Navigating the path to homeownership in Seattle's competitive real estate market can feel overwhelming, especially for those making their first purchase. An fha loan first time buyer program offers an accessible solution, providing lower down payment requirements and more flexible credit standards than conventional financing. These government-backed mortgages have helped countless Seattle-area residents in communities from Bellevue to Lynnwood achieve their homeownership goals, even when traditional financing seemed out of reach. Understanding how FHA loans work and whether they align with your financial situation is essential for making confident decisions in 2026's evolving mortgage landscape.

What Makes FHA Loans Ideal for First-Time Buyers

FHA loans are mortgages insured by the Federal Housing Administration, designed specifically to make homeownership more accessible. For first-time buyers in Seattle, Shoreline, and surrounding areas, these loans present several distinct advantages that address common barriers to entry.

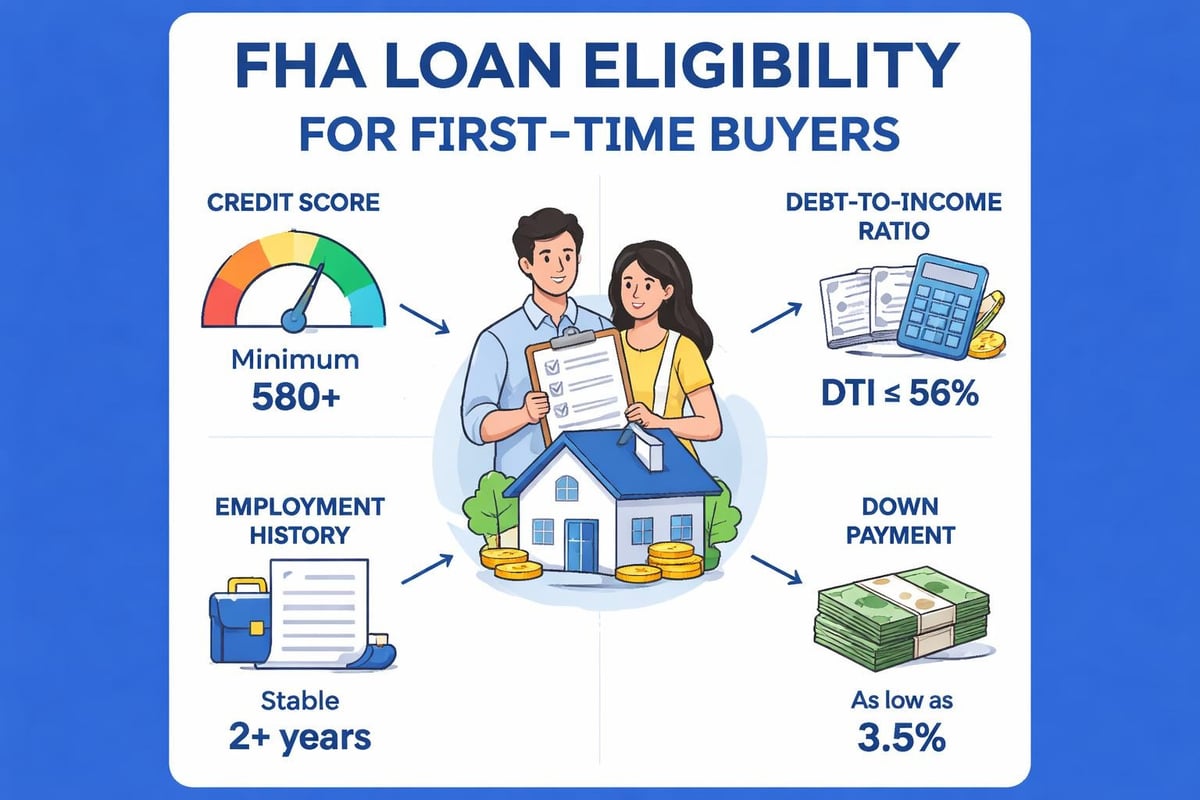

The most significant benefit is the low down payment requirement. While conventional loans typically demand 5-20% down, FHA loans require just 3.5% for borrowers with credit scores of 580 or higher. In Seattle's market, where median home prices continue to challenge buyers, this difference can be substantial.

