Understanding the mortgage broker price is essential for Seattle homebuyers navigating one of the nation's most competitive housing markets. Whether you're purchasing your first condo in Capitol Hill, upgrading to a larger home in Bellevue, or securing a jumbo loan for a waterfront property in Kirkland, knowing how mortgage brokers are compensated helps you make informed financial decisions. The cost structure varies significantly based on loan type, lender relationships, and compensation models, making transparency critical when choosing who will guide your home financing journey.

How Mortgage Broker Pricing Works in Seattle

The mortgage broker price encompasses several compensation models that directly impact what you pay as a borrower. Most brokers earn between 1% and 2% of the loan amount, though this percentage can vary based on loan complexity and size. In Seattle's high-value housing market, where median home prices exceed $800,000 in many neighborhoods, understanding these percentages becomes particularly important.

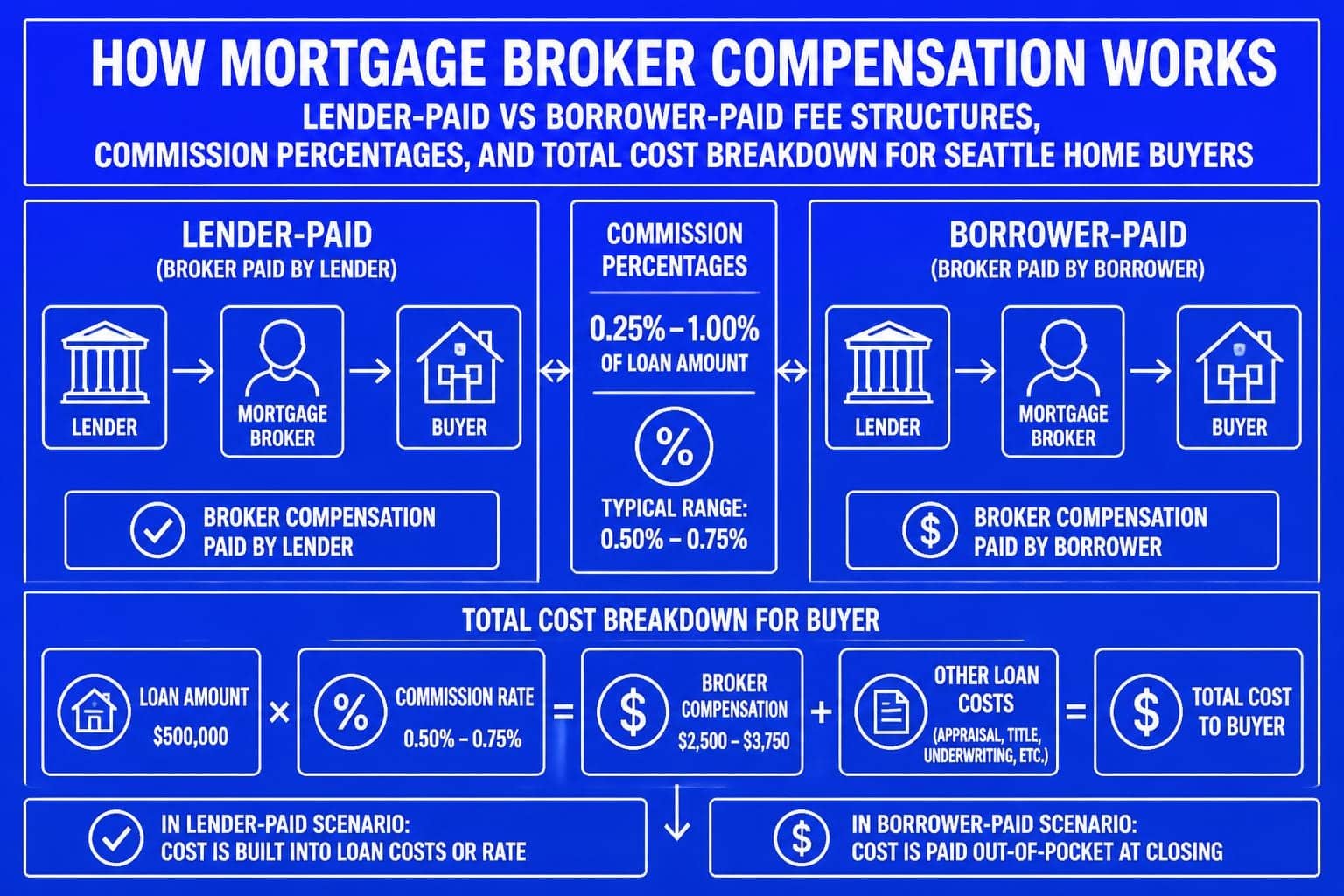

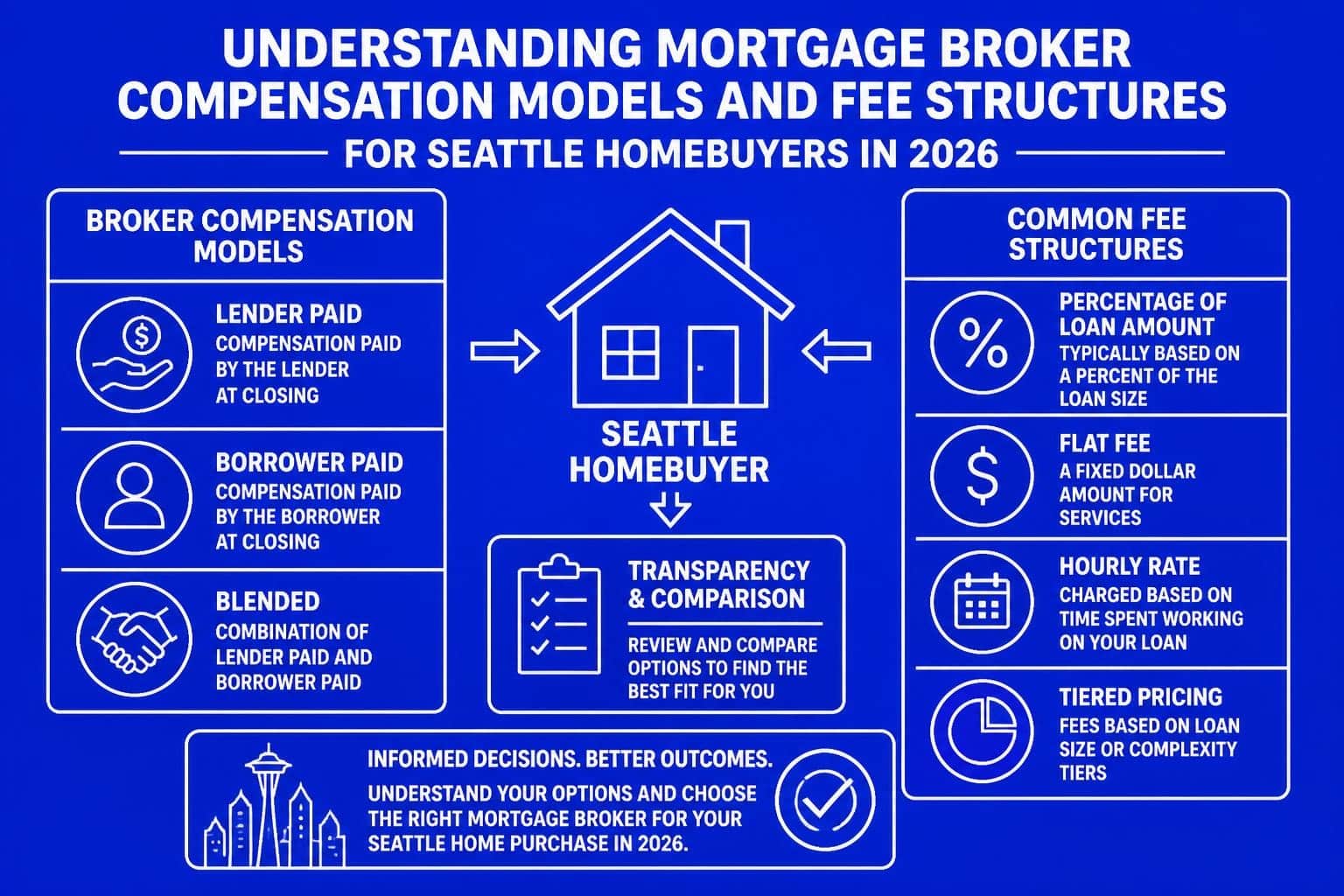

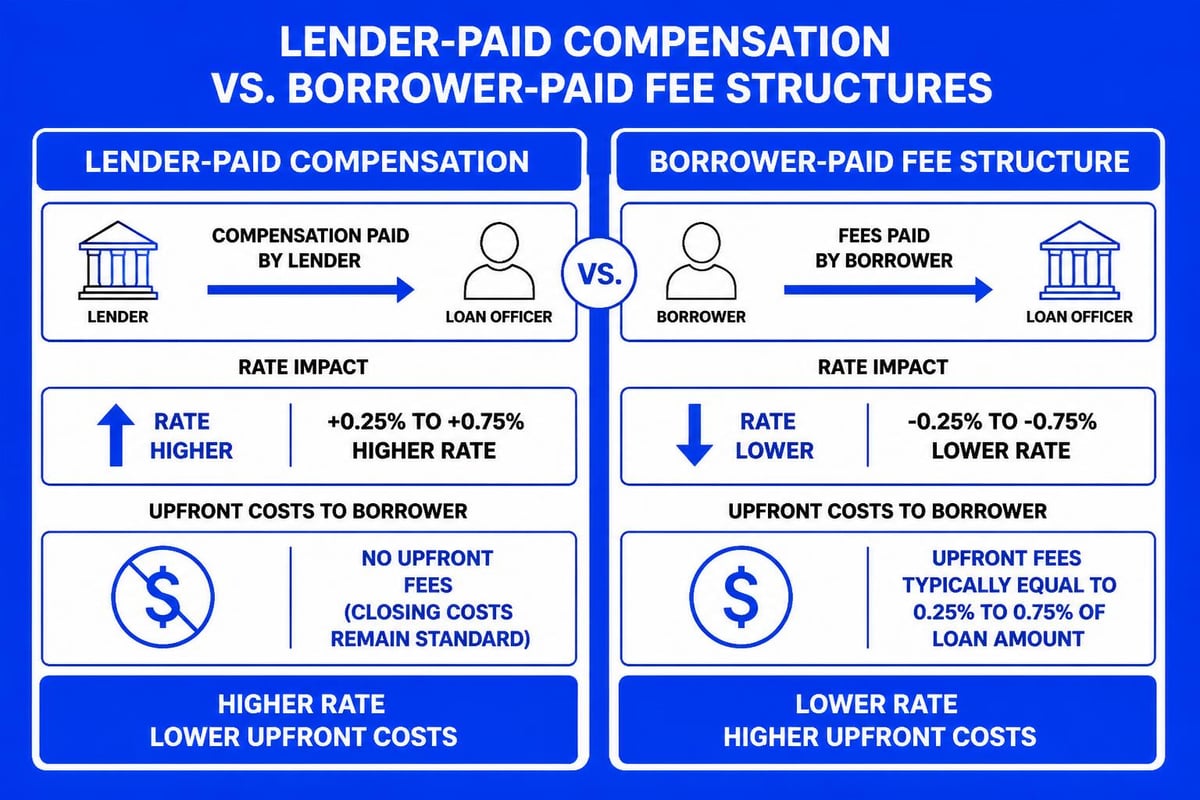

Brokers typically receive compensation through three primary structures: lender-paid compensation, borrower-paid fees, or a hybrid combination of both. The lender-paid model allows lenders to compensate brokers directly from their wholesale pricing, while borrower-paid fees involve direct charges to the homebuyer.

Lender-Paid Compensation Models

When lenders compensate brokers directly, the mortgage broker price is built into the interest rate rather than charged as an upfront fee. This arrangement benefits borrowers who prefer to minimize out-of-pocket closing costs, a common preference among first-time buyers in Seattle's competitive market.

