Veterans and active-duty service members seeking to purchase or refinance homes in the Greater Seattle area have access to one of the most powerful financing tools available: VA loans. These government-backed mortgages offer exceptional benefits, but choosing among va loan mortgage companies requires understanding what differentiates one lender from another. With Seattle's competitive housing market and rising home prices across Bellevue, Redmond, and Kirkland, working with the right VA lender can mean the difference between a smooth transaction and unnecessary complications. This guide breaks down what veterans should know about va loan mortgage companies, how to evaluate lenders, and what to expect when navigating the VA loan process in the Pacific Northwest.

Understanding VA Loan Mortgage Companies and Their Role

VA loan mortgage companies serve as the bridge between veterans and homeownership by originating, processing, and funding loans guaranteed by the U.S. Department of Veterans Affairs. Unlike conventional mortgages, VA loans require lenders to meet specific standards and follow VA guidelines throughout the lending process.

What Makes VA Lenders Different

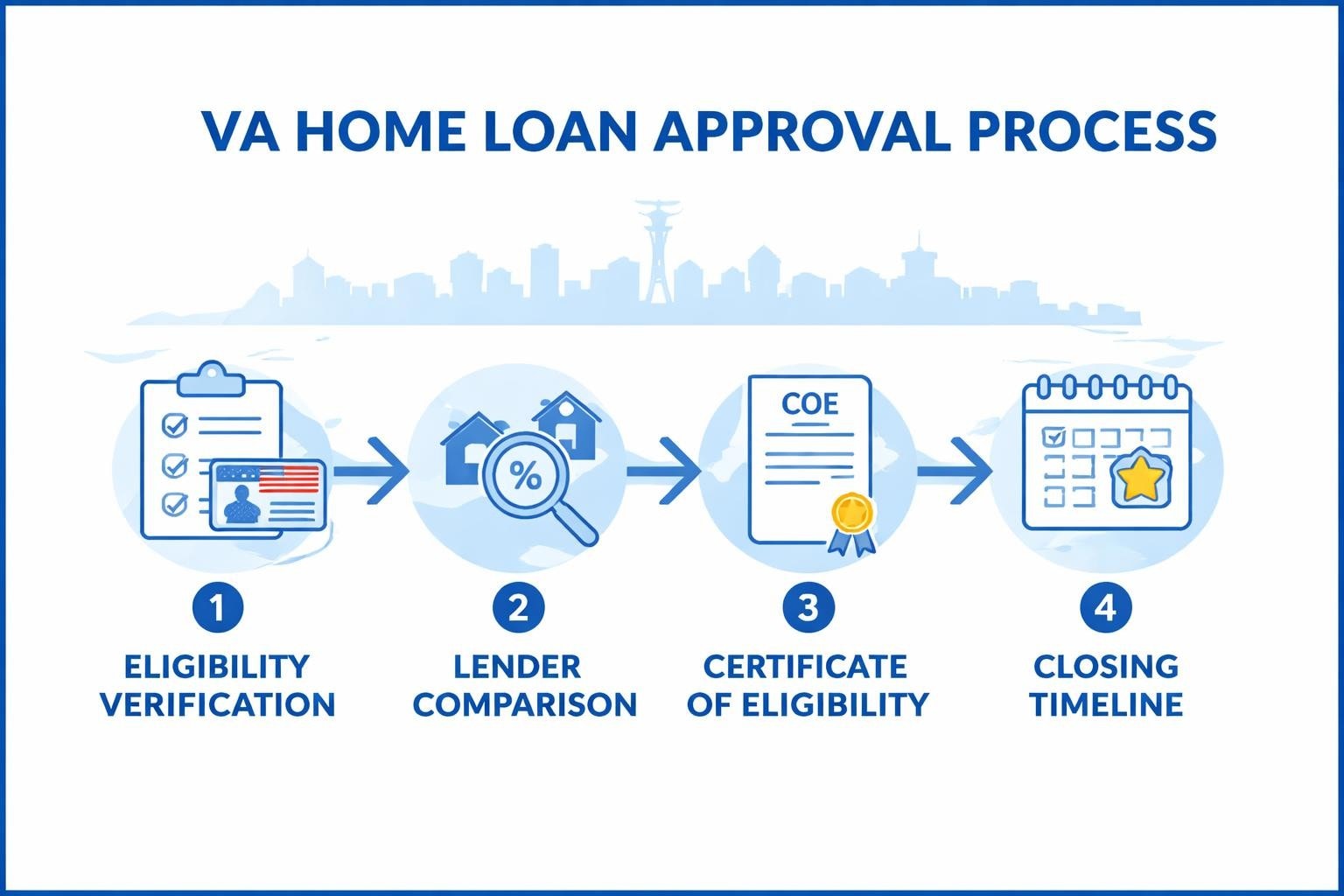

Not all mortgage lenders offer VA loans, and among those that do, expertise levels vary significantly. VA loan mortgage companies must be approved by the VA and maintain compliance with strict underwriting standards. This approval process ensures lenders understand unique aspects of VA lending, including:

- Certificate of Eligibility (COE) verification procedures

- VA appraisal requirements and property standards

- Funding fee calculations and exemptions

- Occupancy and entitlement guidelines

- Residual income calculations specific to regional cost of living

The best va loan mortgage companies go beyond basic compliance by investing in training, maintaining dedicated VA loan specialists, and streamlining processes to benefit military borrowers.

Types of Lenders Offering VA Loans

Veterans shopping for VA financing encounter several categories of lenders. National banks and credit unions often advertise VA products but may lack specialized expertise. Regional lenders sometimes offer more personalized service but potentially limited capacity during high-volume periods. Mortgage brokers, like Mortgage Reel serving Seattle and surrounding communities, provide access to multiple wholesale lenders while offering guidance tailored to local market conditions.

According to HousingWire’s 2026 rankings of top VA loan originators, the largest VA lenders by volume don't always deliver the best borrower experience. Veterans in Shoreline, Lynnwood, and Mill Creek benefit from working with local professionals who understand Pacific Northwest property values, inspection practices, and competitive offer strategies.

Key Benefits Veterans Receive Through VA Financing

VA loans remain one of the strongest mortgage programs available, offering advantages that directly impact affordability and accessibility for military families relocating to or stationed near Joint Base Lewis-McChord and other installations.