Credit Flexibility and Qualification Standards

FHA loans accommodate borrowers with less-than-perfect credit histories. Here's how the credit requirements break down:

- Credit score of 580 or higher: Qualifies for 3.5% down payment

- Credit score between 500-579: May qualify with 10% down payment

- Recent credit issues: FHA guidelines allow consideration of applicants with past bankruptcies or foreclosures after waiting periods

This flexibility proves particularly valuable for young professionals in Redmond and Kirkland who may have limited credit history or tech workers who experienced financial setbacks during industry transitions.

| Loan Type | Minimum Down Payment | Minimum Credit Score | DTI Ratio Limit |

|---|---|---|---|

| FHA Loan | 3.5% | 580 | 43% (flexible to 50%) |

| Conventional Loan | 3-5% | 620 | 43-45% |

| VA Loan | 0% | No minimum | 41% (flexible) |

Understanding FHA Loan Costs and Requirements

While FHA loans offer accessibility, they come with specific costs that buyers should understand before committing. The FHA loan qualification process involves both upfront and ongoing expenses that differ from conventional financing.

Mortgage Insurance Premiums Explained

FHA mortgage insurance protects lenders against default, but it adds to your monthly payment. This insurance comes in two forms:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of the loan amount, typically rolled into the loan

- Annual Mortgage Insurance Premium (MIP): 0.45% to 1.05% annually, divided into monthly payments

For a $600,000 home in Mill Creek with 3.5% down ($21,000), your loan amount would be $579,000. The upfront premium adds $10,132.50, and monthly MIP might range from $217 to $507 depending on your loan terms.

Important distinction: Unlike conventional PMI, which cancels at 20% equity, FHA MIP remains for the loan's life if you put down less than 10%. This long-term cost warrants careful comparison with other loan options.

Property Standards and Appraisal Requirements

FHA loans require properties to meet specific safety and habitability standards. The FHA appraisal examines:

- Structural integrity and safety systems

- Adequate heating, electrical, and plumbing

- Proper drainage and foundation condition

- Lead-based paint compliance for pre-1978 homes

In Seattle's market, where older homes in neighborhoods like Lake Forest Park may require updates, these standards can affect your purchasing timeline. Working with experienced professionals who understand Seattle mortgage financing helps navigate these requirements efficiently.

FHA Loan Limits in the Seattle Market

FHA loan limits vary by county and are adjusted annually based on median home prices. For 2026, King County's FHA loan limits reflect the region's high-cost housing market.

King County FHA Limits for 2026:

- Single-family home: $806,500

- Two-unit property: $1,032,700

- Three-unit property: $1,248,400

- Four-unit property: $1,550,850

These limits exceed the national baseline, acknowledging Seattle's elevated housing costs. However, buyers seeking properties above these thresholds must explore alternative financing, such as jumbo home loans, which require different qualification criteria.

Strategic Considerations for Seattle Buyers

For first-time buyers in Everett or Lynnwood, where home prices may fall comfortably within FHA limits, these loans provide excellent opportunities. Tech professionals at Microsoft or Amazon with strong income but limited savings particularly benefit from the low down payment structure.

Consider this scenario: A software engineer earning $180,000 annually wants to purchase a $650,000 condo in Bellevue. With an FHA loan:

- Down payment needed: $22,750 (3.5%)

- Closing costs: approximately $13,000-$19,500

- Total cash required: $35,750-$42,250

The same purchase with a conventional loan requiring 5% down would demand $32,500 plus closing costs-a difference that allows faster entry into the market while preserving emergency savings.

