Seattle's competitive real estate market presents unique challenges and opportunities for homebuyers pursuing properties above conventional loan limits. Whether you're eyeing a waterfront home in Bellevue, a craftsman in Queen Anne, or a modern estate in Kirkland, understanding jumbo home loans becomes essential when your financing needs exceed the boundaries of standard conforming mortgages. For tech professionals throughout the Greater Seattle area, these specialized mortgage products offer pathways to luxury properties while leveraging compensation structures that traditional lenders often struggle to qualify.

Understanding Jumbo Home Loans and Their Purpose

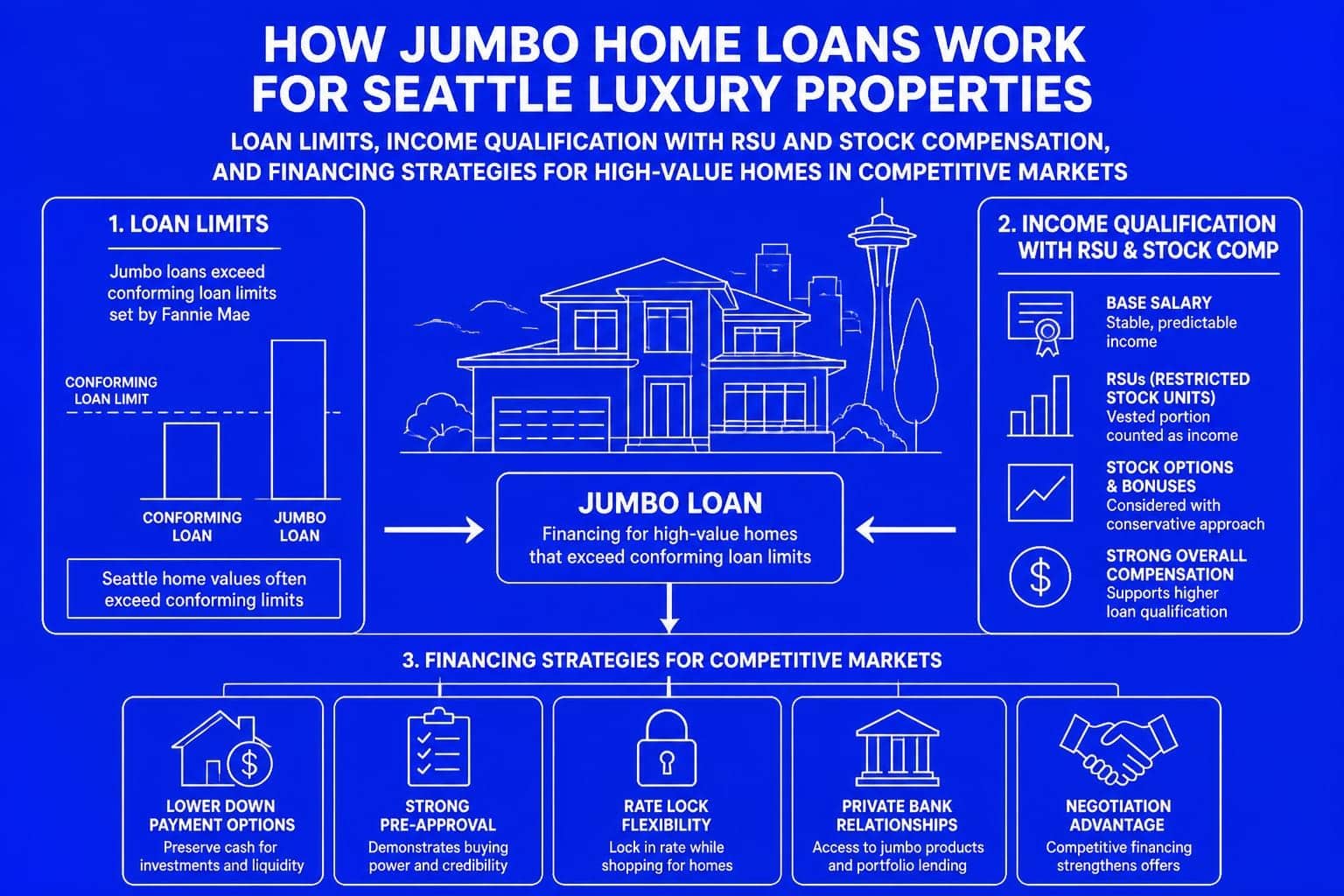

Jumbo home loans serve buyers who need financing beyond the Federal Housing Finance Agency's conforming loan limits. In 2026, King County's conforming loan limit sits at $891,250 for single-family homes, which means any mortgage exceeding this threshold requires jumbo financing. This distinction matters significantly in Seattle, Bellevue, Redmond, and surrounding areas where median home prices frequently surpass conventional limits.

