Securing a mortgage for home purchase represents one of the most significant financial decisions you'll make in your lifetime. For homebuyers in Seattle, Bellevue, Redmond, and surrounding areas, understanding the mortgage process is essential to navigating one of the nation's most competitive housing markets. Whether you're a first-time buyer exploring options in Shoreline or a tech professional relocating to Kirkland, the right mortgage strategy can transform your homeownership journey from overwhelming to achievable.

Understanding the Mortgage for Home Purchase Process

The journey to homeownership begins long before you submit an offer on a property. A mortgage is a loan specifically designed for purchasing real estate, where the property itself serves as collateral. This structured financing allows buyers to spread the cost of a home over time rather than paying the full purchase price upfront.

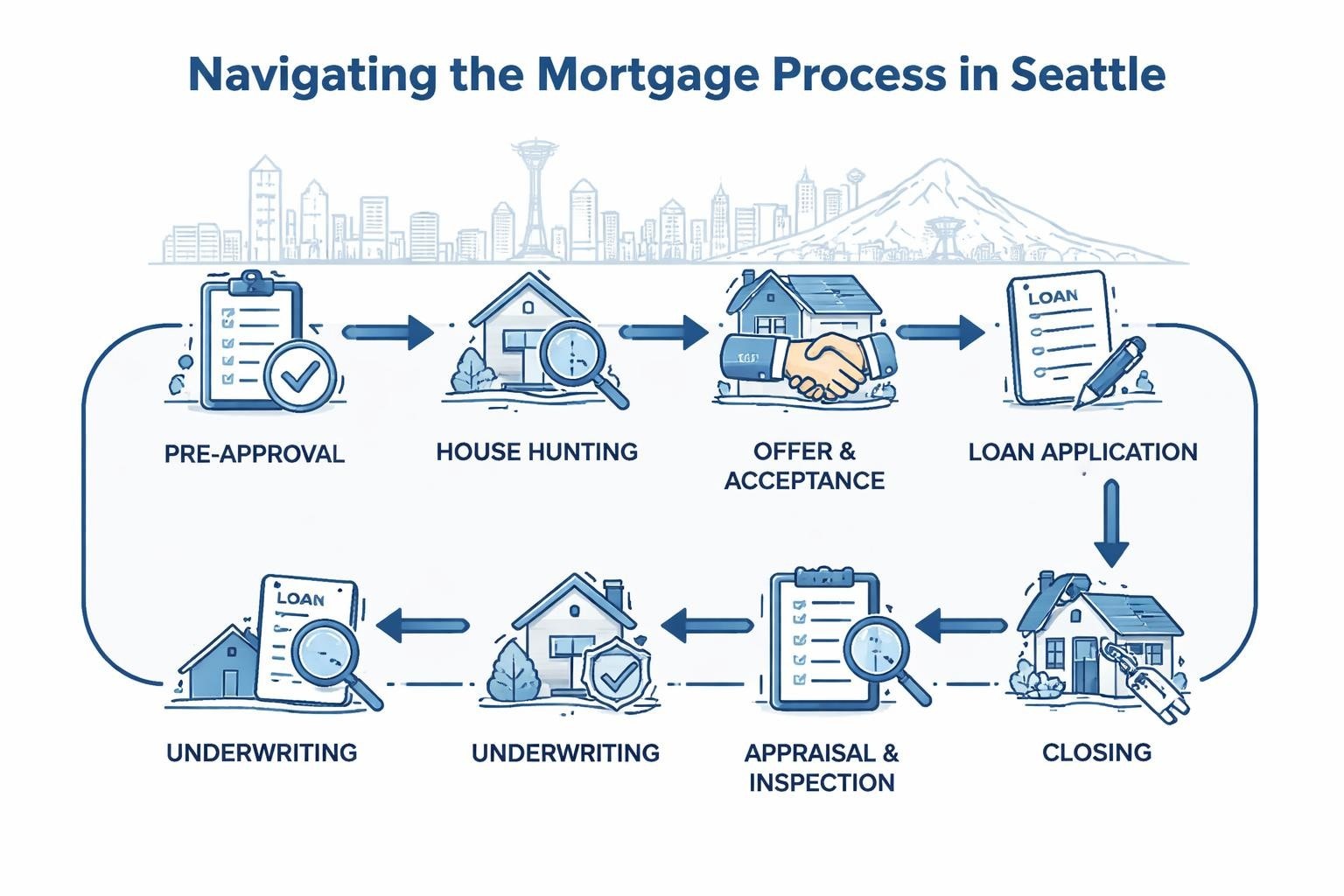

Pre-Approval: Your First Critical Step

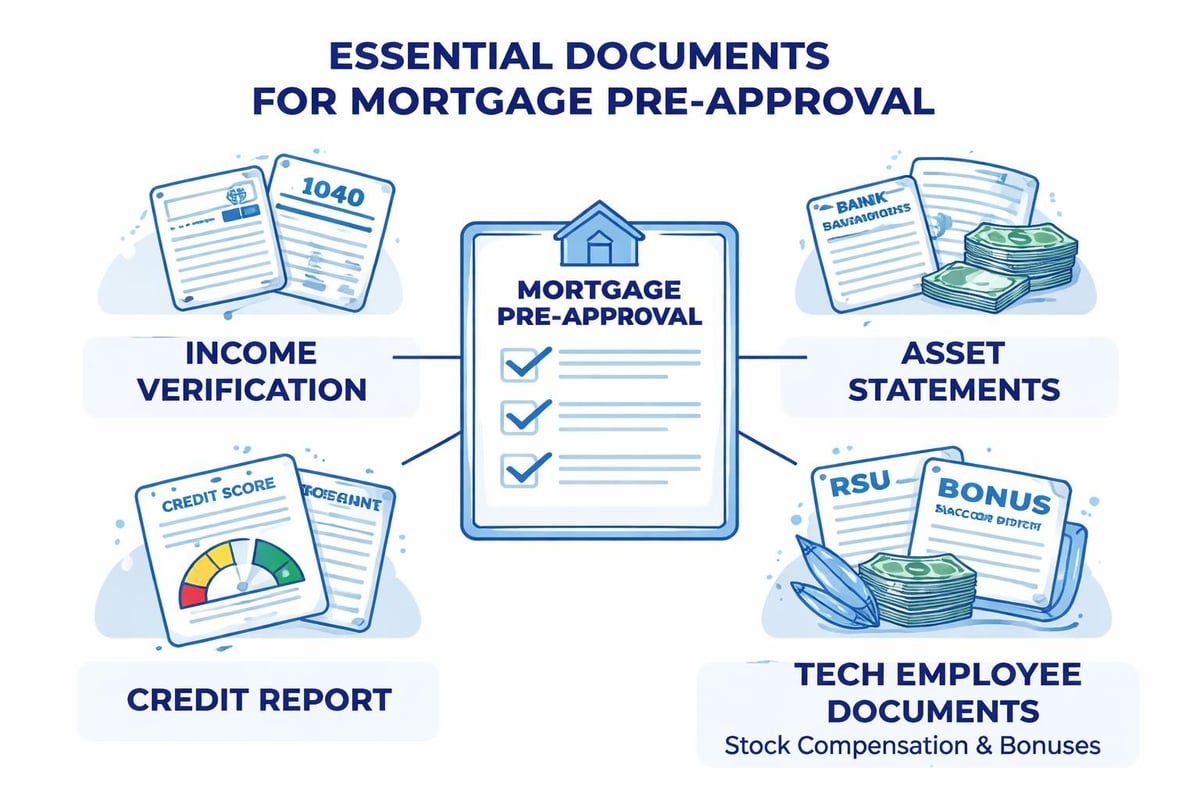

Before touring homes in Lake Forest Park or Mill Creek, obtaining mortgage pre-approval establishes your buying power and demonstrates serious intent to sellers. Pre-approval involves a comprehensive review of your financial profile, including:

