Understanding your down payment on home purchases represents one of the most critical financial decisions you'll make as a homebuyer. In the Greater Seattle area, where median home prices continue to challenge first-time buyers and seasoned investors alike, determining the right down payment strategy can significantly impact your monthly mortgage payment, interest rate, and long-term wealth building. Whether you're a tech professional at Amazon or Microsoft in Bellevue, a growing family in Shoreline, or an investor eyeing rental properties in Everett, the amount you put down affects everything from loan approval to closing costs.

How Much Should You Put Down on a Home in Seattle?

The traditional 20% down payment requirement has become more myth than reality in 2026. While many buyers still aim for this benchmark, especially in competitive neighborhoods like Redmond and Kirkland, the actual down payment on home purchases varies widely based on loan type, borrower qualifications, and financial strategy.

Current down payment trends across different buyer types include:

- First-time buyers: typically 5-10%

- Repeat buyers: generally 15-23%

- Investment properties: minimum 15-25%

- Jumbo loan purchases: often 10-20% or more

According to recent data, the median down payment for all home buyers nationwide is 19%, but first-time buyers average just 10%. In Seattle's competitive market, these numbers can shift based on property type, location, and buyer competition.

Factors That Determine Your Ideal Down Payment Amount

Your optimal down payment on home purchases depends on several interconnected factors. Credit score plays a significant role, as borrowers with scores above 740 often qualify for better rates with lower down payments. Employment stability matters too, especially for tech professionals whose compensation includes RSUs or stock options that can be used toward down payments.

Available cash reserves deserve careful consideration. Even if you can afford a 20% down payment, maintaining adequate emergency funds (typically 3-6 months of expenses) protects you from unexpected repairs or income disruptions. This balance becomes particularly important in areas like Mill Creek or Lake Forest Park, where property maintenance costs can vary significantly.

Minimum Down Payment Requirements by Loan Type

Different mortgage programs offer varying minimum down payment requirements, each designed to serve specific borrower needs and financial situations.

| Loan Type | Minimum Down Payment | Best For | PMI Requirement |

|---|---|---|---|

| Conventional | 3% | Strong credit, stable income | Required below 20% |

| FHA | 3.5% | Lower credit scores, smaller down payments | Always required |

| VA | 0% | Veterans, active military | None |

| USDA | 0% | Rural/suburban eligible areas | None (guarantee fee applies) |

| Jumbo | 10-20% | High-value properties | Varies by lender |

Conventional Loans: Flexibility for Seattle Buyers

Conventional loans dominate the Seattle market, offering down payment options as low as 3% for qualified first-time buyers through programs like HomeReady and Home Possible. These loans work particularly well for buyers in Lynnwood or Shoreline who have strong credit (typically 620+) but limited cash reserves.

The key advantage of conventional financing lies in its flexibility. Once you reach 20% equity through payments or appreciation, private mortgage insurance automatically terminates, reducing your monthly payment. In Seattle's appreciating market, many borrowers reach this threshold within 5-7 years even with smaller initial down payments.

