Finding good mortgage brokers can transform your home buying or refinancing experience from overwhelming to manageable. In Seattle's competitive housing market, where bidding wars and quick closings are common, working with an experienced broker who understands local market dynamics and has access to diverse lending options provides a significant advantage. Whether you're a first-time buyer exploring first-time homebuyer programs or a tech professional navigating RSU income qualification, the right broker becomes your advocate throughout the entire process.

What Distinguishes Good Mortgage Brokers From Average Ones

Good mortgage brokers bring more than just loan access to the table. They combine market knowledge, product expertise, and client advocacy in ways that fundamentally improve your borrowing experience.

Licensing and Professional Credentials

Every legitimate mortgage broker must hold proper state licensing. In Washington State, this means an active Nationwide Mortgage Licensing System (NMLS) number and compliance with continuing education requirements. Good mortgage brokers maintain spotless regulatory records and often pursue additional certifications that demonstrate commitment to professional development.

Beyond basic licensing, look for brokers who specialize in your specific needs. If you're purchasing in Shoreline or Lake Forest Park, a broker with deep knowledge of local lending programs and market conditions brings measurable value. For jumbo loan scenarios common in Bellevue and Kirkland, experience with high-balance financing becomes essential.

Key credentials to verify:

- Active NMLS license

- State-specific licensing

- Years of continuous industry experience

- Specialization in your loan type or situation

- Professional memberships (National Association of Mortgage Brokers, local chapters)

