Securing financing for a home purchase or refinance represents one of the most significant financial decisions you'll make in your lifetime. For homebuyers in Seattle, Bellevue, Redmond, and Kirkland, understanding how to get a mortgage loan efficiently can mean the difference between losing out in a competitive market and confidently closing on your ideal property. The Seattle-area housing market, particularly for tech professionals at Amazon, Microsoft, and Google, requires specialized knowledge of income qualification, loan structuring, and strategic timing. This comprehensive guide walks you through every stage of the mortgage process, from initial preparation to final approval, with insights tailored to the Greater Seattle region.

Understanding Mortgage Loan Basics

Before you begin the application process, establishing a foundation of mortgage knowledge helps you make informed decisions and set realistic expectations. A mortgage loan is a secured debt instrument that allows you to purchase real estate by borrowing funds from a lender, with the property itself serving as collateral.

Core Components of Every Mortgage

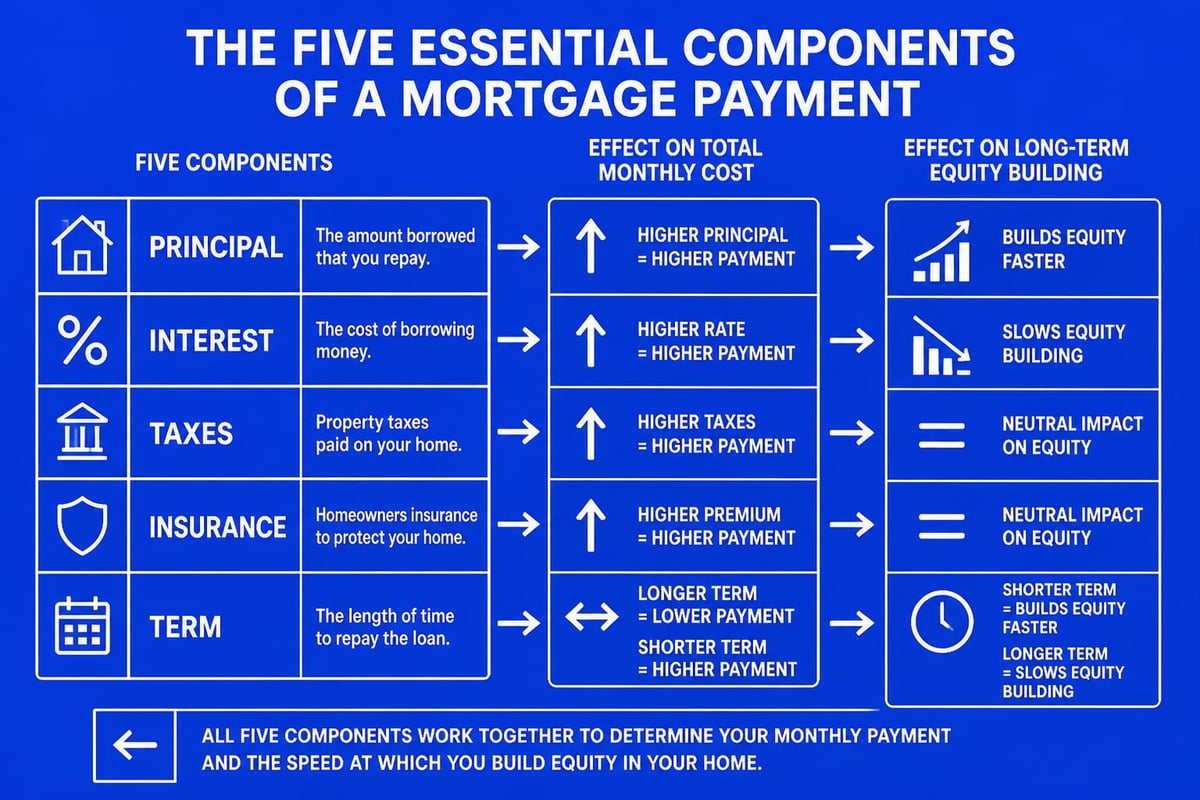

Every mortgage consists of several fundamental elements that determine your monthly payment and long-term costs:

- Principal: The original loan amount borrowed

- Interest: The cost of borrowing, expressed as an annual percentage rate

- Taxes: Property taxes collected through escrow and paid to local authorities

- Insurance: Homeowner's insurance and potentially mortgage insurance (PMI or MIP)

- Term: The length of time to repay the loan, typically 15 or 30 years

Understanding these components helps you evaluate different loan offers and determine which structure aligns with your financial goals. In Seattle and surrounding areas like Shoreline and Lake Forest Park, property taxes and insurance costs vary significantly by location, making local expertise valuable.