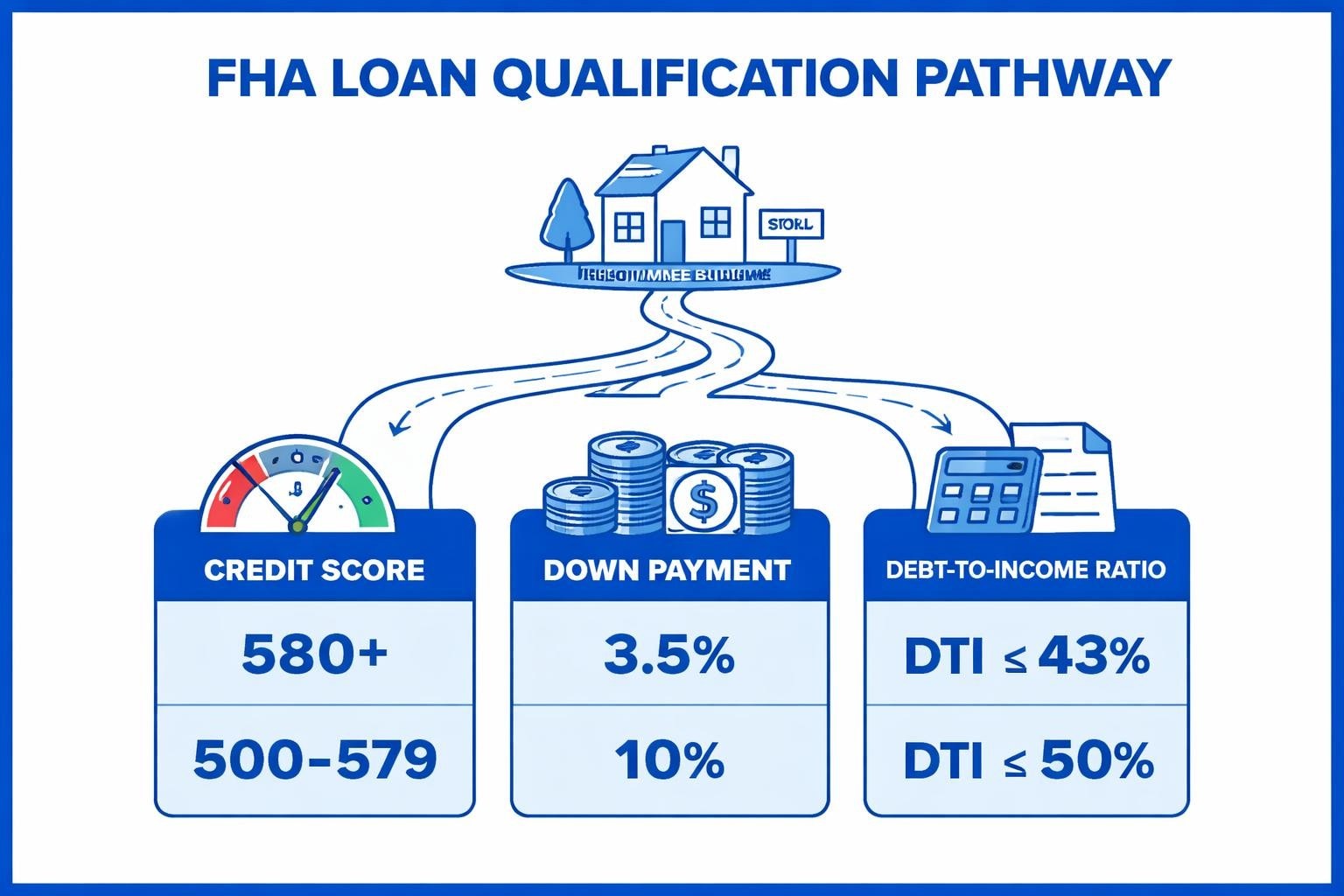

FHA Loans: Lower Down Payment on Home Purchases

FHA loans require just 3.5% down with credit scores as low as 580, making them accessible for buyers who might not qualify for conventional financing. However, FHA mortgages carry both upfront mortgage insurance (1.75% of the loan amount) and ongoing monthly premiums that remain for the life of the loan on most purchases after 2013.

For Seattle-area buyers, FHA loans make sense when:

- Credit scores fall between 580-680

- Down payment savings are limited to 3.5-5%

- The property price falls within FHA loan limits ($1,209,750 for King County in 2026)

- You plan to refinance to conventional once you build equity

VA and USDA: Zero-Down Options

Veterans, active military, and eligible surviving spouses can purchase homes with no down payment through VA loans. This benefit proves particularly valuable in expensive markets like Seattle, where even 5% down on a $800,000 home equals $40,000.

USDA loans also offer zero-down financing, but property location restrictions limit their use in the Seattle metro. However, some areas of Everett and surrounding Snohomish County may qualify, making them worth exploring for buyers seeking suburban or rural settings.

The True Cost of Your Down Payment Strategy

Beyond the immediate cash outlay, your down payment on home purchases creates long-term financial implications that extend throughout your homeownership journey.

