Breaking into Seattle's competitive housing market as a first-time buyer presents unique challenges in 2026, with median home prices hovering around $850,000 in many neighborhoods. However, first home buyer programs offer strategic pathways to homeownership that can reduce upfront costs, lower monthly payments, and make qualifying easier. These programs, offered through federal, state, and local channels, provide down payment assistance, reduced interest rates, and flexible qualification criteria designed specifically for buyers purchasing their first home. Understanding which programs you qualify for and how to layer multiple benefits can mean the difference between staying on the sidelines and securing the keys to your Seattle home.

Understanding First Home Buyer Programs in Washington State

Washington State operates several robust first home buyer programs through the Washington State Housing Finance Commission. These programs specifically target individuals who haven't owned a home in the past three years, though some exceptions apply for single parents and displaced homemakers.

The Home Advantage program stands as one of the most popular options, offering competitive interest rates and down payment assistance up to 5% of the loan amount. This assistance comes as a second mortgage with deferred payment, meaning you won't make monthly payments on it until you sell, refinance, or pay off your first mortgage.

Key State-Level Program Features

Washington's first home buyer programs include several distinct options tailored to different buyer profiles:

- Home Advantage: Down payment assistance up to 5% with competitive rates

- House Key: Targeted support for moderate-income buyers with income limits varying by county

- House Key Opportunity: Designed for buyers with disabilities or family members with disabilities

- Home Choice: Serves very low to moderate-income households with enhanced assistance

Income limits for these programs vary significantly by county and household size. In King County, where Seattle is located, a family of four in 2026 typically cannot exceed $138,000 in annual income for most programs, though limits adjust annually based on area median income.

The U.S. Department of Housing and Urban Development (HUD) publishes updated income limits each year that determine program eligibility across federal and state-sponsored initiatives.

Federal First Home Buyer Programs Available Nationwide

Beyond state offerings, several federal first home buyer programs provide accessible financing options regardless of your location. These programs often feature lower down payment requirements and more flexible qualification standards than conventional loans.

FHA Loans for First-Time Buyers

FHA loans remain the most widely used federal program, requiring just 3.5% down with credit scores as low as 580. In Seattle's high-cost market, FHA loan limits for 2026 reach $806,500 for single-family homes, making them viable for many neighborhoods in Shoreline, Lynnwood, and Lake Forest Park.

The primary trade-off involves mortgage insurance. FHA loans require both an upfront mortgage insurance premium (1.75% of the loan amount) and annual mortgage insurance that persists for the life of the loan if you put down less than 10%.

| Program Type | Minimum Down Payment | Credit Score Requirement | Mortgage Insurance |

|---|---|---|---|

| FHA | 3.5% | 580+ | Upfront + Annual (lifetime) |

| VA | 0% | No minimum | None |

| USDA | 0% | 640+ | Upfront + Annual |

| Conventional 97 | 3% | 620+ | PMI until 20% equity |

VA Loans for Military Service Members

Veterans, active-duty service members, and qualifying spouses access one of the most powerful first home buyer programs through VA loans. These loans require no down payment, no monthly mortgage insurance, and typically offer lower interest rates than conventional options.

In the Seattle metro area, home to Joint Base Lewis-McChord and a substantial veteran population, VA loans provide critical advantages in competitive situations. The VA funding fee (typically 2.3% for first-time users with zero down) can be financed into the loan amount, preserving cash for closing costs and reserves.

USDA Rural Development Loans

While Seattle proper doesn't qualify, portions of Mill Creek and areas north of Everett may be eligible for USDA Rural Development loans. These zero-down-payment loans serve moderate-income buyers in designated rural areas, though the definition of "rural" often surprises buyers.

USDA loans require annual mortgage insurance (0.35% of the loan balance) and have household income limits, but they offer some of the lowest overall costs for qualifying buyers. NerdWallet’s state-by-state guide provides additional details on geographic eligibility across Washington.

