Understanding the relationship between your down payment and mortgage is fundamental to making confident homebuying decisions in Seattle's competitive real estate market. Whether you're a first-time buyer navigating Capitol Hill condos or a tech professional pursuing a jumbo loan in Bellevue, the amount you put down shapes everything from your monthly payment to your interest rate and long-term equity position. This comprehensive guide breaks down how down payment and mortgage choices work together to help you build a strategic financing plan.

How Down Payment Size Impacts Your Mortgage Terms

The down payment you provide directly influences several critical aspects of your mortgage financing. Lenders view larger down payments as reduced risk, which often translates to better loan terms and lower ongoing costs.

Interest Rate Benefits

Borrowers who put down 20% or more typically qualify for lower interest rates compared to those making minimum down payments. This difference might seem small-often 0.125% to 0.375%-but over a 30-year mortgage on a $800,000 home in Redmond, that variance can mean tens of thousands of dollars in interest savings.

Key rate factors influenced by down payment:

- Loan-to-value ratio (LTV) determines risk pricing

- Higher equity positions receive preferential pricing

- Conventional loans offer clearest rate advantages at 20% down

- Jumbo loans may require 10-20% down for optimal rates

Many Seattle-area tech professionals wonder how RSU income affects mortgage qualification when planning their down payment strategy. Stock compensation can be counted toward both income qualification and down payment funds, provided proper documentation and vesting schedules are verified.

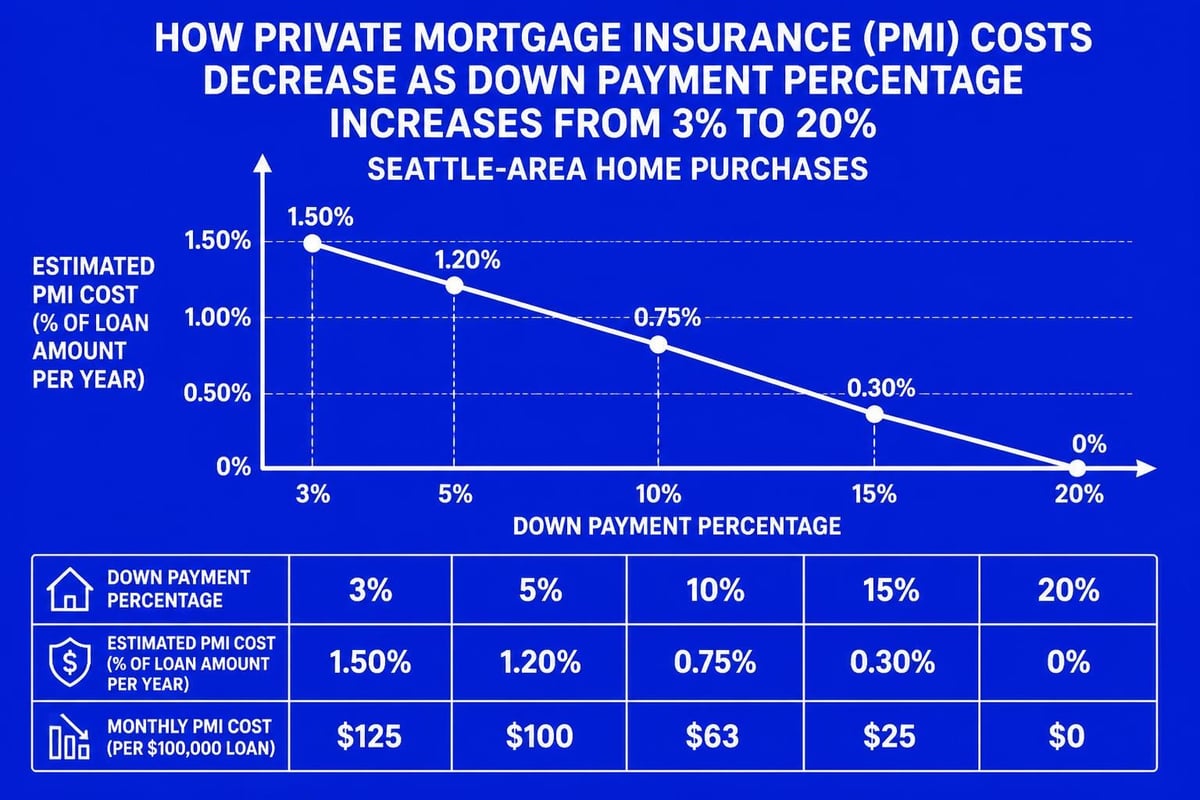

Private Mortgage Insurance Considerations

When you put down less than 20% on a conventional loan, lenders require private mortgage insurance (PMI). This protects the lender if you default, but it increases your monthly housing costs significantly.

