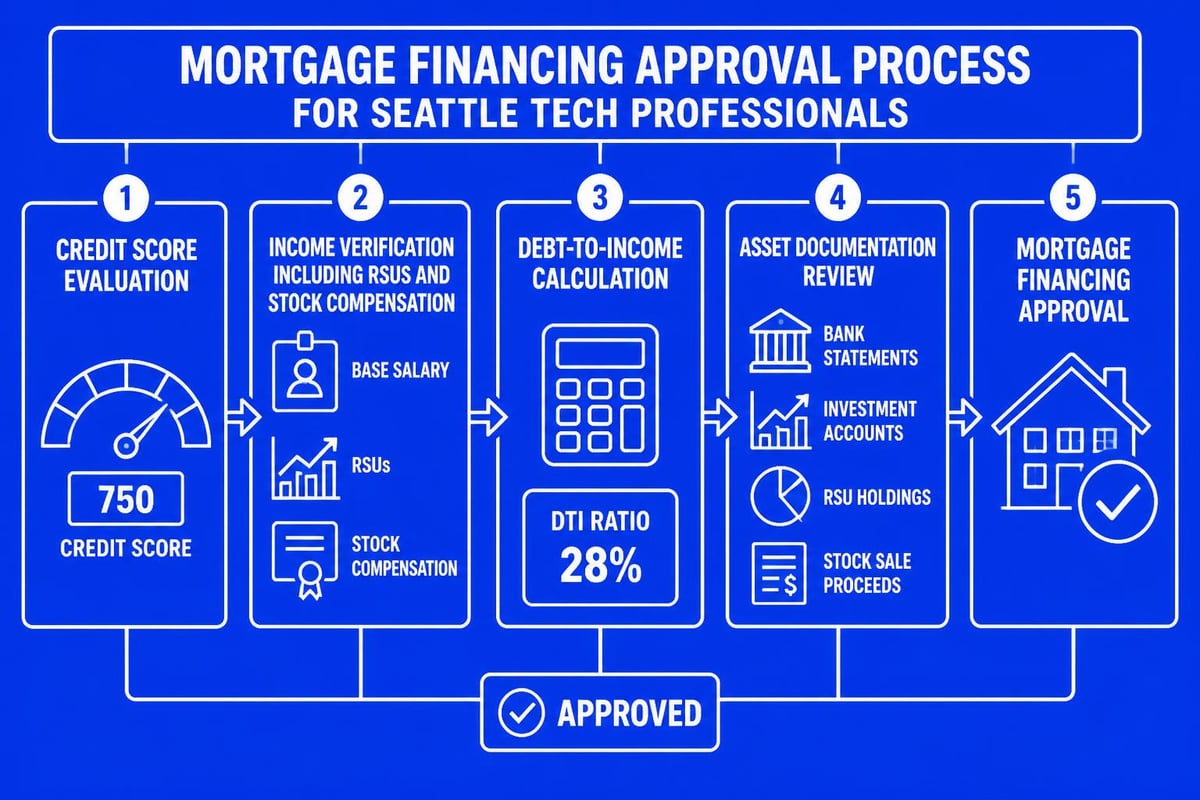

Financial institutions assess mortgage financing applications through a standardized evaluation process focusing on creditworthiness, income stability, and debt-to-income ratios. For Seattle-area tech professionals working at Amazon, Microsoft, or Google, understanding how lenders view stock compensation becomes particularly important.

Lenders examine three primary criteria: credit history, employment verification, and asset documentation. Your credit score directly impacts the interest rate you'll receive, while employment history demonstrates income stability. The debt-to-income (DTI) ratio measures your monthly debt obligations against gross monthly income, with most conventional loans requiring DTI below 43-50%.

Mortgage Financing Options for Seattle Homebuyers

The Pacific Northwest housing market presents unique opportunities and challenges, making the selection of appropriate mortgage financing products crucial for success. A trusted Seattle mortgage broker can guide you through these options based on your specific financial situation.

