Finding the best home financing solution requires understanding your unique situation, local market dynamics, and the full range of loan products available in 2026. Seattle's competitive housing market demands strategic planning, whether you're purchasing your first condo in Lynnwood or refinancing a waterfront property in Shoreline. The right financing strategy balances your down payment capacity, income profile, credit history, and long-term homeownership goals. As a licensed mortgage broker serving Greater Seattle for over 25 years, I've helped thousands of clients navigate these decisions with clarity and confidence.

Understanding Your Home Financing Foundation

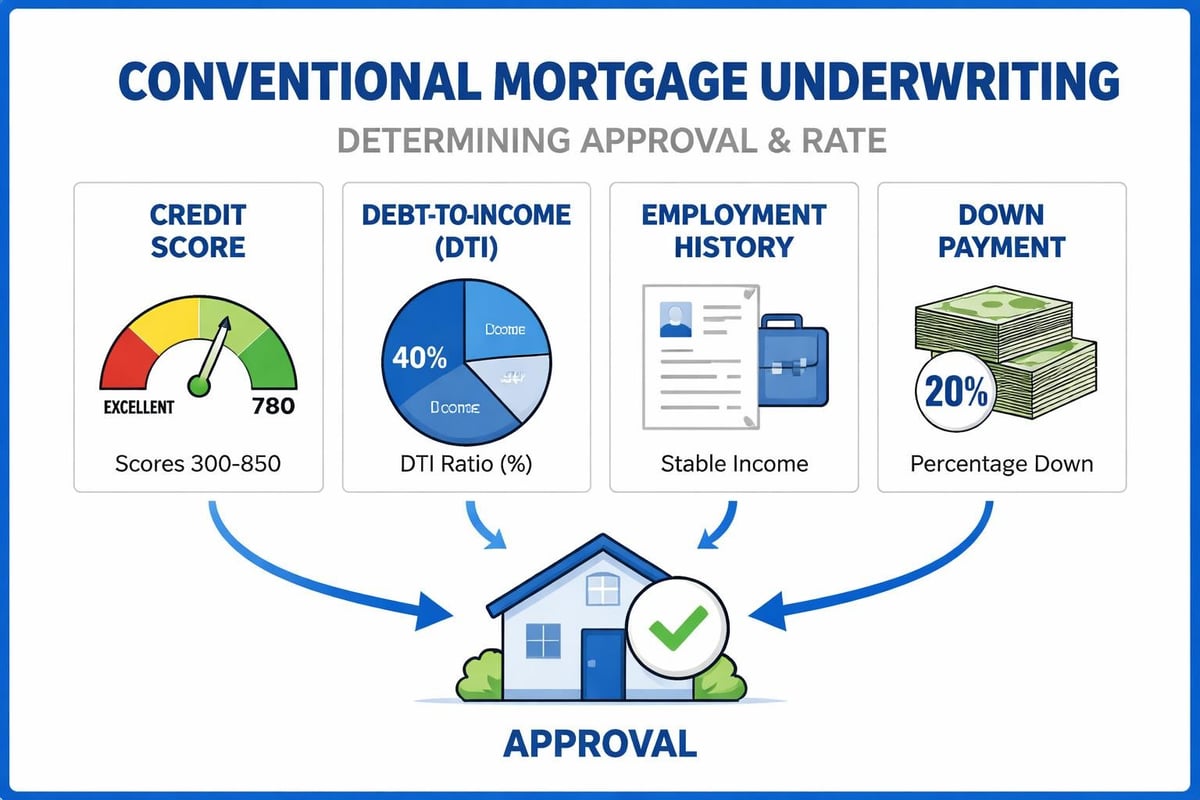

Before exploring specific loan products, establish a clear picture of your financial readiness. Lenders evaluate three primary factors: credit score, debt-to-income ratio, and down payment capacity. Your credit score influences both your approval odds and interest rate, with conventional loans typically requiring 620 or higher, though some programs accommodate lower scores.

Debt-to-income ratio (DTI) measures your monthly debt obligations against gross income. Most programs cap DTI at 43-50%, though exceptions exist for strong borrower profiles. For tech professionals in Seattle, Bellevue, or Redmond with stock compensation, understanding how underwriters qualify RSUs and bonus income becomes critical to maximizing purchasing power.

Down payment requirements vary dramatically by loan type. The Consumer Financial Protection Bureau’s homebuying toolkit provides excellent foundational guidance on preparing financially for homeownership. While 20% down remains the benchmark for avoiding private mortgage insurance (PMI) on conventional loans, numerous programs require far less.

