Understanding mortgage advisor rates is essential for anyone navigating the Seattle housing market in 2026. Whether you're a first-time homebuyer in Shoreline, a tech professional relocating to Bellevue, or a homeowner in Lynnwood considering a refinance, knowing what to expect in terms of advisor compensation helps you make confident financial decisions. Mortgage advisor rates vary based on loan type, lender structure, and market conditions, but transparency in pricing has never been more important as buyers face competitive inventory and rising home values across the Greater Seattle area.

How Mortgage Advisor Compensation Works

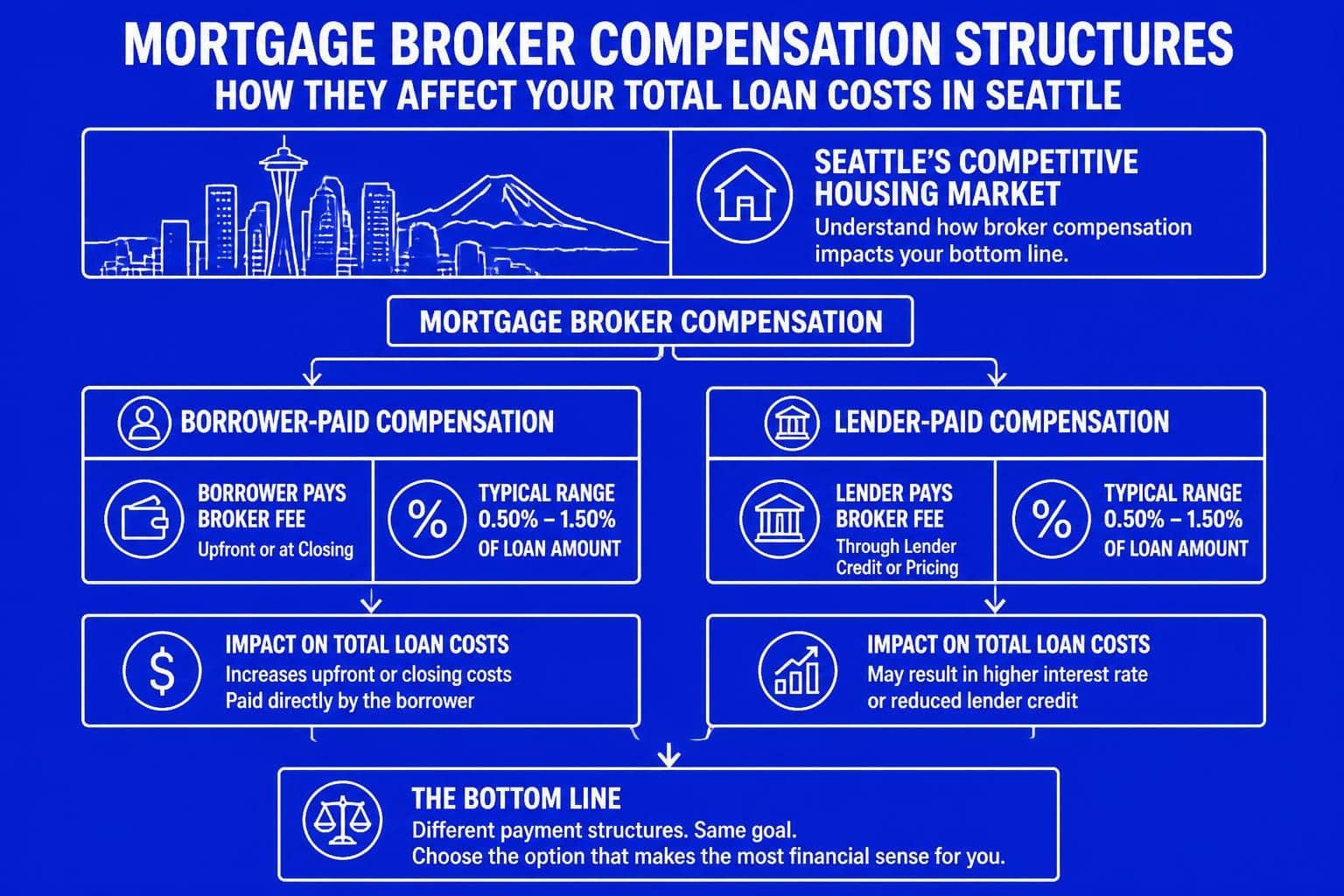

Mortgage advisors, also known as mortgage brokers or loan officers, are compensated through several different structures. Understanding these models helps you evaluate the true cost of your home loan.

