Navigating first time mortgage rates in Seattle's competitive housing market requires understanding how lenders evaluate new buyers, what drives rate differences across loan programs, and which strategies help you secure the most favorable terms. With mortgage rates fluctuating throughout 2026 and recent rate movements creating new opportunities, first-time buyers across Seattle, Bellevue, Redmond, Kirkland, Shoreline, and Lynnwood need clear guidance on how to approach their home financing. This guide breaks down everything you need to know about securing competitive rates, qualifying with tech compensation, and choosing the right loan structure for your financial situation.

Understanding How First Time Mortgage Rates Are Determined

First time mortgage rates depend on multiple factors that lenders evaluate to assess risk. Your credit score plays the most significant role in determining your interest rate, with scores above 740 typically qualifying for the best available rates while scores between 620 and 700 receive higher pricing adjustments.

Lenders evaluate these key factors when setting your rate:

- Credit score and payment history

- Down payment percentage

- Loan-to-value ratio

- Debt-to-income ratio

- Employment stability and income documentation

- Property type and location

- Loan program selection

The loan program you choose significantly impacts your rate structure. Conventional loans typically offer the lowest rates for well-qualified borrowers, while FHA loans provide competitive options for buyers with smaller down payments or lower credit scores. For tech professionals purchasing homes above conforming loan limits in Seattle, Bellevue, and Redmond, jumbo loan programs offer specialized pricing structures.

Rate Variations Across Loan Programs

Different mortgage products carry distinct rate characteristics based on their risk profiles and government backing. Understanding these differences helps first-time buyers select programs aligned with their financial profiles.

