Navigating the mortgage landscape in competitive markets like Seattle, Bellevue, and Redmond requires expertise, strategic planning, and access to diverse financing options. A home finance broker serves as your advocate throughout the home buying journey, connecting you with appropriate loan programs while negotiating favorable terms on your behalf. Unlike loan officers who represent a single lender, brokers maintain relationships with multiple financial institutions, creating opportunities to compare rates, programs, and underwriting flexibility. This comprehensive guide explores how working with a home finance broker can streamline your purchase or refinance experience, particularly in high-cost housing markets where every basis point matters.

Understanding the Role of a Home Finance Broker

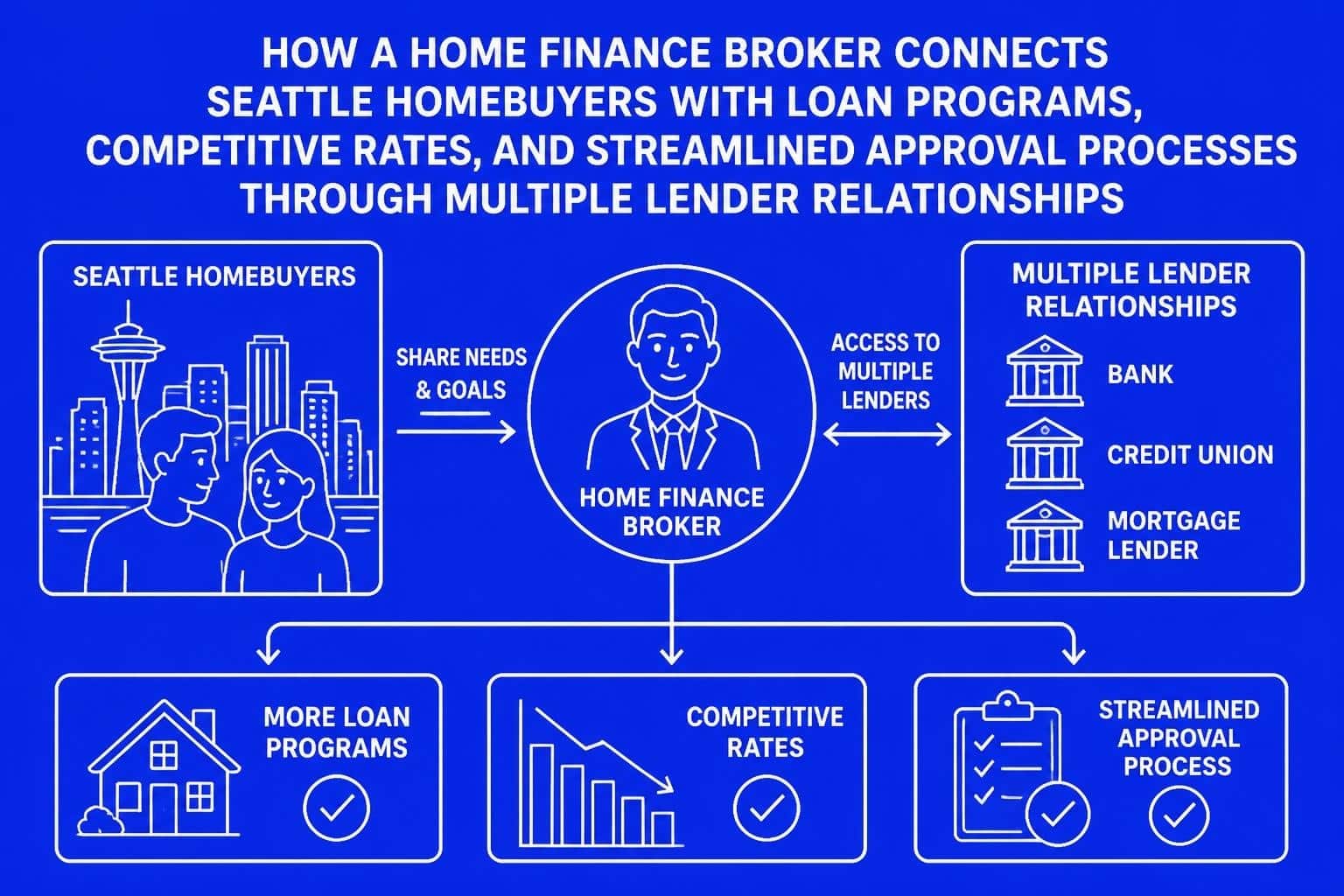

A home finance broker acts as an intermediary between borrowers and lending institutions, offering access to wholesale mortgage pricing that often surpasses what direct lenders advertise to retail customers. These professionals evaluate your financial profile, employment history, assets, and credit standing to identify loan products aligned with your unique circumstances.

How Brokers Differ from Direct Lenders

The distinction between brokers and direct lenders impacts your borrowing experience significantly. Banks and credit unions employ loan officers who exclusively offer their institution's products, creating inherent limitations in program variety and pricing flexibility. According to research on mortgage shopping, nearly half of borrowers fail to compare multiple offers, potentially costing thousands in unnecessary interest payments.

