Purchasing your first home in Seattle represents one of the most significant financial decisions you'll make, and understanding your loan options can make the difference between a smooth transaction and a stressful experience. A first time homebuyer loan provides structured financing designed specifically for individuals entering the housing market for the first time, offering benefits like lower down payments, flexible credit requirements, and reduced closing costs. With Seattle's competitive real estate landscape spanning from Shoreline to Everett, selecting the right loan program requires careful consideration of your financial situation, career trajectory, and long-term goals.

Understanding First Time Homebuyer Loan Programs

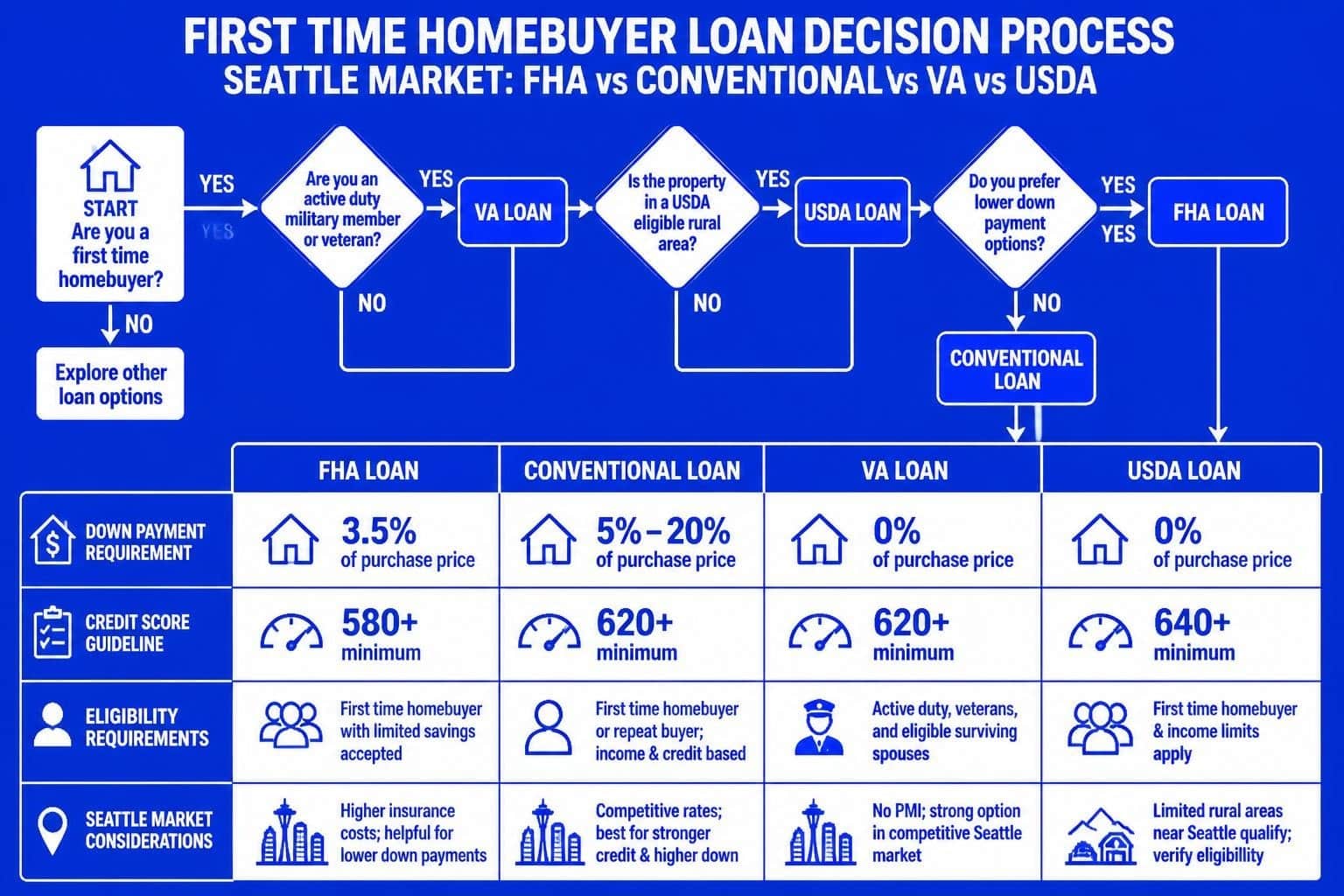

The term "first time homebuyer" carries a broader definition than many realize. According to federal guidelines, you qualify if you haven't owned a home as your primary residence in the past three years. This means even if you previously owned property, you might still access these specialized programs.