Lender Network Breadth and Quality

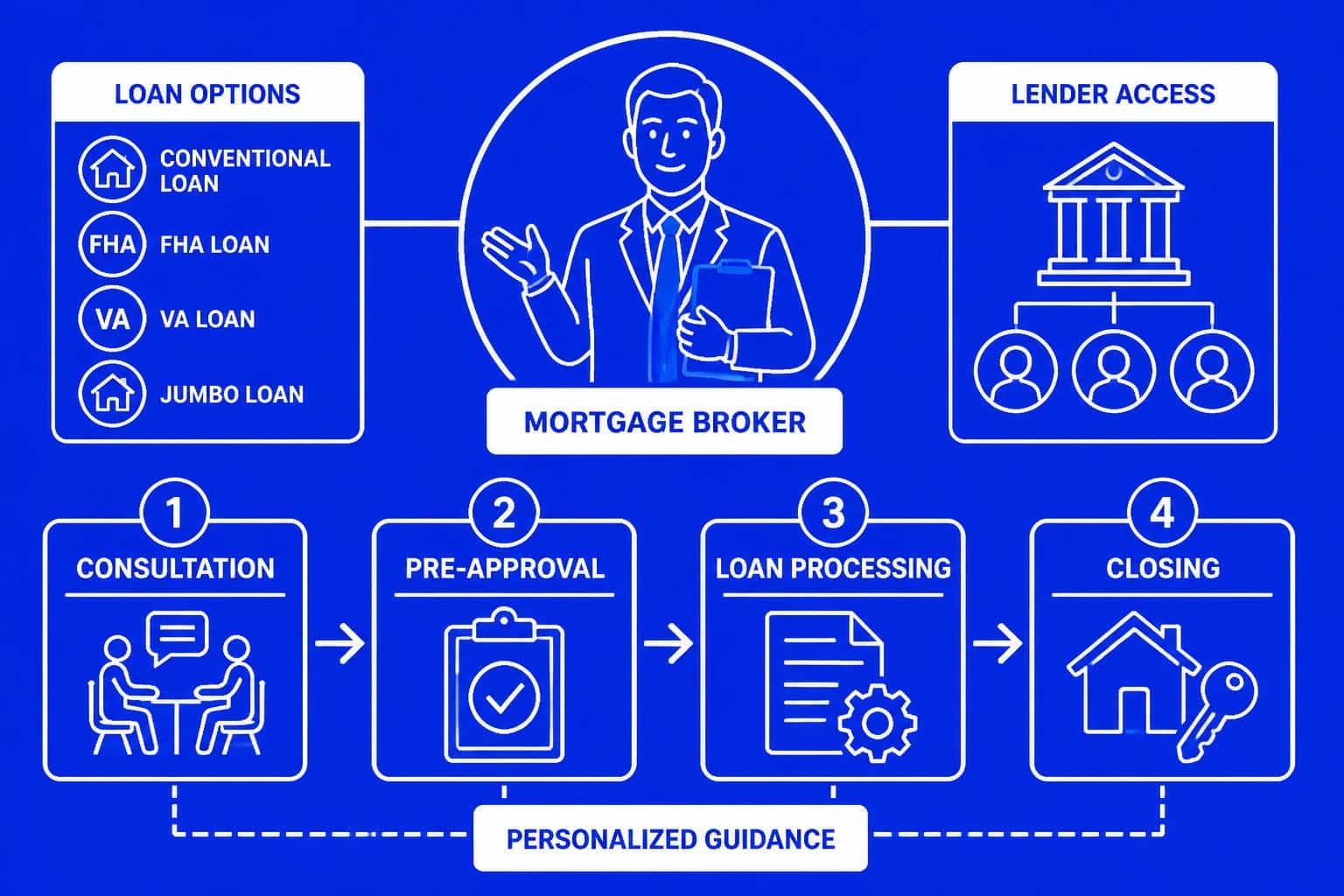

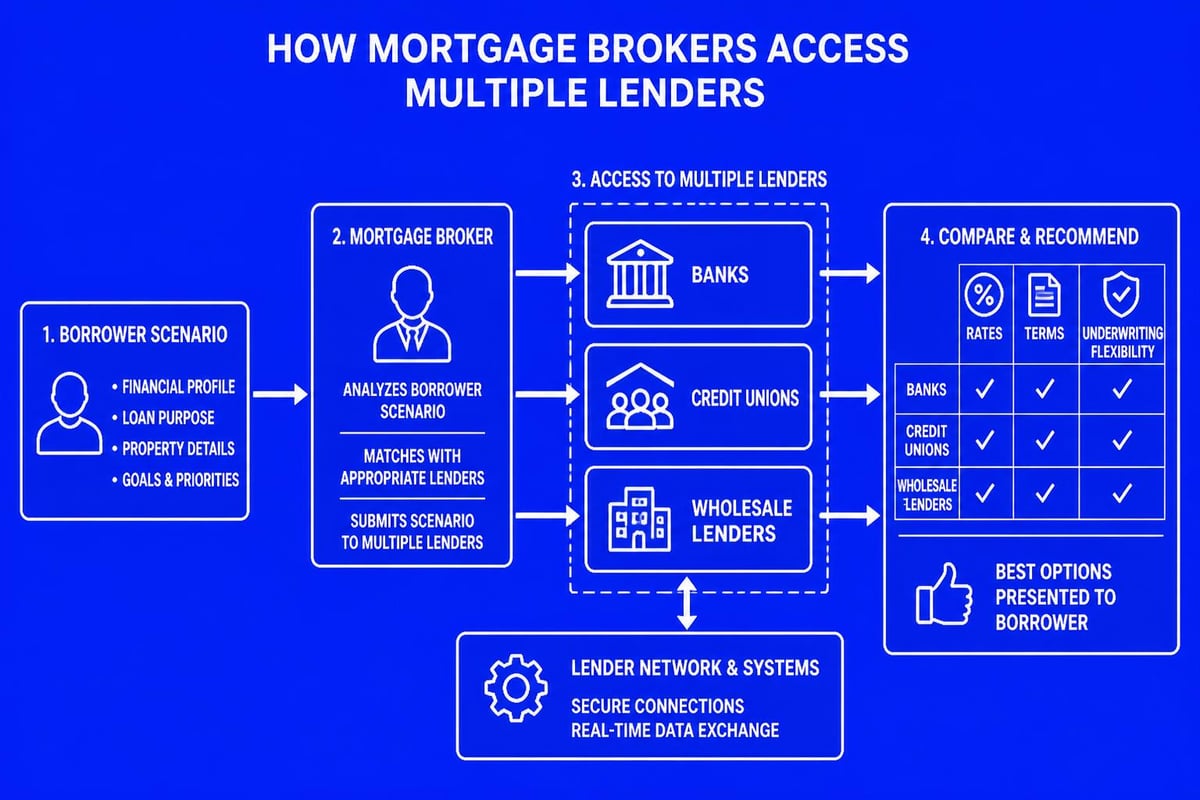

One primary advantage of working with mortgage brokers versus direct lenders is access to multiple lending sources. Understanding what mortgage brokers do reveals that they act as intermediaries between borrowers and lenders, shopping your scenario across their network to find optimal pricing and terms.

Good mortgage brokers maintain relationships with 20-40+ lenders representing diverse lending philosophies. This breadth matters because different lenders excel in different scenarios. A bank that offers competitive conventional rates might struggle with self-employment income documentation, while a specialized lender handles complex compensation structures from Amazon or Microsoft with ease.

| Lender Type | Typical Strengths | Best For |

|---|---|---|

| National Banks | Jumbo loans, relationship pricing | High-income borrowers, existing customers |

| Credit Unions | Member benefits, lower fees | First-time buyers, modest loan amounts |

| Wholesale Lenders | Competitive pricing, flexible guidelines | Unique scenarios, broker-only programs |

| Portfolio Lenders | Custom underwriting, local focus | Non-traditional income, investment properties |

The quality of these relationships determines how effectively your broker can advocate for exceptions, expedite underwriting, and secure pricing adjustments. In Seattle's fast-moving market, these relationships often mean the difference between winning and losing in competitive offer situations.

Communication Standards That Define Excellence

Transaction transparency separates good mortgage brokers from those who leave clients confused and anxious. Clear, proactive communication builds trust and enables better decision-making throughout your loan process.

Response Time and Availability

In competitive Seattle neighborhoods like Capitol Hill or Montlake, where properties receive multiple offers within days, broker responsiveness directly impacts your success. Good mortgage brokers establish clear communication protocols from your first conversation and maintain them through closing.

