When navigating Seattle's competitive housing market, understanding mortgage broker charges can make a significant difference in your overall borrowing costs. Whether you're a tech professional at Amazon or Microsoft looking to leverage RSU compensation for a jumbo loan, a first-time buyer in Lynnwood, or a homeowner refinancing in Bellevue, clarity about how brokers earn their compensation helps you make confident financial decisions. Mortgage broker charges typically range from 1% to 2% of the loan amount, though the structure varies depending on whether the borrower or lender pays the fee, and understanding these nuances is essential for budgeting your home purchase or refinance in 2026.

Understanding Mortgage Broker Charges in Seattle

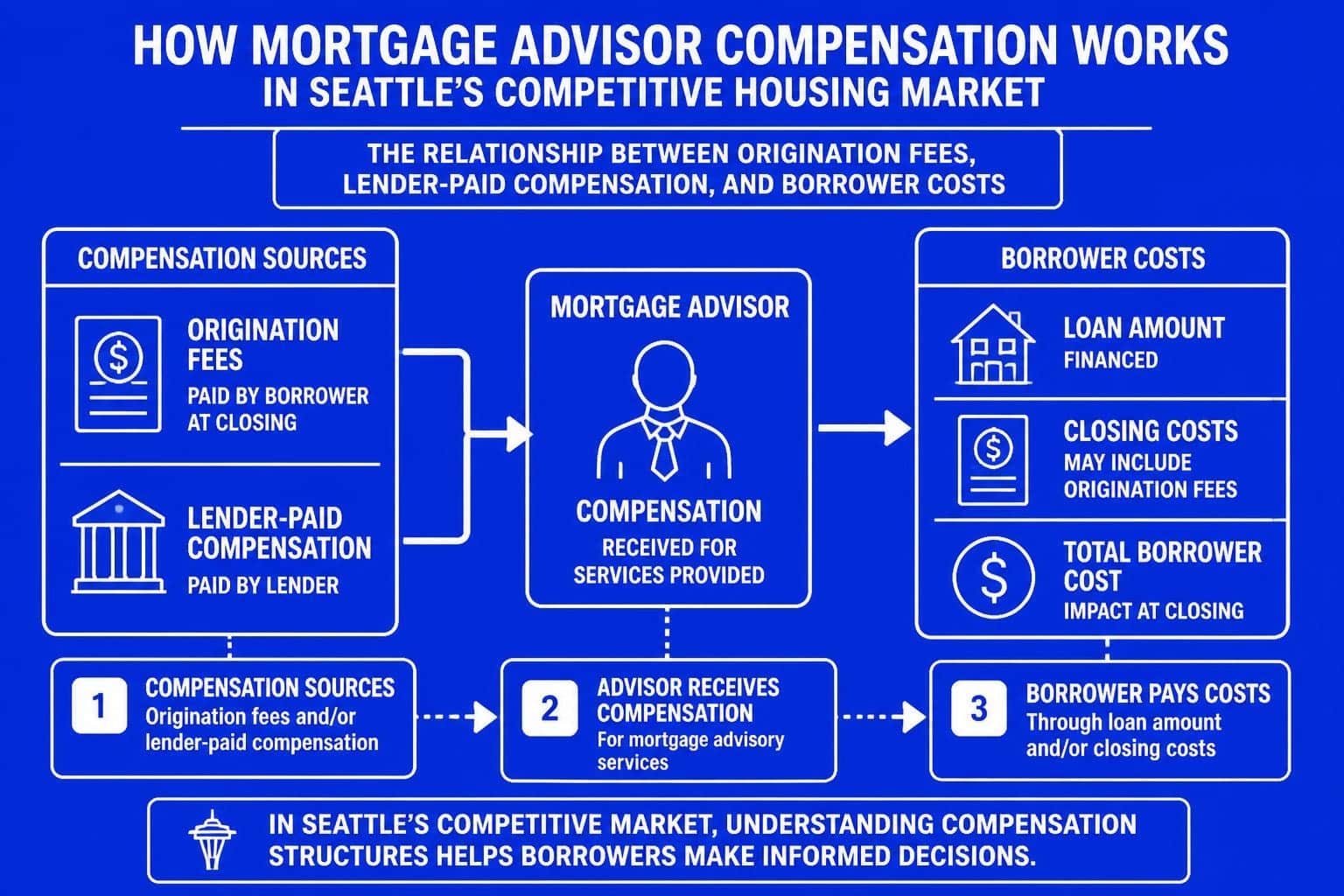

Mortgage broker charges represent the compensation mortgage brokers receive for their services in connecting borrowers with lenders and managing the loan process from application through closing. In the Greater Seattle area, including Redmond, Kirkland, and Shoreline, these charges reflect the value brokers provide: access to multiple lenders, expert guidance on loan products, and negotiation on your behalf.

The fee structure can take several forms. Some brokers charge a direct origination fee paid by the borrower at closing, while others receive compensation from the lender through yield spread premiums. Understanding how mortgage brokers get paid helps you evaluate the true cost of working with a broker versus going directly to a bank.

