Are you ready to unlock the secrets to financial success in a changing market? As broker rates mortgage trends shift in 2026, mastering the right strategies is more important than ever for homebuyers and investors.

This guide provides you with a powerful blueprint to confidently navigate broker rates, from understanding market influences to securing the best possible deal. Discover how to compare rates, negotiate effectively, and future-proof your mortgage decisions.

Stay ahead with expert insights, proven tactics, and a clear roadmap to achieve your home financing goals in 2026.

Understanding Broker Rates in 2026: Trends and Influences

Unlocking the dynamics behind broker rates mortgage options in 2026 is essential for buyers and investors alike. As the market shifts, understanding how these rates evolve, what drives them, and how they compare to bank offerings will give you a strategic edge.

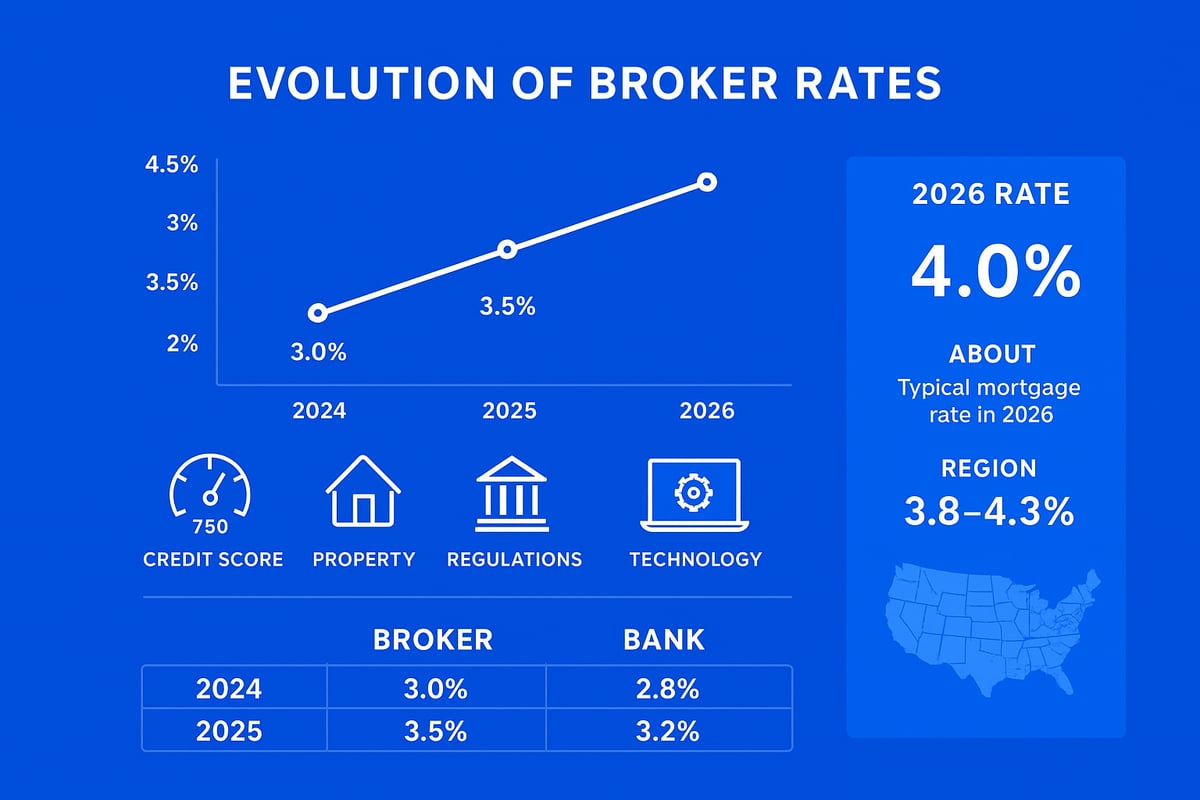

The Evolution of Broker Rates: 2024-2026

Broker rates mortgage offerings have undergone significant changes from 2024 to 2026. Economic cycles, especially Federal Reserve policy shifts, have played a crucial role in these changes. In 2024, the average 30-year fixed mortgage rate hovered around 6.7 percent. Projections for 2026 suggest rates may trend downward, influenced by anticipated rate cuts and increased competition.

Digital platforms have also improved rate transparency, allowing borrowers to compare broker rates mortgage options more efficiently than ever. Historically, rates have fluctuated with inflation and policy, but the drive toward online tools marks a new era in rate discovery.

| Year | Avg 30-Year Fixed | Rate Trend |

|---|---|---|

| 2024 | 6.7% | Stable |

| 2026 | 5.9% (projected) | Decreasing |

Key Factors Driving Broker Rates

Several elements shape broker rates mortgage outcomes for borrowers in 2026. Your credit score remains one of the most influential factors, directly impacting the rates offered. The loan-to-value ratio and your down payment amount can also affect your qualifying rate.

