Navigating the Seattle housing market requires strategic planning, especially when it comes to financing your home purchase. For many first-time buyers across Seattle, Shoreline, and Lynnwood, understanding the fha home loan down payment requirements represents a critical first step toward homeownership. The Federal Housing Administration (FHA) loan program offers accessible financing options with lower down payment thresholds compared to conventional mortgages, making it an attractive choice for buyers who may not have substantial cash reserves. Whether you're a tech professional at Amazon or Microsoft, or a growing family in Mill Creek looking to purchase your first home, knowing exactly how much you need to save and what sources are acceptable can significantly impact your buying timeline and budget.

Minimum FHA Home Loan Down Payment Requirements

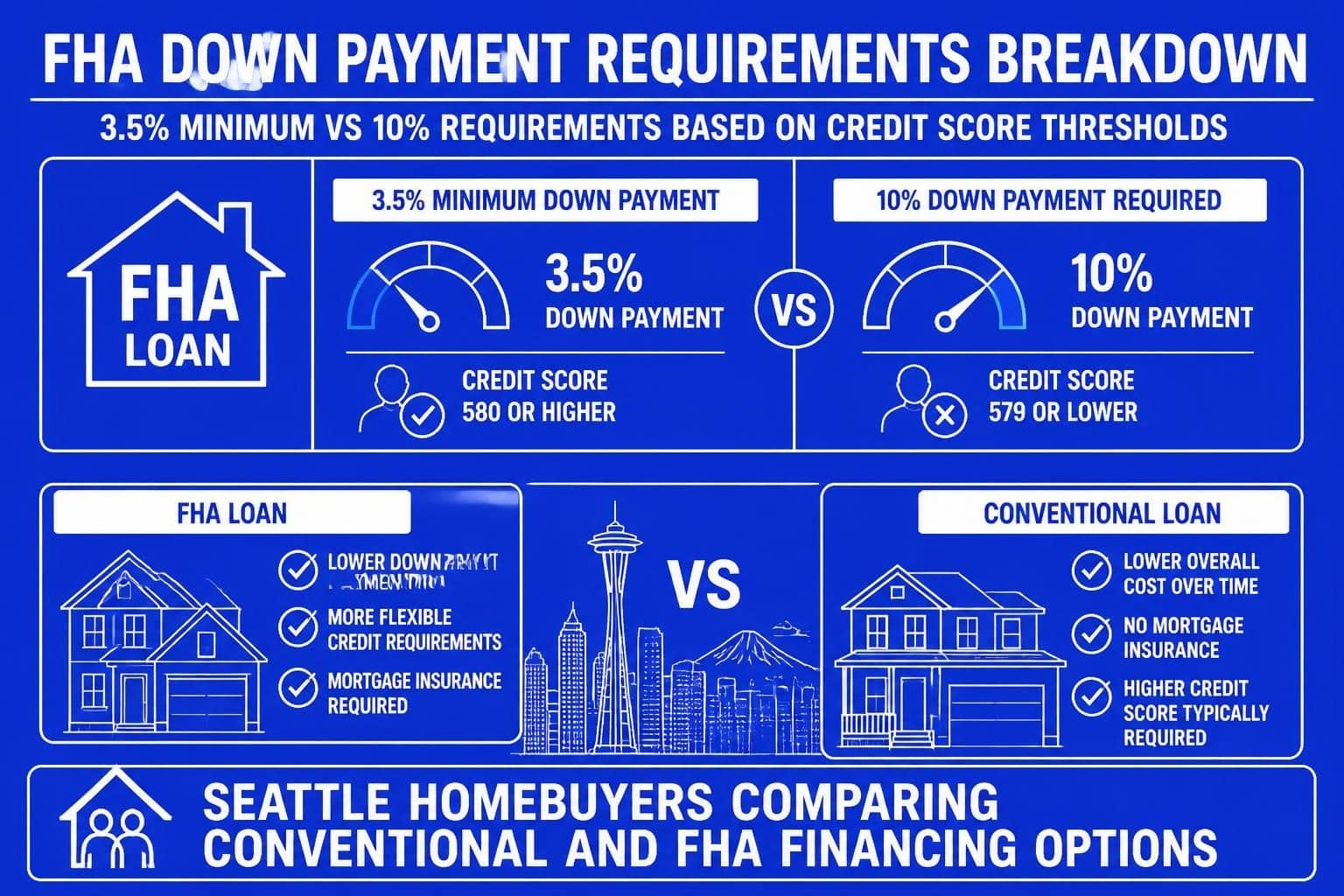

The fha home loan down payment structure operates on a tiered system based primarily on your credit score. This approach allows the FHA to balance accessibility with risk management, creating opportunities for borrowers with varying financial profiles.

