Understanding conventional loans down payment requirements is essential for homebuyers navigating Seattle's competitive real estate market in 2026. Whether you're a tech professional at Amazon or Microsoft, a first-time buyer in Shoreline, or someone upgrading in Bellevue, the amount you put down affects your interest rate, monthly payment, and whether you'll pay private mortgage insurance. With median home prices in the Greater Seattle area remaining elevated, knowing your down payment options helps you make strategic decisions that align with your financial goals and homeownership timeline.

Minimum Down Payment Requirements for Conventional Loans

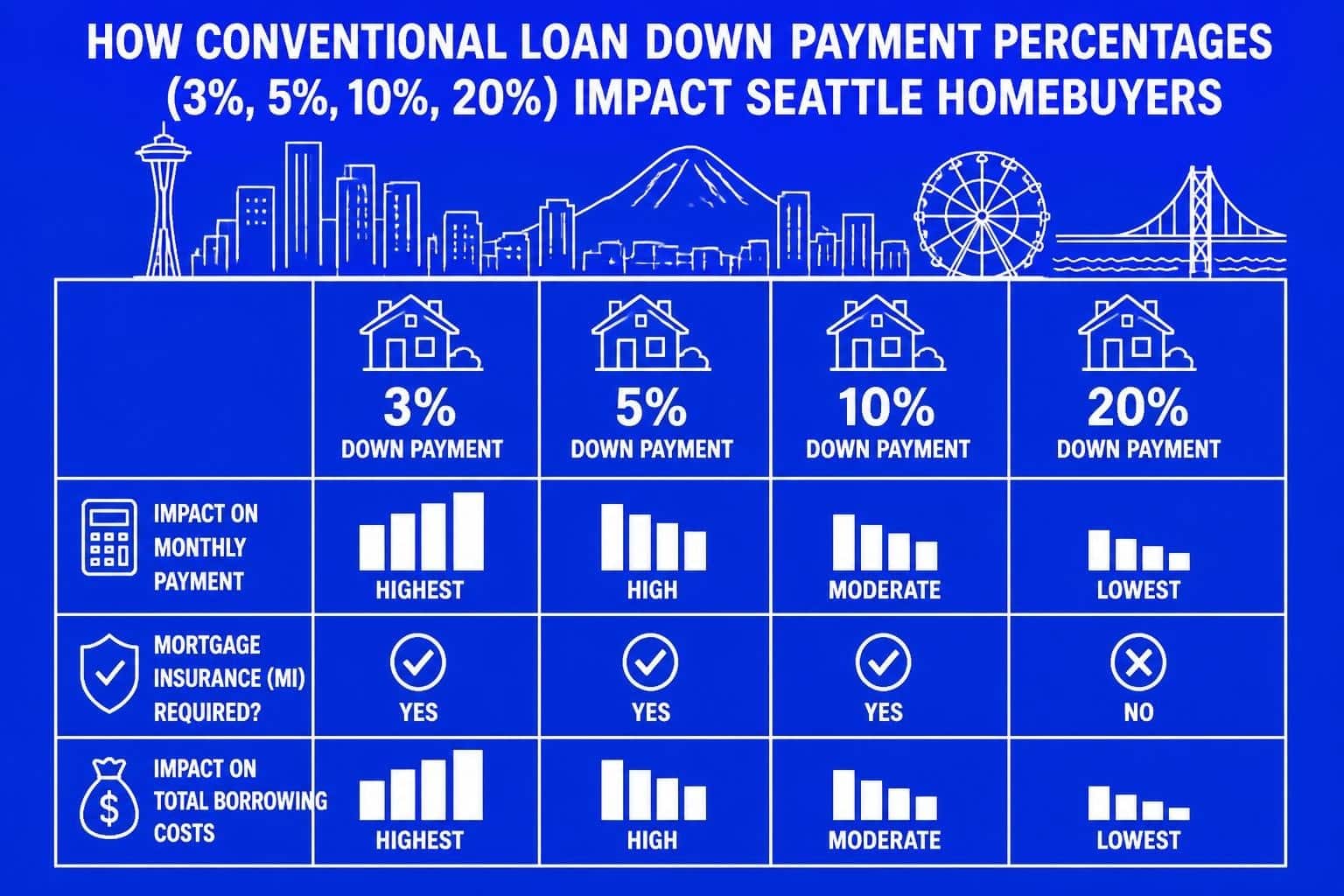

The conventional loans down payment minimum starts at just 3% for qualified borrowers, contrary to the widespread belief that 20% is always required. This lower threshold makes homeownership accessible to buyers who have strong credit and stable income but haven't yet accumulated a substantial savings cushion.