Key differences include:

- Product Access: Brokers connect borrowers with 20-50+ lenders, while direct lenders offer their proprietary programs only

- Rate Competition: Multiple lender relationships enable brokers to secure competitive pricing through wholesale channels

- Underwriting Flexibility: Different lenders maintain varying guidelines for credit overlays, debt-to-income ratios, and documentation requirements

- Specialized Programs: Brokers identify niche products for unique situations-jumbo loans for tech professionals, investor financing, or construction-to-permanent loans

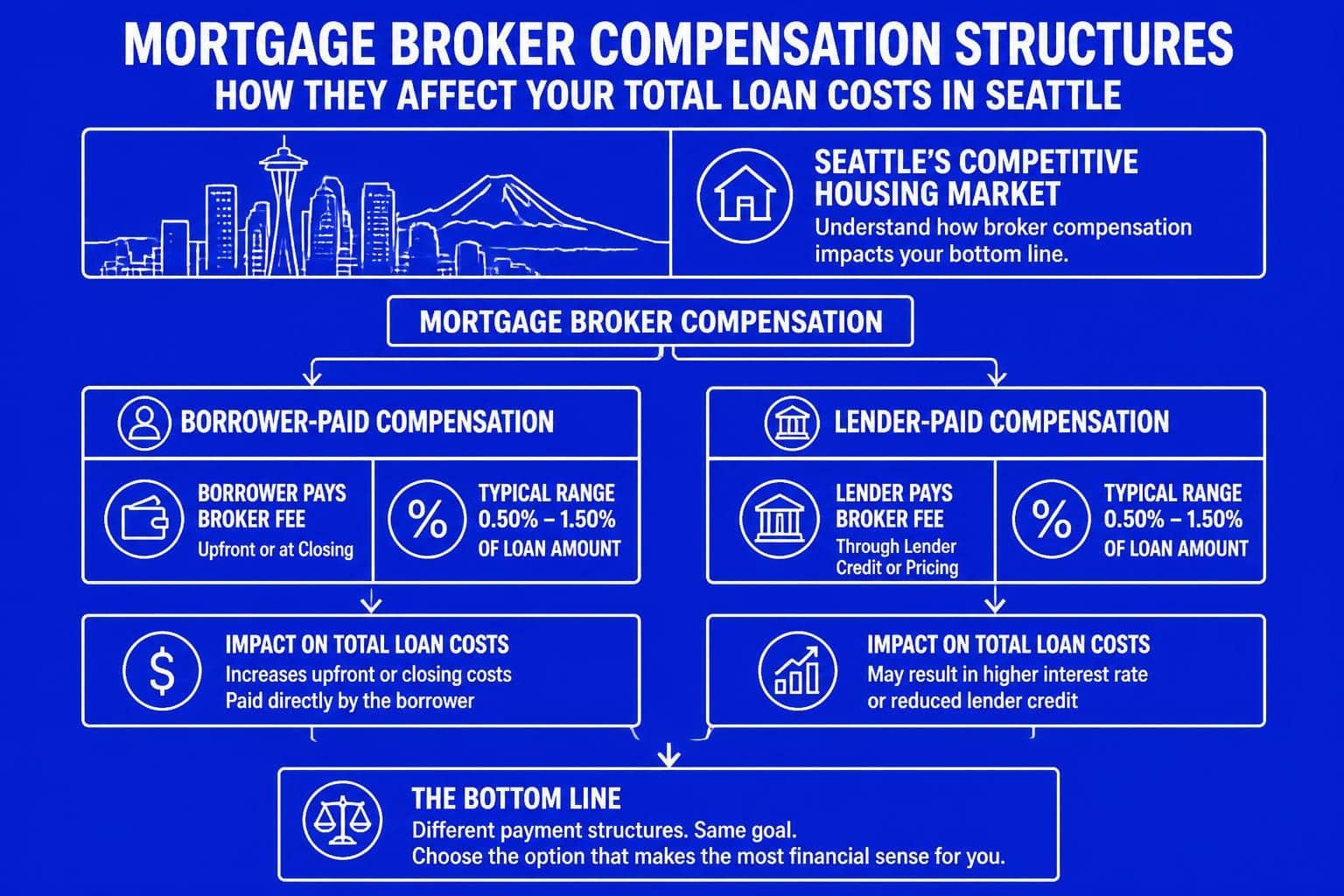

The Broker Compensation Model

Transparency in how your home finance broker earns compensation builds trust and ensures alignment with your financial interests. Brokers receive wholesale pricing from lenders and add a clearly disclosed origination fee or yield spread premium. Federal regulations require full transparency in mortgage disclosures, meaning you'll see exactly what your broker charges on your Loan Estimate within three business days of application.

| Compensation Type | Description | Typical Range |

|---|---|---|

| Origination Fee | Direct charge to borrower | 0.5% – 1.5% of loan amount |

| Lender Premium | Paid by lender for rate selection | 0.5% – 2.75% |

| Hybrid Model | Combination of both | Varies by scenario |

Most experienced brokers structure compensation to balance competitive pricing with sustainable business operations, often resulting in total costs comparable to or lower than direct lenders when factoring in interest rate differences.