Lender-paid compensation represents the most common model in 2026. In this structure, the lender pays the mortgage advisor a percentage of the loan amount, typically ranging from 0.50% to 2.75%. This compensation comes from the lender's revenue, not as a separate charge to the borrower. For a $750,000 home purchase in Redmond, this might represent $3,750 to $20,625 in advisor compensation, though you won't see this as a line item on your loan estimate.

Borrower-paid origination fees offer another compensation method. Some advisors charge origination fees directly to borrowers, typically 0.5% to 1% of the loan amount. This approach provides transparency, as the fee appears clearly on your closing disclosure. A $600,000 loan in Kirkland might carry a $3,000 to $6,000 origination fee.

Fee Transparency Requirements

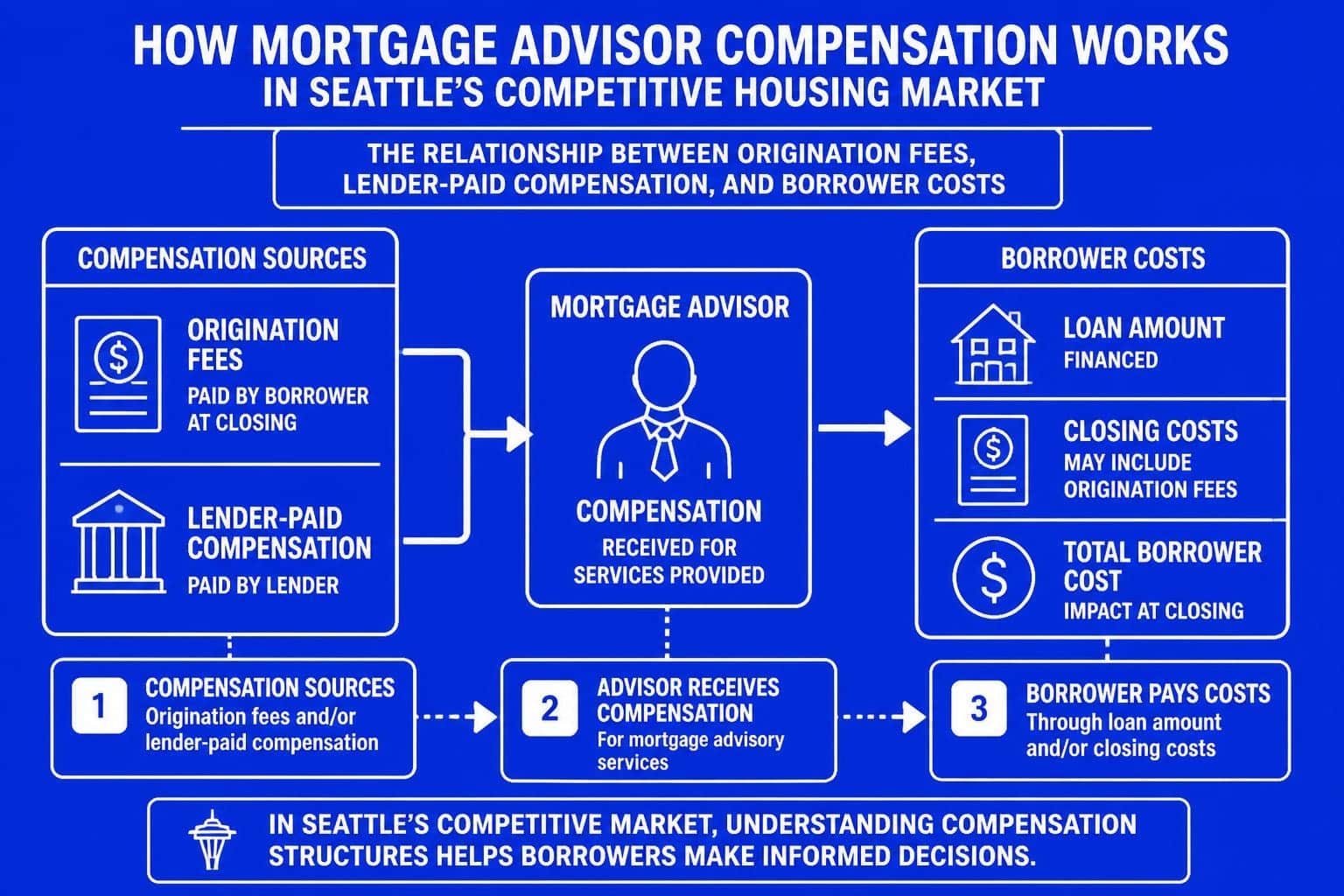

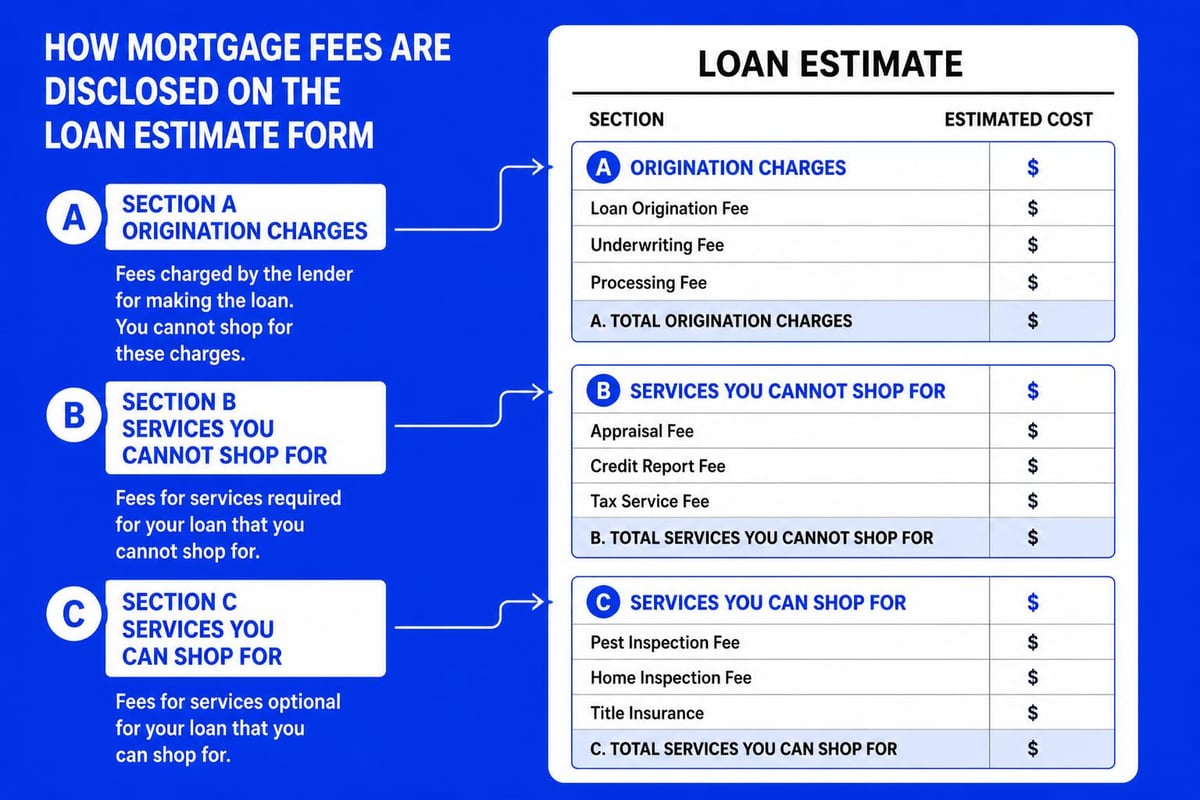

Federal regulations require mortgage advisors to disclose all compensation within three business days of your application. The Loan Estimate form breaks down every cost associated with your mortgage, including origination charges, discount points, and third-party fees.