Standard 3.5% Down Payment Option

Borrowers with a credit score of 580 or higher qualify for the minimum fha home loan down payment of 3.5% of the purchase price. This represents one of the lowest down payment options available in the mortgage industry today.

For example, on a $600,000 home in Everett, the minimum down payment would be $21,000. Compare this to a conventional loan requiring 20% down, which would demand $120,000 upfront. The difference is substantial and often represents the deciding factor for buyers entering the market.

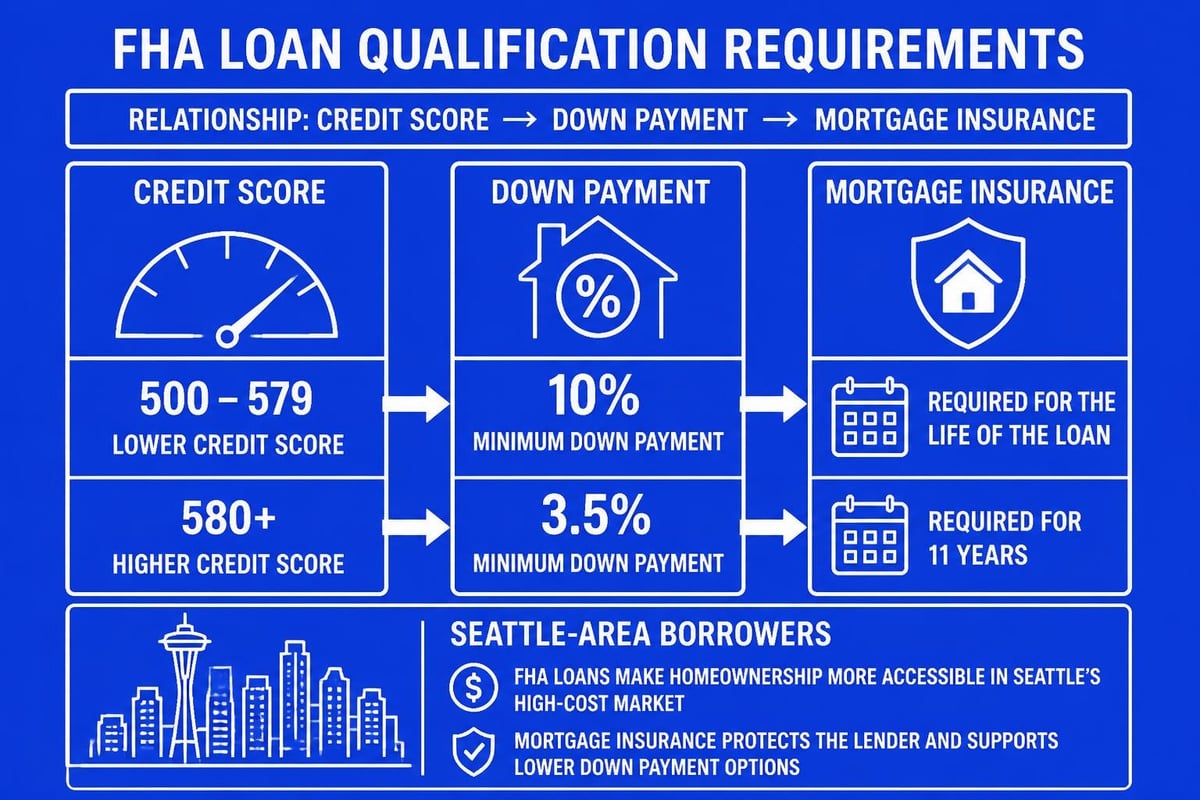

| Credit Score | Minimum Down Payment | Example on $500K Home | Monthly MI Cost (Approx) |

|---|---|---|---|

| 580 or higher | 3.5% | $17,500 | $350-450 |

| 500-579 | 10% | $50,000 | $350-450 |

| Below 500 | Not eligible | N/A | N/A |

The 10% Down Payment Requirement

Borrowers with credit scores between 500 and 579 face a higher fha home loan down payment requirement of 10% of the purchase price. While this threshold is significantly higher than the 3.5% option, it still provides access to homeownership for individuals working to rebuild or establish credit.