Expect responses to urgent questions within two hours during business days. Non-urgent inquiries should receive attention within 24 hours. Brokers who consistently exceed these standards demonstrate the organizational systems and staffing necessary to serve clients effectively.

Communication benchmarks:

- Initial consultation scheduled within 48 hours of inquiry

- Pre-approval letters delivered within 24 hours of application

- Regular status updates without prompting

- After-hours availability for time-sensitive situations

- Clear escalation paths for complex questions

Educational Approach vs. Sales Tactics

Good mortgage brokers prioritize education over persuasion. Rather than pushing specific products, they explain how different loan structures align with your financial goals and risk tolerance. This educational approach proves particularly valuable when comparing mortgage broker advantages versus direct bank lending.

During initial consultations, notice whether your broker asks probing questions about your financial situation, homeownership timeline, and long-term goals before recommending products. Those who lead with solutions rather than questions often lack the diagnostic discipline that characterizes true expertise.

When evaluating conventional loans, FHA financing, or VA benefits, good mortgage brokers outline specific pros and cons relevant to your situation. They explain rate-term tradeoffs, discuss impact of credit score ranges, and project how different down payment amounts affect monthly obligations and long-term costs.

Evaluating Track Record and Market Reputation

Past performance provides the most reliable predictor of future results. Good mortgage brokers accumulate verifiable evidence of client satisfaction and successful transactions over years of consistent service.

Review Quality and Quantity Across Platforms

Online reviews offer unfiltered insights into broker performance, but interpretation requires nuance. A broker with 750+ five-star reviews across Google, Zillow, Redfin, Yelp, and other platforms demonstrates sustained excellence that survives diverse client expectations and market conditions.

