Real estate investing in Seattle, Bellevue, Redmond, and Kirkland requires more than just market knowledge and capital-it demands access to the right financing partners. Finding qualified lenders for real estate investors can mean the difference between securing a profitable rental property in Shoreline or watching a fix-and-flip opportunity in Lynnwood slip away. Unlike traditional mortgage products designed for owner-occupied homes, investment property financing operates under different guidelines, qualification standards, and rate structures. Understanding which lenders specialize in investor loans and how they evaluate deals is essential for building a successful real estate portfolio across the Greater Seattle area.

Understanding Investment Property Financing

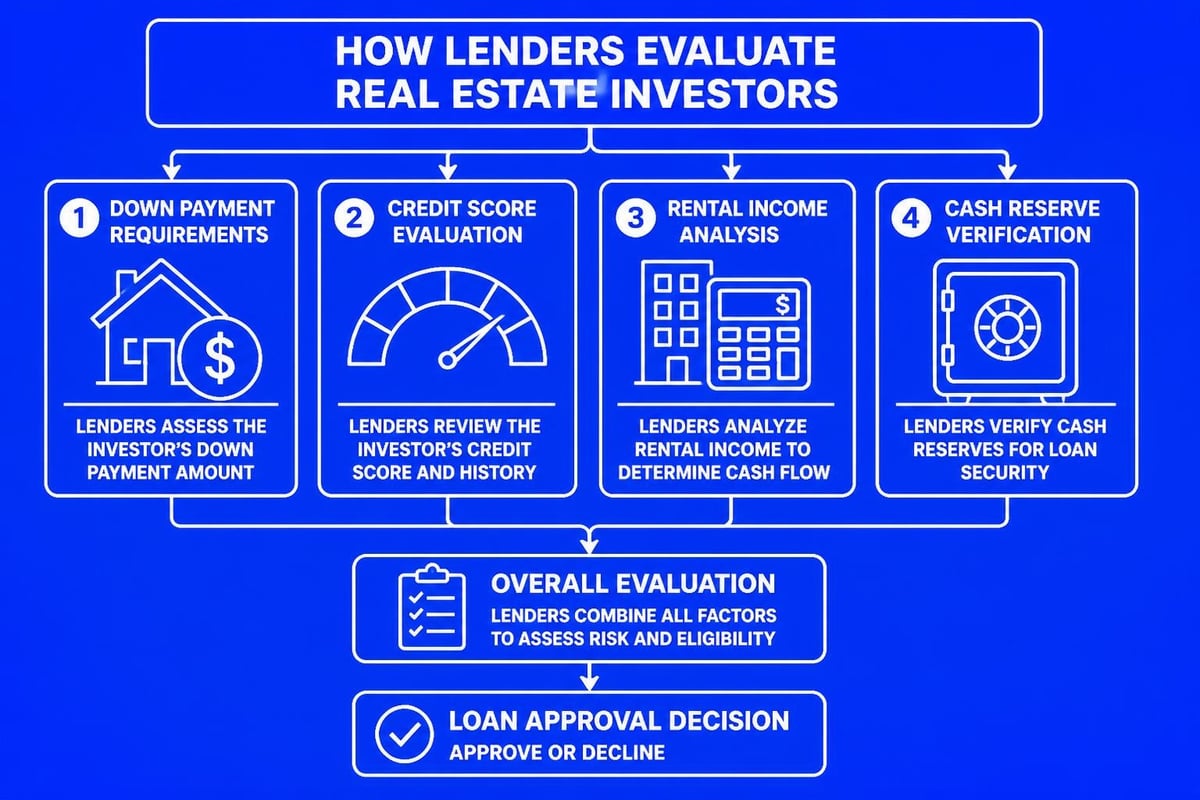

Investment property loans differ fundamentally from traditional residential mortgages. While conventional loan lenders evaluate owner-occupied homes primarily on borrower creditworthiness and income, lenders for real estate investors assess deals based on property cash flow, rental income potential, and investment experience.

Key Differences in Qualification Standards

Investment properties typically require larger down payments than primary residences. Most lenders require 20-25% down for single-family rental properties, with requirements increasing to 25-30% for multi-unit buildings. Credit score expectations also run higher, with most investment loan programs requiring minimum scores of 680-700.