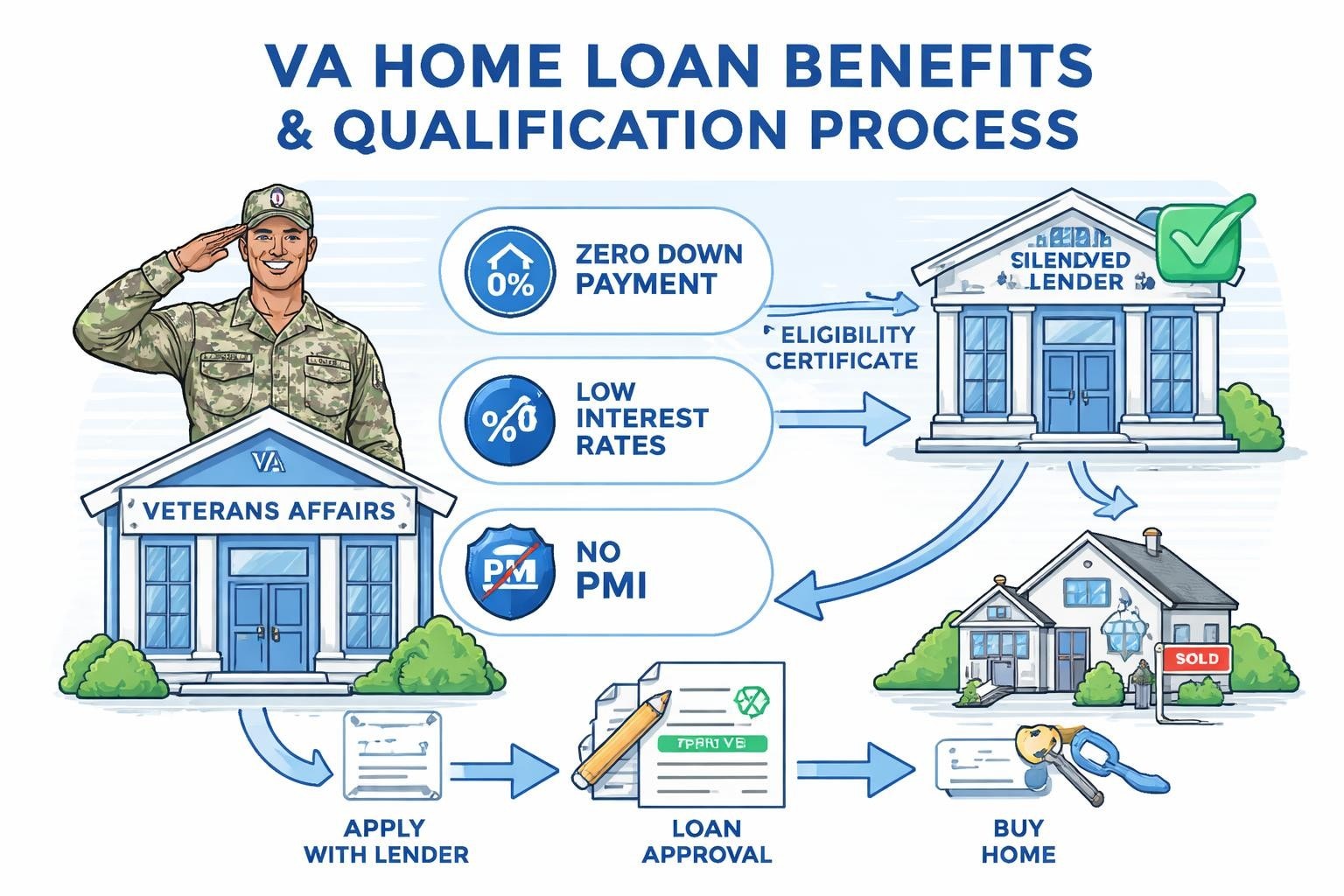

Zero Down Payment Requirements

The most significant benefit of working with va loan mortgage companies is the ability to finance 100% of a home's purchase price without private mortgage insurance. For a median-priced Seattle home at approximately $825,000 in 2026, this eliminates the need for a $165,000 down payment that conventional financing would require.

This feature proves particularly valuable for:

- First-time homebuyers who haven't accumulated substantial savings

- Veterans transitioning from military service to civilian careers

- Military families frequently relocating who need to preserve cash reserves

- Service members whose compensation includes non-traditional income sources

Competitive Interest Rates and No PMI

VA loan mortgage companies typically offer interest rates 0.25% to 0.50% lower than conventional loans. Combined with the absence of monthly mortgage insurance premiums, veterans achieve significantly lower monthly payments. A $500,000 VA loan at 6.25% costs approximately $3,078 monthly (principal and interest), while a conventional loan at 6.50% with PMI exceeds $3,450-a difference of $372 monthly or $4,464 annually.

| Loan Feature | VA Loan | Conventional Loan (5% Down) |

|---|---|---|

| Down Payment | $0 | $25,000 (on $500,000) |

| Interest Rate | 6.25% | 6.50% |

| Monthly PMI | $0 | $208 |

| Monthly Payment | $3,078 | $3,210 |

| Cash to Close | ~$8,500 (costs only) | ~$35,000 |

Seller Concessions and Closing Cost Assistance

VA guidelines permit sellers to contribute up to 4% of the purchase price toward buyer closing costs, significantly more generous than conventional loan limits. In competitive Seattle markets, skilled negotiation can secure thousands in seller-paid costs, reducing the veteran's out-of-pocket expenses at closing.