Conventional Loan Products

Conventional mortgages represent the most common mortgage financing vehicle, offering flexibility for borrowers with strong credit profiles and stable income. These loans come in two varieties: conforming (meeting Fannie Mae and Freddie Mac guidelines) and non-conforming (exceeding standard limits).

For properties in Lynnwood, Mill Creek, or Everett, conventional loan options with 5% down provide accessible entry points for first-time buyers. However, putting down less than 20% requires private mortgage insurance (PMI), which adds to monthly costs until you reach 20% equity.

| Loan Type | Minimum Down Payment | PMI Requirement | Best For |

|---|---|---|---|

| Conventional | 3-5% | Yes (if <20% down) | Strong credit borrowers |

| FHA | 3.5% | Yes (lifetime) | Lower credit scores |

| VA | 0% | No | Military veterans |

| Jumbo | 10-20% | No | High-value properties |

Government-Backed Financing Solutions

Government-backed mortgage financing programs offer advantageous terms for qualified borrowers. FHA home loans accommodate lower credit scores and smaller down payments, making homeownership accessible for buyers still building credit history.

VA loans provide exceptional benefits for military service members and veterans, including zero down payment requirements and no PMI. For eligible borrowers purchasing in Seattle neighborhoods, these terms translate to significant monthly savings and reduced upfront costs.

Jumbo Loan Financing Strategies

Seattle's robust housing market frequently requires jumbo mortgage financing, particularly in premium neighborhoods throughout the metro area. These loans exceed conforming loan limits ($806,500 for single-family homes in King County for 2026) and demand more stringent qualification standards.

For tech professionals with substantial equity compensation, jumbo home loans unlock purchasing power in competitive markets. Lenders typically require excellent credit (720+), lower DTI ratios (36-43%), and larger reserves-often 12 months of payments in liquid assets.