Debt-to-income ratios are calculated differently for investment properties:

- Rental income can offset mortgage payments

- Lenders apply vacancy factors (typically 25%)

- Property management costs reduce qualifying income

- Multiple properties create complex DTI calculations

Cash reserves play a critical role in approval. Lenders typically require 6-12 months of mortgage payments in reserves per property, meaning investors with multiple rental properties in Mill Creek and Lake Forest Park need substantial liquid assets.

Types of Lenders Serving Real Estate Investors

Not all financial institutions offer investment property financing, and those that do often specialize in specific loan types. Understanding the landscape helps investors match their strategy with the right lending partner.

Traditional Banks and Credit Unions

Regional banks and credit unions offer investment property mortgages with competitive rates but stricter qualification requirements. These institutions excel at financing stabilized rental properties with documented rental history and strong borrower profiles.

| Lender Type | Best For | Typical Rates | Speed |

|---|---|---|---|

| National Banks | Experienced investors with strong financials | Competitive | 30-45 days |

| Regional Banks | Local market expertise, relationship-based | Moderate | 30-60 days |

| Credit Unions | Members with excellent credit | Very competitive | 45-60 days |

Seattle-area credit unions often provide attractive terms for investors who maintain primary banking relationships and have established histories.

Portfolio Lenders and Private Money

Portfolio lenders hold loans on their own books rather than selling them to secondary markets. This structure allows flexibility in underwriting guidelines, making them valuable partners for complex deals or non-traditional properties.

Private money lenders and hard money lenders specialize in short-term financing for fix-and-flip projects and properties requiring renovation. These lenders evaluate deals based primarily on property value and exit strategy rather than borrower financials.

Advantages of portfolio and private lenders include:

- Faster approval and closing timelines

- Flexibility on property condition

- Creative deal structuring

- Less emphasis on borrower debt-to-income ratios

- Ability to fund non-warrantable condos

Specialized Investment Property Lenders

Dedicated investment property lending platforms have emerged as primary resources for real estate investors. Companies like Lima One Capital, CoreVest Finance, and BrightPath Loans focus exclusively on investor financing, offering programs tailored to various strategies.

These specialized lenders understand investor needs and offer products traditional banks cannot provide, including DSCR loans that qualify based solely on rental income without personal income verification.

Popular Loan Programs for Seattle Investors

The Seattle market's high property values and strong rental demand create opportunities for various investment strategies, each requiring different financing approaches.