Property type and location matter, too. For example, urban condos may have different risk profiles compared to suburban single-family homes. Whether you are a first-time buyer or an investor, your borrower profile influences the broker rates mortgage lenders present.

Lender competition and overall market demand further drive rate variability, making it vital to compare options before deciding.

Broker vs. Bank Mortgage Rates: What’s the Difference?

Understanding broker rates mortgage options compared to direct bank rates is crucial. Mortgage brokers act as intermediaries, sourcing rates from various lenders, while banks typically offer their own in-house products.

Brokers often provide more flexibility in loan products and may have access to exclusive rates or promotions. Fee structures differ; brokers might charge origination or service fees, while banks may bundle fees with their loans. In competitive markets like Seattle, brokered loans can sometimes secure lower rates or better terms than bank-only options, especially for unique borrower situations.

| Feature | Broker | Bank |

|---|---|---|

| Rate Access | Multiple lenders | Single institution |

| Flexibility | High | Moderate |

| Fees | May vary | Often bundled |

Regulatory and Economic Influences in 2026

The regulatory landscape in 2026 is expected to introduce new lending guidelines affecting broker rates mortgage qualifications. Changes in federal programs like FHA and VA loans could offer new incentives or modify eligibility criteria.

Inflation trends will continue to impact mortgage rates. Even a 0.5 percent rate change can significantly alter monthly payments, emphasizing the importance of timing. For example, on a $500,000 loan, a 0.5 percent shift could change payments by over $150 per month.

Government incentives may also play a role in lowering broker rates mortgage options for certain buyers, making it important to stay informed on policy updates.

Predicting the 2026 Mortgage Landscape

Expert forecasts indicate that broker rates mortgage competition will intensify as technology advances and more lenders enter the market. Regional variations will persist, with urban areas potentially seeing different trends than suburban regions.

Online rate comparison platforms are expected to further empower buyers, while analysts anticipate 2026 rates to remain moderately lower than their 2024 peak. For a comprehensive look at expert projections and market drivers, review the latest mortgage rate trends and predictions for 2026.

Staying proactive and informed is key to securing the most favorable broker rates mortgage deals in this evolving landscape.

