Purchasing your first home represents one of the most significant financial decisions you'll make, particularly in competitive markets like Seattle, Bellevue, and Redmond. Many prospective buyers feel overwhelmed by mortgage terminology, down payment requirements, and the intricacies of closing costs. First time home buyers courses provide structured education that demystifies the home buying process while potentially qualifying you for valuable financial assistance programs. These educational programs have become increasingly popular among tech professionals at Amazon, Microsoft, and Google who want to maximize their buying power through comprehensive preparation.

Understanding First Time Home Buyers Courses

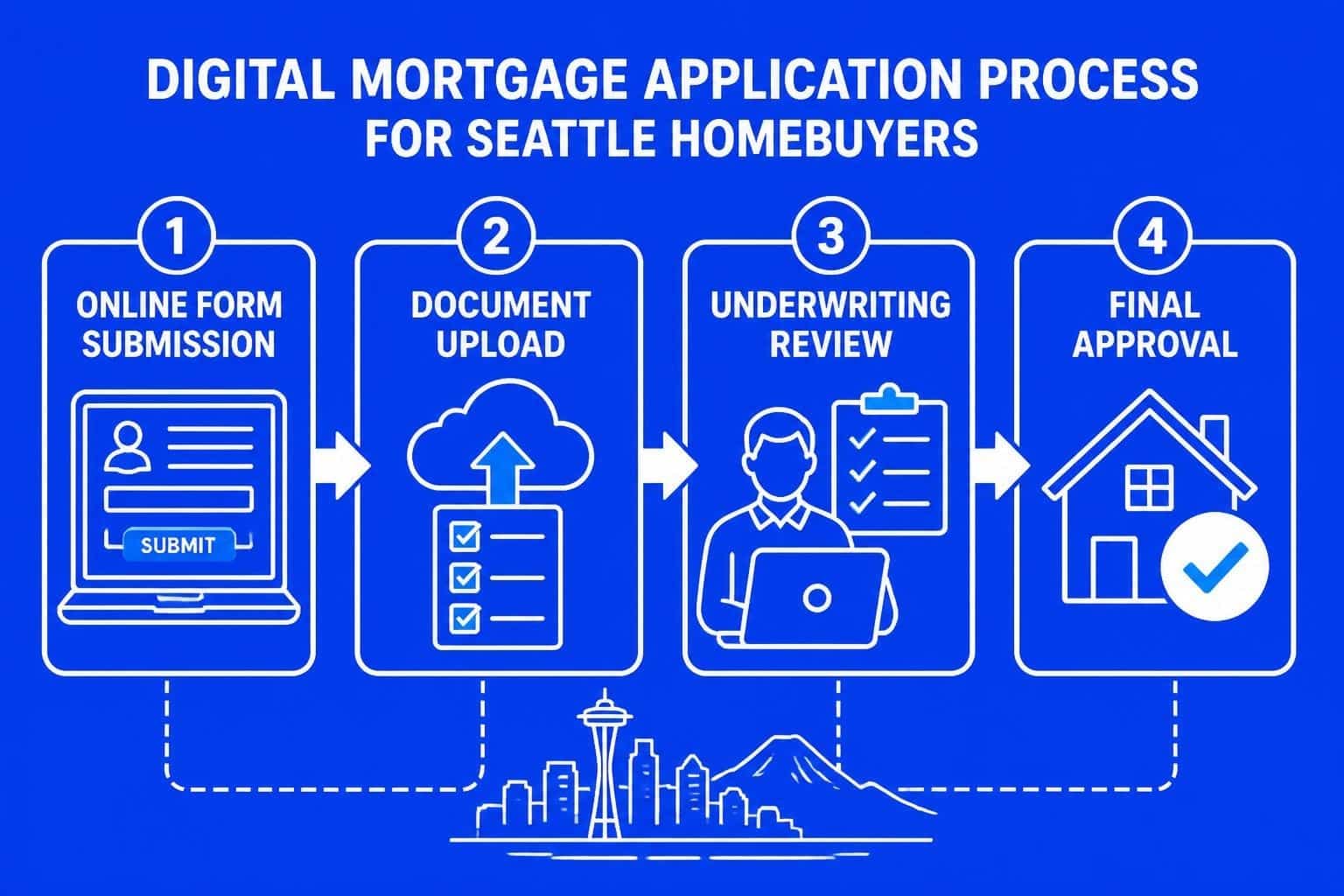

First time home buyers courses offer comprehensive instruction covering every aspect of purchasing a home, from initial budgeting through closing day and beyond. These programs typically span several hours and may be offered in-person, online, or through hybrid formats to accommodate different schedules and learning preferences.