| Down Payment | PMI Requirement | Approximate Monthly PMI (on $700,000) |

|---|---|---|

| 3-5% | Yes | $350-$450 |

| 10% | Yes | $250-$325 |

| 15% | Yes | $150-$200 |

| 20%+ | No | $0 |

PMI typically costs 0.5% to 1.5% of the original loan amount annually, divided into monthly payments. For a $665,000 loan (5% down on a $700,000 home), you might pay $300-$400 monthly until you reach 20% equity through payments and appreciation.

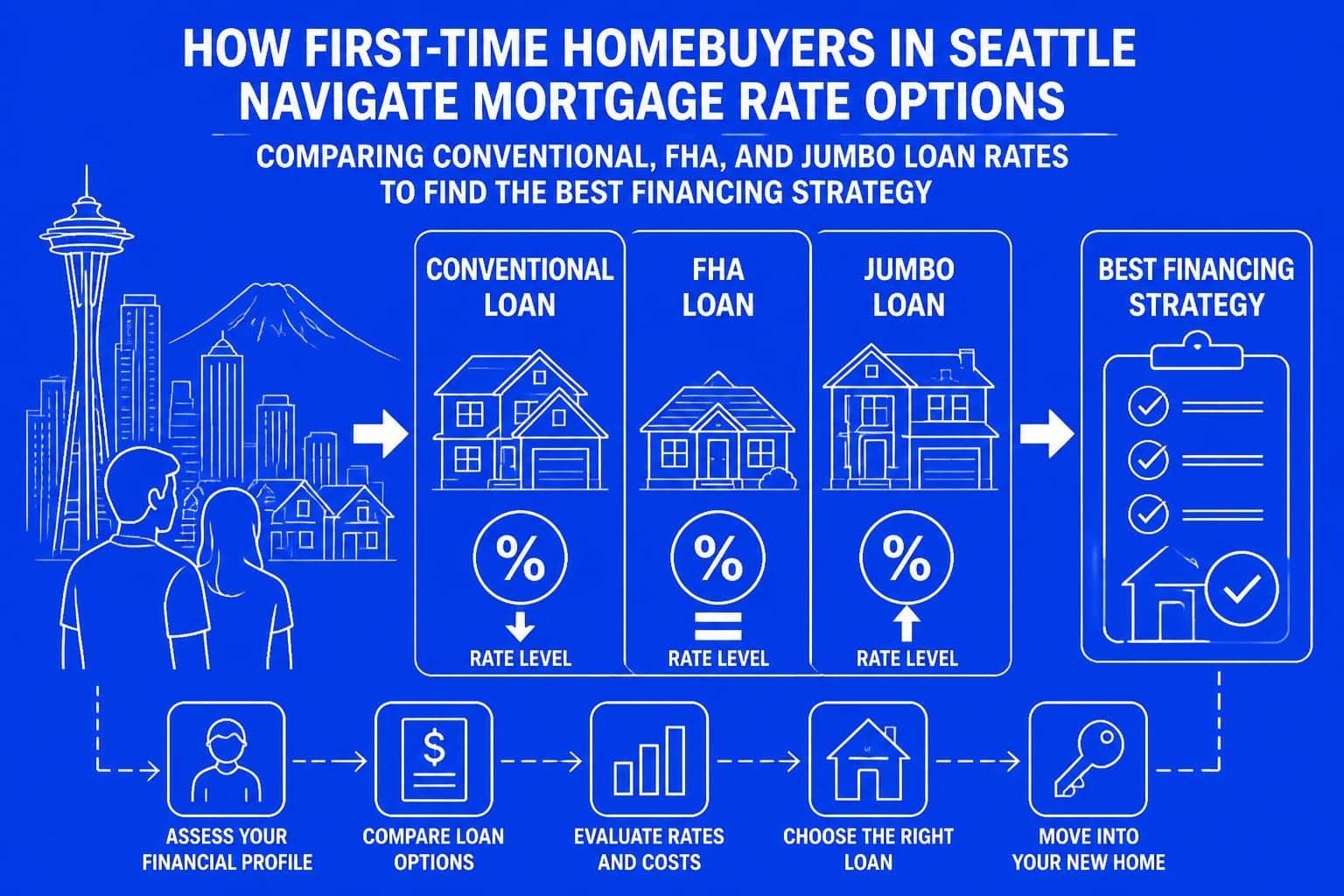

Down Payment Requirements Across Loan Programs

Different mortgage programs have varying down payment minimums, each designed to serve specific borrower profiles and financial situations. Understanding these options helps you identify the most strategic path forward.