Look beyond star ratings to review content. Good mortgage brokers earn detailed testimonials that describe specific value delivered: complex scenarios solved, exceptional communication, competitive pricing, or creative problem-solving. Generic praise ("great service!") carries less weight than specific examples of expertise.

Review analysis checklist:

- Total review volume (100+ reviews suggests established practice)

- Recent reviews (activity within the past three months)

- Detailed responses to negative feedback

- Specific mentions of process elements (communication, problem-solving, pricing)

- Reviews across multiple platforms (demonstrates legitimacy)

Finding the right mortgage broker involves verifying credentials through independent sources, not just trusting advertised claims. Check NMLS Consumer Access for licensing history, regulatory actions, and employment chronology.

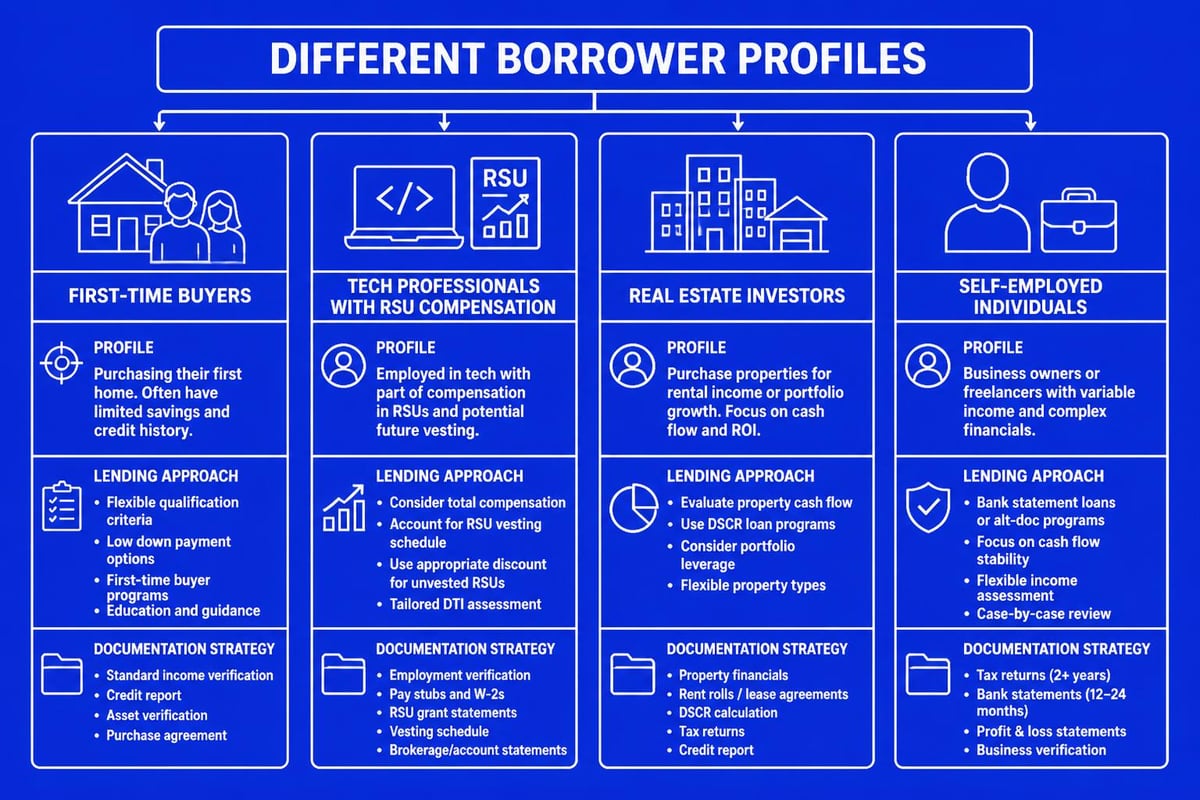

Specialization in Your Borrower Profile

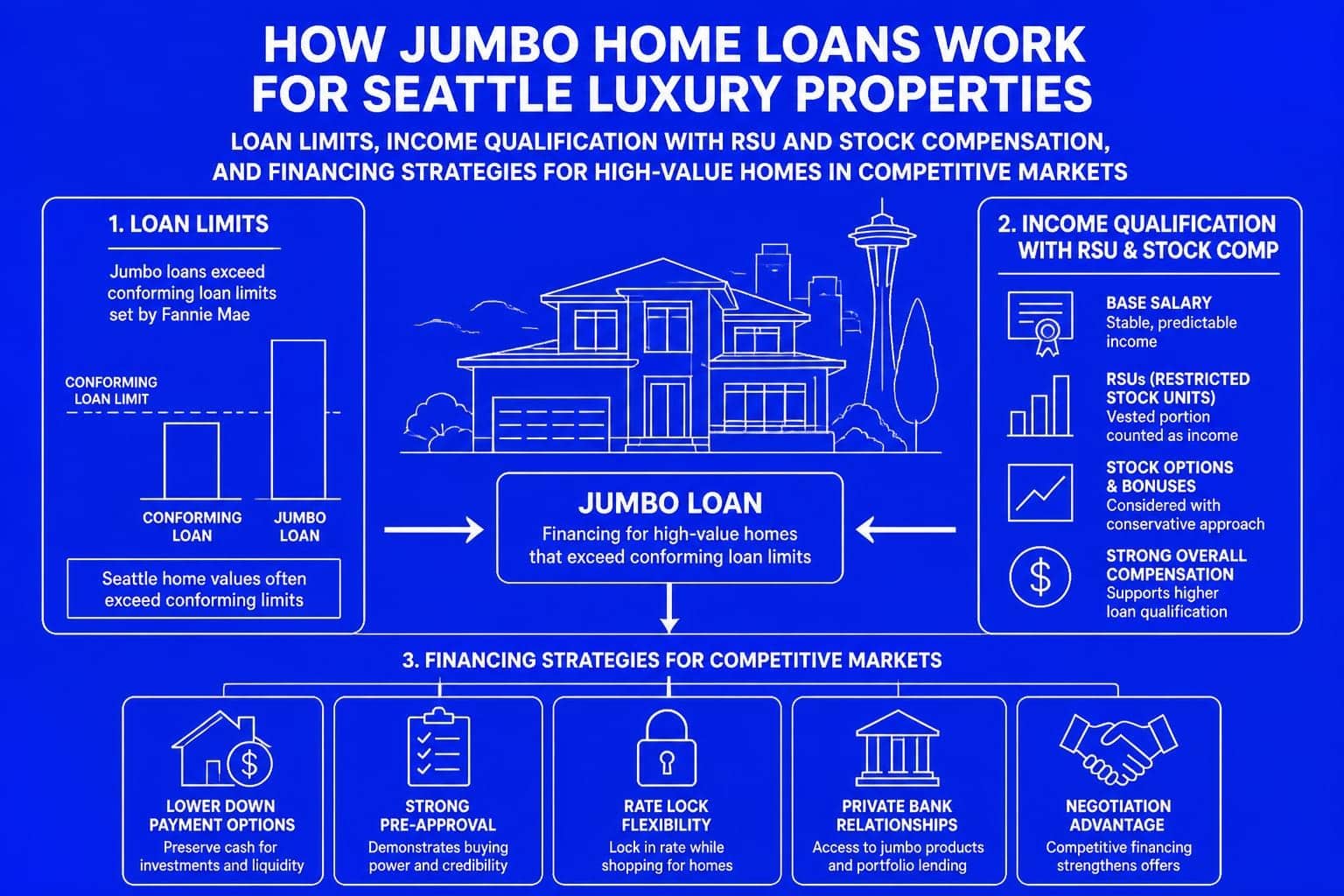

Mortgage financing spans enormous diversity. First-time buyers in Lynnwood face different challenges than seasoned investors purchasing Capitol Hill properties or tech professionals managing jumbo loan scenarios. Good mortgage brokers develop deep expertise in specific borrower segments rather than claiming universal competence.