3% Down Payment Programs

First-time homebuyers can access conventional loan programs requiring only 3% down, making them competitive with FHA alternatives. Fannie Mae's HomeReady and Freddie Mac's Home Possible programs specifically target this market segment.

Eligibility requirements for 3% down conventional loans include:

- Credit score minimum of 620 (though 680+ strengthens approval)

- Debt-to-income ratio typically below 45%

- First-time homebuyer status or previous homeownership more than three years ago

- Property must be a primary residence

- Income limits may apply in certain high-cost areas

In Seattle, Bellevue, and Redmond, these programs provide opportunities for tech professionals early in their careers who earn solid W-2 income but haven't built significant savings. The key is demonstrating consistent employment and strong creditworthiness.

5% and 10% Down Payment Options

Buyers who don't qualify as first-time purchasers or prefer more conventional financing typically choose 5% or 10% down payments. These middle-ground options reduce monthly mortgage insurance costs while keeping more capital available for renovations, emergency funds, or investment opportunities.

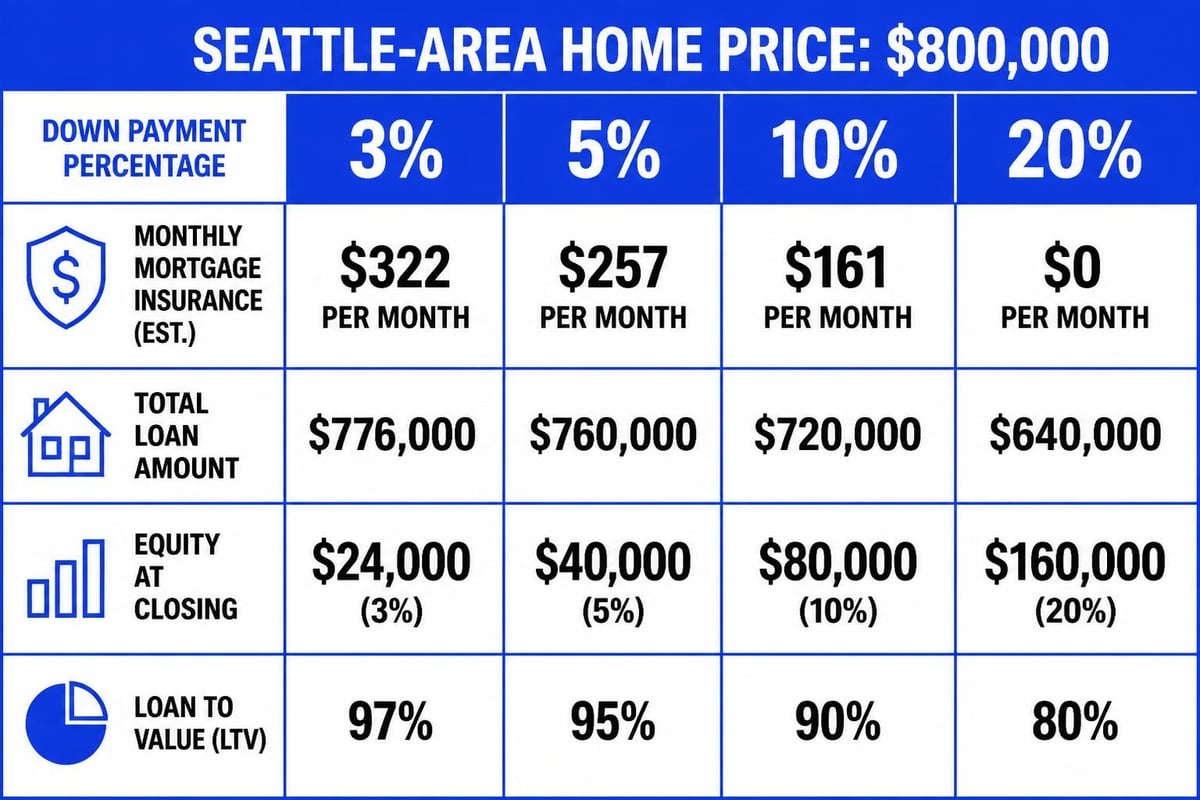

A 5% down payment on a $800,000 home in Kirkland equals $40,000, while 10% requires $80,000. The difference significantly impacts your cash reserves after closing, which matters when you're also covering moving costs, furniture, and potential property improvements.

