Understanding how rates loan products work in today's Seattle housing market requires navigating multiple factors that influence your borrowing costs. For homebuyers and homeowners in Seattle, Bellevue, Redmond, and Kirkland, the rates you secure on your mortgage can significantly impact your monthly payments and long-term financial strategy. As we move through 2026, the landscape of mortgage lending continues to evolve with changing economic conditions, Federal Reserve policies, and regional market dynamics that make securing the best possible rates loan terms more important than ever.

What Determines Your Rates Loan in Seattle's Market

The rates loan products available to Seattle homebuyers depend on a complex interplay of personal financial factors and broader economic conditions. Seven key factors determine your mortgage interest rate, according to the Consumer Financial Protection Bureau, and understanding these elements helps you position yourself for the most favorable terms.

Credit Score Impact on Borrowing Costs

Your credit score stands as the single most influential factor in determining your rates loan qualification. Lenders view borrowers with scores above 740 as lower risk, typically offering them the most competitive interest rates. For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, maintaining excellent credit is often achievable through disciplined financial management and timely debt payments.

Credit score tiers and their impact:

- Excellent (760+): Access to the lowest available rates

- Good (700-759): Competitive rates with minimal adjustments

- Fair (660-699): Moderate rate increases and additional scrutiny

- Below 660: Higher rates and potentially stricter qualification requirements

Even small improvements in your credit score can translate to meaningful savings. A 20-point increase might reduce your interest rate by 0.25% to 0.50%, saving tens of thousands over a 30-year mortgage term.