What constitutes a jumbo loan depends on your specific county and property type. Snohomish County maintains slightly different thresholds, affecting buyers in Lynnwood, Mill Creek, and Everett. These loans aren't backed by Fannie Mae or Freddie Mac, which means lenders assume greater risk and consequently implement stricter qualification standards.

Key Differences from Conforming Mortgages

The fundamental distinction between jumbo and conforming loans extends beyond simple dollar amounts:

- Risk assessment protocols: Lenders conduct more rigorous underwriting reviews

- Reserve requirements: Typically 6-12 months of housing payments in liquid assets

- Documentation standards: Enhanced verification of income, assets, and employment

- Interest rate structures: Historically higher, though competitive markets have narrowed gaps

- Down payment expectations: Generally 10-20% minimum depending on loan amount

Qualification Requirements for Seattle Jumbo Borrowers

Securing jumbo financing in competitive markets demands preparation across multiple financial dimensions. Lenders evaluate borrowers through heightened scrutiny because these loans represent substantial capital without government backing.

Credit Score and History Standards

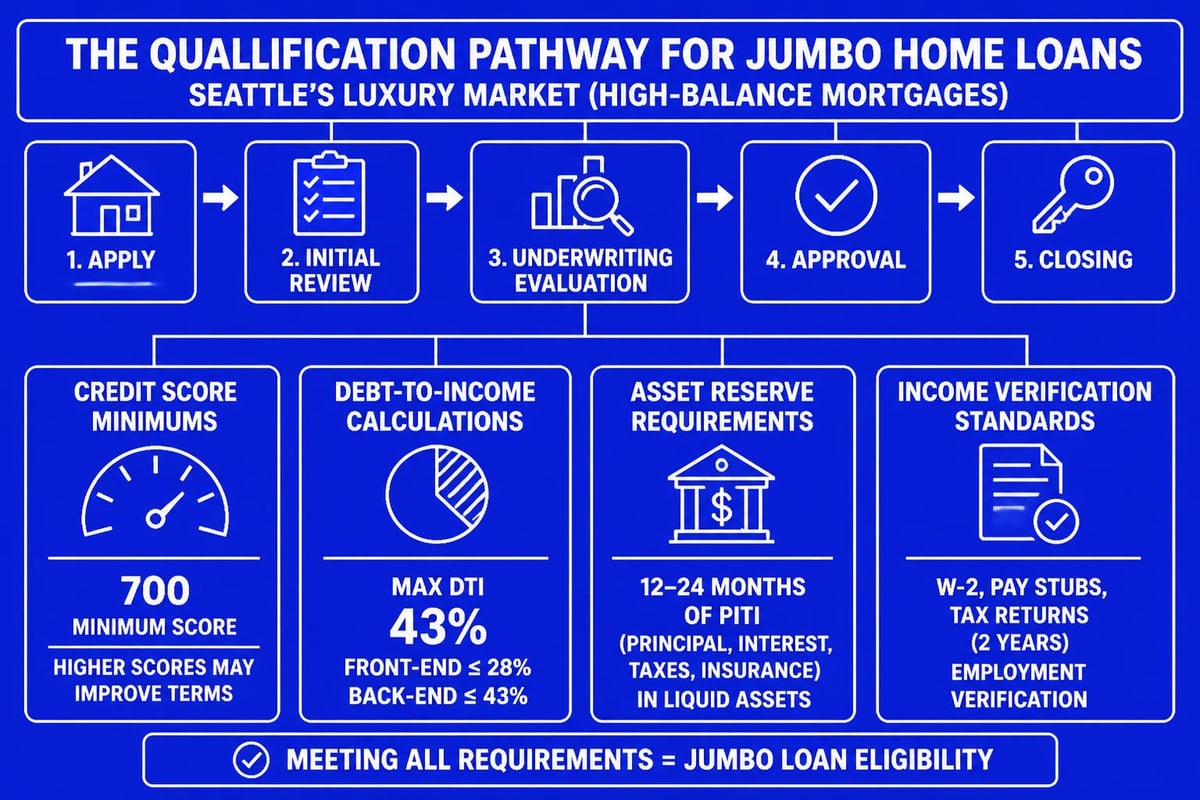

Most jumbo lenders in 2026 require minimum credit scores between 700 and 720, though some programs accept scores as low as 680 with compensating factors. Your credit history receives comprehensive review beyond just numerical scores. Lenders examine payment patterns, credit utilization ratios, recent inquiries, and any derogatory marks within the past seven years.

For Seattle mortgage borrowers, maintaining pristine credit becomes particularly valuable. A score above 740 typically unlocks the most competitive rates and flexible terms. Tech professionals with strong income but limited credit history should focus on establishing diverse credit types well before pursuing jumbo financing.

Income Documentation and Verification