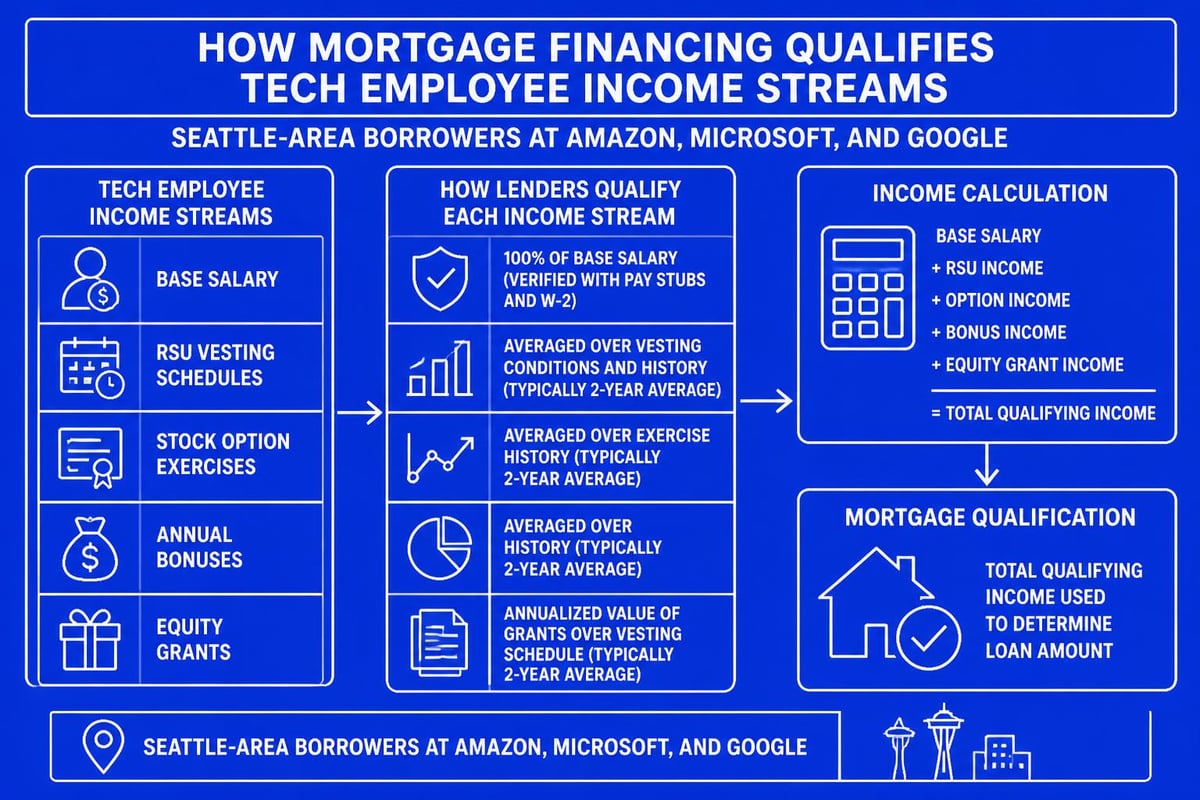

Qualifying Complex Income for Mortgage Financing

Tech sector employees face unique challenges when qualifying income for mortgage financing. Traditional W-2 salary represents just one component of total compensation, with RSUs, stock options, bonus structures, and equity grants comprising significant portions of annual earnings.

Understanding how underwriters evaluate these income sources proves essential for maximizing borrowing capacity. Most lenders require a two-year history of receiving variable income before including it in qualification calculations, though experienced brokers can sometimes work with shorter timeframes when documentation strongly supports stability.

Documentation requirements for complex income include:

- Two years of personal tax returns with all schedules

- Two years of W-2 statements

- Recent pay stubs showing year-to-date earnings

- Vesting schedules for RSUs and stock options

- Award letters documenting equity compensation

- Bank statements showing stock sales and deposits

Working with Stock Compensation

RSUs and stock options require careful handling in mortgage financing applications. Underwriters distinguish between vested and unvested shares, typically only considering vested amounts or applying conservative vesting schedules to future grants. For professionals working with tools like Bank Statement Boss to organize their financial documentation, having clean, well-categorized records of stock sales and transactions can streamline the qualification process significantly.