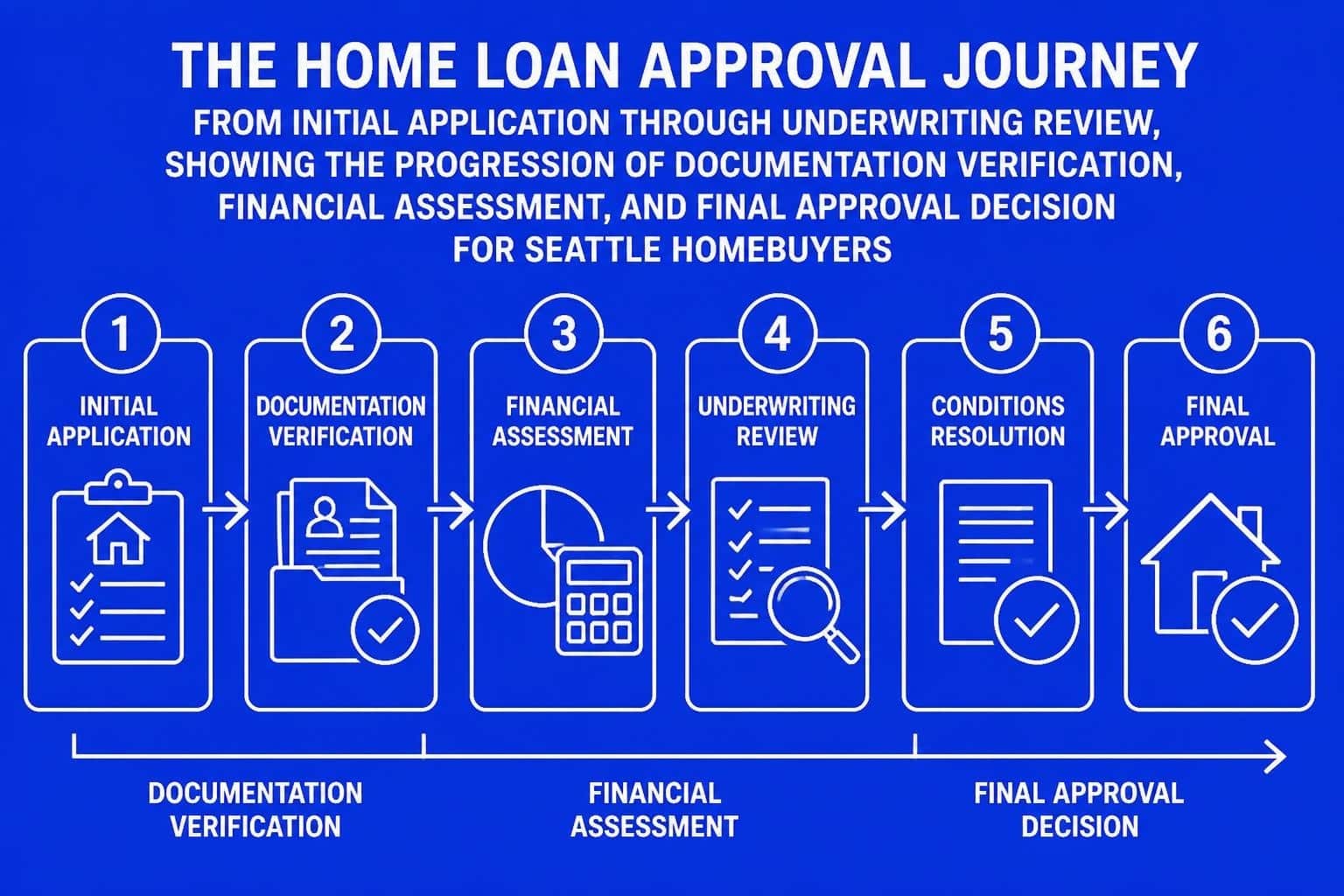

The Application Process for FHA Loan First Time Buyer Programs

Securing an FHA loan follows a structured process that requires preparation and documentation. Understanding each step helps first-time buyers move efficiently toward closing.