Key Financial Metrics Lenders Evaluate

| Metric | Conventional | FHA | VA | Jumbo |

|---|---|---|---|---|

| Minimum Credit Score | 620 | 580 | No minimum | 680-700 |

| Maximum DTI | 50% | 56.9% | 41-60% | 43-45% |

| Minimum Down Payment | 3% | 3.5% | 0% | 10-20% |

| PMI Required | Yes (under 20%) | Yes (MIP) | No | Varies |

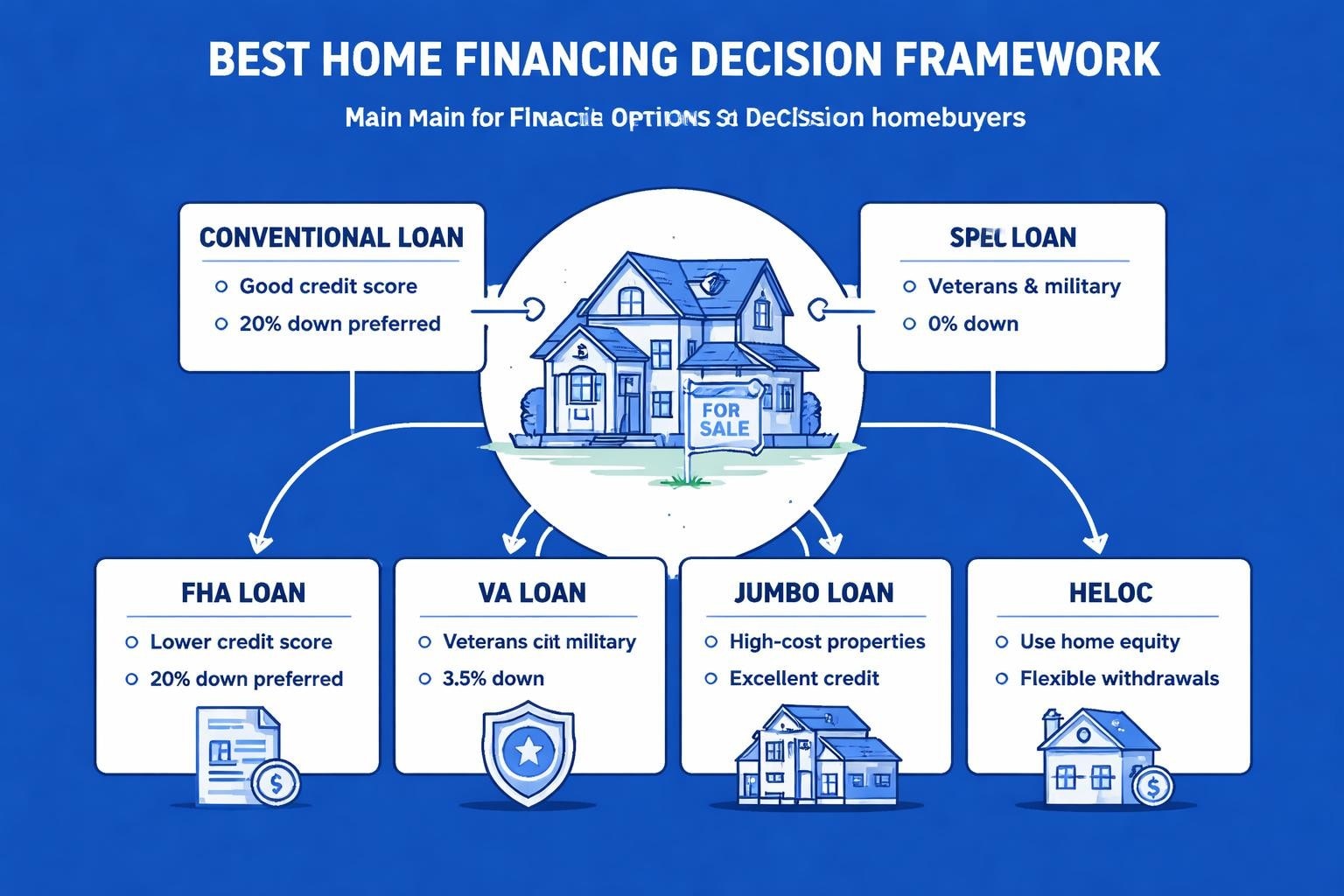

Conventional Loans: The Most Flexible Path

Conventional mortgages backed by Fannie Mae or Freddie Mac represent the most common form of best home financing for borrowers with solid credit and stable income. These loans offer flexibility in property type, loan amount, and repayment terms. First-time buyers can qualify with as little as 3% down through HomeReady or Home Possible programs, making homeownership accessible even in expensive markets like Mill Creek or Lake Forest Park.