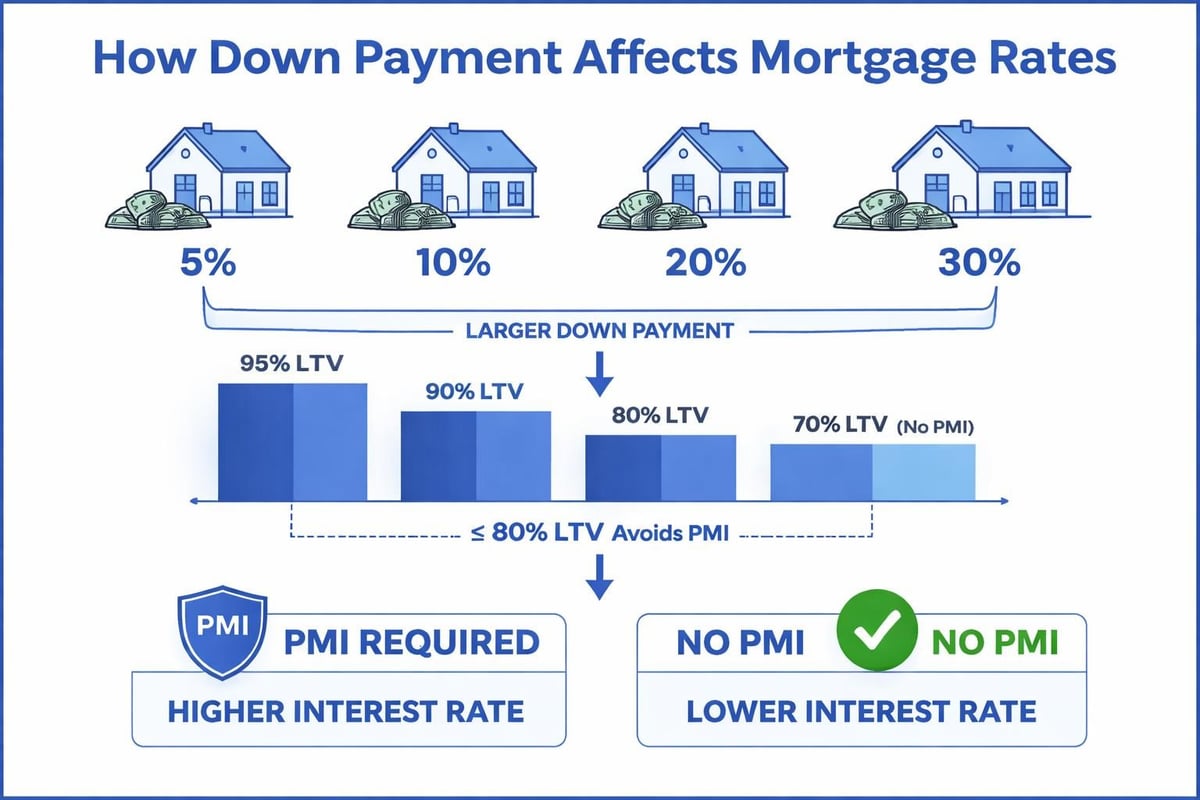

Loan-to-Value Ratio Considerations

The amount you borrow relative to your property's value creates another critical variable in rates loan pricing. Lenders offer their best rates to borrowers who make larger down payments, typically 20% or more, because these transactions carry less risk. However, various down payment options exist for Washington State homebuyers, each with different rate implications.

| Down Payment | LTV Ratio | Rate Impact | PMI Required |

|---|---|---|---|

| 20%+ | 80% or less | Best rates | No |

| 10-19% | 81-90% | Slightly higher | Yes |

| 5-9% | 91-95% | Moderate increase | Yes |

| 3-4.99% | 95-97% | Higher rates | Yes |

For homebuyers in Shoreline or Lynnwood considering lower down payment options, understanding this trade-off between upfront costs and ongoing interest expenses becomes essential for making informed decisions.

Property Type and Location Variables

Not all properties receive identical rates loan treatment from lenders. Single-family homes in Seattle typically qualify for the most favorable rates, while condominiums, multi-unit properties, and investment homes face rate adjustments based on perceived risk levels.

Single-Family vs. Condo Financing

Condominiums in Bellevue or Redmond high-rises often carry rate premiums of 0.125% to 0.375% compared to single-family homes. Lenders conduct additional due diligence on condominium associations, reviewing budgets, reserve funds, and owner-occupancy ratios before finalizing rates loan approvals.

Investment properties command even higher rates, typically 0.50% to 0.75% above owner-occupied residences. If you're purchasing rental property in Mill Creek or Everett, budget for these rate adjustments when calculating your expected returns and cash flow.

Economic Factors Beyond Your Control

While personal financial factors significantly influence your individual rates loan terms, broader economic conditions set the baseline from which all adjustments are made. The Federal Reserve's monetary policy decisions ripple through mortgage markets, affecting rates for all borrowers regardless of credit profile or down payment.

Federal Reserve Policy Impact

Economic conditions and Federal Reserve policies create the foundation upon which mortgage rates are built. When the Fed adjusts its benchmark interest rate, mortgage lenders typically respond within days or weeks, repricing their loan products accordingly.

In 2026, Seattle homebuyers have witnessed how quickly rates can shift in response to inflation data, employment reports, and economic growth indicators. These macro-level forces operate independently of individual borrower qualifications, creating market conditions that favor either buyers or refinance candidates depending on the trend direction.

Key economic indicators affecting rates:

- Consumer Price Index (CPI) and inflation measurements

- Employment and wage growth statistics

- GDP growth and recession indicators

- Treasury bond yields and investor sentiment

- Housing market supply and demand dynamics

For those working in Seattle's technology sector, understanding these connections helps you time major home purchase or refinance decisions more strategically.