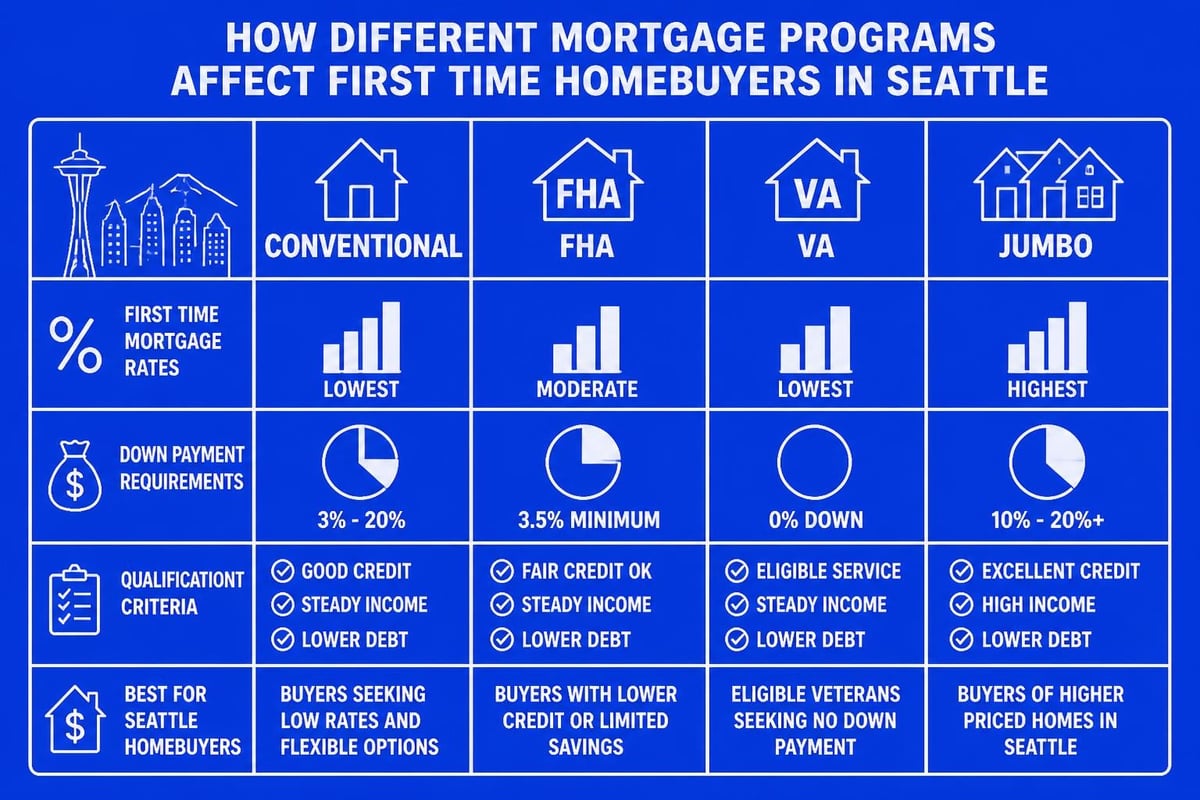

| Loan Type | Typical Rate Range | Down Payment | Credit Requirement |

|---|---|---|---|

| Conventional | Lowest available | 3-20% | 620+ (best at 740+) |

| FHA | Competitive | 3.5% | 580+ |

| VA | Highly competitive | 0% | 620+ recommended |

| Jumbo | Premium pricing | 10-20% | 700+ |

Market conditions influence all first time mortgage rates simultaneously, but the degree of movement varies by product. When the Federal Reserve adjusts monetary policy or mortgage rates experience significant fluctuations, conventional and jumbo products typically react more dramatically than government-backed programs.