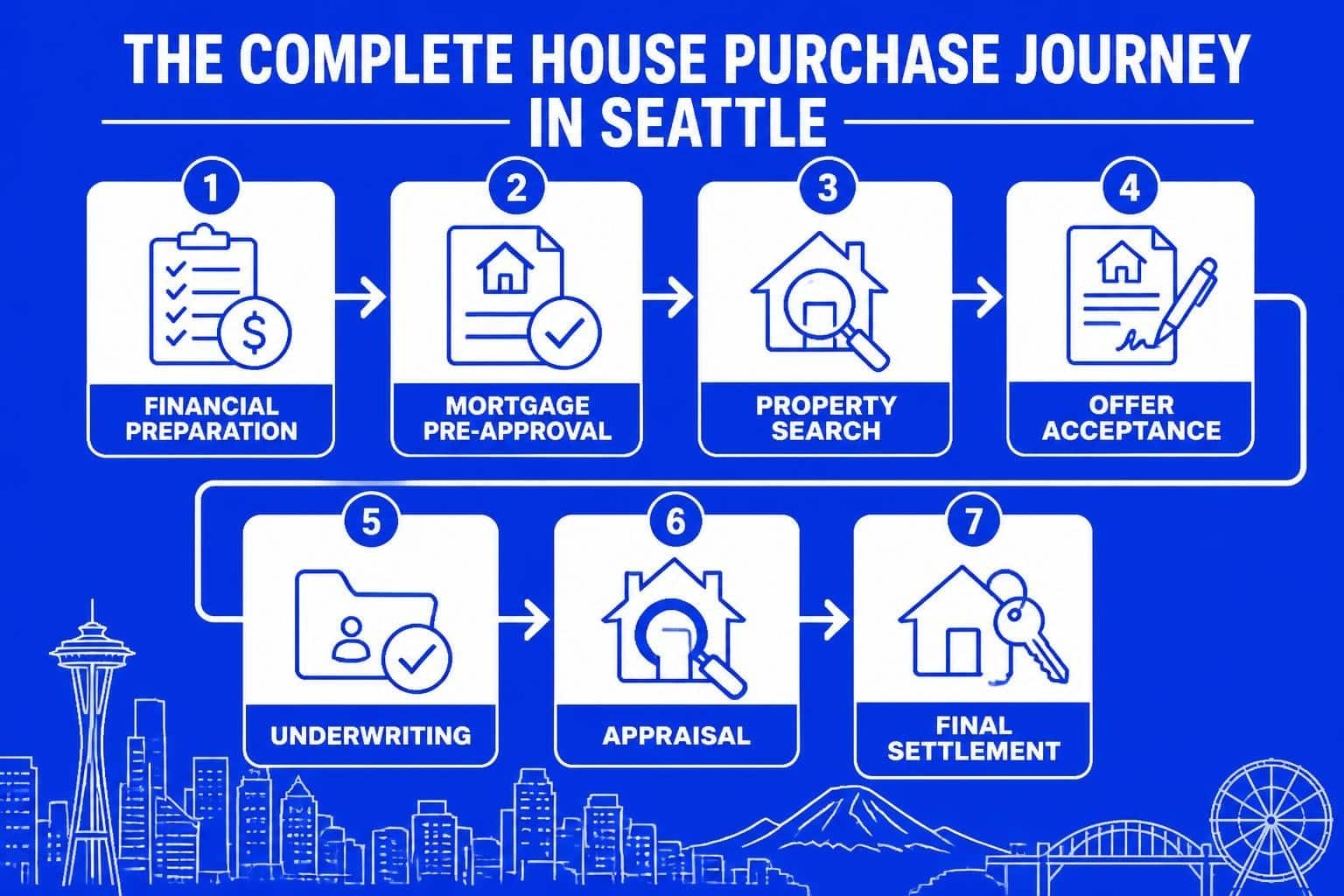

Step-by-Step Mortgage Process: From Pre-Approval to Closing

Navigating the broker rates mortgage journey in 2026 requires a clear, step-by-step approach. Whether you are a first-time buyer or a seasoned investor, understanding each phase helps you avoid surprises and secure the best terms. Let us break down the full process from financial assessment to closing, so you can tackle your broker rates mortgage with confidence.

Step 1: Assessing Your Financial Readiness

Start your broker rates mortgage process by reviewing your credit reports and scores. Lenders in 2026 will examine your debt-to-income (DTI) ratio, so calculate your monthly obligations carefully. Saving for a down payment is crucial, along with budgeting for closing costs. For example, conventional loans may require a minimum 620 credit score and at least 3% down, while FHA loans may allow lower scores but higher insurance premiums. VA loans often offer zero down for eligible veterans. Assessing your readiness sets the foundation for a successful broker rates mortgage experience.

Step 2: Getting Pre-Approved with a Mortgage Broker

The next step in your broker rates mortgage journey is pre-approval. Gather documentation such as pay stubs, tax returns, and bank statements. Mortgage brokers will evaluate your income, assets, and credit profile to determine your eligibility. A pre-approval letter strengthens your offer, especially in competitive 2026 markets. Typically, pre-approval can be completed within a few business days. Having this step complete signals to sellers that you are a serious and qualified buyer, streamlining the broker rates mortgage process.

