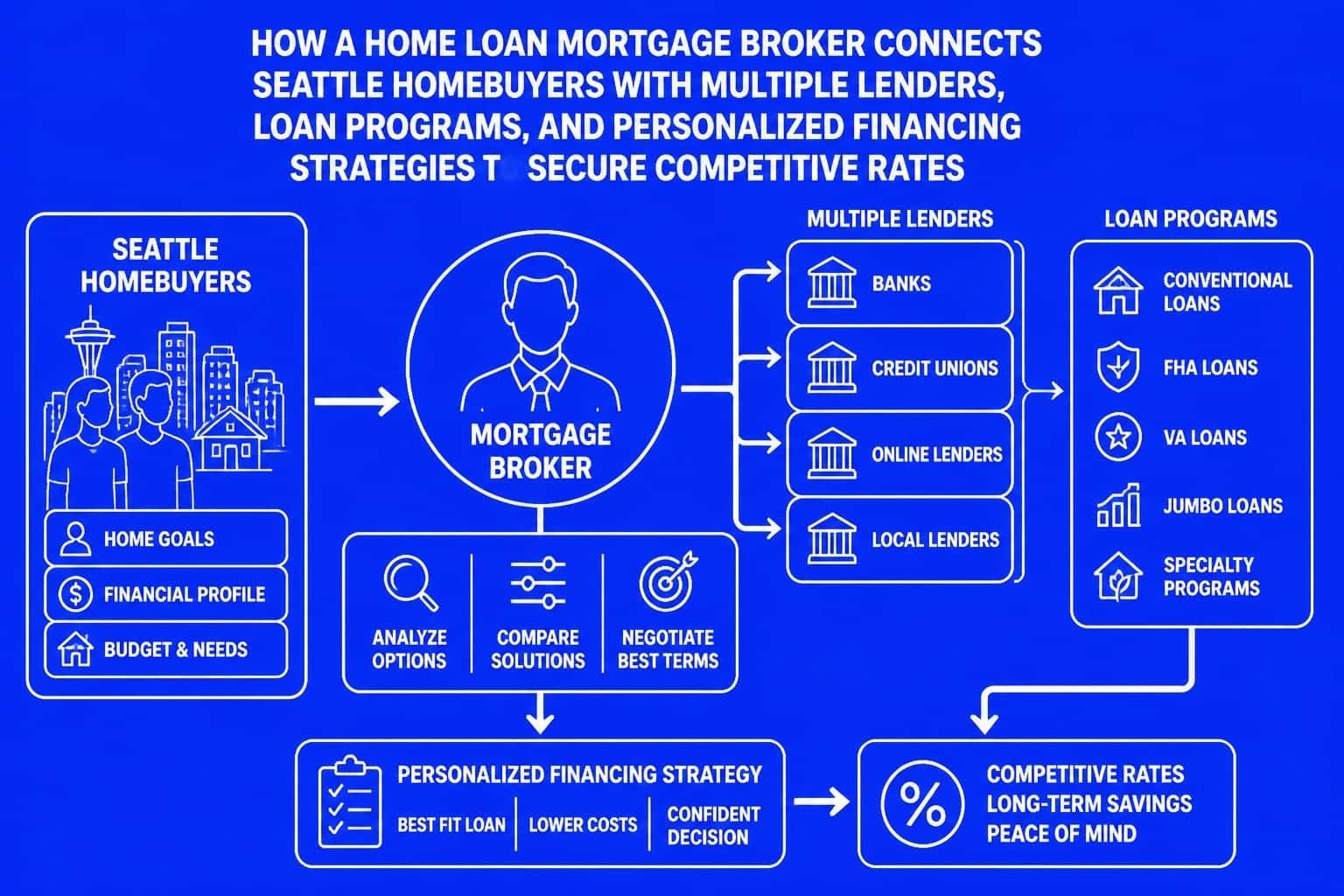

Working with a home loan mortgage broker can transform your homebuying experience from overwhelming to manageable, especially in competitive markets like Seattle, Bellevue, and Redmond. Unlike traditional bank loan officers who represent a single institution, a broker serves as your advocate, connecting you with multiple lending sources to find the financing that best matches your financial profile and homeownership goals. For tech professionals navigating complex compensation structures or first-time buyers exploring various loan programs, understanding how mortgage brokers operate makes the difference between settling for convenient financing and securing optimal terms.

What a Home Loan Mortgage Broker Does

A home loan mortgage broker functions as an intermediary between borrowers and lenders, working on your behalf to identify, compare, and secure financing options. Rather than being limited to one bank's products, brokers maintain relationships with numerous wholesale lenders, credit unions, and specialty finance companies.

