The ability to mortgage loan apply online has transformed how Seattle homebuyers and homeowners secure financing in 2026. Digital mortgage applications now offer unprecedented convenience, speed, and transparency throughout the lending process. Whether you're purchasing your first home in Shoreline, refinancing in Bellevue, or securing a jumbo loan in Kirkland, understanding how online mortgage applications work empowers you to navigate the process with confidence and close faster in competitive Pacific Northwest markets.

How Online Mortgage Applications Work in 2026

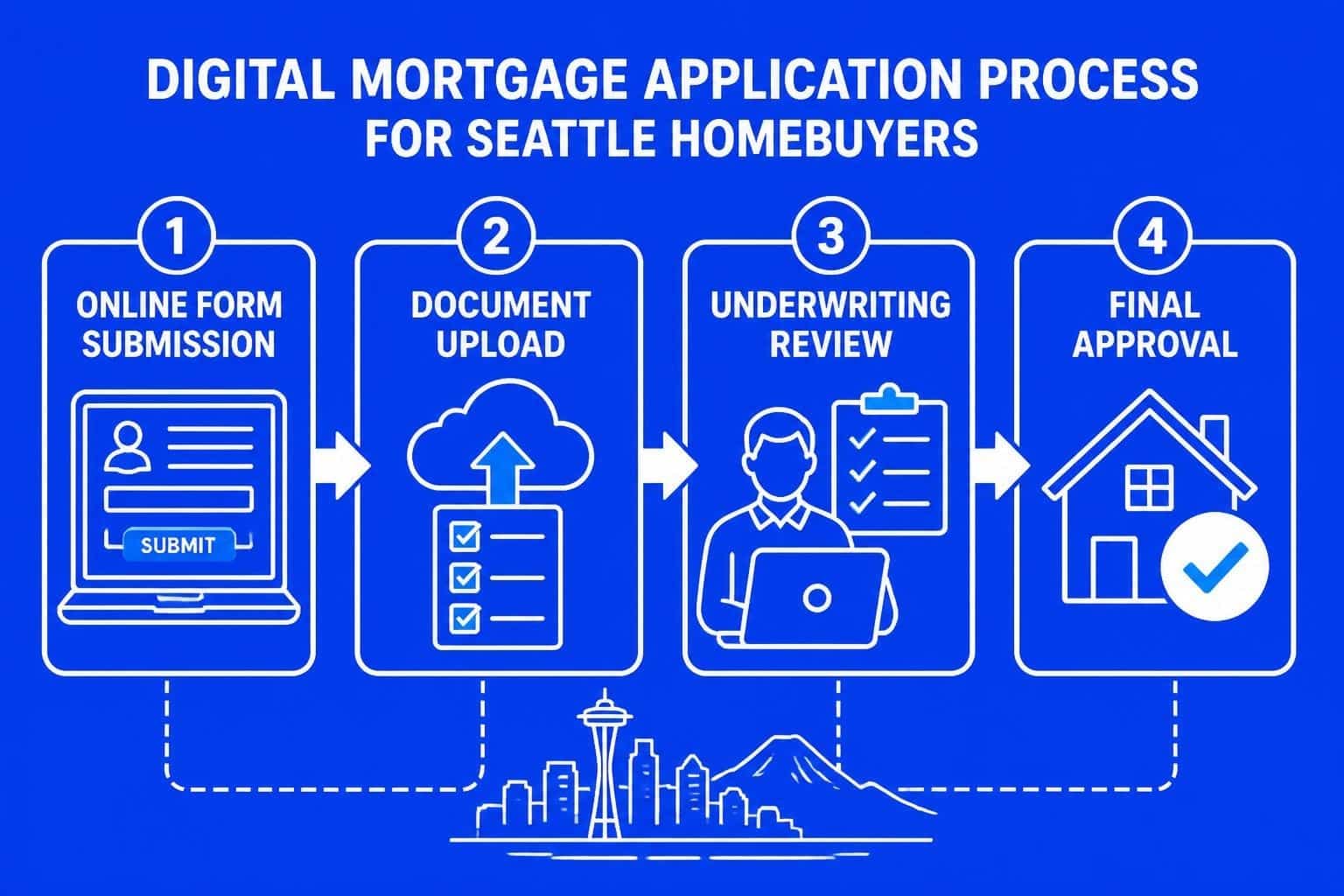

Digital mortgage platforms have evolved significantly, allowing borrowers to complete the entire application process from initial submission through final approval without visiting a physical office. When you mortgage loan apply online, you're accessing sophisticated systems that connect directly to underwriting teams, document verification services, and loan processing workflows.