Private Mortgage Insurance (PMI) and Down Payment Size

One of the most significant factors in your conventional loans down payment decision is private mortgage insurance. Understanding how PMI works helps you evaluate the true cost of putting less than 20% down.

PMI protects the lender if you default on your loan. It's required on conventional loans when your down payment is less than 20%, but it's not permanent-unlike the mortgage insurance premium on FHA loans.

| Down Payment | PMI Requirement | Typical Monthly PMI (on $800K loan) | When PMI Ends |

|---|---|---|---|

| 3% | Yes | $350-$500 | At 78-80% LTV |

| 5% | Yes | $325-$450 | At 78-80% LTV |

| 10% | Yes | $250-$375 | At 78-80% LTV |

| 20%+ | No | $0 | N/A |

PMI costs vary based on your credit score, loan amount, and down payment percentage. A buyer with a 740 credit score pays significantly less than someone with a 660 score, even with identical down payments.

Removing PMI from Your Conventional Loan

Unlike FHA home loan down payment options where mortgage insurance remains for the loan's life in many cases, conventional loan PMI can be eliminated once you reach 20% equity. This happens through:

- Automatic termination at 78% loan-to-value ratio

- Borrower-requested cancellation at 80% LTV with good payment history

- Home value appreciation in strong markets like Lake Forest Park or Mill Creek

- Principal reduction through regular payments or lump-sum contributions

In Seattle's historically appreciating market, homeowners who purchased with 5% down in 2022 often reached 20% equity by 2025 through price appreciation alone, allowing PMI removal without refinancing.

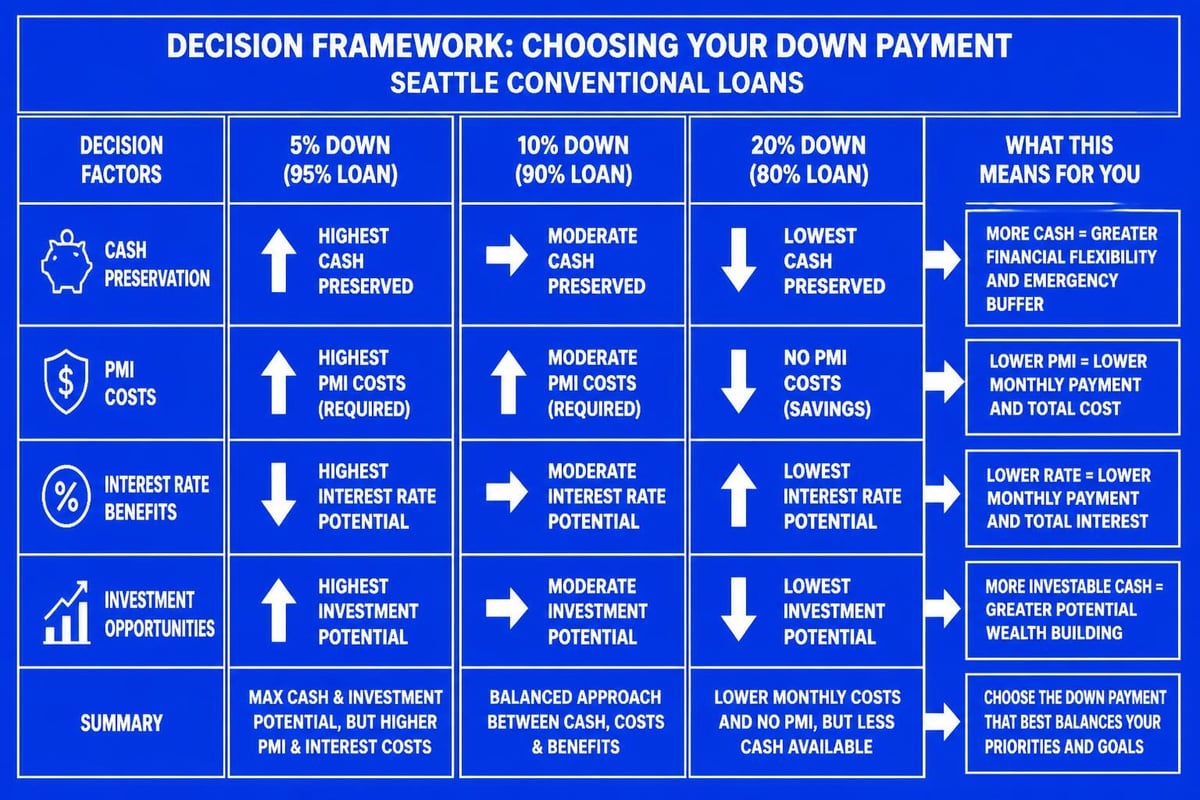

Strategic Down Payment Decisions for Seattle Homebuyers

The optimal conventional loans down payment amount depends on your complete financial picture, not just what you've saved. Tech professionals working for Seattle-area employers often face unique considerations around liquidity, stock compensation timing, and tax planning.