Access to Multiple Lending Sources

Brokers tap into wholesale lending channels unavailable to retail consumers. This network includes:

- National banks offering conventional and government-backed loans

- Portfolio lenders with flexible underwriting for unique situations

- Credit unions providing competitive member rates

- Non-QM lenders specializing in self-employed borrowers or complex income scenarios

- Jumbo loan specialists for high-balance financing in expensive markets like Kirkland and Bellevue

The Consumer Financial Protection Bureau explains the distinction between lenders who fund loans directly and brokers who originate loans through multiple channels.

Personalized Loan Matching

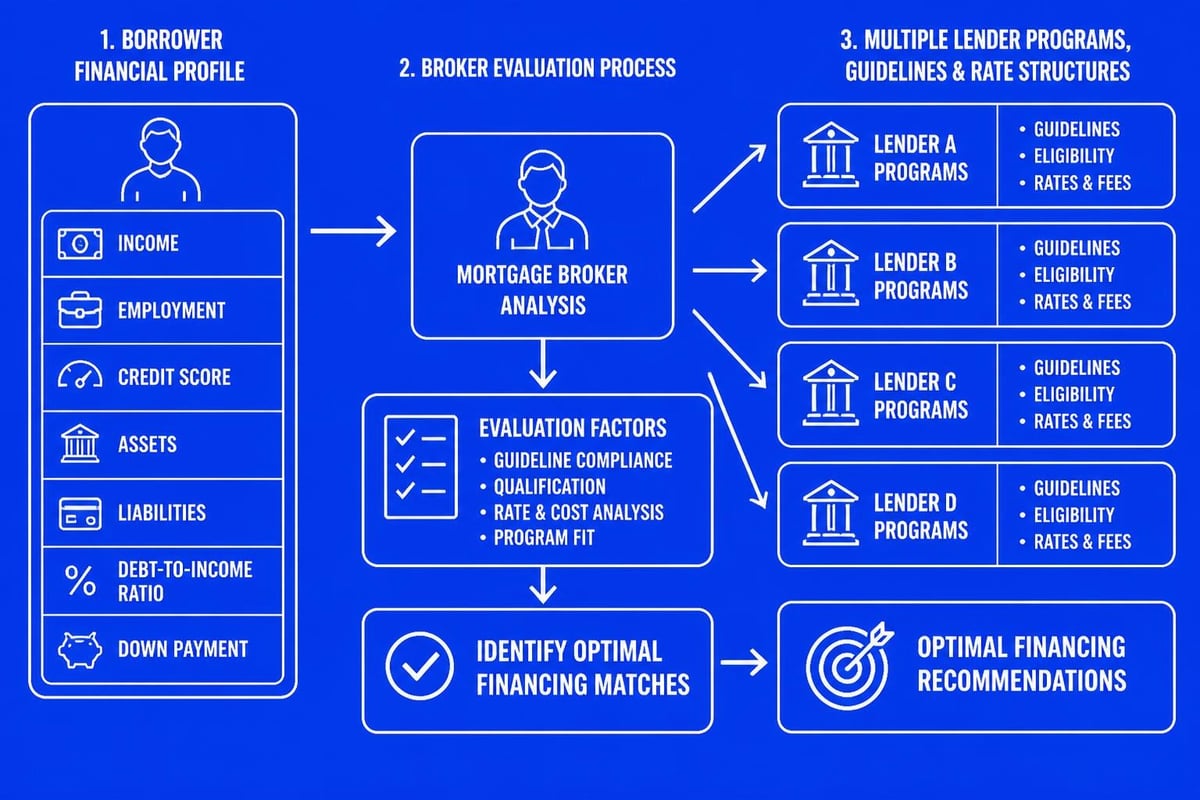

Your broker analyzes your complete financial picture: income documentation, credit profile, down payment resources, employment history, and debt obligations. For Seattle-area tech employees, this includes understanding how to qualify restricted stock units, performance bonuses, and equity compensation.

The matching process involves:

- Reviewing your credit reports and scores from all three bureaus

- Calculating debt-to-income ratios across different loan programs

- Identifying which lenders best accommodate your income type

- Comparing rate-and-fee structures for equivalent loan products

- Presenting options with clear explanations of trade-offs

Broker Advantages in the Seattle Market

The Puget Sound region presents unique financing challenges that experienced brokers navigate daily. Median home prices in Seattle, Shoreline, and surrounding communities often exceed conventional loan limits, requiring specialized jumbo financing knowledge.