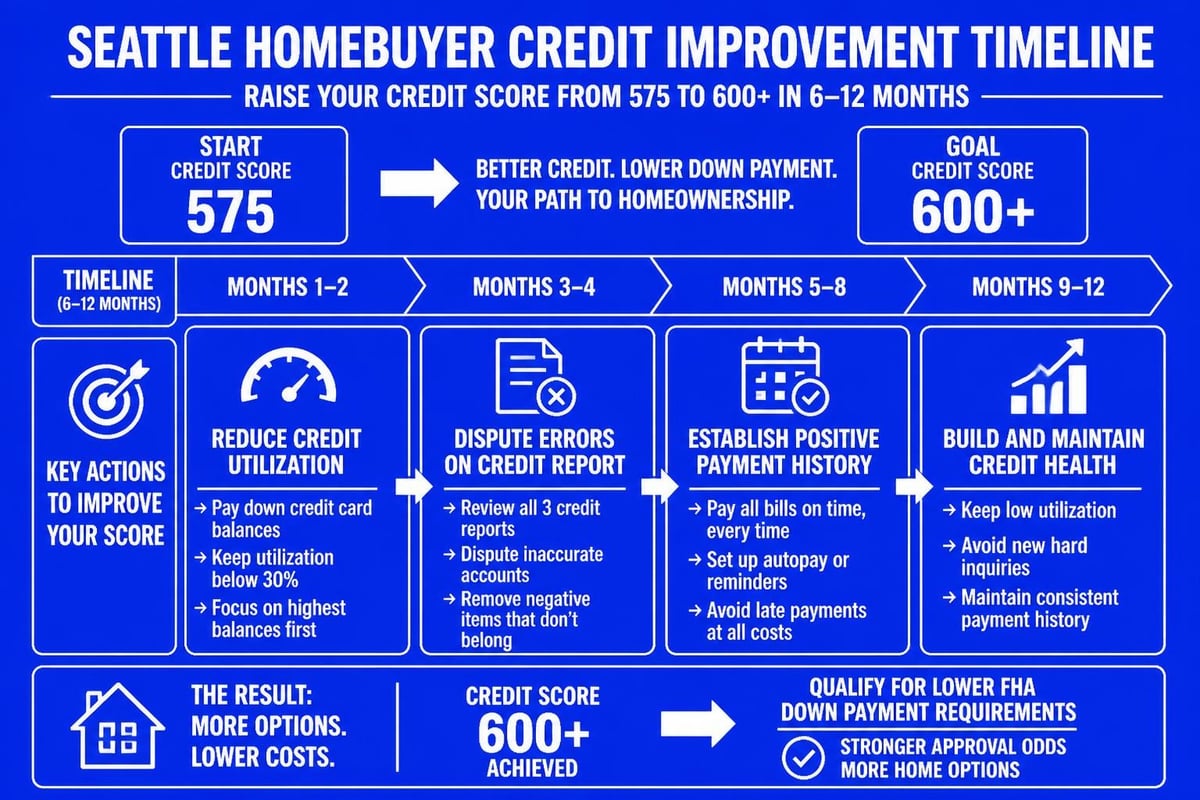

In the competitive Seattle market, buyers in this credit range should focus on improving their scores before applying. Even a modest improvement from 575 to 580 can save tens of thousands of dollars in upfront costs. Working with a trusted Seattle mortgage broker can help you develop a strategic timeline for credit improvement and purchase readiness.

Acceptable Sources for Your FHA Down Payment

Understanding where your fha home loan down payment funds can originate is essential for proper planning. The FHA maintains specific guidelines to ensure down payments come from legitimate sources and that borrowers aren't taking on excessive debt to complete their purchase.