Strategic Advantages in Seattle's Housing Market

Seattle's housing market presents unique challenges that make broker relationships particularly valuable. With median home prices consistently exceeding $800,000 and tech-driven competition creating multiple-offer scenarios, buyers need every advantage to succeed.

Navigating Jumbo Loan Requirements

Properties above the conforming loan limit of $806,500 in 2026 require jumbo financing, which demands specialized underwriting expertise. A knowledgeable home finance broker understands which lenders offer the most favorable jumbo terms for Seattle-area buyers, particularly those employed by Amazon, Microsoft, or Google who receive substantial stock compensation.

Jumbo loan considerations include:

- Reserve requirements often ranging from 6-12 months of housing payments

- Documentation standards for equity compensation, including RSUs and stock options

- Debt-to-income calculations that properly account for bonus income and equity vesting schedules

- Portfolio products that provide flexibility beyond agency guidelines

Tech professionals in Bellevue, Redmond, and Kirkland benefit significantly from brokers who specialize in qualifying complex income structures, maximizing purchasing power while maintaining competitive rates on jumbo home loans.

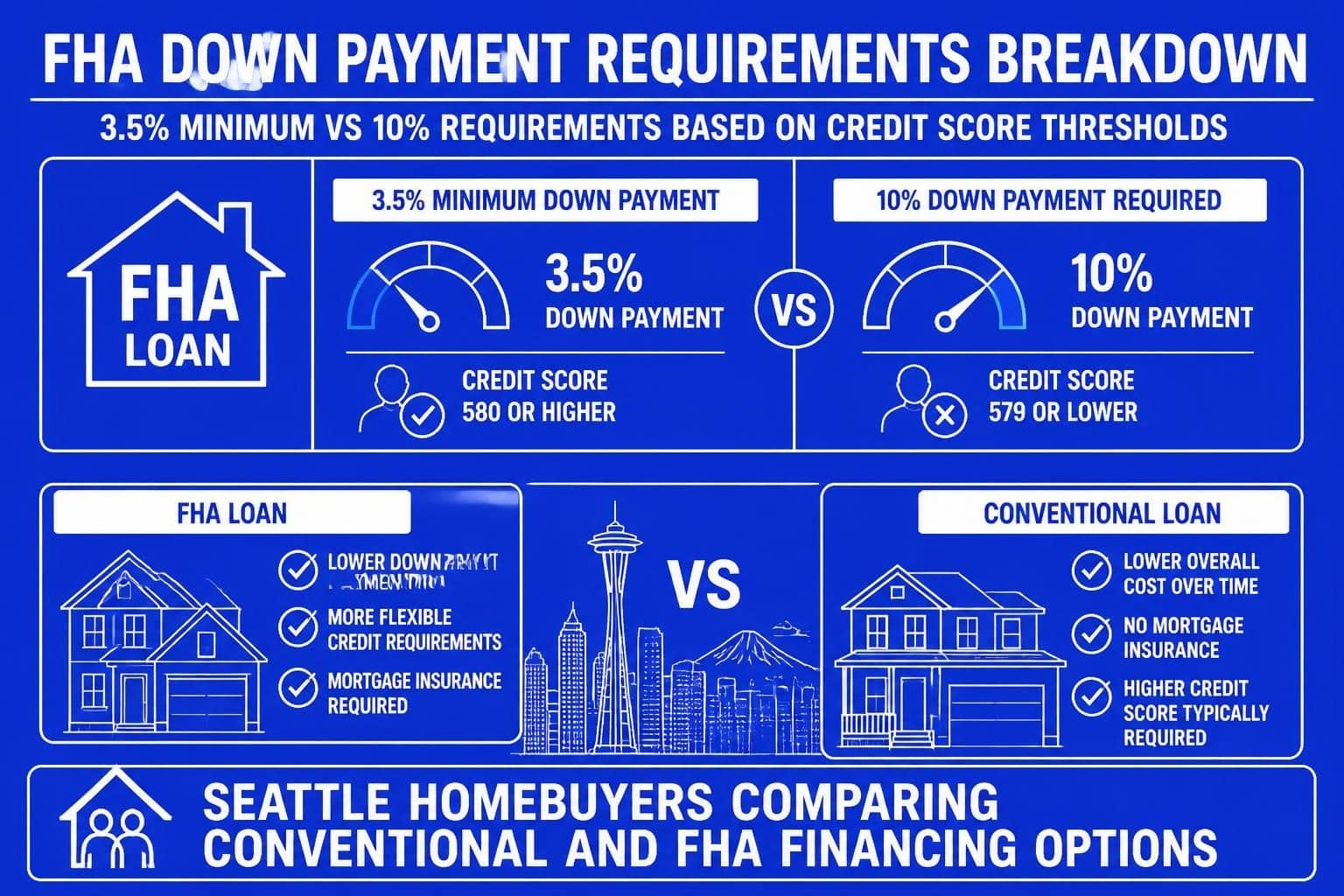

First-Time Buyer Program Access

First-time buyers in Seattle, Shoreline, and Lynnwood face substantial down payment challenges given elevated home prices. A home finance broker identifies programs that reduce upfront cash requirements while avoiding private mortgage insurance penalties when possible.