Monthly Payment Impact

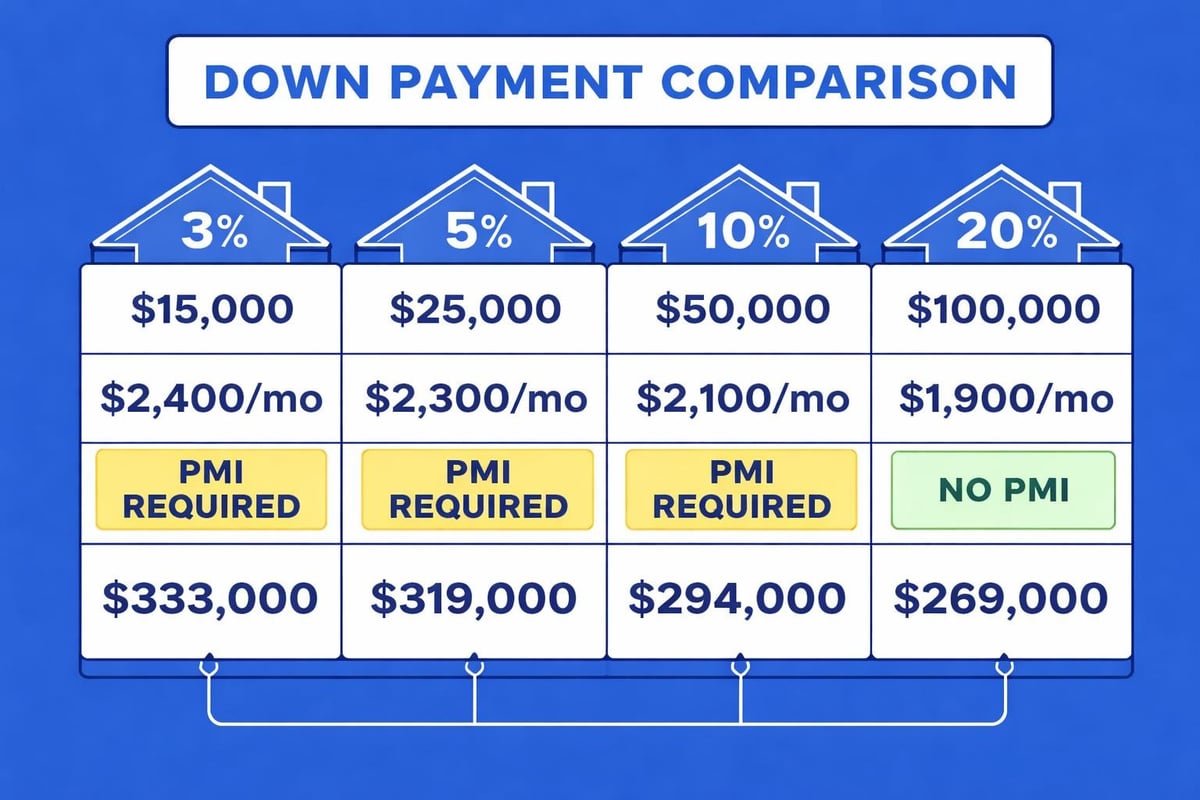

A larger down payment directly reduces your monthly mortgage payment by decreasing the principal loan amount. On a $750,000 home in Bellevue, the difference between 5% and 20% down equals approximately $650-750 per month in principal and interest alone at current rates.

Monthly payment comparison on $750,000 purchase:

- 5% down ($37,500): Loan amount $712,500, monthly P&I approximately $4,400

- 10% down ($75,000): Loan amount $675,000, monthly P&I approximately $4,170

- 20% down ($150,000): Loan amount $600,000, monthly P&I approximately $3,710

These estimates use a 6.75% interest rate typical for 2026 conventional loans. The 5% and 10% scenarios also include PMI, adding another $350-500 monthly until reaching 20% equity.

Interest Rate Considerations

Lenders price loans based on risk, and your down payment signals your financial strength. Borrowers putting down less than 20% typically pay 0.25-0.50% higher interest rates than those with larger down payments. Over 30 years, this seemingly small difference compounds significantly.