Conventional Loan Down Payments

Conventional loans represent the most flexible financing option for many Seattle homebuyers. These loans, backed by Fannie Mae or Freddie Mac, offer multiple down payment tiers.

Standard conventional down payment options:

- 3% down for first-time buyers

- 5% down for repeat buyers (standard minimum)

- 10% down for improved rates and lower PMI

- 20% down to eliminate PMI entirely

The conventional loan down payment requirements vary based on whether you're purchasing a primary residence, second home, or investment property. Investment properties typically require 15-25% down, while second homes need at least 10%.

FHA Loan Requirements

Federal Housing Administration loans serve buyers who may have lower credit scores or smaller down payment reserves. The FHA home loan down payment minimum is 3.5% with a credit score of 580 or higher.

FHA loans require both upfront and annual mortgage insurance premiums regardless of down payment size. Even if you put down 20%, you'll pay mortgage insurance for the loan's life unless you put down at least 10%, which allows removal after 11 years.

Jumbo Loan Down Payment Strategies

Seattle's high home prices mean many buyers need jumbo financing. King County's conforming loan limit for 2026 is $806,500 for single-family homes, so properties above this threshold require jumbo loans.

Jumbo loan requirements are more stringent, but down payment flexibility exists. While 20% down is traditional, many lenders now offer 10% down jumbo programs for well-qualified borrowers with strong credit and substantial reserves.

Should you put 10% or 20% down on a jumbo loan? The answer depends on your cash position, opportunity cost of capital, and whether you have other high-return investment opportunities for those funds.

Calculating What You Can Afford

Understanding the down payment and mortgage relationship requires looking beyond just the minimum required. Your total upfront investment includes several components that affect your purchasing power.

Complete Upfront Cost Breakdown

When planning your home purchase in Shoreline or Lynnwood, budget for these typical costs:

- Down payment (3-20% of purchase price)

- Closing costs (2-5% of purchase price)

- Earnest money deposit (1-3% of purchase price, credited at closing)

- Prepaid items (property taxes, insurance, interest)

- Reserves (2-12 months of payments, depending on loan type)

For a $750,000 home with 10% down, your total cash needed at closing might be $115,000-$130,000 when factoring in all costs. This includes the $75,000 down payment plus approximately $15,000-$22,500 in closing costs and $25,000-$32,500 in prepaids and reserves.