- Credit history and scores across all three major bureaus

- Income documentation including W-2s, pay stubs, and tax returns

- Asset verification for down payment and reserves

- Debt-to-income ratio calculation to determine affordability

- Employment verification to confirm income stability

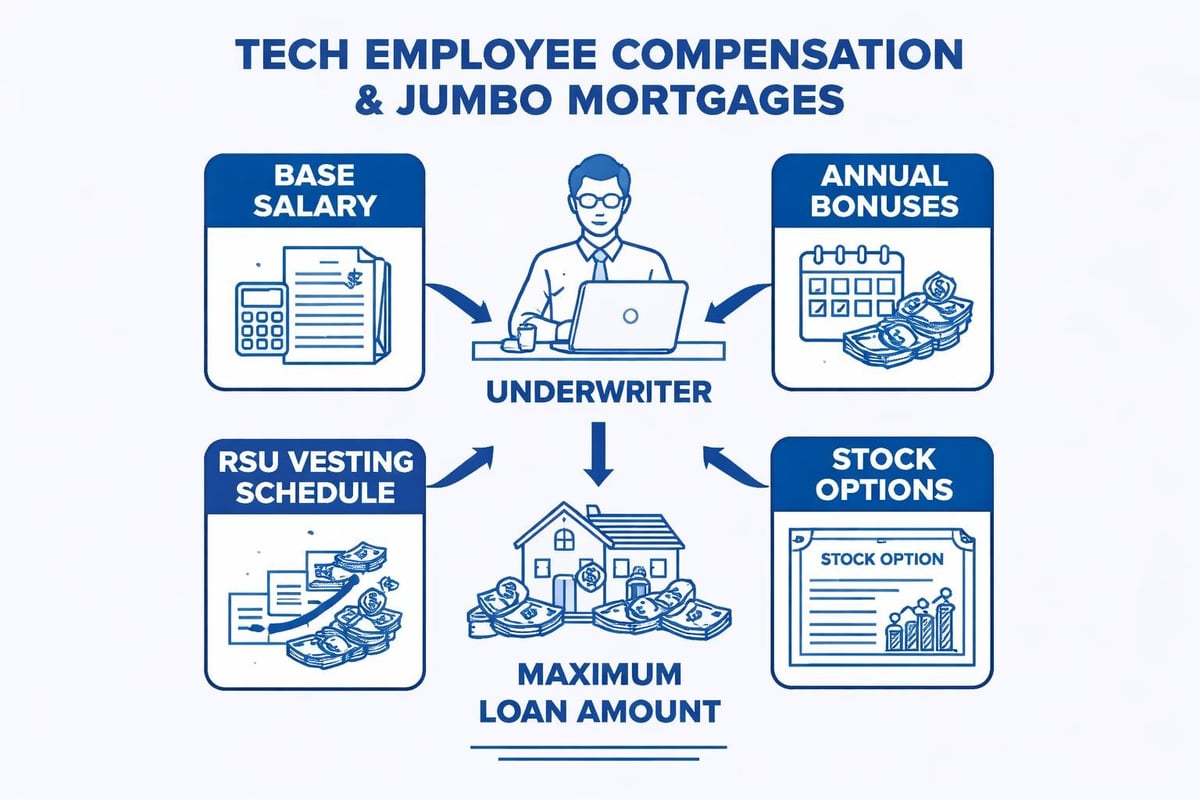

For Seattle-area tech professionals working at Amazon, Microsoft, or Google, pre-approval requires additional attention to stock-based compensation. RSUs, ESPP shares, and annual bonuses can significantly increase buying power when properly documented and underwritten. This specialized knowledge separates experienced mortgage brokers from generic lenders who may undervalue or exclude equity compensation entirely.

Choosing Your Mortgage for Home Financing

The mortgage landscape offers numerous loan products, each designed for different financial situations and homeownership goals. Understanding these options empowers you to select financing aligned with your long-term strategy.