Borrower-Paid vs. Lender-Paid Compensation

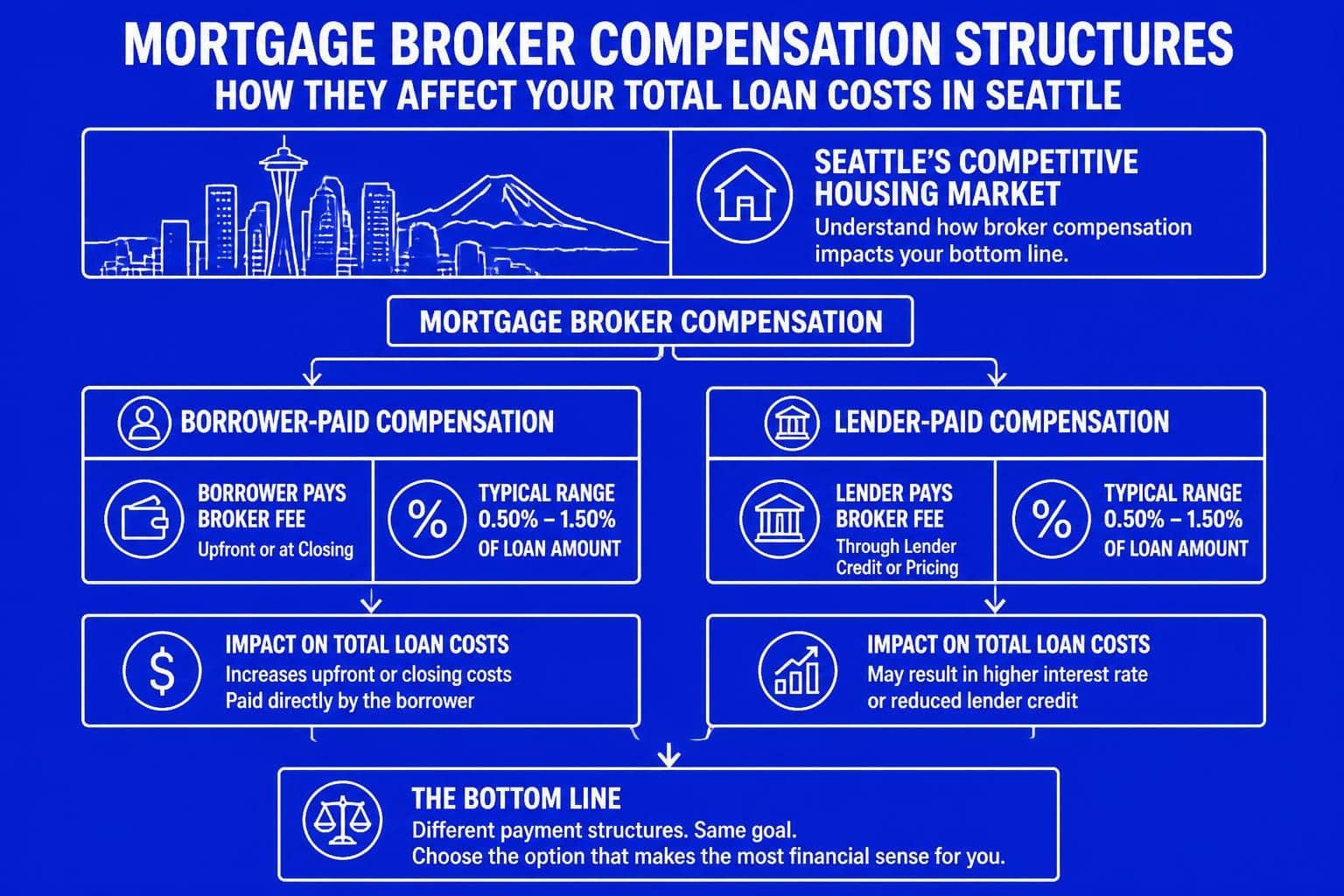

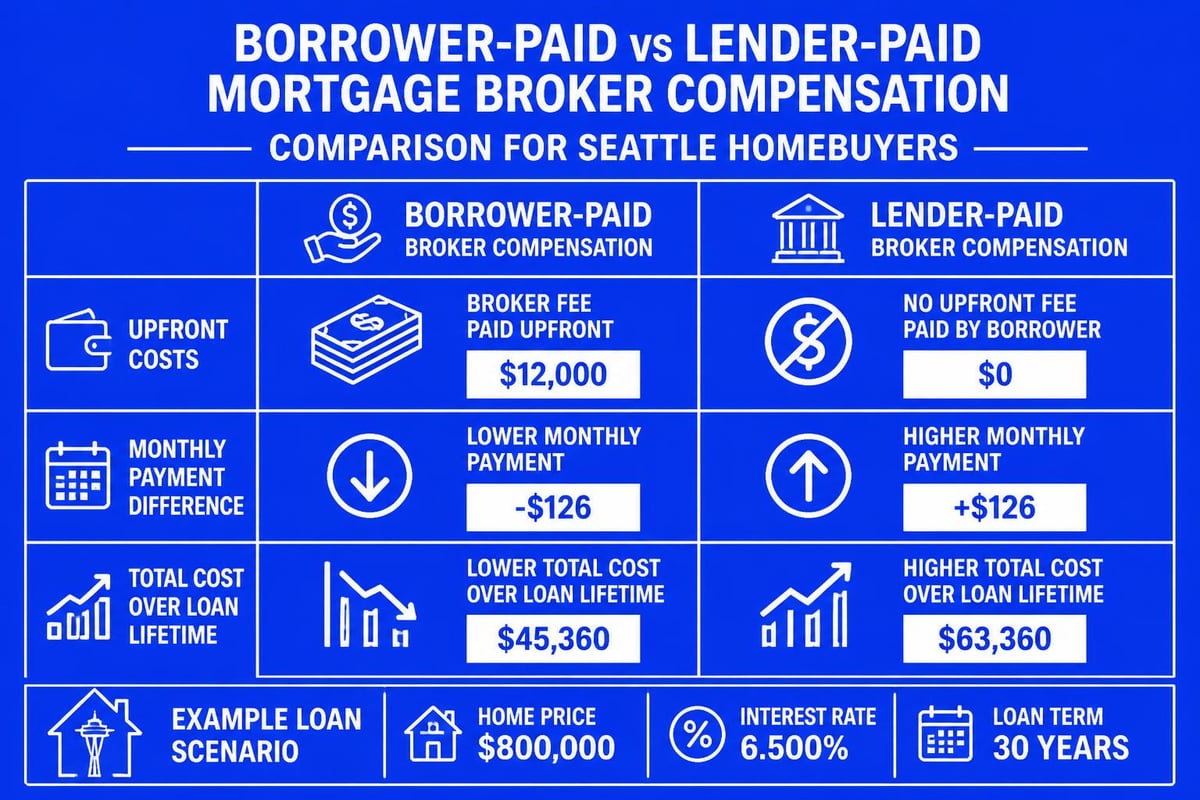

The question of who pays mortgage broker fees significantly impacts your upfront costs and long-term loan economics. In borrower-paid arrangements, you pay the broker directly at closing, typically 1% to 2% of the loan amount. For a $750,000 home purchase in Mill Creek, that could mean $7,500 to $15,000 in broker fees.