The typical online application process includes:

- Completing a comprehensive digital application form with personal and financial information

- Uploading required documents through secure portals

- Receiving automated updates on application status

- Communicating with loan officers through messaging platforms or video calls

- E-signing disclosures and final documents electronically

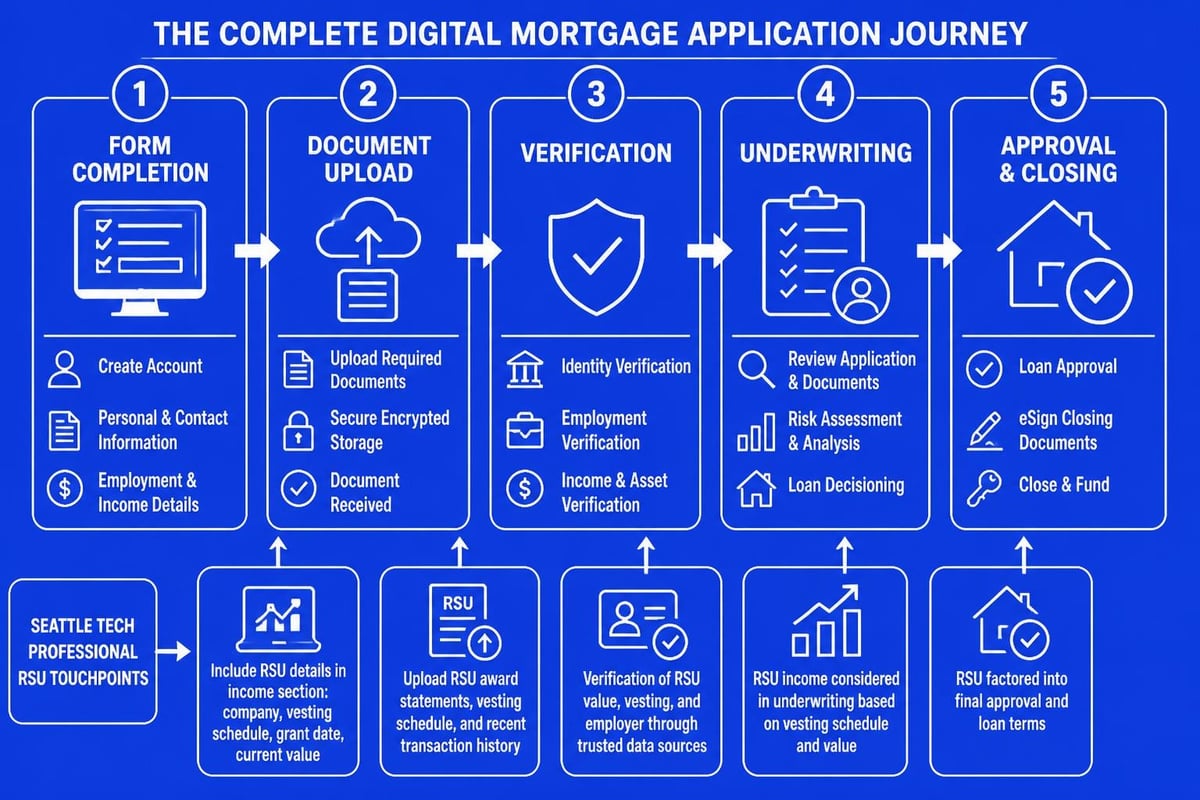

Tech professionals working at Amazon, Microsoft, and Google in the Seattle area particularly benefit from online applications because they can upload stock compensation documentation, RSU vesting schedules, and bonus letters directly into the system. This streamlined approach often reduces processing time significantly.

Document Preparation Before You Apply

Success with online mortgage applications begins with proper document preparation. According to the Consumer Financial Protection Bureau’s mortgage application guidance, having complete documentation ready before starting your application prevents delays and accelerates approval timelines.

| Document Category | Standard Requirements | Seattle Tech Professional Additions |

|---|---|---|

| Income Verification | W-2s (2 years), pay stubs (30 days) | RSU vesting schedules, stock award letters |

| Asset Documentation | Bank statements (2 months) | Investment account statements showing stock sales |

| Employment Verification | Employer contact information | Equity compensation documentation |

| Tax Returns | 1040s with schedules (2 years) | Schedule D for capital gains reporting |

For those exploring first-time home buyer programs, additional documentation regarding down payment assistance or educational certificates may be required upfront.