Several loan types cater specifically to first-time buyers:

- FHA loans backed by the Federal Housing Administration

- Conventional loans meeting Fannie Mae and Freddie Mac standards

- VA loans for qualifying military service members and veterans

- USDA loans for properties in designated rural areas

- State and local assistance programs unique to Washington

Each program brings distinct advantages depending on your credit profile, income stability, and down payment capacity. For tech professionals working at Amazon, Microsoft, or Google in the Seattle metro area, conventional loan options often provide the best flexibility for qualifying stock compensation and bonuses.

FHA Loans: Accessible Entry Points

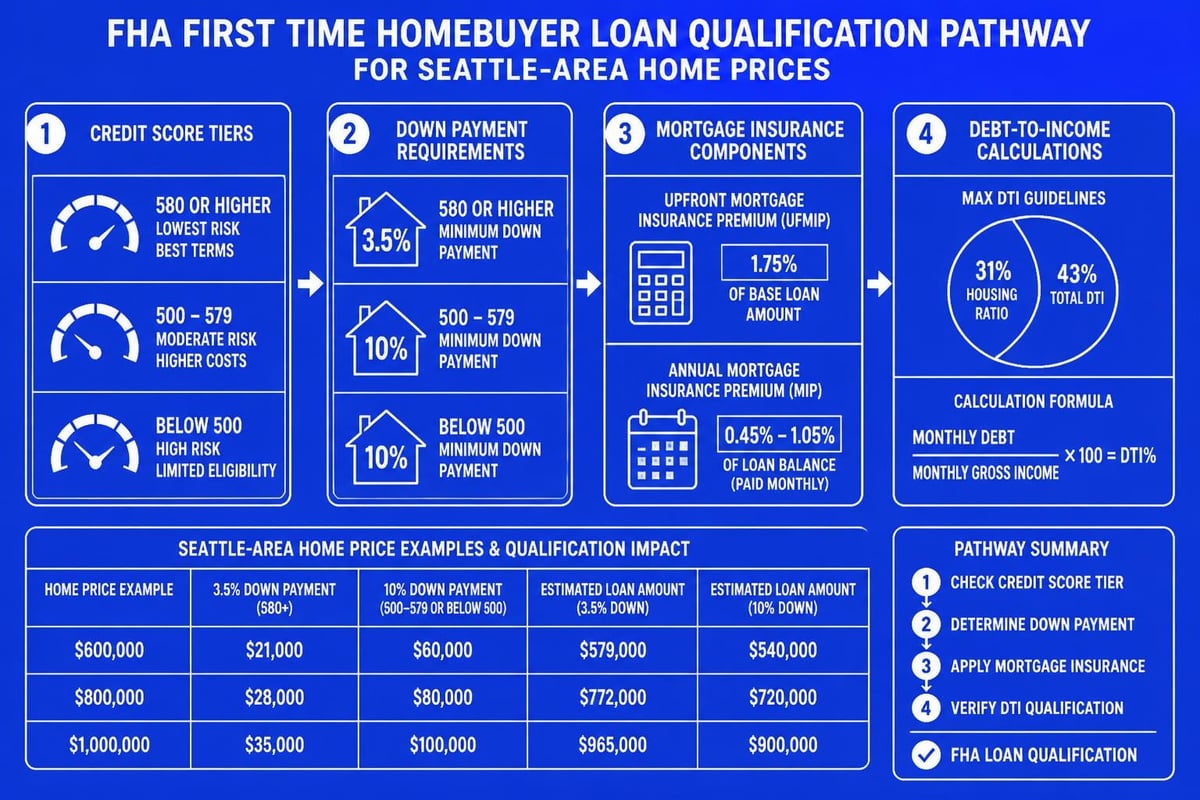

Federal Housing Administration loans remain among the most popular choices for those seeking a first time homebuyer loan with minimal upfront investment. These government-backed mortgages require as little as 3.5% down with credit scores as low as 580, making homeownership accessible even with limited savings.