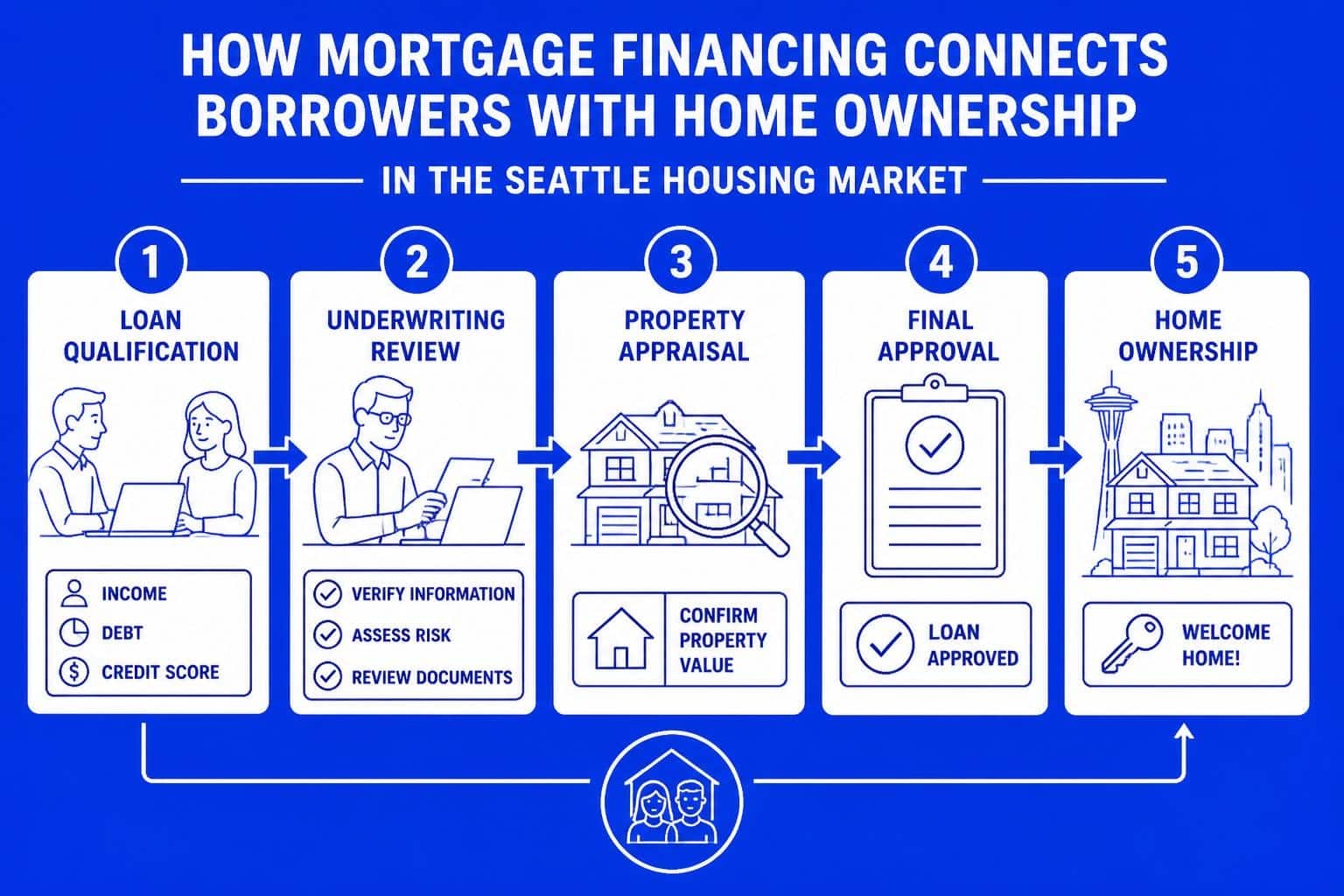

The Mortgage Financing Timeline and Process

Successful mortgage financing requires understanding the typical timeline from application through closing. While some lenders advertise closings in as few as 9 business days with streamlined underwriting, most transactions take 30-45 days from accepted offer to funding.

Initial Application and Pre-Approval

The process begins with pre-approval, where lenders review your financial profile and issue a conditional commitment. This critical step provides negotiating power in competitive Seattle markets, demonstrating to sellers that you're a serious, qualified buyer. Understanding home loan approval time helps you set realistic expectations and plan accordingly.

Pre-approval differs from pre-qualification. Pre-qualification represents an informal estimate based on self-reported information, while pre-approval involves verification of credit, income, and assets. Sellers and listing agents strongly prefer pre-approved buyers, particularly in multiple-offer situations common throughout Shoreline, Lake Forest Park, and surrounding communities.

Underwriting and Conditional Approval

Once you've identified a property and entered contract, your file moves to underwriting where detailed verification occurs. The underwriter examines every aspect of your mortgage financing application, requesting additional documentation to confirm the information provided.

The FDIC provides comprehensive information on mortgage lending regulations that lenders must follow during this stage, including Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) compliance, ensuring borrower protection throughout the process.

Underwriters issue conditions-specific documentation requests or explanations needed before final approval. Common conditions include employment verification (often within days of closing), explanation of large deposits, updated bank statements, and clarification of credit inquiries.