Key disclosure requirements include:

- Itemization of all fees within Section A of the Loan Estimate

- Lender credits that may offset borrower costs

- Rate lock confirmation showing how long your quoted rate remains valid

- Total loan costs combining origination and other charges

Working with a trusted Seattle mortgage broker ensures you receive clear explanations of every fee before you commit to a loan program.

Typical Mortgage Advisor Rates in 2026

The mortgage industry has evolved significantly, with increased competition leading to more favorable pricing for borrowers across Seattle and surrounding communities.

| Compensation Type | Typical Range | Who Pays | Seattle Example ($700K Loan) |

|---|---|---|---|

| Lender-Paid | 0.50% – 2.75% | Lender | $3,500 – $19,250 |

| Origination Fee | 0.5% – 1.0% | Borrower | $3,500 – $7,000 |

| Flat Fee | $2,000 – $5,000 | Borrower | $2,000 – $5,000 |

| Hybrid Model | Varies | Split | $4,000 – $10,000 |

Understanding mortgage broker costs helps you compare options effectively. In competitive markets like Mill Creek and Lake Forest Park, advisors often adjust their compensation to win business while maintaining service quality.

Regional Variations in the Seattle Market

Mortgage advisor rates can vary based on property location, even within the Greater Seattle area. High-value markets like downtown Seattle or waterfront properties in Everett may see different pricing structures than suburban neighborhoods in Lynnwood.

Premium property considerations include higher loan amounts requiring jumbo financing, complex income verification for stock-based compensation common among Amazon and Microsoft employees, and investment properties with unique underwriting requirements.

For tech professionals with RSUs, stock options, or bonus income, specialized expertise in jumbo home loans justifies working with advisors who understand these compensation structures, even if their rates fall toward the higher end of typical ranges.

Factors Influencing Mortgage Advisor Rates

Multiple variables affect what you'll pay for mortgage advisory services in 2026. Understanding these factors helps you evaluate whether quoted rates represent fair market value.