Traditional W-2 employees face straightforward income verification through pay stubs, tax returns, and employer confirmation. The process becomes more nuanced for tech professionals whose compensation includes restricted stock units, stock options, bonuses, and equity grants. Understanding how RSU income qualifies for mortgage purposes requires specialized expertise that standard retail banks often lack.

Most jumbo lenders apply these income qualification approaches:

- Base salary: Full value counted with two-year employment history

- Annual bonuses: Two-year average if consistently received

- RSU and stock compensation: Percentage of vested value (typically 70-100%) depending on vesting schedule

- Commission income: Two-year average with stability considerations

- Rental income: 75% of documented lease payments on investment properties

The ability to maximize qualifying income directly impacts purchasing power in expensive Seattle neighborhoods. A Microsoft engineer with $200,000 base salary plus $150,000 in annual RSU income potentially qualifies for significantly more than lenders who only count base compensation.

Asset and Reserve Requirements

Beyond down payment funds, jumbo lenders require substantial liquid reserves. These reserves demonstrate financial stability and ability to weather unexpected circumstances. Typical requirements include:

| Loan Amount | Minimum Reserves Required |

|---|---|

| $766,551 – $1,000,000 | 6 months PITI |

| $1,000,001 – $1,500,000 | 9 months PITI |

| $1,500,001 – $2,000,000 | 12 months PITI |

| Above $2,000,000 | 12-18 months PITI |

PITI represents principal, interest, taxes, and insurance. For a $1.2 million home in Bellevue with $8,000 monthly housing payment, you'd need approximately $72,000 in reserves after closing costs and down payment. Acceptable reserve sources include checking accounts, savings accounts, retirement accounts (with 30% discount for early withdrawal penalties), and investment portfolios.