Competitive Rate Shopping

Brokers submit your application to multiple lenders simultaneously, creating competitive tension that often results in better pricing. This approach proves particularly valuable when:

- Market conditions shift rapidly between rate-lock and closing

- Your credit score falls near key pricing thresholds (680, 700, 740)

- Property types require specialized underwriting (condos, multi-family, investment properties)

- Down payment percentages trigger different rate tiers

| Scenario | Direct Bank Approach | Broker Approach |

|---|---|---|

| Rate comparison | Single institution | 10+ lenders |

| Program options | Bank's portfolio only | Conventional, FHA, VA, jumbo, non-QM |

| Underwriting flexibility | Fixed guidelines | Multiple guideline sets |

| Closing timeline | 30-45 days typical | As fast as 9 business days with select lenders |

Guidance Through Complex Transactions

Seattle's competitive housing market demands precision and speed. Experienced brokers like those at Mortgage Reel bring procedural knowledge that prevents common delays:

- Pre-underwriting strategies that identify documentation issues before offers

- Appraisal gap planning for markets where homes regularly sell above list price

- Contingency management coordinating inspection, financing, and closing timelines

- Multiple offer scenarios structuring financing terms that strengthen your position

For first-time buyers exploring down payment options, brokers explain how different programs affect monthly payments, mortgage insurance requirements, and closing costs.

Understanding Broker Compensation

Transparency around how brokers earn fees helps you evaluate the value proposition. Most home loan mortgage broker compensation comes from lender-paid commissions rather than direct borrower charges.

Lender-Paid Compensation Structure

When you close a loan through a broker, the wholesale lender pays a percentage of the loan amount as an origination fee. This commission typically ranges from 0.5% to 2.5%, depending on loan type, amount, and lender agreements.

Important considerations:

- Broker compensation appears on your Loan Estimate and Closing Disclosure

- Federal regulations prohibit brokers from receiving undisclosed fees

- You can negotiate broker fees or compare against direct lender charges

- Higher commissions don't necessarily mean worse borrower pricing

NerdWallet’s guide provides additional context on broker fee structures and what questions to ask during initial consultations.

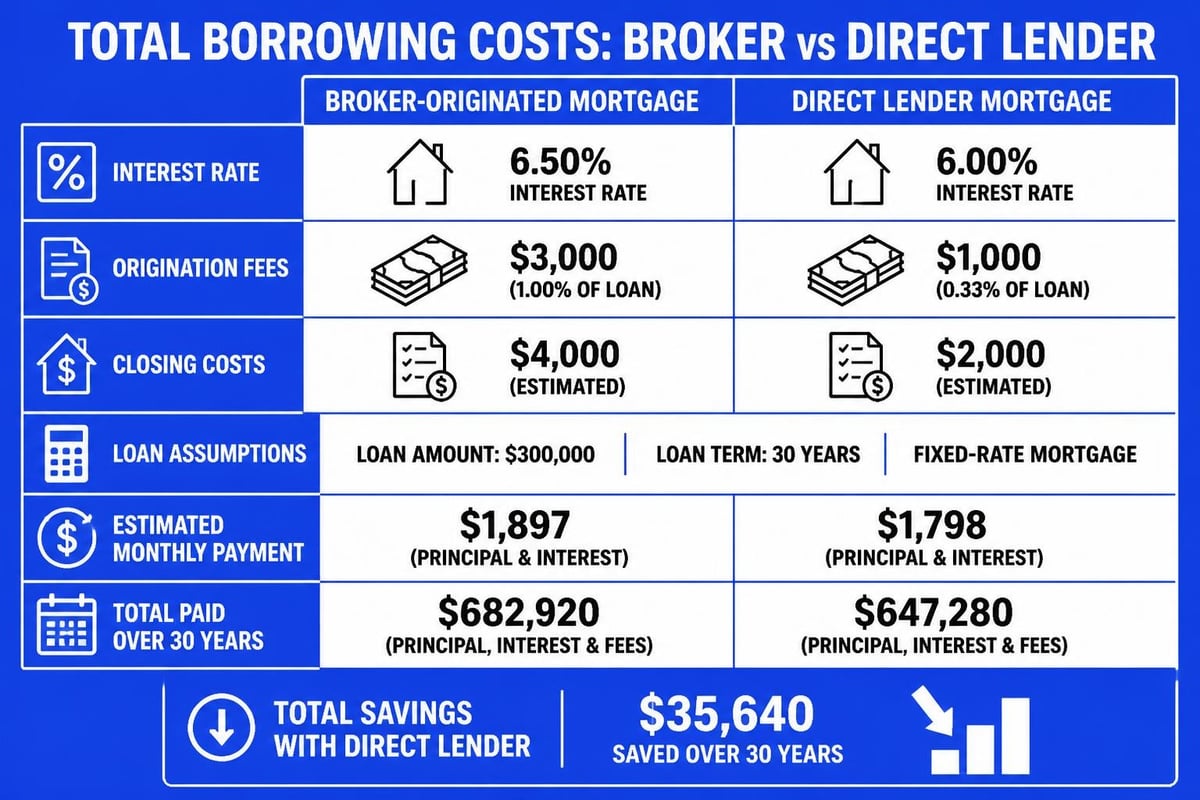

Cost Comparison: Broker vs. Direct Lender

Many borrowers assume direct lenders offer lower costs by eliminating the middleman. However, wholesale lending channels often provide better pricing than retail divisions of the same bank.