Loan-to-Value Ratio and Equity

Your loan-to-value (LTV) ratio represents the relationship between your loan amount and the property's appraised value. This metric directly impacts your interest rate, qualification requirements, and whether you'll need mortgage insurance.

For example, a $600,000 home purchase in Redmond with a $120,000 down payment creates a loan amount of $480,000, resulting in an 80% LTV. Maintaining an LTV at or below 80% typically eliminates the need for private mortgage insurance on conventional loans, reducing your monthly payment.

Types of Mortgage Loans Available

Choosing the right loan type requires understanding your financial profile, homeownership timeline, and property specifics. The Consumer Financial Protection Bureau provides detailed comparisons of loan options that can help you evaluate which programs suit your situation.

Conventional Loans

Conventional mortgages are not backed by government agencies and typically require stronger credit profiles and larger down payments than government-backed alternatives. These loans offer flexibility in property types and usage, making them popular among Seattle-area homebuyers.

Key Advantages:

- Lower overall costs for borrowers with strong credit (typically 620+)

- No upfront mortgage insurance premium

- PMI can be removed once equity reaches 20%

- Available for primary residences, second homes, and investment properties

Common Scenarios:

- Tech professionals with substantial stock compensation purchasing in Bellevue

- Move-up buyers with existing equity from previous home sales

- Borrowers seeking flexibility in property types or rental strategies

For Seattle homebuyers, conventional home loans provide competitive rates and streamlined processing when you meet qualification standards.