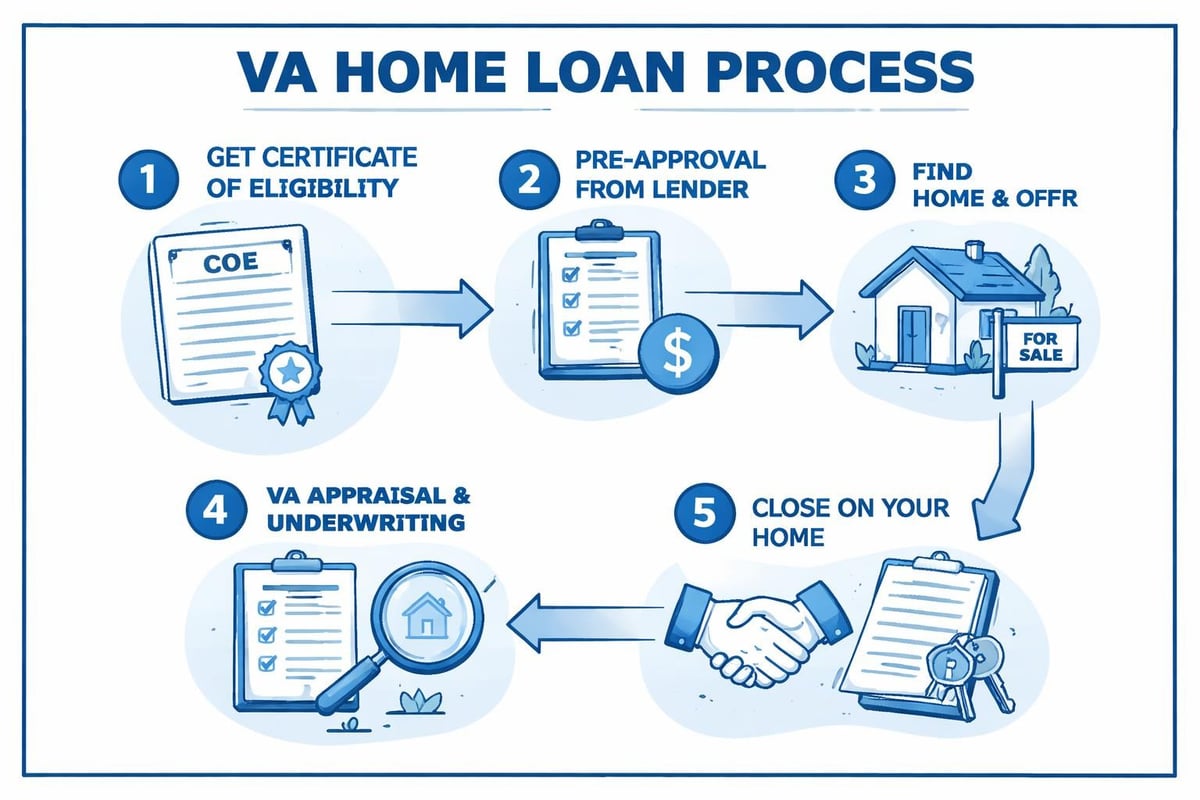

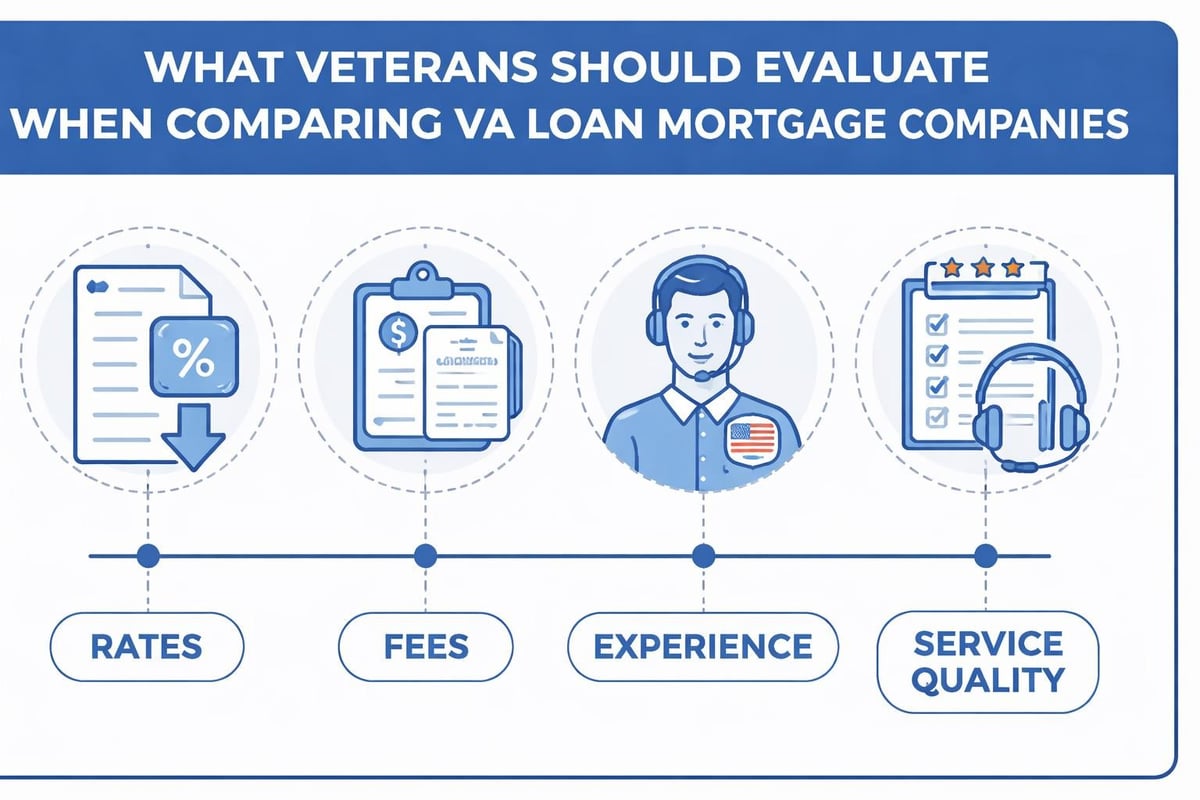

How to Evaluate and Choose VA Loan Mortgage Companies

Selecting the right lender requires research beyond comparing interest rates. Veterans should assess multiple factors that impact both the transaction experience and long-term loan performance.

Experience and VA Loan Volume

Questions to ask potential lenders include:

- How many VA loans do you originate annually?

- What percentage of your business consists of VA lending?

- Do you have dedicated VA loan specialists on staff?

- Can you provide references from recent VA borrowers?

Companies processing hundreds of VA loans yearly develop institutional knowledge that smooths the approval process. Bankrate’s guide to the best VA mortgage lenders emphasizes that specialized experience directly correlates with faster approvals and fewer complications.

Technology and Communication Systems

Modern va loan mortgage companies leverage technology to enhance borrower experience. Look for lenders offering:

- Digital document upload and e-signature capabilities

- Real-time loan status tracking through mobile apps

- Automated COE retrieval systems

- Direct communication channels to loan officers and processors

For tech professionals at Amazon, Microsoft, and Google relocating to Bellevue or Redmond, efficient digital workflows align with expectations for streamlined processes. Understanding how different Seattle mortgage brokers utilize technology helps identify lenders matching your communication preferences.

Closing Speed and Underwriting Capacity