The trade-off involves mandatory mortgage insurance premiums-both upfront (1.75% of the loan amount) and annual premiums that typically range from 0.45% to 1.05% depending on loan size and down payment. For a $600,000 home in Lynnwood, that translates to approximately $10,500 upfront plus $260 to $605 monthly.

| Feature | FHA Requirement | Benefit |

|---|---|---|

| Minimum down payment | 3.5% | Lower barrier to entry |

| Credit score minimum | 580 (580+ for 3.5% down) | Accessible for rebuilding credit |

| Debt-to-income ratio | Up to 50% with compensating factors | Higher borrowing capacity |

| Property standards | Must meet HUD requirements | Ensures home safety and habitability |

Despite insurance costs, FHA loans excel for buyers with student debt, shorter credit histories, or employment gaps-common scenarios for younger professionals entering Seattle's housing market.

Conventional Loans and Down Payment Flexibility

Conventional mortgages offer compelling advantages for buyers with stronger credit profiles and stable income documentation. Unlike FHA loans, these aren't government-insured, which means lenders assume more risk and consequently maintain stricter qualification standards.

The down payment flexibility for conventional loans has improved dramatically. Programs like HomeReady and Home Possible allow qualified borrowers to purchase with just 3% down, rivaling FHA accessibility while avoiding upfront mortgage insurance fees.

Key conventional loan advantages include:

- Private mortgage insurance (PMI) that cancels automatically at 78% loan-to-value

- No upfront insurance premiums

- Higher loan limits ($806,500 for King County in 2026)

- Potential for lower overall costs with good credit

- Greater property type flexibility including condos and investment properties

For Lake Forest Park or Mill Creek buyers earning $150,000+ annually with credit scores above 700, conventional products frequently deliver lower monthly payments than FHA alternatives despite similar down payment requirements.

Jumbo Loans for Seattle's Premium Markets

Seattle's robust tech economy drives home prices well above national averages, with median prices in Bellevue and Redmond regularly exceeding conventional loan limits. This creates demand for jumbo home loans among first-time buyers with substantial stock compensation.

Jumbo loans require more rigorous documentation and typically demand 10-20% down payments, though specialized programs exist for well-qualified borrowers. Tech employees with substantial RSU packages often discover their total compensation qualifies them for significantly higher purchase prices than base salary alone would suggest.

Working with a broker experienced in qualifying complex compensation structures ensures you maximize buying power without unnecessary document requests or approval delays. The ability to close in as few as 9 business days becomes particularly valuable in competitive multiple-offer situations common throughout greater Seattle.