What These Courses Cover

The curriculum for first time home buyers courses addresses fundamental topics that every new buyer should understand before entering the market. Most programs include detailed instruction on:

- Budgeting and financial readiness: Calculating how much house you can afford based on income, debt, and savings

- Credit fundamentals: Understanding credit scores, reports, and strategies for improvement

- Mortgage types and options: Comparing conventional, FHA, VA, and USDA loans with their respective requirements

- Down payment strategies: Exploring assistance programs, gift funds, and savings approaches

- The home search process: Working with real estate agents and identifying properties that match your criteria

- Making competitive offers: Crafting strong proposals in markets like Seattle where bidding wars are common

- Home inspections and appraisals: Understanding their role in protecting your investment

- Closing procedures: Navigating final walkthroughs, signing documents, and transferring ownership

These educational programs help buyers avoid common pitfalls that can derail transactions or lead to buyer's remorse after closing.

Certification and Accreditation

Quality first time home buyers courses typically carry certification from recognized housing authorities. HUD-approved housing counseling agencies provide programs that meet federal standards and qualify participants for certain assistance programs.

Look for courses certified by:

- U.S. Department of Housing and Urban Development (HUD)

- State housing finance agencies

- NeighborWorks America

- National Foundation for Credit Counseling

Completing a certified course often generates an official certificate of completion, which you'll need to access specific down payment assistance programs or special mortgage products designed for first-time purchasers.

Benefits Beyond Basic Education

While knowledge acquisition represents the primary value proposition, first time home buyers courses deliver additional advantages that can significantly impact your purchasing power and long-term financial success.

Financial Assistance Qualification

Many state and local housing programs require course completion as a prerequisite for accessing benefits. In Washington State, several down payment assistance programs mandate education certificates before disbursing funds.

| Program Type | Typical Benefit | Education Requirement |

|---|---|---|

| Down Payment Assistance | $5,000-$20,000 | HUD-approved course |

| Reduced Interest Rates | 0.25%-0.50% reduction | State-certified program |

| Closing Cost Grants | $1,500-$5,000 | Approved counseling |

| Tax Credits | Annual savings | MCC-qualifying education |

For buyers in Seattle, Shoreline, and Lynnwood, understanding down payment strategies becomes particularly important given the region's elevated home prices.

Improved Mortgage Approval Rates

Lenders view course completion favorably because educated buyers typically understand their obligations and demonstrate lower default rates. Some mortgage programs offer preferential treatment to graduates of first time home buyers courses, including reduced documentation requirements or more flexible qualifying criteria.

This proves especially valuable for tech professionals with complex compensation structures involving RSUs, stock options, and performance bonuses. Understanding how lenders evaluate these income sources helps you present your financial profile more effectively.

Negotiation Confidence

Armed with comprehensive knowledge, course graduates negotiate more confidently with sellers, real estate agents, and lenders. You'll understand standard contingencies, recognize unreasonable requests, and identify favorable terms versus predatory lending practices.

In competitive markets like Bellevue and Redmond, where multiple offers on desirable properties are common, this confidence translates into better decision-making under pressure.