Weighing Cash Preservation Against Monthly Costs

Putting 20% down eliminates PMI and typically secures the best interest rate, but it also depletes savings that might serve better purposes. Consider this scenario for a $900,000 home in Bellevue:

20% Down Payment ($180,000):

- No PMI ($0/month savings)

- Lower interest rate (potentially 0.125-0.25% better)

- Reduced cash reserves for emergencies, investments, or opportunities

10% Down Payment ($90,000):

- PMI required ($300-$400/month)

- Slightly higher interest rate

- $90,000 retained for stock market investments, emergency fund, or future opportunities

If you're a Microsoft or Amazon employee expecting RSU vesting over the next 12-24 months, understanding how to qualify RSU income matters more than maximizing your down payment today. Working with a specialized Seattle mortgage broker who understands tech compensation helps you time your purchase strategically.

Down Payment Assistance Programs

Several down payment assistance programs work with conventional loans in Washington State, particularly benefiting first-time buyers in Shoreline, Lynnwood, and Everett. These programs offer grants or second mortgages to cover part of your down payment.

Washington State Housing Finance Commission provides multiple programs:

- House Key Down Payment Assistance: Up to 5% of the loan amount

- Home Advantage: Lower interest rates for qualified buyers

- House Key Opportunity: Expanded eligibility for moderate-income buyers

Income limits and purchase price caps apply to these programs, and they typically require homebuyer education courses. However, combining a 3% conventional loan with down payment assistance can reduce your out-of-pocket costs to under 1% in some cases.

For buyers exploring first-time buyer programs in Lake Forest Park, these assistance options paired with conventional financing often outperform FHA loans when considering long-term costs.

Jumbo Loan Down Payment Requirements

When your home purchase exceeds conforming loan limits ($806,500 for single-family homes in King County in 2026), you're entering jumbo loan territory. Conventional jumbo home loans carry different down payment expectations.

Standard Jumbo Down Payments

Traditional jumbo loan guidelines typically require:

- 10% minimum for loan amounts up to $1.5 million

- 15-20% for loans between $1.5-$2.5 million

- 20-30% for loans exceeding $2.5 million

These requirements vary by lender, credit profile, and debt-to-income ratio. Borrowers with exceptional credit (760+) and low DTI (under 36%) sometimes access 10% down jumbo home loans even on higher loan amounts.

The conventional loans down payment for jumbo financing reflects the increased risk lenders assume on larger mortgages without government backing. However, jumbo loans don't require PMI, which changes the calculation.

Jumbo Loans Without PMI

A significant advantage of jumbo financing is the absence of mortgage insurance, even with less than 20% down. On a $1.2 million home in Kirkland, a 10% down payment ($120,000) results in a $1.08 million loan without PMI, whereas a conforming loan of the same size would require insurance.

For tech professionals considering whether to put 10% or 20% down on a jumbo loan, the decision often hinges on investment opportunity costs and liquidity needs rather than eliminating insurance payments.

Impact of Down Payment on Interest Rates

Your conventional loans down payment directly influences your interest rate. Lenders price loans based on risk, and borrowers with more equity stake present lower default risk.

Typical rate adjustments by down payment:

- 3-5% down: Baseline rate

- 10% down: 0.125% lower than 5% down

- 15% down: 0.125-0.25% lower than 10% down

- 20%+ down: 0.125-0.375% lower than 10% down

These adjustments seem small, but on an $800,000 loan, a 0.25% rate difference equals approximately $120 monthly or $43,000 over 30 years. However, you must weigh this against opportunity costs of tying up capital.

Rate Locks and Down Payment Strategy

When working through your purchase timeline in Seattle's fast-moving market, your down payment amount should be confirmed before locking your rate. Changing your down payment percentage after rate lock can require repricing and potentially losing a favorable rate.