Timing matters in competitive markets. Veterans submitting offers on homes in Lake Forest Park or Everett compete against conventional buyers who may close faster. The strongest va loan mortgage companies maintain adequate underwriting staff and streamlined workflows to deliver quick decisions.

Standard VA loan timelines range from 30 to 45 days, but experienced lenders can close in 21 days or less when borrowers provide documentation promptly. Some lenders, including those with direct underwriting authority, can even close in as few as 9 business days-a critical advantage when competing for desirable properties.

Understanding VA Loan Costs and Fees

While VA loans offer exceptional benefits, veterans should understand associated costs to make informed decisions and accurately budget for homeownership.

VA Funding Fee Structure

The VA funding fee represents a one-time charge that helps sustain the loan program for future generations of service members. In 2026, funding fees vary based on military service category, down payment amount, and whether it's a first or subsequent use of VA benefits.

| Service Type | First Use (0% Down) | Subsequent Use (0% Down) |

|---|---|---|

| Active Duty/Veteran | 2.15% | 3.30% |

| Reserve/National Guard | 2.40% | 3.30% |

| With 5% Down | 1.50% | 1.50% |

| With 10%+ Down | 1.25% | 1.25% |

Veterans receiving disability compensation or surviving spouses are exempt from funding fees entirely. On a $600,000 loan, the funding fee for first-time active-duty users equals $12,900, which can be financed into the loan amount rather than paid upfront.