Understanding how down payments affect your overall mortgage costs helps you make informed decisions balancing immediate affordability with long-term savings.

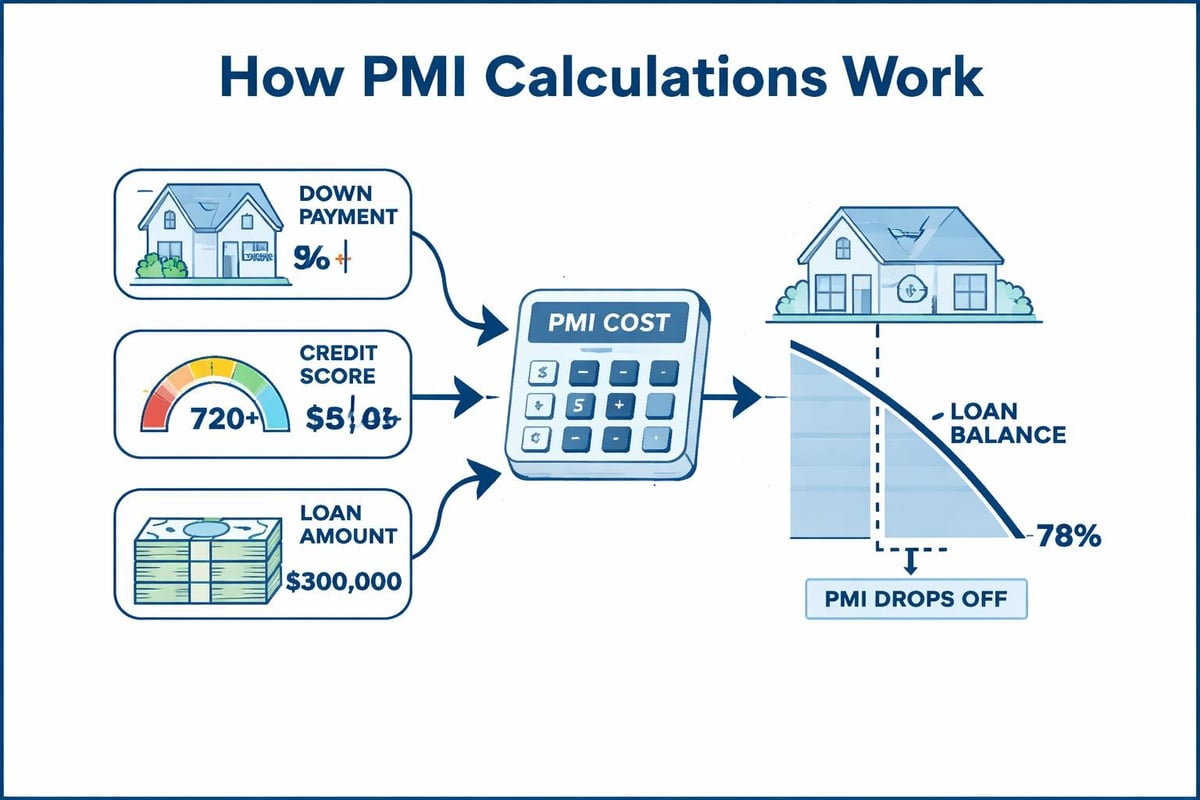

Private Mortgage Insurance Explained

Private mortgage insurance protects lenders when borrowers put down less than 20%, but it adds to your monthly housing costs without building equity. Understanding PMI mechanics helps Seattle buyers make strategic down payment decisions.

How PMI Costs Are Calculated

PMI typically ranges from 0.3% to 1.5% of the original loan amount annually, paid in monthly installments. The exact rate depends on your credit score, down payment percentage, and loan type. A borrower with a 720 credit score putting 10% down might pay 0.5% annually, while someone with a 650 score and 5% down could pay 1.2%.