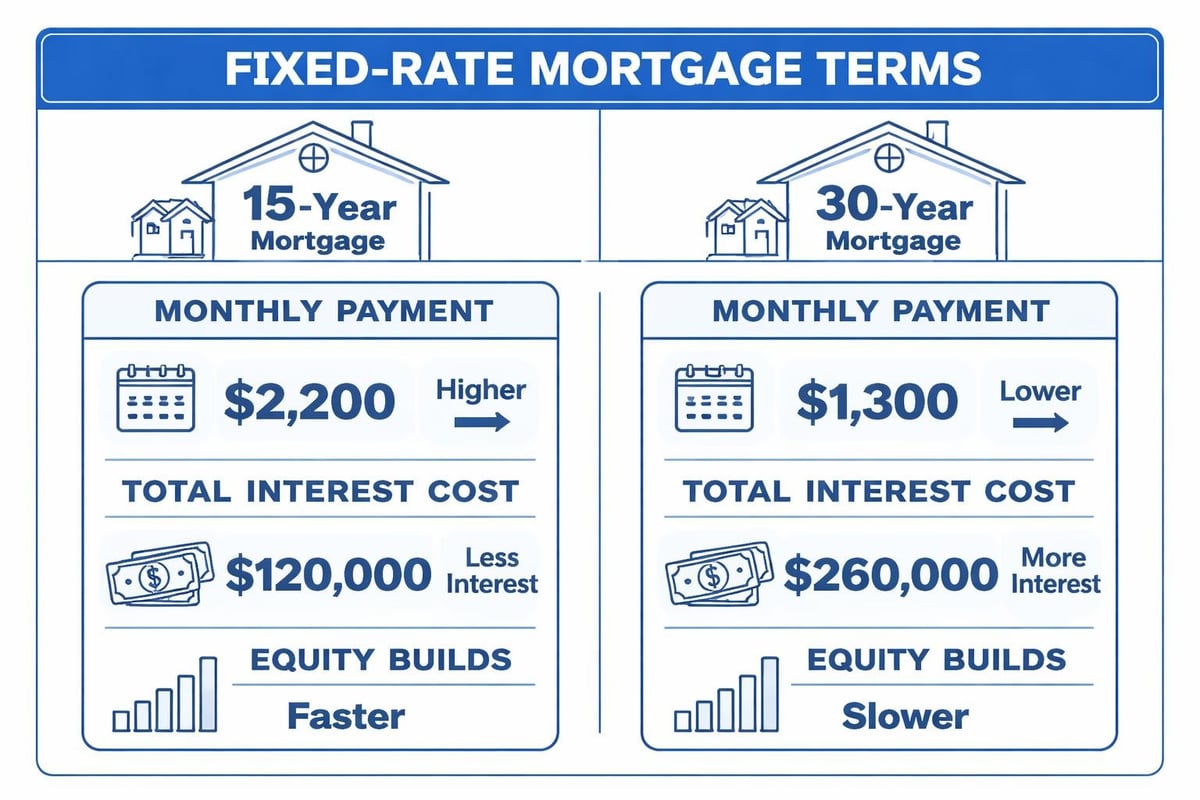

Loan Term and Product Selection

The specific mortgage product you choose creates substantial variation in your rates loan structure. Shorter-term loans typically offer lower interest rates but require higher monthly payments, while longer terms spread payments over more years at incrementally higher rates.

15-Year vs. 30-Year Comparison

| Loan Term | Typical Rate Advantage | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 15-year | 0.50-0.75% lower | Significantly higher | Substantially less |

| 30-year | Baseline rate | More affordable | Much higher overall |

Seattle homeowners with strong cash flow, such as those earning stock compensation from major employers, often benefit from 15-year mortgages that build equity faster and minimize lifetime interest costs. Conversely, first-time buyers in Lake Forest Park might prioritize the payment flexibility that 30-year terms provide.

Adjustable-Rate Mortgage Considerations

Adjustable-rate mortgages (ARMs) present another rates loan alternative worth examining, particularly for borrowers who plan to relocate or refinance within five to seven years. Initial ARM rates typically sit 0.50% to 1.00% below comparable fixed-rate mortgages, creating significant short-term savings.

Common ARM structures include 5/1, 7/1, and 10/1 configurations, where the first number represents years of fixed rates before annual adjustments begin. Tech professionals on assignment in Seattle for limited timeframes often find ARMs align perfectly with their housing timelines.

Documentation and Income Verification Standards

How lenders verify and evaluate your income directly affects your rates loan approval and pricing. Traditional W-2 employees typically navigate simpler documentation requirements than self-employed borrowers or those receiving complex compensation packages.

Stock Compensation Qualification

For Amazon, Microsoft, and Google employees, restricted stock units (RSUs) and equity compensation create unique underwriting scenarios. Specialized mortgage professionals understand how to structure income calculations that maximize borrowing power while securing competitive rates.