State and Local Down Payment Assistance

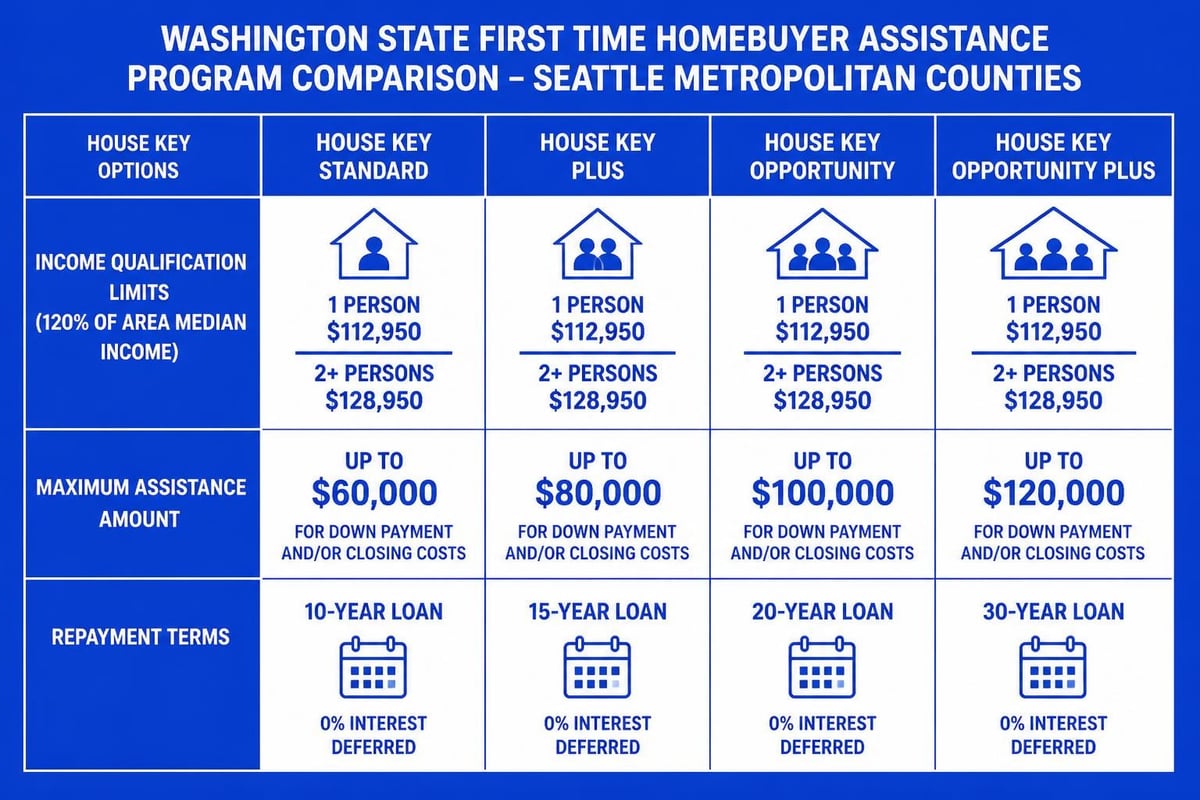

Washington State and King County offer various programs to help first-time homebuyers reduce upfront costs. The Washington State Housing Finance Commission administers several initiatives worth exploring before finalizing your first time homebuyer loan strategy.

Available assistance programs include:

- House Key Down Payment Assistance: Provides up to 4% of the purchase price (maximum $20,000) as a deferred, non-interest-bearing second mortgage

- Home Advantage Program: Offers competitive interest rates for qualified first-time buyers

- House Key Opportunity: Combines reduced rates with down payment help for specific professions

- Local City Programs: Seattle, Shoreline, and Everett each maintain additional resources

These programs typically require completion of a homebuyer education course and impose income limits based on area median income. For 2026, King County AMI limits generally cap eligibility at 80-120% of median income depending on household size.

Stacking down payment assistance with a low-down-payment first time homebuyer loan can reduce out-of-pocket requirements to under 1% of purchase price in some scenarios. However, assistance programs add complexity to the approval process and may restrict your ability to negotiate seller concessions.

VA Loans: Zero Down for Eligible Service Members

Veterans, active-duty service members, and qualifying spouses access arguably the most powerful first time homebuyer loan through the Department of Veterans Affairs. VA loans require no down payment, charge no monthly mortgage insurance, and typically offer below-market interest rates.

The program's flexibility extends to credit requirements, with many lenders approving scores as low as 580 with compensating factors like strong employment history or substantial asset reserves. For eligible buyers in Everett near Naval Station Everett or Joint Base Lewis-McChord personnel purchasing in the Seattle area, VA financing delivers unmatched value.