Pre-Qualification and Documentation

Step 1: Financial Assessment

Begin by evaluating your financial readiness. Lenders examine:

- Credit history and score

- Employment stability (typically 2 years)

- Debt-to-income ratio

- Available funds for down payment and closing

Step 2: Document Gathering

Prepare comprehensive documentation including:

- Two years of tax returns and W-2s

- Recent pay stubs (30-60 days)

- Bank statements (2-3 months)

- Explanation letters for credit issues or employment gaps

For tech professionals with RSU compensation, additional documentation of stock awards and vesting schedules strengthens your application. Understanding how to qualify stock income maximizes your purchasing power in Seattle's competitive market.

Finding the Right Lender and Property

Step 3: Lender Selection

Not all lenders offer identical FHA experiences. Prioritize those who:

- Demonstrate Seattle market expertise

- Provide clear communication throughout the process

- Offer competitive rates and closing timelines

- Have strong reviews from previous clients

The top mortgage brokers in Seattle combine local knowledge with efficient processing, essential in markets where properties receive multiple offers within days.

Step 4: Home Search and Offer

Working with a real estate agent familiar with FHA requirements prevents wasted time on incompatible properties. Some sellers prefer conventional or cash offers, perceiving FHA loans as slower or more restrictive. However, in 2026's balanced market, many sellers welcome qualified FHA buyers, especially with quick closing capabilities.

| Timeline Phase | Typical Duration | Key Activities |

|---|---|---|

| Pre-approval | 1-3 days | Document review, credit check |

| Home search | 2-8 weeks | Property tours, offer preparation |

| Under contract | 30-45 days | Appraisal, underwriting, inspection |

| Closing | 1 day | Final walkthrough, signing documents |

Maximizing Your FHA Loan Strategy in 2026

Strategic planning separates successful first-time buyers from those who struggle or overpay. Several approaches enhance your FHA loan experience in Seattle's unique market conditions.

Credit Optimization Before Application

Timing matters significantly. If your credit score hovers near 580, delaying your purchase by 3-6 months to improve your score can save thousands over the loan term. Focus on:

- Paying down credit card balances below 30% utilization

- Avoiding new credit inquiries or accounts

- Correcting errors on credit reports

- Making all payments on time without exception

A 20-point score improvement from 575 to 595 might not change your down payment requirement but typically results in better interest rates and lower mortgage insurance premiums.

Down Payment Strategies Beyond the Minimum

While 3.5% down opens the door, contributing more provides advantages:

- Lower monthly payments: Smaller loan amount reduces principal and interest

- Reduced mortgage insurance: Some tiers have lower MIP rates

- Stronger offers: Larger down payments signal financial stability to sellers

- Faster equity building: Starting with more equity protects against short-term market fluctuations

First-time buyers in Shoreline or Mill Creek should explore down payment assistance programs available through Washington State Housing Finance Commission, which can supplement FHA financing and reduce out-of-pocket costs.

Rate Shopping and Timing Considerations

Interest rates fluctuate based on economic conditions, and even small differences compound significantly over 30 years. On a $580,000 FHA loan:

- At 6.5% interest: Monthly payment of $3,665 (principal and interest)

- At 6.0% interest: Monthly payment of $3,476 (principal and interest)

- Savings: $189 monthly, $68,040 over loan life

Monitor Seattle mortgage rates regularly and consider rate lock strategies when application timing aligns with favorable conditions. Most lenders offer 30-60 day rate locks, protecting you from increases during the closing process.

Common Misconceptions About FHA Loans

Several myths persist about FHA financing that deter qualified buyers from considering this option. Addressing these misconceptions helps first-time buyers make informed decisions.

Myth 1: FHA loans are only for low-income buyers

Reality: FHA loans serve buyers across income spectrums. In Seattle, high earners with excellent income stability but limited savings frequently choose FHA loans to enter the market faster while preserving cash for renovations, investments, or emergencies.

Myth 2: Sellers won't accept FHA offers

Reality: While some sellers prefer conventional financing, many accept FHA offers, particularly in balanced or buyer-favorable markets. Professional presentation, strong pre-approval letters, and competitive terms overcome most seller hesitations. Quick closing capabilities, sometimes as fast as 9 business days, further strengthen FHA offers.