Personal Savings and Verified Assets

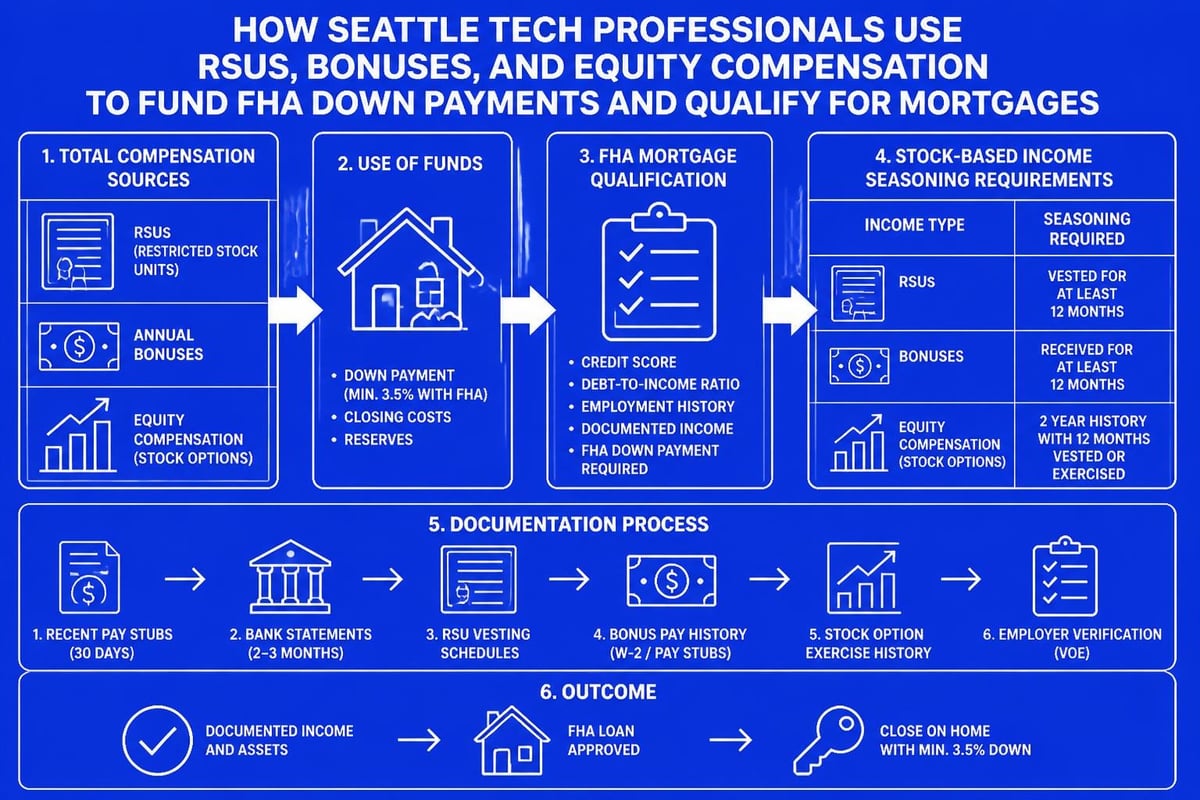

Your own savings accounts, checking accounts, certificates of deposit, and retirement accounts represent the most straightforward sources. Lenders require seasoned funds, typically meaning the money has been in your account for at least 60 days before application. For Seattle tech professionals with substantial RSU compensation, recently vested stock can be sold and used once properly documented and seasoned.

Gift Funds from Family Members

Gift funds represent a popular and fully acceptable source for your fha home loan down payment. Family members, including parents, siblings, grandparents, or even your fiancé, can provide gift money without repayment expectation.

The process requires:

- A signed gift letter stating the amount, relationship, and confirmation that no repayment is expected

- Documentation showing the transfer of funds from the donor's account to yours

- Bank statements proving the donor had sufficient funds available

In Lake Forest Park and surrounding communities, many multigenerational families utilize this option to help younger members enter homeownership. According to FHA down payment guidance from Chase, proper documentation is critical to ensure smooth underwriting.

Down Payment Assistance Programs

Washington State offers several down payment assistance programs that pair effectively with FHA financing. The Chenoa Fund provides eligible FHA borrowers with second-lien financing to cover down payment and closing costs, which can be particularly valuable for buyers in higher-priced markets like Bellevue and Redmond.

State and local programs often provide:

- Forgivable loans that disappear after you occupy the home for a specified period

- Low-interest second mortgages

- Matching funds programs

- Grants for specific occupations (teachers, first responders, healthcare workers)

How Credit Scores Impact Your Down Payment

Your credit score plays a dual role in FHA financing, affecting both the minimum fha home loan down payment percentage and your overall loan costs through interest rates and mortgage insurance premiums.