Qualifying for Competitive First Time Mortgage Rates in Seattle

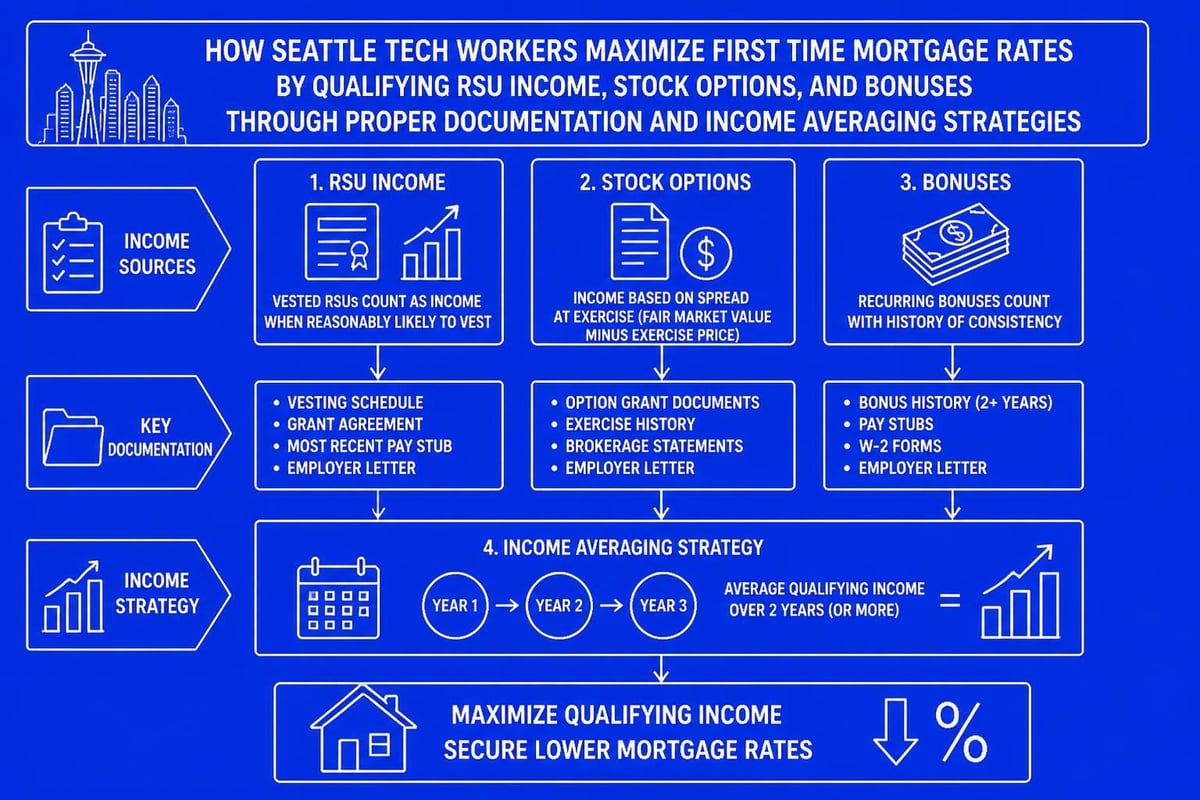

Seattle's unique employment landscape creates both opportunities and challenges for first-time buyers seeking optimal rates. Tech professionals working at Amazon, Microsoft, and Google often qualify for exceptional rates due to stable employment and strong income profiles, but must properly document equity compensation.

Documentation Requirements for Tech Compensation

Stock-based compensation requires specific documentation approaches to maximize your qualifying income and secure better rates. RSUs, stock options, and performance bonuses can significantly increase your buying power when properly verified.

Essential documentation for equity compensation:

- Two years of W-2s showing vested RSU income

- Most recent pay stubs reflecting stock compensation

- Grant agreements or vesting schedules

- Tax returns documenting bonus and equity income

- Employment verification letter confirming compensation structure

Lenders typically average your two-year equity compensation history to establish qualifying income. This approach benefits Seattle tech workers whose stock-based income has increased consistently, as it demonstrates stable high earnings that reduce lender risk and improve rate pricing.