Myth 3: You must be a first-time buyer

Reality: Despite the common association with first-time buyers, FHA loans welcome repeat buyers who meet standard qualifications. The program simply provides features particularly beneficial to those purchasing their first home.

Myth 4: FHA loans are difficult to qualify for

Reality: FHA qualification is often more accessible than conventional financing. The flexible credit standards, higher debt-to-income allowances, and lower down payment requirements actually simplify qualification for many buyers.

Comparing FHA Loans to Other First-Time Buyer Options

Understanding your complete range of financing options ensures you select the best fit for your specific situation. Seattle first-time buyers should evaluate several alternatives alongside FHA loans.

Conventional 97 Loans

These conventional loans require just 3% down and offer some advantages over FHA:

- Mortgage insurance cancels at 20% equity

- No upfront mortgage insurance premium

- Sometimes lower total costs for high-credit borrowers

However, they require higher credit scores (typically 620-680) and stricter debt-to-income limits. For buyers with strong credit but minimal savings, conventional 97 loans deserve consideration.

Washington State First-Time Buyer Programs

Washington State Housing Finance Commission offers programs combining conventional or FHA loans with down payment assistance. These programs provide:

- Grants or low-interest second mortgages for down payment

- Reduced interest rates for qualified buyers

- Income and purchase price limits varying by county

These programs work particularly well in Lynnwood, Everett, and other areas where median prices fall within program limits.

HomeReady and Home Possible Loans

Fannie Mae's HomeReady and Freddie Mac's Home Possible programs target moderate-income buyers with:

- 3% minimum down payment

- Flexible income sources (including non-borrower household income)

- Reduced mortgage insurance costs

- Income limits based on area median

For Seattle buyers in qualifying income ranges, these programs sometimes provide better long-term value than FHA loans, especially given the cancellable mortgage insurance.

| Feature | FHA Loan | Conventional 97 | HomeReady/Possible |

|---|---|---|---|

| Minimum down payment | 3.5% | 3% | 3% |

| Credit score minimum | 580 | 620-680 | 620 |

| MI cancellation | Loan life* | At 20% equity | At 20% equity |

| Income limits | None | None | Yes (varies) |

| Best for | Lower credit, limited savings | Strong credit, minimal savings | Moderate income, good credit |

*For loans with less than 10% down

Working with Stock Compensation and Non-Traditional Income

Seattle's tech economy creates unique challenges and opportunities for first-time buyers. Many employees at Amazon, Microsoft, Google, and other major employers receive significant compensation through RSUs, stock options, and bonuses rather than traditional salary alone.

Qualifying RSU and Stock Income

FHA guidelines allow inclusion of stock compensation when documented properly:

Requirements for RSU qualification:

- Two-year history of vesting and liquidation

- Consistent or increasing award amounts

- Documentation through pay stubs, tax returns, and award letters

- Average of past two years used for qualification

For example, a program manager earning $140,000 base salary plus $60,000 annually in RSUs can qualify using $200,000 income if the two-year history demonstrates consistency.

Bonus Income Strategies

Annual bonuses strengthen FHA applications when they meet specific criteria:

- Consistency: Two-year history showing regular receipt

- Stability: Similar or increasing amounts year-over-year

- Likelihood of continuance: Employer verification of ongoing bonus structure

A software engineer receiving $20,000 annual bonuses for three consecutive years can typically include the full amount in qualifying income, significantly increasing purchasing power.

Understanding how lenders evaluate these income sources-especially for Seattle home financing-helps tech professionals maximize their FHA loan approval amounts and secure properties that align with their true financial capacity.

Strategic Refinancing Considerations

While this article focuses on purchase loans, understanding future refinancing possibilities helps first-time buyers plan long-term strategies. Many fha loan first time buyer recipients refinance within 3-5 years as their financial situations improve.