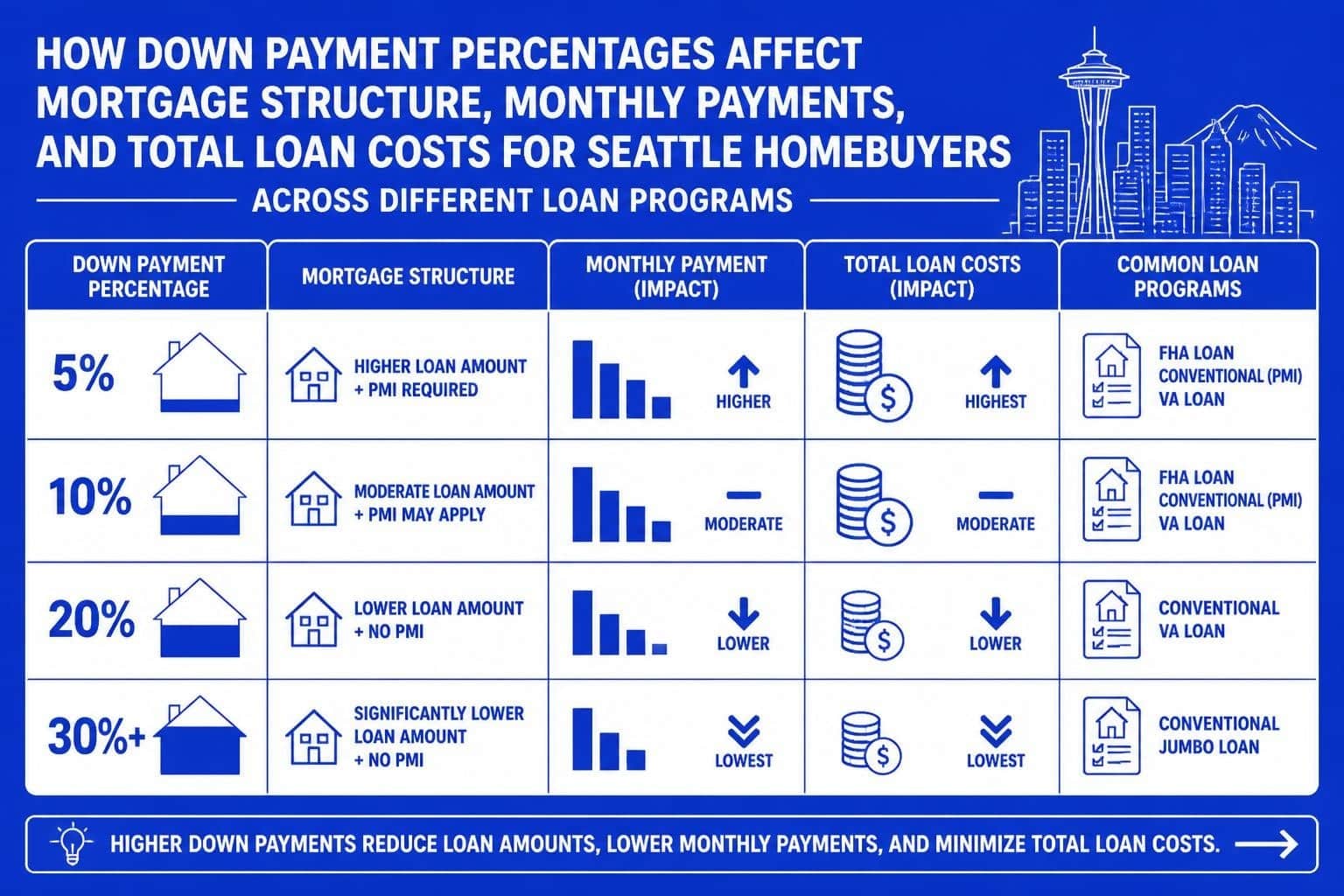

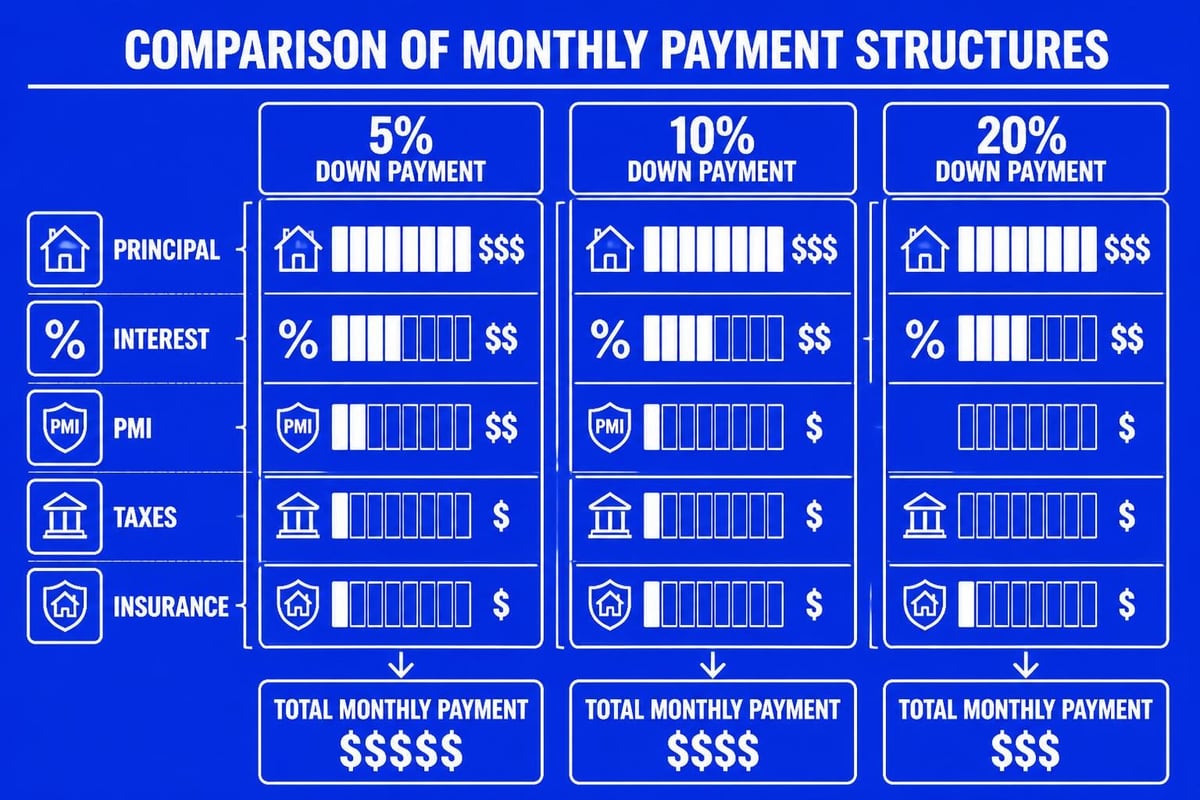

Monthly Payment Implications

Your down payment percentage dramatically affects monthly obligations. Consider these scenarios for a $700,000 home purchase in Kirkland with a 7% interest rate:

| Down Payment | Loan Amount | Monthly P&I | PMI | Total Payment* |

|---|---|---|---|---|

| 5% ($35,000) | $665,000 | $4,423 | $350 | $5,523 |

| 10% ($70,000) | $630,000 | $4,190 | $275 | $5,215 |

| 20% ($140,000) | $560,000 | $3,724 | $0 | $4,474 |

*Includes estimated property tax and insurance ($750/month)

The difference between 5% and 20% down results in over $1,000 monthly savings-$12,600 annually. Over five years, that's $63,000 in reduced payments, though you needed an additional $105,000 upfront to achieve it.

Strategic Down Payment Planning for Seattle Buyers

The optimal down payment strategy balances immediate cash outlay against long-term costs and opportunity. Seattle's market dynamics add unique considerations to this equation.

Market Competition Factors

In competitive Seattle neighborhoods like Lake Forest Park and Mill Creek, larger down payments can strengthen your offer. Sellers and their agents view 20%+ down payments as indicators of financial stability and lower contingency risk.

Cash offers obviously win bidding wars, but strong financing with substantial down payments runs a close second. When competing against multiple offers, demonstrating 15-20% down with quick closing capability often edges out minimum down payment scenarios.