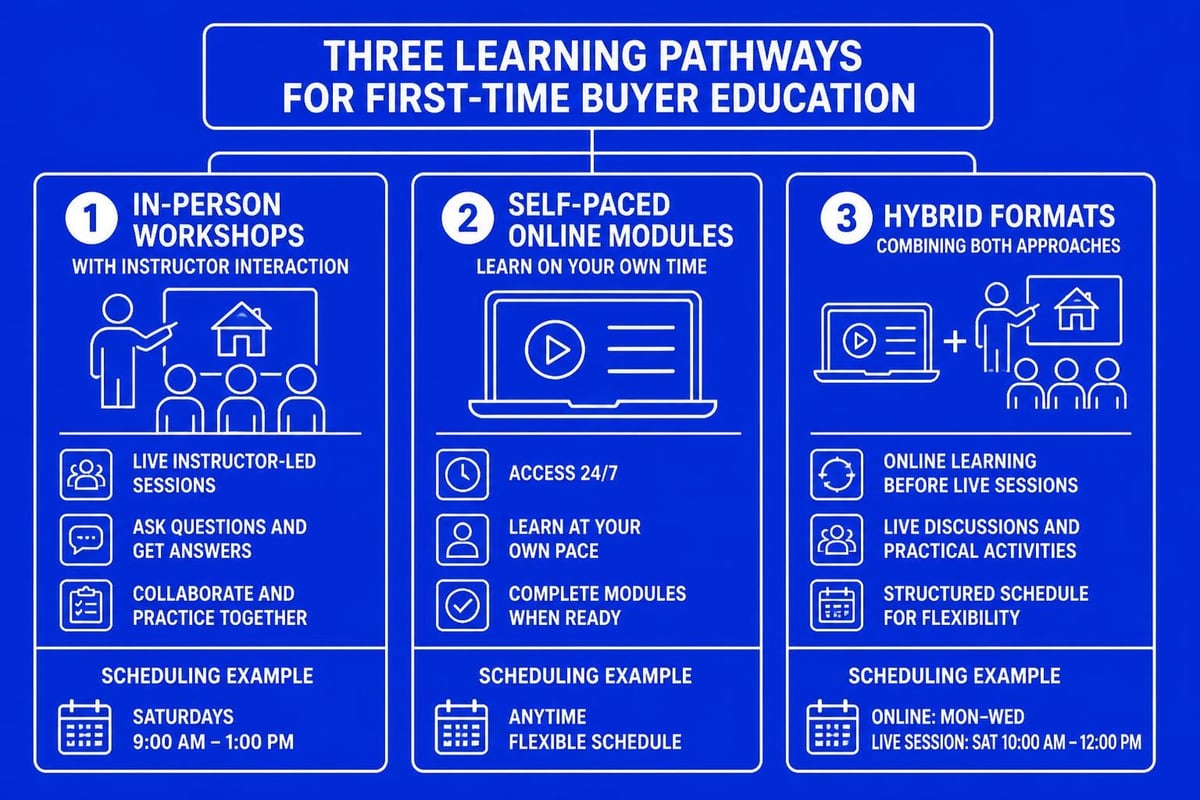

Choosing the Right Course Format

First time home buyers courses come in various delivery methods, each offering distinct advantages depending on your learning style, schedule, and location preferences.

In-Person Workshops

Traditional classroom settings provide face-to-face interaction with certified instructors and opportunities to network with other prospective buyers. Free in-person classes are available across many U.S. cities, creating accessible entry points for education.

Advantages of in-person learning:

- Direct interaction with instructors for immediate question clarification

- Networking opportunities with other first-time buyers

- Hands-on activities and case study discussions

- Local market-specific information relevant to Seattle neighborhoods

Considerations:

- Fixed schedules that may conflict with work commitments

- Geographic limitations for residents in Mill Creek or Everett

- Longer time commitment in single sessions

Online Self-Paced Courses

Digital platforms offer flexibility for busy professionals who need to complete coursework around demanding schedules. Many HUD-certified online programs deliver the same comprehensive curriculum as classroom versions.

Benefits of online formats:

- Complete modules on your schedule, ideal for shift workers or parents

- Review complex topics multiple times at your own pace

- Lower costs, often $50-$100 compared to $150-$300 for in-person options

- Accessibility from anywhere with internet connection

Drawbacks:

- Less personalized interaction with instructors

- Requires self-discipline to complete all modules

- May lack local market specificity for Lake Forest Park or Shoreline buyers

Hybrid and One-on-One Counseling

Some organizations blend online coursework with scheduled counseling sessions, combining flexibility with personalized guidance. Habitat for Humanity’s programs often incorporate this approach, pairing educational content with individualized financial planning.