Programs worth exploring include:

- Conventional 97: 3% down payment with competitive rates for borrowers with strong credit

- FHA Loans: 3.5% down payment with flexible credit requirements

- VA Loans: Zero down payment for eligible veterans and service members

- HomeReady/Home Possible: Income-restricted programs with 3% down and reduced mortgage insurance

For detailed guidance on down payment strategies specific to Seattle's market, first-time buyers can benefit from understanding how gift funds, down payment assistance programs, and creative financing structures reduce barriers to homeownership.

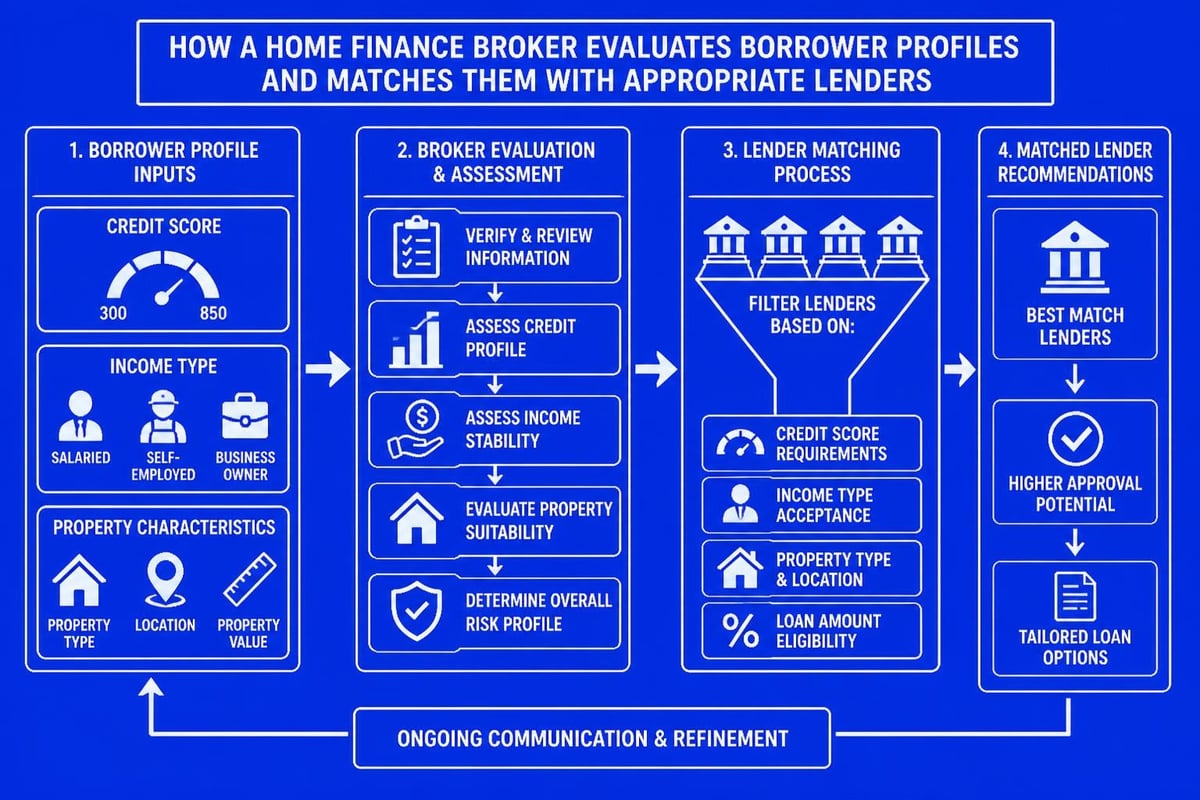

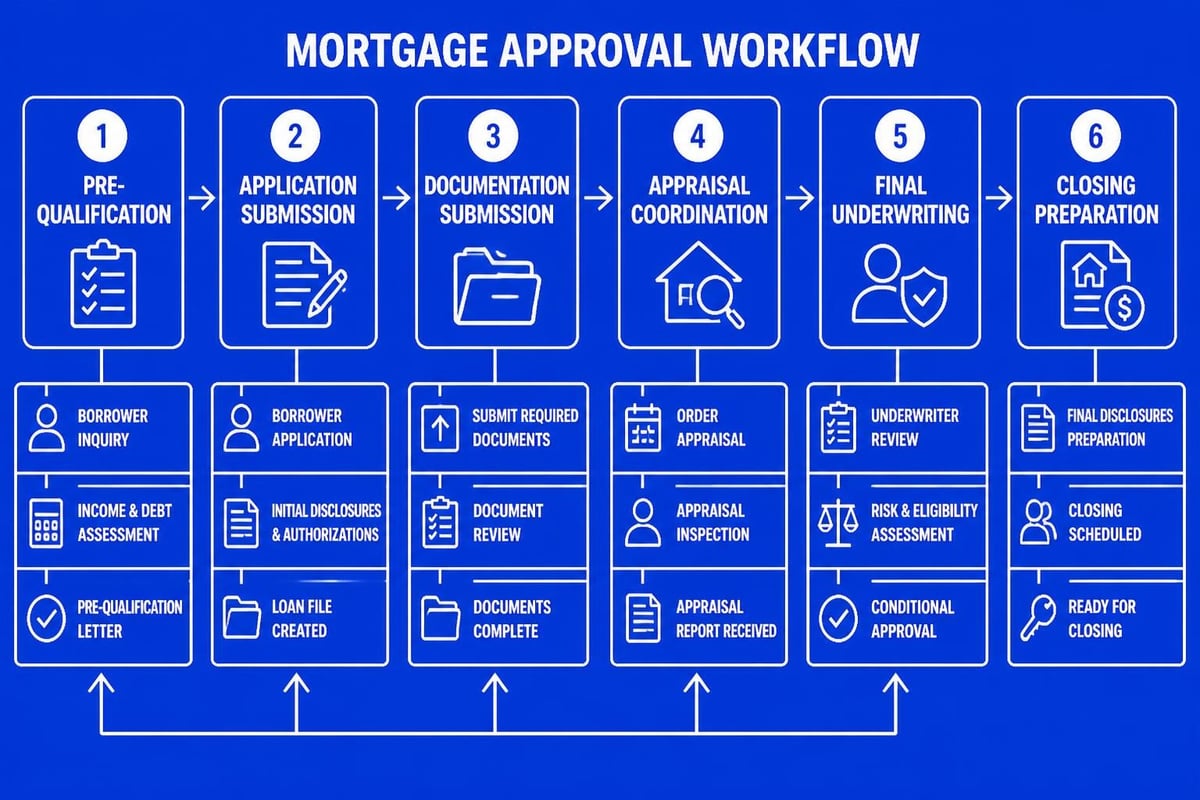

The Application and Approval Process

Understanding what happens after you submit your mortgage application helps set realistic expectations and enables proactive preparation. The timeline from application to closing typically spans 25-35 days, though experienced brokers with strong lender relationships can expedite qualified transactions.

Pre-Approval Strategy

Obtaining pre-approval before house hunting provides critical advantages in competitive markets. Your home finance broker evaluates documentation, runs credit, and secures conditional approval from specific lenders, strengthening your offer credibility.

Required documentation typically includes:

- Two years of W-2s and tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Explanation letters for credit inquiries, deposits, or employment gaps

- Stock compensation statements and vesting schedules for equity income

Tech professionals should prepare documentation showing RSU vesting schedules and historical stock sale patterns, as lenders apply varying qualification methods to equity compensation. Some lenders average the most recent two years, while others use more conservative calculations based on current vested shares.

Underwriting and Closing Timeline

After application submission, your file moves through several distinct phases that your home finance broker coordinates on your behalf.

| Phase | Timeline | Key Activities |