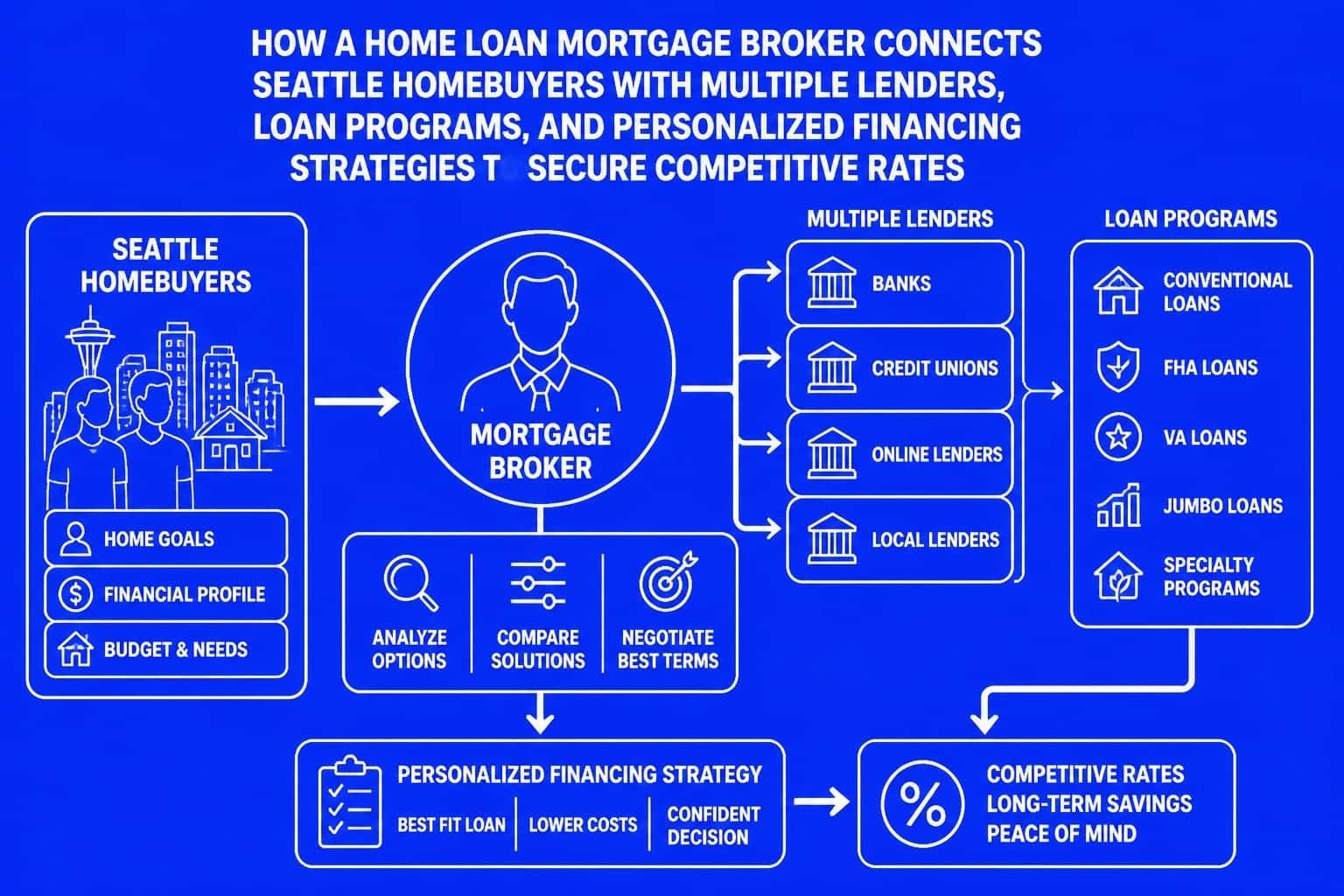

Working with an experienced Seattle mortgage broker who can provide pre-approval credibility and fast closing timelines becomes crucial. The ability to close in 9-12 business days with complete documentation can be the deciding factor when sellers compare similar offers.

Preserving Liquidity vs. Reducing Debt

Tech professionals in Seattle face a unique calculation: should you maximize your down payment or preserve capital for other opportunities?

Arguments for larger down payments:

- Eliminate PMI immediately

- Reduce monthly obligations and improve cash flow

- Lower interest rate qualification

- Build equity faster through less interest paid

- Reduce default risk during market downturns

Arguments for minimum down payments:

- Preserve cash for emergencies and opportunities

- Maintain investment capital for higher-return options

- Leverage allows you to buy more house sooner

- Market appreciation may outpace interest costs

- Tax deduction benefits on mortgage interest

For Amazon, Microsoft, and Google employees with RSU-heavy compensation, keeping more liquid assets often makes sense. Your stock compensation continues vesting and potentially appreciating, while mortgage rates remain fixed. If your expected RSU growth exceeds your mortgage rate, minimal down payments can be strategically sound.