For Seattle-area technology workers, RSU and stock option qualification represents a specialized skill. Many lenders discount or exclude equity compensation when calculating qualifying income. Brokers experienced with Microsoft, Amazon, Google, and other local employers understand which lenders offer favorable treatment of these income sources, potentially increasing buying power by hundreds of thousands of dollars.

Self-employed borrowers benefit from brokers who maintain relationships with lenders offering bank statement programs or alternative documentation paths. Real estate investors need access to portfolio lending and experience with DSCR (debt service coverage ratio) qualification methods.

Strategic Guidance Beyond Rate Shopping

While competitive pricing matters, good mortgage brokers deliver value that extends far beyond interest rate comparison. Strategic counsel regarding loan structure, timing, and financial positioning often saves more money than marginal rate differences.

Loan Structure Optimization

Cookie-cutter loan recommendations rarely serve borrowers optimally. Good mortgage brokers analyze how different structures affect both immediate affordability and long-term wealth building. This analysis considers factors like expected homeownership duration, career trajectory, and refinancing probability.

Consider a tech professional with substantial equity compensation. A broker might recommend a jumbo loan with 10% down rather than the traditional 20%, preserving liquidity for RSU tax obligations while maintaining competitive pricing through lender-paid mortgage insurance structures. This approach requires understanding both mortgage products and client financial ecosystems.

Similarly, mortgage recast strategies allow borrowers to make large principal payments and recalculate monthly payments without full refinancing. Good mortgage brokers proactively discuss these options during origination, ensuring loan selection that accommodates future lump-sum applications from bonuses, inheritance, or stock vesting events.

| Strategy | Best For | Typical Benefit |

|---|---|---|

| Lower down payment + investment | High-income growth trajectory | 6-8% annual return differential |

| Rate buydown | Certain long-term ownership | $15K-$30K lifetime savings |

| ARM vs. fixed analysis | Mobile professionals | 0.5-1.0% rate advantage |

| Recast-friendly products | Bonus/RSU recipients | Payment reduction without refinance cost |

Market Timing and Rate Lock Strategy

Interest rate volatility creates both opportunity and risk. Good mortgage brokers monitor rate movements and advise on optimal lock timing based on your specific closing timeline and risk tolerance. Understanding how long mortgage approval takes helps inform these timing decisions.

During volatile periods, float-down provisions and extended lock options provide flexibility while managing risk. Brokers should explain these options clearly, including costs and conditions, enabling informed decisions rather than making unilateral choices.

For buyers in Mill Creek or Everett competing in multiple-offer situations, pre-approval strength matters enormously. Good mortgage brokers structure pre-approvals that demonstrate financial capacity while protecting privacy, often including strategies that help buyers win bidding wars through enhanced credibility and faster closing capabilities.

Red Flags and Warning Signs to Avoid

Identifying what makes good mortgage brokers excellent requires equal attention to behaviors that signal incompetence or misconduct. Certain warning signs should immediately disqualify a broker from consideration.

Unrealistic Promises and Guarantee Claims

No ethical broker guarantees approval before reviewing documentation or promises rates significantly below current market levels. These tactics attract applicants but inevitably lead to disappointment when reality emerges.

Good mortgage brokers set realistic expectations from initial conversations. They explain that pre-qualification and pre-approval represent different commitment levels, outline documentation requirements upfront, and avoid creating false urgency through artificial scarcity claims.

Immediate disqualifiers:

- Guaranteed approval without documentation review

- Rates more than 0.5% below competing quotes without clear explanation

- Pressure to submit applications immediately

- Reluctance to provide written estimates

- Vague answers about fees or lender identity

- Requests for unusual upfront payments

Lack of Transparency on Compensation

Broker compensation structures vary significantly. Some receive lender-paid compensation, others charge borrower-paid origination fees, many use hybrid approaches. None of these models inherently indicates superiority, but lack of transparency signals potential conflicts of interest.