|---|---|---|

| Processing | Days 1-7 | Document collection, initial review, title order |

| Underwriting | Days 8-20 | Credit analysis, income verification, appraisal review |

| Conditional Approval | Days 15-25 | Address underwriter conditions, final documentation |

| Clear to Close | Days 25-30 | Final review, closing disclosure delivery, funding authorization |

Experienced brokers anticipate potential underwriting conditions and address them proactively, significantly reducing the likelihood of last-minute delays. For buyers working within tight timelines, understanding home loan approval time expectations helps coordinate inspection periods, appraisal scheduling, and closing dates effectively.

Evaluating Broker Credentials and Performance

Selecting the right home finance broker requires research beyond simple rate comparisons. Professional credentials, client reviews, and market specialization all contribute to successful outcomes.

Licensing and Regulatory Compliance

All mortgage brokers must maintain active licensing through the Nationwide Mortgage Licensing System (NMLS), which tracks disciplinary actions, licensing status, and professional history. While FINRA’s BrokerCheck focuses primarily on securities professionals, the NMLS Consumer Access portal provides similar verification for mortgage professionals.

Verify these credentials:

- Active NMLS license number

- State licensing in Washington

- No significant disciplinary history

- Professional designations (CRMS, CMB, etc.)

- Years of experience in mortgage origination

Transparency extends to fee disclosure as well. The Consumer Financial Protection Bureau emphasizes borrower protection through clear communication and ethical lending practices, making regulatory compliance a fundamental consideration.

Client Reviews and Testimonials

Past client experiences provide valuable insight into a broker's communication style, problem-solving capabilities, and execution consistency. Look for patterns across multiple review platforms rather than focusing on isolated testimonials.