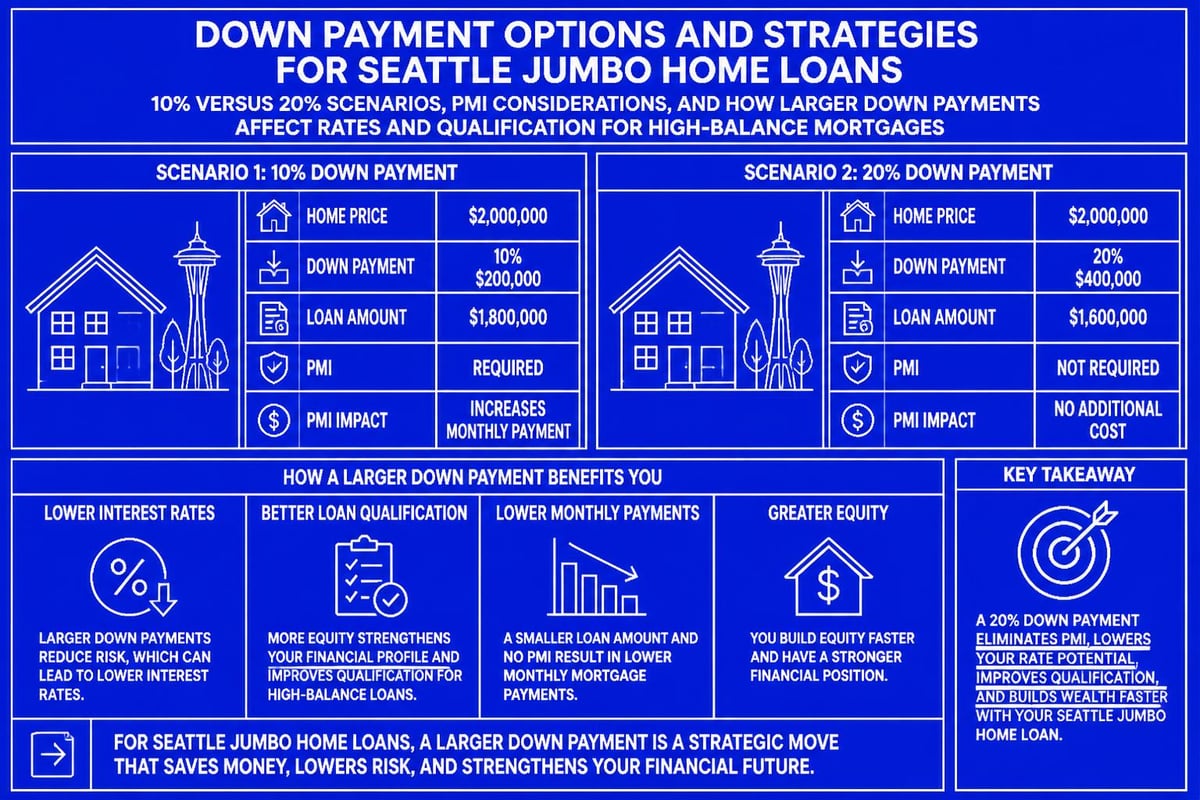

Down Payment Considerations and Strategies

Down payment requirements for jumbo home loans vary based on loan amount, property type, and borrower profile. While conventional wisdom suggests 20% remains standard, competitive lending environments have expanded options for qualified borrowers.

Minimum Down Payment Thresholds

Current jumbo loan programs in Washington State offer these typical down payment structures:

- 10% down: Available for loans up to $1.5 million with strong credit (740+) and reserves

- 15% down: Standard offering for most jumbo amounts with good credit (720+)

- 20% down: Traditional benchmark providing best rates and avoiding mortgage insurance

- 25%+ down: Premium pricing tier with lowest rates and most flexible underwriting

The decision between 10% and 20% down involves analyzing opportunity costs, investment returns, and cash flow preferences. Tech professionals with significant stock portfolios might prefer preserving liquidity rather than depleting investment accounts for larger down payments.

Private Mortgage Insurance on Jumbo Loans

Unlike conforming loans, jumbo mortgages handle mortgage insurance differently. Some lenders offer true PMI on jumbo loans, while others use lender-paid mortgage insurance reflected through slightly higher interest rates. A third option involves piggyback second mortgages, though these have become less common in recent years.

When comparing jumbo loan programs, calculate the effective cost of insurance premiums against rate adjustments. A 0.25% rate increase on a $1 million loan costs approximately $2,500 annually, while PMI might run $4,000-$6,000 yearly on the same loan amount.

Interest Rates and Pricing Factors

Jumbo loan interest rates reflect the increased risk lenders assume on non-conforming mortgages. However, Seattle's competitive lending landscape and high concentration of qualified borrowers have compressed rate spreads between jumbo and conforming products.

Current Rate Environment in 2026

Today's jumbo rates typically run 0.125% to 0.375% higher than comparable conforming mortgages, though exceptional borrowers sometimes secure rates at or below conforming levels. Several factors influence your specific rate:

- Credit score impact: 40-60 basis points between 700 and 780+ scores

- Loan-to-value ratio: Better rates at 80% LTV versus 90% LTV

- Reserve depth: Additional reserves beyond minimums improve pricing

- Property type: Single-family residences receive best rates versus condos or multi-unit properties

- Occupancy status: Primary residences outperform second homes and investment properties

Rate locks for jumbo loans follow similar timeframes as conforming products, though some lenders charge premium pricing for extended locks beyond 60 days given market volatility on high-balance loans.

Adjustable-Rate versus Fixed-Rate Options

Jumbo borrowers often consider ARM products more seriously than conforming borrowers due to initial rate advantages. A 7/1 or 10/1 ARM might offer 0.50% to 0.75% lower rates compared to 30-year fixed jumbo mortgages, creating substantial monthly savings on large loan amounts.