Advantages of Digital Mortgage Applications

The shift to online platforms delivers measurable benefits for borrowers throughout the Greater Seattle area. When you mortgage loan apply online, you gain control over timing, reduce paperwork handling, and receive faster responses than traditional paper-based processes.

Speed and Efficiency

Digital applications eliminate mail delays and manual data entry errors. Advanced lenders can now close loans in as few as nine business days when borrowers submit complete documentation upfront. This speed proves particularly valuable in competitive markets like Bellevue and Redmond, where purchase agreements often include tight financing contingency periods.

24/7 Accessibility

Online platforms allow you to work on your application during hours that fit your schedule. Seattle tech workers managing demanding project deadlines can upload documents at midnight or review disclosures during lunch breaks without coordinating office appointments.

Key accessibility benefits include:

- Starting applications outside traditional business hours

- Uploading documents as you receive them from employers or accountants

- Reviewing loan estimates and disclosures at your own pace

- Tracking application progress through real-time dashboards

Enhanced Transparency

Modern online mortgage platforms provide clear visibility into every stage of the lending process. Borrowers can see exactly which documents are pending, when underwriting reviews occur, and what conditions need clearing before closing.

Understanding Online Application Security

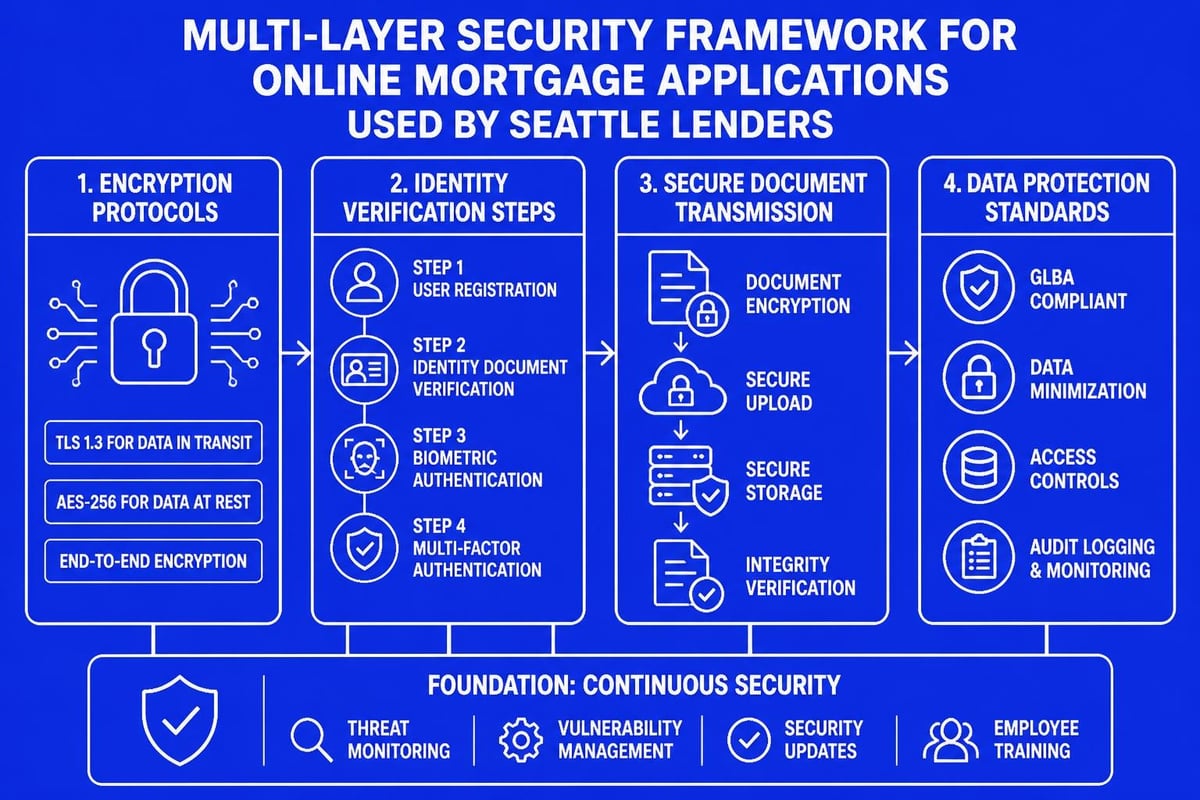

Security concerns represent the primary hesitation many borrowers express when deciding to mortgage loan apply online. Reputable lenders implement multiple layers of protection to safeguard sensitive financial information throughout the digital application process.