Common Mortgage Types for Seattle Homebuyers

| Loan Type | Down Payment | Credit Score | Best For |

|---|---|---|---|

| Conventional | 3-20% | 620+ | Strong credit, flexible terms |

| FHA | 3.5% | 580+ | Lower credit, smaller down payment |

| VA | 0% | No minimum | Veterans and active military |

| Jumbo | 10-20% | 700+ | High-value Seattle properties |

Conventional loans remain the most popular choice for Seattle homebuyers with solid credit and stable income. These loans, conforming to guidelines set by Fannie Mae and Freddie Mac, offer competitive rates and flexible loan terms ranging from 15 to 30 years. With as little as 3% down, first-time buyers can enter the market while those putting down 20% or more avoid private mortgage insurance entirely.

FHA loans provide accessible financing for buyers with limited savings or credit challenges. These government-backed mortgages require just 3.5% down and accept credit scores as low as 580. However, FHA loans include both upfront and ongoing mortgage insurance premiums that increase overall costs compared to conventional financing.

VA loans offer exceptional benefits for military service members, veterans, and eligible spouses. With zero down payment required, no private mortgage insurance, and competitive interest rates, VA financing provides unmatched value. The VA veterans loan program acknowledges military service through favorable terms unavailable in conventional lending.

Jumbo loans address Seattle's high housing costs, financing properties exceeding conventional loan limits of $806,500 in 2026. These specialized mortgages require larger down payments, stronger credit profiles, and more substantial reserves, but they enable purchases in premium neighborhoods throughout Bellevue, Redmond, and Seattle's sought-after communities.

Down Payment Strategies and Options

The down payment requirement significantly impacts which mortgage for home purchase you can access. While the traditional 20% down payment eliminates mortgage insurance and secures favorable rates, numerous lower down payment options exist for qualified buyers.

Seattle homebuyers frequently utilize these down payment approaches:

- 3% down conventional loans through programs like HomeReady and Conventional 97

- 5% down conventional financing for broader property eligibility

- 10% down options balancing lower payments with reduced insurance costs

- 20% down to eliminate PMI and maximize equity from purchase

For those exploring 5 percent down conventional loans or 20 percent down home loans, understanding the trade-offs between lower upfront costs and long-term expenses guides smarter decisions.