A $1.2 million loan at 6.50% (30-year fixed) versus 5.75% (10/1 ARM) demonstrates the trade-off:

| Product Type | Interest Rate | Monthly Payment | 10-Year Interest Paid |

|---|---|---|---|

| 30-Year Fixed | 6.50% | $7,586 | $765,432 |

| 10/1 ARM | 5.75% | $7,002 | $679,518 |

| Monthly Savings | – | $584 | $85,914 total savings |

Tech professionals anticipating job changes, relocations, or refinancing opportunities within 7-10 years frequently benefit from ARM structures. However, rate adjustment caps and potential payment increases require careful analysis against personal risk tolerance.

Specialized Jumbo Programs for Tech Professionals

Seattle's concentration of technology employers creates unique opportunities for mortgage products designed around equity compensation and stock-based income. These specialized programs acknowledge that traditional underwriting often undervalues total compensation for Amazon, Microsoft, Google, and other tech company employees.

Qualifying Stock Compensation and RSUs

Standard mortgage guidelines treat stock compensation conservatively, sometimes requiring two-year vesting history or applying significant discounts to unvested equity. Advanced jumbo programs recognize the reliability of major tech company stock grants and apply more aggressive qualification methods.

Progressive lenders evaluate RSUs through these enhanced approaches:

- Immediate vesting credit: Full value of RSUs vesting within 12 months

- Stock option valuation: Current spread between strike price and market value

- Bonus income optimization: One-year averaging for consistent bonus structures

- Sign-on bonus inclusion: Amortized over guarantee period for recent hires

A Microsoft employee with $150,000 base salary, $200,000 in annual RSU vesting, and $50,000 bonus might qualify for $1.6-$1.8 million in purchasing power versus $600,000-$700,000 counting base salary alone. This difference fundamentally changes accessible neighborhoods and property options throughout Seattle, Bellevue, and Redmond.

Fast-Close Capabilities for Competitive Markets

Seattle's housing market demands speed and certainty. Properties in desirable neighborhoods like Capitol Hill, Queen Anne, and Madison Park often receive multiple offers within days of listing. The ability to close quickly strengthens offers significantly, sometimes more than price escalations.

Advanced jumbo programs through specialized lenders offer closing timelines as short as 9-15 business days for well-qualified borrowers with complete documentation. This speed requires:

- Pre-underwriting before offer submission

- Rapid appraisal ordering and completion

- Streamlined documentation review processes

- Dedicated underwriting teams for jumbo products

- Clear communication channels between all transaction parties

Working with experienced mortgage professionals who specialize in jumbo financing and tech compensation becomes invaluable when competing against cash offers or conventional financing with longer timelines.