Encryption and Data Protection

Leading mortgage platforms use bank-level 256-bit encryption to protect data transmission. This means information traveling between your device and the lender's servers remains unreadable to unauthorized parties. Additionally, documents stored in application portals reside on servers with comprehensive security protocols including firewalls, intrusion detection, and regular security audits.

Identity Verification Processes

Before accessing online mortgage portals, borrowers typically complete multi-factor authentication requiring:

- Email confirmation links

- Mobile phone verification codes

- Knowledge-based authentication questions based on credit history

- Government-issued ID uploads for comparison

These verification steps prevent fraudulent applications while ensuring legitimate borrowers maintain exclusive access to their mortgage files.

Comparing Loan Offers Through Online Platforms

One strategic advantage of digital applications involves the ease of shopping for mortgage offers from multiple lenders. In 2026, borrowers can mortgage loan apply online with several institutions within a short timeframe without negatively impacting credit scores, provided applications occur within a 45-day window.

Rate and Fee Comparison

When evaluating online mortgage offers for properties in Lynnwood, Mill Creek, or Everett, focus on the following comparison points:

| Comparison Factor | What to Evaluate | Why It Matters |

|---|---|---|

| Interest Rate | Base rate offered | Determines monthly payment amount |

| Annual Percentage Rate (APR) | Total cost including fees | Reflects true loan cost over time |

| Origination Fees | Lender charges for processing | Impacts cash needed at closing |

| Discount Points | Optional upfront payment for lower rate | Affects break-even timeline |

| Closing Timeline | Days from application to funding | Critical in competitive markets |

The Consumer Financial Protection Bureau’s loan comparison tools provide standardized formats for evaluating these factors across different lenders.

Understanding Loan Estimates

Federal regulations require lenders to provide a standardized Loan Estimate within three business days of receiving your online application. This document clearly outlines loan terms, projected payments, and closing costs in a consistent format designed for easy comparison.

Tech professionals in Seattle pursuing jumbo loans should pay particular attention to how lenders calculate qualifying income from stock compensation, as methodologies vary and directly impact loan amounts.

Navigating the Online Application Form

The initial online application form requests detailed information across several categories. Understanding what information you'll need beforehand streamlines completion and reduces errors that could delay processing.

Personal and Property Information

When you mortgage loan apply online, expect to provide:

- Full legal name, Social Security number, and date of birth

- Current address and two-year residence history

- Property address and intended use (primary residence, investment, second home)

- Estimated property value or purchase price

- Desired loan amount and loan type

Financial Profile Details

Lenders require comprehensive financial information to assess your ability to repay the mortgage. This section typically includes:

- Current employment information including employer name, position, and length of employment

- Gross monthly income from all sources

- Additional income from bonuses, commissions, or rental properties

- Monthly debt obligations including car loans, student loans, and credit cards

- Asset information including checking, savings, investment, and retirement accounts

For Seattle homebuyers working in technology, accurately reporting income from RSUs requires understanding how lenders calculate qualifying income from equity compensation. Most lenders average vested stock income over a two-year period, requiring documentation of historical vesting and future vesting schedules.

Working with Loan Officers During Online Applications

Despite the digital nature of modern mortgage applications, experienced loan officers remain essential to successful outcomes. When you mortgage loan apply online through established brokerages, you gain access to professional guidance throughout the process while enjoying the convenience of digital tools.

Communication Options

Professional mortgage brokers offer multiple communication channels to support online applicants:

- Secure messaging within application portals for document-related questions

- Email correspondence for detailed strategy discussions

- Phone consultations for complex scenarios

- Video meetings for document review and closing preparation

This hybrid approach combines digital efficiency with personalized expertise, particularly valuable for first-time buyers navigating unfamiliar territory.