RSU qualification strategies include:

- Averaging vested RSU income over two years

- Including documented bonus history in qualifying income

- Structuring loan applications to emphasize stable base salary

- Timing applications after major vest dates for stronger documentation

Working with experienced mortgage brokers who understand Seattle mortgage financing for technology sector employees ensures you don't leave buying power on the table due to incomplete income documentation.

Points, Fees, and Rate Buydowns

The relationship between upfront costs and interest rates gives borrowers flexibility in structuring their rates loan products. Paying discount points at closing reduces your interest rate permanently, while lender credits increase your rate in exchange for covering some closing costs.

Strategic Point Purchases

Each discount point costs 1% of your loan amount and typically reduces your interest rate by 0.25%. For a $800,000 mortgage common in Seattle's housing market, one point costs $8,000 and might lower your rate from 6.50% to 6.25%.

Calculate your break-even point by dividing the point cost by monthly payment savings. If that $8,000 investment saves you $150 monthly, you'll recover the cost in 53 months. Borrowers planning to stay in their homes beyond this period benefit from point purchases, while those expecting to move or refinance sooner should avoid them.

Property Condition and Appraisal Factors

The physical condition of your prospective home influences rates loan availability and pricing more than many borrowers realize. Properties requiring significant repairs or renovations face stricter lending standards and potentially higher rates, particularly in competitive markets like Bellevue or Redmond.

Appraisal-Related Rate Adjustments

When appraisals come in below purchase price, your loan-to-value ratio increases unexpectedly, triggering rate adjustments or requiring additional down payment funds. Seattle's fast-moving market sometimes creates gaps between seller expectations and appraiser valuations, especially in rapidly appreciating neighborhoods.

JVM Lending highlights five key factors affecting borrower rates, including property type and condition. Homes requiring major work like roof replacement might benefit from contractors like Texcore Construction, who can provide detailed repair estimates and timelines that help lenders understand post-repair property values. Their expertise in commercial and residential roofing solutions ensures accurate documentation for underwriting purposes.