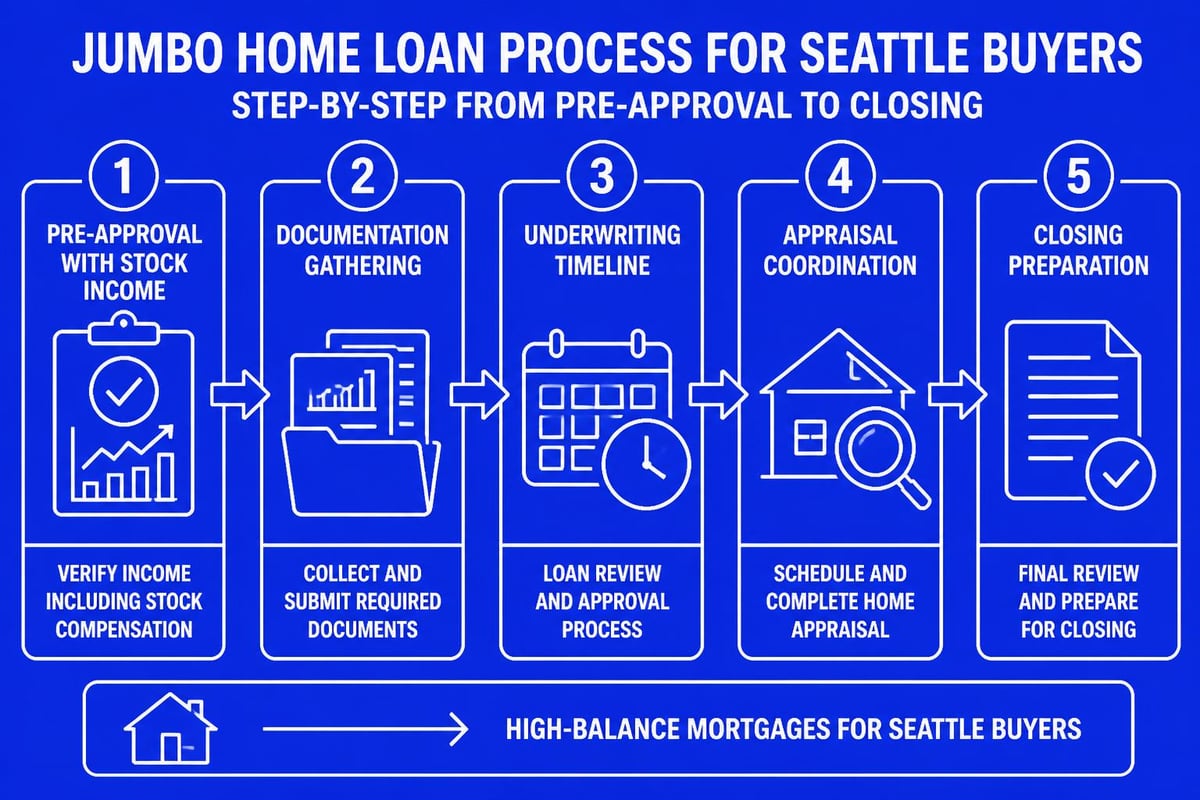

The Jumbo Loan Application Process

Securing jumbo financing requires methodical preparation and comprehensive documentation. While the fundamental process mirrors conforming loans, enhanced scrutiny demands greater attention to detail and proactive communication.

Pre-Approval Preparation Checklist

Before pursuing pre-approval for Seattle home financing, gather these essential documents:

- Income verification: Two years W-2s, recent pay stubs, two years tax returns with all schedules

- Asset documentation: Two months statements for all accounts, retirement account statements, investment portfolios

- Stock compensation records: Vesting schedules, grant letters, online account access for real-time valuations

- Existing debt obligations: Current mortgage statements, auto loans, student loans, credit card statements

- Property tax history: If selling current home, recent tax bills demonstrating payment history

- Rental income proof: Leases and deposit records if qualifying rental properties

Complete documentation accelerates underwriting timelines and prevents delays during competitive offer situations. Missing or incomplete documentation represents the primary cause of extended closing periods on jumbo transactions.

Appraisal Requirements and Challenges

Jumbo loans require full appraisals conducted by certified appraisers experienced with high-value properties. In Seattle's diverse neighborhoods, finding comparable sales for unique properties sometimes challenges valuation accuracy. Waterfront homes in Portage Bay, historic mansions in Capitol Hill, or modern new construction in Bellevue each present distinct appraisal considerations.

Some jumbo lenders require additional valuation support:

- Second appraisals for loans exceeding $1.5 million

- Desktop reviews by independent appraisal firms

- Broker price opinions as supplemental documentation

- Comparative market analysis from listing agents

Appraisal gaps occur when professional valuations come in below purchase prices. On jumbo transactions, borrowers must cover shortfalls with additional cash since loan-to-value ratios calculate from the lower of purchase price or appraised value. A $1.5 million purchase appraising at $1.45 million with 20% down requires an additional $50,000 beyond the planned $300,000 down payment.

Common Scenarios for Jumbo Financing in Seattle

Understanding how different buyer profiles utilize jumbo home loans clarifies whether these products align with your situation and goals.

First-Time Luxury Buyers

Tech professionals purchasing their first home often skip traditional starter properties and move directly into luxury price points. A couple with combined income of $400,000-$500,000 and substantial savings from years of high earnings might target properties in the $1.2-$1.5 million range throughout Seattle, Kirkland, or Bellevue.

These buyers benefit from first-time buyer strategies adapted for jumbo scenarios, including maximizing gift funds from family members and leveraging down payment assistance programs available for higher-income brackets in Washington State.

Move-Up Buyers with Substantial Equity

Homeowners selling properties in appreciating Seattle neighborhoods often carry significant equity into their next purchase. Someone selling a $900,000 home purchased for $500,000 five years ago might net $350,000-$400,000 after selling costs, providing substantial down payment capacity for properties in the $1.5-$2 million range.