Professional guidance from a Seattle mortgage broker helps you model different scenarios before committing to a specific strategy. This planning becomes especially important when coordinating equity compensation vesting with your purchase timeline.

Credit Score Requirements by Down Payment Amount

Conventional loan approval standards combine credit scores with down payment amounts. Higher down payments offset lower credit scores, while exceptional credit can justify minimal down payments.

| Credit Score | Minimum Down Payment | Preferred Down Payment |

|---|---|---|

| 620-659 | 10-15% | 20% |

| 660-699 | 5% | 10% |

| 700-739 | 3-5% | 5-10% |

| 740+ | 3% | 3-5% |

These guidelines aren't absolute rules but reflect common underwriting practices. A buyer with a 680 credit score might access 3% down through HomeReady or Home Possible if income limits and property requirements align.

For Seattle homebuyers wondering about the credit score needed to buy a home, understanding how credit interacts with down payment requirements helps set realistic expectations and timelines.

Tax Implications and Opportunity Costs

Beyond monthly payments and PMI, your conventional loans down payment decision carries tax and investment considerations that matter to high-earning tech professionals.

Mortgage Interest Deduction

The 2026 tax code allows mortgage interest deduction on loans up to $750,000 for married couples filing jointly. Larger down payments reduce your loan amount and therefore your deductible interest, potentially increasing your tax liability.

On a $1 million home purchase:

- 10% down creates a $900,000 loan (full deduction)

- 30% down creates a $700,000 loan (full deduction)

Both qualify for complete interest deduction, but the monthly payment difference is substantial. This influences cash flow planning, especially for buyers in Seattle's high-tax environment.

Investment Alternative Analysis

Money used for down payments can't be invested elsewhere. Tech professionals often compare potential stock market returns against the "return" from avoiding PMI and securing better rates.

Example scenario: $100,000 additional down payment (going from 10% to 20% on a $1M home)

- Eliminates $350/month PMI ($4,200/year)

- Reduces interest rate by 0.125% (saves approximately $550/year)

- Total annual benefit: $4,750

- Effective return: 4.75% on the $100,000

If you believe your investment portfolio will return more than 4.75% annually after taxes, keeping that capital invested might outperform the down payment benefits. This calculation becomes more complex when factoring in risk tolerance, time horizon, and tax efficiency.

Working with professionals who understand both Seattle home financing and wealth management helps you make integrated decisions rather than viewing your mortgage in isolation.

Special Considerations for Tech Professionals

Seattle-area technology employees face unique advantages and challenges when determining their conventional loans down payment strategy. Stock compensation, bonus structures, and rapid career progression create opportunities that traditional mortgage guidance doesn't always address.

Qualifying RSU and Stock Income

Many lenders require two years of history before counting RSU or stock compensation toward qualifying income. However, specialized underwriting can incorporate RSU income sooner with proper documentation and vesting schedules.

This matters for down payment planning because it affects:

- Loan amount qualification: Higher qualifying income means larger loan approval

- Down payment percentage: Larger approved loans require proportionally larger down payments for the same home

- Timing decisions: Waiting for RSU vesting might provide down payment funds but delays purchase

Consider partnering with mortgage professionals experienced in tech compensation who can maximize your buying power while you decide whether to liquidate vested equity for a larger down payment or preserve it for diversification.

Bonus Income and Down Payment Timing

Year-end bonuses at Amazon, Microsoft, and Google often create optimal windows for increasing down payments. Receiving a $40,000 bonus in February that pushes you from 10% to 15% down can improve your rate and reduce PMI costs.

However, timing your closing around bonus payments requires coordination. If you're already in contract, increasing your down payment mid-process triggers additional underwriting and verification. Planning these moves before going under contract produces smoother transactions.

Jumbo Loan Qualification for Tech Buyers

Seattle tech professionals frequently need jumbo loan qualification strategies that account for variable compensation. The conventional loans down payment for jumbo financing combines with income documentation to determine approval.

Lenders evaluate:

- Base salary stability: W-2 income provides the foundation

- Equity compensation trends: Increasing RSU values strengthen applications

- Bonus consistency: Two-year averages smooth qualification calculations

- Cash reserves: Post-closing liquidity requirements increase with loan size

On a $1.8 million home in Bellevue, putting 15% down ($270,000) instead of 10% ($180,000) might not only improve your rate but also reduce the reserve requirements from 12 months to 6 months of payments.

Conventional Loans vs. Other Mortgage Types

Understanding how conventional loans down payment requirements compare to alternatives helps you select the right financing for your situation.