Credit Score Optimization Strategies

Before applying for an FHA loan in Seattle or Shoreline, consider these credit-building approaches:

- Pay down revolving credit balances to below 30% of available limits

- Dispute any inaccuracies on your credit reports across all three bureaus

- Avoid opening new credit accounts within six months of your planned purchase

- Make all payments on time for at least 12 months prior to application

- Become an authorized user on a family member's well-managed credit card

Even a 20-point improvement can make a significant difference. A borrower moving from a 575 to a 595 credit score not only qualifies for the 3.5% down payment option but may also secure a better interest rate, saving thousands over the loan's lifetime.

Understanding Experian’s FHA loan requirements can help you benchmark your current position and set realistic improvement goals.

Mortgage Insurance and Total Investment Calculations

While the low fha home loan down payment threshold attracts many buyers, understanding the complete financial picture requires examining mortgage insurance costs.

Upfront and Monthly Mortgage Insurance Premiums

FHA loans require two types of mortgage insurance:

Upfront Mortgage Insurance Premium (UFMIP): Currently 1.75% of the loan amount, typically financed into the loan rather than paid in cash at closing.

Annual Mortgage Insurance Premium (MIP): Ranges from 0.45% to 1.05% of the loan amount annually, divided into monthly payments. The rate depends on your loan term, loan-to-value ratio, and loan amount.

| Down Payment | Loan Term | Base Loan Amount | Annual MIP Rate | Monthly MIP |

|---|---|---|---|---|

| 3.5% | 30 years | ? $726,200 | 0.55% | Varies by loan |

| 3.5% | 30 years | > $726,200 | 0.75% | Varies by loan |

| 10% | 30 years | Any amount | 0.50% | Varies by loan |

For borrowers putting down less than 10%, mortgage insurance remains for the life of the loan. Those contributing 10% or more can have it removed after 11 years. This represents a significant long-term cost consideration when evaluating whether to save additional funds before purchasing.

FHA vs Conventional Down Payment Comparison

Seattle buyers often wonder whether an FHA loan or conventional loan with 5% down makes more financial sense for their situation.

When FHA Makes Strategic Sense

FHA loans excel for borrowers with:

- Credit scores between 580-680

- Limited savings beyond the minimum down payment

- Higher debt-to-income ratios (up to 50% in some cases)

- Recent credit events (bankruptcy, foreclosure) with appropriate waiting periods

- Self-employment income with shorter history

When Conventional Becomes More Attractive

Conventional financing often wins for borrowers with:

- Credit scores above 720

- Down payment capacity of 10% or higher

- Lower debt-to-income ratios (below 43%)

- Desire to avoid lifetime mortgage insurance

- Purchase prices exceeding FHA loan limits

The 2026 down payment guide for Seattle homebuyers provides detailed scenarios comparing total costs across loan types for various price points and borrower profiles.

FHA Loan Limits in the Seattle Metro Area

The fha home loan down payment percentage applies to the base loan amount, which cannot exceed FHA loan limits established annually for each county. For 2026, King County (including Seattle, Bellevue, Redmond, and Kirkland) has an FHA loan limit of $1,209,750 for single-family homes.

Snohomish County (covering Everett, Lynnwood, Mill Creek, and Shoreline) maintains the same limit. These elevated limits reflect the high-cost nature of the Seattle metropolitan housing market, allowing FHA financing on homes well above the national average price.

Calculating Maximum Purchase Price

To determine the maximum home price you can purchase with an FHA loan:

With 3.5% down: Divide the loan limit by 0.965 (since you're financing 96.5% of the purchase price)

- $1,209,750 ÷ 0.965 = $1,253,626 maximum purchase price

With 10% down: Divide the loan limit by 0.90

- $1,209,750 ÷ 0.90 = $1,344,167 maximum purchase price

These calculations demonstrate how your fha home loan down payment percentage directly impacts your maximum buying power within FHA program guidelines.

Closing Costs Beyond Your Down Payment

First-time buyers often focus exclusively on the down payment while underestimating additional cash requirements at closing. Zillow’s FHA loan down payment overview emphasizes the importance of budgeting for total out-of-pocket expenses.

Typical Closing Cost Components

Beyond your fha home loan down payment, expect to pay:

- Origination fees: 0.5% to 1% of loan amount

- Appraisal fee: $500-$700 in Seattle area

- Credit report: $30-$100

- Title insurance: Varies by purchase price, often $1,500-$3,000

- Escrow deposits: 2-3 months of property taxes and insurance

- Recording fees: $200-$400

- Home inspection: $400-$600 (optional but recommended)

Total closing costs typically range from 3% to 5% of the purchase price in the Seattle market. On a $500,000 home, budget $15,000-$25,000 for closing costs in addition to your down payment.

