Purchasing your first home in Seattle's competitive market can feel overwhelming, especially when navigating mortgage options with limited savings or moderate credit scores. The fha first time home loan has become one of the most accessible pathways to homeownership for buyers across Seattle, Bellevue, Redmond, and Kirkland, offering flexible qualification standards and low down payment requirements. Unlike conventional loans that typically require 20 percent down, FHA loans allow eligible borrowers to secure financing with as little as 3.5 percent down, making them particularly attractive for tech professionals, young families, and anyone building equity for the first time. Understanding how these loans work, what they require, and how to maximize your approval odds can significantly accelerate your journey toward homeownership in the Puget Sound region.

What Makes an FHA First Time Home Loan Different

The Federal Housing Administration backs these mortgages through approved lenders, reducing risk and enabling more generous qualification criteria than conventional financing. This government insurance allows lenders to approve borrowers who might not meet traditional underwriting standards.

Lower Down Payment Requirements

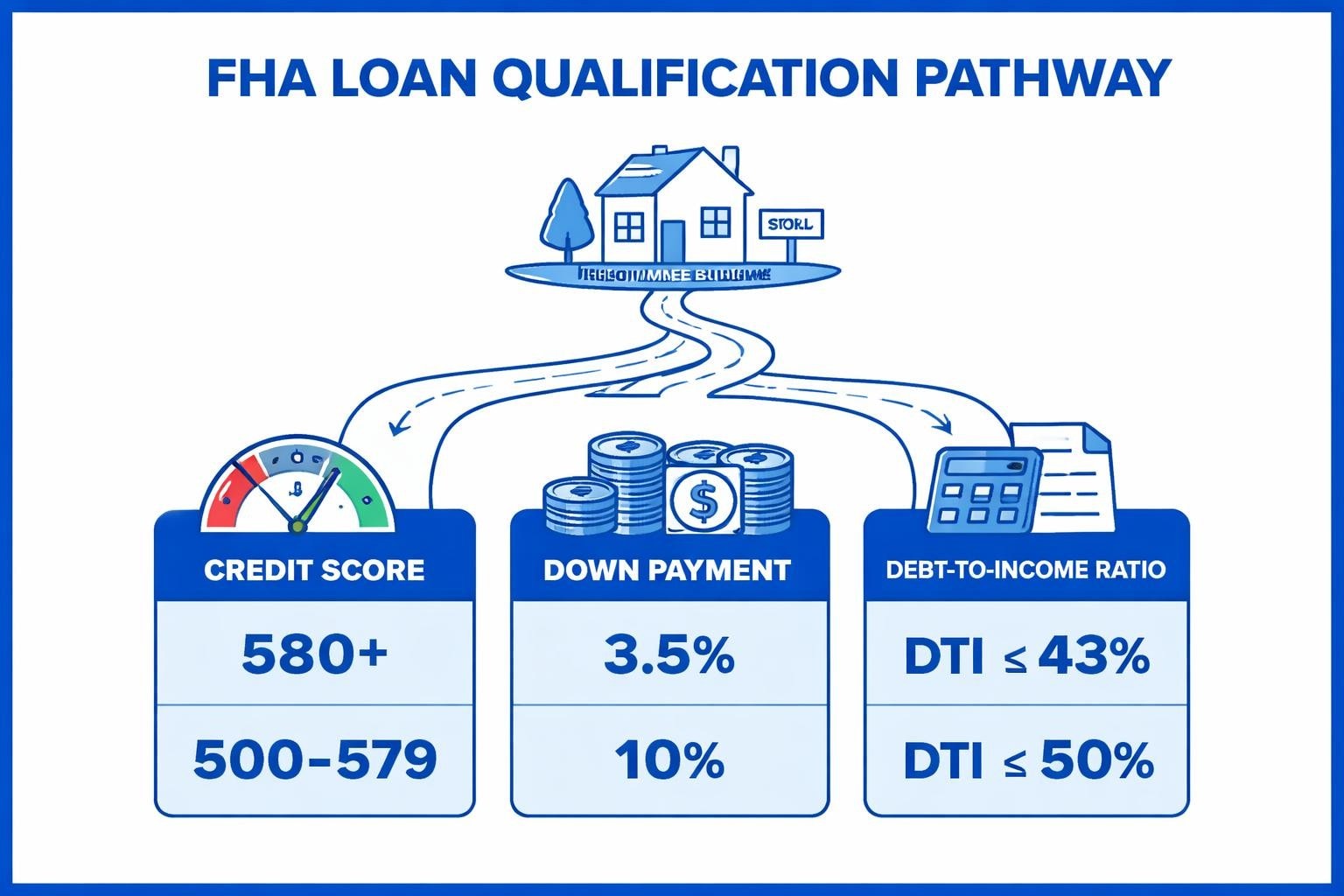

FHA loans require just 3.5 percent down for borrowers with credit scores of 580 or higher. For a $600,000 home in Shoreline, that translates to $21,000 rather than the $120,000 needed for a conventional 20 percent down payment.

- Minimum 10 percent down required for credit scores between 500-579

- Down payment can come from savings, gifts, or down payment assistance programs

- Sellers can contribute up to 6 percent toward closing costs

This accessibility has made the fha first time home loan a cornerstone strategy for first-time buyers navigating Seattle’s housing market, where median home prices consistently challenge entry-level budgets.

Flexible Credit Score Standards

While conventional loans increasingly demand scores above 680 for competitive rates, FHA financing accepts borrowers with:

- Credit scores as low as 580 with 3.5 percent down

- Scores between 500-579 with 10 percent down