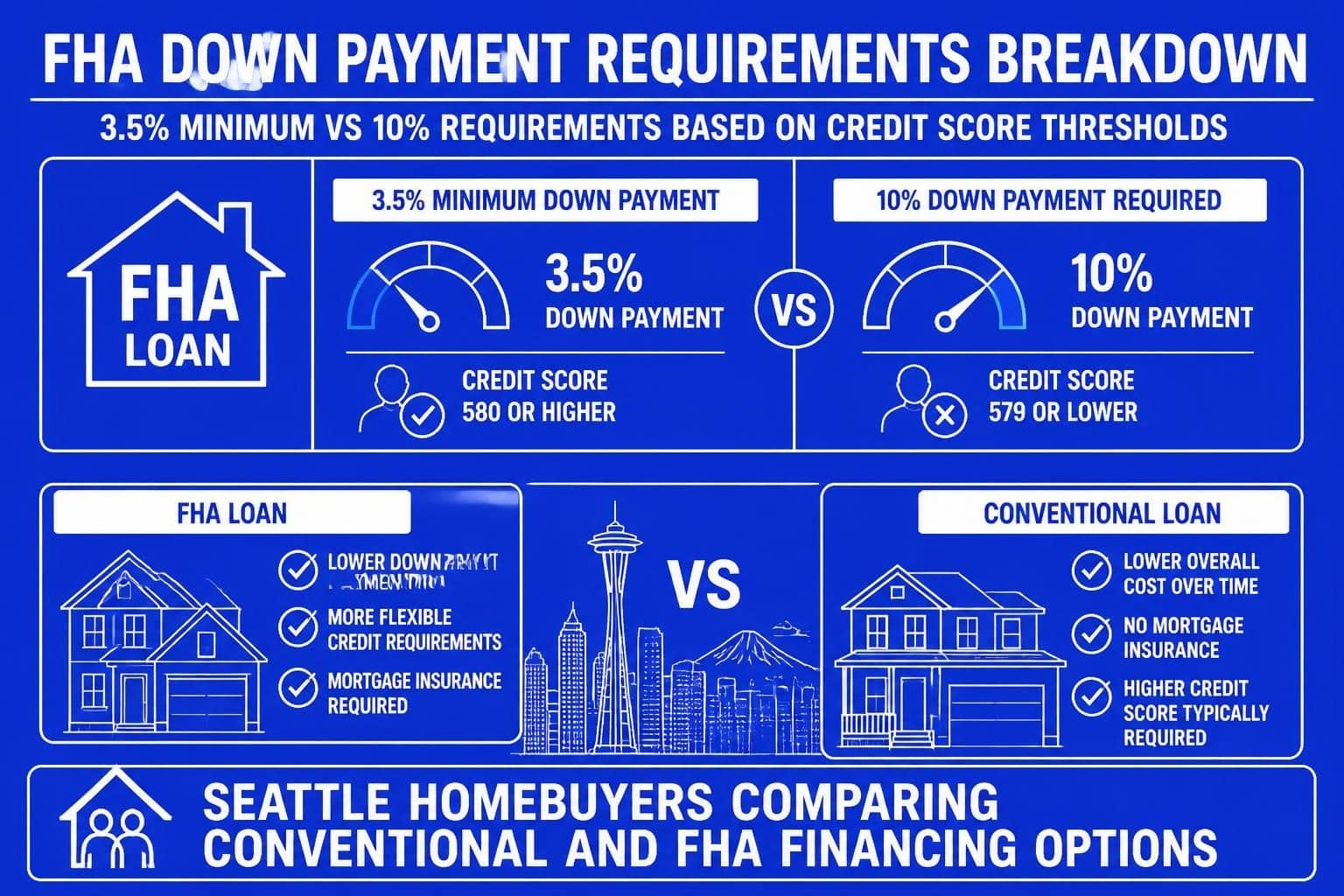

Government-Backed Loan Programs

Government-backed loans serve specific borrower segments and property requirements, offering advantages like lower down payments and flexible credit standards.

| Loan Type | Down Payment | Credit Requirement | Insurance | Best For |

|---|---|---|---|---|

| FHA | 3.5% minimum | 580+ (typically) | Upfront + monthly MIP | First-time buyers, lower credit scores |

| VA | 0% possible | No minimum | Funding fee (waived for disabled veterans) | Active military, veterans, eligible spouses |

| USDA | 0% required | 640+ (typically) | Upfront + annual fee | Rural/suburban properties, income limits |

FHA home loans remain popular with first-time buyers in neighborhoods throughout Seattle and Mill Creek, while VA loans provide exceptional benefits for military service members purchasing in the region.

Jumbo Loans for High-Value Properties

When your loan amount exceeds conforming loan limits (set at $806,500 for most Washington counties in 2026, higher for King County), you enter jumbo loan territory. These loans require stronger qualifications but provide access to Seattle's higher-priced housing market.

Jumbo Loan Characteristics:

- Larger loan amounts above conforming limits

- Typically require 10-20% down payment depending on loan amount

- Credit scores generally 700+ for best rates

- More stringent income and asset documentation

- Competitive rates for well-qualified borrowers

Seattle's competitive housing market, particularly in Kirkland and Bellevue, frequently requires jumbo home loans for properties exceeding conforming limits. Understanding RSU income qualification becomes critical for tech professionals seeking to maximize purchasing power.

Preparing to Get a Mortgage Loan

Preparation significantly impacts your success rate, interest rate, and overall experience. Strong preparation positions you as a competitive buyer in fast-moving markets like Seattle and Lynnwood.

Credit Profile Optimization

Your credit score serves as a primary qualification factor, influencing both approval odds and pricing. Three to six months before you plan to get a mortgage loan, review your credit reports from all three bureaus and address any issues.

Credit Improvement Strategies:

- Pay down revolving balances below 30% of credit limits

- Dispute inaccurate information on credit reports

- Avoid opening new credit accounts

- Maintain on-time payments across all obligations

- Keep old credit accounts open to preserve history length

For Seattle-area homebuyers wondering about minimum credit score requirements, standards vary by loan type, but stronger scores unlock better rates and terms.