This format works particularly well for buyers with unique situations, such as:

- Self-employed individuals with variable income

- Recent immigrants building U.S. credit history

- Buyers recovering from past credit challenges

- Tech professionals navigating complex compensation packages

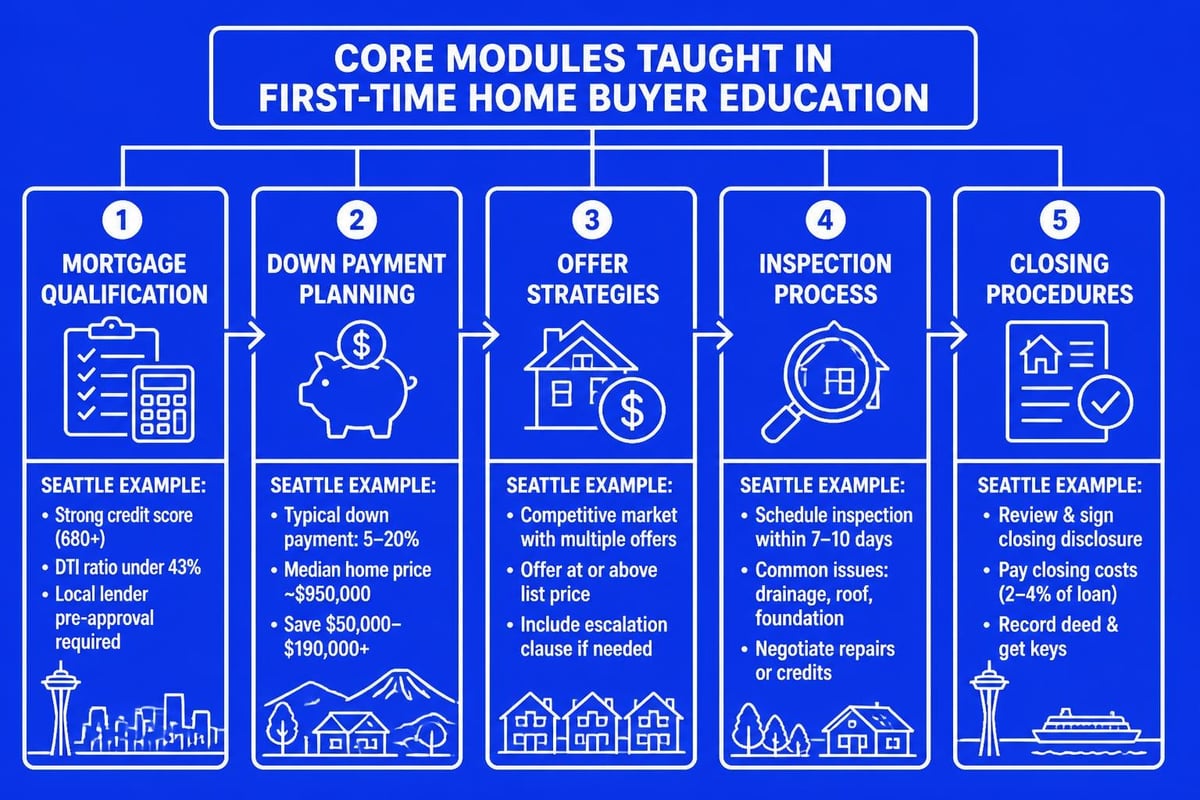

Course Content Deep Dive

Understanding what you'll actually learn helps you select programs aligned with your knowledge gaps and specific circumstances. Quality first time home buyers courses address both universal principles and situation-specific strategies.

Mortgage Qualification Fundamentals

Comprehensive instruction on how lenders evaluate your application forms the foundation of most programs. You'll learn the specific calculations lenders use for debt-to-income ratios, how different loan types vary in their requirements, and strategies for strengthening your application.

For first-time home buyers in Seattle's competitive market, understanding qualification nuances can mean the difference between approval and denial.

Key topics include:

- Income documentation: Pay stubs, tax returns, and employment verification requirements