Meaningful indicators include:

- Response time: How quickly does the broker address questions and concerns?

- Proactive communication: Does the broker anticipate issues or simply react to problems?

- Rate competitiveness: Do clients consistently mention securing favorable terms?

- Closing reliability: Did transactions close on time without unexpected delays?

- Complex scenario expertise: Can the broker navigate challenging income documentation or tight timelines?

Seattle's competitive market demands brokers who execute reliably under pressure, particularly when coordinating with listing agents, title companies, and appraisal management companies simultaneously.

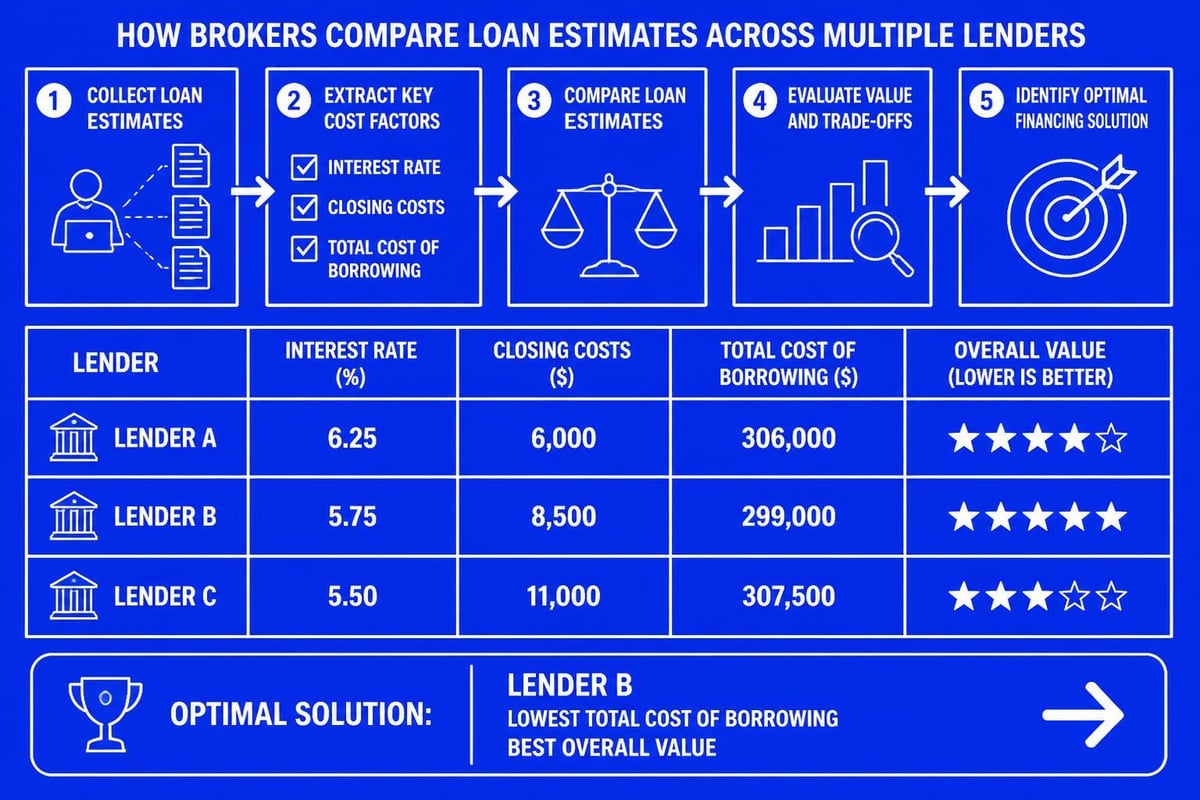

Rate Shopping and Lender Comparison

One of the most valuable services a home finance broker provides is comprehensive rate shopping across their lender network. Rather than contacting multiple institutions individually-each triggering credit inquiries and application processes-working with a broker consolidates this research.

Understanding Rate Quotes

Mortgage rates fluctuate based on lock period, loan-to-value ratio, credit score, property type, and occupancy status. When comparing quotes, ensure you're evaluating equivalent scenarios.

Critical comparison factors:

- Lock period: 30-day versus 45-day or 60-day rate locks

- Points and credits: Upfront costs to buy down the rate or lender credits to offset closing costs

- Annual Percentage Rate (APR): Total borrowing cost including fees

- Loan program: Conventional versus FHA versus jumbo pricing structures

According to information from the American Bankers Association, understanding these variables enables more informed decision-making beyond simply selecting the lowest quoted rate.

When to Lock Your Rate

Timing your rate lock requires market awareness and strategic planning. Your home finance broker monitors interest rate trends and recommends optimal lock timing based on your purchase timeline and market conditions.