Key advantages of lender-paid compensation:

- No direct broker fees at closing

- Lower upfront cash requirements

- Simplified closing cost calculations

- Competitive with bank direct lending

The trade-off typically involves a slightly higher interest rate, usually between 0.125% and 0.25% above the wholesale rate. For a $700,000 conventional loan in Redmond, this might translate to an additional $50-$100 monthly payment but saves $7,000-$14,000 in upfront broker fees.

Borrower-Paid Fee Structures

Some brokers charge direct fees to borrowers in exchange for accessing the lowest available interest rates. This mortgage broker price approach works well for buyers with substantial down payments who plan to hold their loans long-term, making the upfront investment worthwhile through monthly payment savings.

| Fee Type | Typical Range | When It Makes Sense |

|---|---|---|

| Origination Fee | 0.5% – 1.5% | Larger loan amounts, long-term ownership |

| Processing Fee | $300 – $800 | Streamlined transactions |

| Administration Fee | $200 – $500 | Complex income documentation |

| Underwriting Fee | $400 – $900 | Jumbo loans, non-traditional income |

For tech professionals in Seattle earning RSU compensation, working with specialists who understand how to qualify stock income for mortgages often justifies higher broker fees through superior loan structuring and faster approvals.

Federal Regulations Governing Mortgage Broker Prices

The mortgage broker price is heavily regulated by federal law to protect consumers from predatory practices. The Dodd-Frank Wall Street Reform Act established strict guidelines requiring full disclosure of all broker compensation and prohibiting certain payment structures that created conflicts of interest.

Brokers must now provide detailed Loan Estimates within three business days of application, clearly itemizing all fees and compensation. Federal regulations cap broker fees and require transparency about whether compensation comes from borrowers, lenders, or both sources.

Disclosure Requirements for Seattle Borrowers

Washington State adds additional consumer protections beyond federal requirements. Licensed mortgage brokers must provide:

- Complete fee breakdowns in the initial Loan Estimate

- Written explanations of compensation sources

- Comparative rate sheets showing different pricing scenarios

- Good Faith Estimate accuracy within specified tolerances

- Final disclosure at least three days before closing

These regulations ensure Seattle homebuyers in neighborhoods from Shoreline to Mill Creek receive consistent, transparent information about the mortgage broker price before committing to any loan program.