- Asset verification: Acceptable sources for down payments and reserves

- Credit analysis: How scores impact interest rates and loan approval

- Debt calculations: Which obligations count toward your qualifying ratios

- Compensating factors: Strengths that offset potential weaknesses

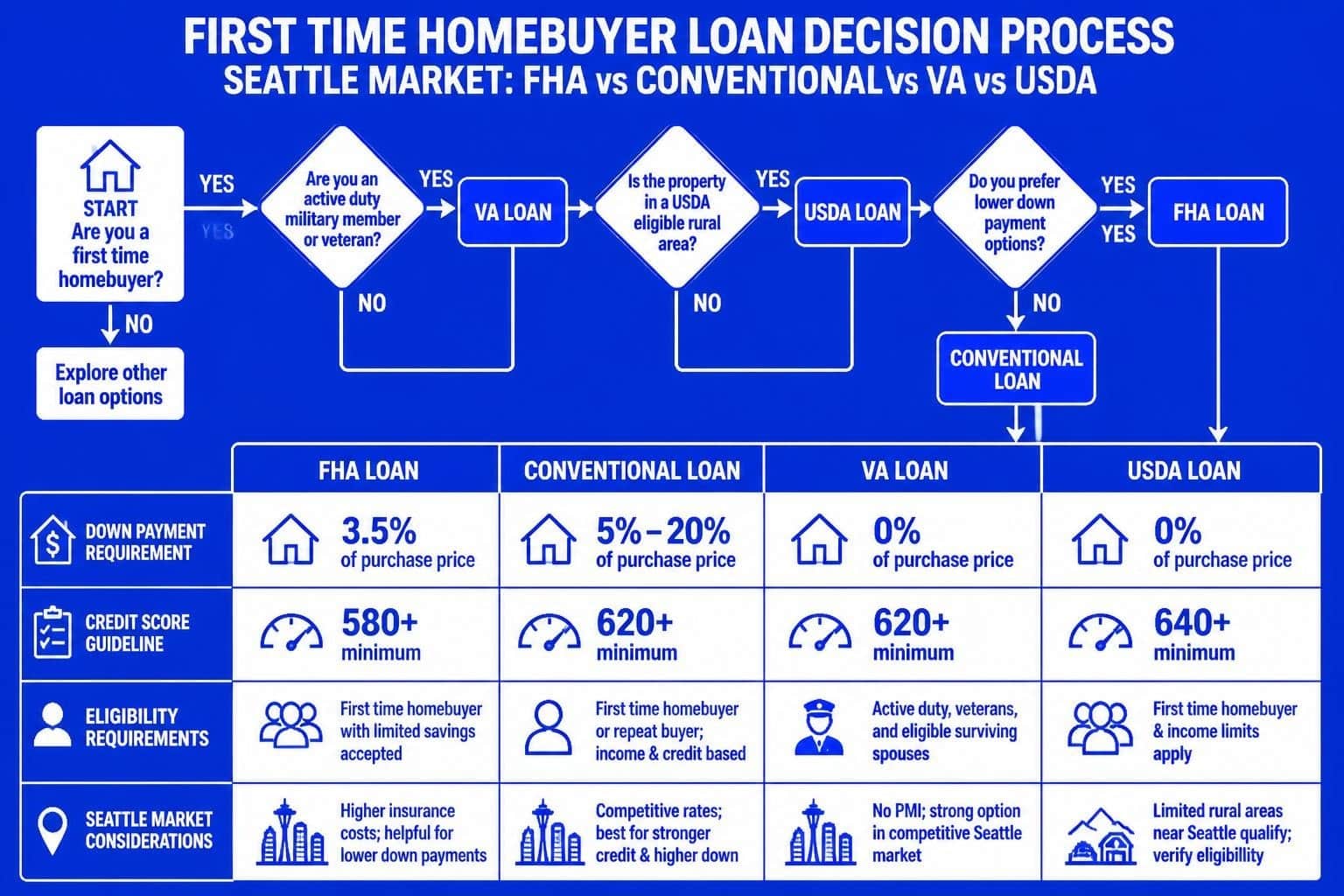

Understanding Loan Products

First time home buyers courses demystify the alphabet soup of mortgage products, explaining when each option makes sense for different buyer profiles. Conventional loans serve many Seattle-area buyers well, but alternatives may offer advantages depending on your circumstances.

| Loan Type | Minimum Down Payment | Credit Score Requirement | Best For |

|---|---|---|---|

| Conventional | 3% | 620+ | Strong credit, stable employment |

| FHA | 3.5% | 580+ | Lower credit scores, smaller down payments |

| VA | 0% | No minimum | Military service members and veterans |

| USDA | 0% | 640+ | Rural/suburban properties outside metro areas |

Courses explain how mortgage insurance works, when it's required, and how to eventually eliminate this expense through refinancing or reaching 20% equity.