The primary advantage of conventional financing lies in competitive interest rates for well-qualified borrowers and the ability to remove PMI once you reach 20% equity. For Seattle-area buyers purchasing properties above conforming loan limits, conventional jumbo loans provide financing without the constraints of government-backed programs.

Conventional loans work exceptionally well when:

- Your credit score exceeds 680

- You have 5-20% available for down payment

- Your employment history shows two years of stability

- You're purchasing a primary residence, second home, or investment property

- Property value falls within or above conforming limits

One strategic consideration involves understanding how to explore different mortgage options based on your specific circumstances. The Seattle market's median home price requires thoughtful planning around loan structure and long-term financial impact.

FHA Loans: Accessible Financing for First-Time Buyers

Federal Housing Administration loans remain a cornerstone of best home financing for borrowers with limited down payment savings or credit challenges. With just 3.5% down and credit scores as low as 580, FHA loans open homeownership opportunities that conventional financing might exclude.

The tradeoff involves mortgage insurance premiums (MIP) that persist for the loan's life on purchases with less than 10% down. This ongoing cost impacts long-term affordability, making FHA loans ideal for buyers who plan to refinance after building equity and improving credit. First-time buyers in Everett or Shoreline frequently leverage FHA financing to enter the market, then refinance to conventional terms within 3-5 years.

FHA Loan Advantages and Considerations

Benefits:

- Low down payment requirement

- Flexible credit guidelines

- Seller can contribute up to 6% toward closing costs

- Assumable mortgage feature

- Gift funds allowed for entire down payment

Considerations:

- Upfront mortgage insurance premium (1.75% of loan amount)

- Ongoing monthly MIP

- Property must meet specific condition standards

- Loan limits apply (varies by county)

Programs designed to help first-time homebuyers provide detailed comparisons of FHA advantages against other entry-level financing options. Understanding these distinctions helps you make informed decisions aligned with your financial trajectory.

VA Loans: Unmatched Benefits for Military Families

Veterans, active-duty service members, and eligible spouses access the best home financing terms available through VA-backed mortgages. Zero down payment, no mortgage insurance, competitive interest rates, and flexible credit guidelines make VA loans extraordinarily powerful.

The VA funding fee (typically 2.3% for first-time use with zero down) represents the primary upfront cost, though this can be financed into the loan amount. Disabled veterans may qualify for exemption from this fee entirely. For military families relocating to Joint Base Lewis-McChord or settling in Seattle after service, VA financing provides unparalleled advantages.

VA loans accommodate higher DTI ratios than conventional financing, recognizing the stable income military service provides. This flexibility proves especially valuable for service members with student loans or other obligations that might challenge conventional underwriting.