Lender Fees and Origination Charges

VA regulations limit what lenders can charge, protecting veterans from excessive fees. Allowable charges include:

- Loan origination fees (typically 1% or less)

- Appraisal and inspection costs

- Credit report fees

- Title insurance and escrow services

- Recording fees and transfer taxes

Non-allowable fees that va loan mortgage companies cannot charge veterans include attorney fees (except in specific states), loan processing fees, and underwriting fees. Reputable lenders provide detailed Loan Estimates showing all costs within three business days of application.

Special Considerations for Seattle-Area Veterans

The Pacific Northwest housing market presents unique challenges and opportunities for military borrowers working with va loan mortgage companies.

Property Eligibility and VA Appraisals

VA appraisers evaluate properties not just for value but also for safety and livability standards. Seattle's older housing stock, particularly in neighborhoods like Montlake and Broadway, sometimes requires repairs to meet VA Minimum Property Requirements (MPRs).

Common issues in Seattle-area homes include:

- Wood-destroying organism damage in moisture-prone climates

- Outdated electrical systems in pre-1970s construction

- Drainage and foundation concerns on hillside properties

- Required repairs identified during VA appraisals

Working with experienced va loan mortgage companies helps navigate these situations. Knowledgeable loan officers coordinate with sellers, agents, and contractors to resolve property condition issues without derailing transactions.