Down Payment and Closing Cost Planning

Detailed financial planning instruction helps you determine realistic savings goals and timelines. Most first time home buyers courses cover creative down payment strategies beyond traditional savings, including:

- Employer assistance programs offered by major Seattle companies

- Gift funds from family members and proper documentation procedures

- Down payment assistance grants and loans available through state programs

- IRA withdrawal exceptions for first-time home purchases

- Rent-to-own arrangements and seller financing

Understanding down payment requirements specific to different loan products helps you set achievable goals aligned with your timeline and budget.

The Search and Offer Process

Beyond financial preparation, courses provide practical guidance on working with real estate professionals, evaluating properties, and crafting competitive offers. This proves invaluable in markets like Redmond and Bellevue where desirable homes often receive multiple offers within days of listing.

You'll learn about:

- Choosing qualified buyer's agents and understanding agency relationships

- Identifying deal-breakers versus negotiable issues during home tours

- Writing strong offers with appropriate contingencies

- Navigating inspection findings and requesting repairs

- Understanding appraisal gaps and strategies for addressing them

Special Considerations for Seattle-Area Buyers

First time home buyers courses often incorporate regional content, but supplementing general education with local market knowledge proves essential for success in the Greater Seattle area.

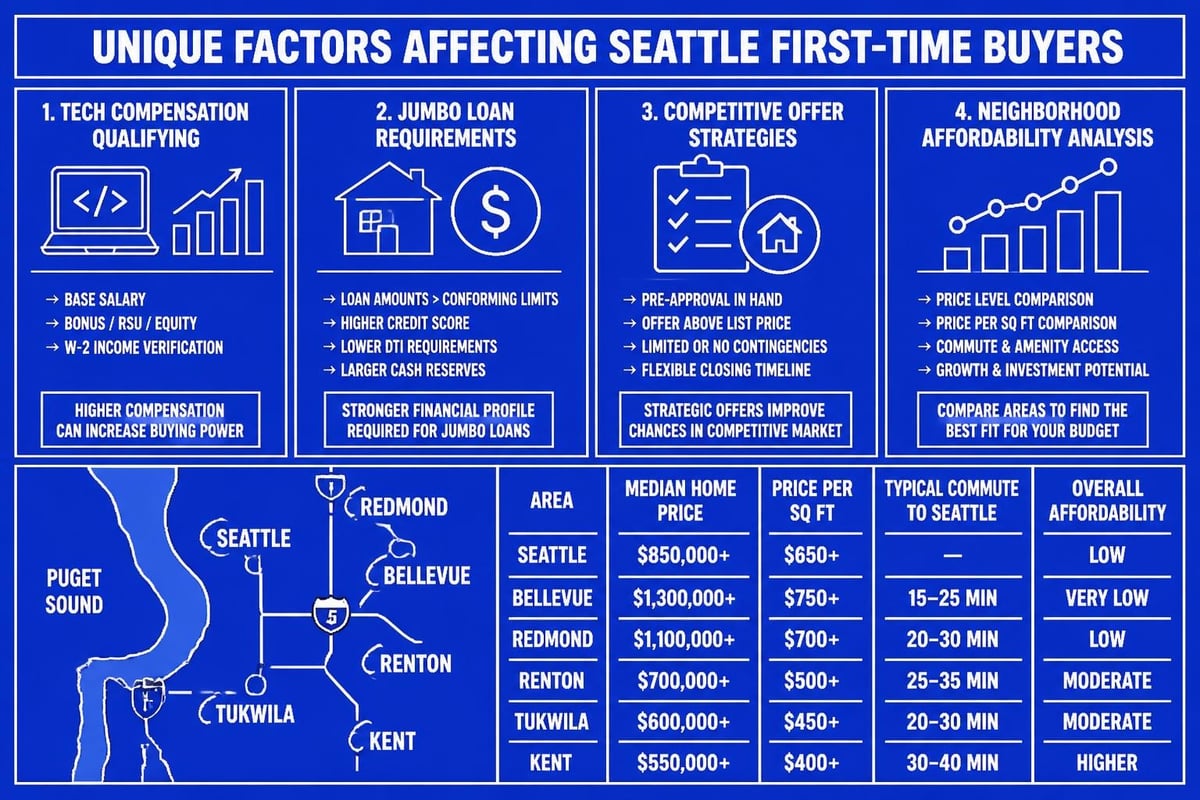

Tech Compensation Complexities

Amazon, Microsoft, and Google employees face unique challenges when qualifying for mortgages due to compensation structures heavily weighted toward stock grants and bonuses. While many first time home buyers courses cover basic income documentation, few address the nuances of qualifying RSUs and unvested stock options.