Lender-paid compensation models shift the fee burden to the lender, who pays the broker from their own revenue. This arrangement often results in a slightly higher interest rate, as lenders build their costs into the loan pricing. The trade-off is lower upfront costs but potentially higher total interest over the life of the loan.

Key factors influencing which model works best:

- Available cash for closing costs

- Length of time you plan to keep the loan

- Current interest rate environment

- Total loan amount and property value

- Your overall financial strategy

Typical Fee Ranges and What They Include

Mortgage broker charges in the Seattle area generally follow industry standards, though specific amounts vary based on loan complexity, property type, and market conditions. For conventional loans on single-family homes in Everett or Lake Forest Park, expect fees at the lower end of the range. Jumbo loans, investment properties, or complex compensation scenarios involving stock options may command higher fees reflecting the additional expertise required.

| Loan Type | Typical Broker Fee | What's Included |

|---|---|---|

| Conventional Purchase | 1.0% – 1.5% | Application processing, lender negotiation, document coordination |

| FHA/VA Loan | 0.5% – 1.0% | Government program expertise, compliance management |

| Jumbo Loan | 1.5% – 2.0% | Advanced underwriting support, stock compensation qualification |

| Refinance | 0.75% – 1.5% | Rate analysis, break-even calculations, closing coordination |

| Investment Property | 1.5% – 2.0% | Rental income qualification, multi-property strategy |

These fees cover comprehensive services beyond simply submitting your application. Working with good mortgage brokers means receiving strategic advice on loan structure, timing, and product selection that can save thousands over the loan term.

Services Covered by Broker Fees

Your broker fee pays for expert guidance throughout the mortgage process. This includes initial consultation and needs assessment, comprehensive comparison of loan products from multiple lenders, pre-approval and credit analysis, documentation gathering and review, negotiation of rates and terms, and coordination through underwriting and closing.

For Seattle-area tech professionals, brokers specializing in complex compensation structures provide additional value. Qualifying RSUs, stock options, and bonus income requires detailed documentation and lender expertise. The right broker knows which lenders accept these income sources and how to present them for maximum buying power.

The fee also covers problem-solving when issues arise. Whether addressing appraisal gaps common in competitive Seattle neighborhoods, navigating inspection contingencies, or restructuring your loan when rate changes occur, experienced brokers earn their compensation through expert execution.

Federal Regulations Governing Broker Compensation

Federal regulations establish clear rules about mortgage broker charges to protect consumers and ensure transparency. The Real Estate Settlement Procedures Act (RESPA) and subsequent Dodd-Frank reforms prohibit certain practices and mandate disclosures that help borrowers understand exactly what they're paying.

Commission structures for mortgage brokers must comply with federal compensation rules that eliminate dual compensation and steering incentives. Brokers cannot receive payment from both the borrower and lender on the same transaction, preventing conflicts of interest that could lead to inappropriate loan recommendations.

Loan Estimate Disclosure Requirements

Within three business days of your loan application, your broker must provide a Loan Estimate that clearly itemizes all mortgage broker charges and other closing costs. This standardized form allows you to compare offers from different brokers and lenders accurately.

The Loan Estimate shows:

- Origination charges and points

- Services the broker cannot shop for

- Services you can shop for

- Total estimated closing costs

- Estimated monthly payment

- Total cash needed to close

This transparency empowers you to ask questions and understand whether the broker charges align with the services provided. In Seattle's fast-moving market, having this information early helps you budget accurately and make competitive offers with confidence.