Why wholesale rates compete favorably:

- Lower operational overhead without branch networks

- Streamlined processing through specialized teams

- Volume-based pricing agreements between brokers and lenders

- Competition among lenders for broker business

The key is requesting detailed Loan Estimates from both brokers and direct lenders, then comparing total costs over your expected holding period. Shopping multiple offers remains the most effective way to ensure competitive pricing.

Selecting the Right Home Loan Mortgage Broker

Not all mortgage professionals offer equivalent service quality or market expertise. Seattle homebuyers benefit from evaluating brokers across multiple dimensions beyond advertised rates.

Experience and Market Knowledge

Years in business indicate a broker's ability to navigate changing market conditions, but local expertise matters equally. A broker serving the Greater Seattle area should understand:

- Regional lending patterns including condo warrantability issues in downtown Seattle high-rises

- Tech compensation qualification for employees at Amazon, Microsoft, Google, and other major employers

- Jumbo loan requirements specific to high-balance conforming and super-jumbo programs

- Investment property financing in rapidly appreciating neighborhoods across Lynnwood and Mill Creek

Ask potential brokers how long they've served your target market and request client references from similar purchase scenarios.

Technology and Communication Systems

Modern mortgage transactions require sophisticated coordination between brokers, underwriters, title companies, real estate agents, and borrowers. Evaluate a broker's operational capabilities:

- Digital application platforms allowing secure document upload and electronic signatures

- Real-time status updates through client portals or automated notifications

- Mobile accessibility for time-sensitive rate locks and condition clearances

- Proactive communication habits keeping all parties informed of progress and potential issues

For first-time homebuyers, clear communication about process steps and timeline expectations reduces anxiety and prevents misunderstandings.

Review History and Reputation

Online reviews provide insight into client experiences, but volume and consistency matter more than isolated testimonials. Brokers with hundreds of verified reviews across multiple platforms demonstrate sustained service quality.

Platforms to research:

- Google Business profiles with location-specific reviews

- Zillow lender ratings from actual borrowers

- Yelp feedback emphasizing service aspects

- Redfin partner agent recommendations

Look for patterns in reviews rather than perfect scores. How does the broker respond to criticism? Do clients mention specific strengths like education, responsiveness, or problem-solving?