These scenarios involve coordinating sale and purchase timelines, potentially utilizing bridge financing or home sale contingencies. Experienced jumbo lenders structure transactions to accommodate equity transfer while maintaining competitive offer positioning.

Investment Property Acquisition

Real estate investors targeting premium rental properties in desirable Seattle neighborhoods require jumbo financing for properties generating strong rental income. Investment property jumbo loans carry higher rates and larger down payment requirements (typically 25-30%), but experienced investors recognize the wealth-building potential of Seattle's appreciation trends.

Qualifying rental income on jumbo investment properties requires documented lease agreements, rent rolls demonstrating collection history, and careful debt-to-income calculations incorporating PITI on the new property.

Comparing Jumbo Lenders and Programs

Not all jumbo loan programs offer equivalent terms, flexibility, or service quality. Evaluating lenders requires analyzing multiple dimensions beyond advertised interest rates.

National Banks versus Local Mortgage Brokers

Large national banks offer jumbo programs with name recognition and established processes. However, their underwriting often follows rigid guidelines with limited flexibility for unique compensation structures or non-traditional scenarios. Decision-making occurs through centralized underwriting departments potentially unfamiliar with Seattle market dynamics and tech industry compensation.

Local mortgage brokers access multiple wholesale lenders, comparing programs to identify optimal fits for specific borrower profiles. This approach provides:

- Program variety: Access to 20-30 different jumbo lenders versus single-bank limitations

- Specialized expertise: Deep knowledge of tech compensation and Seattle market conditions

- Responsive service: Direct access to decision-makers rather than call center routing

- Competitive pricing: Wholesale rate access often beats retail bank pricing

Working with local Seattle mortgage professionals particularly benefits borrowers with complex income structures, multiple properties, or tight timeline requirements.

Portfolio Lenders and Credit Unions

Some banks and credit unions hold jumbo loans in portfolio rather than selling them on secondary markets. This approach allows greater underwriting flexibility since loans don't need to meet investor guidelines. Portfolio jumbo programs might accommodate lower credit scores, higher debt-to-income ratios, or unique property types rejected by traditional jumbo lenders.

Trade-offs include potentially higher rates, limited geographic lending areas, and relationship requirements like maintaining deposit accounts or membership qualifications. These programs serve valuable niches but require careful comparison against conventional jumbo offerings.

Tax Implications and Financial Planning

Jumbo mortgages carry specific tax considerations that impact overall financial strategy, particularly for high-income borrowers in upper tax brackets.

Mortgage Interest Deduction Limitations

Tax legislation limits mortgage interest deductions to interest paid on the first $750,000 of acquisition debt for mortgages originated after December 15, 2017. Borrowers with jumbo loans exceeding this threshold cannot deduct interest on amounts above $750,000, reducing the effective tax benefit of larger mortgages.

A married couple filing jointly in the 35% federal tax bracket with a $1.5 million mortgage at 6.5% pays approximately $97,500 in annual interest. Only interest on the first $750,000 ($48,750) qualifies for deduction, providing roughly $17,063 in federal tax savings rather than the $34,125 they would receive if the full amount were deductible.

Strategic Debt Management Considerations

High-net-worth individuals often debate optimal debt levels given investment opportunities and tax efficiency. Some financial advisors recommend minimizing mortgage debt and maximizing investment portfolio growth, while others advocate maintaining low-rate mortgage debt while investing excess capital in higher-return assets.

For tech professionals with substantial stock portfolios, this decision involves analyzing:

- After-tax mortgage costs versus expected investment returns

- Sequence of returns risk and market volatility

- Liquidity needs and emergency reserve adequacy

- Estate planning considerations and legacy goals

- Personal risk tolerance and debt comfort levels

There's no universal answer, but comprehensive analysis should precede major financial decisions about down payment amounts, mortgage payoff strategies, or refinancing approaches.

Refinancing Jumbo Mortgages

Market conditions, life changes, and financial optimization create refinancing opportunities throughout mortgage lifecycles. Jumbo refinancing follows similar mechanics as purchase financing but with additional strategic considerations.

Rate-and-Term Refinancing Scenarios

When rates drop significantly below your current mortgage rate, refinancing can generate substantial savings on jumbo loan balances. A 1% rate reduction on a $1.2 million balance saves approximately $12,000 annually, easily justifying typical refinancing costs of $8,000-$12,000 on jumbo transactions.