One-time funding fees range from 1.4% to 3.6% depending on down payment and whether you've used your VA benefit previously. These fees can be financed into the loan amount rather than paid upfront, preserving cash for closing costs, reserves, and moving expenses.

| VA Loan Feature | Benefit | Consideration |

|---|---|---|

| Down payment | 0% required | Full purchase price financed |

| Mortgage insurance | None | Lower monthly payments |

| Interest rates | Typically 0.25-0.5% below conventional | Significant long-term savings |

| Funding fee | 1.4-3.6% of loan amount | Can be financed into mortgage |

| Credit flexibility | More lenient than conventional | Easier qualification |

Properties must meet VA minimum property requirements, which occasionally eliminate fixer-uppers from consideration. However, for move-in-ready homes throughout Seattle and surrounding communities, these loans represent exceptional value for those who've served.

Qualifying Your Income and Assets

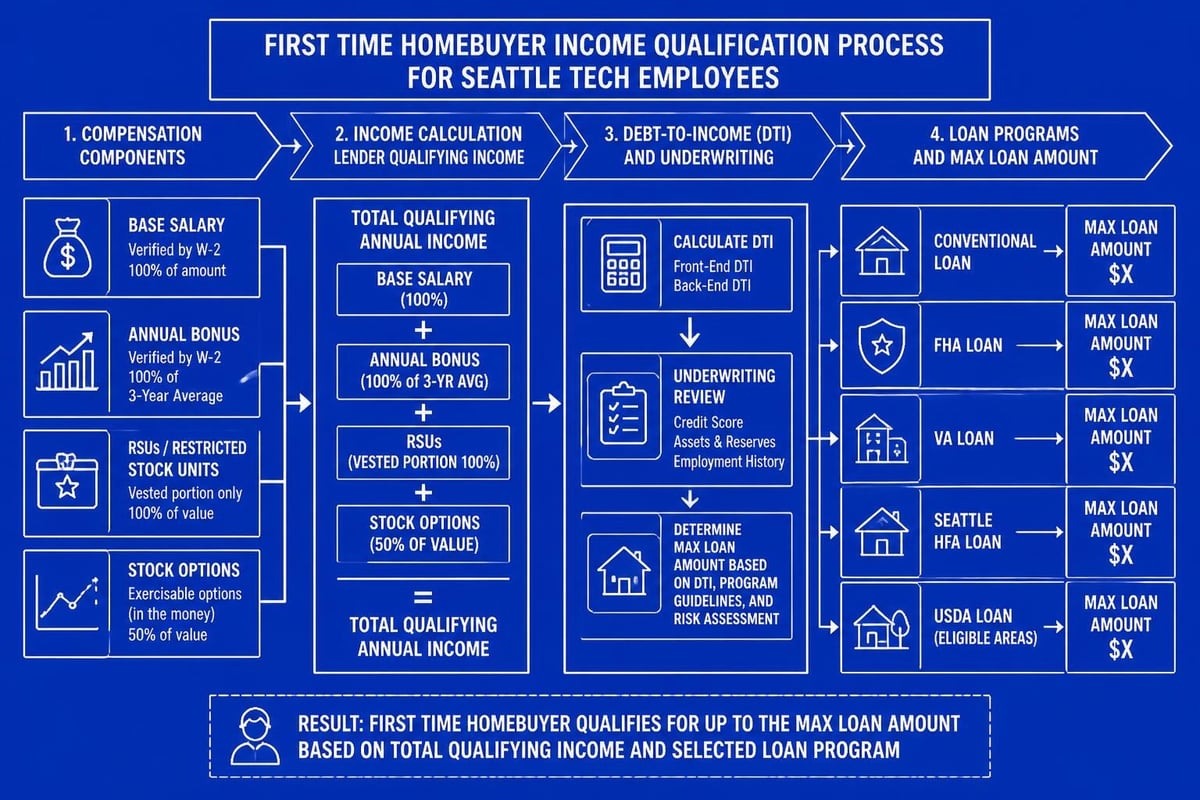

Securing approval for a first time homebuyer loan requires demonstrating stable income, manageable debt levels, and sufficient reserves. Traditional employment verification involves two years of W-2s, recent pay stubs, and verbal confirmation from your employer.

Seattle's concentration of tech companies introduces complexity many loan officers struggle to navigate. Restricted Stock Units (RSUs), Employee Stock Purchase Plans (ESPPs), performance bonuses, and equity refreshers require specialized underwriting knowledge to qualify properly.