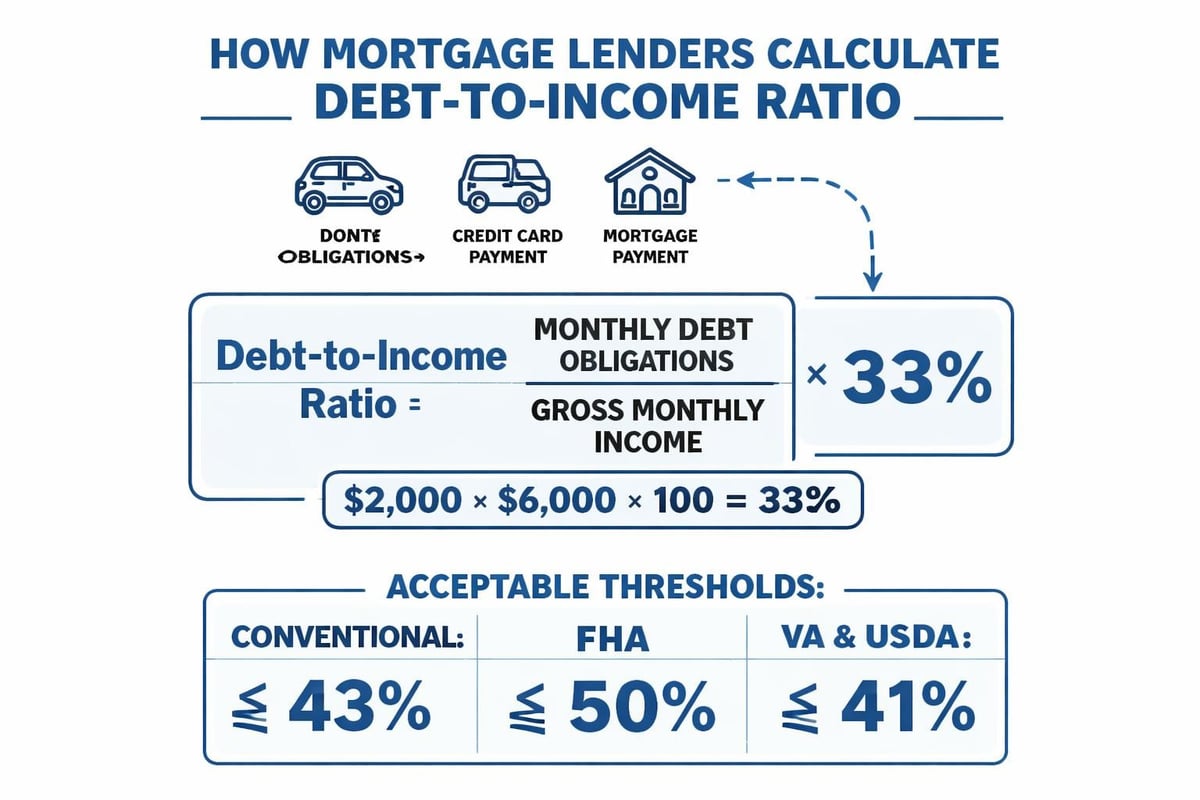

Qualifying for Your Mortgage for Home Purchase

Mortgage underwriting evaluates your ability to repay the loan through systematic analysis of credit, income, assets, and employment. For Seattle-area buyers, especially those in technology sectors, qualification involves nuances that generic online calculators cannot capture.

Income Documentation for Tech Professionals

Standard W-2 employment provides straightforward income verification. However, tech professionals earning substantial compensation through equity face additional complexity. Underwriters assess RSU vesting schedules, historical grant patterns, and stock price stability to determine reliable income.

Base salary receives full consideration with two years of consistent employment. Annual bonuses typically require two-year averaging unless employment contracts guarantee these amounts. RSUs and stock options may qualify at 70-100% of their value depending on vesting schedules and documentation quality.

Credit Requirements Across Loan Programs

Your credit score directly influences both mortgage approval and interest rate pricing. Seattle's competitive market rewards strong credit profiles with better terms and increased negotiating power.

- 740+ scores access the best available rates across all loan types

- 700-739 scores receive favorable pricing with minimal adjustments

- 660-699 scores face modest rate increases but maintain strong options

- 620-659 scores qualify for conventional loans with higher costs

- Below 620 typically requires FHA financing or credit improvement

Beyond scores, underwriters examine credit reports for late payments, collections, bankruptcies, and debt levels. Clean credit histories demonstrate financial responsibility and risk management.

Asset Verification and Reserve Requirements

Lenders verify you possess sufficient funds for down payment, closing costs, and financial reserves. Bank statements, investment accounts, and retirement funds document available assets. Most programs require reserves covering two to six months of mortgage payments depending on loan type, down payment size, and property characteristics.

For buyers receiving gift funds from family members, proper documentation ensures these contributions meet underwriting guidelines. Gift letters, proof of transfer, and donor asset verification create a clean paper trail for compliance.

Navigating Seattle's Competitive Housing Market

Seattle's real estate landscape demands strategic mortgage planning. With median home prices exceeding $850,000 in many neighborhoods and inventory remaining tight, buyers need every competitive advantage available.

Fast Closing Timelines Matter

In multiple-offer situations, closing speed can differentiate winning offers from rejected bids. Traditional mortgage timelines span 30-45 days, but experienced lenders with streamlined processes close loans in as few as 9 business days. This efficiency appeals to sellers prioritizing certainty and quick closings.

Understanding Loan Estimates and Closing Costs

The Loan Estimate provides a standardized disclosure of mortgage terms, projected payments, and closing costs within three business days of application. This three-page document enables comparison shopping across lenders and reveals total borrowing costs.