Strategic Guidance on Loan Programs

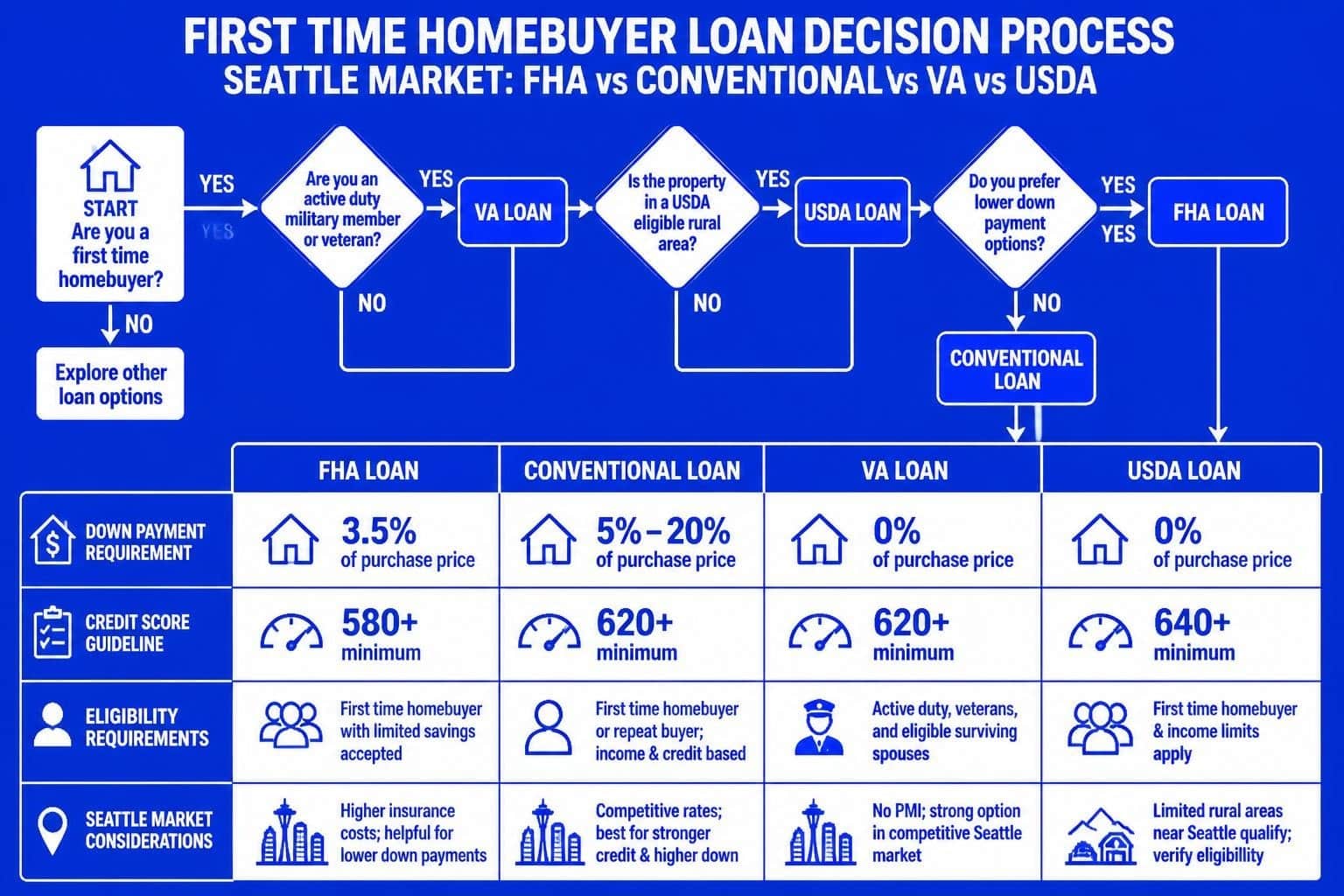

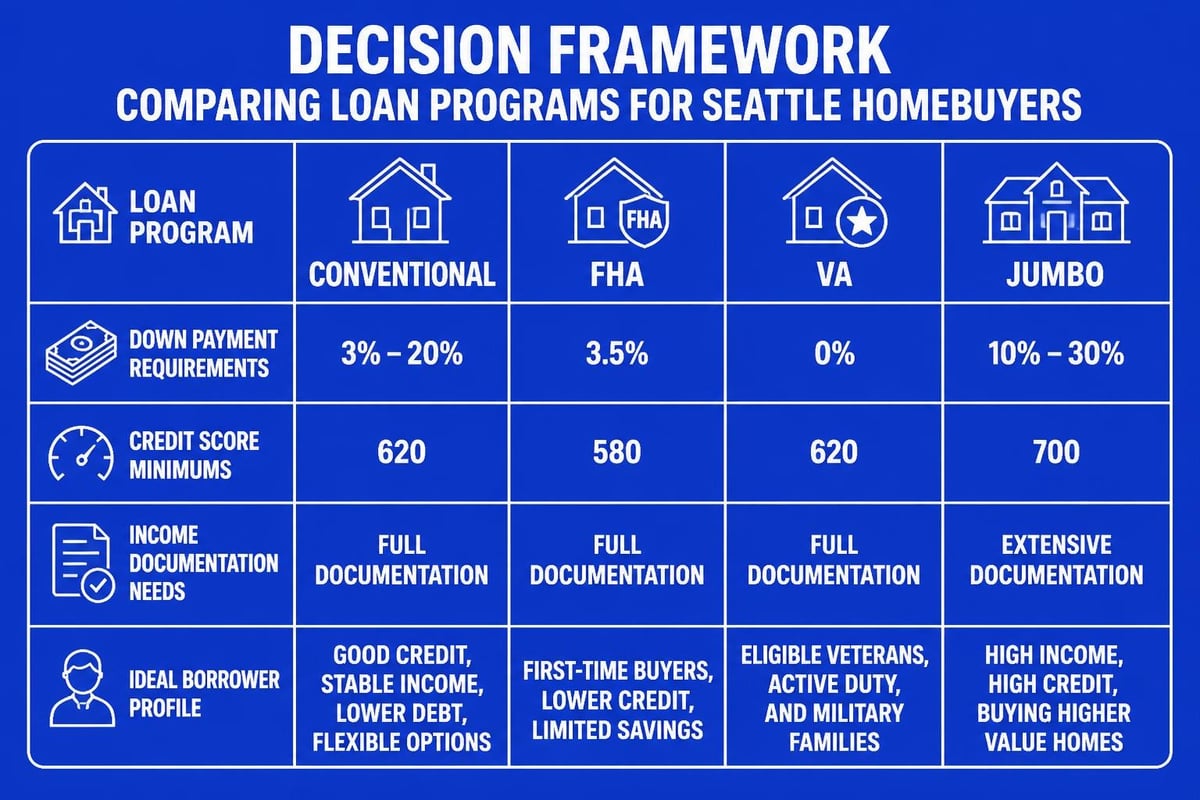

Experienced brokers help Seattle-area borrowers select optimal loan programs based on individual circumstances. Options include:

- Conventional loans with competitive rates for borrowers with strong credit and stable income

- FHA loans offering lower down payment requirements for qualifying buyers

- VA loans providing zero-down financing for eligible veterans and service members

- Jumbo loans for high-value properties exceeding conforming loan limits in expensive Seattle neighborhoods

Understanding the mortgage lending process helps borrowers make informed decisions aligned with long-term financial goals.

Timeline Expectations for Online Applications

Understanding realistic timelines helps borrowers plan effectively when they mortgage loan apply online. While digital platforms accelerate many aspects of the process, certain steps require specific timeframes regardless of technology.

Initial Review and Loan Estimate: 1-3 Business Days

After submitting your online application, lenders conduct an initial review of your credit profile and provided information. Federal law requires delivery of the Loan Estimate within three business days, though many digital-first lenders provide this document within 24 hours for complete applications.

Document Collection and Verification: 3-7 Business Days

The timeline for this phase depends heavily on borrower responsiveness. Uploading complete, legible documents immediately upon request significantly reduces this window. Common delays occur when:

- Bank statements don't cover required periods

- Pay stubs are outdated

- Tax returns lack necessary schedules

- Asset documentation doesn't clearly show source of funds

Underwriting Review: 5-10 Business Days

During underwriting, specialists analyze your complete financial profile against lending guidelines. Automated underwriting systems can provide initial decisions within minutes for straightforward applications, but human underwriters review most files to address nuances like stock compensation calculations or complex employment situations common among Seattle tech professionals.

Appraisal and Title Work: 7-14 Business Days

These third-party services operate on independent timelines. Appraisal scheduling depends on appraiser availability in specific Seattle neighborhoods, while title companies research property ownership history and lien status. In hot markets like Kirkland or Bellevue, appraisal backlogs can extend timelines during peak buying seasons.

Clear to Close and Funding: 1-3 Business Days

Once all conditions are satisfied, lenders issue "clear to close" status. Final document preparation, signing coordination, and funding typically occur within three days, with advanced lenders capable of same-day funding when circumstances require expedited closing.