- Recent credit challenges including past bankruptcies or foreclosures (with waiting periods)

| Credit Event | FHA Waiting Period | Conventional Waiting Period |

|---|---|---|

| Chapter 7 Bankruptcy | 2 years | 4 years |

| Chapter 13 Bankruptcy | 1 year (with payments) | 2-4 years |

| Foreclosure | 3 years | 7 years |

| Short Sale | 3 years | 4 years |

These timelines assume responsible financial management following the credit event. Lenders review the full credit narrative, not just the score itself.

Understanding FHA Loan Limits in Seattle Metro

The FHA sets maximum loan amounts based on county median home prices, which are updated annually. For 2026, these limits directly impact how much you can borrow in different areas.

King County Loan Limits

King County, which includes Seattle, Bellevue, and Redmond, has higher limits reflecting the elevated cost of housing:

- Single-family home limit: $1,209,750

- Two-unit property limit: $1,548,450

- Three-unit property limit: $1,871,800

- Four-unit property limit: $2,326,000

These amounts represent the maximum loan value the FHA will insure in this market. Buyers purchasing above these thresholds need alternative financing, such as jumbo loan programs available through specialized lenders.

Snohomish County Considerations

For buyers exploring Lynnwood, Mill Creek, or Everett, Snohomish County has identical limits to King County due to similar housing costs. This consistency simplifies planning for buyers considering homes in both markets.

The fha first time home loan structure allows you to maximize borrowing capacity while maintaining manageable monthly payments through extended 30-year terms and competitive interest rates.

Mortgage Insurance Requirements You Need to Know

FHA loans include both upfront and ongoing mortgage insurance premiums that protect the lender against default risk. Understanding these costs is essential for accurate budget planning.

Upfront Mortgage Insurance Premium (UFMIP)

Every FHA loan includes a 1.75 percent upfront premium calculated on the base loan amount. On a $550,000 mortgage, that equals $9,625. Most borrowers finance this amount into the loan rather than paying cash at closing.