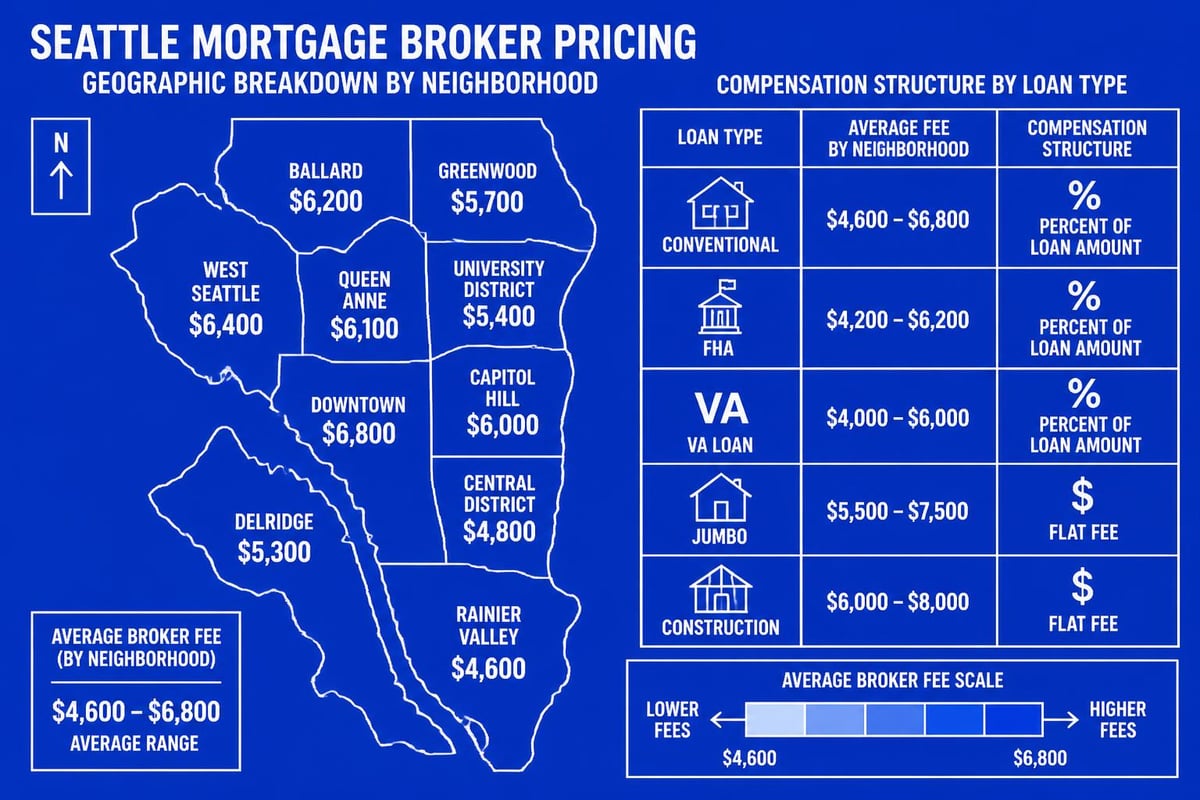

Comparing Mortgage Broker Prices Across Seattle Markets

The mortgage broker price varies based on property location, loan amount, and market conditions across the Greater Seattle area. Jumbo loans above $766,550 (the 2026 conforming loan limit for King County) typically command higher broker fees due to increased complexity and risk.

Regional pricing considerations:

- Downtown Seattle & Bellevue: Higher property values often mean larger dollar amounts in fees but similar percentages

- Shoreline & Lake Forest Park: Mid-range pricing with competitive broker options

- Lynnwood & Everett: Slightly lower average fees due to more moderate home prices

- Kirkland & Redmond: Tech-focused communities with brokers specializing in equity compensation

Buyers pursuing conventional loan options generally pay standard broker fees, while government-backed FHA and VA loans have regulated fee caps that limit maximum charges.

What Seattle Homebuyers Actually Pay

Real-world mortgage broker price examples help clarify what buyers can expect in 2026's Seattle market. The total cost depends on loan size, property type, and chosen compensation structure.

Sample Scenarios for Common Seattle Purchases

First-time buyer in Lake Forest Park:

- Purchase price: $625,000

- Loan amount: $500,000 (20% down)

- Lender-paid compensation: 1.25%

- Borrower cost: $0 upfront, rate increase of 0.125%

- Monthly payment impact: Approximately $42

Tech professional buying in Redmond:

- Purchase price: $1,100,000

- Loan amount: $880,000 (jumbo loan)

- Broker origination fee: 1%

- Borrower cost: $8,800 upfront

- Rate savings: 0.25% below lender-paid option

Investment property in Everett:

- Purchase price: $485,000

- Loan amount: $388,000 (20% down)

- Hybrid compensation: 0.5% broker fee + lender credit

- Borrower cost: $1,940 upfront

- Balanced approach with moderate rate

Understanding how mortgage financing works helps buyers evaluate whether paying direct broker fees or accepting higher rates makes more financial sense for their specific situation.

Negotiating Mortgage Broker Prices

The mortgage broker price is often negotiable, particularly for experienced buyers, large loan amounts, or clients with exceptional credit profiles. Brokers have flexibility within their compensation structures and may reduce fees to secure business in competitive situations.

Successful negotiation strategies include:

- Obtaining multiple Loan Estimates for comparison

- Highlighting strong credit scores (740+) and stable employment

- Demonstrating significant assets and low debt-to-income ratios

- Discussing long-term relationship potential for future refinances

- Timing applications during slower market periods

Seattle's real estate market moves quickly, but working with a local broker who understands neighborhood dynamics from Capitol Hill to Mill Creek provides advantages that extend beyond simple price comparisons.