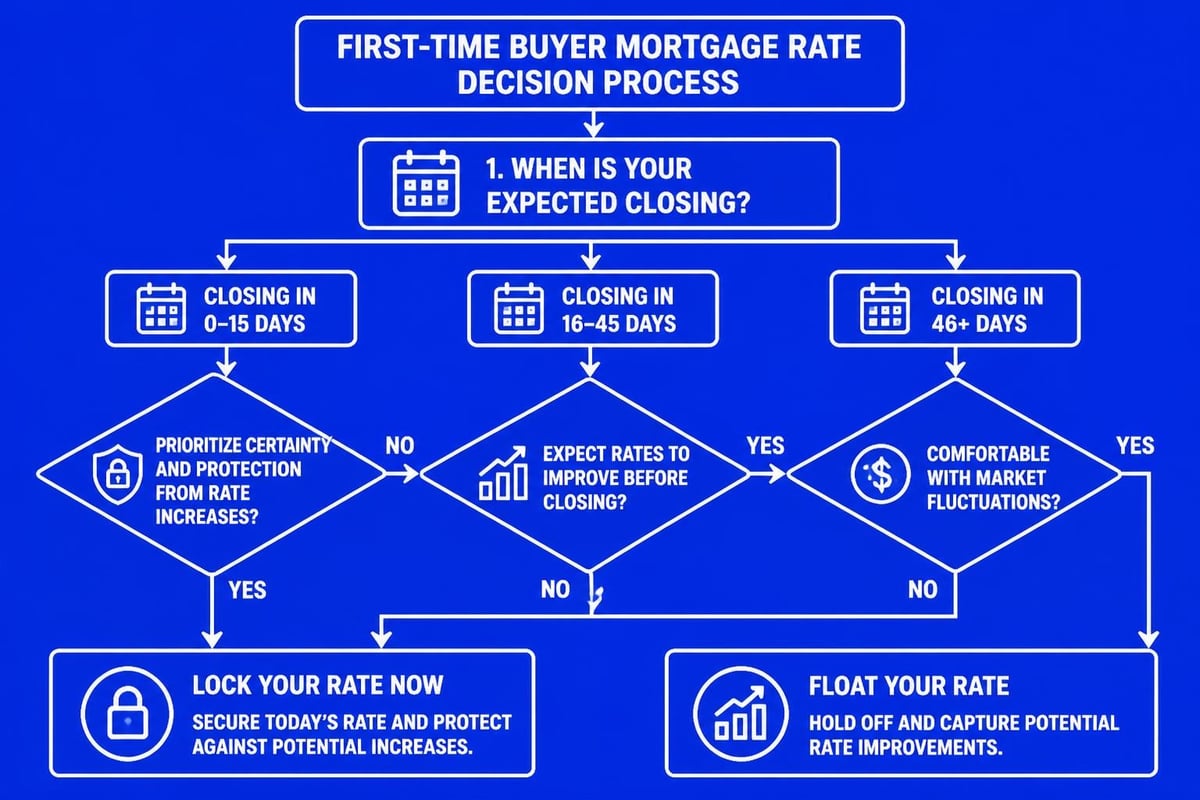

Strategic Timing and Rate Lock Decisions

First time mortgage rates change daily based on bond market activity, economic indicators, and Federal Reserve policy signals. The current mortgage rate environment requires strategic timing decisions about when to lock your rate versus floating to potentially capture improvements.

Rate locks protect you from upward movement but prevent you from benefiting if rates drop. Most lenders offer lock periods ranging from 15 to 60 days, with longer locks carrying slightly higher costs.

Evaluating Whether to Lock or Float

Your rate lock decision should align with your purchase timeline, risk tolerance, and market conditions. In rising rate environments, earlier locks provide valuable protection, while falling rate markets may favor strategic floating with backup lock options.

Consider locking your rate when you have a signed purchase agreement and confirmed closing timeline. For buyers in competitive Seattle neighborhoods like Ballard, Wallingford, or Capitol Hill where bidding wars remain common, having a locked rate provides certainty when calculating maximum purchase price.

Buyers in Shoreline, Lake Forest Park, and Mill Creek often have more flexibility given slightly longer negotiation timelines. This additional time allows for monitoring rate trends while maintaining the option to lock when favorable conditions emerge.