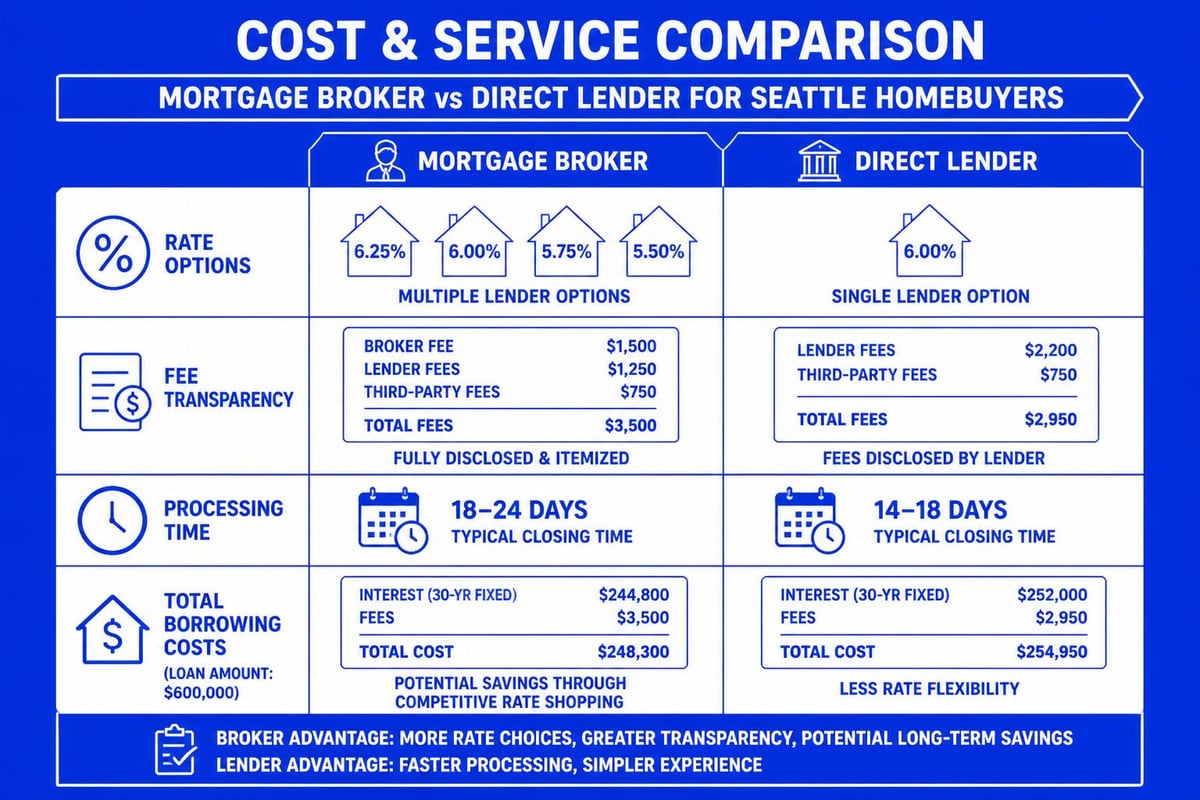

Comparing Broker Costs to Direct Lender Options

Many Seattle homebuyers wonder whether working with a broker or going directly to a bank offers better value. The answer depends on your specific situation, loan complexity, and how you value time and expertise.

Direct lenders typically don't charge separate origination fees labeled as "broker charges," but they build their compensation into the loan pricing through interest rates and lender fees. The total cost may be similar or even higher than working with a broker who has access to wholesale rates from multiple lenders.

Value Proposition for Seattle Homebuyers

For first-time buyers navigating home loans for first-time buyers, the educational value and personalized guidance often justify mortgage broker charges. Brokers explain complex concepts, help you understand different loan programs, and match you with products that align with your long-term financial goals.

In competitive Seattle neighborhoods where offers need to move quickly, brokers with established lender relationships can expedite processing and provide certainty that attracts sellers. Some brokers can close loans in as few as 9 business days, a significant advantage when competing against all-cash offers.

For jumbo home loans common in Bellevue and Kirkland, brokers provide access to portfolio lenders and specialized products not available through retail bank branches. The complexity of qualifying stock compensation and achieving optimal loan structure often requires expertise that justifies the fee.

Negotiating Mortgage Broker Charges

While mortgage broker charges follow general market ranges, they're often negotiable depending on your loan size, credit profile, and overall relationship potential. Brokers value long-term client relationships and referrals, which can create flexibility in fee structures.

Larger loan amounts naturally support lower percentage fees while maintaining reasonable compensation for the broker's work. A 0.75% fee on a $1.2 million purchase in Redmond generates $9,000, adequate compensation that costs you less on a percentage basis than 1.5% on a $400,000 purchase.