On a $700,000 loan, annual PMI costs could range from:

- $2,100 (0.3% rate) = $175/month

- $5,600 (0.8% rate) = $467/month

- $8,400 (1.2% rate) = $700/month

Strategies to Avoid or Eliminate PMI

Several approaches help buyers minimize or eliminate PMI costs. The most straightforward method involves saving for a 20% down payment, though this delays homeownership in appreciating markets where prices may rise faster than you can save.

Lender-paid mortgage insurance (LPMI) shifts the PMI cost into a slightly higher interest rate, eliminating the separate monthly PMI payment. This option makes sense for buyers who plan to keep their mortgage long-term or who prioritize lower monthly payments for qualification purposes.

Piggyback loans involve taking a second mortgage (typically 10%) alongside a first mortgage (80%) to avoid PMI with just 10% down. While creative, this strategy requires qualifying for both loans and managing two monthly payments, making it less common in 2026 than it was historically.

Down Payment Sources and Strategies for Seattle Buyers

Where your down payment on home purchases comes from matters almost as much as how much you put down. Lenders scrutinize down payment sources to ensure funds come from acceptable origins and that borrowers aren't taking on excessive debt immediately before closing.

Acceptable Down Payment Sources

Verified and documented sources include:

- Personal savings from checking, savings, or money market accounts

- Retirement account withdrawals (with proper documentation and tax consideration)

- Gift funds from family members (requires gift letter stating no repayment expected)

- Proceeds from selling another property

- Grants from eligible down payment assistance programs

- Vested RSUs, stock compensation, or bonuses (critical for Seattle tech workers)

Tech Professional Down Payment Strategies

Seattle's concentration of tech employers creates unique opportunities for down payment accumulation. Many Amazon, Microsoft, and Google employees receive significant RSU compensation that can be strategically timed for home purchases.

Key considerations for using stock compensation:

- RSUs must be fully vested and sellable

- Documentation of vesting schedule and sale proceeds required

- Tax implications should be calculated (typically 35-40% withholding)

- Volatile stock prices may require flexibility in purchase timing

- Some lenders require stocks to be sold and funds seasoned for 60 days

Working with a mortgage broker experienced in tech compensation helps maximize your qualifying income while properly documenting stock-based down payments. This expertise proves especially valuable for jumbo loans common in Redmond, Kirkland, and Seattle's urban neighborhoods.

When Bigger Isn't Always Better

While larger down payments reduce monthly costs and eliminate PMI, they're not always the optimal financial strategy. Opportunity cost considerations matter significantly in 2026's financial landscape.

Preserving Liquidity and Investment Opportunity

Real estate equity is illiquid, accessible only through selling, refinancing, or home equity loans. Putting every available dollar into your down payment on home purchases can leave you cash-poor and unable to handle emergencies, fund home improvements, or capitalize on investment opportunities.

Consider keeping additional funds available for:

- Emergency reserves (minimum 3-6 months expenses)

- Moving costs, furniture, and immediate home improvements

- Property taxes and insurance (if not escrowed)

- HOA fees, utilities, and maintenance

- Retirement contributions and other investments

Investment Returns vs. Mortgage Costs

If your mortgage rate is 6.75% but you can invest conservatively at 8-10% average annual returns, putting the minimum down while investing the difference may build more wealth long-term. This strategy requires discipline, risk tolerance, and understanding that investment returns fluctuate while mortgage savings are guaranteed.

Recent analysis of down payment strategies shows that the median down payment has actually decreased as buyers prioritize preserving cash flexibility, especially in high-cost markets like Seattle.

Down Payment Assistance Programs for Seattle Area Buyers

Various programs help qualified buyers bridge the down payment gap, though awareness remains surprisingly low. Many first-time buyers in Seattle, Lynnwood, and Everett miss opportunities simply because they don't know these resources exist.

State and Local Programs

Washington State Housing Finance Commission offers several programs providing down payment and closing cost assistance. The House Key program, for instance, provides loans up to 4% of the purchase price for qualified first-time buyers with income limits that vary by county and household size.