Closing costs typically include:

- Origination charges and lender fees

- Appraisal, credit report, and title services

- Prepaid interest, property taxes, and insurance

- Escrow deposits for ongoing tax and insurance payments

- Recording fees and transfer taxes

For Seattle homebuyers, closing costs generally range from 2-5% of the purchase price depending on loan type, property location, and negotiated terms.

Building Home Equity Through Your Mortgage

Homeownership creates wealth through equity accumulation as you reduce mortgage principal and property values appreciate. Each monthly payment increases your ownership stake while market appreciation in strong regions like greater Seattle compounds these gains.

Principal Reduction and Amortization

Early mortgage payments allocate heavily toward interest with modest principal reduction. As the loan matures, this balance shifts dramatically. A 30-year mortgage reaches the halfway point of principal paydown around year 22, demonstrating the front-loaded interest structure.

Shorter loan terms accelerate equity building through higher monthly payments applied more aggressively to principal. 15-year versus 30-year mortgages represent the classic trade-off between monthly affordability and long-term wealth accumulation.

Market Appreciation in Seattle

Seattle's housing market historically demonstrates strong appreciation despite periodic corrections. Homeowners in established neighborhoods like Shoreline, Lynnwood, and Everett benefit from regional economic strength, limited land availability, and consistent population growth driven by employment opportunities.

Mortgage Options for Different Buyer Profiles

Your financial situation, homeownership goals, and market timing influence which mortgage for home financing delivers optimal results. Consider these common buyer scenarios throughout the Seattle area.

First-Time Homebuyers in Seattle

First-time buyers often prioritize low down payments and accessible qualification standards. FHA loans and low down payment home loans in Washington State provide entry points into homeownership. Educational resources and patient guidance help navigate unfamiliar processes with confidence.

Move-Up Buyers and Relocation

Established homeowners upgrading to larger properties or relocating within the Puget Sound region bring equity from previous home sales. These buyers typically pursue conventional financing with substantial down payments, avoiding mortgage insurance and securing favorable rates.

For those moving from out of state, coordinating with professional long-distance movers like US Prime Movers streamlines the transition into your new Seattle-area home while managing the logistics of interstate relocation.

Tech Professionals and High Earners

Amazon, Microsoft, and Google employees with significant equity compensation require specialized mortgage expertise. Jumbo loan qualification using RSUs and stock options maximizes buying power in premium neighborhoods throughout Bellevue, Redmond, and Seattle. Understanding how underwriters evaluate equity compensation prevents leaving hundreds of thousands in buying power on the table.

Real Estate Investors

Investment property financing follows different guidelines than owner-occupied mortgages. Higher down payments, stricter credit requirements, and rental income analysis characterize investor loans. Experienced investors often maintain relationships with lenders familiar with portfolio expansion strategies and creative financing structures.

Refinancing Your Existing Mortgage

Homeowners with existing mortgages periodically evaluate refinancing opportunities to reduce rates, access equity, or modify loan terms. Rate-and-term refinancing replaces your current mortgage with new terms, while cash-out refinancing extracts equity for other purposes.

When Refinancing Makes Sense

Refinancing delivers value when interest rate reductions exceed costs within a reasonable timeframe. Additional motivations include:

- Eliminating mortgage insurance after reaching 20% equity

- Converting adjustable-rate mortgages to fixed rates

- Shortening loan terms to build equity faster

- Consolidating high-interest debt through cash-out refinancing

Before refinancing, verify your loan doesn't include prepayment penalties that negate potential savings. While rare in modern mortgages, these fees occasionally appear in specialized loan products.

Assumable Mortgages in Special Circumstances

In rising rate environments, mortgage assumption allows buyers to take over existing loans with favorable terms. FHA, VA, and USDA loans include assumability features, though conventional mortgages typically prohibit this practice. When available, assumption provides significant value if the existing rate substantially undercuts current market rates.