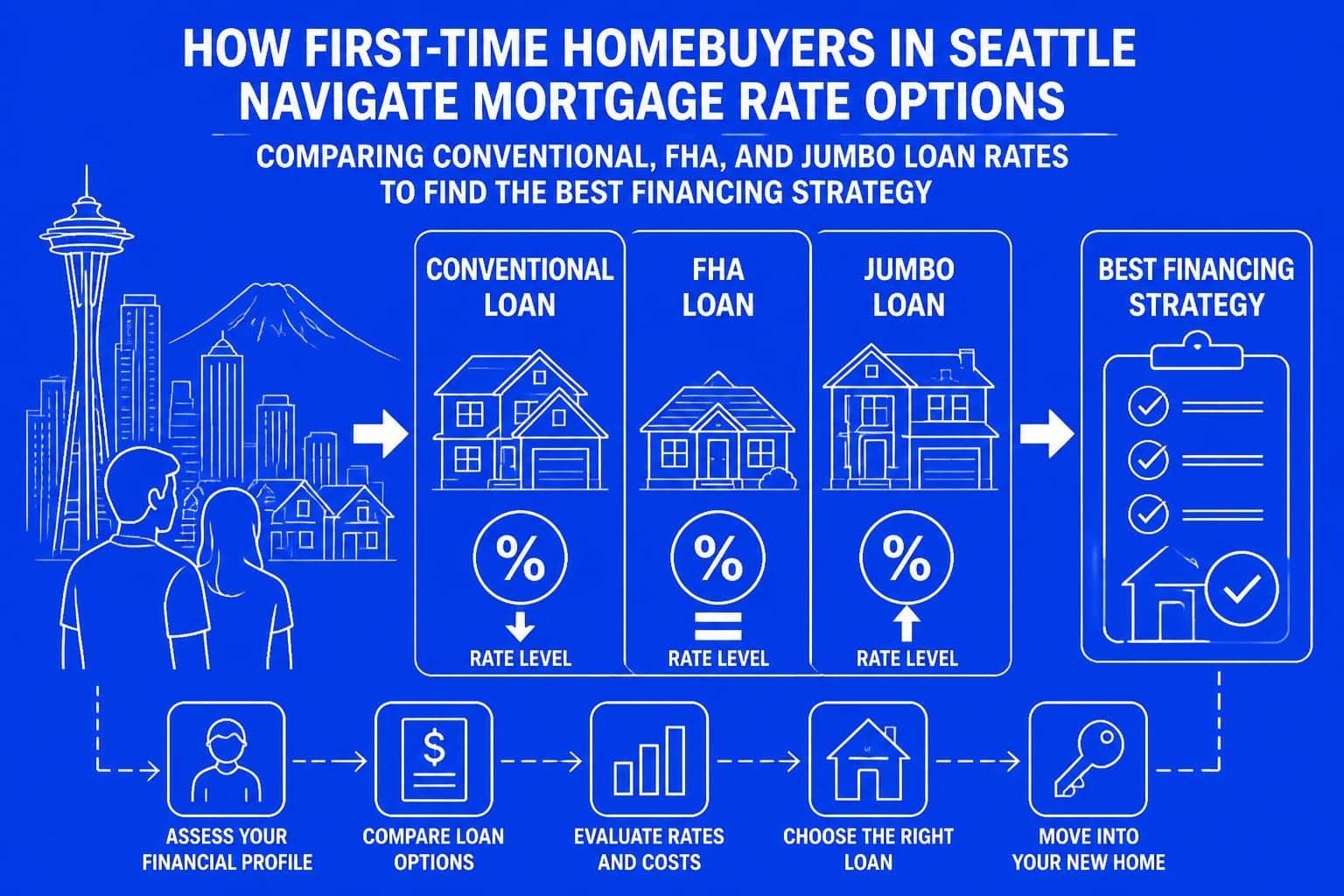

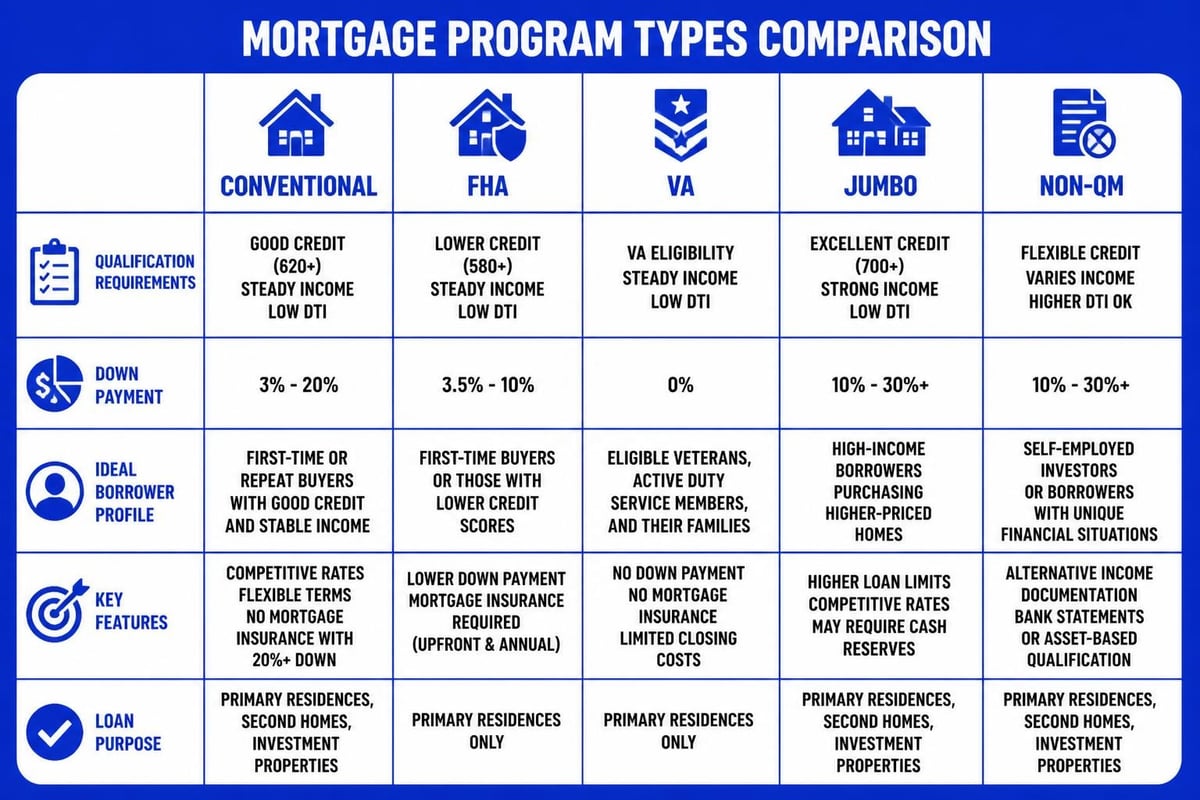

Loan Programs Available Through Brokers

A competent home loan mortgage broker presents the full spectrum of financing options, explaining trade-offs between programs rather than steering toward one solution.