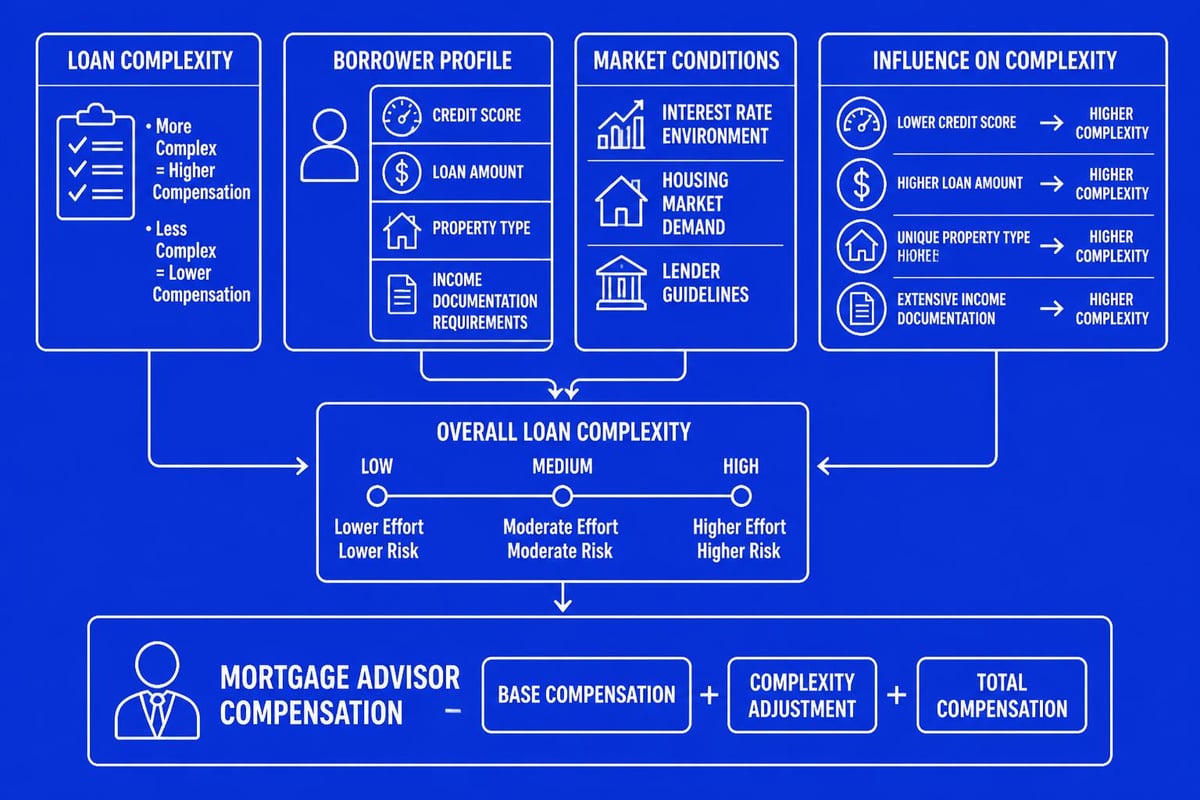

Loan complexity significantly impacts pricing. A straightforward conventional loan with W-2 income, strong credit, and 20% down requires less advisor time than a scenario involving self-employment income, multiple properties, or recent credit events. First-time buyers in Shoreline using down payment assistance programs may work with advisors charging different rates than investors purchasing rental properties.

Loan amount directly correlates with compensation in percentage-based models. A $400,000 purchase generates less advisor compensation than a $1.2 million jumbo loan, though the work involved may differ only marginally.

Market Competition and Pricing

Seattle's competitive lending environment in 2026 benefits borrowers through several mechanisms:

- Online lenders offering reduced origination fees

- Credit unions providing member-focused pricing

- Bank loan officers with relationship-based discounts

- Independent brokers accessing multiple lender channels

This competition drives mortgage broker pricing toward borrower-friendly levels while maintaining service standards. Advisors differentiate themselves through expertise, responsiveness, and proven track records rather than just price.

Lender relationships also influence rates. Advisors with strong lending partner networks can often negotiate better pricing, especially for borrowers with excellent credit profiles or significant assets. Someone purchasing in Bellevue with a 780 credit score and 30% down payment might receive more favorable terms than standard rate sheets suggest.