Good mortgage brokers explain their compensation clearly and discuss how it might influence product recommendations. They also demonstrate that recommended solutions align with your stated goals regardless of compensation differences across lenders. Choosing between mortgage brokers and direct lenders requires understanding these compensation dynamics.

When working with real estate professionals like Wendy Dean, Esq. Realtor and Associate Broker, mortgage brokers should coordinate seamlessly while maintaining clear professional boundaries. Undisclosed referral relationships or pressure to work with specific service providers warrant scrutiny.

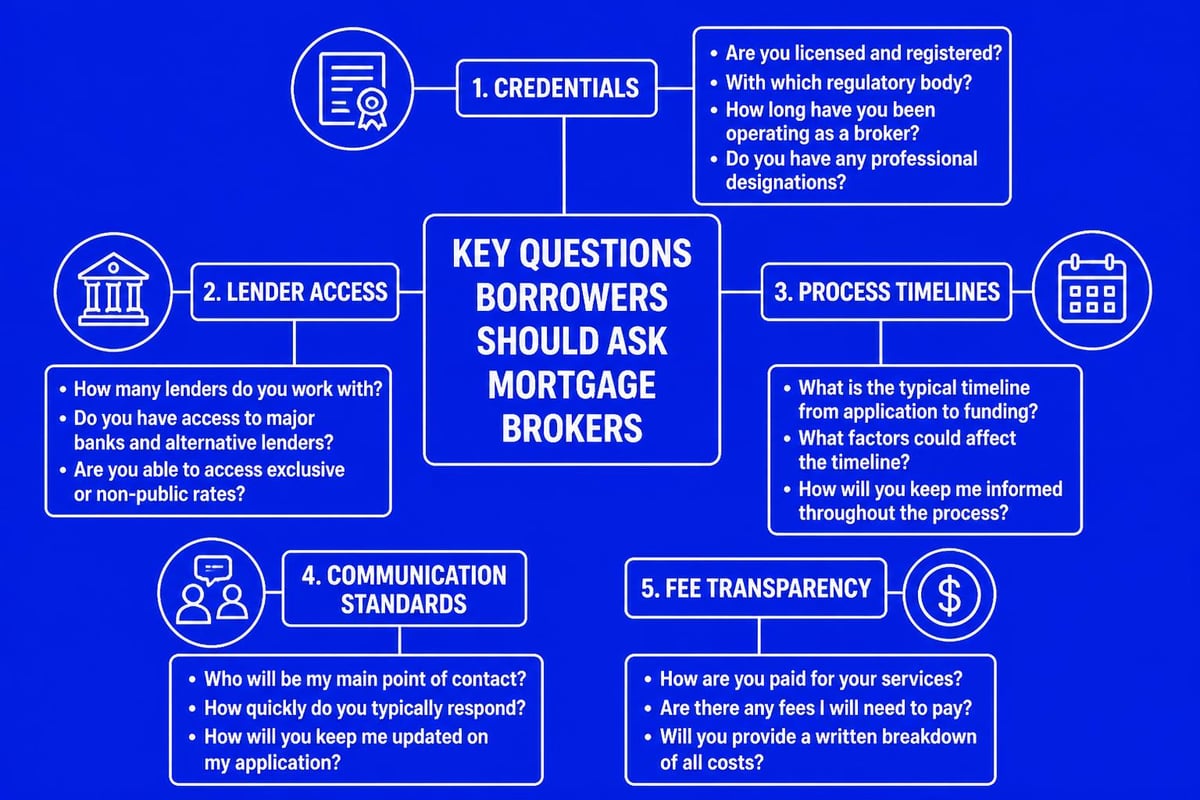

Questions to Ask During Broker Selection

Your initial broker consultations should function as mutual interviews. Good mortgage brokers welcome informed questions and provide substantive answers that demonstrate expertise and build confidence.