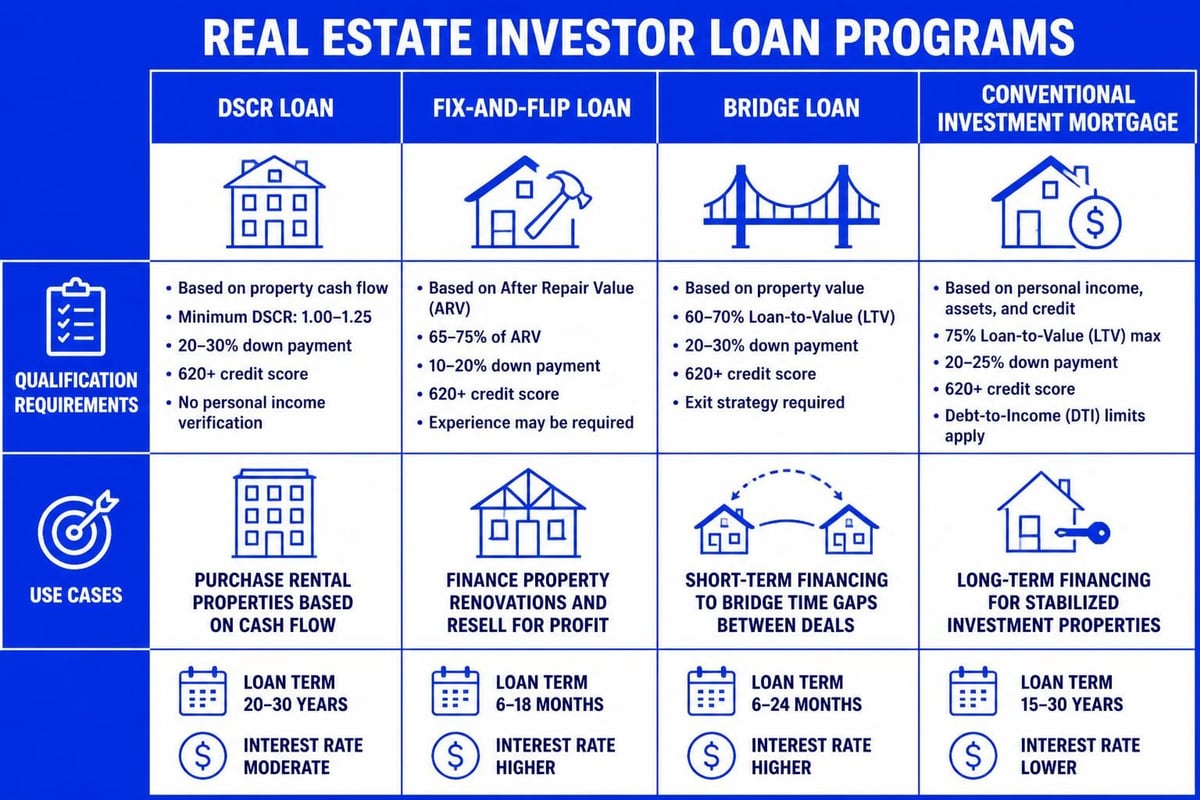

DSCR Loans (Debt Service Coverage Ratio)

DSCR loans have become increasingly popular among lenders for real estate investors because they qualify borrowers based on property cash flow rather than personal income. This structure benefits self-employed investors, those with complex tax returns, or anyone seeking to scale their portfolio without income limitations.

The debt service coverage ratio compares monthly rental income to monthly mortgage payment. A DSCR of 1.0 means rental income exactly covers the mortgage payment. Most lenders require ratios of 1.15-1.25 for approval.

DSCR loan characteristics:

- No personal income verification required

- Qualification based solely on rental income

- Typically higher interest rates than conventional loans

- Down payments starting at 20-25%

- Available for single-family and multi-unit properties

For a rental property in Everett generating $3,000 monthly rent with a $2,400 proposed mortgage payment, the DSCR would be 1.25 ($3,000 ÷ $2,400), meeting most lender requirements.

Fix-and-Flip Financing

Investors targeting renovation projects in Seattle neighborhoods need short-term financing that funds both acquisition and renovation costs. Fix-and-flip lenders typically offer 12-24 month terms with funding based on the after-repair value (ARV) of the property.

These loans close quickly-often within 10-14 days-allowing investors to act on time-sensitive opportunities. Interest rates run higher than traditional mortgages, typically 8-12%, but the short holding period minimizes total interest costs.

Bridge Loans for Investment Properties

Bridge loans provide temporary financing while investors transition between properties or complete renovations that will increase property value and enable permanent financing. These loans work well for investors purchasing properties that do not currently qualify for traditional financing.

A Lynnwood investor might use a bridge loan to purchase a multifamily property with deferred maintenance, complete necessary repairs over 6-12 months, then refinance into permanent DSCR financing once the property is stabilized and generating consistent rental income.

Conventional Investment Property Mortgages

Traditional conventional loan programs remain viable options for qualified investors, particularly those purchasing stabilized rental properties with documented rental income.

Fannie Mae and Freddie Mac Investment Guidelines

Government-sponsored enterprises set the standards for conventional investment property loans. These programs offer competitive rates but maintain strict qualification requirements.

Investors can finance up to 10 financed properties under conventional guidelines, though reserves and down payment requirements increase with each additional property. The first investment property requires 15-20% down, while properties 5-10 may require 25-30% down payments.

Reserve requirements scale with portfolio size:

- Properties 1-4: Six months reserves per property

- Properties 5-6: Nine months reserves per property

- Properties 7-10: Twelve months reserves per property

For Seattle investors with multiple properties valued at $600,000-$800,000 each, reserve requirements can easily exceed $200,000-$300,000 in liquid assets.

Working with Mortgage Brokers

Experienced mortgage brokers maintain relationships with multiple lenders for real estate investors, providing access to diverse loan programs and competitive pricing. A Seattle mortgage broker can shop investor deals across conventional banks, portfolio lenders, and specialized investment platforms.

Brokers particularly benefit investors pursuing non-traditional strategies or properties, as they understand which lenders accept specific property types, investor experience levels, and deal structures. This expertise becomes critical when financing properties in competitive Seattle neighborhoods where quick closings provide negotiating advantages.