Local Down Payment Assistance Programs in Greater Seattle

King County and surrounding jurisdictions offer targeted first home buyer programs that complement state and federal options. These local programs often provide grants or forgivable loans specifically for down payment and closing costs.

King County Home Buyer Programs

The King County Housing Authority administers programs funded through local housing levies and federal HOME Investment Partnerships. These programs typically provide $10,000 to $50,000 in assistance, structured as either grants or deferred loans that don't require monthly payments.

Eligibility requires completing a HUD-approved homebuyer education course, meeting income limits (usually 80% of area median income or lower), and purchasing within specific price ranges. Priority often goes to essential workers, teachers, and public servants.

For Seattle professionals working at Amazon or Microsoft in Bellevue and Redmond, household income frequently exceeds these limits, making state programs like Home Advantage more accessible than county-level assistance.

City-Specific Initiatives

Seattle's Office of Housing periodically launches targeted assistance programs, though funding limitations mean these programs often operate on a first-come, first-served basis with waiting lists. Monitoring Seattle mortgage financing updates helps you catch application windows when they open.

Neighboring cities including Shoreline and Lynnwood sometimes offer their own initiatives, often funded through developer impact fees or state grants. These programs vary year to year based on available funding.

Conventional Loan Options for First-Time Buyers

Conventional loans, while not specifically designated as first home buyer programs, offer competitive options for buyers with strong credit and stable income. In 2026, several conventional programs cater specifically to first-time buyers with limited down payment funds.

HomeReady and Home Possible Programs

Fannie Mae's HomeReady and Freddie Mac's Home Possible programs allow 3% down payments for first-time buyers with incomes up to 100% of area median income. These programs offer:

- Lower mortgage insurance rates than standard conventional loans

- Flexibility to count non-borrower household income toward qualifying

- Reduced interest rates compared to FHA in many market conditions

- Ability to cancel mortgage insurance once you reach 20% equity

For a $700,000 home in Everett (requiring $21,000 down at 3%), the monthly mortgage insurance might run $300-400 monthly, compared to $450-550 with FHA financing. Over time, this difference compounds significantly.

Conforming Loan Limits and Jumbo Considerations

King County's conforming loan limit for 2026 stands at $806,500, meaning purchases above this threshold require jumbo financing. First home buyer programs through conventional channels typically max out at conforming limits, though some portfolio lenders offer low-down-payment jumbo options.

Jumbo home loan qualification becomes critical for Seattle buyers targeting neighborhoods where median prices exceed $850,000. These loans typically require larger down payments (10-20%) and higher credit scores (700+), though experienced mortgage brokers can sometimes structure transactions creatively to avoid jumbo territory.

Qualifying for First Home Buyer Programs in Competitive Markets

Meeting the basic eligibility criteria represents just the first step. Successfully using first home buyer programs in Seattle's competitive market requires strategic preparation across several dimensions.

Credit Score Optimization

Different programs impose varying credit requirements, but higher scores always improve your position:

- Review credit reports from all three bureaus 6-12 months before applying

- Dispute inaccuracies immediately through the bureau's online portal

- Pay down credit cards to below 30% utilization, ideally below 10%

- Avoid new credit applications in the 6 months before applying

- Maintain payment history with zero late payments for at least 12 months

Tech professionals in Seattle often carry excellent credit but may have limited credit history if they've primarily used debit cards or corporate cards. Establishing 2-3 revolving accounts at least 12 months before applying strengthens your file.

Income Documentation Standards

First home buyer programs require thorough income documentation, though standards vary by loan type. W-2 employees with stable pay history face the simplest process, typically providing:

- Two years of W-2 forms and tax returns

- Two most recent pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts

For Amazon, Microsoft, or Google employees with stock compensation, mortgage brokers must navigate complex guidelines around RSU vesting schedules, bonus history, and equity valuation. The Consumer Financial Protection Bureau offers resources on understanding different income types and documentation requirements.