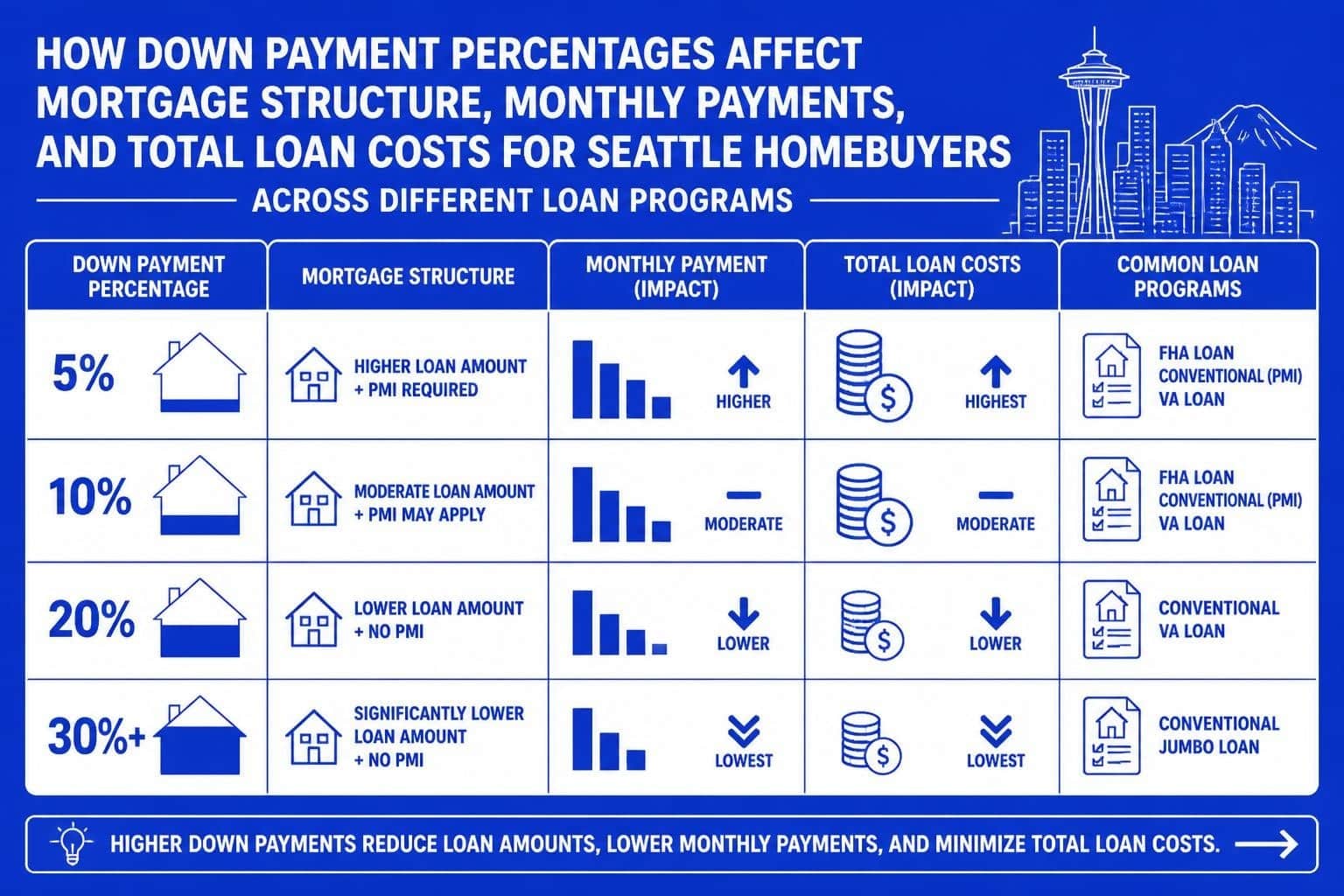

Down Payment Impact on First Time Mortgage Rates

Down payment size directly influences your interest rate through loan-to-value pricing adjustments. Conventional loans penalize higher LTV ratios with rate increases, while government programs maintain more consistent pricing across down payment levels.

Rate Improvements by Down Payment Tier

Conventional loan pricing improves at specific down payment thresholds. Moving from 5% to 10% down typically reduces your rate by 0.125% to 0.25%, while increasing from 10% to 20% provides another 0.125% to 0.375% improvement.

- 3% down: Highest conventional rates, requires PMI

- 5% down: Moderate rate pricing, requires PMI

- 10% down: Improved pricing, still requires PMI

- 15% down: Better rates, PMI required until 20%

- 20% down: Optimal conventional pricing, no PMI

For detailed guidance on accumulating funds for larger down payments, review the comprehensive down payment guide for Seattle homebuyers which covers savings strategies, gift funds, and down payment assistance programs available in Washington State.

FHA loans maintain relatively consistent rate pricing regardless of down payment percentage. Whether you put 3.5% or 10% down, your base interest rate remains similar, though the higher down payment reduces your upfront and ongoing mortgage insurance costs.

Program-Specific Rate Considerations for First-Time Buyers

Each loan program offers distinct advantages depending on your financial profile, property price point, and long-term homeownership plans. Understanding these program-specific characteristics helps optimize your rate strategy.

Conventional Loan Rate Optimization

Conventional loans reward strong credit profiles with the lowest available first time mortgage rates. Borrowers with 740+ credit scores, 20% down payments, and debt-to-income ratios below 36% access premium pricing tiers.

Strategies to optimize conventional rates:

- Improve credit scores above key thresholds (700, 720, 740, 760)

- Lower DTI ratios by paying down revolving debt

- Increase down payment to reduce LTV pricing hits

- Consider points to buy down your rate if planning long-term ownership

- Maintain strong employment documentation and reserves

Working with experienced conventional loan lenders who understand Seattle's housing market ensures you receive accurate pricing and appropriate program selection based on your specific financial situation.

