Understanding the fha requirements for home loan approval can make the difference between homeownership and another year of renting, especially in competitive markets like Seattle, Bellevue, and Redmond. FHA loans remain one of the most accessible mortgage options for first-time buyers, moderate-income households, and borrowers rebuilding credit. With lower down payment requirements and flexible credit guidelines compared to conventional financing, these government-backed mortgages help thousands of Washington state residents purchase homes each year. Whether you're searching in Shoreline, Lynnwood, or Lake Forest Park, knowing exactly what lenders require can streamline your application and strengthen your offer.

Credit Score Standards for FHA Financing

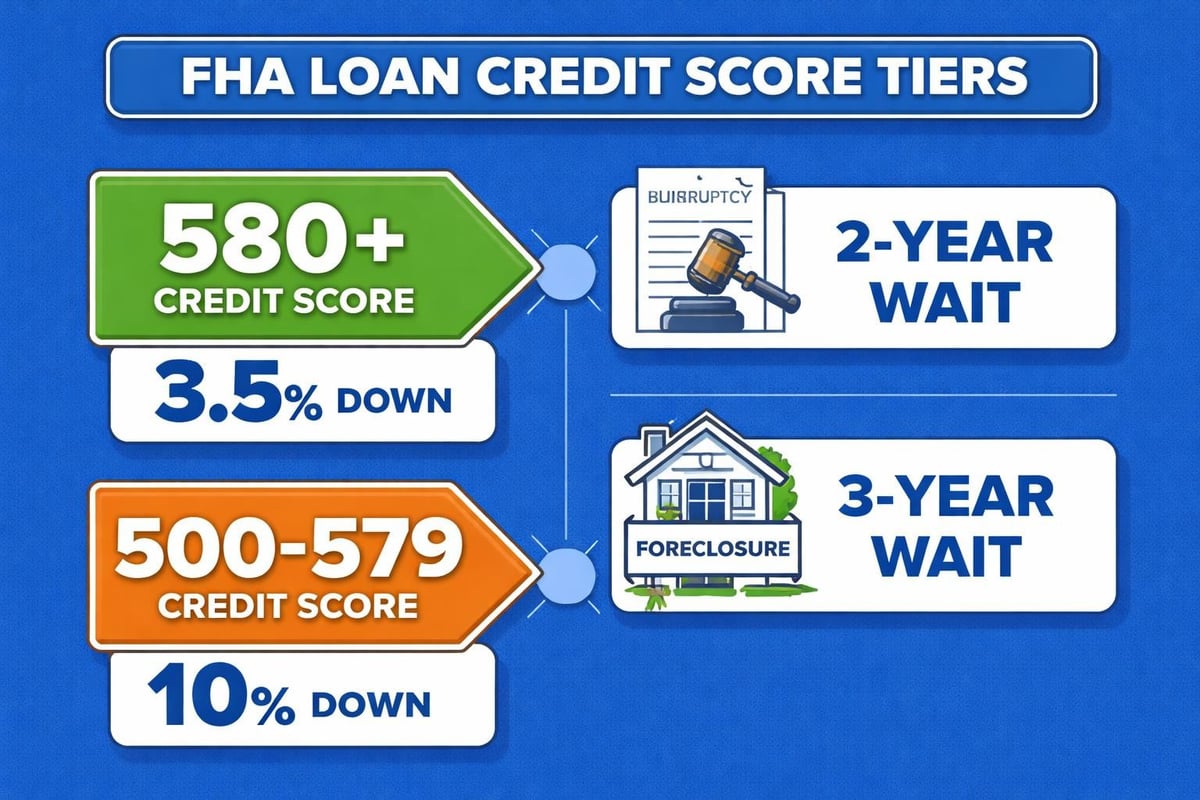

The Federal Housing Administration sets minimum credit score thresholds that determine your down payment requirement and overall eligibility. Borrowers with credit scores of 580 or higher qualify for the minimum 3.5% down payment option, which makes FHA loans particularly attractive for those who haven't accumulated significant savings.

If your credit score falls between 500 and 579, you can still potentially qualify, but you'll need to provide a 10% down payment. This higher threshold compensates lenders for the increased risk associated with lower credit profiles.