Qualifying Rental Income for Investment Loans

Lenders calculate rental income differently depending on the loan program and property situation. Understanding these calculations helps investors accurately assess their borrowing capacity.

Properties with Existing Leases

For properties with current tenants, lenders typically use actual rental income documented through lease agreements and deposit records. Most lenders apply a 75% factor to gross rents, accounting for vacancy and maintenance costs.

A Bellevue duplex generating $4,000 monthly rent would qualify with $3,000 monthly income ($4,000 × 0.75) for debt-to-income calculations. This income offsets the mortgage payment when calculating the investor's overall DTI ratio.

Using Market Rents for Vacant Properties

Properties purchased vacant or being renovated require appraisal-based market rent analysis. The appraiser provides a rent schedule estimating fair market rental value based on comparable properties.

Lenders typically apply more conservative vacancy factors to market rents-often 25-30%-since the income is projected rather than actual. Some loan programs require the property to be rented and cash-flowing before closing, particularly for investors with limited experience.

Multi-Unit Property Income Analysis

Analyzing multifamily properties requires comprehensive income and expense review. Lenders examine profit and loss statements, rent rolls, and operating expense ratios to determine net operating income.

For buildings with 5+ units, lenders often treat the property as a commercial investment, requiring different loan programs with terms based on debt service coverage rather than personal debt-to-income ratios.

Finding the Right Lender for Your Strategy

Matching your investment approach with appropriate financing partners maximizes approval chances and ensures optimal loan terms.

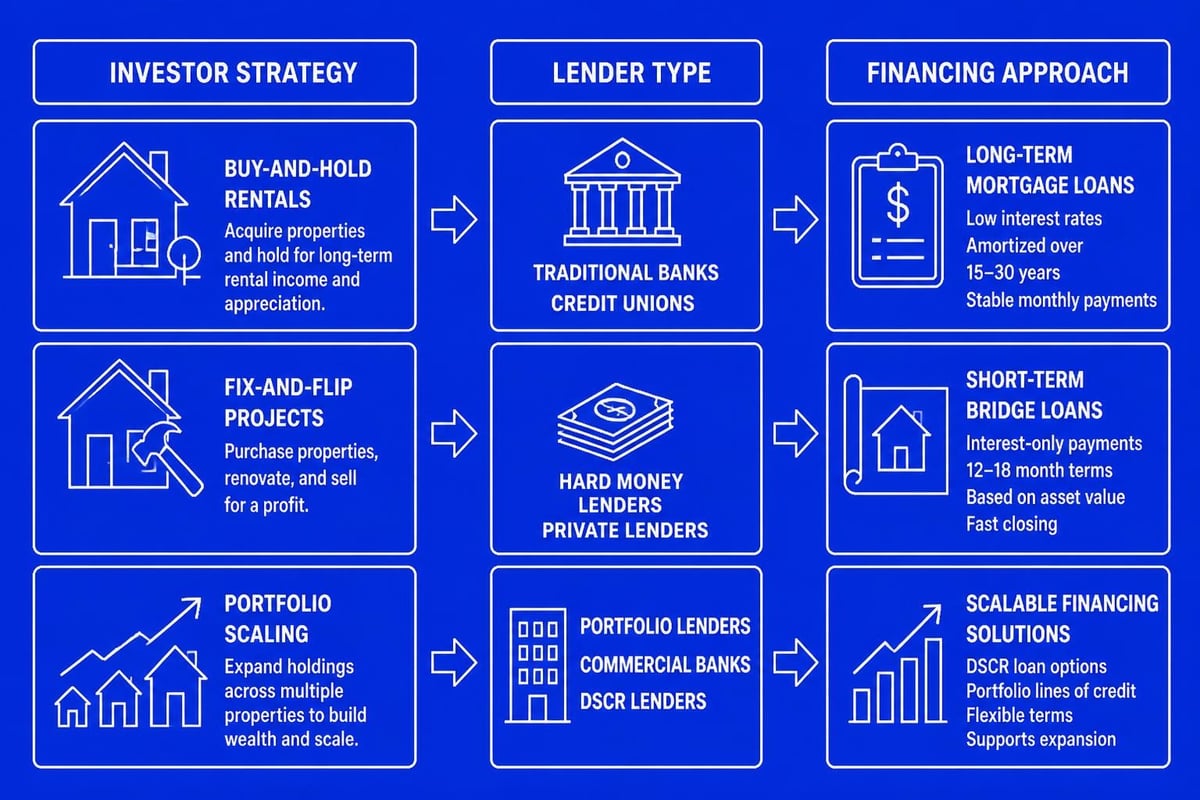

Buy-and-Hold Investors

Long-term rental property investors benefit from lenders offering permanent financing with 30-year fixed rates. Conventional loans, portfolio lender programs, and DSCR products all serve this strategy effectively.