Credential and Experience Verification

Start with foundational questions that establish qualifications and specialization. Request NMLS numbers and verify licensing independently through the Nationwide Mortgage Licensing System database. This simple step confirms regulatory compliance and reveals any disciplinary history.

Essential credential questions:

- How long have you been originating loans in Washington State?

- What percentage of your business comes from borrowers with profiles similar to mine?

- Which lenders in your network excel with scenarios like mine?

- How many transactions do you personally close monthly?

- What continuing education or specializations have you pursued recently?

These questions reveal whether a broker possesses relevant experience or attempts to serve all markets generically. For Snohomish County home loans or specialized products, geographic and product expertise both matter.

Process and Communication Expectations

Establishing clear process expectations prevents misunderstandings and reveals organizational capability. Good mortgage brokers maintain documented workflows that ensure consistent execution across dozens of simultaneous transactions.

Ask about typical timelines from application to clear-to-close status. While variables affect every transaction, experienced brokers provide realistic ranges and explain common delay causes. Capabilities like 9-business-day closings require exceptional coordination between brokers, processors, underwriters, and closing agents.

Communication preferences vary among borrowers. Some want daily updates, others prefer milestone-based contact. Good mortgage brokers adapt to client preferences while maintaining proactive communication about issues requiring attention or decisions.

Fee Structure and Cost Comparison

Transparent fee discussion separates professional brokers from those who obscure costs through confusing explanations. Request Loan Estimates from multiple brokers to enable direct comparison, but understand that lowest cost doesn't automatically mean best value.

Good mortgage brokers explain each fee component: origination charges, third-party costs, prepaid expenses, and escrow requirements. They clarify which costs they control versus those determined by external parties. When discussing how to lower mortgage payments, comprehensive cost analysis proves essential.

Compare total monthly payment obligations and cash-to-close requirements across different scenarios. A slightly higher rate with lower closing costs might optimize cash preservation for buyers stretching to afford their target price range. Conversely, buyers planning long-term ownership often benefit from higher upfront costs that secure lower rates.

Technology and Process Efficiency Indicators

Modern mortgage origination increasingly relies on technology that improves accuracy, speed, and borrower experience. Good mortgage brokers invest in systems that streamline processes while maintaining personal service quality.

Digital Application and Document Management

Secure online application portals with document upload capabilities protect sensitive information while accelerating processing. Mobile-responsive systems enable borrowers to complete tasks conveniently rather than scheduling office visits or managing paper files.

Good mortgage brokers use automated tracking systems that provide real-time visibility into application status, pending tasks, and projected timelines. These systems reduce status-check calls while keeping borrowers informed through their preferred channels.

Electronic signature capabilities expedite disclosures and acknowledgments. Combined with remote notarization options now permanent in Washington State, these technologies enable fully remote transactions when desired, particularly valuable for relocating buyers or investment property purchases.

Integration with Local Real Estate Professionals

Seattle's real estate market operates through tight-knit professional networks. Good mortgage brokers maintain strong relationships with agents, escrow officers, and appraisers that facilitate smooth transactions. These connections prove invaluable when coordinating inspection contingency removals, title issues, or last-minute closing adjustments.

Brokers should demonstrate familiarity with your target neighborhoods and their specific market dynamics. Someone extensively working Capitol Hill, Montlake, or Portage Bay understands condo financing nuances, parking appraisal considerations, and typical closing timelines that generic brokers miss.

Selecting good mortgage brokers requires evaluating credentials, communication standards, lender access, and strategic expertise specific to your borrowing scenario. The right broker transforms complex financing into manageable processes while optimizing terms and protecting your interests throughout the transaction. Whether you're exploring Seattle home financing options as a first-time buyer or navigating complex equity compensation as a technology professional, working with experienced specialists delivers measurable advantages. Connect with Mortgage Reel to experience the difference that 25+ years of expertise, 750+ five-star reviews, and deep Seattle market knowledge make in your home financing journey.