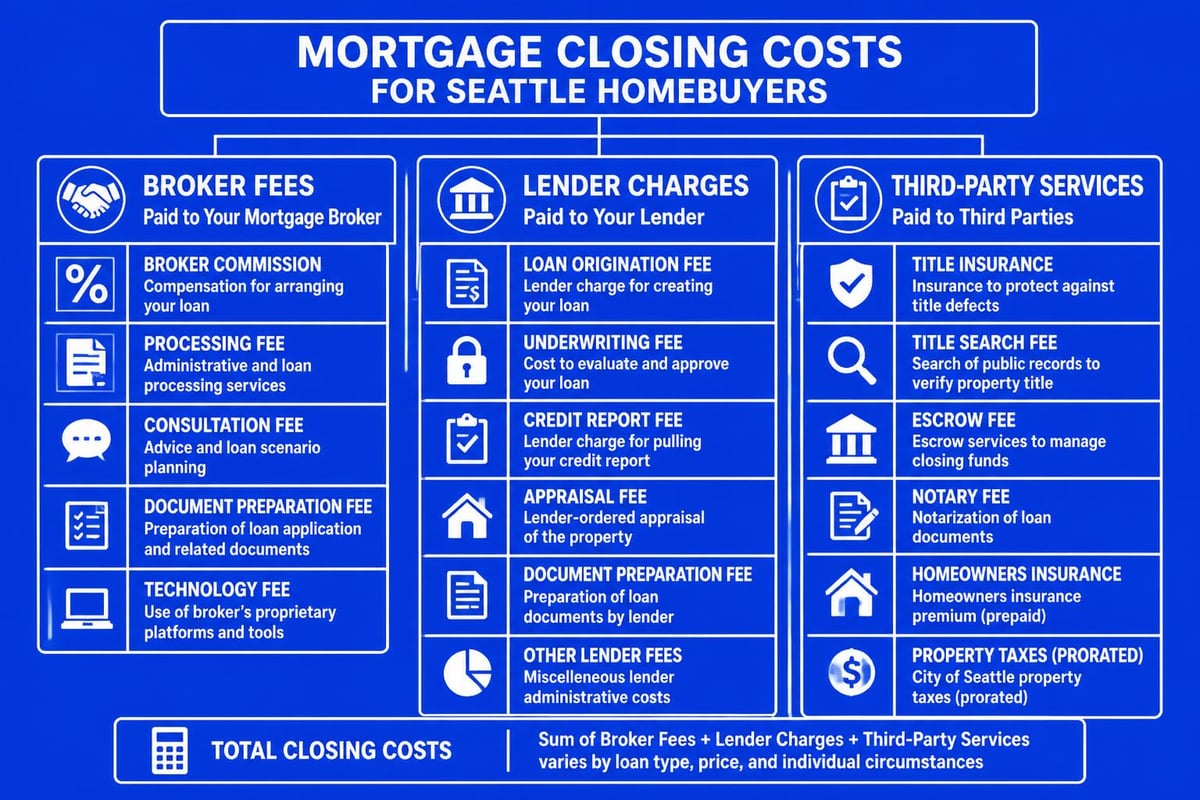

Hidden Costs Beyond Basic Broker Fees

While the primary mortgage broker price appears clearly on Loan Estimates, borrowers should understand the complete cost picture. Some brokers charge administrative fees, processing fees, or documentation fees that increase total costs beyond the standard origination percentage.

| Additional Fee | Typical Cost | Purpose | Negotiability |

|---|---|---|---|

| Application Fee | $200 – $500 | Initial processing | Often refundable |

| Credit Report | $30 – $75 | Tri-merge report | Standard cost |

| Appraisal Fee | $500 – $800 | Property valuation | Market rate |

| Title Services | $1,200 – $2,000 | Legal transfer | Competitive |

| Tax Service Fee | $75 – $95 | Tax monitoring | Limited |

Understanding mortgage payment components helps buyers distinguish between broker-controlled fees and third-party costs required regardless of who originates the loan.