Investors focused on steady cash flow in Seattle's strong rental market should prioritize lenders with competitive rates and streamlined refinance processes for portfolio optimization over time.

Active Fix-and-Flip Investors

Flippers need lenders who close quickly and fund renovation costs. Hard money lenders and specialized fix-and-flip financing platforms provide the speed and flexibility required for this strategy.

Successful flippers in Redmond and Kirkland often maintain relationships with 2-3 different hard money lenders to ensure funding availability when opportunities arise. Rate shopping each deal ensures competitive terms while maintaining backup options.

Scaling Multi-Property Portfolios

Investors building large portfolios require lenders comfortable financing multiple properties simultaneously. Portfolio lenders and specialized investment platforms like CoreVest Finance often accommodate investors with 10+ financed properties, while conventional programs cap at 10.

Tech Professional Investors in Seattle

Seattle's concentration of technology workers creates unique opportunities for real estate investors with stock-based compensation. Amazon, Microsoft, and Google employees often possess significant equity compensation that can fund investment property down payments.

Leveraging RSUs and Stock Options

Restricted stock units and stock options provide substantial capital for real estate investments once vested and exercised. Strategic tax planning around RSU vesting can optimize down payment funding while managing tax liability.

Tech professionals should work with mortgage brokers experienced in stock compensation to properly document equity income for loan qualification. Some investment loan programs count RSUs as qualifying income, while others require two-year histories.

Jumbo Investment Property Loans

Seattle's high property values frequently push investment loans into jumbo territory, requiring specialized lenders comfortable with larger loan amounts. Investment property jumbo loans typically start at $766,550 in 2026, though some lenders use lower thresholds.

Jumbo investment loans require stronger qualification profiles, including higher credit scores (typically 720+), larger reserves, and lower debt-to-income ratios. However, competitive rates remain available for well-qualified borrowers.

Rate and Term Considerations

Investment property rates run 0.50-0.75% higher than owner-occupied rates for conventional loans, reflecting increased lender risk. DSCR and portfolio loan rates may run 1-2% higher than conventional mortgages.

Fixed vs. Adjustable Rate Products

Many investors prefer fixed-rate financing for long-term rental properties, providing payment stability and protection against rate increases. However, adjustable-rate mortgages (ARMs) can make sense for fix-and-flip projects or properties the investor plans to refinance within 3-5 years.

Five-year and seven-year ARM products offer lower initial rates than 30-year fixed loans, potentially improving cash flow for properties held temporarily while providing rate protection during the fixed period.

Comparing Lender Fees and Costs

Lenders for real estate investors charge various fees beyond interest rates. Origination fees typically range from 0.5-2% of the loan amount, though some portfolio lenders and hard money lenders charge higher fees for specialized programs.

| Fee Type | Typical Range | Negotiable |

|---|---|---|

| Origination | 0.5-2% | Often |

| Processing | $500-$1,500 | Sometimes |

| Underwriting | $500-$1,200 | Rarely |

| Appraisal | $500-$800 | No |

Comparing total costs across lenders requires examining both rate and fees. A lender offering slightly higher rates with minimal fees may provide better overall value than one with lower rates but significant upfront costs.

Building Lender Relationships

Successful real estate investors cultivate relationships with multiple financing sources, creating competitive advantages in Seattle's fast-moving market.

Portfolio Performance and Access to Capital

Consistently performing loans build credibility with lenders. Investors who maintain on-time payments, keep properties well-maintained, and provide prompt documentation when requested often receive preferential treatment on future deals.

Strong track records can translate into better rates, higher leverage, or faster approvals. Some portfolio lenders offer relationship pricing, reducing rates for borrowers with multiple performing loans.

Pre-Qualification Strategies

Obtaining pre-qualification from multiple lenders before pursuing specific properties enables faster closings when opportunities arise. In competitive Seattle neighborhoods where multiple offers are common, the ability to close quickly provides significant negotiating leverage.