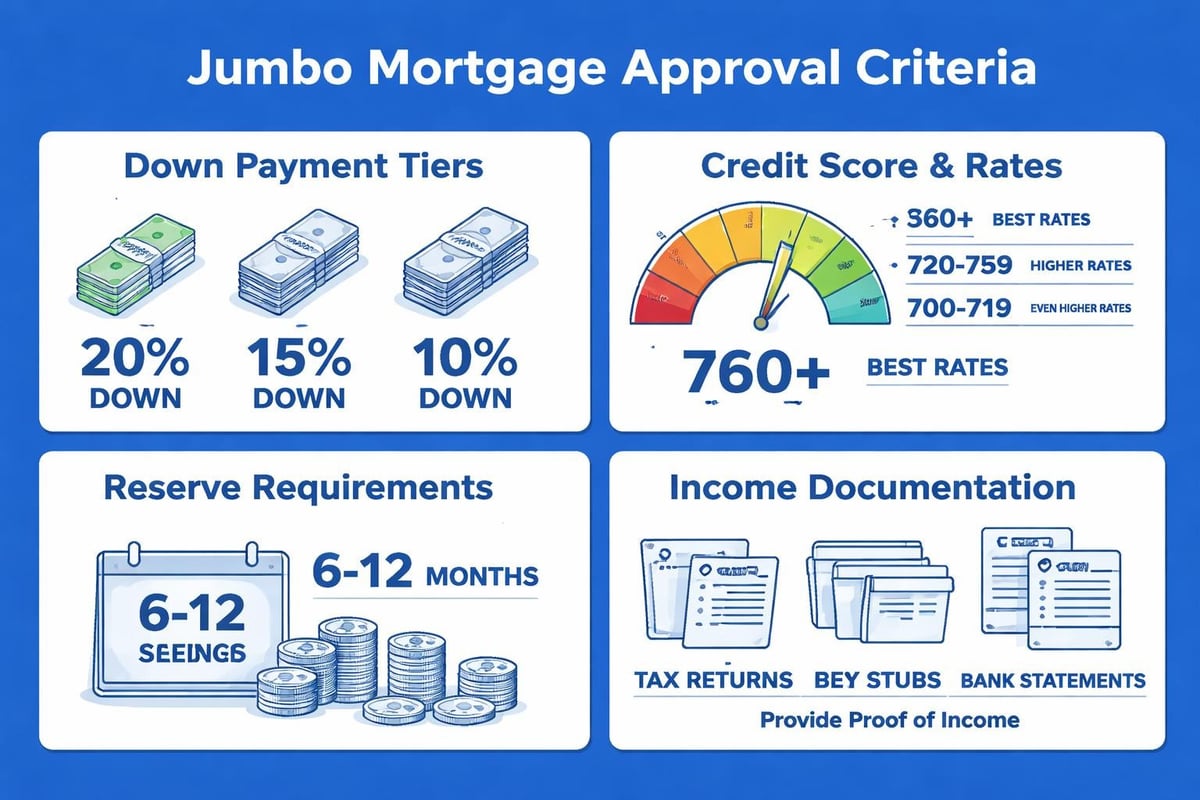

Jumbo Loans: Financing Seattle's Premium Properties

When property values exceed conforming loan limits ($806,500 for most of Washington in 2026), jumbo financing becomes necessary. Seattle, Bellevue, and surrounding communities regularly see transactions requiring jumbo loans, making understanding these products essential for serious buyers.

Best home financing in the jumbo space demands stronger qualifications: higher credit scores (typically 700+), larger down payments (often 10-20%), and lower debt-to-income ratios. The reward comes through financing luxury properties, waterfront homes, or prime urban real estate that exceeds conventional limits.

For tech professionals at Amazon, Microsoft, or Google, jumbo loans often involve complex income calculations. Stock options, RSUs, and performance bonuses require specialized underwriting expertise to maximize borrowing capacity. Working with a Seattle mortgage broker experienced in tech compensation structures ensures you present the strongest possible application.

| Down Payment | Typical Credit Requirement | Cash Reserves | Rate Impact |

|---|---|---|---|

| 10% | 720+ | 12 months | Higher |

| 15% | 700+ | 9 months | Moderate |

| 20% | 680+ | 6 months | Competitive |

| 25%+ | 680+ | 6 months | Best available |

USDA Loans: Rural Property Financing

United States Department of Agriculture loans provide 100% financing for eligible properties in designated rural areas. While Seattle proper doesn't qualify, portions of Snohomish County and outlying areas may meet USDA criteria. These loans target low-to-moderate income households, imposing income limits based on household size and location.

The complete absence of down payment requirements makes USDA loans attractive, though geographic restrictions limit applicability. Properties must serve as primary residences, and borrowers must demonstrate creditworthiness despite no minimum credit score requirement.

Alternative Financing: Home Equity and Renovation Products

Existing homeowners pursuing renovations or accessing equity have additional financing tools beyond traditional mortgages. Home Equity Lines of Credit (HELOCs) provide flexible, revolving credit secured by home equity. Innovative products like the Trovy HELOC card combine traditional HELOC benefits with credit card convenience for renovation projects.

Cash-out refinancing replaces your existing mortgage with a larger loan, distributing the difference as cash. This strategy works well when current rates remain favorable and you've built substantial equity. For homeowners in Kirkland or Redmond considering major improvements, comparing HELOC versus cash-out refinancing reveals the best home financing approach for your situation.