Key credit considerations include:

- Payment history over the past 12-24 months carries significant weight

- Recent bankruptcies require a waiting period of two years from discharge

- Foreclosures typically require a three-year waiting period

- Collections and charge-offs don't automatically disqualify you

- Credit disputes should be resolved before application

Most Seattle-area lenders prefer scores above 620 for smoother underwriting, though the official FHA minimum remains 580. Working with an experienced mortgage broker can help you understand which compensating factors might offset a borderline credit score, such as substantial cash reserves or a low debt-to-income ratio.

How Seattle's Housing Market Affects Credit Requirements

In competitive neighborhoods throughout Mill Creek and Everett, sellers often receive multiple offers. A stronger credit profile can make your FHA offer more attractive, even though the loan type itself doesn't change. Demonstrating financial stability through solid credit helps sellers feel confident you'll successfully close.

Down Payment and Upfront Costs

The fha requirements for home loan down payments are among the most borrower-friendly in the mortgage industry. The minimum 3.5% down payment can come from multiple sources, providing flexibility that conventional mortgage programs don't always offer.

Acceptable down payment sources:

- Personal savings and checking accounts

- Gift funds from family members (with proper documentation)

- Down payment assistance programs

- Employer assistance programs

- Proceeds from sale of personal property

You'll also need funds for closing costs, which typically range from 2% to 5% of the purchase price. In Seattle's market, where median home prices remain elevated, this can represent a substantial amount even on an FHA loan.

| Expense Category | Typical Cost Range | Can Be Financed? |

|---|---|---|

| Upfront Mortgage Insurance Premium | 1.75% of loan amount | Yes, rolled into loan |

| Appraisal Fee | $500-$800 | No, paid at application |

| Title Insurance | $1,000-$2,500 | Negotiable with seller |

| Origination Fees | 0%-1% of loan amount | No |

| Prepaid Property Taxes | Varies by purchase date | No |

Many first-time buyers in Lynnwood and Lake Forest Park successfully negotiate seller concessions to cover a portion of closing costs. FHA guidelines allow sellers to contribute up to 6% of the purchase price toward buyer closing costs, which can preserve your savings for reserves and post-closing expenses.