Conventional Mortgages

Backed by Fannie Mae and Freddie Mac, conventional loans remain the most common financing for Seattle-area purchases. Brokers help borrowers navigate:

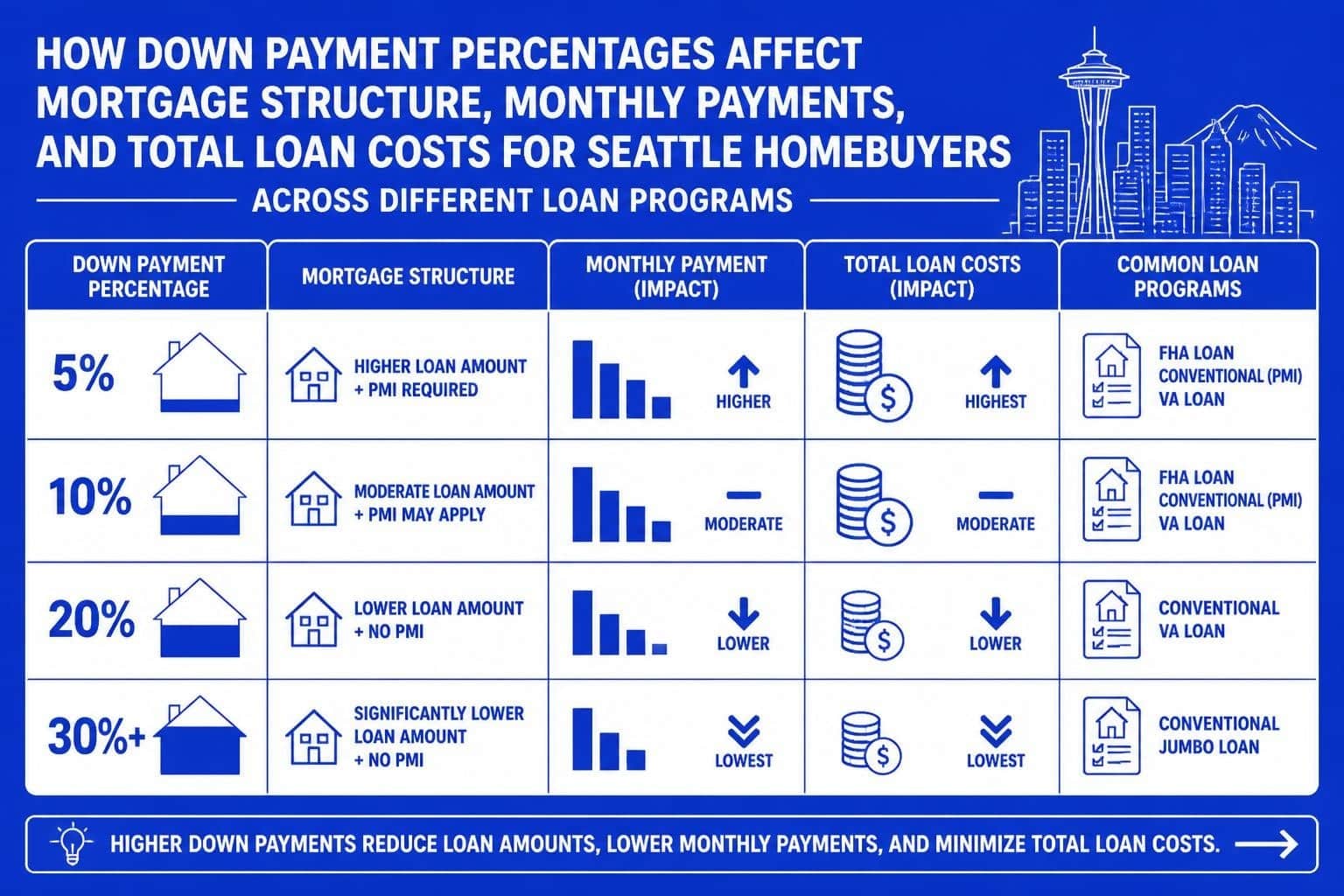

- Down payment requirements from 3% for first-time buyers to 20% for avoiding PMI

- Credit score tiers affecting rate pricing at 680, 700, 720, and 740 thresholds

- Debt-to-income limits up to 50% with compensating factors

- Property type restrictions and occupancy requirements

Conventional loan options work well for borrowers with stable income and solid credit profiles.