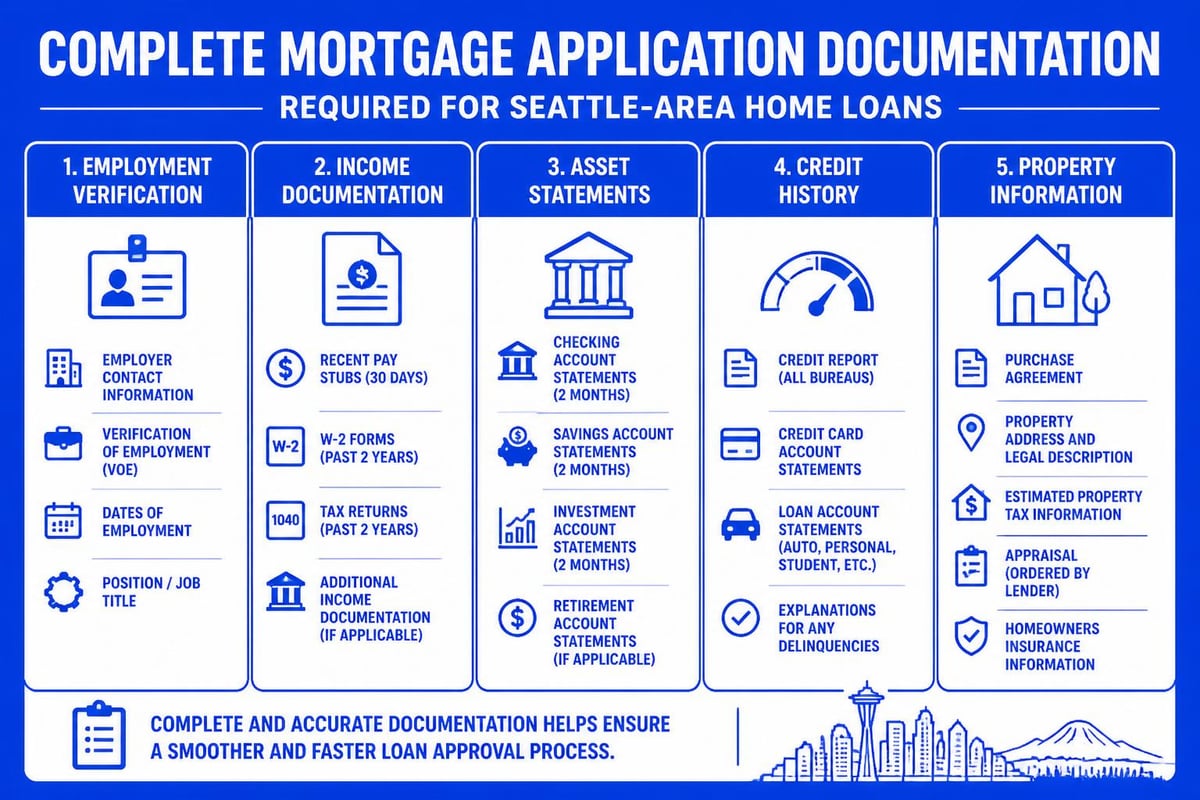

Documentation Assembly

Gathering documentation before you apply streamlines the process and demonstrates preparedness to lenders. The mortgage application process requires comprehensive financial documentation.

Essential Documents for Employment:

- Two years of W-2s and tax returns

- Recent pay stubs (typically last 30 days)

- Year-to-date profit and loss statement for self-employed borrowers

- Stock compensation documentation (RSU grants, vesting schedules, exercise history)

- Employer verification of bonuses or commission income

Asset Documentation:

- Two months of bank statements for all accounts

- Retirement account statements showing balances

- Investment account statements

- Gift letter and proof of transfer for down payment gifts

- Documentation of other real estate owned

For tech professionals in Seattle with complex compensation structures, organizing comprehensive stock documentation early in the process prevents delays during underwriting.

Down Payment Planning

Your down payment amount influences loan type eligibility, interest rates, and monthly payment structure. Down payment requirements vary significantly by loan program and property price.

Down Payment Sources:

- Personal savings and checking accounts

- Investment account liquidation

- Employer stock sales (with careful tax planning)

- Gift funds from family members

- Down payment assistance programs for qualified buyers

- Sale proceeds from existing property

Seattle-area buyers should evaluate whether 10% or 20% down payments make more sense for their situation, particularly on jumbo loans where requirements differ from conforming mortgages.