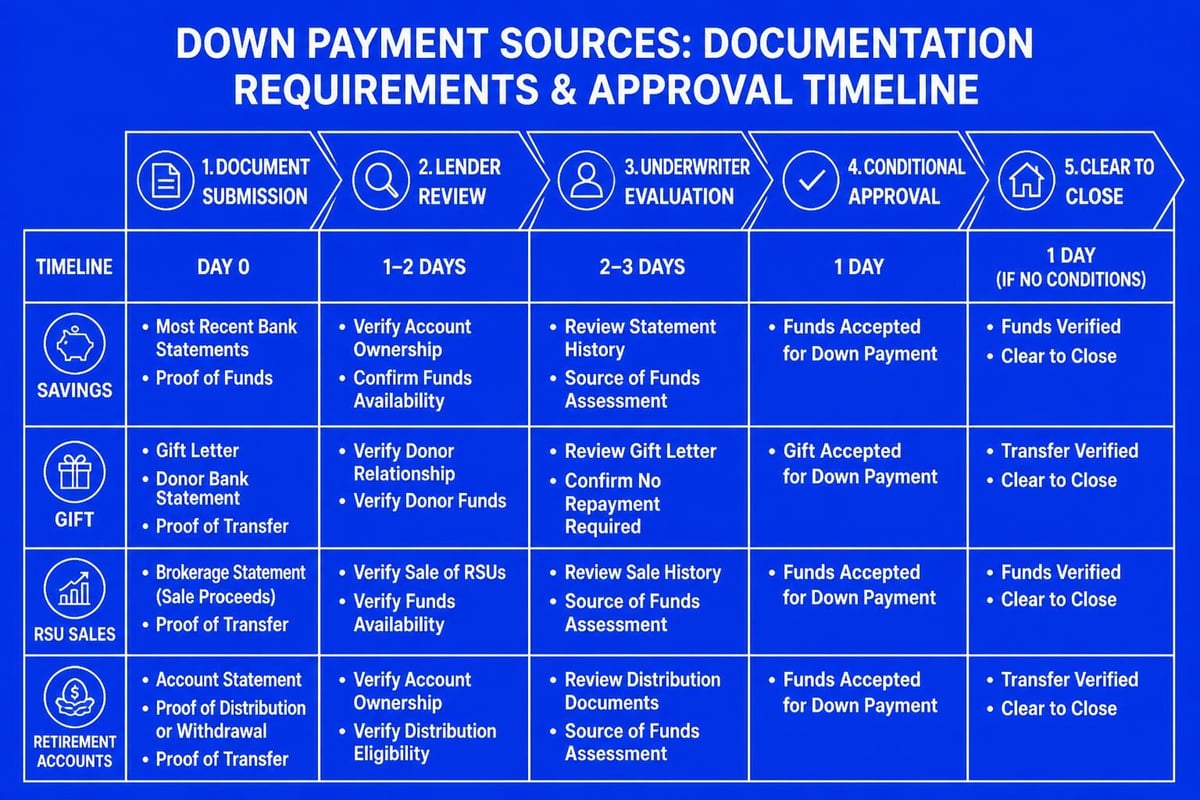

Down Payment Sources and Documentation

Lenders scrutinize down payment sources carefully to ensure funds are legitimate and borrowers aren't taking on hidden debt. Understanding acceptable sources helps you plan properly.

Acceptable Down Payment Sources

Most mortgage programs accept these down payment sources:

- Personal savings and checking accounts

- Investment accounts (stocks, bonds, mutual funds)

- Retirement accounts (401k, IRA with proper documentation)

- Gift funds from qualified family members

- Sale proceeds from another property

- Employer assistance programs

- Grants from government or nonprofit programs

Each source requires specific documentation. Bank statements need 2-3 months of history showing consistent balances. Large deposits require explanation letters and source verification. Gift funds need gift letters stating no repayment expectation, plus documentation of the donor's ability to give.

Seasoning Requirements

"Seasoned" funds have been in your account for at least 60 days, making them easier to verify. Unseasoned funds trigger additional scrutiny and documentation requirements.

If you receive a work bonus, inheritance, or tax refund within 60 days of applying for your mortgage, expect to provide complete paper trails. This might include bonus letters from employers, estate settlement documents, or complete tax returns showing refund amounts.

Special Programs and Assistance Options

Several programs help Seattle-area buyers reduce down payment burdens, particularly for first-time purchasers in Lake Forest Park, Everett, and surrounding communities.

Washington State Housing Finance Commission

The Washington State Housing Finance Commission offers down payment assistance through various programs. These typically provide $15,000-$30,000 in second-lien loans or grants for qualified buyers meeting income limits.

Income limits vary by county and household size, but generally cap around 80-120% of area median income. For King County in 2026, this means roughly $100,000-$150,000 for households of 1-2 people, with higher limits for larger families.

Employer Assistance Programs

Many Seattle tech companies offer homebuying assistance programs. Amazon, Microsoft, and other major employers sometimes provide forgivable loans, grants, or matching programs to help employees purchase homes.

These programs typically require you to remain employed for a specified period (3-5 years) for full forgiveness. They're considered legitimate down payment sources when properly documented and disclosed to your lender.

First-Time Buyer Programs

Despite high prices, first-time buyer programs exist throughout King County and surrounding areas. These programs often combine reduced down payment requirements with seller concessions and closing cost assistance.

The down payment guide for Seattle homebuyers provides comprehensive details on local programs, eligibility requirements, and application processes.

Tax and Financial Planning Considerations

The down payment and mortgage relationship extends into tax strategy and long-term wealth building. Understanding these implications helps optimize your overall financial position.