Renovation Financing Comparison

203(k) Renovation Loans:

- Single loan for purchase and improvements

- FHA-backed with flexible credit requirements

- Complex documentation and contractor requirements

- Best for significant structural renovations

HomeStyle Renovation Loans:

- Conventional equivalent to 203(k)

- Stricter credit requirements (620+)

- More flexibility in property types

- Streamlined process for moderate renovations

HELOCs:

- Access equity without refinancing primary mortgage

- Variable interest rates

- Revolving credit line

- Ideal for ongoing or phased projects

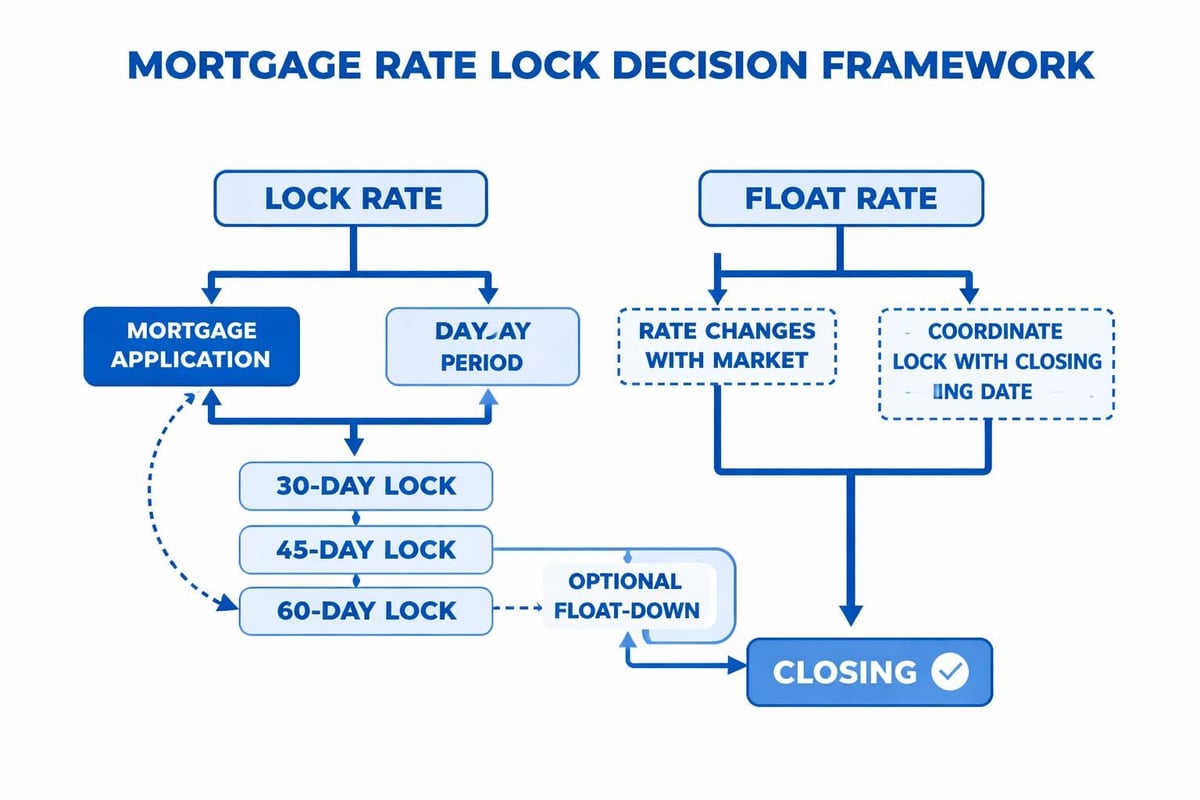

Strategic Timing and Rate Considerations

Interest rates significantly impact long-term affordability. A difference of just 0.5% on a $600,000 loan translates to roughly $180 monthly and over $64,000 across 30 years. Current Seattle mortgage rates fluctuate based on economic conditions, Federal Reserve policy, and individual borrower qualifications.

The best home financing strategy considers both today's rates and your ability to refinance if rates decline. Avoid the temptation to time the market perfectly. If you've found the right property and can comfortably afford monthly payments, proceeding makes sense even if rates aren't at historic lows.

Points and rate buydowns offer another strategic lever. Paying upfront costs to reduce your interest rate makes sense when you plan to stay in the property long enough to recoup the investment. Calculate your break-even point by dividing the upfront cost by monthly savings.

Qualifying Complex Income Sources

Seattle's tech-heavy economy means many borrowers earn significant compensation through stock awards, bonuses, and equity. Traditional W-2 income requires just two years of history, but RSUs, stock options, and variable compensation demand specialized documentation.

Underwriters typically average restricted stock units over the vesting schedule, discount unvested awards, and apply continuity requirements. Understanding these nuances before applying ensures you maximize purchasing power rather than leaving borrowing capacity on the table.

Self-employed borrowers face different documentation requirements:

- Two years of personal and business tax returns

- Year-to-date profit and loss statement

- Business license and proof of continuity

- Explanation of any significant income fluctuations

- CPA letter validating ongoing business viability

Working with an experienced broker familiar with Seattle mortgage financing for diverse income types streamlines the process and prevents surprises during underwriting.