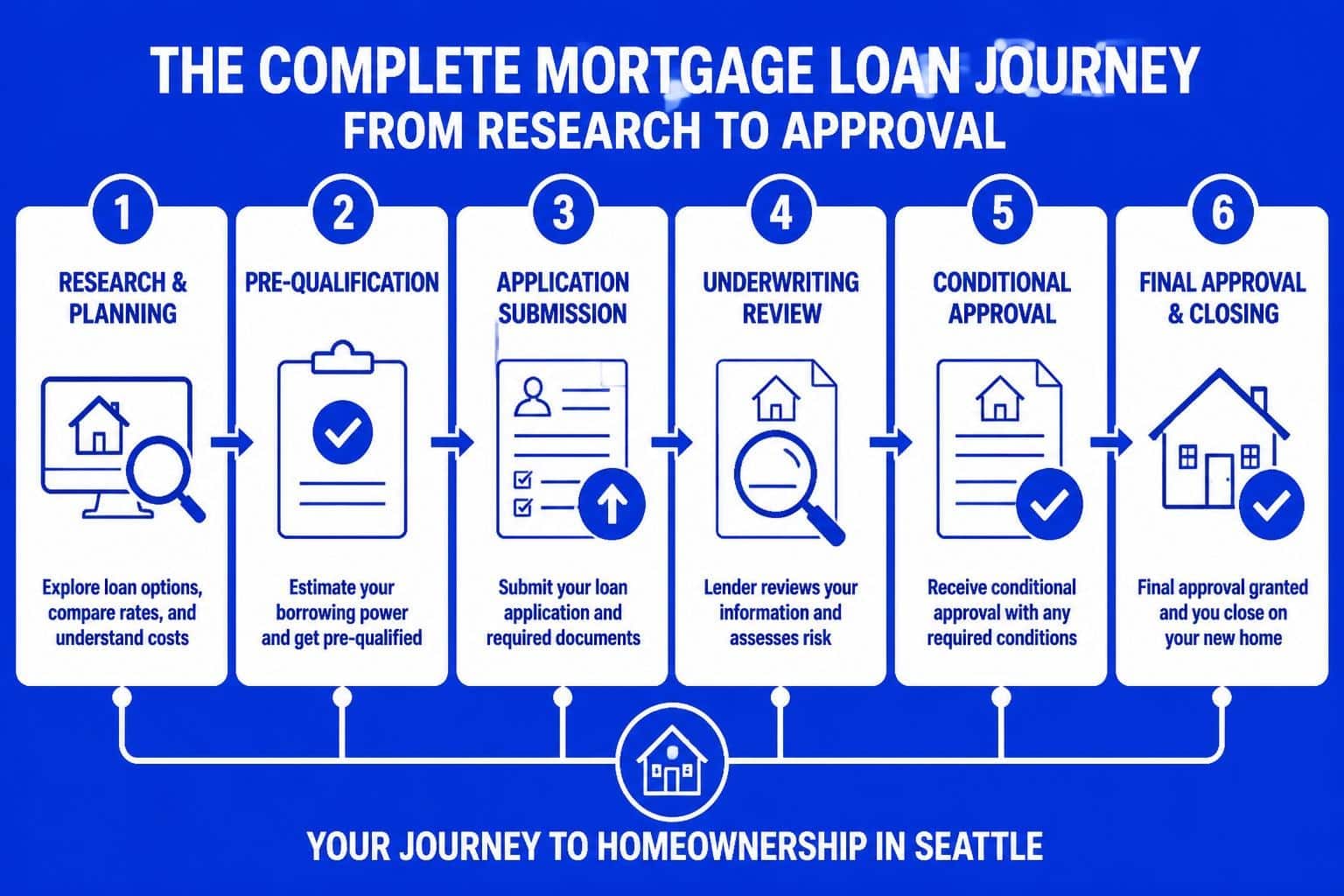

The Step-by-Step Mortgage Application Process

Understanding each stage of the mortgage process helps you set expectations and respond promptly to lender requests. Redfin’s comprehensive guide outlines the typical timeline and milestones.

Pre-Approval vs. Pre-Qualification

These terms are often confused, but they represent different levels of lender commitment and buyer readiness.

Pre-qualification provides a rough estimate based on self-reported information without verification. Pre-approval involves a full credit check, income verification, and conditional approval subject to finding a property and final underwriting.

In competitive Seattle markets, sellers and listing agents strongly prefer pre-approved buyers who demonstrate serious intent and verified financial capacity.

Formal Application Submission

Once you've identified a property and have an accepted offer, you submit a formal loan application (Uniform Residential Loan Application, or URLA). This triggers several immediate actions:

- Lender pulls credit reports from all three bureaus

- You provide all required documentation

- Property appraisal gets ordered

- Title company begins title search and insurance process

- Application enters processing queue

Timeline Expectations:

From application to closing typically ranges from 21 to 45 days, though experienced lenders with advanced underwriting systems can close loans in as few as 9 business days when all conditions align properly.

Processing and Underwriting

During processing, a loan processor verifies every aspect of your application, ordering verifications of employment, reviewing bank statements, and ensuring documentation completeness.

Underwriting represents the lender's risk assessment phase, where an underwriter evaluates three primary factors:

- Credit: Your history of managing debt obligations

- Capacity: Your ability to repay based on income and debt ratios

- Collateral: The property's value and condition

Underwriters may request additional documentation or explanations, called conditions. Responding promptly to conditions keeps your timeline on track. Understanding how long the mortgage process takes in Seattle's market helps you plan accordingly.

Appraisal and Property Evaluation

The lender orders an independent appraisal to confirm the property's market value supports the loan amount. In competitive markets like Everett and Shoreline, appraisal values occasionally come in below purchase prices, creating challenges that require negotiation or additional cash.

Appraisers evaluate:

- Recent comparable sales in the immediate area

- Property condition, size, and features

- Location factors and neighborhood characteristics

- Any health or safety issues requiring repair

If the appraisal comes in low, you have several options: negotiate a lower purchase price, increase your down payment to maintain the same LTV, or cancel the contract if your financing contingency remains in effect.