Annual Mortgage Insurance Premium (MIP)

Monthly mortgage insurance continues for the life of the loan on most fha first time home loan agreements:

- 0.55 percent annual rate for loans over $726,200 with less than 5 percent down

- 0.50 percent annual rate for loans under $726,200 with less than 5 percent down

- 0.15-0.75 percent depending on loan amount, term, and down payment

On a $550,000 loan, expect approximately $229 monthly for mortgage insurance. Unlike conventional PMI, which cancels at 20 percent equity, FHA MIP typically remains for the entire loan term unless you refinance.

| Down Payment | Loan Term | MIP Duration |

|---|---|---|

| Less than 10% | 30 years | Life of loan |

| 10% or more | 30 years | 11 years |

| Any amount | 15 years | 11 years |

This permanent insurance is a trade-off for the lower initial barriers to entry that make FHA loans accessible.

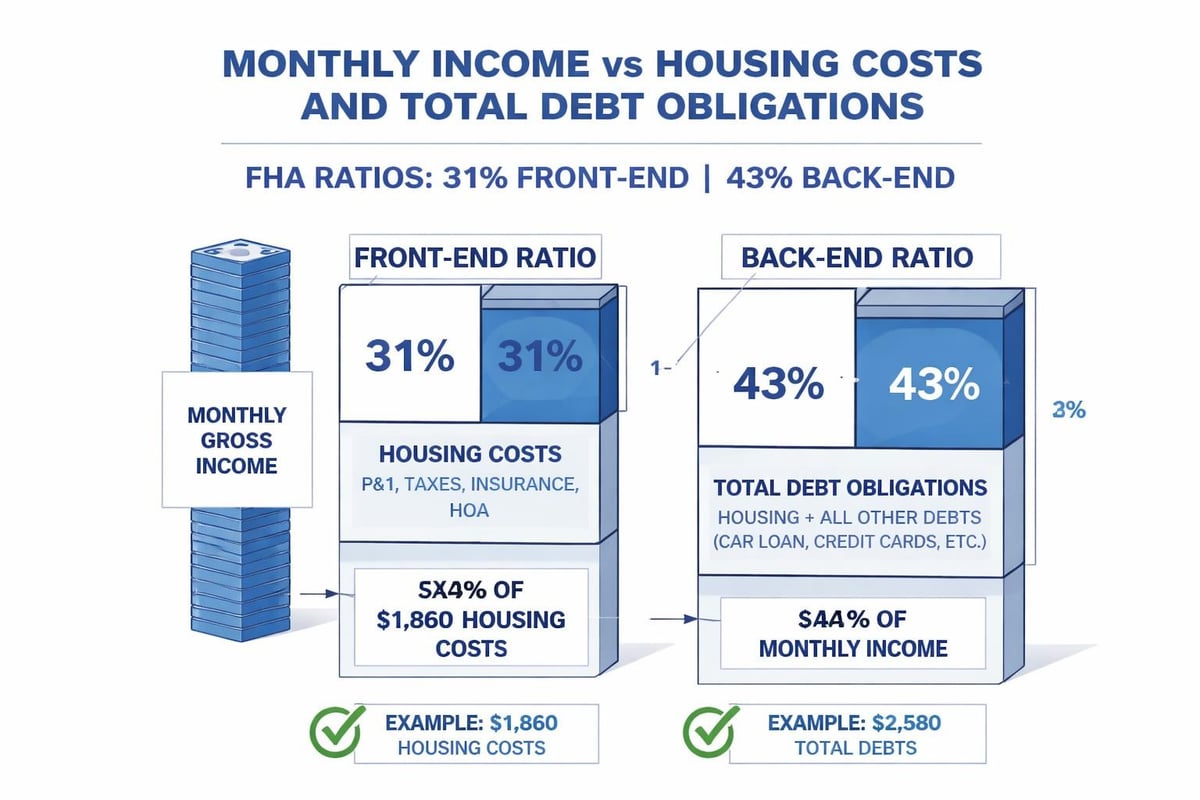

Debt-to-Income Ratio Guidelines

FHA underwriting evaluates your ability to manage monthly obligations relative to gross income. These ratios determine how much house you can afford.