FHA Rate Advantages for Limited Down Payment Buyers

FHA loans provide accessible first time mortgage rates for buyers with smaller down payments or credit profiles that don't qualify for optimal conventional pricing. The FHA down payment requirement of just 3.5% makes homeownership attainable for buyers still building savings.

While FHA rates compete favorably with conventional products, the required mortgage insurance premiums increase your total monthly payment. FHA charges both an upfront premium (1.75% of loan amount) and ongoing annual premiums (0.55% to 0.85% annually), which remain for the loan's life on purchases with less than 10% down.

Jumbo Rate Structures for High-Cost Areas

Seattle's housing market frequently requires jumbo financing for properties exceeding the 2026 conforming loan limit of $806,500. Jumbo first time mortgage rates typically carry premiums of 0.25% to 0.75% above conforming conventional rates, though well-qualified borrowers can access competitive pricing.

| Credit Score | Typical Jumbo Rate Premium |

|---|---|

| 760+ | +0.25% to +0.375% |

| 740-759 | +0.375% to +0.50% |

| 720-739 | +0.50% to +0.625% |

| 700-719 | +0.625% to +0.75% |

Tech professionals in Bellevue, Redmond, and Kirkland frequently need jumbo home loan solutions given median home prices in these submarkets. Properly documenting equity compensation and maintaining substantial reserves (typically 6-12 months) helps secure optimal jumbo rates.

Market Conditions and Rate Forecasting for 2026

Understanding broader mortgage rate trends helps first-time buyers make informed timing decisions. While no one can predict exact rate movements, analyzing Federal Reserve policy, inflation trends, and economic indicators provides directional guidance.

Throughout 2026, first time mortgage rates have shown volatility in response to employment data, inflation reports, and Federal Reserve communications. Buyers should focus on their personal readiness rather than attempting to perfectly time the market, as rates represent just one component of total homeownership costs.

Local Market Factors Affecting Seattle Rates

Seattle's strong employment base, limited housing inventory, and consistent population growth create stable demand that supports home values. This market strength allows lenders to offer competitive rates knowing property values maintain stability even during broader economic uncertainty.

Neighborhoods in Shoreline, Lynnwood, Mill Creek, and Everett often provide more accessible price points for first-time buyers while maintaining excellent access to Seattle employment centers. Properties in these areas qualify for the same rate programs as Seattle proper while requiring smaller loan amounts, potentially avoiding jumbo territory.

Credit Optimization Timeline for First-Time Buyers

Improving your credit score before applying for a mortgage can reduce your first time mortgage rates significantly. Each 20-point improvement in your credit score can lower your rate by 0.125% to 0.25%, translating to substantial savings over a 30-year loan.

Effective credit improvement strategies (6-12 months before applying):

- Pay down credit card balances below 30% utilization

- Dispute any inaccuracies on credit reports

- Avoid opening new credit accounts

- Maintain on-time payment history across all accounts

- Consider becoming an authorized user on established accounts

- Keep old accounts open to maintain credit history length

Working with a mortgage broker who reviews your credit before formal application allows you to address issues proactively. This strategic approach ensures you present the strongest possible profile when rates are locked, maximizing your negotiating position with lenders.

Comparing Total Costs Beyond Interest Rates

First time mortgage rates represent your base borrowing cost, but total loan expenses include origination fees, discount points, title insurance, appraisal fees, and ongoing costs like property taxes and insurance. Evaluating loans based on Annual Percentage Rate (APR) provides better comparison across lenders.

Understanding APR vs. Interest Rate

Your interest rate determines your monthly principal and interest payment, while APR incorporates upfront fees amortized over the loan term. A loan with a slightly higher rate but lower fees may provide better value than one with a lower rate but substantial upfront costs.

Seattle's title insurance and escrow fee structures differ from other markets, making local lender experience valuable when estimating total closing costs. Lenders familiar with King and Snohomish County closing requirements provide more accurate estimates and smoother transactions.