Many buyers wonder if they can finance these costs. While the upfront mortgage insurance premium can be financed, most other closing costs require cash payment. However, sellers can contribute up to 6% of the purchase price toward your closing costs under FHA guidelines, significantly more generous than conventional loans.

Special Considerations for Seattle-Area Tech Professionals

Microsoft, Amazon, Google, and other major Seattle employers compensate professionals through complex structures including base salary, bonuses, and equity compensation. Qualifying this income for your fha home loan down payment calculation and overall approval requires specialized expertise.

Using RSUs and Stock Compensation

Restricted Stock Units (RSUs) can fund your down payment once vested and sold, though timing matters. Lenders typically require:

- Two years of RSU history if using for income qualification

- Immediate availability if using vested shares for down payment funds

- Documentation of vesting schedules and historical patterns

- Proper seasoning of proceeds after sale (60 days in account)

Many tech professionals discover they have more buying power than anticipated when working with lenders experienced in qualifying complex compensation structures. While jumbo loans often make more sense for higher earners, FHA financing can still serve strategic purposes, particularly for investment properties (though FHA requires owner occupancy for primary financing).

Preparing Your Down Payment Documentation

Proper documentation separates smooth closings from delayed frustrations. Lenders scrutinize down payment sources carefully to ensure compliance with FHA guidelines and anti-fraud regulations.

Required Documentation Checklist

For personal savings:

- Two months of bank statements showing consistent balances

- Explanation letters for any large deposits over $1,000

- Paper trail for transferred funds between your own accounts

For gift funds:

- Signed gift letter with donor information and relationship

- Donor's bank statement showing withdrawal

- Your bank statement showing deposit

- Wire transfer confirmation or canceled check

For retirement account withdrawals:

- Distribution request and approval

- Documentation showing funds deposited into checking/savings

- Penalty and tax withholding calculations

For sale of assets:

- Sale documentation (vehicle title, investment statements)

- Receipt showing funds received

- Deposit confirmation into your account

Understanding home loan approval timelines helps you prepare documentation early, avoiding last-minute scrambles that could jeopardize your closing date.

FHA Down Payment Strategies for Different Buyer Profiles

Your optimal fha home loan down payment approach depends on your specific financial situation, goals, and market position.

Strategy for Limited Savings

If you've saved exactly the 3.5% minimum:

- Request maximum seller concessions (6% toward closing costs)

- Explore down payment assistance programs

- Consider asking family for gift funds to cover closing costs

- Budget carefully for post-closing reserves and moving expenses

- Ensure you qualify comfortably to avoid payment shock

Strategy for Moderate Savings (5-9% Available)

If you have more than the minimum but less than 10%:

- Evaluate conventional financing with 5% down if your credit score exceeds 680

- Consider putting 3.5% down and keeping reserves for home improvements

- Assess whether waiting to save to 10% makes sense (removes MI after 11 years)

- Calculate break-even points between FHA and conventional options

- Factor in potential property upgrades, especially if working with renovation specialists like Kreeative Renovations & Design Co. to customize your new home

Strategy for Substantial Savings (10%+ Available)

If you can put down 10% or more:

- Seriously consider conventional financing to avoid lifetime mortgage insurance

- Evaluate the 10% FHA option if credit challenges exist

- Model long-term costs comparing FHA vs conventional

- Consider saving additional funds for the conventional 15% or 20% threshold

- Explore jumbo loan options if purchasing above FHA limits

Market Timing and Down Payment Readiness

The Seattle housing market experiences seasonal fluctuations and cyclical trends that can impact your down payment strategy and overall purchasing power.

Seasonal Market Considerations

Spring/Summer (Peak Season):

- Higher competition may require stronger offers

- Multiple offer situations favor larger down payments

- Consider conventional over FHA if competing with cash buyers

- Be prepared to waive financing contingencies only with pre-approval confidence

Fall/Winter (Slower Season):

- More negotiating leverage on price and terms

- Sellers more willing to accept FHA financing and offer concessions

- Potentially lower prices offset any seasonal rate variations

- Fewer competing buyers means your fha home loan down payment strategy faces less scrutiny

Understanding how to work effectively with a Seattle mortgage broker throughout the year ensures you're positioned to act when the right property appears, regardless of season.