Mortgage Broker Price vs. Bank Direct Lending

Comparing the mortgage broker price to direct bank lending reveals important distinctions. Banks employ loan officers as salaried or commissioned employees, while brokers operate as independent professionals accessing multiple lender programs.

Banks typically don't charge separate origination fees but may offer less competitive rates because they lack the broker's ability to shop wholesale pricing across dozens of lenders. The fee differences between brokers and banks often favor brokers for sophisticated borrowers who benefit from program variety.

Broker advantages for Seattle buyers:

- Access to 20-50+ different lenders and programs

- Wholesale pricing unavailable to retail bank customers

- Specialized expertise with complex income (RSUs, bonuses, commissions)

- Faster closings through established lender relationships

- Personalized service throughout the loan process

Bank lending advantages:

- Streamlined processing for existing customers

- Potential relationship discounts on rates or fees

- Simplified documentation for straightforward transactions

- In-branch support and established brand recognition

Commission Structures for Different Loan Types

The mortgage broker price varies significantly based on loan program. Commission structures differ between conventional conforming loans, jumbo mortgages, FHA products, and VA financing.

Conventional and Conforming Loans

Standard conventional loans typically generate broker compensation between 0.75% and 1.5% of the loan amount. These loans follow Fannie Mae and Freddie Mac guidelines, providing consistent pricing across most brokers.

For a $600,000 conventional purchase in Shoreline, expect broker compensation around $6,000-$9,000, whether paid directly by the borrower or through lender credits.

Jumbo Loan Pricing

Jumbo home loans exceeding conforming limits often command higher broker fees due to increased documentation requirements, stricter underwriting standards, and specialized lender relationships. Compensation typically ranges from 1% to 2% on jumbo transactions.

Seattle's high property values mean many buyers need jumbo financing for homes in Bellevue, Kirkland, and waterfront neighborhoods. The additional mortgage broker price reflects the complexity of qualifying large loan amounts and coordinating sophisticated financial documentation.

Government-Backed Loan Programs

FHA and VA loans have regulated fee caps limiting what brokers can charge. FHA mortgage programs restrict origination fees to 1% of the loan amount, while VA loans prohibit certain fees entirely.

These restrictions mean the mortgage broker price for government loans is often lower in absolute dollars but may result in higher percentage costs on smaller loan amounts for first-time buyers in Lynnwood or Everett.

Value Beyond Price: What Seattle Buyers Receive

The mortgage broker price represents more than simple transaction costs. Experienced brokers provide strategic value that justifies their compensation through better loan structuring, faster closings, and superior problem-solving.

Services included in broker compensation:

- Pre-qualification analysis with multiple scenarios

- Credit optimization strategies before formal application

- Documentation guidance for complex income sources

- Rate shopping across dozens of lenders simultaneously

- Underwriting coordination to prevent delays

- Clear communication throughout 30-45 day closing periods

- Post-closing support for payment questions or refinancing

Tech professionals at Amazon, Microsoft, and Google benefit particularly from brokers experienced with RSU qualification strategies, which can increase buying power by $100,000 or more compared to traditional income calculations.

Timing and Market Impact on Broker Pricing

The mortgage broker price fluctuates with market conditions, seasonal demand, and interest rate environments. Seattle's busy spring and summer seasons often see less negotiable pricing, while winter months may offer opportunities for fee reductions.

Rising rate environments typically maintain stable broker compensation, but falling rates can compress margins as lenders compete aggressively. The 2026 market shows moderate rates after several years of volatility, creating balanced pricing conditions for Seattle homebuyers.

When to Lock Rates and Finalize Pricing

Broker compensation becomes final when you lock your interest rate, typically 30-60 days before closing. Understanding this timing helps buyers:

- Compare multiple broker quotes before commitment

- Negotiate fees during initial consultation rather than mid-process

- Request detailed breakdowns of all costs upfront

- Verify whether fees are credited if transactions cancel

Working with trusted Seattle mortgage professionals ensures transparent pricing discussions from initial consultation through closing day.