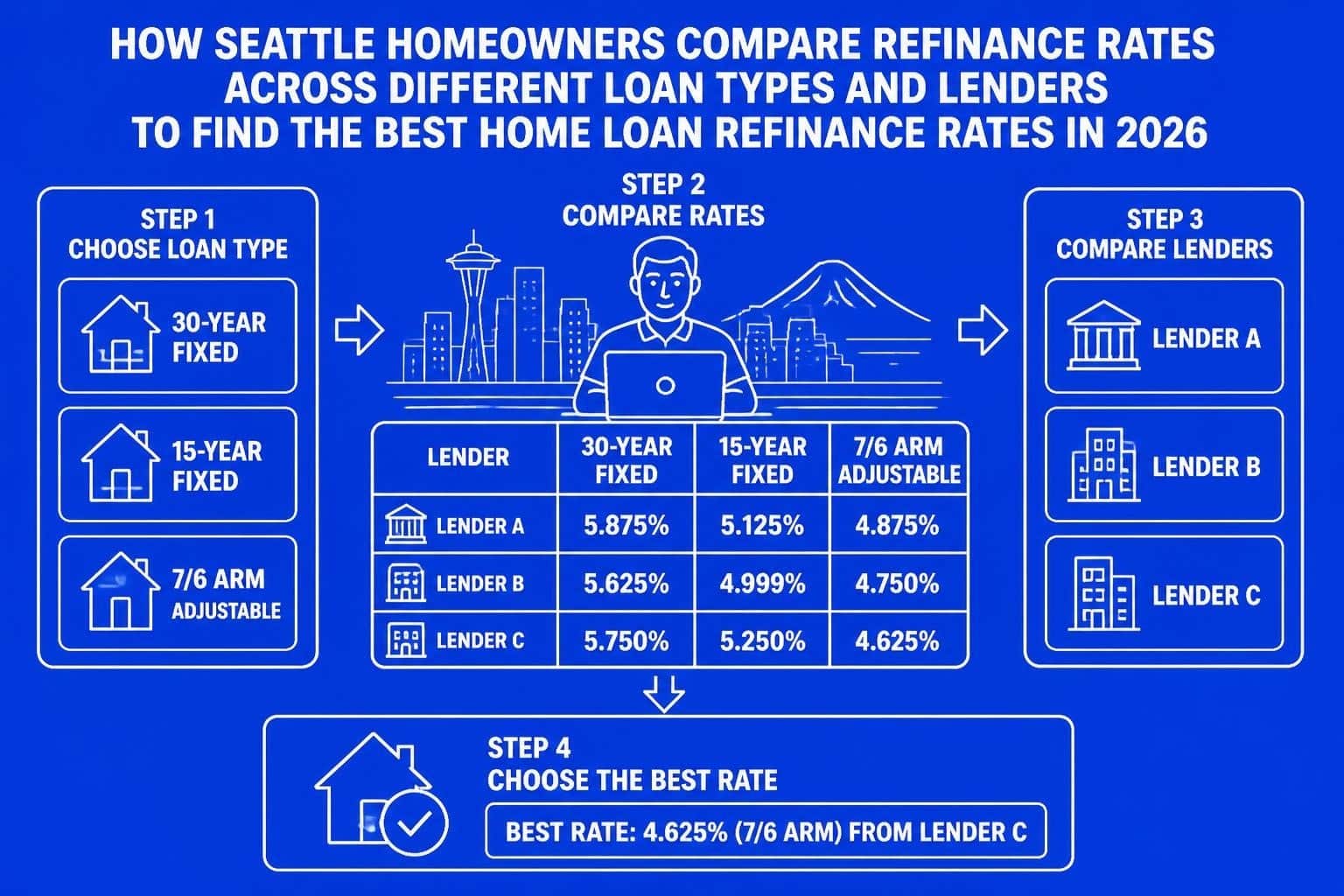

Step 3: Comparing Broker Rates and Loan Options

Once pre-approved, compare broker rates mortgage options to find the best fit. Decide between fixed and adjustable-rate mortgages based on your risk tolerance. Evaluate annual percentage rates (APR), points, and fees for a clear cost comparison. Leverage online comparison tools to view multiple offers side by side. For up-to-date data, check Seattle mortgage rates today for real-world examples and trends. For instance, a $600K home in Seattle might yield different broker rates mortgage quotes depending on your profile and loan type.

Step 4: Locking in Your Rate

Timing is everything when locking in your broker rates mortgage. After selecting your lender and loan, decide when to secure your interest rate. Rate lock periods in 2026 often range from 30 to 60 days, with extensions available if your closing is delayed. Monitor market trends and economic news to pinpoint favorable moments for locking in. Data shows that the average lock duration can impact your broker rates mortgage cost, as rates may fluctuate daily. A timely lock can protect you from unexpected increases.

Step 5: Navigating the Underwriting Process

During underwriting, lenders scrutinize every aspect of your broker rates mortgage application. Expect requests for updated documentation or clarifications regarding your finances. Underwriters will verify your employment, assets, and property details. Address conditional approvals promptly to avoid delays. On average, underwriting in 2026 takes five to ten business days, depending on loan complexity. Staying organized and responsive ensures your broker rates mortgage moves smoothly through this critical stage.

Step 6: Closing the Deal

The final step in the broker rates mortgage process is closing. Review your Closing Disclosure (CD) to ensure all fees and terms match your expectations. Understand the breakdown of closing costs, which typically include lender fees, title insurance, and taxes. Complete a final property walkthrough to confirm the home’s condition. Once you sign the legal documents and provide any required funds, ownership transfers to you. In Washington State, closing costs usually range from 2% to 5% of the purchase price. Celebrate your successful broker rates mortgage closing and prepare to move in.

Maximizing Savings: Strategies to Secure the Best Broker Rates

Unlocking the best broker rates mortgage deals in 2026 is about more than just timing. With the right strategies, you can save thousands over the life of your loan. Let us break down actionable steps to help you maximize savings and secure the most competitive rates possible.