Debt-to-Income Ratio Management

Most first home buyer programs cap debt-to-income ratios at 43-50%, though some allow higher ratios with compensating factors. Your DTI includes:

- Proposed mortgage payment (principal, interest, taxes, insurance, HOA)

- Car loans and leases

- Student loan payments (even if in deferment)

- Credit card minimum payments

- Personal loans and other installment debt

Paying off a $15,000 car loan before applying might increase your buying power by $80,000-100,000, making strategic debt paydown worthwhile for buyers near DTI limits.

Stacking Benefits: Combining Multiple Programs

One of the most powerful strategies involves layering first home buyer programs to minimize out-of-pocket costs and maximize purchasing power. Many programs can be combined, though understanding specific restrictions matters.

Allowable Program Combinations

You can typically combine:

- FHA loan + state down payment assistance: Use Home Advantage DPA with FHA financing for 3.5% down plus closing cost help

- VA loan + seller concessions: VA allows sellers to pay all buyer closing costs, requiring zero cash at closing

- Conventional 97 + HomeReady: Layer 3% down conventional with HomeReady income flexibility features

- State program + local assistance: Some county programs stack with Washington State Housing Finance Commission offerings

However, you cannot usually combine USDA with other down payment assistance, and VA has specific rules about seller concessions and lender credits.

Working with Experienced Mortgage Professionals

Navigating the intricacies of multiple first home buyer programs requires expertise in underwriting guidelines, program rules, and lender overlays. Not all lenders offer every program, and some impose additional restrictions beyond baseline requirements.

Working with mortgage brokers who maintain relationships with multiple lenders provides access to the full spectrum of options. Seattle mortgage brokers specializing in first-time buyers can often identify program combinations others miss.

Property Eligibility and Purchase Restrictions

First home buyer programs don't just impose borrower requirements. Properties must also meet specific standards regarding condition, price, and property type.

Property Type Restrictions

Most programs allow:

- Single-family detached homes

- Townhomes and row houses

- Condominiums (if the complex is approved)

- 2-4 unit properties (if you occupy one unit)

Manufactured homes, co-ops, and investment properties typically don't qualify. For condominiums, the complex must meet specific requirements around owner-occupancy ratios, HOA financial health, and insurance coverage.

Property Condition Standards

FHA loans require properties to meet minimum property standards addressing safety, security, and structural soundness. Homes needing significant repairs often don't qualify until repairs are completed, though FHA 203(k) renovation loans provide a workaround.

Conventional and state first home buyer programs typically require properties to be in livable condition but impose fewer specific requirements than FHA. Properties in Lake Forest Park or Shoreline with deferred maintenance might qualify conventionally but fail FHA standards.

Price Limits and Geographic Restrictions

State programs typically cap purchase prices at levels designed to target moderate-income housing stock. In King County for 2026, these limits often fall around $550,000-650,000, excluding many Seattle neighborhoods but covering substantial inventory in Everett, Lynnwood, and Mill Creek.

Federal programs use different approaches. FHA and conventional loans have no purchase price limits (only loan amount limits), while USDA restricts eligible properties to designated rural areas.

Required Education and Counseling

Nearly all first home buyer programs require completion of homebuyer education, though the format and specific requirements vary. These courses cover budgeting, mortgage basics, home maintenance, and avoiding foreclosure.

Course Options and Providers

Approved education comes from HUD-certified counseling agencies offering:

- In-person classes: 6-8 hour sessions, often on weekends

- Online courses: Self-paced programs taking 6-10 hours

- One-on-one counseling: Personalized sessions addressing your specific situation

Washington State programs require courses meeting specific standards, and many local down payment assistance programs mandate longer courses than federal minimums. Home ownership education resources help identify approved providers in the Seattle area.