Working with a mortgage broker provides access to multiple pre-qualification options simultaneously, positioning investors to move decisively on the right properties.

Common Challenges and Solutions

Even experienced investors encounter financing obstacles. Understanding common issues and their solutions improves transaction success rates.

Properties Requiring Extensive Repairs

Traditional lenders typically decline properties needing significant work, requiring investors to seek renovation financing or hard money loans. Bridge loans or fix-and-flip programs fund both acquisition and renovation, then investors refinance into permanent financing once work completes.

Title and Legal Issues

Properties with title defects, estate situations, or legal complications may not qualify for traditional financing. Portfolio lenders and private money sources often accommodate properties with solvable issues, funding deals while borrowers resolve complications.

Low Appraisal Values

When appraisals come in below purchase price, investors need additional cash to cover the gap or must renegotiate purchase terms. Building relationships with lenders who use multiple appraisers or order second opinions can sometimes resolve valuation discrepancies.

Rental Property Loan Alternatives

Beyond traditional mortgage products, investors can access capital through various creative financing structures.

Seller Financing Arrangements

Some property owners, particularly older investors liquidating portfolios, offer seller financing where they act as the lender. These arrangements provide flexibility on terms, qualification requirements, and closing timelines.

Seller-financed deals often involve shorter terms (3-7 years) with balloon payments, requiring investors to refinance with conventional lenders before the note matures.

Home Equity for Investment Property Down Payments

Investors with substantial equity in primary residences or existing rental properties can access capital through home equity lines of credit (HELOCs) or cash-out refinances. This strategy provides down payment funds without liquidating other investments.

HELOCs offer revolving credit lines investors can draw against repeatedly, making them efficient funding sources for multiple deals. However, overleveraging across properties increases risk during market downturns.

Partnership and Syndication Structures

Investors can pool capital with partners to fund larger deals or multiple properties simultaneously. Partnership structures spread risk while providing access to opportunities requiring more capital than individual investors possess.

These arrangements require clear operating agreements defining each partner's role, capital contribution, profit distribution, and exit strategies.

Due Diligence When Selecting Lenders

Not all lenders for real estate investors deliver consistent service or competitive terms. Thorough vetting prevents financing delays and ensures optimal deal structures.

Researching Lender Track Records

Reviewing online feedback, checking Better Business Bureau ratings, and requesting references from other investors reveals lender reliability. Consistent complaints about slow closings, poor communication, or unexpected fee changes warrant caution.

Understanding Total Loan Costs

Beyond interest rates and origination fees, investors should clarify prepayment penalties, extension fees, and refinancing costs. Some hard money lenders charge significant penalties for early payoff, potentially eroding flip project profits.

Verifying License and Credentials

All mortgage lenders must maintain proper licensing through state regulatory agencies. Verifying credentials through the Nationwide Mortgage Licensing System confirms legitimacy and reveals any regulatory actions.

Geographic Considerations in Greater Seattle

Local market knowledge influences financing decisions across Seattle-area submarkets.

Seattle vs. Surrounding Communities

Investment properties in Seattle proper typically command higher prices but generate stronger rents than surrounding areas. Investors might find better cash flow in Everett or Lake Forest Park where purchase prices are lower relative to rental rates.

Lenders familiar with Seattle market dynamics understand these nuances and can provide realistic rental income projections for different neighborhoods.

New Construction Investment Opportunities

Mill Creek and Shoreline continue seeing residential development, creating opportunities for investors purchasing newly constructed rental properties. New construction often qualifies for better financing terms since properties require minimal immediate maintenance.

Some lenders offer construction-to-permanent loans funding both building phases, eliminating the need for separate construction and takeout financing.

Securing the right financing partner is as critical as finding the right investment property. Understanding how lenders for real estate investors evaluate deals, comparing loan programs across different lender types, and building strong relationships with multiple financing sources positions investors for success in Seattle's competitive market. Whether you're purchasing your first rental property in Bellevue or expanding a multi-unit portfolio across the Greater Seattle area, Keith Akada at Mortgage Reel brings 25+ years of experience helping real estate investors structure optimal financing solutions. With deep knowledge of investment property lending, stock compensation qualification for tech professionals, and the ability to close in as few as 9 business days, Keith provides the strategic guidance and reliable execution Seattle investors need to build profitable portfolios.