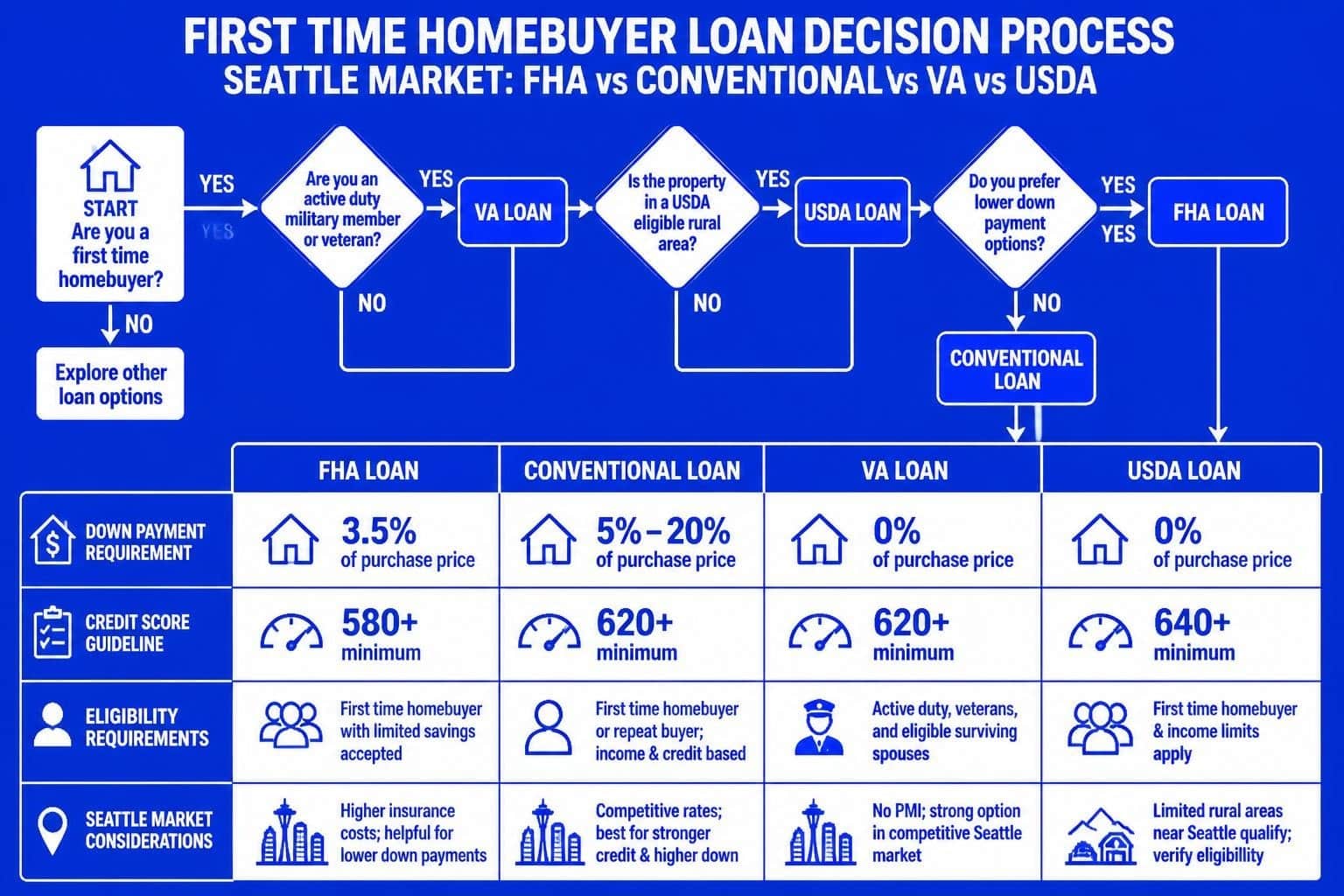

Conventional vs. FHA Down Payments

FHA loans require 3.5% down with credit scores as low as 580, seemingly competitive with conventional 3% programs. However, FHA mortgages carry both upfront and annual mortgage insurance that typically exceeds conventional PMI costs.

Key differences:

- FHA insurance remains for the loan's life (if you put less than 10% down)

- Conventional PMI drops off at 78-80% LTV

- FHA accepts lower credit scores but charges higher insurance

- Conventional loans offer better rates for borrowers with 680+ scores

For most Seattle-area buyers with decent credit, conventional home loans provide superior long-term value despite similar minimum down payments.