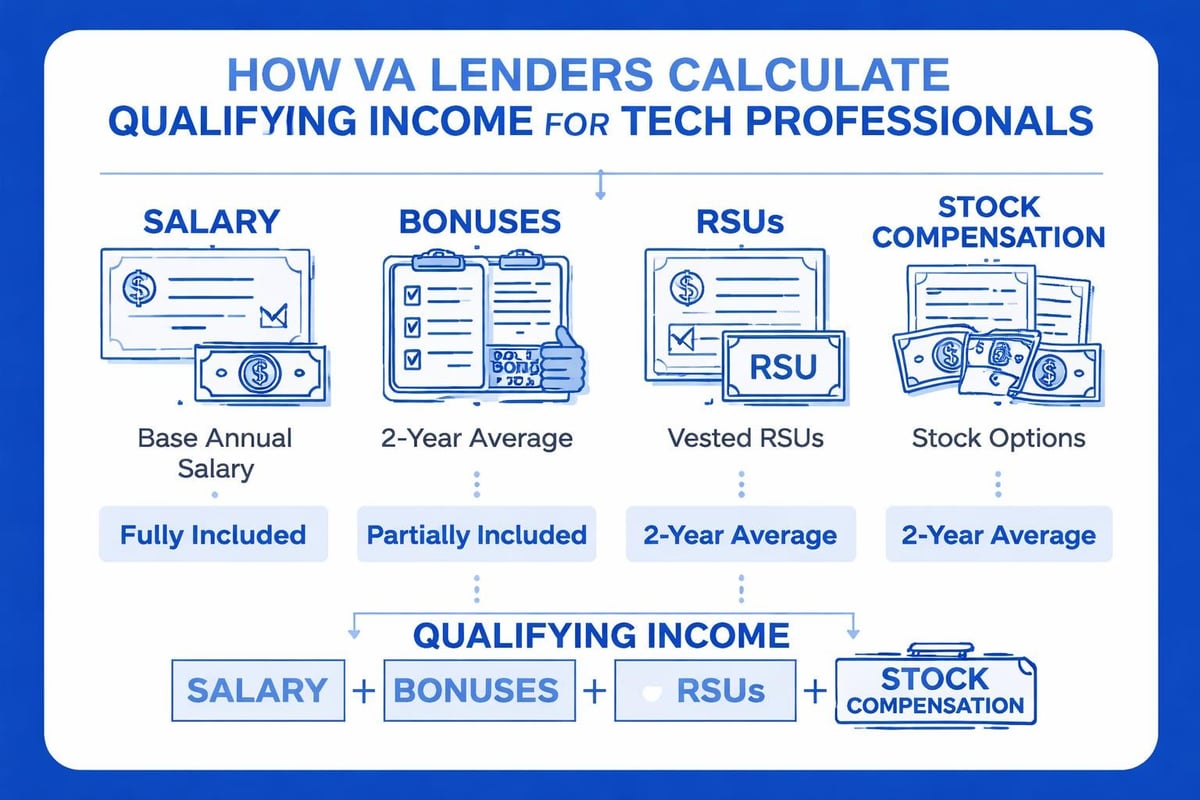

Qualifying Non-Traditional Income

Seattle's concentration of tech employers creates unique qualification scenarios. Veterans employed by Amazon, Microsoft, or other technology companies often receive substantial compensation through restricted stock units (RSUs), stock options, and performance bonuses.

Traditional lenders may struggle to properly document and qualify non-W2 income. Specialized mortgage brokers experienced with jumbo loans and complex compensation understand how to maximize qualifying income from equity compensation, potentially increasing purchasing power by hundreds of thousands of dollars.

Navigating Competitive Offer Situations

Multiple-offer scenarios remain common across Bellevue, Kirkland, and Seattle neighborhoods. VA buyers sometimes face seller resistance based on misconceptions about VA financing. Education and strategic positioning overcome these barriers:

- Pre-approval strength matters more than loan type

- Appraisal gap coverage demonstrates commitment when appropriate

- Quick closing timelines from capable lenders level the playing field

- Strong communication from loan officers to listing agents builds confidence

CNBC’s analysis of the largest VA mortgage lenders shows that while large institutions dominate by volume, local expertise and relationship-driven service often prove more valuable in competitive markets.

VA Loan Servicing and Long-Term Management

The relationship with va loan mortgage companies extends beyond closing. Understanding loan servicing helps veterans protect their investment and navigate potential challenges.

Loan Servicing Transfer and Rights

Most lenders sell VA loans to servicers after closing, as explained in the VA’s guidance on loan servicers. Veterans receive notification before transfers occur and maintain all rights and benefits regardless of who services the loan.

Key servicer responsibilities include:

- Processing monthly payments and managing escrow accounts

- Providing annual tax documentation

- Handling property tax and insurance payments

- Offering loss mitigation assistance if financial hardship occurs