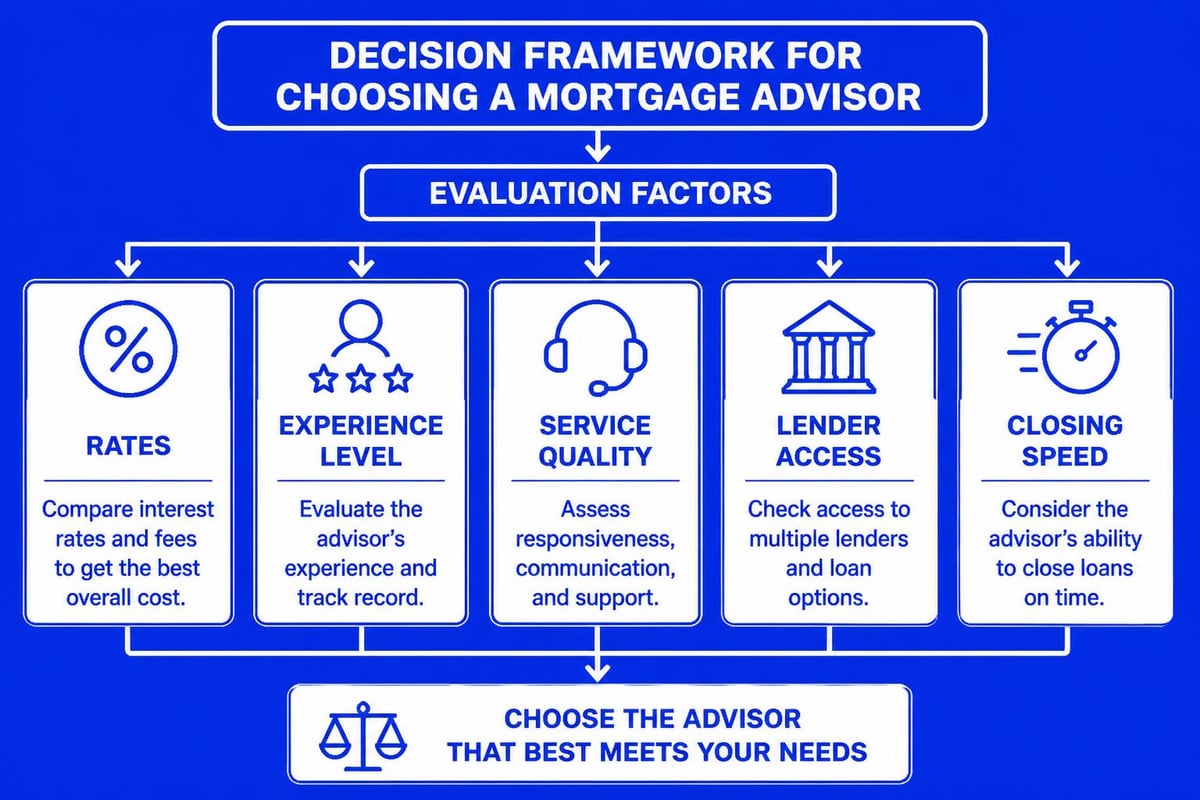

Comparing Advisor Options in Seattle

Evaluating mortgage advisors requires looking beyond quoted rates to assess total value, service quality, and market expertise specific to Greater Seattle communities.

Direct Lender vs. Mortgage Broker

Understanding the distinction between working directly with a bank and using an independent mortgage broker affects both your rate options and service experience.

Direct lenders employ loan officers who originate mortgages exclusively for their institution. These advisors access one set of loan products, underwriting guidelines, and pricing. Benefits include streamlined communication and potential relationship discounts. Limitations involve reduced product variety and potentially less competitive pricing.

Mortgage brokers work with multiple lenders, accessing diverse loan programs and competitive pricing across institutions. This model particularly benefits borrowers with unique situations, such as tech professionals with stock compensation or buyers seeking conventional loans with 5% down. Brokers can compare options and select the best combination of rate, fees, and terms for your specific scenario.

Quality brokers bring additional value through:

- Market expertise in Seattle neighborhoods and property types

- Lender negotiation leveraging volume relationships

- Problem-solving ability for complex income or credit situations

- Process management coordinating with sellers, agents, and title companies

Working with experienced Seattle mortgage advisors who maintain 750+ five-star reviews demonstrates consistent service delivery that justifies fair compensation.

Hidden Costs Beyond Advisor Rates

Mortgage advisor rates represent only one component of your total home financing costs. Comprehensive evaluation requires understanding the full fee structure.

Third-party fees include appraisal costs ($600-$1,200 in Seattle), title insurance ($1,500-$3,500), credit reports ($30-$100), and various government recording charges. These costs remain relatively consistent regardless of which advisor you select.

Rate buydown costs allow borrowers to reduce interest rates through discount points. Each point costs 1% of the loan amount and typically reduces your rate by 0.125% to 0.250%. On a $650,000 loan in Everett, purchasing two points might cost $13,000 but reduce your rate from 6.75% to 6.375%, saving approximately $175 monthly.

Evaluating Total Loan Costs

Smart borrowers analyze upfront fees and long-term costs together when comparing advisor options. A slightly higher origination fee paired with a lower interest rate often provides better value than minimal upfront costs with a higher rate.