Strategies for Fee Discussions

Approach fee conversations professionally and respectfully. Great mortgage brokers understand that informed clients have questions about costs and welcome transparent discussions about value and pricing.

Effective negotiation approaches:

- Request a detailed breakdown of services included in the fee

- Compare total costs including interest rates, not just upfront fees

- Ask about fee structures for different loan scenarios

- Inquire about discounts for repeat clients or referrals

- Consider the total value package rather than focusing solely on lowest cost

Remember that the lowest fee doesn't always deliver the best outcome. A broker charging 1.25% who secures you a rate 0.25% lower than another lender saves you significantly more over the loan term than saving 0.25% on the broker fee.

Special Considerations for Seattle-Area Tech Professionals

Tech employees at Amazon, Microsoft, Google, and other Seattle-area companies face unique situations when obtaining financing. Stock-based compensation represents a significant portion of total income, but not all lenders understand how to qualify RSUs, stock options, and vesting schedules properly.

Mortgage broker charges for these complex scenarios may run slightly higher, reflecting the specialized expertise required. Brokers familiar with tech compensation work with specific underwriters who accept two-year histories of stock income, understand vesting cliffs, and properly calculate qualifying income from equity compensation.

Maximizing Buying Power with Complex Income

The value delivered often exceeds the additional cost. A broker experienced with mortgage financing for tech professionals might qualify you for $200,000 more in borrowing power by properly documenting and presenting your stock compensation. That difference can mean securing your ideal home in a competitive neighborhood rather than settling for a backup option.

For jumbo financing common among Seattle tech buyers, understanding conventional loan lenders that specialize in high-balance mortgages ensures you receive competitive rates and terms. The broker's lender relationships and product knowledge directly impact your financial outcome.