Common Mistakes to Avoid with Online Applications

Even with user-friendly platforms, borrowers sometimes make errors that complicate or delay their mortgage approval. Awareness of common pitfalls helps you navigate the process smoothly when you mortgage loan apply online.

Incomplete or Inconsistent Information

Discrepancies between your application and supporting documents raise red flags for underwriters. If you report $120,000 annual income but your W-2 shows $115,000, underwriters will require explanation and documentation reconciling the difference.

Best practices include:

- Using exact figures from official documents

- Double-checking employment dates against pay stubs

- Ensuring addresses match credit report information

- Reporting all debts visible on credit reports, even if paying off before closing

Making Major Financial Changes During Processing

Large purchases, new credit applications, or job changes during the mortgage process can derail approvals. Lenders verify employment and re-pull credit reports before closing, and significant changes may require re-underwriting or could invalidate approvals.

Avoid these actions between application and closing:

- Opening new credit cards or loans

- Making large purchases on credit

- Co-signing loans for others

- Changing jobs or employment status

- Moving money between accounts without documentation

Ignoring Lender Communication

Online platforms send automated notifications when documents are requested or status changes occur. Failing to respond promptly extends timelines and may cause purchase agreements to fall through in time-sensitive transactions.

Special Considerations for Seattle Tech Professionals

The concentration of major technology employers in the Seattle metropolitan area creates unique mortgage scenarios that benefit from specialized expertise when borrowers mortgage loan apply online. Understanding how lenders evaluate stock-based compensation ensures you qualify for appropriate loan amounts.

RSU and Stock Option Qualification

Lenders typically require two-year histories of restricted stock unit vesting before including this income in qualification calculations. The methodology involves:

- Averaging RSU income over the most recent 24 months

- Applying a percentage of future scheduled vesting (often 70-100% depending on vesting certainty)

- Documenting grant schedules and historical vesting patterns

- Providing employer letters confirming ongoing compensation structure

For Microsoft, Amazon, or Google employees pursuing jumbo home loans, properly documented stock compensation can significantly increase purchasing power in expensive Eastside markets.

Bonus and Commission Income

Technology professionals often receive substantial annual bonuses or performance-based compensation. Lenders typically average this income over two years, requiring:

- Tax returns showing bonus receipt history

- Year-to-date pay stubs reflecting current year bonuses

- Employer documentation confirming bonus structure

- Evidence of income stability or increasing trend

Multiple Income Sources

Many Seattle tech workers supplement primary employment with consulting, rental properties, or investment income. When you mortgage loan apply online, clearly documenting these additional income streams requires:

| Income Type | Required Documentation | Typical Qualifying Percentage |

|---|---|---|

| Rental Income | Leases, tax Schedule E | 75% of gross rent minus PITIA |

| Self-Employment | 2 years tax returns, P&L | Net income after expenses |

| Investment Income | 1099s, account statements | 2-year average |

| Passive Income | K-1s, partnership agreements | Varies by source stability |

Mobile Applications and On-the-Go Access

Modern mortgage platforms offer full-featured mobile applications allowing borrowers to manage every aspect of their loan file from smartphones or tablets. This mobility particularly benefits busy professionals in Shoreline, Lake Forest Park, and throughout the Greater Seattle area.

Document Upload Capabilities

Mobile apps enable instant document upload using device cameras. Rather than scanning documents at home or work, borrowers can photograph required paperwork and upload directly to secure portals. Advanced apps include:

- Edge detection to automatically crop document borders

- Image enhancement for clarity

- Multi-page PDF creation from multiple photos

- Instant upload confirmation and status updates

Real-Time Notifications

Push notifications keep borrowers informed about critical milestones and required actions. Whether waiting for appraisal results or clearing final conditions, mobile alerts ensure you respond quickly to lender requests regardless of location.

Refinance Applications Through Online Platforms

Homeowners seeking to refinance existing mortgages find online applications particularly convenient, as they already possess detailed property and financial information. When you mortgage loan apply online for refinancing, the process often moves faster than purchase applications due to existing homeownership documentation.

Rate-and-Term Refinancing

This common refinance strategy involves replacing your current mortgage with a new loan featuring better terms, such as lower interest rates or different loan duration. Online applications for rate-and-term refinances require:

- Current mortgage statement

- Property insurance documentation

- Homeowners association information (if applicable)

- Standard income and asset documentation

Borrowers interested in exploring VA refinance options can complete streamlined applications with reduced documentation requirements when refinancing existing VA loans.