Working with a Seattle Mortgage Broker

The complexity of mortgage for home financing, especially in competitive markets like Seattle, rewards working with experienced professionals who prioritize education and transparency. Mortgage brokers access multiple lenders and programs, comparing options to identify optimal solutions for your specific situation.

Advantages of Local Expertise

Seattle-area mortgage brokers understand regional market dynamics, property values, and buyer challenges. This local knowledge proves invaluable when structuring offers, negotiating terms, and navigating competitive bidding situations in neighborhoods from Mill Creek to downtown Seattle.

Professional brokers guide buyers through documentation requirements, explain underwriting decisions, and maintain communication throughout the process. For complex income scenarios involving stock compensation or self-employment, specialized expertise prevents delays and maximizes approval chances.

Common Mortgage Mistakes to Avoid

Even informed buyers occasionally stumble through preventable errors that delay closings or increase costs. Awareness of these pitfalls protects your transaction and financial interests.

Changing employment during the mortgage process triggers re-verification and potential denial. Lenders require employment stability, so job changes should wait until after closing. Large purchases or new credit inquiries before closing alter debt-to-income ratios and credit profiles, potentially affecting approval.

Insufficient documentation preparation causes delays when underwriters request clarification on deposits, credit inquiries, or income sources. Proactive document gathering and transparent communication prevent last-minute scrambles.

Overlooking total costs of homeownership beyond the mortgage payment leads to budget strain. Property taxes, insurance, maintenance, HOA fees, and utilities substantially increase monthly housing expenses compared to the principal and interest payment alone.

Seattle Neighborhood Considerations

Location significantly impacts both property values and mortgage qualification. Seattle's diverse neighborhoods each present unique opportunities and considerations for homebuyers.

Shoreline and Lake Forest Park offer suburban accessibility with excellent schools and parks, attracting families seeking space and community. Lynnwood and Mill Creek provide newer construction and value compared to Seattle proper while maintaining reasonable commute times to major employment centers.

Everett continues growing as an affordable alternative for buyers priced out of closer-in neighborhoods, with improving infrastructure and employment opportunities at Boeing and related industries.

Understanding neighborhood-specific factors like property tax rates, HOA requirements, and future development plans informs smarter purchase decisions aligned with long-term goals.

Mortgage Rate Considerations in 2026

Interest rates directly impact affordability and total mortgage costs over time. While precise rate prediction remains impossible, understanding factors influencing rates helps buyers make informed timing decisions.

Federal Reserve policy, inflation trends, economic growth, and housing market conditions all affect mortgage rates. In 2026, buyers benefit from comparing current Seattle mortgage rates across multiple lenders to identify competitive pricing.

Even small rate differences compound significantly over 30-year terms. A 0.25% rate reduction on a $750,000 mortgage saves approximately $50,000 in interest over the loan's life, demonstrating the value of thorough rate shopping.

Rate Locks and Timing Strategy

Once you've identified a favorable rate, locking protects against increases during your transaction. Rate locks typically last 30-60 days, aligning with standard closing timelines. Extended locks cost more but provide security in volatile rate environments.

For buyers with flexibility, monitoring rate trends and timing purchases during favorable periods optimizes borrowing costs. However, attempting to perfectly time the market often backfires, as waiting for theoretically better rates may mean watching prices appreciate beyond any rate savings.

Securing the right mortgage for home purchase requires understanding loan options, qualification requirements, and market dynamics specific to Seattle and surrounding communities. Whether you're exploring neighborhoods in Bellevue or evaluating jumbo loan options for premium properties, informed decisions stem from working with experienced professionals who prioritize your long-term success. Keith Akada and the team at Mortgage Reel bring over 25 years of expertise helping Seattle-area homebuyers navigate complex mortgage decisions with transparency and strategy, from first-time purchases to sophisticated jumbo financing for tech professionals. With 750+ five-star reviews and specialized knowledge of equity compensation qualification, we're ready to help you achieve your homeownership goals efficiently and confidently.