Income documentation for tech professionals typically includes:

- Two years of W-2s showing base salary and vested stock compensation

- Most recent pay stub indicating year-to-date earnings

- RSU vesting schedule for the next 12-24 months

- Letter from employer confirming employment and compensation structure

- Recent brokerage statements showing vested shares

Lenders generally count 70-100% of vested RSU value toward qualifying income, with specific treatment varying by loan type and company stock volatility. Properly documenting this compensation can increase your buying power by $100,000-$300,000 or more compared to qualifying on base salary alone.

Debt-to-income ratios compare your monthly debt obligations to gross monthly income. Most first time homebuyer loan programs accept ratios up to 43-50%, meaning your total monthly debts (including the proposed mortgage payment) shouldn't exceed roughly half your gross income.

Building Reserves and Down Payment

Beyond qualifying income, lenders verify you maintain sufficient reserves-liquid assets remaining after down payment and closing costs. Reserve requirements vary by loan type and property characteristics, ranging from zero months for some FHA purchases to six months for jumbo loans on investment properties.

For buyers in competitive Seattle neighborhoods, demonstrating strong reserves strengthens your offer even when not technically required. Sellers and listing agents view substantial assets as evidence you'll successfully close without last-minute financing complications.

Down payment sources undergo scrutiny to ensure funds represent legitimate savings rather than undisclosed borrowed money. Large deposits within 60 days of application require explanation through paper trails showing the money's origin.

Acceptable down payment sources include:

- Personal savings and checking accounts

- Vested 401(k) or IRA withdrawals (with tax implications considered)

- Gifts from immediate family members with proper documentation

- Sale proceeds from stocks, bonds, or other assets

- Employer down payment assistance programs

The Pre-Approval Process

Beginning your home search without pre-approval puts you at severe disadvantage in Seattle's competitive market. A comprehensive pre-approval involves full income documentation review, credit analysis, and asset verification-providing confidence you'll secure financing for homes within your approved price range.

Distinguished from pre-qualification (which estimates borrowing capacity based on self-reported information), pre-approval requires a mortgage broker to submit your complete loan package for underwriter review. This process identifies potential issues early, allowing time to address credit concerns, explain income gaps, or accumulate additional reserves.

Working with a Seattle-based mortgage professional familiar with local market dynamics ensures your pre-approval letter carries weight with listing agents. Letters from online lenders or out-of-state banks often receive less favorable consideration, particularly in multiple-offer scenarios.

The pre-approval timeline typically spans 24-72 hours for straightforward W-2 employees with strong credit. Complex income situations involving RSUs, self-employment components, or recent job changes may require additional documentation and extend the process to 5-7 business days.

Choosing the Right First Time Homebuyer Loan

Selecting among available loan programs depends on your unique financial profile, property preferences, and long-term ownership timeline. No single product serves every buyer's needs optimally.

Decision framework considerations:

- Credit score and history: Scores above 720 favor conventional loans; 580-680 may benefit from FHA flexibility

- Down payment capacity: Limited savings (under 5%) point toward FHA or assistance programs; 10%+ enables conventional options

- Income documentation: Complex compensation structures require experienced underwriting often better suited to conventional or jumbo products

- Property type and price: Condos, new construction, and properties above conforming limits restrict certain loan types

- Long-term ownership plans: Shorter timelines (under 5 years) may justify higher upfront costs for lower rates; longer ownership rewards programs minimizing total interest paid

Mill Creek and Shoreline buyers often discover conventional loans with small down payments deliver the best combination of accessibility and long-term cost efficiency. Meanwhile, Everett purchasers with VA eligibility rarely find better alternatives than zero-down VA financing.

Running detailed comparisons across multiple scenarios with actual numbers from your situation reveals true costs more accurately than general guidelines. Total interest paid over expected ownership duration matters more than minor monthly payment differences.

Common First Time Buyer Mistakes to Avoid

Even well-prepared buyers frequently encounter preventable obstacles when securing their first time homebuyer loan. Awareness of common pitfalls helps you navigate the process smoothly.