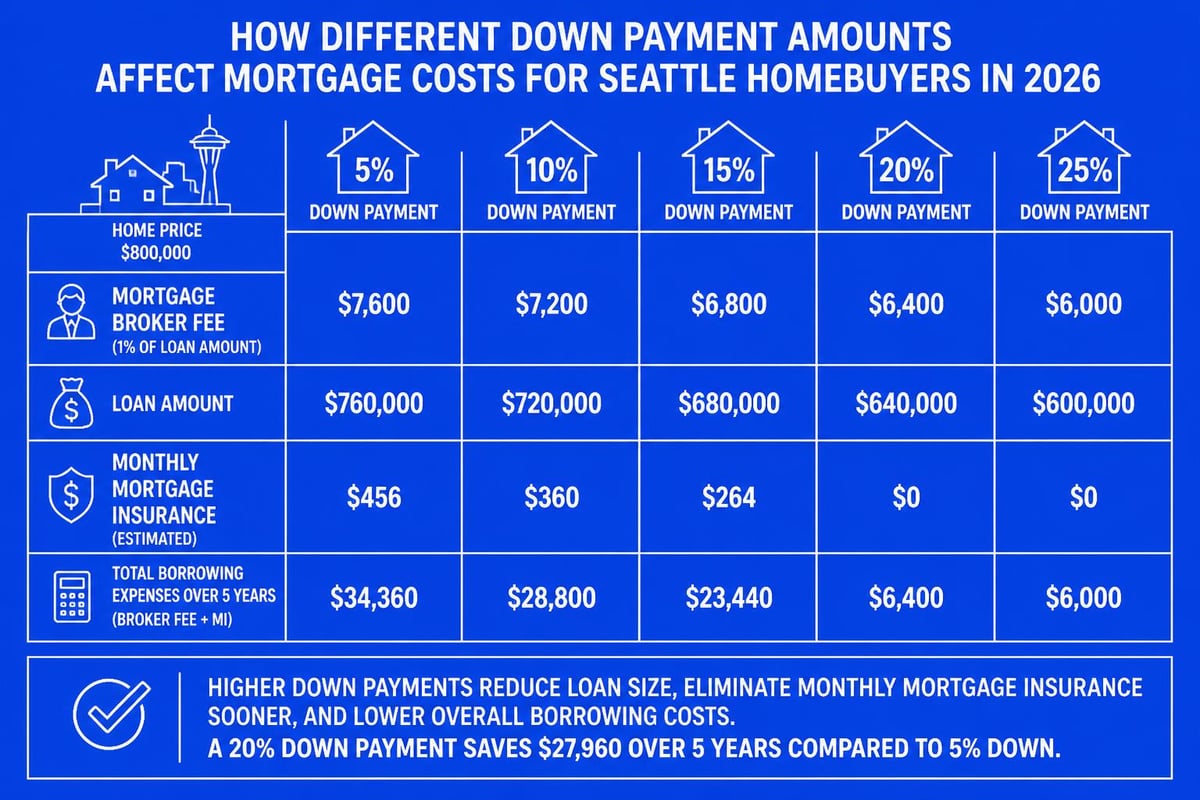

Down Payment Strategies and Their Impact on Broker Fees

Your down payment amount affects total loan size, which directly influences mortgage broker charges calculated as a percentage of the loan amount. Seattle homebuyers should understand how different down payment strategies affect both broker compensation and overall loan costs.

A 20% down payment on a $900,000 home in Shoreline means a $720,000 loan amount. At 1% broker fee, that's $7,200. Putting down only 5% creates a $855,000 loan and $8,550 in broker fees at the same percentage. However, the smaller down payment also triggers mortgage insurance costs that dwarf the difference in broker fees.

Down payment considerations:

| Down Payment | Loan Amount | Broker Fee (1%) | PMI Impact | Total Cost Difference |

|---|---|---|---|---|

| 5% | $855,000 | $8,550 | ~$400/month | Higher long-term cost |

| 10% | $810,000 | $8,100 | ~$300/month | Moderate savings |

| 20% | $720,000 | $7,200 | None | Optimal cost structure |

Understanding the down payment guide for Seattle homebuyers helps you balance upfront cash needs against long-term costs and how broker fees fit into the total picture.

Refinance Scenarios and Broker Compensation

Mortgage broker charges for refinances typically run lower than purchase transactions, ranging from 0.75% to 1.5% depending on loan complexity. The reduced fee reflects less coordination required compared to purchase transactions, though the analysis and lender comparison work remains substantial.

Seattle homeowners considering refinancing should evaluate whether the savings justify the costs, including broker fees. A break-even analysis determines how many months of reduced payments are needed to recover the refinance costs.

When Refinancing Makes Sense

Rate improvements of at least 0.5% to 0.75% generally justify refinancing when you plan to keep the loan for several years. Current homeowners in Everett or Lake Forest Park who locked rates above 7% in recent years may find significant savings opportunities as rates decline in 2026.

Cash-out refinances for debt consolidation or home improvements involve larger loan amounts and more complex analysis. Mortgage broker charges reflect the additional work in evaluating equity positions, qualifying new loan amounts, and structuring optimal loan terms.

Brokers add value by comparing multiple refinance scenarios: rate-and-term refinances, cash-out options, switching from adjustable to fixed rates, or restructuring for different loan terms. How brokers make money through refinances depends on delivering genuine savings that improve your financial position.

Investment Property Financing Fees

Investors purchasing rental properties in Seattle's surrounding communities face different fee structures and underwriting requirements. Mortgage broker charges for investment properties typically range from 1.5% to 2%, reflecting additional complexity in qualifying rental income, evaluating cash flow, and managing stricter debt-to-income requirements.

Brokers experienced with investment property financing understand which lenders offer the best programs for single-family rentals, multi-family properties, and portfolio investors managing multiple properties. They navigate unique documentation requirements including lease agreements, rent rolls, and property management considerations.

Investment property broker services include:

- Cash flow analysis and rent qualification strategies

- Multi-property portfolio management

- DSCR loan product identification

- Entity structure coordination

- 1031 exchange timing considerations

For Seattle-area investors building rental portfolios in more affordable surrounding markets like Mill Creek or Lynnwood, the expertise justifies the higher broker fee through better loan products and smoother execution.

Transparency and Disclosure Best Practices

Professional mortgage brokers embrace transparency about their compensation. Before starting the loan process, ask direct questions about how your broker gets paid, what services the fee covers, and whether any circumstances might change the quoted fee.