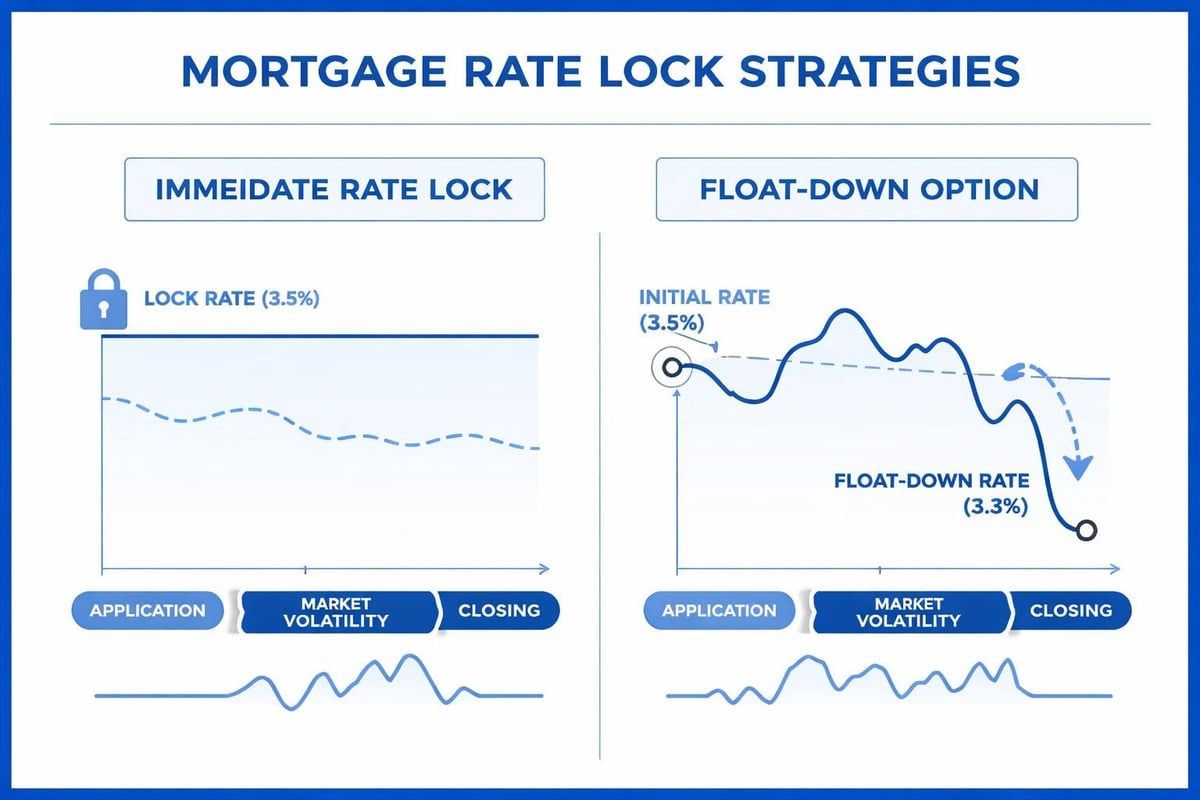

Timing Your Rate Lock Strategy

Interest rates fluctuate daily based on bond market activity and economic news releases. Understanding when to lock your rate versus letting it float requires balancing risk tolerance with market awareness.

Rate Lock Mechanics

Standard rate locks guarantee your interest rate for 30, 45, or 60 days while your loan processes. Longer lock periods typically cost more through higher rates or upfront fees. Some lenders offer float-down provisions allowing you to capture lower rates if markets improve during your lock period, though these features carry additional costs.

Rate lock decision factors:

- Current rate trend direction (rising or falling)

- Days until scheduled closing

- Economic data releases on the calendar

- Your risk tolerance for potential rate increases

- Strength of your purchase contract

Working with Seattle mortgage brokers who monitor daily rate movements helps you make informed lock timing decisions based on real-time market intelligence rather than guesswork.

Debt-to-Income Ratio Management

Lenders evaluate your existing debt obligations against verified income to determine rates loan qualification limits. Lower debt-to-income (DTI) ratios signal stronger repayment capacity, often resulting in better rate offerings and smoother approval processes.

Front-End and Back-End Ratios

Front-end DTI calculates your proposed housing payment as a percentage of gross monthly income, while back-end DTI includes all monthly debt obligations. Most conforming loans accept back-end ratios up to 43%, though some programs allow higher percentages with compensating factors like substantial reserves or excellent credit.

| DTI Ratio | Lending Impact | Rate Effect |

|---|---|---|

| Below 36% | Strongest position | Best rates available |

| 36-43% | Standard approval | Minimal rate impact |

| 43-50% | Requires strong credit | Possible rate adjustments |

| Above 50% | Limited options | Significantly higher rates |

For borrowers in Shoreline or Lynnwood carrying student loans, car payments, or credit card balances, strategically paying down debt before applying can improve both approval odds and rates loan terms.

Comparing Lender Rate Quotes Effectively

Not all rate quotes reflect true borrowing costs equally. Annual Percentage Rate (APR) provides more accurate comparison metrics than interest rate alone because it incorporates fees, points, and other loan costs into a single percentage.

Understanding APR vs. Interest Rate

Your interest rate determines your monthly principal and interest payment, while APR reflects the total cost of borrowing including origination fees, discount points, and certain closing costs spread over the loan term. Two lenders might quote identical interest rates but have substantially different APRs based on their fee structures.

When comparing offers from multiple lenders, request detailed Loan Estimates showing all costs itemized clearly. Pay particular attention to lender fees, appraisal costs, title charges, and prepaid items that vary between quotes.

Refinance Rate Considerations

Existing homeowners evaluating refinance opportunities face similar but distinct rate considerations compared to purchase borrowers. Your current equity position, remaining loan term, and cash-out requirements all influence the rates loan products available through refinancing.

Break-Even Analysis for Refinancing

Calculate whether refinancing makes financial sense by comparing closing costs against monthly savings. Current loan pricing trends for 2025 show that economic outlook significantly affects refinance activity volumes and available rate structures.