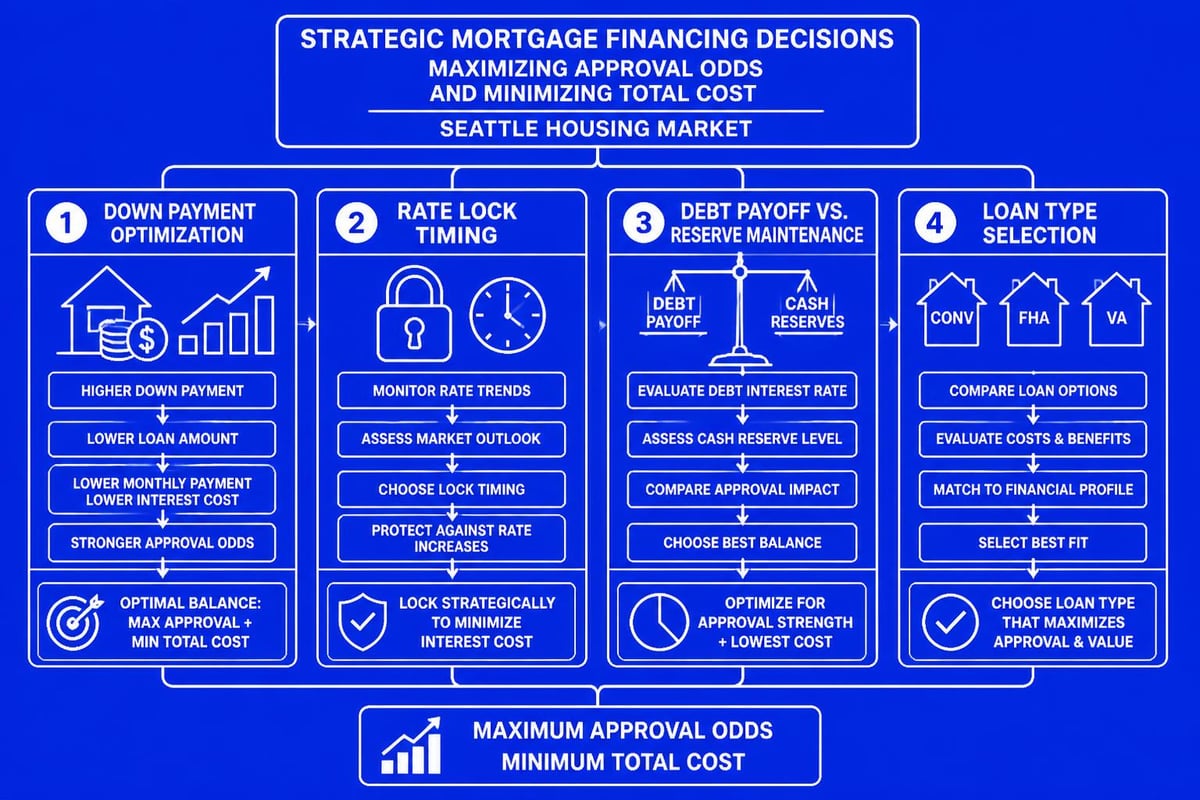

Strategic Approaches to Mortgage Financing

Developing a strategic approach to mortgage financing yields better rates, terms, and overall outcomes. This becomes particularly important in the Seattle market where property values and competition remain elevated.

Down Payment Strategy and Planning

The down payment represents your initial equity stake and significantly impacts mortgage financing terms. While minimum down payment requirements vary by loan type, strategic buyers consider the broader implications of their down payment amount.

Larger down payments reduce monthly payments, eliminate PMI requirements, and often secure better interest rates. However, they also reduce liquidity and opportunity cost-money used for down payment cannot be invested elsewhere or maintained as emergency reserves. For jumbo loan buyers deciding between 10% or 20% down, running detailed cash flow analyses reveals the optimal balance.

| Down Payment | Monthly Payment Impact | PMI Requirement | Rate Benefit | Liquidity Impact |

|---|---|---|---|---|

| 3-5% | Higher | Yes | Standard | Low |

| 10% | Moderate | Yes (conventional) | Slight improvement | Moderate |

| 20% | Lower | No | Better rates | Significant |

| 25%+ | Lowest | No | Best rates | Very significant |

Rate Lock Timing and Management

Interest rate volatility makes timing crucial in mortgage financing. Rate locks protect borrowers from increases during the processing period, typically offered for 30, 45, or 60 days. Understanding when to lock versus float requires market knowledge and risk assessment.