- Coordinating refinance transactions

VA Refinancing Options

Veterans with existing VA loans can access streamlined refinancing through the Interest Rate Reduction Refinance Loan (IRRRL), also called a VA streamline refinance. This program requires minimal documentation, no appraisal in most cases, and no out-of-pocket costs when closing costs are financed.

Additionally, VA cash-out refinancing allows veterans to access home equity at competitive rates without triggering PMI requirements that conventional cash-out loans impose. For Seattle homeowners who purchased several years ago, substantial equity gains make refinancing strategies worth exploring.

Protecting Yourself from VA Loan Scams

Veterans should remain vigilant against deceptive marketing practices targeting military borrowers. The VA warns that it doesn’t send unsolicited mortgage advertisements, and any mail claiming VA endorsement or government affiliation requires scrutiny.

Red Flags When Choosing Lenders

Warning signs of problematic va loan mortgage companies include:

- Unsolicited calls or mail claiming urgent action required

- Pressure to refinance when it doesn't benefit you financially

- Requests for upfront fees before loan approval

- Promises that sound too good to be true

- Lack of proper state licensing or VA approval

Verify lender credentials through state regulatory databases and confirm VA approval status before sharing personal information. Legitimate lenders welcome verification and transparency.

VA Entitlement and Repeat Usage

Understanding how VA loan entitlement works enables veterans to maximize program benefits throughout their homeownership journey. The VA doesn't limit how many times you can use VA loans, but entitlement amounts affect borrowing capacity.

Basic Entitlement and Bonus Entitlement

In 2026, veterans receive basic entitlement of $36,000 plus additional entitlement that varies by county loan limits. For high-cost areas like King County (covering Seattle, Bellevue, and Redmond), the conforming loan limit is $806,500, giving veterans total entitlement of $201,625.