Rate Buydown Options and Long-Term Strategy

Paying discount points to reduce your interest rate makes financial sense when you plan to own the property long enough to recoup the upfront cost through monthly payment savings. Each point (1% of loan amount) typically reduces your rate by 0.25%.

Calculate your break-even timeline:

If you pay $8,000 in points to save $100 monthly, your break-even period is 80 months (6.7 years). Planning to own the home beyond this timeline makes the buydown financially advantageous.

First-time buyers in Seattle's competitive market should balance rate buydowns against reserve requirements. Maintaining substantial cash reserves often provides more flexibility and financial security than minimizing your interest rate through points.

Navigating First-Time Buyer Programs and Incentives

Washington State offers several programs specifically designed to help first-time buyers access competitive rates and down payment assistance. The Washington State Housing Finance Commission provides programs with favorable terms for qualified buyers.

Understanding eligibility for first-time home buyer programs in Washington helps you access resources that reduce upfront costs and potentially improve your rate structure. Many programs combine conventional or FHA financing with state-backed down payment assistance.

Combining Programs for Optimal Results

Sophisticated first-time buyers often layer multiple programs to minimize cash requirements while maintaining competitive rates. For example, using a conventional 97 loan (3% down) combined with gift funds or down payment assistance preserves savings for reserves and closing costs.

The Consumer Financial Protection Bureau’s loan options guide provides comprehensive information on federal programs and protections available to first-time buyers, complementing state and local resources.

Documentation Preparation for Rate Approval

Lenders verify every aspect of your financial profile before approving your rate quote. Incomplete or inconsistent documentation delays approval and risks rate lock expiration, potentially costing you favorable pricing.

Essential documentation for all first-time buyers:

- Two years of W-2s and tax returns

- 30 days of pay stubs

- Two months of bank statements for all accounts

- Gift letters if using gift funds for down payment

- Signed purchase agreement (for rate lock)

- Employment verification letter

- Explanation letters for any credit issues

Tech professionals should also prepare grant agreements, vesting schedules, and documentation of any equity compensation. Proactive preparation allows for rapid approval once you identify your target property, critical in competitive Seattle neighborhoods where sellers favor buyers with solid financing.