Government-Backed Programs

FHA, VA, and USDA loans serve specific borrower segments with advantageous terms:

| Program | Down Payment | Credit Requirements | Income Limits | Best For |

|---|---|---|---|---|

| FHA | 3.5% minimum | 580+ score typical | None | Lower credit scores, smaller down payments |

| VA | 0% for eligible | 620+ recommended | None | Military service members, veterans |

| USDA | 0% for eligible | 640+ typical | Regional limits apply | Rural/suburban properties |

For Seattle buyers considering FHA financing, brokers explain how mortgage insurance requirements differ from conventional PMI.

Jumbo Loan Expertise

Properties exceeding conforming loan limits ($806,500 in most Washington counties for 2026) require jumbo financing with distinct qualification standards. Brokers specializing in high-balance loans understand:

- Reserve requirements typically 6-12 months of housing payments

- Documentation intensity for income, assets, and employment verification

- Property appraisal standards including requirements for second appraisals on large loans

- Rate pricing factors influenced by loan-to-value ratios and credit scores

Tech professionals in Bellevue and Redmond purchasing homes above $1.5 million benefit from jumbo loan specialists who qualify stock compensation and bonus income effectively.

Non-QM and Alternative Documentation

Self-employed borrowers, those with recent credit events, or individuals with complex income structures often need non-qualified mortgage solutions. These programs offer:

- Bank statement income verification for business owners

- Asset depletion calculations for retirees or high-net-worth individuals

- Interest-only payment structures for cash flow optimization

- Alternative credit data for borrowers rebuilding credit histories

The Broker-Assisted Purchase Process

Understanding workflow expectations helps Seattle homebuyers prepare documentation and make timely decisions throughout the financing process.

Initial Consultation and Pre-Approval

Your first meeting with a home loan mortgage broker establishes the foundation for successful financing. Bring comprehensive financial documentation:

- Income verification including recent pay stubs, W-2s, tax returns for the past two years

- Asset statements showing checking, savings, investment, and retirement accounts

- Credit authorization allowing broker to pull reports and scores

- Employment documentation including offer letters for recent job changes

- Stock compensation details for tech employees with RSUs, options, or equity grants

Based on this information, brokers issue pre-approval letters specifying maximum loan amounts and likely program types. Strong pre-approvals in competitive markets like Lake Forest Park and Everett often include preliminary underwriting verification.

Rate Lock Strategy

Interest rates fluctuate daily based on economic indicators and bond market movements. Brokers help you decide when to lock rates based on:

- Market trend analysis indicating whether rates are rising or falling

- Lock period selection matching your expected closing timeline (30, 45, or 60 days)

- Float-down options allowing one-time rate reductions if markets improve

- Extension fees protecting against delays beyond the initial lock period

Experienced brokers monitor rate sheets throughout the day, locking at optimal moments rather than defaulting to morning rate releases.

Underwriting Coordination

After you're under contract, the underwriting phase involves detailed verification of everything claimed in your application. Your broker coordinates:

- Title and escrow ordering preliminary reports and scheduling closing

- Appraisal management selecting qualified appraisers and expediting inspections

- Condition clearing gathering supplemental documentation for underwriter requests

- Final approval ensuring all guidelines are satisfied before closing date

The typical approval timeline ranges from 21 to 30 days for standard transactions, though experienced brokers with efficient lender relationships often close faster.

Special Considerations for Seattle Tech Professionals

High-earning employees at major technology companies present unique qualification opportunities that skilled brokers leverage for maximum purchasing power.

Qualifying Stock-Based Compensation

Restricted stock units, employee stock purchase plans, and stock options constitute significant income for many Seattle tech workers. Different compensation types follow specific qualification rules:

RSU income calculation methods:

- Two-year average of vested shares converted to cash

- Current year projection based on vesting schedule

- Reduced calculation percentages for unvested future grants

- Special documentation including grant agreements and vesting schedules

Brokers familiar with tech compensation work directly with HR departments to obtain necessary verification and structure income calculations favorably.

Bonus and Variable Income

Performance bonuses and variable compensation require two-year history for qualification, but brokers can maximize impact through:

- Averaging calculations that smooth year-over-year variations

- Trend analysis showing consistent or increasing bonus patterns

- Employer verification letters documenting likelihood of continuation

- Strategic timing of applications after bonus payments appear in bank statements

Debt-to-Income Optimization

High earners often carry significant student loans, auto financing, or investment property debt. Brokers optimize qualifying ratios by:

- Structuring down payments to improve loan-to-value ratios and reduce PMI

- Timing payoffs of small debts before application submission

- Removing authorized user accounts that don't represent actual obligations

- Documenting rental income from investment properties to offset mortgage debt

Common Broker Selection Mistakes

Seattle homebuyers occasionally choose mortgage professionals based on factors that don't predict successful outcomes. Avoid these common errors:

Focusing Exclusively on Advertised Rates

Teaser rates without context regarding fees, points, and closing costs mislead borrowers. Legal resources emphasize the importance of comparing complete Loan Estimates rather than headline rates.