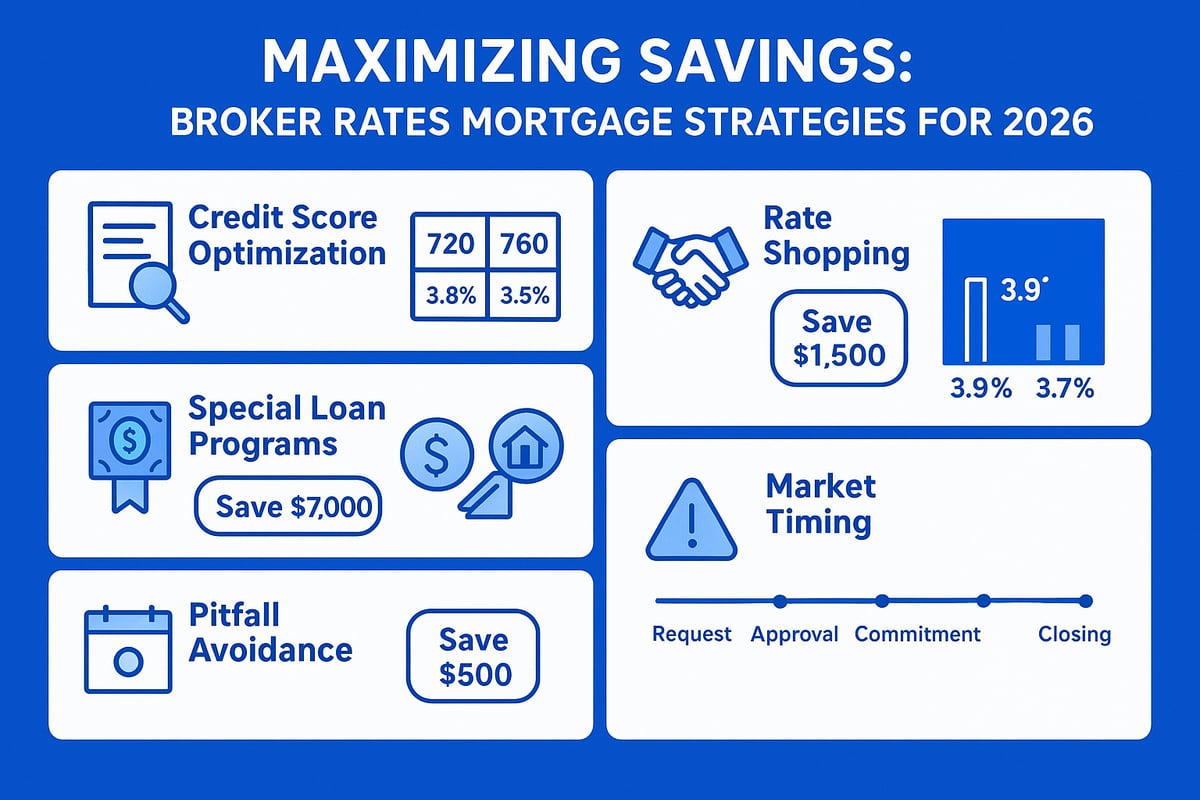

Improving Your Borrower Profile

Your borrower profile shapes the broker rates mortgage offers you receive. Start by reviewing your credit report for errors and paying down revolving debts. Increasing your credit score by even 20 points can lead to a noticeable rate reduction. Aim for a lower debt-to-income ratio by avoiding large purchases before applying. Save for a higher down payment, as this can improve your loan-to-value ratio and unlock better rates. If you’re changing jobs, consider waiting until after your loan closes to avoid complications. Remember, a strong profile is your ticket to the best broker rates mortgage deals.

Shopping and Negotiating Like a Pro

Comparison shopping is essential for securing favorable broker rates mortgage terms. Gather official Loan Estimates from at least three brokers and lenders. Review each for differences in interest rates, APR, and closing costs. Use competing offers as leverage—brokers are often willing to match or beat competitor rates. Negotiating broker fees and requesting lender credits can further reduce your out-of-pocket expenses. For more strategies to boost your savings, check out how to lower your mortgage payment. Every dollar you save on broker rates mortgage fees adds up over time.

Leveraging Special Programs and Incentives

Special programs can help you access lower broker rates mortgage options. First-time homebuyers may qualify for grants or down payment assistance, reducing upfront costs. VA, FHA, and USDA loans offer competitive rates and relaxed qualification criteria for eligible buyers. Research local and national programs to see which incentives align with your situation. For example, a qualified buyer using a down payment assistance program could save thousands in the first year alone. Always ask your broker about available programs that can make your broker rates mortgage more affordable.

Timing Your Application for Market Advantage

Timing can significantly impact your broker rates mortgage outcome. Historically, mortgage rates dip during certain months, such as late spring or early fall. Monitor economic announcements, like Federal Reserve rate changes, as they often trigger market shifts. Locking in your rate during a temporary dip could secure a lower payment for years to come. Use online tools to track rate trends and plan your application accordingly. By being strategic, you can capitalize on market conditions and secure the most competitive broker rates mortgage available.