Refinance evaluation steps:

- Determine your current rate and remaining balance

- Obtain new rate quotes and estimated closing costs

- Calculate monthly payment difference

- Divide closing costs by monthly savings for break-even months

- Evaluate whether you'll remain in the home beyond break-even point

For Seattle homeowners who purchased when rates were higher, refinancing might offer substantial savings even with closing costs factored in. Those with existing low rates from previous years should carefully evaluate whether marginal improvements justify refinance expenses.

International Buyer Considerations

Foreign nationals and non-permanent residents face additional scrutiny and typically higher rates when seeking mortgage financing in Seattle's market. These borrowers often encounter minimum down payment requirements of 20-30% and rate premiums of 0.50-1.00% above standard pricing.

Documentation Requirements for International Buyers

International buyers purchasing property in Kirkland or Bellevue must provide additional documentation including passport copies, visa status verification, foreign credit reports, and proof of income from overseas sources. Some lenders specialize in these complex scenarios, offering competitive programs despite the additional underwriting complexity.

For those seeking mortgage guidance internationally, resources like Roling Advies provide comprehensive mortgage advisory services that help borrowers understand financing structures across different markets, though Seattle buyers ultimately need local lending expertise for U.S. property transactions.

Market Conditions and Rate Volatility

Seattle's housing market dynamics create local variations in rates loan availability and pricing strategies. The 2025 housing market experienced notable challenges, with elevated mortgage rates affecting home sales velocity and price appreciation patterns that continue influencing 2026 market conditions.

Supply and Demand Influences

When housing inventory remains tight in desirable Seattle neighborhoods, buyer competition intensifies regardless of prevailing rates. Conversely, increasing supply or economic uncertainty can shift leverage toward buyers, potentially creating more favorable rate negotiation opportunities.

Understanding these local market conditions helps time both purchase and refinance decisions more strategically, particularly in submarkets like Mill Creek or Everett where inventory levels fluctuate seasonally.

Jumbo Loan Rate Structures

Properties exceeding conforming loan limits require jumbo financing with distinct rate characteristics. In King County, loans above $802,650 in 2026 fall into jumbo territory, though these thresholds adjust annually based on housing price indices.

Jumbo vs. Conforming Rate Spreads

Historically, jumbo rates sat 0.25-0.50% above conforming rates due to higher lending risk and lack of government backing. However, competitive pressure among portfolio lenders has occasionally compressed or even eliminated this spread for well-qualified borrowers with strong credit and substantial down payments.

Jumbo loan qualification typically requires:

- Credit scores of 700 or higher (720+ for best rates)

- Down payments of at least 10-20%

- Cash reserves covering 6-12 months of payments

- Debt-to-income ratios below 43%

- Comprehensive income documentation

Seattle's robust jumbo lending market, driven by high housing costs and affluent tech sector employees, creates competitive rate environments for qualified borrowers pursuing properties in premium neighborhoods.

Professional Guidance Value

Navigating the complexities of rates loan products, underwriting guidelines, and timing strategies presents challenges even for financially sophisticated borrowers. Experienced mortgage professionals provide value through current market knowledge, lender relationship leverage, and strategic guidance tailored to individual circumstances.

Broker vs. Direct Lender Considerations

Mortgage brokers access multiple lender platforms, comparing rates and programs to find optimal matches for borrower profiles. Direct lenders offer their own products exclusively, sometimes providing faster approvals but potentially limiting options. Factors determining interest rates vary between lenders based on their underwriting models and portfolio strategies.

Working with professionals who maintain relationships across numerous lending sources ensures you see comprehensive market options rather than single-channel perspectives. This becomes particularly valuable for complex scenarios involving stock compensation, self-employment income, or unique property types.

Securing optimal rates loan terms in Seattle's 2026 housing market requires understanding personal financial factors, broader economic conditions, and strategic timing considerations that collectively determine your borrowing costs. Whether you're purchasing your first home in Lake Forest Park, upgrading to a larger property in Bellevue, or refinancing your existing Redmond residence, informed decision-making starts with clear education and expert guidance. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area homebuyers and homeowners navigate complex mortgage scenarios with transparency and strategic insight, specializing in stock compensation qualification for tech professionals and delivering closings in as few as 9 business days.