Income Documentation and Employment Verification

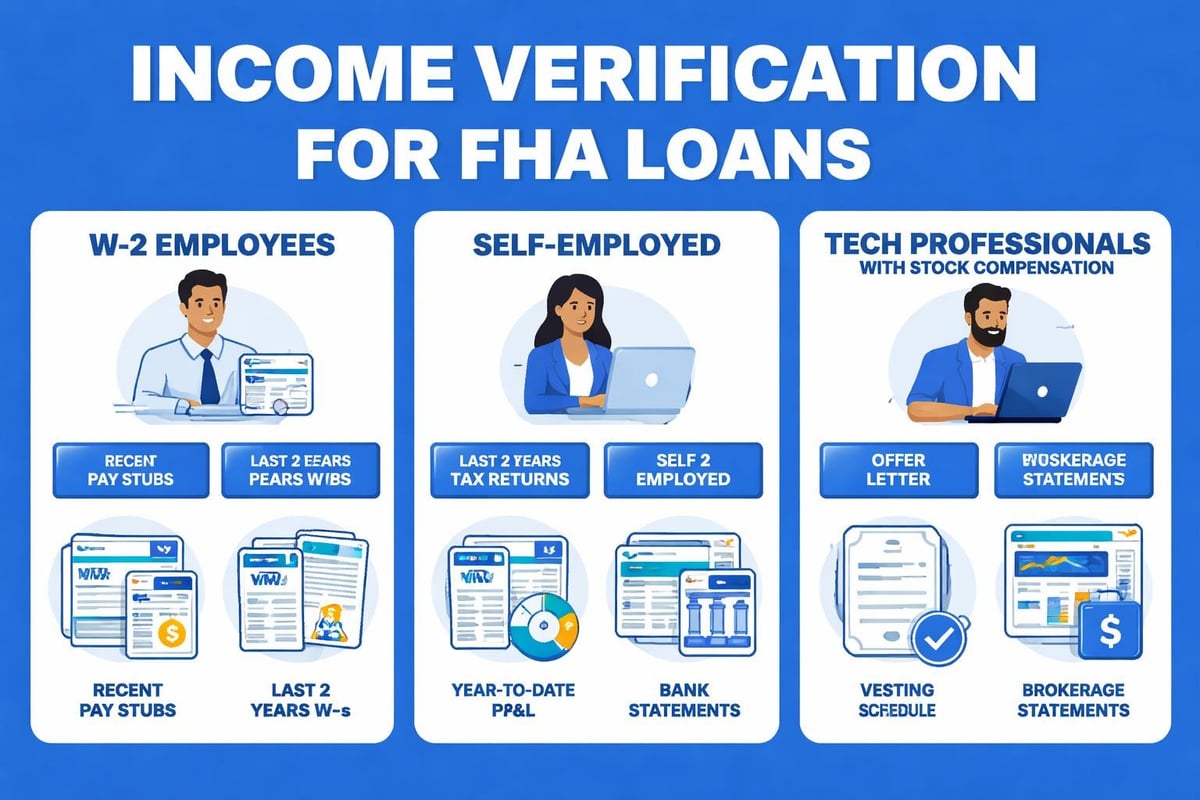

Lenders must verify stable, reliable income to ensure you can handle monthly mortgage payments. The fha requirements for home loan income verification are thorough but straightforward for most W-2 employees.

Standard documentation includes:

- Two years of W-2 forms

- Two years of federal tax returns with all schedules

- Recent pay stubs covering 30 days

- Year-to-date earnings statement

- Verification of Employment (VOE) form completed by employer

For Seattle tech professionals working at Amazon, Microsoft, or Google, income verification becomes more nuanced. Stock compensation, bonuses, and RSUs require special handling. While FHA guidelines allow these income sources, lenders must establish a two-year history and demonstrate likelihood of continuation.

Self-Employed Borrowers and FHA Loans

Business owners and self-employed individuals face additional documentation requirements. You'll typically need two years of personal and business tax returns, profit and loss statements, and possibly a CPA letter verifying your business structure and income stability.

The key challenge for self-employed borrowers involves write-offs and deductions. While these reduce your tax liability, they also reduce your qualifying income for mortgage purposes. Strategic tax planning in the years before applying can help maximize your borrowing power.

Debt-to-Income Ratio Limits

Your debt-to-income (DTI) ratio compares monthly debt obligations to gross monthly income. According to NerdWallet’s article on FHA loan requirements, FHA guidelines generally allow DTI ratios up to 43%, though some lenders approve ratios as high as 50% with compensating factors.

The DTI calculation includes:

- Proposed monthly mortgage payment (principal, interest, taxes, insurance, HOA fees)

- Car loans and lease payments

- Student loan payments

- Credit card minimum payments

- Personal loans

- Child support and alimony obligations

In Seattle's expensive housing market, many qualified buyers push against these DTI limits. A software engineer in Redmond earning $150,000 annually might comfortably afford a $650,000 home with an FHA loan, but still needs to manage existing debts carefully to stay within ratio guidelines.

Strategies to improve your DTI ratio:

- Pay down credit card balances before applying

- Avoid taking on new debt in the months before purchase

- Consider paying off small installment loans

- Increase income through bonuses or side work

- Request student loan forbearance if applicable

Understanding these ratios helps you realistically assess how much home you can afford in Shoreline versus Mill Creek, where price points and property taxes vary significantly.

Property Standards and Appraisal Requirements

FHA loans come with specific property condition standards designed to protect both borrowers and the FHA insurance fund. The home must serve as your primary residence and meet minimum safety, security, and structural integrity requirements.

During the FHA appraisal, the appraiser evaluates both market value and property condition. Issues that commonly arise in older Seattle-area homes include:

- Peeling exterior paint (potential lead-based paint hazard)

- Missing handrails on stairs

- Non-functioning mechanical systems

- Roof damage or deterioration

- Foundation cracks or settlement

- Safety hazards like exposed wiring

Properties that don't meet FHA standards require repairs before closing. The LendEDU guide on FHA loan requirements provides detailed information about property inspection criteria and how repairs are handled during the transaction.

Condominiums and FHA Approval

Not all condominium projects qualify for FHA financing. The entire building or development must receive FHA approval, which requires proper insurance coverage, adequate reserves, and adherence to owner-occupancy ratios.