In rising rate environments, locking early provides certainty and protection. When rates trend downward, floating allows you to capture improvements. Many lenders offer one-time float-down options, permitting you to lock but still benefit if rates drop significantly before closing-though this feature typically costs 0.125-0.25% in points.

Optimizing Debt-to-Income Ratios

Strategic mortgage financing involves optimizing your DTI before application. Paying down revolving debt, avoiding new credit obligations, and timing large purchases appropriately can improve your qualification position. Some borrowers strategically pay off smaller installment loans entirely, removing them from DTI calculations even though the cash used reduces available reserves.

For Seattle tech professionals with substantial equity compensation, converting RSU proceeds to down payment or paying off existing debts creates flexibility in mortgage financing scenarios. However, maintaining adequate reserves often proves more valuable than marginally improving DTI, particularly for jumbo loan applications where lenders scrutinize liquidity.

Regulatory Framework and Consumer Protections

Modern mortgage financing operates within a comprehensive regulatory framework designed to protect consumers and ensure fair lending practices. The regulation of financial institutions encompasses federal and state-level oversight affecting every aspect of loan origination and servicing.

Ability-to-Repay Requirements

Federal regulations require lenders to make reasonable, good-faith determinations of borrowers' ability to repay before extending mortgage financing. The qualified mortgage standards outlined in federal regulations establish minimum standards for these assessments, including DTI limitations and verification requirements.

These protections benefit borrowers by preventing predatory lending while ensuring you're not approved for mortgage financing beyond your realistic repayment capacity. Lenders must document and verify income, assets, employment, credit history, and monthly debt obligations through reliable third-party records.

Disclosure and Transparency Requirements

TILA-RESPA Integrated Disclosure (TRID) rules mandate specific timing and content for mortgage financing disclosures. Borrowers receive a Loan Estimate within three business days of application, detailing all costs, terms, and projected payments. A Closing Disclosure follows at least three business days before closing, confirming final terms and allowing comparison to the initial estimate.

These standardized forms enable meaningful comparison shopping across different mortgage financing offers and protect against last-minute surprises. Understanding how to read and interpret these documents empowers borrowers to make informed decisions and identify potential issues before closing.

Market Dynamics Affecting Mortgage Financing in 2026

Current market conditions significantly influence mortgage financing availability, pricing, and terms. According to comprehensive mortgage market statistics, national trends show continued evolution in lending standards, product availability, and regional variations.

Seattle-Specific Market Considerations

The Greater Seattle housing market presents unique dynamics affecting mortgage financing strategies. Limited inventory, strong employment fundamentals, and continued population growth support property values while creating competitive purchasing conditions in neighborhoods from Lynnwood to Everett.

Local market knowledge becomes essential when structuring mortgage financing for success. Understanding neighborhood-specific trends, school district boundaries, development patterns, and commute considerations helps align financing strategies with long-term property performance. Home buying strategies tailored to Seattle’s market incorporate these factors into comprehensive planning.

Interest Rate Environment and Economic Factors

Mortgage financing costs reflect broader economic conditions including Federal Reserve policy, inflation trends, and bond market dynamics. While direct Fed rate changes don't determine mortgage rates, the overall policy direction influences the yield curve and investor appetite for mortgage-backed securities.

Monitoring economic indicators provides context for mortgage financing decisions. Employment reports, inflation data, GDP growth, and Fed communications all factor into rate forecasting. Working with an experienced broker who tracks these dynamics helps time applications and locks advantageously.

Portfolio Management and Refinancing Strategies

Mortgage financing extends beyond initial purchase-managing your loan portfolio over time maximizes financial efficiency. Strategic refinancing, payment optimization, and portfolio structuring create long-term value.

When Refinancing Makes Sense

Refinancing involves replacing existing mortgage financing with new terms, potentially lowering rates, changing loan duration, or accessing equity. The decision requires calculating break-even periods-how long it takes for monthly savings to offset closing costs.