Front-End Ratio (Housing Expense)

Your total housing payment, including principal, interest, taxes, insurance, and HOA fees, should not exceed 31 percent of gross monthly income. For a tech professional earning $120,000 annually ($10,000 monthly), that caps housing costs at $3,100.

Back-End Ratio (Total Debt)

All monthly obligations-housing payment plus car loans, student loans, credit cards, and other debts-must stay under 43 percent of gross income. Using the same $10,000 monthly income, total debts cannot exceed $4,300.

Experienced lenders can sometimes approve ratios up to 46.9 percent or even 50 percent with compensating factors:

- Significant cash reserves (six months or more)

- Minimal increase from current rent to proposed mortgage

- Strong credit history with no recent delinquencies

- Additional income sources not fully counted in qualification

For Amazon, Microsoft, and Google employees with stock compensation, working with a broker experienced in tech income qualification ensures RSUs and bonuses are properly documented and maximized.

Property Standards and Inspection Requirements

The FHA mandates specific property conditions to ensure the home is safe, sound, and sanitary. This protects both you and the government's insurance investment.

FHA Appraisal Process

An FHA-approved appraiser must inspect the property and verify:

- Structural integrity of foundation, roof, and load-bearing elements

- Working systems including electrical, plumbing, and heating

- Safe access with functional stairs, railings, and walkways

- Adequate ventilation and moisture control

- Compliant electrical panels (no outdated fuse boxes in many cases)

In Seattle's older housing stock, particularly in neighborhoods like Lake Forest Park and parts of Shoreline, these inspections sometimes reveal needed repairs. Sellers must complete required fixes before closing, or buyers can negotiate repair credits.

Common Property Issues

Homes with the following conditions may not qualify for an fha first time home loan without corrections:

- Peeling paint (lead-based paint hazard on pre-1978 homes)

- Damaged or missing handrails on stairs

- Evidence of active roof leaks or water damage

- Cracked or broken windows

- Non-functioning major appliances that convey with the property

These standards sometimes create negotiation opportunities. Motivated sellers often address repairs rather than lose qualified FHA buyers.