Avoiding Common Pitfalls in the Rate Search

Even savvy buyers can stumble into costly traps during the broker rates mortgage search. Watch for hidden fees in the fine print and always verify the total cost of your loan. Beware of rate bait and switch tactics, where an initially attractive rate changes before closing. Protect yourself by verifying your broker’s credentials and reading client reviews. Learning from others’ mistakes can save you both time and money. Staying vigilant ensures you benefit from the best broker rates mortgage without unwelcome surprises.

Broker Rates Mortgage Guide: Expert Insights and Tools for 2026

Navigating the broker rates mortgage landscape in 2026 requires a toolkit of expert strategies, digital resources, and local insight. Whether you are a first-time homebuyer or a seasoned investor, understanding the right tools and tactics can help you secure the most competitive rates and terms for your mortgage goals.

Essential Tools for Comparing Broker Rates

To master the broker rates mortgage process, leverage a range of modern comparison tools. Start with reputable online rate comparison platforms, which aggregate up-to-the-minute lender and broker offers. These platforms allow you to filter by loan type, term, and location, ensuring you see the most relevant options.

Mobile apps now deliver real-time alerts on rate changes, while mortgage calculators help you estimate monthly payments, interest costs, and amortization schedules. Interpreting rate tables and APR disclosures is crucial; always compare the annual percentage rate, not just the advertised interest rate. For 2026, top-rated tools include RateHub, Mortgage News Daily’s rate tracker, and local broker platforms.

Understanding Fees, Points, and APR

A key element of broker rates mortgage decisions is understanding how fees and points influence your total loan cost. Origination fees, discount points, and third-party charges all contribute to your closing expenses.

The APR, or annual percentage rate, reflects not just the interest rate but also these additional costs. Use the following table to compare two $500,000 loan scenarios:

| Fee Type | Loan A (No Points) | Loan B (With Points) |

|---|---|---|

| Origination Fee | $2,500 | $2,500 |

| Discount Points | $0 | $5,000 (1 point) |

| Third-Party Costs | $3,000 | $3,000 |

| Interest Rate | 6.00% | 5.75% |

| APR | 6.12% | 5.96% |

Calculate your break-even point to decide if paying points makes sense for your broker rates mortgage. Always request a detailed Loan Estimate for transparency.

The Role of Mortgage Brokers in Rate Negotiation

Mortgage brokers are your advocates in the broker rates mortgage process, negotiating with multiple lenders to secure competitive terms. They can access exclusive lender credits, offer flexible fee structures, and explain complex rate lock options.

Transparent compensation is key. Brokers may be paid by the lender or borrower, but must disclose all fees upfront. Their local market knowledge can be invaluable, especially in dynamic areas like Seattle and Bellevue. For a deeper understanding of broker advantages, see the Choosing a Seattle mortgage broker guide.