Cash-Out Refinancing

Homeowners with substantial equity can access funds through cash-out refinancing while potentially securing better rates than home equity loans. These applications require:

- Recent appraisal or broker price opinion

- Detailed explanation of fund usage

- Complete financial profile documentation

- Verification of property condition

Integration with Real Estate Platforms

Leading online mortgage applications now integrate directly with real estate listing platforms and transaction management systems used throughout Seattle markets. This connectivity streamlines the homebuying process when you mortgage loan apply online simultaneously with house hunting.

Pre-Approval Letter Generation

Digital platforms can generate pre-approval letters within hours of completing online applications, providing Seattle homebuyers with competitive advantages in multiple-offer situations. These letters demonstrate serious intent and verified financial capacity to sellers and listing agents.

Offer-to-Close Coordination

Advanced integration allows real estate agents, loan officers, title companies, and escrow officers to access relevant information through connected platforms. This coordination reduces duplicate requests and ensures all parties work from current information throughout the transaction.

Evaluating Online Lender Reviews and Reputation

Before you mortgage loan apply online with any lender, research their reputation through multiple review platforms and regulatory resources. For Seattle-area borrowers, understanding lender performance in local markets provides valuable insight beyond national ratings.

Key Evaluation Criteria

- Closing timeline reliability: Do borrowers consistently close on promised dates?

- Communication quality: Are borrowers kept informed throughout the process?

- Problem resolution: How does the lender handle unexpected issues?

- Local market knowledge: Does the lender understand Seattle-area property types and market conditions?

- Rate competitiveness: Are rates and fees aligned with or better than market averages?

Working with experienced local professionals ensures you receive guidance tailored to Pacific Northwest real estate markets and can leverage established relationships with appraisers, title companies, and underwriters familiar with regional property characteristics.

Future Developments in Online Mortgage Applications

The mortgage industry continues evolving toward increased automation and improved borrower experiences. Understanding emerging trends helps Seattle homebuyers anticipate future capabilities when they mortgage loan apply online.

Artificial Intelligence Integration

AI-powered systems now assist with document recognition, automatically extracting data from uploaded pay stubs, W-2s, and bank statements. This technology reduces manual data entry errors and accelerates initial processing. Research on mortgage loan origination systems demonstrates both the potential and limitations of AI in lending decisions.

Instant Verification Services

Direct connections between lenders and employers, banks, and government databases enable real-time verification of income, assets, and employment. These services reduce documentation requirements and processing timelines while maintaining accuracy and fraud prevention.

Blockchain and Digital Identity

Emerging technologies promise to create portable digital identities that borrowers can use across multiple lenders, eliminating repetitive data entry for each application. While widespread adoption remains years away, pilots are underway testing these concepts in mortgage lending.

Regulatory Protections for Online Applicants

Federal and state regulations protect consumers throughout the mortgage application process, whether conducted online or in person. Understanding these protections empowers borrowers to recognize their rights when they mortgage loan apply online.

Equal Credit Opportunity Act (ECOA)

This federal law prohibits discrimination based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Research on racial and ethnic disparities in mortgage lending highlights the importance of continued enforcement and borrower awareness.

Truth in Lending Act (TILA)

TILA requires lenders to disclose key loan terms and costs in standardized formats, enabling meaningful comparison between offers. The Loan Estimate and Closing Disclosure forms mandated under TILA-RESPA Integrated Disclosure rules provide consistent information regardless of lender.

Right to Receive Loan Estimate

Lenders must provide Loan Estimates within three business days of receiving complete applications, giving borrowers time to review terms before proceeding. This cooling-off period prevents pressure tactics and supports informed decision-making.

Successfully navigating online mortgage applications requires understanding the digital tools, documentation requirements, and strategic considerations that drive efficient approvals. Whether you're purchasing in Seattle, refinancing in Bellevue, or securing financing for investment properties throughout the Puget Sound region, the ability to mortgage loan apply online provides unprecedented convenience without sacrificing the personalized guidance essential for optimal outcomes. Keith Akada and the team at Mortgage Reel combine cutting-edge digital platforms with 25+ years of local expertise, specializing in complex income scenarios common among Seattle tech professionals while maintaining the transparency and education-focused approach that has earned 750+ five-star reviews. If you're ready to explore your mortgage options with a trusted Seattle broker who understands both the technology and the local market, connect with Mortgage Reel today.