Consider this comparison for a $700,000 30-year fixed mortgage:

| Option | Origination Fee | Interest Rate | Monthly Payment | Total Interest (30 Years) |

|---|---|---|---|---|

| A | $0 | 6.875% | $4,604 | $957,440 |

| B | $3,500 | 6.625% | $4,488 | $915,680 |

| C | $7,000 | 6.375% | $4,373 | $874,280 |

Option C costs $7,000 more upfront but saves $83,160 in interest over the loan term compared to Option A. For buyers planning to remain in Lake Forest Park or Mill Creek properties long-term, this represents substantial savings that dwarf the higher advisor rate.

Questions to Ask About Advisor Rates

Informed borrowers ask specific questions that reveal true costs and service value. These conversations help you select the right mortgage advisor for your Seattle-area home purchase or refinance.

What is your total compensation on this loan? This direct question requires a straightforward answer. Advisors should clearly explain whether they receive lender-paid compensation, borrower-paid fees, or a combination, along with approximate percentages or dollar amounts.

Can you provide multiple loan options with different fee structures? Quality advisors present scenarios allowing you to choose between paying points for lower rates, accepting higher rates with lender credits, or finding middle-ground solutions. This flexibility demonstrates they're working in your interest rather than maximizing their compensation.

Service Value Questions

Beyond rates, evaluate the advisor's expertise and support structure:

- How quickly can you close this loan in Seattle's competitive market?

- What experience do you have with stock-based compensation for tech employees?

- How many loans have you closed in my target neighborhood?

- What is your availability for questions throughout the process?

Advisors who consistently approve loans quickly and close in as few as 9 business days provide tangible value in competitive bidding situations, potentially making the difference between winning and losing your desired property in Redmond or Kirkland.

Regional Considerations for Seattle Homebuyers

Seattle's unique housing market characteristics influence both mortgage advisor selection and rate structures. Understanding these local factors helps you make informed decisions.

High home values across Seattle, Bellevue, and surrounding communities frequently require jumbo financing. Conventional loan limits for 2026 stand at $806,500 for single-family homes in King County, meaning many Seattle-area purchases exceed this threshold. Advisors specializing in jumbo home mortgages bring specific expertise worth considering, even if their rates don't represent the absolute lowest option.

Tech industry employment creates unique income documentation scenarios. Amazon, Microsoft, and Google employees often receive significant compensation through RSUs, which require specialized underwriting knowledge. Advisors experienced in qualifying stock-based income understand how underwriters evaluate vesting schedules, grant documents, and historical stock performance when calculating debt-to-income ratios.

Neighborhood-Specific Market Knowledge

Advisors familiar with specific Seattle neighborhoods provide value through local expertise. Understanding condominium approval status in downtown Seattle high-rises, working with co-op financing in certain buildings, or navigating unique title issues in older Everett properties requires specific knowledge that generic advisors may lack.

First-time homebuyers in Seattle benefit from advisors who understand state and local assistance programs, including the Washington State Housing Finance Commission options, down payment assistance through Seattle's Office of Housing, and special programs for educators, healthcare workers, and other essential service providers.

Rate Negotiation Strategies

While mortgage advisor rates follow industry norms, negotiation opportunities exist, especially for borrowers with strong financial profiles or those bringing significant business potential.

Strong applicant leverage includes excellent credit scores above 760, substantial down payments exceeding 20%, significant liquid reserves, and stable employment history. These factors reduce lender risk and may allow advisors to reduce their compensation while maintaining profitability through volume.

Multiple quote comparison remains your strongest negotiation tool. When advisors know you're evaluating competitive options from quality mortgage lenders, they're more likely to offer their best pricing upfront rather than testing higher rates.

When to Focus Beyond Price

Certain scenarios justify accepting higher mortgage advisor rates in exchange for specialized expertise or superior service:

- Complex income situations requiring creative underwriting solutions

- Tight closing timelines in competitive Seattle markets

- Unique property types including investment properties or non-standard construction

- Credit challenges requiring manual underwriting and lender negotiation

An advisor charging 1% origination versus 0.5% may deliver $10,000 in additional value by structuring your loan to qualify for a property you otherwise couldn't purchase or by closing quickly enough to beat out competing offers in Lynnwood's seller's market.