Lock strategies include:

- Float until contract: Wait for purchase agreement ratification before locking

- Lock at application: Secure current rates immediately if favorable

- Float-down options: Pay for the right to lock a lower rate if markets improve

- Extended locks: Lock for 60-75 days on new construction with delayed closings

Mill Creek and Lake Forest Park buyers purchasing new construction particularly benefit from extended lock options, as construction delays can push closing dates beyond standard 30-day lock periods.

Specialized Financing Scenarios

Experienced home finance brokers add greatest value when navigating complex financing scenarios that fall outside standard agency guidelines. Whether you're self-employed, investing in rental properties, or purchasing a unique property type, specialized expertise matters.

Investment Property Financing

Rental property investors in Everett, Lynnwood, and surrounding areas require financing solutions that differ substantially from primary residence mortgages. Investment property loans typically demand higher down payments (15-25%), charge premium interest rates, and require more stringent qualification criteria.

Investment financing considerations:

- Rental income qualification methodologies

- Reserve requirements (typically 6-12 months)

- Property management expense calculations

- Portfolio lending for experienced investors with multiple properties

- DSCR (Debt Service Coverage Ratio) loans using rental income only

For detailed guidance on conventional loan for investment property requirements, experienced brokers help investors structure acquisitions that maximize cash flow while minimizing tax liability.

Self-Employed Borrower Solutions

Self-employed borrowers face additional documentation requirements and income calculation methodologies. Unlike W-2 employees with straightforward income verification, business owners must provide tax returns showing consistent earnings after business expense deductions.

Lenders typically average two years of tax returns, adding back non-cash deductions like depreciation. A skilled home finance broker knows which lenders offer the most favorable self-employment income calculations and which programs provide alternatives to traditional tax return analysis.

Strategic Refinancing Opportunities

While purchase transactions generate excitement, refinancing represents a significant portion of mortgage broker activity. Whether capturing lower interest rates, eliminating mortgage insurance, or consolidating debt, strategic refinancing produces measurable financial benefits.

Rate-and-Term Refinancing

The most straightforward refinance scenario involves replacing your current mortgage with a new loan featuring better terms-typically a lower interest rate, shorter loan term, or both. When rates decline significantly from your original mortgage, refinancing can reduce monthly payments substantially or accelerate equity building through shorter amortization.

Refinancing benefits:

- Monthly payment reduction through lower rates

- Interest savings over the loan life

- Accelerated payoff through 15-year or 20-year terms

- Elimination of private mortgage insurance once reaching 20% equity

For comprehensive strategies on paying off your mortgage faster, consider both refinancing to shorter terms and making additional principal payments strategically.

Cash-Out Refinancing Strategies

Seattle homeowners who have built substantial equity may benefit from cash-out refinancing to fund renovations, consolidate high-interest debt, or finance investment opportunities. A home finance broker evaluates whether accessing home equity makes financial sense given current market rates and your specific circumstances.

Responsible cash-out refinancing requires:

- Sufficient equity remaining after the transaction (typically 80% loan-to-value maximum)

- Documented purpose for funds that provides financial benefit

- Interest rate competitive with your current mortgage

- Debt-to-income ratio within acceptable limits including new loan payment

Working Effectively with Your Broker

Maximizing the value of your home finance broker relationship requires proactive communication, organized documentation, and realistic expectations. The most successful borrower-broker partnerships involve mutual respect, transparency, and collaboration.

Documentation Organization

Gathering required documents before beginning your search accelerates the approval process significantly. Create digital folders containing:

- Tax returns (personal and business if self-employed) for the past two years

- W-2s and recent pay stubs

- Bank statements for all accounts showing two months of activity

- Investment account statements

- Retirement account statements

- Documentation for non-wage income (rental income, dividends, trust distributions)

Tech professionals should include RSU documentation, stock option agreements, and vesting schedules. Your broker uses this information to calculate qualifying income accurately before submitting to underwriting.

Communication Expectations

Establishing communication preferences early prevents frustration during the transaction. Discuss your preferred contact methods (email, text, phone), response time expectations, and update frequency with your home finance broker at the initial consultation.

Professional brokers maintain proactive communication throughout the process:

- Application acknowledgment within 24 hours

- Regular status updates at key milestones

- Same-day responses to urgent questions

- Pre-emptive notification of potential issues or delays

- Coordination updates involving other transaction parties

Market-Specific Considerations for Greater Seattle

Each market within the Greater Seattle area presents unique characteristics that influence financing approaches. Understanding these nuances helps you and your home finance broker develop appropriate strategies.

Seattle and Bellevue

Core Seattle and Bellevue markets command premium pricing with median values frequently exceeding $1 million in desirable neighborhoods. Buyers here typically require jumbo financing, substantial reserves, and strong credit profiles.

Competition remains intense, particularly for well-located properties near major employers. Pre-approval with verified documentation and quick closing capabilities provide distinct advantages when competing against multiple offers.

Redmond and Kirkland

These eastside communities attract significant tech worker demand given proximity to Microsoft, Google, and other major employers. Properties here frequently involve buyers with complex compensation structures requiring specialized income qualification expertise.