Conventional vs. VA Loans

Veterans and active military have access to VA loans requiring $0 down payment, which appears to outperform any conventional option. However, VA loans aren't available to most Seattle homebuyers, and they carry funding fees that effectively function as upfront costs.

For eligible veterans, VA financing typically beats conventional loans when buying under conforming limits. Above those limits, conventional jumbo products sometimes offer competitive terms, especially for buyers with substantial down payments available.

When Conventional Loans Make the Most Sense

Conventional financing excels for buyers who:

- Have credit scores above 680

- Can comfortably afford 5-10% down

- Plan to stay in the home long enough to eliminate PMI through appreciation or principal reduction

- Purchase properties above FHA loan limits

- Want flexibility in property type and condition (conventional loans accept properties FHA might reject)

The Seattle market's strong appreciation history means buyers who started with 5% down in neighborhoods like Mill Creek or Lynnwood often reach 20% equity within 3-5 years through a combination of payments and value growth.

Regional Market Considerations for Seattle-Area Buyers

Local market dynamics influence your conventional loans down payment strategy in ways that national guidelines don't capture. Seattle, Shoreline, Bellevue, Redmond, Kirkland, Lake Forest Park, Lynnwood, Mill Creek, and Everett each present distinct characteristics.

Competitive Offer Environments

In multiple-offer situations common across the Seattle metro, your down payment percentage sends signals to sellers about deal strength. A 20% down conventional offer typically appears more secure than 3% down, even when both buyers are equally qualified.

Sellers and their agents perceive lower default risk with higher down payments, making these offers more attractive in competitive scenarios. This doesn't mean you should overextend your down payment, but understanding the perception helps you compete strategically.

Appraisal Contingency Strategies

When you put 20% or more down on a conventional loan, you gain flexibility around appraisal contingencies. If the home appraises low, you can more easily cover the gap with additional down payment rather than renegotiating or walking away.

On a $950,000 purchase in Redmond that appraises at $920,000:

- A buyer with 10% down ($95,000) would need to find an extra $30,000 or renegotiate

- A buyer planning 20% down ($190,000) can adjust to $220,000 (23.2% down) and proceed

This flexibility often proves valuable in Seattle's fast-moving market where slight appraisal variances occur regularly. Some buyers choose slightly larger down payments specifically to create this buffer.

Appreciation and Equity Building

Historical appreciation rates in the Greater Seattle area have averaged 6-8% annually over the past decade, though individual years vary considerably. This growth rate dramatically affects how quickly you eliminate PMI and build equity.

A buyer who purchased a $700,000 home in Lake Forest Park in 2023 with 5% down:

- Started with $35,000 equity (5%)

- After three years at 6% appreciation and regular payments: approximately $168,000 equity (21.5%)

- PMI eliminated, saving $250-350 monthly going forward

This equity acceleration means the long-term cost of starting with a smaller conventional loans down payment is often lower than static calculations suggest, especially in strong markets.

Documentation and Verification Requirements

Lenders scrutinize down payment sources more carefully than ever, particularly on loans with minimal equity. Understanding documentation requirements helps you prepare properly and avoid delays.

Acceptable Down Payment Sources

Conventional loan guidelines permit down payment funds from:

- Personal savings: Checking, savings, money market accounts

- Investment accounts: Stocks, bonds, mutual funds (must be liquidated and seasoned)

- Retirement accounts: 401(k) loans or withdrawals (with consideration for penalties)

- Gift funds: From family members with proper documentation

- Down payment assistance: Approved programs only

- Sale of previous home: Documented through closing statements

Each source requires specific documentation. Savings accounts need two months of statements showing the funds existed before application. Gift funds require gift letters confirming the money doesn't need to be repaid.

Sourcing and Seasoning Rules

"Seasoning" refers to how long funds have been in your accounts. Large deposits within 60 days of application trigger inquiries. If you receive a $50,000 bonus and deposit it two weeks before applying, expect to document its source thoroughly.

Best practices for down payment preparation:

- Accumulate funds in accounts three+ months before applying

- Avoid moving money between accounts unnecessarily

- Document any large deposits with clear paper trails

- Keep gift funds separate until needed at closing

- Maintain minimum required reserves after closing

Seattle tech professionals liquidating RSUs for down payments should complete these transactions well before starting their home search, allowing time for funds to season properly. Cash transactions and cryptocurrency conversions receive extra scrutiny, requiring clear documentation trails.