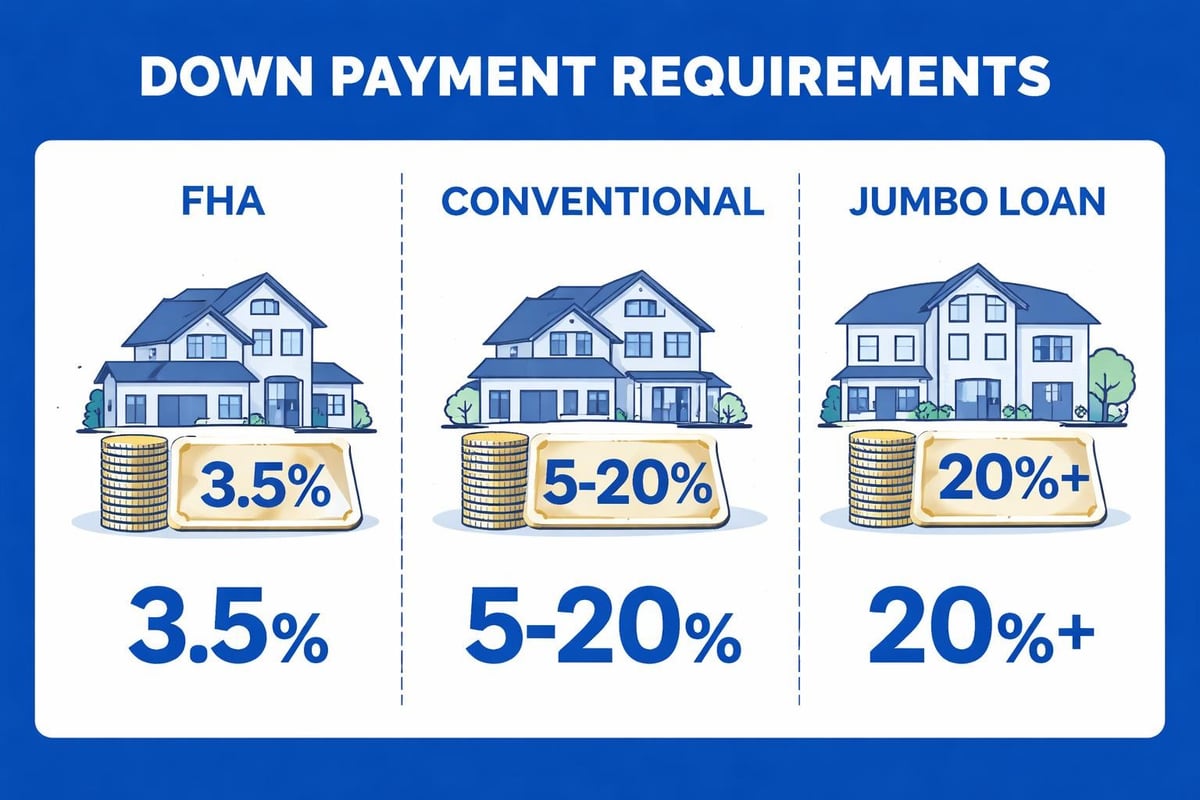

Comparing FHA to Conventional Loan Options

Many first-time buyers weigh the fha first time home loan against conventional financing with lower down payments. Each path offers distinct advantages depending on your financial profile.

When FHA Makes More Sense

Choose FHA financing if you have:

- Credit scores between 580-680 where conventional rates become expensive

- Limited savings requiring the minimum 3.5 percent down

- Recent credit challenges within the past 2-4 years

- Higher debt ratios near or above 43 percent

When Conventional Is Better

Consider conventional loans when you can:

- Put down 5-10 percent with a credit score above 700

- Avoid permanent mortgage insurance by reaching 20 percent equity faster

- Purchase a condo that isn't FHA-approved but meets Fannie Mae standards

- Exceed FHA loan limits while staying under jumbo thresholds

| Feature | FHA | Conventional (5% Down) |

|---|---|---|

| Minimum Credit Score | 580 | 620 |

| Down Payment | 3.5% | 5% |

| Mortgage Insurance | Life of loan | Cancels at 78% LTV |

| Seller Concessions | Up to 6% | Up to 3% |

| Property Standards | Strict | Moderate |

Working with knowledgeable Seattle mortgage brokers allows you to compare live pricing across both programs and select the option that minimizes long-term costs.

Income Documentation for Tech Professionals

Seattle's concentration of high-paying tech employers creates unique opportunities for first-time buyers using FHA financing, particularly when qualifying stock compensation.

Base Salary Qualification

W-2 wage earners need:

- Two years of continuous employment history (same field, not necessarily same employer)

- Recent pay stubs covering the most recent 30-day period

- W-2 forms from the previous two years

- Verbal verification of employment from HR departments

Restricted Stock Units (RSUs) and Bonuses

Tech compensation includes substantial non-salary income that can significantly increase buying power. FHA underwriting allows:

- Two-year average of RSUs if you have consistent vesting history

- Bonus income averaged over two years if regularly received

- Stock grants documented through paystubs and vesting schedules

A Microsoft engineer earning $140,000 base salary plus $60,000 annual in RSUs could qualify using $200,000 in total income after meeting documentation requirements. This dramatically increases the affordable purchase price.

Down Payment Assistance Programs

Multiple state and local programs help first-time buyers in the Seattle metro area supplement their down payment and closing costs, making the fha first time home loan even more accessible.

Washington State Housing Finance Commission

The Commission offers several programs:

- House Key Down Payment Assistance: Up to 4 percent of the purchase price as a 0 percent interest second loan

- House Key Open Doors: Conventional loan product with just 3 percent down

- Home Advantage: Combines low down payment with closing cost assistance

These programs have income and purchase price limits but can provide thousands in additional funding. A buyer in Everett purchasing a $475,000 home could receive up to $19,000 in assistance.