Critical mistakes to avoid:

- Changing jobs during the transaction: Employment changes raise red flags requiring extensive documentation and potentially delaying closing

- Making large purchases on credit: New car loans or furniture financing alter debt-to-income ratios and can invalidate approval

- Depleting all savings: Retaining reserves beyond down payment provides financial cushion for unexpected expenses

- Skipping home inspection: Waiving inspections in competitive markets creates risk of costly surprises post-purchase

- Neglecting property tax and insurance research: Actual ownership costs frequently exceed online estimates, particularly for older homes or high-value properties

Seattle's property tax rates hover around 1% of assessed value annually, with significant variation between jurisdictions. A $700,000 home in Bellevue carries roughly $7,000 in annual property taxes, while comparable properties in unincorporated King County may see different assessments.

Understanding the complete mortgage process from application through closing prevents surprises and enables proactive planning. The typical 30-45 day timeline from offer acceptance to funding involves appraisal coordination, title work, final underwriting, and document preparation-each presenting potential delays if not managed carefully.

Interest Rates and Market Timing

First time homebuyer loan rates fluctuate based on broader economic conditions, Federal Reserve policy, and individual borrower qualifications. Attempting to time the market perfectly often backfires, as life circumstances and housing needs rarely align with optimal rate environments.

Current rate trends in 2026 reflect stabilization after the volatility of previous years, with conventional 30-year fixed mortgages generally available in the 6-7% range for well-qualified borrowers. FHA and VA rates typically run 0.125-0.25% lower due to government backing reducing lender risk.

Your specific rate depends heavily on credit score, down payment, loan amount, property type, and occupancy status. A 740 credit score typically commands rates 0.5-0.75% lower than a 660 score, translating to roughly $175-$260 monthly savings on a $500,000 loan.

Rate locks protect against increases during your transaction, typically guaranteed for 30-60 days. Extended locks (90+ days) carry premium costs but provide security for new construction purchases or complex transactions with extended closing timelines.

Rather than obsessing over small rate fluctuations, focus on qualifying for the best possible terms through strong credit, stable employment documentation, and adequate down payment. The difference between a 6.5% and 6.625% rate pales in comparison to the benefit of entering the market versus delaying another year while prices appreciate.

Working with a Seattle Mortgage Specialist

The complexity of qualifying Seattle-area home prices with tech industry compensation demands expertise beyond what large national lenders typically provide. Specialized knowledge of RSU qualification, local assistance programs, and fast-close capabilities creates measurable advantages in competitive markets.

Keith Akada brings 25+ years of experience helping first-time buyers navigate the intricate landscape of loan programs, qualification requirements, and market strategies. With 750+ five-star reviews across major platforms, his track record demonstrates consistent delivery of clear communication and reliable execution.

Benefits of specialized local expertise include:

- Accurate qualification of stock-based compensation for maximum buying power

- Familiarity with specific condo buildings and their financing eligibility

- Relationships with local appraisers enabling faster turnaround

- Knowledge of neighborhood-specific considerations affecting loan approval

- Ability to close in as few as 9 business days when necessary

From getting pre-approved through final funding, having an experienced advisor who understands both mortgage guidelines and local market dynamics provides peace of mind throughout your transaction. This proves particularly valuable for buyers balancing demanding careers at Amazon, Microsoft, or Google with the already-stressful home buying process.

The right first time homebuyer loan positions you for successful homeownership while preserving financial flexibility for life beyond closing. Taking time to understand your options, qualify your income properly, and select the program aligning with your specific circumstances creates a foundation for long-term success in Seattle's dynamic real estate market.

Securing the right first time homebuyer loan requires understanding your options, qualifying your income accurately, and working with professionals who know Seattle's unique market. Whether you're a tech professional in Bellevue leveraging RSU income or a buyer in Shoreline exploring down payment assistance, the path to homeownership becomes clearer with expert guidance. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping first-time buyers throughout Seattle, Redmond, Kirkland, and surrounding communities navigate loan programs, maximize buying power, and close confidently in competitive markets.