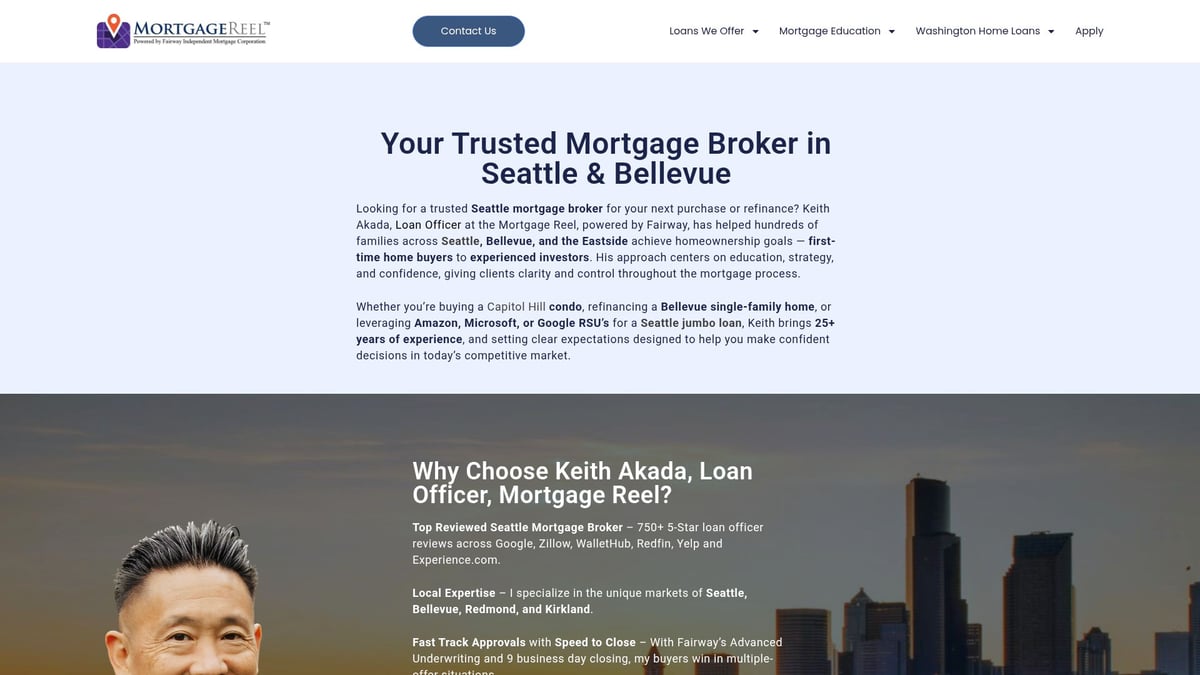

The Mortgage Reel: Local Expertise for Seattle & Bellevue Homebuyers

The Mortgage Reel stands out as a leader in broker rates mortgage solutions, bringing over 25 years of experience to Seattle and Bellevue clients. Their team specializes in tailored mortgages for first-time buyers, tech professionals, and investors.

Clients benefit from fast-track approvals and a deep understanding of local market trends. The Mortgage Reel’s education-first approach ensures you are guided through every option, from rate negotiation to final closing. With more than 750 five-star reviews, they set the standard for award-winning, client-focused service.

Case Studies: Real-World Rate Successes

Broker rates mortgage expertise delivers measurable results. Consider a first-time Seattle buyer who, with broker assistance, secured a rate 0.35% below the 2025 market average, saving over $1,200 annually.

Another case: An investor obtained jumbo loan approval after leveraging a broker’s relationship with niche lenders. On average, borrowers who partner with brokers saved 0.25–0.40% on rates compared to direct bank offers in 2025, according to regional data.

Frequently Asked Questions About Broker Rates

Common broker rates mortgage questions focus on rate changes, broker credibility, and education resources. How do you verify a broker’s license? Check state databases and read online reviews.

If your rate changes before closing, ask for a written explanation and renegotiate if possible. For ongoing mortgage education, explore home ownership education resources to stay updated on rate trends and best practices.

Future-Proofing Your Mortgage: Strategies for Long-Term Success

Securing a home loan is just the beginning. To truly maximize your investment, you need to future-proof your broker rates mortgage strategy with proactive planning and ongoing education. The following steps will help you build resilience, protect your finances, and seize opportunities in a changing market.