Critical considerations include:

- Two-year history requirements for bonus and commission income

- Treatment of stock compensation as stable income versus one-time events

- Documentation needed for equity grants and vesting schedules

- Impact of employer stock purchase programs on qualifying income

- Strategies for maximizing buying power with variable compensation

Working with mortgage professionals experienced in tech compensation ensures you present your income optimally to underwriters.

Jumbo Loan Realities

Seattle's median home prices often exceed conforming loan limits, pushing many first-time buyers into jumbo loan territory. Standard first time home buyers courses may not adequately cover jumbo financing requirements, which differ significantly from conventional mortgages.

Jumbo loan distinctions:

- Higher credit score requirements, typically 700+

- Larger down payments, often 10-20% minimum

- More extensive documentation and asset verification

- Multiple appraisals required in some cases

- Stricter debt-to-income ratio standards

Competitive Market Strategies

Seattle's limited housing inventory creates intense competition for well-priced properties. Effective first time home buyers courses address strategies for succeeding in seller's markets, including:

- Pre-approval strength: Understanding the difference between pre-qualification and full underwriting approval

- Escalation clauses: When they make sense and how to structure them safely

- Waiving contingencies: Risks and benefits of removing inspection or appraisal contingencies

- Backup offers: Positioning yourself if the primary offer falls through

- New construction: Working with builders and understanding purchase agreements

For buyers targeting neighborhoods in Shoreline, Lake Forest Park, or Mill Creek, understanding local market dynamics helps you compete effectively against more experienced buyers.

Maximizing Course Value

Simply attending a first time home buyers course doesn't guarantee success. Strategic engagement and follow-through transforms education into actionable results.

Pre-Course Preparation

Arriving prepared maximizes your learning and allows you to ask specific questions relevant to your situation. Before your first session:

- Pull your credit reports from all three bureaus and review for accuracy

- Gather recent pay stubs, tax returns, and bank statements

- Calculate your current monthly debts and income

- List questions about your specific circumstances

- Research neighborhoods and price ranges of interest

This preparation helps instructors provide targeted guidance rather than generic advice.

Active Participation

Engage fully during sessions by asking questions, participating in exercises, and connecting concepts to your personal situation. Many courses include case studies and scenarios-use these opportunities to practice decision-making in low-stakes environments.

Build relationships with other participants who may become valuable resources during your home search, particularly those targeting similar neighborhoods or price points in the Seattle area.

Post-Course Action Steps

Education without implementation delivers limited value. After completing your course, take immediate action:

- Schedule consultations with recommended lenders to compare mortgage options

- Interview buyer's agents who specialize in your target neighborhoods

- Apply for down payment assistance programs requiring course certificates

- Address credit issues identified during the course

- Establish or accelerate your down payment savings plan

Setting specific timelines for each action step maintains momentum and prevents procrastination that can delay your purchase by months or years.

Cost Considerations and Free Options

First time home buyers courses range from completely free to several hundred dollars depending on format, provider, and certification level. Understanding cost structures helps you select appropriate programs without overpaying for unnecessary features.

Free Course Offerings

Numerous organizations provide free education to remove financial barriers for prospective homeowners. Non-profit housing counseling agencies, credit unions, and community development organizations frequently sponsor no-cost programs.

Common free course providers:

- HUD-approved housing counseling agencies

- Local credit unions and community banks

- Non-profit housing organizations

- State housing finance authorities

- Employer-sponsored programs through benefits departments

While free courses deliver comparable content to paid versions, they may have limited availability or longer wait times for scheduling.

Paid Program Benefits

Fee-based first time home buyers courses often provide additional resources, smaller class sizes, and more personalized attention. Typical costs range from $50 for online self-paced options to $300 for comprehensive in-person workshops with ongoing counseling access.

Premium features may include:

- Personalized financial action plans

- One-on-one counseling sessions beyond group instruction

- Ongoing support throughout your home search and closing

- Advanced tools like affordability calculators and budget spreadsheets

- Priority access to down payment assistance programs

For many Seattle-area buyers, the relatively modest investment pays dividends through better preparation and potential qualification for thousands in assistance funds.