FHA Streamline Refinancing

FHA streamline refinance programs allow existing FHA borrowers to refinance with minimal documentation and no appraisal in many cases. Benefits include:

- Lower interest rates without full underwriting

- Reduced documentation requirements

- No income or employment verification needed

- Quick processing timelines

Conventional Refinancing to Eliminate MIP

Once you build 20% equity through appreciation or principal paydown, refinancing to a conventional loan eliminates ongoing mortgage insurance. In Seattle's appreciating market, this timeline often arrives faster than the standard amortization schedule suggests.

Consider a Lake Forest Park buyer purchasing a $650,000 home in 2026. If the property appreciates 4% annually:

- 2026: Purchase price $650,000, equity $22,750 (3.5%)

- 2029: Estimated value $731,000, equity ~$103,500 (14.2%)

- 2031: Estimated value $791,000, equity ~$163,000 (20.6%)

At this point, refinancing to conventional financing eliminates MIP and potentially secures better rates, reducing monthly payments significantly.

Navigating Seattle's Competitive Market with FHA Loans

Seattle's real estate market presents unique challenges requiring strategic approaches. First-time buyers using FHA loans can compete successfully by understanding market dynamics and implementing specific tactics.

Making Competitive FHA Offers

Strength signals that matter:

- Strong pre-approval letters: Detailed letters from reputable lenders demonstrate serious qualification

- Flexible timelines: Accommodating seller moving needs shows cooperation

- Personal letters: Connecting emotionally with sellers can differentiate similar offers

- Escalation clauses: Automatic bid increases up to specified limits

- Minimal contingencies: Reducing unnecessary contingencies while maintaining critical protections

In Redmond's competitive neighborhoods, working with agents experienced in multiple-offer situations ensures your FHA offer receives proper consideration against conventional and cash competitors.

Inspection and Appraisal Strategies

FHA appraisals examine properties more thoroughly than conventional appraisals, potentially identifying required repairs. Prepare for this by:

- Requesting seller pre-inspection reports

- Building repair negotiation strategies into offers

- Maintaining flexibility for minor repair requirements

- Understanding which issues are negotiable versus deal-breakers

Experienced buyers in Kirkland and Bellevue often include repair allowances in initial offers, demonstrating awareness of FHA standards and willingness to address issues cooperatively.

Tax Benefits and Long-Term Financial Planning

Homeownership through FHA loans provides financial advantages extending beyond monthly housing costs. Understanding these benefits helps first-time buyers appreciate the complete value proposition.

Mortgage Interest Deduction

Mortgage interest paid on FHA loans remains tax-deductible for most borrowers, subject to current tax law limits. For Seattle-area buyers in higher tax brackets, this deduction provides meaningful annual savings.

On a $580,000 FHA loan at 6.5% interest, first-year interest approximates $37,000. For a borrower in the 24% federal tax bracket, this deduction could save approximately $8,880 annually in federal taxes alone.

Equity Building and Wealth Creation

Despite higher upfront costs, FHA loans facilitate wealth building through forced savings (principal paydown) and appreciation exposure. Seattle's historical appreciation rates, averaging 4-6% annually over long periods, amplify these benefits.

A first-time buyer purchasing a $650,000 Shoreline home in 2026 might see:

- Year 5: ~$80,000 equity from principal and appreciation

- Year 10: ~$220,000 equity from principal and appreciation

- Year 15: ~$400,000 equity from principal and appreciation

This wealth accumulation typically exceeds what renters achieve through other savings vehicles, even accounting for maintenance costs and property taxes.

FHA loans provide Seattle-area first-time buyers with an accessible, flexible path to homeownership despite the region's challenging housing costs. From Everett to Bellevue, these government-backed mortgages help qualified buyers overcome down payment barriers while building long-term equity and wealth. Whether you're navigating stock compensation as a tech professional or simply ready to stop renting and start building equity, understanding FHA loan mechanics empowers confident decision-making. Keith Akada at Mortgage Reel brings 25+ years of experience helping first-time buyers throughout Seattle, Shoreline, Redmond, and surrounding communities navigate FHA loans and alternative financing options with transparency, education, and proven execution that consistently earns five-star reviews from satisfied clients.