King and Snohomish County programs include:

- Home Advantage: Down payment assistance for first-time buyers

- House Key Plus: Additional support for lower-income households

- Military and Veteran programs: Special benefits for service members

- County-specific grants: Available in some jurisdictions with residency requirements

Employer Assistance Programs

Major Seattle employers increasingly offer home buying assistance as a retention and recruitment tool. Amazon, Microsoft, and other tech companies may provide grants, forgivable loans, or matching programs to help employees purchase homes near campus locations.

These benefits vary significantly by employer and sometimes by role or tenure. Human resources departments can provide details, though mortgage brokers familiar with tech industry benefits often know more about how to properly document and use these funds for lending purposes.

Jumbo Loan Down Payment Considerations

Seattle's high home prices mean many purchases exceed conforming loan limits ($806,500 for most of the country, higher in some high-cost areas), requiring jumbo financing. These loans carry different down payment expectations and qualification standards.

Typical Jumbo Down Payment Requirements

Most jumbo lenders prefer 15-20% down payments, though qualified borrowers with excellent credit (typically 740+), strong reserves, and stable income can sometimes secure jumbo loans with 10% down. The trade-off usually involves slightly higher interest rates and more stringent documentation.

Jumbo lending focuses heavily on:

- Debt-to-income ratios (typically 43% maximum, sometimes 38%)

- Cash reserves (often 6-12 months required after closing)

- Credit score minimums (usually 700-740 depending on down payment)

- Income documentation and employment verification

- Asset verification and source of funds

Seattle Market Jumbo Realities

In neighborhoods like Madison Park, Queen Anne, or Mercer Island, median prices regularly exceed $1.5 million, making jumbo loans the norm rather than exception. Tech professionals with RSU compensation often qualify more easily than traditional W-2 employees at the same income level because their total compensation package demonstrates substantial earning power.

Specialized mortgage brokers understand how to structure jumbo applications for tech workers, properly documenting stock compensation while maintaining conservative debt-ratios that satisfy jumbo underwriting guidelines. Learn more about navigating Seattle’s mortgage landscape with experienced local expertise.

How Your Down Payment Affects Closing Costs

Your down payment on home purchases influences more than just your loan amount and monthly payment. It also affects various closing costs and the cash you need to bring to settlement.

Loan-Level Price Adjustments

Conventional loans apply pricing adjustments based on credit score and down payment combinations. A borrower with a 680 credit score putting 5% down might pay a 2.5% adjustment added to their loan amount, while the same borrower with 20% down might pay just 0.5%.

These adjustments significantly impact your effective interest rate or can be rolled into the loan amount, reducing cash needed at closing but increasing your monthly payment. Understanding these adjustments helps you optimize your down payment strategy for minimum total cost.

Title Insurance and Other Percentage-Based Fees

Some closing costs calculate as percentages of the loan amount. Larger down payments mean smaller loans and therefore lower costs for these services. However, the savings rarely justify stretching your down payment beyond your comfort level solely to reduce these fees.

Frequently Asked Questions About Home Down Payments

Can I use a personal loan for my down payment?

Lenders generally prohibit using unsecured personal loans for down payments because it increases your debt burden without adding collateral. However, secured loans against assets like paid-off vehicles or documented borrowing from retirement accounts may be acceptable with proper documentation.

How long does money need to be in my account before it counts toward down payment?

Most lenders require 60 days of bank statements showing funds "seasoned" in your accounts. Large deposits within this period require documentation showing their source. Planning ahead by consolidating funds at least two months before loan application simplifies the process.

Does earnest money count toward my down payment?

Yes, earnest money deposits (typically 1-3% of purchase price in Seattle) paid when your offer is accepted apply directly to your down payment at closing. This reduces the cash you need to bring to settlement by the earnest money amount already on deposit with the title company.

Can I change my down payment amount after pre-approval?

Absolutely. Pre-approval provides a maximum loan amount, but you can adjust your down payment up or down (within the lender's minimums) as your situation changes. Increasing your down payment may improve your rate or eliminate PMI, while decreasing it preserves cash but increases monthly costs.

Strategic Down Payment Planning for Seattle Buyers

Success in Seattle's competitive market requires strategic thinking about your down payment on home purchases. Simple rules of thumb fail to account for individual circumstances, market conditions, and financial goals.