Pre-Approval: Your Competitive Advantage

Seattle's competitive market demands more than casual browsing. Sellers expect serious offers backed by solid financing. Pre-approval provides that credibility, demonstrating you've undergone credit review, income verification, and asset documentation.

Distinguished from pre-qualification (which involves only basic information), true pre-approval includes credit report review, employment verification, and preliminary underwriting. In multiple-offer situations common throughout Bellevue, Redmond, and Seattle neighborhoods, pre-approval strengthens your position substantially.

The best home financing preparation involves gathering documentation proactively: recent pay stubs, W-2s, tax returns, bank statements, and retirement account statements. This completeness accelerates approval and positions you to move quickly when you find the right property.

Closing Cost Planning and Down Payment Assistance

Beyond down payment, budget for closing costs typically ranging 2-5% of purchase price. These include origination fees, appraisal, title insurance, escrow setup, prepaid insurance and taxes, and recording fees. Some costs remain negotiable, while others are fixed.

Seller concessions allow sellers to contribute toward your closing costs, effectively reducing cash needed at closing. FHA loans permit up to 6% in seller concessions, while conventional loans typically allow 3-9% depending on down payment size.

Washington State and local programs offer down payment assistance:

- Washington State Housing Finance Commission programs

- City-specific first-time buyer initiatives

- Employer-sponsored homebuyer assistance (common among major Seattle employers)

- Credit union and community bank special programs

These resources expand access to homeownership, particularly for first-time buyers in Lake Forest Park, Mill Creek, or Lynnwood facing high entry costs.

Refinancing: Optimizing Existing Financing

Refinancing replaces your current mortgage with new terms, potentially lowering rates, accessing equity, or changing loan duration. Rate-and-term refinancing focuses purely on improving your interest rate or repayment period without taking cash out.

The break-even analysis determines whether refinancing makes sense. Calculate total closing costs divided by monthly savings to identify how many months until you recover expenses. If you plan to stay in your home beyond that point, refinancing delivers value.

Cash-out refinancing converts equity to cash for debt consolidation, home improvements, or other purposes. This strategy makes sense when refinance rates remain competitive with your current rate and you have substantial equity available.

Working With a Trusted Mortgage Broker

The best home financing decisions emerge from clear understanding, strategic planning, and expert guidance. While online calculators and articles provide valuable information, complex scenarios involving stock compensation, jumbo financing, or unique property types benefit from personalized expertise.

A skilled broker compares options across multiple lenders, identifies programs matching your specific situation, and navigates underwriting complexities that might derail less experienced applicants. The difference between a smooth closing and a stressful experience often traces directly to choosing the right lending partner.

For borrowers in Everett, Shoreline, or Seattle proper, local market knowledge matters. Understanding neighborhood-specific considerations, knowing which lenders handle certain property types efficiently, and anticipating potential appraisal challenges comes from boots-on-the-ground experience.

Final Considerations Before Applying

Review your complete financial picture before pursuing home financing. Beyond qualifying for a loan, ensure monthly payments fit comfortably within your budget while allowing for property taxes, insurance, maintenance, and unexpected repairs. The housing expense ratio (housing costs divided by gross income) should typically remain below 28%, though this varies based on other financial obligations.

Consider your timeline for homeownership. If you anticipate relocating within 3-5 years, adjustable-rate mortgages might offer lower initial rates. Conversely, if you're settling long-term in Lake Forest Park or Bellevue, the stability of fixed-rate financing provides peace of mind against future rate increases.

Property type influences financing options. Condos require additional review of homeowner association finances and legal status. Investment properties demand larger down payments and higher rates. Multi-unit properties up to four units qualify for owner-occupied financing if you'll live in one unit.

Understanding these distinctions ensures you approach the best home financing search with realistic expectations and proper preparation, positioning yourself for approval and long-term success.

Securing the best home financing requires balancing immediate affordability with long-term financial strategy, understanding the full range of loan products, and working with experienced professionals who prioritize your success. Whether you're a first-time buyer in Mill Creek, a tech professional seeking jumbo financing in Seattle, or a homeowner optimizing through refinancing, the right guidance makes all the difference. Keith Akada at Mortgage Reel brings over 25 years of experience helping Greater Seattle homebuyers navigate these decisions with transparency and expertise, backed by 750+ five-star reviews and proven execution in competitive markets.