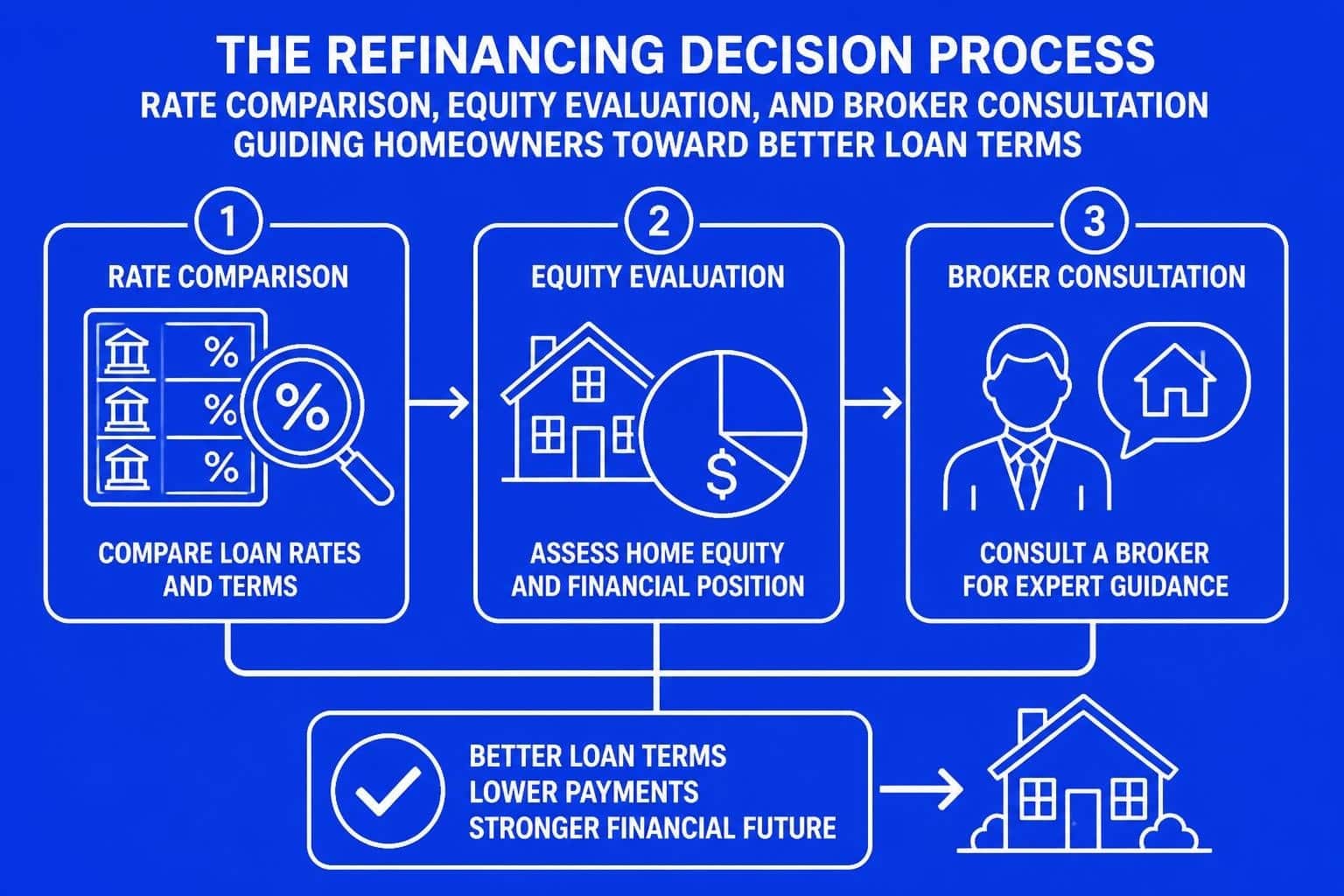

Preparing for Rate Changes and Refinancing Opportunities

Staying alert to interest rate shifts is crucial for anyone with a broker rates mortgage. After closing, monitor economic signals and news, especially regarding Federal Reserve rate cuts projected for 2026, as these can directly impact mortgage costs.

Refinancing becomes attractive when rates drop, allowing you to lower monthly payments or reduce your loan term. For example, refinancing from 6.5% to 6.0% on a $500,000 loan can save thousands in interest.

Set calendar reminders to review your mortgage annually and assess if a rate change or new product could benefit your financial goals.

Building Equity and Managing Your Loan

Accelerating your equity build in a broker rates mortgage can provide long-term financial stability. Consider making extra principal payments or switching to a bi-weekly payment plan to pay down your loan faster.

A simple table illustrates the impact:

| Payment Plan | 30-Year Savings | Loan Paid Off In |

|---|---|---|

| Monthly | $0 | 30 years |

| Bi-Weekly | $25,000+ | ~25 years |

Even one additional payment per year can shave years off your term and save significant interest. Consistent equity growth increases your options for future borrowing or home improvements.

Protecting Against Payment Shock and Financial Stress

If your broker rates mortgage includes variable or adjustable rates, it is vital to budget for possible payment increases. Calculate your maximum potential payment and ensure you have an emergency fund covering at least three to six months of expenses.

Consider these protective steps:

- Maintain a buffer in your checking account

- Review mortgage insurance options

- Use online calculators to model payment changes

By planning ahead, you minimize the risk of financial stress if rates rise unexpectedly.

Leveraging Home Value Appreciation

Home appreciation can be a powerful tool in your broker rates mortgage strategy. According to the 2026 housing market outlook and mortgage rate forecasts, property values in key metro areas like Seattle and Bellevue are projected to rise.

As your home’s value climbs, you may qualify for a cash-out refinance, enabling renovations or investments. Regularly review your home’s market value and consult your broker about leveraging equity for future opportunities.

Data-driven planning ensures you capitalize on appreciation trends.

Staying Informed: Ongoing Mortgage Education

Continuous education is essential for anyone managing a broker rates mortgage. Track market news, attend webinars, and subscribe to trusted mortgage publications.

Recommended actions:

- Set up alerts for rate changes

- Attend local seminars for homeowners

- Join online forums for up-to-date broker advice

Staying informed allows you to respond quickly to market shifts and regulatory updates, keeping your strategy current.

Planning for Your Next Move: Portability and Future Purchases

As your needs change, it is smart to plan ahead for future transactions involving your broker rates mortgage. Some lenders offer portability, letting you transfer your loan to a new property without penalty.

Checklist before your next move:

- Review your current loan’s portability features

- Assess your equity for potential down payments

- Prepare updated financial documents for swift approval

Strategic preparation ensures you are ready for upsizing, downsizing, or investing, maximizing the benefits of your existing mortgage.

You’ve just explored the key strategies for navigating broker rates and securing the best mortgage options in 2026, whether you’re buying your first home or building your investment portfolio. The choices you make today can set you up for years of financial confidence and peace of mind. If you want to discuss your specific goals, review your options, or get expert advice tailored to your situation, I’m here to help. Let’s connect and turn your blueprint into reality—Let’s have a conversation.