Before making an offer on a Bellevue or Kirkland condo, verify the project's FHA approval status. This prevents complications during underwriting and protects your earnest money deposit.

| Property Type | FHA Eligible? | Special Requirements |

|---|---|---|

| Single-family detached | Yes | Must meet minimum property standards |

| Townhome | Yes | Same as single-family |

| Condo (FHA-approved) | Yes | Project must be on approved list |

| Manufactured home | Yes | Must be on permanent foundation, built after 1976 |

| Multi-unit (2-4 units) | Yes | Borrower must occupy one unit |

Mortgage Insurance Premiums

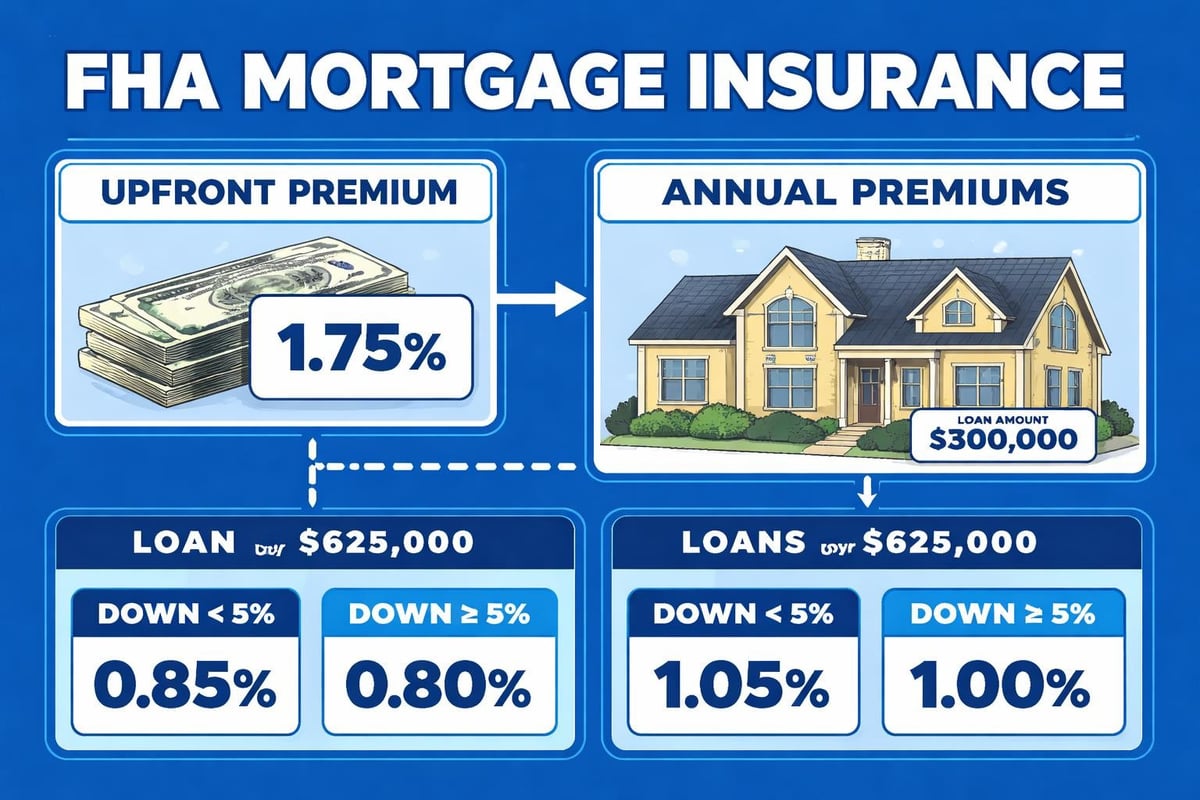

All FHA loans require two types of mortgage insurance, regardless of down payment size. This insurance protects lenders if borrowers default, enabling the flexible qualifying guidelines that make FHA loans accessible.

The upfront mortgage insurance premium (UFMIP) equals 1.75% of the base loan amount. According to Rate.com’s resource on FHA qualifications, this fee is typically financed into the loan rather than paid at closing, minimizing out-of-pocket costs.