Specialized Qualification Strategies for Seattle Tech Professionals

Seattle's concentration of major tech employers creates unique qualification opportunities and challenges. Maximizing your borrowing power requires understanding how lenders evaluate non-traditional income sources.

Stock Compensation Qualification

Restricted stock units (RSUs), stock options, and employee stock purchase plans represent substantial income sources for many Seattle-area tech workers. Lenders can use this income for qualification, but specific documentation and calculation methods apply.

RSU Qualification Requirements:

- Two-year history of vesting and receiving RSU income

- Year-to-date vesting schedule showing continued income

- Average of past two years, or current year if lower

- Documentation from employer confirming ongoing grants

For professionals wondering about RSU income mortgage qualification, working with a broker experienced in tech compensation structures ensures maximum qualification without delays.

Bonus and Commission Income

Variable income requires a two-year history and conservative calculation methodology. Underwriters typically average the past two years of bonus or commission income, adjusting downward if there's a declining trend.

Documentation Needed:

- Tax returns showing bonuses reported as W-2 income

- Year-to-date pay stubs reflecting current year bonuses

- Letter from employer confirming bonus structure continuation

- Calculation worksheet showing averaging methodology

Closing the Loan

The final stage brings together all previous work into a coordinated closing event where ownership transfers and funding occurs.

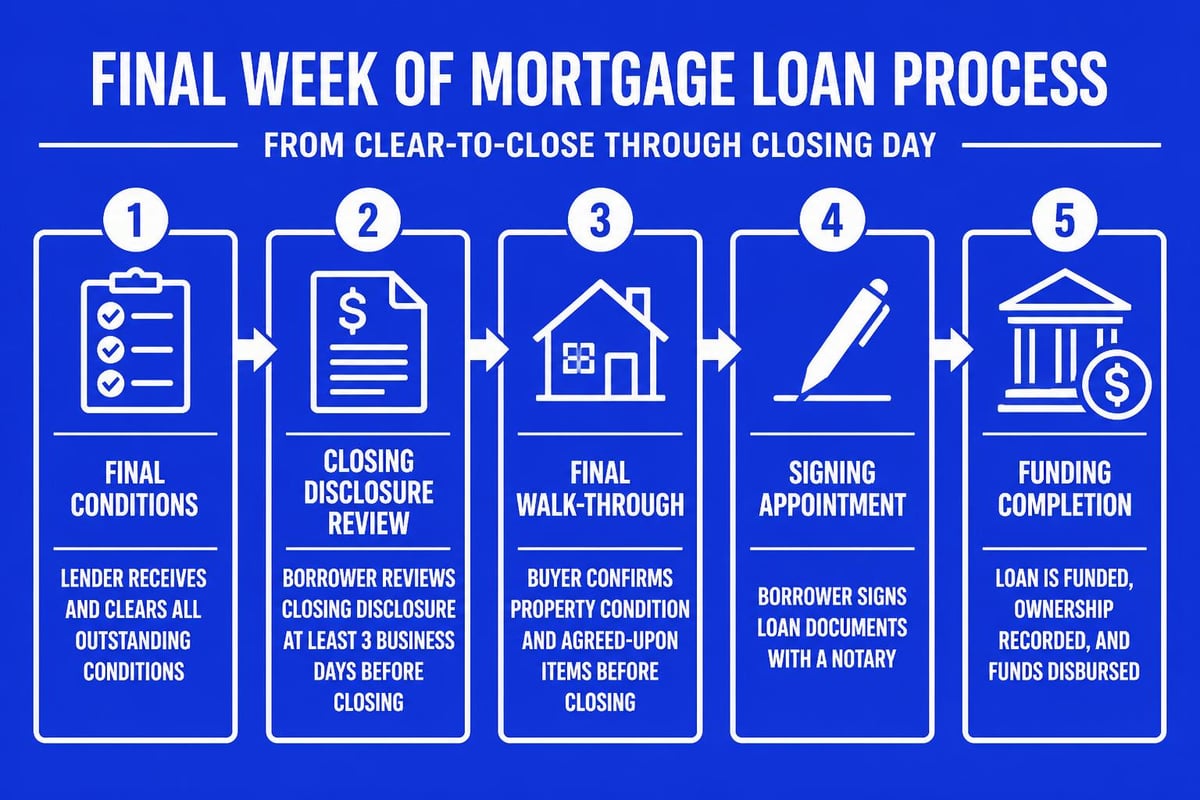

Final Walk-Through and Conditions

Three to five days before closing, you'll receive a Closing Disclosure detailing final loan terms, closing costs, and cash required. Review this document carefully and compare it against your Loan Estimate to ensure alignment.