This structure allows qualified veterans to purchase homes exceeding $1 million with zero down payment when working with va loan mortgage companies that understand entitlement calculations. The comprehensive Wikipedia overview of VA loans provides historical context on how the program evolved to support veterans in expensive housing markets.

Restoring and Reusing Entitlement

Veterans who sell homes purchased with VA loans can restore full entitlement for future purchases. Alternatively, veterans with remaining entitlement can use it for second properties or while still owning a VA-financed home, subject to occupancy requirements and lender overlays.

Working with Local Mortgage Professionals

While national va loan mortgage companies offer convenience and marketing reach, local mortgage brokers bring distinct advantages to Seattle-area veterans. Brokers access multiple wholesale lenders, comparing programs to find optimal solutions for each borrower's unique situation.

Benefits of working with experienced Seattle mortgage brokers include personalized guidance through complex scenarios, relationships with local real estate professionals who facilitate smooth transactions, and knowledge of Pacific Northwest property markets that inform strategic decisions.

For veterans purchasing in Lynnwood, Mill Creek, Everett, or other suburban markets, local expertise helps identify neighborhoods with strong value propositions, school quality, and appreciation potential. Combined with VA loan benefits, strategic property selection builds long-term wealth for military families.

Common VA Loan Myths and Misconceptions

Several persistent myths about VA financing create unnecessary hesitation among eligible veterans. Dispelling these misconceptions helps military borrowers make confident decisions.

Myth: VA loans take longer to close than conventional loans. Reality: Experienced va loan mortgage companies close VA loans as quickly as conventional mortgages, often within 21 days or less with proper documentation.

Myth: Sellers won't accept VA offers. Reality: In 2026, educated sellers and agents recognize that well-qualified VA buyers with strong pre-approvals represent excellent purchasers, especially given VA loans' low default rates.

Myth: VA appraisals are overly strict. Reality: VA appraisals protect both veterans and the VA by ensuring properties meet basic safety standards. Most homes pass without issue.

Myth: You can only use VA loans once. Reality: Veterans can use VA loans repeatedly throughout their lives, subject to available entitlement.

Maximizing Your VA Loan Benefits in 2026

Strategic planning helps veterans optimize VA loan advantages for their specific circumstances and homeownership goals in the Seattle area.

Timing Your Purchase

Interest rate environments fluctuate, but waiting for perfect conditions often costs more than acting when personally ready. Veterans should focus on:

- Personal financial readiness and stable employment

- Local market inventory and seasonal patterns

- Life circumstances that make homeownership appropriate

- Long-term housing plans aligned with military career trajectory

Current Seattle mortgage rates and market conditions help inform timing decisions, but individual readiness matters most.

Preparing Strong Applications

Documentation preparation accelerates approvals and strengthens negotiating positions. Veterans should gather:

- Two years of W-2s and tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Certificate of Eligibility from the VA

- Documentation of non-traditional income sources

For service members with complex financial profiles, including those with stock compensation or business income, early consultation with knowledgeable va loan mortgage companies identifies potential challenges and solutions before house hunting begins.

Leveraging Residual Income Standards

VA underwriting includes residual income requirements based on family size and regional cost of living. These standards ensure veterans have adequate monthly income remaining after all debts and obligations. While conventional loans focus primarily on debt-to-income ratios, VA's residual income approach provides a more holistic assessment of financial capacity.

Seattle's high cost of living means regional residual income requirements exceed national averages. For a family of four in the Pacific Northwest, VA guidelines require $1,062 in monthly residual income. Working with lenders who understand these calculations helps structure debt payoff strategies that maximize qualifying potential.

Choosing among va loan mortgage companies represents a critical decision that impacts both your home purchase experience and long-term financial success. Veterans in the Seattle area deserve lenders who combine VA expertise with local market knowledge, transparent communication, and proven execution in competitive environments. Keith Akada at Mortgage Reel brings 25+ years of experience helping military families and civilians navigate complex mortgage scenarios, from VA loans to jumbo financing for tech professionals with stock-based compensation, serving Seattle, Bellevue, Redmond, Kirkland, and surrounding communities with the responsiveness and strategic guidance that earn 750+ five-star reviews.