Questions Seattle Buyers Should Ask About Pricing

Before committing to any broker, Seattle homebuyers should clarify exactly what the mortgage broker price includes and how compensation is structured. Direct questions prevent surprises and ensure alignment between broker incentives and borrower goals.

Essential pricing questions:

- What is your total compensation on this loan, including all lender and borrower payments?

- Can you provide scenarios showing lender-paid versus borrower-paid options?

- Are there circumstances where your fees might increase after application?

- Which third-party fees do you control versus pass-through costs?

- How does your pricing compare to direct bank lending for my situation?

- What additional value do you provide beyond basic loan origination?

Brokers who welcome these questions and provide detailed written answers demonstrate the transparency that defines professional service in Seattle's competitive mortgage market.

Maximizing Value While Managing Costs

Smart Seattle buyers optimize the mortgage broker price by focusing on total loan cost rather than isolated fees. A broker charging 1.5% but securing a rate 0.375% lower than competitors saves significant money over typical 7-10 year ownership periods.

Calculate total costs using this framework:

| Cost Component | Year 1 | Years 2-5 | Years 6-10 | Total |

|---|---|---|---|---|

| Upfront fees | $X | $0 | $0 | $X |

| Rate difference impact | $Y/month | $Y × 48 | $Y × 60 | Calculate |

| Tax benefits | Deduction | Deduction | Deduction | Variable |

| Refinance potential | Consider | Likely | Possible | Future value |

This analysis often reveals that higher upfront mortgage broker prices deliver superior long-term value through better rates, particularly for buyers planning extended ownership in Redmond, Bellevue, or established Seattle neighborhoods.

Specialized Pricing for Complex Situations

Seattle's diverse buyer population includes unique scenarios requiring specialized broker expertise. Self-employed tech consultants, real estate investors, and divorced buyers often face complex documentation that impacts the mortgage broker price.

Brokers may charge premium fees for:

- Self-employment income: Additional documentation review and tax return analysis

- Investment properties: Non-owner occupied pricing and rental income calculations

- Divorce situations: Coordinating with attorneys and reviewing settlement agreements

- Foreign nationals: Visa status verification and alternative documentation

- Bank statement loans: Enhanced underwriting for non-traditional income verification

These situations benefit from experienced local guidance that justifies higher compensation through successful loan approvals that larger banks often decline.

Technology and Transparency in 2026

Modern mortgage technology has revolutionized how brokers present pricing to Seattle buyers. Digital platforms provide instant rate quotes, automated fee comparisons, and transparent disclosure of all compensation sources.

Progressive brokers now offer:

- Real-time rate shopping across multiple lenders

- Digital application processes reducing administrative costs

- Automated document collection lowering processing fees

- Video consultations eliminating travel time and expenses

- Online portals tracking loan progress transparently

These technological improvements often reduce the mortgage broker price while improving service quality, benefiting buyers throughout King and Snohomish Counties.

Long-Term Relationships Beyond Single Transactions

The mortgage broker price should be evaluated within the context of potential long-term value. Buyers who establish relationships with trusted brokers benefit from:

- Priority service during future refinances

- Proactive notifications when rate improvements create savings opportunities

- Strategic advice on property laddering and portfolio growth

- Referrals to qualified real estate agents, attorneys, and financial planners

- Educational resources supporting informed homeownership decisions

Seattle's dynamic real estate market creates ongoing opportunities for refinancing, home equity utilization, and investment property acquisition. A broker invested in your success provides value extending decades beyond initial purchase transactions.

Understanding mortgage broker price structures empowers Seattle homebuyers to make confident financing decisions aligned with their financial goals. Whether you're purchasing your first home, upgrading to accommodate a growing family, or building a real estate portfolio, transparent pricing combined with expert guidance creates the foundation for successful homeownership. Keith Akada brings 25+ years of experience and over 750 five-star reviews to every client relationship, specializing in complex income qualification for tech professionals while maintaining clear, competitive pricing throughout the Greater Seattle area. Connect with Mortgage Reel to discuss your specific situation and receive personalized pricing tailored to your homeownership objectives.