Value-Based Advisor Selection

The lowest mortgage advisor rates don't always deliver the best outcome. Evaluating total value requires considering expertise, service quality, and long-term relationship potential.

Educational approach distinguishes exceptional advisors. Those who invest time explaining home buying strategies, comparing loan programs thoughtfully, and helping you understand both immediate and long-term implications of financing decisions provide value beyond transaction completion.

Proactive communication prevents delays and stress throughout the mortgage process. Advisors who respond quickly, anticipate potential issues, and keep all parties informed create smoother transactions worth paying fair compensation to secure.

Long-Term Relationship Value

The right mortgage advisor becomes a valuable resource for future refinancing, home equity lending, and investment property purchases. Establishing a relationship with a great mortgage broker who understands your financial situation and goals provides ongoing value as your needs evolve.

Seattle homeowners who refinanced multiple times between 2020 and 2023 as rates declined found that working with the same trusted advisor streamlined each subsequent transaction. That advisor's knowledge of your income documentation, credit profile, and property already existed in their files, accelerating approvals and closings while ensuring competitive pricing based on an established relationship.

Technology and Rate Transparency

Digital tools have transformed mortgage shopping, providing borrowers unprecedented access to rate information and fee comparisons. Understanding how to use these resources effectively maximizes your negotiating position.

Online rate aggregators display daily rate averages from multiple lenders, though these quotes often represent best-case scenarios for borrowers with excellent credit and specific loan parameters. Use these tools to understand general market trends rather than expecting to match advertised rates exactly.

Direct lender platforms allow you to input detailed financial information and receive personalized quotes, including all fees. These systems provide more accurate pricing than generic rate advertisements but still require careful reading of disclosure documents.

Balancing Technology with Personal Service

While technology improves price transparency, human expertise remains invaluable for complex scenarios common in Seattle's market. Self-service platforms work well for straightforward conventional loans with W-2 income and standard down payments. They struggle with RSU qualification, multi-property portfolio lending, or unique credit situations requiring manual underwriting.

The optimal approach combines digital research with expert guidance. Use online tools to understand current mortgage rates and broker fees, then consult experienced advisors who can apply that market knowledge to your specific circumstances while adding value through personalized strategy and execution.

Future Trends in Advisor Compensation

The mortgage industry continues evolving, with several trends likely to influence advisor rates throughout 2026 and beyond.

Increased competition from online lenders and automated platforms puts downward pressure on traditional origination fees. However, complex transactions requiring human expertise maintain premium pricing, creating a two-tiered market where simple refinances cost less than jumbo purchases with stock-based income qualification.

Regulatory changes may impact how advisors disclose compensation and structure fees. Ongoing discussions about fee transparency and borrower protection could standardize certain pricing elements while maintaining competitive markets.

Technology Integration

Advisors who effectively integrate technology into their processes deliver better value at competitive prices. Automated document collection, digital income verification, and electronic closing capabilities reduce processing time and costs, allowing advisors to maintain service quality while offering competitive mortgage advisor rates.

Borrowers benefit by selecting advisors who combine technological efficiency with personal expertise, particularly valuable in Seattle's fast-moving market where the ability to close quickly often determines whether your offer gets accepted.

Understanding mortgage advisor rates empowers you to make informed financing decisions while recognizing that value extends beyond price to include expertise, service, and market knowledge. Whether you're purchasing your first home in Shoreline, upgrading to a larger property in Bellevue, or leveraging stock compensation for a jumbo loan in Seattle, working with the right advisor makes all the difference. Keith Akada brings 25+ years of experience and 750+ five-star reviews to every client relationship, offering transparent pricing, specialized knowledge of tech employee compensation, and the ability to close loans in as few as 9 business days. Discover how strategic mortgage guidance helps you achieve your homeownership goals by connecting with Mortgage Reel today.