Timing Your Course Completion

Strategic timing of your first time home buyers course completion can significantly impact your purchasing timeline and success rate. While education is valuable at any stage, optimal timing maximizes immediate application of knowledge.

Ideal Timeline

Most experts recommend completing your course 6-12 months before you plan to actively search for homes. This window allows sufficient time to:

- Address credit issues identified during the course

- Build additional down payment savings

- Research neighborhoods and refine your criteria

- Interview and select real estate professionals

- Monitor market conditions and price trends

Starting too early risks information becoming outdated, particularly regarding specific programs or lending requirements that change annually. Beginning too late leaves insufficient time to address qualification obstacles discovered through education.

Market Condition Considerations

In rapidly appreciating markets like Seattle, Bellevue, and Redmond, balancing education with market timing becomes critical. If prices are rising quickly, delaying your purchase for extensive preparation may cost more in price appreciation than you save through better negotiation skills.

Conversely, in stabilizing or declining markets, taking time for thorough education typically proves worthwhile without significant opportunity cost.

Seasonal Factors

Real estate markets exhibit seasonal patterns, with spring and summer bringing increased inventory and competition. Completing your course in late fall or winter positions you to act quickly when desirable properties emerge in slower seasons, often with less competition and more negotiation leverage.

For first-time buyers in Seattle neighborhoods, understanding these patterns helps you time both education and purchasing strategically.

Beyond the Course: Continuing Education

First time home buyers courses provide foundational knowledge, but successful homeownership requires ongoing learning and adaptation. Markets evolve, regulations change, and your financial situation develops over time.

Staying Informed

After course completion, maintain your knowledge through:

- Following reputable real estate and mortgage industry publications

- Attending homeownership workshops offered by community organizations

- Joining local first-time buyer groups or online communities

- Consulting with experienced mortgage brokers who provide ongoing education

- Monitoring changes to assistance programs and lending requirements

Building relationships with trusted professionals who prioritize education ensures you receive updates on opportunities and avoid pitfalls.

Advanced Topics

As you progress from course graduate to active buyer, investigate advanced topics relevant to your specific situation:

- Investment property considerations if you plan to rent out space

- Tax implications of homeownership and mortgage interest deductions

- Refinancing strategies for optimizing your mortgage over time

- Home equity management and responsible borrowing practices

- Long-term maintenance planning and budgeting

These advanced concepts build upon your foundational education, transforming you from an informed buyer into a sophisticated homeowner.

Common Misconceptions Addressed

First time home buyers courses help dispel prevalent myths that can derail purchasing plans or lead to poor decisions. Understanding what's actually true versus common misconceptions prevents costly mistakes.

Myth 1: You need 20% down payment

Reality: Numerous programs accept 3-5% down, and some require zero down payment for qualified buyers. The 20% threshold eliminates mortgage insurance but isn't mandatory for purchase.

Myth 2: Perfect credit is required

Reality: While higher scores secure better rates, many mortgage programs accept scores as low as 580. Focus on improvement rather than perfection.

Myth 3: Pre-qualification equals approval

Reality: Pre-qualification involves basic information review, while pre-approval requires full documentation and underwriting analysis. Only pre-approval carries significant weight in competitive markets.

Myth 4: You must use the lender your agent recommends

Reality: While agent referrals can be valuable, you should compare multiple lenders to ensure competitive rates and terms that match your needs.

Myth 5: Closing costs are fixed

Reality: Many closing costs are negotiable, and some sellers may cover portions depending on market conditions and negotiation strength.

Quality first time home buyers courses systematically address these misconceptions, replacing them with accurate information that empowers better decision-making.

First time home buyers courses transform overwhelming complexity into manageable steps, equipping you with knowledge that strengthens your purchasing power and confidence throughout the home buying journey. Whether you're a tech professional in Redmond navigating stock compensation or a family in Lynnwood seeking down payment assistance, structured education provides the foundation for successful homeownership. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area buyers translate education into action, specializing in complex income qualifying and fast closings that meet your timeline. With 750+ five-star reviews and expertise serving Amazon, Microsoft, and Google employees, we provide the transparency and strategic guidance that turns first-time buyers into confident homeowners.