Quality brokers provide written fee agreements outlining their compensation structure. This protects both parties and ensures clear expectations. Any fee increases during the process should be explained and justified, typically relating to unexpected loan complexity or program changes.

Red Flags to Watch For

Be cautious of brokers who avoid discussing fees directly, provide vague answers about compensation, or claim their services are "free" without explaining the lender-paid structure. Understanding whether mortgage advisors charge fees helps you identify professionals who prioritize transparency over misleading marketing.

Pressure to close quickly without adequate time to review fees and loan terms suggests priorities misaligned with your interests. Reputable brokers encourage questions and provide time to understand all costs before proceeding.

The Value Equation Beyond Just Fees

Evaluating mortgage broker charges requires looking beyond the percentage or dollar amount to consider the total value delivered. A broker who saves you 0.375% on your interest rate through superior lender relationships and negotiation delivers substantially more value than the fee charged.

For a $700,000 loan, that rate improvement saves approximately $175 monthly or $63,000 over a 30-year term. Even a 1.5% broker fee of $10,500 represents exceptional value when the rate savings alone recovers the cost in five years and continues delivering savings thereafter.

Time savings and stress reduction also factor into the value equation. Managing your own loan process while working full-time and coordinating a home purchase creates significant stress. Professional brokers handle details, solve problems, and provide peace of mind that allows you to focus on other aspects of your move.

Common Questions Seattle Homebuyers Ask

Are mortgage broker charges tax deductible?

Origination fees and points paid to secure your mortgage may be deductible on purchase transactions if you itemize deductions. The IRS allows deducting points paid on your primary residence in the year paid. Refinance points must be deducted over the life of the loan. Consult a tax professional for guidance specific to your situation.

Can I pay broker fees with my down payment funds?

Yes, broker fees can be paid from your down payment funds at closing. They're included in your total cash-to-close calculation. Some buyers prefer this approach to minimize out-of-pocket costs, while others keep these fees separate to preserve down payment percentage thresholds.

Do all mortgage brokers charge the same fees?

No, mortgage broker charges vary based on the broker's experience, loan complexity, market positioning, and business model. Competition in Seattle's market creates fee variation, making comparison shopping valuable while remembering that total value matters more than just the lowest fee.

How do broker fees compare to mortgage points?

Broker fees compensate the broker for services rendered. Mortgage points are optional fees you pay to the lender to reduce your interest rate. One point equals 1% of the loan amount. Both appear on your Loan Estimate but serve different purposes. You might pay both a broker fee and points on the same loan.

What happens to the broker fee if my loan doesn't close?

This depends on your agreement with the broker. Most brokers only collect fees at closing, meaning you owe nothing if the loan doesn't close. Some brokers charge application or processing fees upfront, which may be non-refundable. Review your fee agreement carefully before starting the application process.

Making an Informed Decision

Understanding mortgage broker charges empowers you to make confident decisions about your home financing in Seattle's competitive market. Whether you're a first-time buyer in Shoreline, a tech professional securing a jumbo loan in Bellevue, or an investor building a rental portfolio, clarity about compensation structures helps you evaluate broker relationships effectively.

The most successful mortgage experiences combine reasonable fees with exceptional service, strategic advice, and favorable loan outcomes. Focus on the total value package rather than simply seeking the lowest fee, and choose professionals who demonstrate transparency, expertise, and commitment to your long-term financial success.

Evaluate brokers based on their track record with loans similar to yours, their lender relationships and product access, their communication style and responsiveness, their understanding of your specific financial situation, and yes, their fee structure and overall cost competitiveness.

Understanding mortgage broker charges helps you budget accurately and choose the right professional partnership for your home financing needs. Keith Akada and the team at Mortgage Reel bring 25+ years of experience serving Seattle, Bellevue, Redmond, and Kirkland homebuyers with transparent pricing, strategic guidance, and proven execution in competitive markets. With expertise in qualifying stock compensation for tech professionals and the ability to close in as few as 9 business days, Keith delivers exceptional value backed by 750+ five-star reviews. Contact Mortgage Reel today to discuss your mortgage options and receive a clear, comprehensive fee breakdown tailored to your unique situation.