Final conditions typically include:

- Final verification of employment (often within 24-48 hours of closing)

- Updated bank statements if initial ones have aged

- Explanation of any large deposits since application

- Proof of homeowner's insurance policy

- Clear-to-close status from underwriting

Closing Day Execution

Closing occurs at a title company office where you'll sign loan documents, ownership transfer paperwork, and authorize final fund disbursement. Bring a government-issued ID and certified funds for your down payment and closing costs.

Key Documents You'll Sign:

- Promissory note (your promise to repay)

- Deed of trust (security instrument giving lender collateral rights)

- Closing disclosure (final settlement statement)

- Initial escrow disclosure (property tax and insurance payment schedule)

After signing, the title company records the deed and mortgage, and funding occurs. In Washington State, recording typically happens the same day or next business day, making your purchase official.

Rate Locks and Timing Strategies

Interest rates fluctuate daily based on market conditions, making rate lock timing an important strategic decision. Understanding fixed-rate loan advantages helps you evaluate different rate structures.

When to Lock Your Rate

Most borrowers lock their interest rate once they have an accepted purchase agreement and know their closing timeline. Rate locks typically range from 15 to 60 days, with longer locks sometimes carrying higher rates or fees.

Rate Lock Considerations:

- Lock length should exceed expected closing timeline by 5-10 days

- Shorter locks (21-30 days) often receive better pricing

- Float-down options may be available if rates drop significantly

- Expired locks require extensions, usually at current market rates

In fast-moving Seattle markets, working with lenders who can close quickly reduces rate lock risk and potentially saves money.

Common Mistakes to Avoid

Even well-prepared borrowers sometimes encounter preventable issues that delay or derail mortgage approval. Awareness of common pitfalls helps you navigate the process smoothly.

Financial Changes During the Process

After applying for a mortgage, maintain financial stability and avoid changes that could impact approval:

- Don't change jobs or employment status

- Avoid large purchases on credit

- Don't open new credit accounts

- Maintain account balances (avoid large withdrawals)

- Don't co-sign loans for others

Lenders verify employment and pull updated credit immediately before closing, making any changes during the process potentially problematic.

Documentation Gaps

Incomplete or missing documentation causes the majority of processing delays. Respond to all lender requests within 24 hours when possible, and proactively provide information you know will be needed.

Bidding War Strategies

In competitive situations, particularly in Seattle, Bellevue, and Kirkland, buyers sometimes waive financing contingencies or agree to problematic terms. Understanding how to win bidding wars without taking excessive risk requires guidance from experienced professionals.