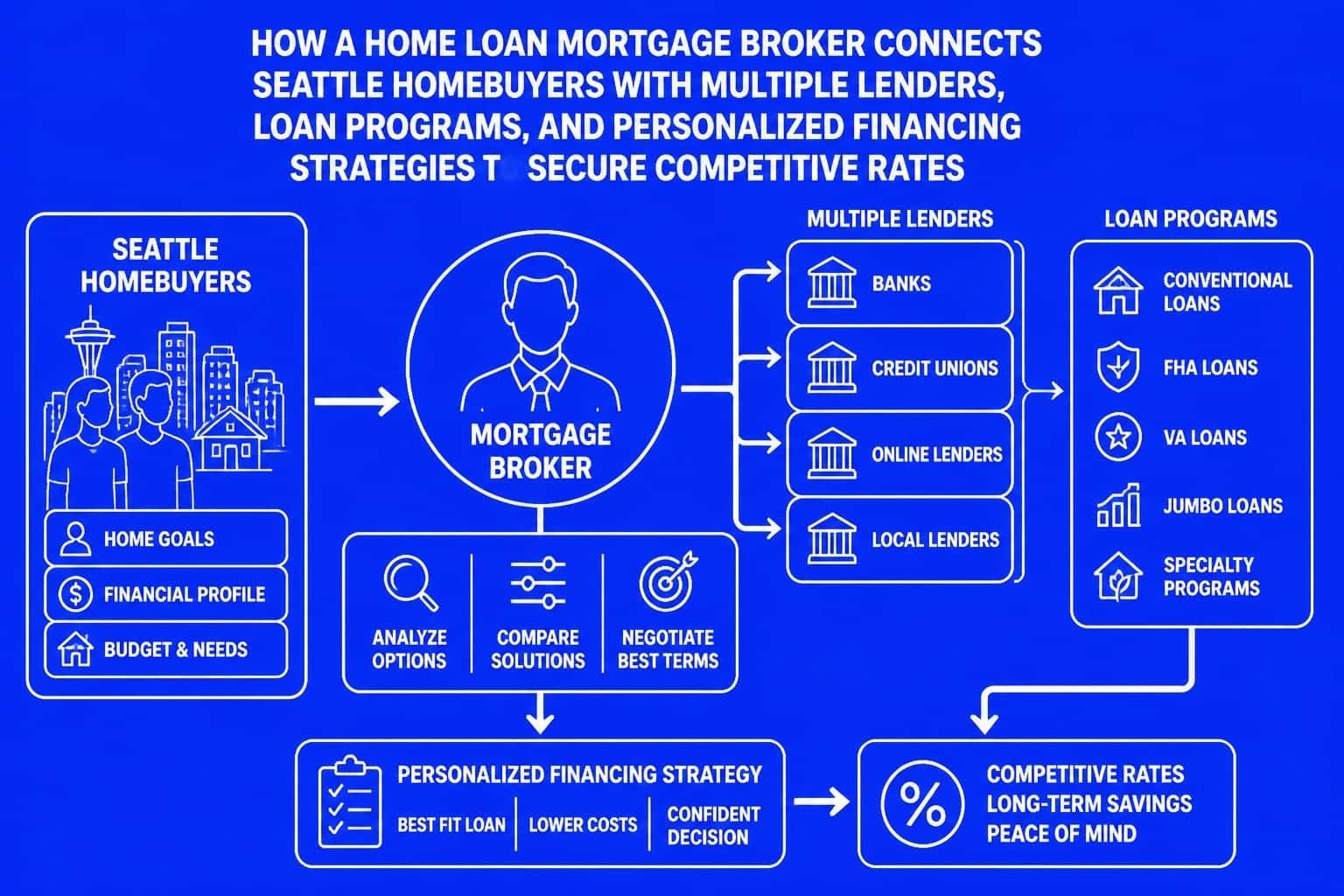

Working with Specialized First-Time Buyer Experts

Mortgage brokers specializing in first-time buyers understand the unique challenges new purchasers face and can access multiple lenders to find optimal rate structures. Unlike retail banks offering only their proprietary products, brokers compare offerings across numerous lenders.

Choosing experienced first-time home buyer brokers who serve Seattle extensively provides advantages in competitive offer situations. Sellers and listing agents recognize established brokers with strong track records, giving your offer additional credibility even when terms are similar to competing bids.

For buyers exploring whether professional mortgage assistance provides value, understanding how mortgage brokers approach pricing helps evaluate the relationship between service quality and fee structures.

Refinancing Considerations for First-Time Buyers

While this guide focuses on purchase mortgage rates, first-time buyers should understand that their initial rate need not be permanent. Market conditions change, credit profiles improve, and refinancing opportunities emerge that can reduce borrowing costs substantially.

Maintaining awareness of rate trends after closing allows you to capitalize on refinancing opportunities when they arise. Generally, refinancing makes financial sense when you can reduce your rate by at least 0.75% and plan to remain in the home long enough to recoup closing costs.

Understanding first time mortgage rates requires evaluating your complete financial profile, comparing loan programs strategically, and timing your application to align with both market conditions and personal readiness. Whether you're a tech professional in Redmond maximizing RSU income or a buyer in Lynnwood seeking accessible pricing with smaller down payments, the right loan structure and competitive rates make homeownership achievable. Keith Akada brings 25+ years of mortgage expertise to first-time buyers across Seattle, Bellevue, Kirkland, Shoreline, and surrounding communities, specializing in tech compensation qualification and fast closings through Fairway's advanced underwriting. Connect with Mortgage Reel to explore your financing options and secure competitive rates tailored to your unique financial situation.