Local City and County Programs

Seattle, Bellevue, and King County maintain additional assistance resources:

- Income-restricted grants for low-to-moderate income households

- Employer-assisted housing programs through major tech companies

- Matched savings programs requiring participant contributions

Combining FHA's low 3.5 percent requirement with assistance grants sometimes enables homeownership with minimal personal savings invested.

The FHA Loan Application Timeline

Understanding the process from application to closing helps you plan effectively and avoid delays in competitive markets where quick closings matter.

Pre-Approval Phase (3-5 Days)

Submit complete documentation including:

- Two years of tax returns

- Recent pay stubs (most recent 30 days)

- Bank statements for all accounts (2 months)

- Photo ID and Social Security card

- Rental history or mortgage statements

A thorough pre-approval letter demonstrates serious intent to Seattle-area sellers receiving multiple offers.

Home Search and Offer

With pre-approval in hand, work with a real estate agent familiar with FHA property requirements. Not all homes meet FHA standards, so experienced representation prevents wasted time on incompatible properties.

Processing and Underwriting (10-14 Days)

Once under contract:

- Lender orders the FHA appraisal

- Title company conducts property research

- Underwriter reviews full documentation package

- Any required repairs are identified and negotiated

Clear to Close (2-3 Days Before Closing)

Final approval arrives after:

- Satisfactory appraisal results

- Completion of any required property repairs

- Verification of employment and assets

- Final underwriting sign-off

The entire fha first time home loan process typically takes 30-35 days from application to funding, though experienced brokers with efficient operations can close faster when needed.

Strategic Considerations for Seattle Buyers

The unique characteristics of Puget Sound housing markets require specific approaches to maximize FHA loan effectiveness.

Multiple Offer Situations

Seattle's competitive environment means most desirable properties receive multiple bids. Strengthen your FHA offer by:

- Larger earnest money deposits showing commitment

- Complete pre-approval with full underwriting review

- Flexible closing timelines accommodating seller needs

- Pre-inspected properties waiving feasibility contingencies when appropriate

Some sellers perceive FHA buyers as weaker due to property condition requirements. Combat this bias with strong financial positioning and responsive communication.

Condo Considerations

Purchasing a condominium with an fha first time home loan requires FHA approval of the entire building. The HOA must meet specific requirements:

- At least 50 percent owner-occupied units

- Maximum 15 percent of units delinquent on HOA dues

- Adequate insurance coverage and reserve funding

- No ongoing litigation against the association

Many newer Seattle condos maintain FHA approval, but always verify status before making an offer to avoid wasted time and inspection costs.

Timing Your Purchase

Interest rates, inventory levels, and seasonal competition all affect your buying power. Consider:

- Winter months (November-February) typically see less competition in Seattle

- Spring markets (March-June) offer maximum inventory but intense bidding

- Rate trends in 2026 favor those prepared to act when opportunities arise

Monitoring current Seattle mortgage rates helps you time your application to secure favorable pricing.

Common Mistakes to Avoid

Even qualified buyers sometimes derail their fha first time home loan approval through preventable errors during the application process.

Financial Changes During Underwriting

Maintain financial stability from application through closing:

- Avoid new credit inquiries or opening additional accounts

- Don't make large purchases that increase debt-to-income ratios

- Maintain employment without changing jobs or careers

- Keep consistent bank account balances without unexplained deposits

A buyer approved with a 42 percent debt ratio who finances a $35,000 car during escrow will likely lose their approval.

Insufficient Documentation

Missing or incomplete paperwork causes delays. Submit everything requested:

- Full bank statements showing all pages (not just summary pages)

- Explanation letters for any unusual deposits or credit items

- Gift letters and documentation if using gifted down payment funds

- Complete tax returns with all schedules

Unrealistic Property Expectations

Some buyers target homes unlikely to meet FHA standards. Red flags include:

- Properties marketed "as-is" or needing significant work

- Homes with obvious deferred maintenance visible in listing photos

- Rural properties on septic systems requiring specialized inspections

- Condos in buildings not yet FHA-approved

Set realistic expectations aligned with FHA property requirements to avoid repeated disappointment.