Certificate Validity and Timing

Homebuyer education certificates typically remain valid for 2-3 years, though some programs accept older certificates. Completing education early in your homebuying journey allows you to apply for assistance programs immediately when you find the right property.

The certificate process takes 1-3 weeks from course completion to receiving the official document, so plan accordingly if you're actively making offers.

Common Mistakes to Avoid

Even qualified buyers make errors that derail first home buyer programs or cost thousands in unnecessary expenses. Understanding common pitfalls helps you navigate successfully.

Application Timing Errors

Applying for multiple credit cards, financing a car, or changing jobs during your home search can tank your approval. Lenders verify employment and pull credit again immediately before closing. A new $40,000 car loan discovered three days before your scheduled closing can cause denial.

Wait until after closing to make any financial changes. If job changes are unavoidable, discuss the situation with your lender immediately. Staying in the same field often poses no problem, but career changes or moves to commission-based income create complications.

Misunderstanding Program Requirements

First home buyer programs often have specific occupancy requirements, typically mandating you live in the home as your primary residence for at least one year. Violating this requirement can trigger full repayment of down payment assistance or even loan default.

State assistance programs frequently include recapture provisions if you sell within a certain timeframe (often 5-9 years). Understanding these provisions prevents surprises if your situation changes unexpectedly.