Closing Costs and Total Cash Needed

Your conventional loans down payment represents only part of the total cash required at closing. Understanding the complete picture prevents surprises and helps you budget accurately.

Typical Closing Cost Ranges

Closing costs on conventional loans typically run 2-5% of the purchase price, varying by location, loan amount, and specific services required.

Common closing costs in Seattle-area transactions:

- Origination and underwriting fees: $1,500-$3,000

- Appraisal: $600-$900

- Title insurance and escrow: $2,000-$4,000

- Property taxes and insurance prepayments: $3,000-$8,000

- Recording fees and transfer taxes: $1,000-$3,000

- Survey and inspection costs: $500-$1,500

On a $850,000 home in Kirkland, total closing costs might reach $25,000-$35,000 beyond your down payment. Some costs can be rolled into your loan amount (increasing it slightly), while others must be paid in cash.

Reserve Requirements

Lenders require proof of cash reserves after closing, typically 2-6 months of mortgage payments depending on loan amount, down payment, and property type. These reserves cannot include your down payment or closing costs.

For a jumbo home loan of $1.5 million with 10% down, you might need:

- $150,000 down payment

- $40,000 closing costs

- $30,000 reserves (6 months × $5,000 payment)

- Total: $220,000 liquid funds

Planning for these complete requirements prevents situations where you have enough for the down payment but insufficient total liquidity for approval. This is where working with businesses specializing in lead generation helps real estate professionals connect buyers with appropriate resources before they begin searching.

Making Your Down Payment Decision

Selecting your conventional loans down payment amount requires balancing multiple factors specific to your financial situation, goals, and timeline. There's rarely a single "correct" answer that applies to everyone.

Key Decision Factors

Financial considerations:

- Total liquid savings available

- Emergency fund adequacy (maintain 6-12 months expenses)

- Investment opportunity costs

- Tax implications and deductions

- Income stability and growth trajectory

Lifestyle factors:

- How long you plan to stay in the home

- Renovation or improvement plans requiring capital

- Other major expenses on the horizon (education, vehicles, etc.)

- Risk tolerance and comfort with debt

Market conditions:

- Competitive intensity in your target neighborhoods

- Interest rate environment and trends

- Local appreciation expectations

- Seasonal timing considerations

Seattle homebuyers often benefit from exploring their complete mortgage types landscape before finalizing down payment strategy, as different loan products offer varying flexibility.

Scenario Planning

Run multiple scenarios with actual numbers for your situation:

- Minimum down (3-5%): Maximize leverage, retain capital, accept PMI

- Middle ground (10-15%): Balance monthly costs with cash preservation

- Conventional wisdom (20%): Eliminate PMI, best rates, maximum equity

Calculate the total five-year cost of each approach, including opportunity costs of deployed capital. This longer-term view often reveals surprising insights that monthly payment comparisons miss.

For example, if you're a professional with growing income who expects equity compensation to increase substantially, starting with 5% down and reinvesting the difference might build more wealth than maximizing your initial down payment, even accounting for PMI costs. Real estate professionals like Steven Cirillo who work with investors understand these trade-offs intimately.

Professional Guidance Value

The complexity of optimizing your conventional loans down payment strategy justifies working with mortgage professionals who understand both the technical lending requirements and the broader financial planning implications. Generic advice rarely accounts for your specific compensation structure, tax situation, and goals.

Questions to discuss with your mortgage advisor:

- How does my equity compensation affect qualifying income vs. down payment sourcing?

- What's my total cash requirement including reserves, not just down payment?

- How quickly might I eliminate PMI based on local appreciation trends?

- Should I time my closing around bonus or vesting schedules?

- What down payment percentage makes my offer most competitive without overextending?

These conversations become especially valuable for buyers navigating how to buy a home in complex markets like Seattle, where timing, strategy, and execution all influence outcomes.

Choosing the right conventional loans down payment requires understanding minimum requirements, weighing PMI costs against cash preservation, and aligning your mortgage strategy with broader financial goals specific to Seattle's dynamic market. Whether you're putting 3% down as a first-time buyer in Lynnwood or 15% down on a jumbo loan in Bellevue, your decision impacts both immediate affordability and long-term wealth building. Keith Akada at Mortgage Reel brings over 25 years of experience helping Seattle-area homebuyers navigate these decisions with clarity and confidence, specializing in qualifying tech professionals' equity compensation to maximize buying power while maintaining financial flexibility.