Mortgage Interest Deduction

The Tax Cuts and Jobs Act of 2017 limited mortgage interest deductions to loans up to $750,000 for married couples ($375,000 for individuals). For Seattle's high-cost market, many jumbo borrowers exceed this threshold.

If your loan amount exceeds $750,000, only the interest on the first $750,000 is deductible. This reality shifts the cost-benefit analysis of minimal down payments on expensive properties, as the tax advantage diminishes.

Opportunity Cost Analysis

Every dollar committed to a down payment represents capital unavailable for other investments. In 2026, with mortgage rates around 6.5-7.5%, the comparison rate for alternative investments becomes crucial.

If you can consistently earn 8-10% annually through index fund investing, putting minimum down and investing the difference mathematically outperforms paying extra principal. However, this assumes consistent returns and ignores the psychological benefit of lower monthly obligations and faster equity building.

Building Long-Term Equity

Larger down payments jumpstart your equity position, which compounds over time through both principal paydown and property appreciation. In Seattle's historically appreciating market (averaging 5-7% annually over the past decade), starting with more equity amplifies your wealth accumulation.

A $700,000 home purchased with 20% down starts you with $140,000 in equity. After one year of 6% appreciation and principal paydown, you might have $195,000 in equity. The same home purchased with 5% down starts with $35,000 equity and reaches approximately $90,000 after one year-still strong growth, but $105,000 less equity built.

Refinancing and Down Payment Considerations

Your initial down payment affects future refinancing opportunities and strategies. Understanding this connection helps you make more informed decisions today.

Removing PMI Through Refinancing

If you initially put down less than 20%, you can refinance to remove PMI once you reach 20% equity through appreciation and principal paydown. In Seattle's appreciating market, this often happens within 2-4 years.

Alternatively, mortgage recast offers a simpler, less expensive option than refinancing. A recast allows you to make a lump sum principal payment and have your monthly payment recalculated without changing your interest rate or resetting your loan term.

Cash-Out Refinancing

Building equity through larger initial down payments creates future cash-out refinancing opportunities. If you put 20% down and your home appreciates 15% over two years, you might have 30-35% equity available for cash-out refinancing while maintaining a strong LTV position.

Tech professionals receiving large RSU vests or bonuses might consider the inheritance money mortgage recast strategy, where you make a substantial principal payment to reduce monthly obligations without a full refinance.

Frequently Asked Questions

How much down payment do I need in Seattle?

Minimum down payments range from 3% for conventional first-time buyers to 3.5% for FHA loans. However, Seattle's competitive market often favors 10-20% down to strengthen offers and reduce monthly costs. Jumbo loans typically require 10-20% depending on the lender and loan amount.

Can I use stock options for my down payment?

Yes, vested stock compensation can be used for down payments. You'll need documentation showing vesting schedules, recent statements, and potentially liquidation confirmation. Unvested RSUs cannot be counted as available funds, though they may qualify as income for debt-to-income calculations.

Is 5% down enough in a competitive market?

While 5% down is acceptable for many loan programs, competitive Seattle neighborhoods may favor higher down payments. Sellers often view larger down payments as lower-risk transactions. Consider your offer strategy, property type, and market conditions when determining optimal down payment size.

How does down payment affect my buying power?

Larger down payments reduce your loan amount, potentially keeping you under jumbo loan thresholds and qualifying you for better rates. However, your buying power is primarily limited by income and debt-to-income ratios, not down payment size. More down payment doesn't necessarily mean you can afford a more expensive home.

Should I drain savings for a 20% down payment?

Maintain adequate emergency reserves (3-6 months of expenses) even after your down payment. If achieving 20% down depletes all savings, consider 10-15% down while preserving financial cushion. Job security, family situation, and risk tolerance should guide this decision.

Understanding the relationship between down payment and mortgage strategy empowers you to make confident financing decisions aligned with your financial goals and market realities. Whether you're maximizing buying power with minimal down payment or building equity quickly with substantial upfront investment, the optimal approach depends on your unique situation. Keith Akada and the team at Mortgage Reel specialize in helping Seattle-area homebuyers navigate these decisions with transparency and expertise, offering personalized strategies that account for stock compensation, competitive offer dynamics, and long-term wealth building. With 750+ five-star reviews and the ability to close in as few as 9 business days, we're ready to help you develop your optimal down payment and mortgage strategy.