Beyond simple rate improvements, refinancing enables:

- Converting ARMs to fixed-rate products as adjustment periods approach

- Shortening loan terms from 30 to 20 or 15 years while maintaining similar payments

- Consolidating first and second mortgages into single jumbo loans

- Removing mortgage insurance once reaching 20% equity through appreciation

Understanding refinancing timelines helps borrowers capitalize on rate opportunities before they disappear.

Cash-Out Refinancing for Investment or Debt Consolidation

Jumbo cash-out refinancing allows tapping home equity while maintaining favorable mortgage rates compared to home equity lines of credit or personal loans. Common uses include:

- Funding investment property down payments

- Consolidating high-rate consumer debt

- Financing major home renovations

- Providing liquidity for business investments

Cash-out jumbo refinancing typically limits loan-to-value ratios to 75-80%, meaning you must maintain 20-25% equity after the new loan funds. A home worth $2 million with a $900,000 existing mortgage could support cash-out refinancing up to $1.5-$1.6 million, providing $600,000-$700,000 in cash proceeds.

Mortgage Recasting as an Alternative

Mortgage recasting offers an underutilized alternative to refinancing for borrowers satisfied with current rates but seeking lower monthly payments. This process involves making a large principal payment (typically $100,000 minimum), then having the lender re-amortize the remaining balance over the original term.

Recasting costs only $250-$500 versus $8,000-$15,000 for refinancing, preserving your existing favorable rate while reducing monthly obligations. Tech professionals receiving large RSU vesting events, bonuses, or inheritance funds frequently use recasting to optimize cash flow without sacrificing low interest rates secured in previous market environments.

Regional Considerations for Seattle-Area Jumbo Buyers

Local market dynamics significantly influence jumbo loan strategies throughout King and Snohomish Counties. Understanding these regional factors helps buyers make informed decisions aligned with specific neighborhoods and property types.

King County Loan Limits and Market Premiums

Seattle's status as a high-cost area establishes conforming loan limits substantially above national averages. However, many desirable neighborhoods consistently price beyond even these elevated thresholds. Median home prices in areas like Madison Park, Laurelhurst, and Medina regularly exceed $1.5 million, making jumbo financing standard rather than exceptional.

King County loan limits affect borrowing strategies, particularly for buyers considering properties near conforming boundaries. A home priced at $920,000 versus $880,000 crosses from conforming to jumbo territory, potentially affecting qualification, rates, and down payment requirements.

Snohomish County Opportunities

Buyers seeking larger properties or acreage while maintaining Seattle-area access increasingly explore Snohomish County communities like Mill Creek, Lynnwood, and Everett. These areas offer luxury properties requiring jumbo financing but at lower absolute price points than comparable Seattle or Bellevue homes.

Snohomish County home loans provide value opportunities where $1.2 million purchases significantly more square footage and land than equivalent investments in Seattle proper. For families prioritizing space, school districts, and property features over urban proximity, these submarkets deserve serious consideration.

Competitive Offer Strategies in Multiple-Offer Scenarios

Premium properties throughout Seattle frequently generate multiple offers, with some listings receiving 5-10+ competitive bids. Jumbo buyers strengthen their position through several strategic approaches:

- Pre-underwritten approvals: Full file review before offer submission

- Appraisal gap coverage: Committing to cover specific amounts if appraisal falls short

- Flexible closing timelines: Accommodating seller preferences for close dates

- Minimal contingencies: Waiving financing contingencies when financially secure

- Escalation clauses: Automated price increases to predetermined maximums

Winning bidding wars requires balancing financial protection with competitive positioning. Experienced jumbo lenders help structure offers that protect buyer interests while demonstrating strength and certainty to sellers.

Jumbo home loans open doors to Seattle's most desirable properties while accommodating the unique compensation structures common among tech professionals and high-income earners. From understanding qualification requirements to strategically leveraging stock-based income, successful jumbo financing requires specialized expertise and proactive planning. Keith Akada brings 25+ years of experience helping Seattle-area buyers navigate complex jumbo transactions with clarity and confidence, including rapid closings as fast as 9 business days. Whether you're pursuing your first luxury home or upgrading to a premium property, Mortgage Reel delivers the education, transparency, and strategic guidance that makes competitive Seattle purchases achievable.