Your mortgage broker in Seattle should understand how different lenders calculate RSU income, bonus eligibility, and stock option exercises when determining maximum loan amounts.

Shoreline, Lake Forest Park, and Mill Creek

These markets offer relatively more accessible price points while maintaining excellent school districts and community amenities. First-time buyers and growing families often target these areas, requiring expertise in lower down payment programs and creative financing solutions.

Down payment assistance programs, conventional loans with as little as 3% down, and FHA financing all provide viable paths to homeownership in these communities.

Lynnwood and Everett

North-end markets provide additional value relative to Seattle proper while maintaining reasonable commute access. These areas attract diverse buyer profiles including first-time buyers, move-up purchasers, and investors seeking rental properties.

For comprehensive information on home buying strategies across various price points and market conditions, experienced brokers tailor approaches to individual circumstances rather than applying one-size-fits-all solutions.

Technology and Process Efficiency

Modern mortgage origination leverages technology to streamline documentation collection, communication, and closing processes. Your home finance broker's technological capabilities directly impact transaction efficiency and borrower convenience.

Digital Application Platforms

Contemporary mortgage applications occur entirely online, with secure portals enabling document uploads, electronic signatures, and real-time status tracking. These platforms eliminate unnecessary paperwork while maintaining robust security protocols protecting sensitive financial information.

Benefits include:

- 24/7 access to your application status

- Secure document transmission

- Electronic signature capabilities

- Automated task reminders

- Mobile-friendly interfaces

Automated Underwriting Systems

Most conventional and government loans utilize automated underwriting systems (AUS) that provide preliminary approval within minutes of data submission. These systems evaluate credit, income, assets, and property characteristics against agency guidelines, producing approval decisions with specific documentation conditions.

Understanding AUS results helps set realistic expectations. Your broker interprets findings, addresses identified concerns, and structures the application to maximize approval probability.

Common Mistakes to Avoid

Even experienced borrowers make mistakes during the mortgage process that jeopardize approval or create unnecessary complications. Awareness of these pitfalls enables proactive avoidance.

Credit and Financial Missteps

Avoid these common errors:

- Opening new credit accounts during the application process

- Making large unexplained deposits to bank accounts

- Changing employment or income structure

- Co-signing loans for friends or family members

- Missing payments on existing credit obligations

Your home finance broker provides guidance on maintaining financial stability throughout the approval process, but borrowers must exercise discipline in avoiding actions that raise underwriter concerns.

Communication Breakdowns

Failure to respond promptly to documentation requests, condition clarifications, or status inquiries creates delays and potential rate lock expiration issues. Treat your mortgage application with the urgency it deserves, particularly in time-sensitive purchase scenarios.

For additional context on where to obtain financing and comparing various lending sources, resources like this guide on home loan sources provide helpful comparisons between banks, credit unions, and brokers.

Future-Proofing Your Mortgage Strategy

Strategic mortgage decisions consider not only immediate affordability but long-term financial implications. Your home finance broker helps evaluate tradeoffs between rate, term, payment stability, and flexibility.

Fixed versus Adjustable Rate Mortgages

In 2026's rate environment, the choice between fixed and adjustable rate mortgages (ARMs) requires careful analysis. Fixed rates provide payment certainty over the entire loan term, while ARMs offer initially lower rates that adjust after specified periods.

| Loan Type | Best For | Key Consideration |

|---|---|---|

| 30-Year Fixed | Long-term homeowners, budget certainty | Highest rate, lowest payment |

| 15-Year Fixed | Equity building, interest savings | Higher payment, significant interest savings |

| 7/1 ARM | 5-7 year ownership timeline | Lower initial rate, adjustment risk |

| 5/1 ARM | Short-term ownership, relocation likelihood | Lowest initial rate, highest adjustment risk |

Prepayment Strategies

Even with a 30-year mortgage, strategic principal prepayment accelerates equity building and reduces total interest paid. Your broker can illustrate the impact of various prepayment schedules on loan amortization and long-term costs.

Consider prepayment approaches like:

- Biweekly payment programs (26 half-payments annually equals 13 full payments)

- Annual lump-sum principal payments from bonuses or tax refunds

- Rounding up monthly payments to the nearest hundred dollars

- Refinancing to a 15-year or 20-year term when financially feasible

Working with a qualified home finance broker provides access to diverse loan programs, competitive pricing, and expert guidance throughout the mortgage process. From initial consultation through closing, professional brokers streamline what can otherwise be an overwhelming experience, particularly in competitive markets requiring quick decisions and flawless execution. Keith Akada and the team at Mortgage Reel bring over 25 years of experience serving Seattle, Bellevue, Redmond, Kirkland, and surrounding communities, specializing in complex income qualification for tech professionals and delivering transparent, education-focused guidance backed by 750+ five-star reviews. Whether you're purchasing your first home, upgrading to accommodate a growing family, or refinancing to optimize your current mortgage, experienced local expertise makes a measurable difference in both process efficiency and long-term financial outcomes.