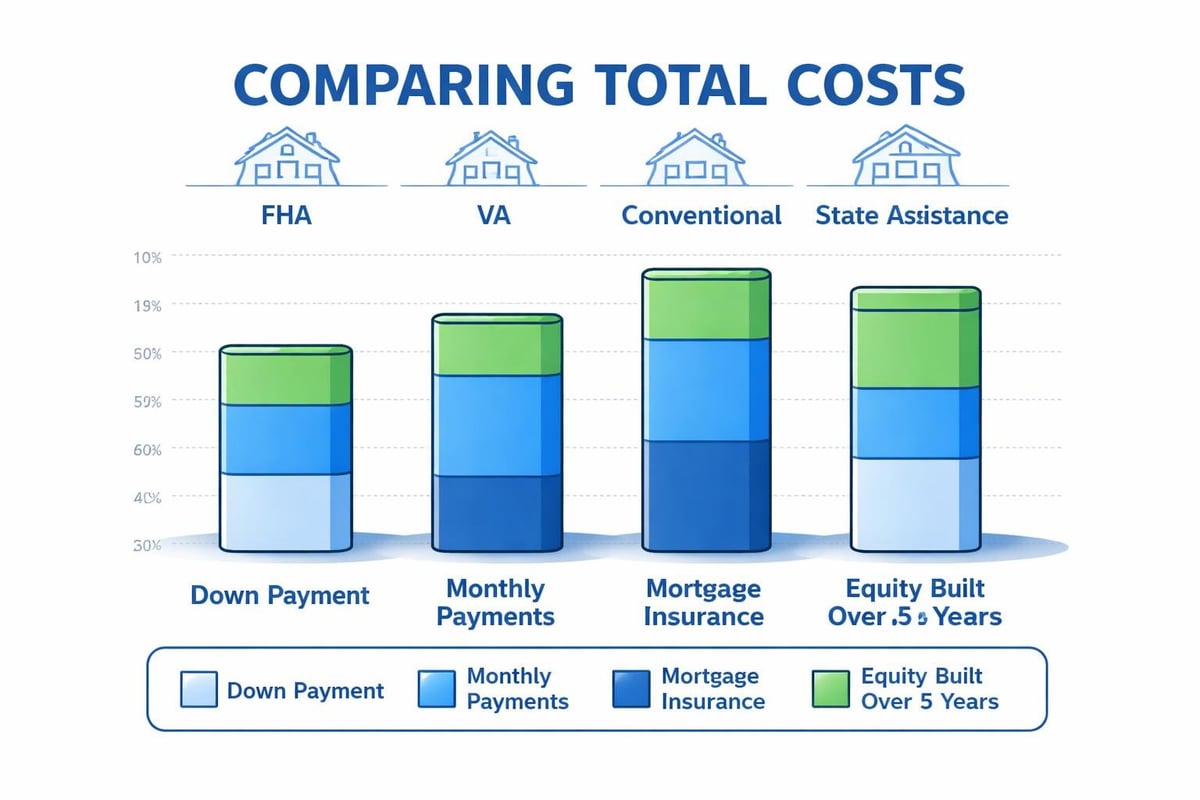

Overlooking Total Cost Analysis

The lowest interest rate doesn't always mean the lowest cost. FHA loans might offer slightly lower rates than conventional options, but lifetime mortgage insurance can cost tens of thousands more over 10-15 years. Bankrate’s first-time homebuyer guide includes calculators comparing total costs across loan types.

Similarly, down payment assistance structured as a second mortgage with 0% interest and no monthly payment seems free, but it must be repaid if you refinance. If rates drop two years after purchase, that "free" assistance prevents you from refinancing without paying back the full amount.

Tax Benefits and Long-Term Financial Planning

First home buyer programs provide immediate benefits through reduced down payments and assistance programs, but homeownership also creates ongoing tax advantages and wealth-building opportunities.

Mortgage Interest Deduction

You can deduct mortgage interest on loans up to $750,000 (the limit for mortgages originated after December 15, 2017). For Seattle homeowners with $700,000 mortgages at 6.5% interest, this deduction can reduce taxable income by approximately $45,000 in the first year.

However, with the standard deduction at $29,200 for married couples in 2026, you only benefit if total itemized deductions (mortgage interest, property taxes, charitable contributions) exceed this threshold. Many first-time buyers with smaller loans find the standard deduction more beneficial.

Property Tax Deduction Caps

State and local tax (SALT) deductions, including property taxes, cap at $10,000 annually for federal tax purposes. Seattle-area property taxes often exceed this limit alone, making the cap binding for most homeowners.

Long-Term Equity Building

Looking beyond immediate tax benefits, homeownership through first home buyer programs builds equity through two mechanisms: principal paydown and appreciation. In Seattle's historically appreciating market, homeowners who purchased in 2016 with first home buyer programs saw typical appreciation of 60-80% by 2026, building $250,000-400,000 in equity.

This equity provides financial flexibility for future moves, renovations, or refinancing opportunities when rates become favorable.

Current Market Conditions and Strategic Timing

Seattle's housing market in 2026 presents unique opportunities for first-time buyers using these programs. Understanding current conditions helps you time your purchase strategically.

Inventory Levels Across Greater Seattle

While Seattle proper maintains tight inventory with just 1.2 months of supply in many neighborhoods, Everett, Mill Creek, and portions of Lynnwood show 2.5-3.5 months of supply. This increased inventory gives buyers more negotiating power and time to conduct thorough due diligence.

Properties priced appropriately for first home buyer programs (under $650,000) still move quickly in desirable areas, but buyers aren't facing the 15-20 offer situations common in 2021-2022. Multiple offer scenarios still occur, but 3-5 offers is more typical than double digits.

Interest Rate Environment

Interest rates in early 2026 hover around 6.25-6.75% for well-qualified buyers using first home buyer programs. While higher than the 2020-2021 period, these rates remain historically moderate and shouldn't prevent qualified buyers from purchasing.

A common mistake involves waiting for rates to drop to some target level. If rates decrease 0.5%, prices typically rise 5-8% as buyer demand surges. The monthly payment might actually increase by waiting. USA.gov’s home buying resources include guidance on timing purchase decisions.

Seasonal Considerations

Spring and early summer (March-June) traditionally bring peak inventory as sellers list before the school year ends. However, this increased inventory comes with maximum competition from other buyers. Fall and winter months (October-February) feature less inventory but also fewer competing buyers and more motivated sellers.

For buyers using first home buyer programs with specific funding windows, timing your pre-approval and education completion to align with target purchase periods maximizes your chances of success.