Better evaluation criteria:

- Total cash required at closing

- Monthly payment amounts including taxes and insurance

- Annual percentage rate (APR) reflecting true borrowing cost

- Total interest paid over expected holding period

Prioritizing Personal Relationships Over Expertise

Working with a friend or family member seems appealing but often compromises results. Professional competence matters more than personal connections when securing optimal financing.

Ignoring Licensing and Credentials

All mortgage brokers must hold state licenses (Nationwide Mortgage Licensing System registration) and comply with continuing education requirements. Verify credentials through state regulatory websites before engaging services.

Assuming All Brokers Access Identical Programs

Broker partnerships vary significantly. Some maintain relationships with dozens of lenders while others work primarily with three or four. Ask specifically which lenders a broker accesses for your loan profile.

Market Conditions and Timing Strategies

Seattle's real estate cycles create distinct advantages for working with knowledgeable home loan mortgage broker professionals who recognize opportunity windows.

Refinance Opportunities

Interest rate fluctuations create periodic refinancing opportunities for existing homeowners in Shoreline and surrounding communities. Brokers monitor when refinancing makes financial sense based on:

- Rate improvement threshold typically 0.5% to 0.75% reduction minimum

- Break-even analysis comparing closing costs against monthly savings

- Cash-out strategies accessing equity for home improvements or debt consolidation

- Loan term optimization shifting from 30-year to 15-year mortgages when affordable

Purchase Market Strategies

Multiple offer scenarios remain common across desirable Seattle neighborhoods. Brokers strengthen purchase offers through:

Pre-underwritten approvals demonstrating verified income and assets beyond basic pre-qualification

Appraisal waiver eligibility reducing contingency periods for conforming loans on properties with strong automated valuation models

Quick-close capabilities leveraging lender relationships to compress timelines to 10-14 days when needed

Earnest money strategies structuring deposits to demonstrate commitment while protecting buyer interests

Understanding home buying strategies specific to competitive markets helps buyers succeed where others fail.

Documentation Requirements and Organization

Thorough preparation accelerates underwriting and prevents last-minute scrambles. Your home loan mortgage broker will request comprehensive documentation across multiple financial categories.

Income Documentation Standards

Employment verification extends beyond simple pay stubs. Expect to provide:

- Salary employees: Recent pay stubs covering 30 days, W-2s for two years, verbal verification of employment

- Self-employed borrowers: Personal and business tax returns for two years, year-to-date profit and loss, business license

- Commission earners: Two-year history, employer verification of continuation likelihood

- Rental property owners: Lease agreements, tax returns showing rental income, property management statements

Asset Documentation Depth

Lenders verify both down payment sources and reserve requirements. Bank and investment statements must show:

- Two-month transaction history for all accounts

- Large deposit explanations for any single deposits exceeding 25% of monthly income

- Source and seasoning for gift funds from family members

- Retirement account statements documenting additional reserves

- Stock portfolio documentation for publicly traded holdings

Credit Profile Components

Beyond credit scores, underwriters analyze:

- Payment history patterns across all tradelines

- Credit utilization percentages on revolving accounts

- Recent credit inquiries indicating other debt applications

- Public records including judgments, liens, or bankruptcies

- Collection accounts requiring payment or explanation

Regulatory Protections and Consumer Rights

Federal and state regulations govern mortgage broker conduct, protecting borrowers through disclosure requirements and fair lending standards.

Loan Estimate Disclosures

Within three business days of application, brokers must provide standardized Loan Estimates showing:

- Estimated interest rate and monthly payment

- Total closing costs broken into specific categories

- Cash required at closing including down payment and fees

- Comparison features for shopping multiple offers

The CFPB’s comparison tool helps borrowers evaluate multiple Loan Estimates side by side.

Fair Lending Compliance

Mortgage professionals must follow Equal Credit Opportunity Act provisions prohibiting discrimination based on:

- Race, color, or national origin

- Sex or marital status

- Religion

- Age (provided applicant has legal capacity)

- Public assistance income sources

Right to Shop Services

Borrowers control selection of certain settlement services including title insurance, homeowner's insurance, and home inspections. Brokers provide recommendations but cannot mandate specific service providers for these categories.

Selecting the right home loan mortgage broker fundamentally impacts your financing success, from initial qualification through closing and beyond. Whether you're purchasing your first home in Mill Creek, refinancing in Everett, or securing jumbo financing for a luxury property in Bellevue, experienced broker guidance navigates the complexity of modern mortgage markets. Keith Akada at Mortgage Reel brings over 25 years of expertise to Seattle-area homebuyers, specializing in tech compensation qualification, competitive rate shopping, and streamlined closings as fast as 9 business days-helping you secure optimal financing with confidence and clarity throughout the process.