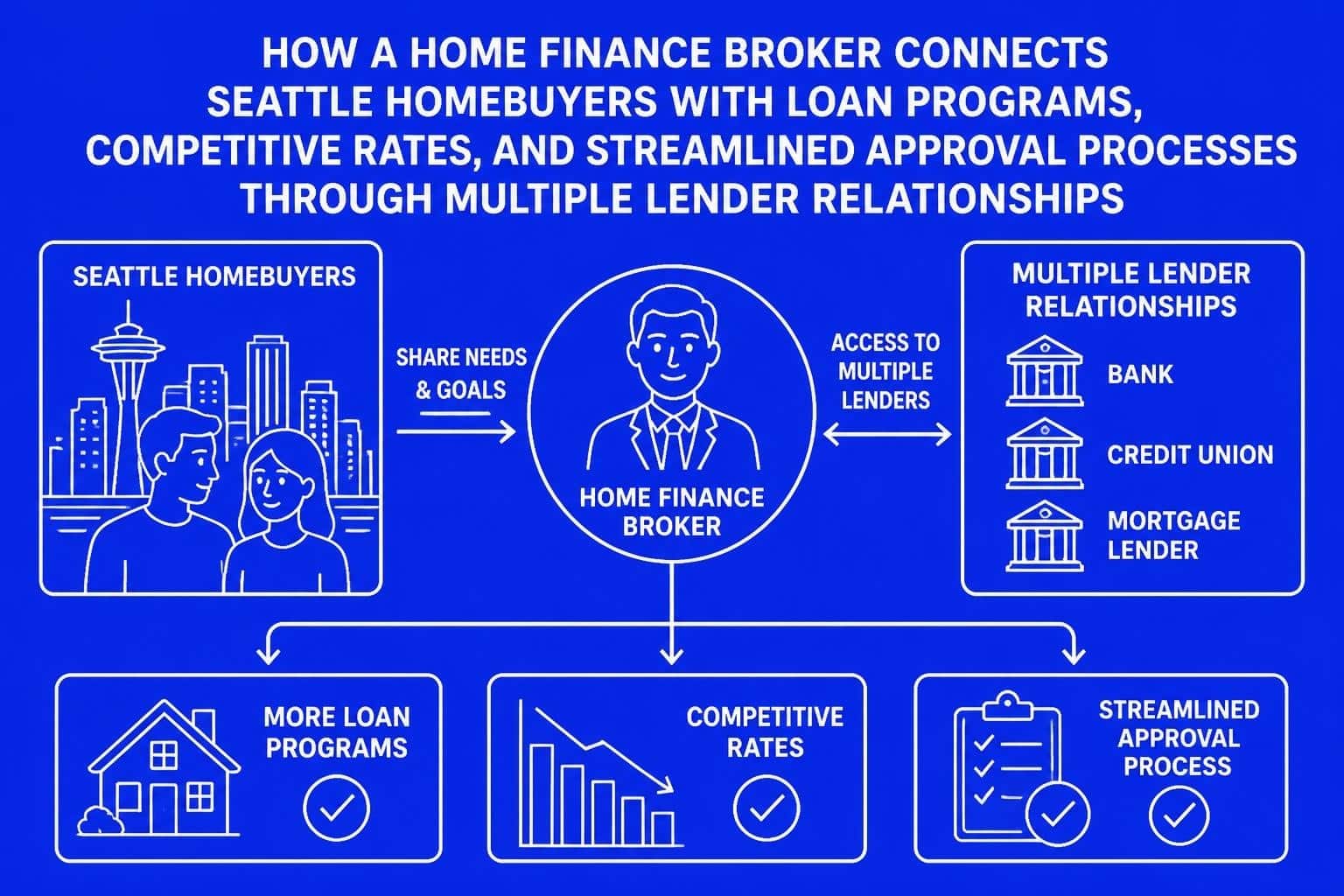

Working with Mortgage Professionals

Choosing between banks, credit unions, and mortgage brokers significantly impacts your experience and outcome. Understanding differences between mortgage brokers and banks helps you make informed decisions.

Benefits of Local Seattle Expertise

Local mortgage professionals understand regional market conditions, property values, and common transaction structures. They maintain relationships with area real estate agents, title companies, and appraisers, facilitating smoother transactions.

Advantages of Local Lenders:

- Knowledge of Seattle-area neighborhoods and property values

- Understanding of competitive offer strategies

- Relationships with local underwriters and processors

- Availability for in-person meetings and property walk-throughs

- Familiarity with area employers and compensation structures

Choosing to work with a local Seattle mortgage broker provides personalized service and market-specific expertise that online lenders cannot match.

Questions to Ask Potential Lenders

Interview multiple lenders before committing to ensure you find the right fit for your situation:

- What interest rates and fees do you offer for my scenario?

- How many days do you need to close the loan?

- What experience do you have with my income type?

- How do you communicate throughout the process?

- Can you provide recent client references?

Comparing multiple loan estimates helps you identify the best combination of rate, fees, and service quality for your specific needs.

Post-Closing Considerations

Your responsibilities continue after closing, and understanding ongoing mortgage management helps you build equity and maintain good standing.

First Payment and Escrow Management

Your first mortgage payment typically occurs 30-45 days after closing. The lender services your loan by collecting payments, managing the escrow account for taxes and insurance, and providing annual statements.

Monitor your escrow account for accuracy, as property tax and insurance changes can trigger payment adjustments. You'll receive an annual escrow analysis showing projected changes.

Mortgage Recasting Opportunities

For Seattle homeowners who receive windfalls like stock option exercises, bonuses, or inheritance, mortgage recasting provides an alternative to refinancing. This strategy lowers your monthly payment without changing your interest rate or loan term.

Understanding when to recast versus refinance helps you optimize your mortgage as circumstances change.

Successfully navigating the mortgage process requires preparation, documentation, and strategic decision-making tailored to your unique financial situation. Whether you're a first-time buyer in Lake Forest Park or a tech professional seeking a jumbo loan in Bellevue, understanding each stage of the process positions you for success in Seattle's competitive market. Keith Akada brings over 25 years of mortgage expertise and 750+ five-star reviews to help you secure the right financing with confidence and clarity. From RSU qualification to fast closings in as few as 9 business days, discover how personalized guidance makes all the difference at Mortgage Reel.