Market Timing Considerations

Seattle's real estate market experiences seasonal patterns, with spring and summer bringing peak competition and winter offering more negotiating leverage. Your down payment strategy should account for these cycles. Having flexibility to increase your down payment slightly during competitive seasons can strengthen your offer without committing maximum funds in slower periods.

Seller perceptions matter too. In multiple-offer situations, a 20% conventional down payment often appears stronger than a 5% down payment, even if both buyers are equally qualified. Sellers and their agents perceive less financing risk with larger down payments, potentially giving you an edge even if your offer price matches competitors.

Long-Term Financial Planning Integration

Your home down payment should integrate with broader financial planning, not exist in isolation. Contributing to retirement accounts, maintaining emergency funds, and preserving investment capital all compete with maximizing your down payment.

A balanced approach considers:

- Your age and years until retirement

- Other major expenses on the horizon (education, business investment)

- Risk tolerance and comfort with monthly payment amounts

- Career trajectory and income growth expectations

- Plans for the property (long-term residence vs. stepping stone)

Working with financial advisors alongside mortgage professionals creates comprehensive strategies aligning your down payment decision with overall wealth-building goals. This coordination proves especially valuable for high-earning tech professionals in Bellevue and Seattle managing complex compensation structures.

Regional Market Insights: Down Payment Trends Across Greater Seattle

Different submarkets within the Greater Seattle area show varying down payment patterns reflecting local price points, buyer demographics, and housing stock characteristics.

Seattle Proper: Premium Prices, Varied Strategies

Downtown Seattle, Capitol Hill, and Ballard attract a mix of first-time buyers using minimum down payments and affluent buyers putting substantial cash down. The median down payment in central Seattle neighborhoods often exceeds 15%, though FHA and low-down conventional loans remain common in more affordable areas.

Eastside Markets: Tech Money and Larger Down Payments

Bellevue, Redmond, and Kirkland show higher average down payments, often 20% or more, reflecting the concentration of tech professionals with RSU compensation. Jumbo loans dominate these markets, and sellers have come to expect strong down payments as a signal of buyer seriousness and financial strength.

North End Suburbs: First-Time Buyer Territory

Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett attract substantial first-time buyer activity, where down payments of 5-10% are common. These areas offer better affordability while maintaining access to Seattle employment centers, making them ideal for buyers building wealth through homeownership despite limited initial cash.

Understanding your down payment options helps you compete effectively regardless of which Greater Seattle submarket you're targeting.

Documentation Requirements for Your Down Payment

Lenders verify every dollar of your down payment on home purchases through extensive documentation. Being prepared with proper paperwork accelerates your loan process and prevents last-minute scrambling.

Bank Statement Requirements

Expect to provide two months of statements for all accounts contributing to your down payment. Statements must show all pages, including blank pages, and clearly display account numbers, your name, and current balances. Digital screenshots or partial statements typically won't suffice.

Red flags that trigger additional documentation requirements:

- Large deposits not matching regular payroll

- Transfers between accounts without clear purpose

- Recent account openings or large balance increases

- Overdrafts or negative balances

- Unexplained withdrawals or irregular transactions

Gift Documentation

Gift funds require a gift letter signed by the donor stating the amount, relationship to you, property address, and confirmation that no repayment is expected. Additionally, lenders need donor bank statements proving the donor had sufficient funds and documentation of the transfer into your account.

Some loan programs limit gift usage or require minimum borrower contribution from personal funds. Conventional loans generally allow 100% gift funding for down payments above 20%, while lower down payments may require 5% personal contribution.

Understanding the nuances of your down payment on home purchases empowers you to make strategic decisions aligned with your financial goals and market realities. Whether you're a first-time buyer in Mill Creek or a tech professional purchasing a jumbo property in Bellevue, the right down payment strategy balances monthly affordability, long-term costs, and cash preservation. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area buyers navigate these decisions with clarity and confidence, specializing in everything from first-time buyer programs to complex jumbo loans utilizing RSU compensation for maximum buying power.