Annual mortgage insurance premiums (MIP) vary based on loan amount, loan-to-value ratio, and loan term:

- Loans with LTV above 95%: 0.85% annually

- Loans with LTV of 95% or below: 0.80% annually

- Loans under $726,200 with terms of 15 years or less: 0.45%-0.70% annually

This annual premium divides into 12 monthly installments added to your mortgage payment. For a $500,000 FHA loan with 3.5% down in Seattle, you'd pay approximately $354 monthly for mortgage insurance.

Important consideration: Unlike conventional loans, FHA mortgage insurance typically remains for the life of the loan if you put down less than 10%. This long-term cost should factor into your comparison between FHA and other loan programs, particularly if you're comparing with jumbo loan benefits for higher-priced properties.

FHA Loan Limits in King County

The FHA sets maximum loan amounts that vary by county and housing type. For 2026, King County's FHA loan limits reflect the area's high housing costs while balancing program affordability goals.

2026 FHA Loan Limits for King County:

- Single-family home: $891,250

- Two-unit property: $1,140,800

- Three-unit property: $1,378,725

- Four-unit property: $1,713,375

These limits apply to the base loan amount before financing the upfront mortgage insurance premium. In Seattle's competitive real estate market, where median home prices frequently exceed these limits, buyers often face a choice between FHA financing for more affordable properties or alternative programs for higher-priced homes.

Properties in Everett (Snohomish County) fall under the same loan limits as King County for 2026, maintaining consistency across the broader Seattle metro area. This allows borrowers flexibility when searching in multiple jurisdictions.

When FHA Limits Become Restrictive

Tech professionals and higher-income buyers in Bellevue or Redmond might find FHA limits too restrictive for their target neighborhoods. In these situations, exploring conventional financing or specialized programs for high earners makes more sense. The historical context of 30-year fixed mortgage rates shows how different loan programs compete based on market conditions.

Specialized FHA Loan Programs

Beyond the standard FHA purchase loan, several specialized programs address specific borrower situations and property types. Understanding these options expands your financing toolkit.

FHA 203(k) Rehabilitation Loan: This program combines purchase financing and renovation costs into a single loan. Perfect for buyers interested in fixer-uppers in established Seattle neighborhoods, the 203(k) allows you to finance repairs that bring the property up to FHA standards or make desired improvements.

FHA Energy Efficient Mortgage: For buyers prioritizing sustainability and lower utility costs, this program finances energy-efficient upgrades. Given Seattle's focus on environmental stewardship, many borrowers in Lake Forest Park and Shoreline explore this option.

FHA Streamline Refinance: Current FHA borrowers can refinance with minimal documentation and no appraisal in many cases, making it easier to capture lower rates when market conditions shift. Learn more about refinancing strategies in Seattle through local refinance resources.

Common FHA Application Mistakes to Avoid

Even qualified borrowers sometimes encounter delays or denials due to preventable errors. Being aware of common pitfalls helps you navigate the application process smoothly.

Frequent mistakes include:

-

Making large deposits without documentation: Any deposit exceeding 1% of the purchase price requires a paper trail. Undocumented funds create underwriting delays.

-

Changing jobs during the process: Employment continuity matters. Switching careers or employers between application and closing can jeopardize approval.

-

Opening new credit accounts: New credit inquiries and accounts affect your DTI ratio and credit score. Avoid financing furniture or cars until after closing.

-

Misunderstanding gift fund requirements: Gift donors must provide a letter confirming funds are a gift, not a loan. Documentation requirements are specific and non-negotiable.

-

Skipping the pre-approval step: In competitive markets like Mill Creek and Lynnwood, sellers expect pre-approval letters with offers. Rate locks and purchase timelines depend on proper pre-approval.

Working with an experienced local lender helps you avoid these pitfalls and positions your application for success. The Wikipedia entry on FHA insured loans provides additional historical context about how the program evolved to include consumer protections.

Timeline Expectations for FHA Loan Processing

Understanding the typical FHA loan timeline helps you coordinate with sellers, manage expectations, and plan your move. While processing speed varies by lender, the general framework remains consistent.

Typical FHA loan timeline:

- Days 1-3: Application submission and initial review

- Days 4-7: Appraisal ordered and scheduled

- Days 8-14: Document collection and verification

- Days 15-21: Underwriting review and conditional approval

- Days 22-28: Condition clearance and final approval

- Days 29-35: Clear to close and closing preparation

- Day 36-45: Closing and funding

These timelines assume no complications and complete documentation. Seattle-area buyers often face tighter timelines due to market competitiveness. Sellers in Redmond or Kirkland might prefer 30-day closings, making lender efficiency crucial.