Converting Your Down Payment Plan Into Action

Once you understand the fha home loan down payment requirements and have calculated your specific needs, implementation requires systematic execution.

Six-Month Action Timeline

Month 1-2: Financial Assessment

- Pull credit reports from all three bureaus

- Calculate current savings and monthly surplus

- Identify down payment funding sources

- Create dedicated savings account for down payment

Month 3-4: Credit Optimization

- Address credit report errors

- Pay down high-balance credit cards

- Avoid new credit applications

- Establish automated savings transfers

Month 5-6: Pre-Approval and Home Search

- Complete pre-approval with experienced lender

- Begin working with real estate agent

- Tour homes within approved price range

- Finalize down payment source documentation

This timeline assumes you're starting with reasonable credit and some savings. Buyers with significant credit challenges or minimal savings may need 12-18 months of preparation before achieving purchase readiness.

Investment vs Primary Residence Considerations

While FHA loans require owner occupancy as your primary residence, understanding how this impacts your long-term real estate strategy matters for Seattle-area buyers planning to build wealth through property ownership.

The FHA Owner Occupancy Requirement

You must:

- Occupy the property as your primary residence within 60 days of closing

- Maintain it as your primary residence for at least 12 months

- Certify your intent to occupy at closing

After the 12-month period, you can convert the property to a rental while maintaining the FHA loan. This creates a potential house-hacking or investment strategy where your low fha home loan down payment enables property accumulation over time.

Many Seattle professionals purchase a home in Mill Creek or Lake Forest Park with FHA financing, live there for the required period, then purchase a larger home with conventional financing while retaining the first property as a rental with favorable FHA terms locked in place.

Regional Market Variations Within Greater Seattle

While FHA guidelines remain consistent, local market dynamics in different Seattle-area cities affect how your down payment performs competitively.

Seattle and Bellevue

In the most competitive neighborhoods, sellers and listing agents sometimes resist FHA offers due to perceived complexity or delays. A larger fha home loan down payment (closer to 10% even if you qualify for 3.5%) can strengthen your position. Alternatively, strong pre-approval documentation and lender reputation matter significantly.

Shoreline and Lake Forest Park

These family-oriented communities often feature more FHA-friendly sellers, particularly for starter homes and condominiums. Your minimum 3.5% down payment typically competes effectively, especially when paired with seller concessions that reduce your total cash outlay.

Everett and Lynnwood

These markets offer more affordable entry points where FHA financing represents a significant portion of transactions. Sellers expect and accommodate FHA buyers, making your standard 3.5% down payment perfectly competitive without additional positioning required.

Understanding these nuances helps you strategically deploy your available funds based on where you're searching and how competitive you need to be.

Common FHA Down Payment Mistakes to Avoid

Even with proper planning, buyers sometimes stumble on preventable errors that delay or derail their FHA loan approval.

Critical Mistakes and Prevention

Large unexplained deposits: Any deposit exceeding $1,000 requires documentation. Avoid cash deposits or unclear transfers during the 60 days before application and throughout your loan process.

Commingling gift funds: Keep gift money separate from your personal funds until after documentation is complete. Deposit the gift directly into the account you'll use for closing.

Last-minute credit changes: Opening new accounts, making large purchases, or changing jobs after pre-approval can invalidate your approval. Maintain financial status quo from application through closing.

Insufficient reserves: FHA doesn't always require reserves beyond your down payment, but having 2-3 months of mortgage payments saved demonstrates financial stability and prevents post-purchase stress.

Ignoring closing cost needs: Focusing solely on the down payment while neglecting the additional 3-5% needed for closing costs creates last-minute funding crises.

Working with experienced professionals who specialize in first-time homebuyers helps you navigate these potential pitfalls before they become problems.

Understanding your fha home loan down payment requirements represents just the first step toward successful homeownership in the Seattle area. The right financing strategy considers your complete financial profile, local market conditions, and long-term wealth-building goals. Whether you're a tech professional in Redmond leveraging RSU compensation, a growing family in Shoreline pursuing your first home, or an experienced buyer in Everett optimizing your purchasing power, working with Keith Akada and the team at Mortgage Reel ensures you receive expert guidance backed by 25+ years of experience, 750+ five-star reviews, and the ability to close in as few as 9 business days in Seattle's competitive market.