Refinancing Options After Purchase

Many fha first time home loan borrowers eventually refinance to eliminate mortgage insurance or access equity. Understanding future options informs smart initial decisions.

FHA Streamline Refinance

After at least six monthly payments, you can refinance to a lower rate through the streamlined process:

- No appraisal required in most cases

- Minimal documentation compared to full refinance

- Lower closing costs than conventional refinancing

- Must demonstrate net benefit through lower payment or rate

The streamline maintains FHA insurance, so it doesn't eliminate MIP but can reduce monthly costs when rates drop.

Conventional Refinance

Once you've built 20 percent equity, refinancing to conventional eliminates monthly mortgage insurance entirely. For a $550,000 purchase, reaching $440,000 loan balance qualifies you for conventional refinancing without MI.

This strategy requires:

- Credit score improvement to 680+ for best conventional rates

- Stable employment with two years at current position

- Low debt ratios maintaining qualification standards

Many Seattle buyers use the FHA loan as a stepping stone, then refinance to conventional within 3-5 years as equity builds and credit strengthens.

How Local Market Knowledge Matters

Working with mortgage professionals deeply familiar with Seattle, Bellevue, Redmond, Kirkland, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett provides advantages beyond basic loan qualification.

Neighborhood-Specific Insights

Different areas present unique opportunities:

- Shoreline offers relatively affordable single-family homes within Seattle school proximity

- Lake Forest Park features established neighborhoods with good FHA-eligible housing stock

- Everett provides entry-level pricing for buyers stretching maximum qualification

- Mill Creek attracts families with newer construction and planned communities

Experienced local brokers guide you toward neighborhoods where your fha first time home loan budget aligns with realistic property options.

Lender and Underwriter Relationships

Brokers with established relationships at FHA-approved lenders can:

- Expedite underwriting review through direct communication channels

- Navigate complex income situations common among tech employees

- Troubleshoot appraisal challenges specific to Seattle's housing stock

- Close transactions quickly when competing offers demand speed

These relationships prove invaluable when your offer competes against conventional or cash buyers.

Building Long-Term Wealth Through Homeownership

The fha first time home loan serves as the foundation for building equity and financial stability in one of the nation's strongest real estate markets.

Equity Accumulation

Seattle home values have historically appreciated 4-6 percent annually over extended periods. A $575,000 home purchased in 2026 could be worth:

- $612,000 after two years (4% annual growth)

- $689,000 after five years

- $829,000 after ten years

With just $20,125 down (3.5%), you control an asset generating substantial wealth while living in it.

Tax Benefits

Homeownership provides ongoing tax advantages:

- Mortgage interest deduction on loans up to $750,000

- Property tax deduction up to $10,000 annually

- No capital gains tax on up to $250,000 profit (single) or $500,000 (married) when selling primary residence

These benefits reduce effective housing costs compared to renting equivalent properties.

Forced Savings Mechanism

Each monthly payment builds equity through principal reduction. Unlike rent-which generates no equity-your housing payment becomes investment in an appreciating asset. Over a 30-year term, even with mortgage insurance costs, total equity accumulation substantially exceeds the alternative of continued renting.

The fha first time home loan remains one of the most effective pathways to Seattle-area homeownership for buyers with moderate credit, limited savings, or unique income situations common among tech professionals. Understanding qualification requirements, property standards, and strategic application timing maximizes your approval odds while minimizing long-term costs. Keith Akada brings 25+ years of mortgage expertise to first-time buyers throughout Seattle, Bellevue, Redmond, Kirkland, and surrounding communities, with specialized knowledge in qualifying complex tech compensation and closing loans efficiently in competitive markets. Whether you're ready to start your pre-approval or have questions about how FHA compares to other loan options, connect with Mortgage Reel to develop a personalized strategy that gets you into your first home with confidence.