Some lenders can close FHA loans in as few as 21 days with complete documentation and cooperative appraisers. However, planning for 35-45 days provides buffer for normal processing variations.

Comparing FHA to Other Loan Programs

While FHA loans offer significant advantages, they're not always the optimal choice. Understanding how they compare to alternatives helps you select the right financing strategy.

| Feature | FHA Loan | Conventional Loan | VA Loan | USDA Loan |

|---|---|---|---|---|

| Minimum Down Payment | 3.5% | 3%-20% | 0% | 0% |

| Minimum Credit Score | 580 (500 with 10% down) | 620-680 | No official minimum | 640 |

| Mortgage Insurance | Required for life of loan (unless 10%+ down) | Required until 20% equity | None | Annual fee of 0.35% |

| Property Location | No restrictions | No restrictions | No restrictions | Rural areas only |

| Loan Limits | $891,250 (King County) | $766,550 (conforming) | Same as FHA | Varies by income |

For military veterans and active service members, VA loans typically offer better terms than FHA. For buyers in rural parts of Snohomish County, USDA loans might provide competitive zero-down options.

Tech professionals with substantial income and assets might benefit from conventional mortgage programs that eliminate mortgage insurance sooner and accommodate higher loan amounts without FHA restrictions.

FHA Requirements for Reserves and Assets

Beyond the down payment and closing costs, FHA guidelines don't mandate specific reserve requirements for single-family primary residences. However, individual lenders often impose reserve requirements based on loan amount, credit profile, or property type.

Typical reserve scenarios:

- Strong credit borrowers with stable employment: Often no reserves required

- Borderline DTI ratios or credit: 2-3 months of mortgage payments in reserves

- Multi-unit properties (2-4 units): 3-6 months of reserves for all units

- Investment properties: Not eligible for FHA (must be primary residence)

Reserves must be liquid and accessible, typically held in checking, savings, or money market accounts. Retirement accounts like 401(k)s can sometimes count as reserves, though lenders typically discount them by 30-40% to account for early withdrawal penalties and taxes.

For Seattle buyers stretching to afford homes in desirable neighborhoods, building adequate reserves demonstrates financial stability and strengthens your application even when not required.

Tax Benefits and Long-Term Considerations

FHA homeownership provides the same tax advantages as other mortgage types. Mortgage interest and property taxes remain deductible for those who itemize, though recent tax law changes increased the standard deduction, making itemization less common.

The permanent mortgage insurance premium on most FHA loans represents a significant long-term cost compared to conventional financing. Borrowers should evaluate refinancing to conventional loans once they build 20% equity, eliminating ongoing mortgage insurance.

For energy-conscious buyers in Seattle's environmentally focused market, exploring energy-efficient home upgrades can provide both tax benefits and utility savings that offset some FHA costs.

Next Steps in Your FHA Loan Journey

Understanding the fha requirements for home loan approval positions you for success, but knowledge alone doesn't close transactions. Taking concrete action moves you toward homeownership.

Immediate action steps:

- Check your credit reports for errors and address any issues

- Calculate your realistic debt-to-income ratio

- Start saving for down payment and closing costs

- Research FHA-approved condo projects if considering condos

- Connect with an experienced local mortgage broker

- Get pre-approved before house hunting

The competitive nature of Seattle real estate rewards prepared buyers who understand their financing before making offers. Sellers in desirable neighborhoods throughout Bellevue, Kirkland, and Redmond receive multiple offers, and financial readiness separates successful buyers from disappointed searchers.

Understanding FHA requirements gives you the foundation for confident homebuying decisions, but navigating Seattle's unique market dynamics requires local expertise and strategic guidance. Keith Akada at Mortgage Reel brings 25+ years of experience helping first-time buyers, tech professionals, and growing families throughout the Greater Seattle area secure the right financing for their situations. Whether you're exploring FHA options in Shoreline or comparing loan programs for a Redmond tech campus commute, connect with a trusted broker who combines transparent education with reliable execution in one of the nation's most competitive housing markets.