Program-Specific Application Processes

Each category of first home buyer programs follows distinct application workflows, and understanding these processes prevents delays and ensures you meet all requirements.

State Program Application Steps

Washington State Housing Finance Commission programs require:

- Complete homebuyer education through an approved provider

- Find a participating lender (not all lenders offer these programs)

- Submit initial application with income and asset documentation

- Receive conditional approval with program reservation

- Find a property meeting program guidelines within the reservation period

- Complete full underwriting with the same documentation standards as conventional loans

The reservation period typically lasts 120 days, after which you must reapply if you haven't found a property. In competitive markets, getting pre-approved first with standard financing gives you flexibility to switch to state programs when you find the right property.

Federal Program Processing

FHA, VA, and USDA loans follow standard mortgage application processes with some program-specific additions:

- VA loans require a Certificate of Eligibility (COE) obtained through the VA's website or your lender

- USDA loans need property address verification of rural status early in the process

- FHA loans require the property appraisal to specifically address minimum property standards

Processing times vary by lender and market conditions, typically running 30-45 days from application to closing for straightforward transactions.

Local Assistance Program Coordination

County and city-level down payment assistance programs often require separate applications submitted to the housing authority or designated administrator. These applications typically need submission after you have a purchase agreement, with funding approval contingent on meeting all program requirements.

Coordinating timing between your mortgage approval, assistance program approval, and purchase contract contingency periods requires careful planning and proactive communication with all parties.

Financial Preparation Timeline

Successfully using first home buyer programs requires advance preparation across multiple areas. Most buyers need 6-12 months to optimize their financial profile and complete necessary steps.

12 Months Before Purchasing

Credit Building Phase

- Pull credit reports and address any errors

- Pay down credit cards to below 30% utilization

- Set up automatic payments to prevent late payments

- Avoid new credit applications or closing old accounts

Savings Acceleration

- Calculate down payment and closing cost targets based on price range

- Set up automatic transfers to dedicated homebuying savings account

- Research first home buyer programs to understand assistance options

- Create budget showing comfortable monthly payment range

6 Months Before Purchasing

Education and Pre-Qualification

- Complete homebuyer education course

- Gather financial documents (tax returns, pay stubs, bank statements)

- Get pre-qualified with 2-3 lenders to compare programs

- Review Seattle mortgage rates and lock timing strategies

Needs Assessment

- Define must-haves vs. nice-to-haves for your home

- Research target neighborhoods and price ranges

- Consider commute times and proximity to work

- Identify 3-5 neighborhoods meeting your criteria

3 Months Before Purchasing

Active Preparation

- Obtain formal pre-approval with specific loan program

- Research properties actively through Redfin, Zillow, and attending open houses

- Interview real estate agents specializing in buyer representation

- Apply for down payment assistance if using local programs

Document Organization

- Maintain clean bank accounts with clear sourcing of all deposits

- Avoid large cash deposits or unusual transactions

- Keep digital and physical copies of all financial documents

- Track employment history and prepare to explain any gaps

Active House Hunting Period

Once you begin making offers, responsiveness becomes critical. Lenders need 24-48 hours to update pre-approvals with specific property addresses, and delays can cost you the house in competitive situations.

Navigating first home buyer programs requires understanding program-specific requirements, strategic financial preparation, and expert guidance through complex qualification processes. Whether you're exploring FHA financing in Everett, VA benefits in Lynnwood, or state assistance programs throughout King County, the right combination of programs can make Seattle-area homeownership achievable. Keith Akada brings 25+ years of experience helping first-time buyers throughout Seattle, Bellevue, Redmond, and Kirkland maximize their purchasing power through strategic program selection and qualification. With 750+ five-star reviews and specialized expertise in qualifying complex income for tech professionals, Keith and the team at Mortgage Reel provide the education, transparency, and execution you need to confidently pursue your first home purchase.