Generally, refinancing makes financial sense when you can reduce your rate by at least 0.75-1.00%, plan to remain in the property beyond the break-even period, and have adequate equity. For borrowers who initially used FHA financing, refinancing to conventional loans once you reach 20% equity eliminates mortgage insurance permanently.

Accelerated Payoff Strategies

While mortgage financing typically spans 30 years, paying off your mortgage faster through extra principal payments or shorter terms builds equity and reduces total interest paid. The optimal approach balances opportunity cost against guaranteed returns from principal reduction.

For high-income Seattle tech professionals, the decision involves comparing after-tax mortgage rates against alternative investment returns. With average mortgage rates around 6-7% in 2026 and mortgage interest deductibility limited for high earners, the guaranteed return from extra principal payments becomes increasingly attractive.

Specialized Mortgage Financing Scenarios

Certain situations require specialized approaches to mortgage financing, from investment properties to unique property types or borrower circumstances.

Investment Property Financing

Purchasing rental properties in neighborhoods like Mill Creek or Everett requires understanding conventional loans for investment properties, which demand larger down payments (typically 15-25%) and higher interest rates than primary residence financing.

Lenders evaluate investment property mortgage financing differently, considering potential rental income in qualification calculations while applying more conservative underwriting standards. Documentation requirements expand to include existing lease agreements, rent rolls, and property management experience.

Self-Employment and Alternative Documentation

Self-employed borrowers face additional scrutiny in mortgage financing applications since income verification relies on tax returns rather than W-2s. Lenders typically average two years of net income from Schedule C, adding back non-cash deductions like depreciation.

Bank statement programs offer alternatives for self-employed borrowers who legitimately write off substantial business expenses, reducing taxable income below actual cash flow. These specialized mortgage financing products analyze deposits rather than tax returns, though they command premium pricing reflecting additional risk.

Working with Mortgage Professionals

Navigating mortgage financing successfully often requires professional guidance, particularly in complex scenarios involving high-value properties, unique income structures, or competitive markets. The value of experienced representation extends beyond rate shopping to strategic guidance throughout the process.

Broker vs. Direct Lender Considerations

Understanding the distinction between mortgage brokers and direct lenders helps you select the right partnership. Mortgage brokers in Seattle work with multiple lenders, providing access to diverse mortgage financing products and competitive pricing through wholesale channels. Direct lenders offer their own products exclusively, potentially streamlining processes but limiting options.

Experienced brokers bring market knowledge, relationship capital with underwriters, and problem-solving capabilities when challenges arise. This proves particularly valuable for buyers with complex income, tight timelines, or properties requiring specialized financing approaches. The American Bankers Association provides insights into current mortgage topics that inform professional practices and product offerings.

The Value of Local Expertise

Local market expertise significantly impacts mortgage financing outcomes. Understanding neighborhood-specific appraisal challenges, knowing which lenders close successfully in particular submarkets, and maintaining relationships with local processors and underwriters creates competitive advantages. Choosing a local lender in Seattle provides these benefits while supporting community-based relationships.

Local professionals understand regional employment dynamics, particularly relevant when qualifying tech sector income or evaluating job stability in a market heavily influenced by Amazon, Microsoft, and related employers. They recognize seasonal market patterns, inventory constraints by neighborhood, and pricing trends affecting appraisal outcomes.

Understanding mortgage financing fundamentals and strategic approaches positions you for success in Seattle's competitive housing market. Whether you're a first-time buyer in Lake Forest Park, a tech professional leveraging equity compensation for a jumbo loan in Bellevue, or an investor expanding your portfolio in Shoreline, having an experienced guide makes all the difference. Keith Akada at Mortgage Reel brings 25+ years of expertise helping Seattle-area buyers navigate complex financing scenarios with transparency, education, and proven execution-from qualifying RSU income to closing in as few as 9 business days.