Unlock the doors to your dream home in Seattle with confidence. Navigating the first time buyers loan process can be overwhelming, especially with fast-moving markets in Shoreline, Everett, and beyond.

This guide is your trusted roadmap for securing a first time buyers loan in 2026. You will discover clear steps to understand loan options, prepare your finances, and make smart choices in Seattle, Mill Creek, and Lynnwood. Ready for expert-backed guidance tailored to your goals? Your journey to homeownership starts here.

Understanding First-Time Buyers Loans in Seattle

Finding the right first time buyers loan in Seattle is essential for turning your dream of homeownership into reality. With a variety of options and local programs, understanding how these loans work and which ones fit your situation will help you buy with confidence, whether you are searching in Seattle, Shoreline, Lynnwood, or Everett.

What Qualifies as a First-Time Buyer Loan?

A first time buyers loan is a mortgage designed for individuals purchasing their first home or those who have not owned property in the past three years. In Seattle and surrounding areas, this definition applies to both true first-time buyers and repeat buyers who meet the three-year rule.

Eligibility typically includes:

- Not owning a primary residence in the last three years

- Meeting income and property requirements

- Using the home as your primary residence

Common misconceptions include thinking you must be a "never-ever" homeowner or that all first time buyers loan programs are only for low-income applicants. In King and Snohomish counties, some programs allow higher income limits due to the area's median prices.

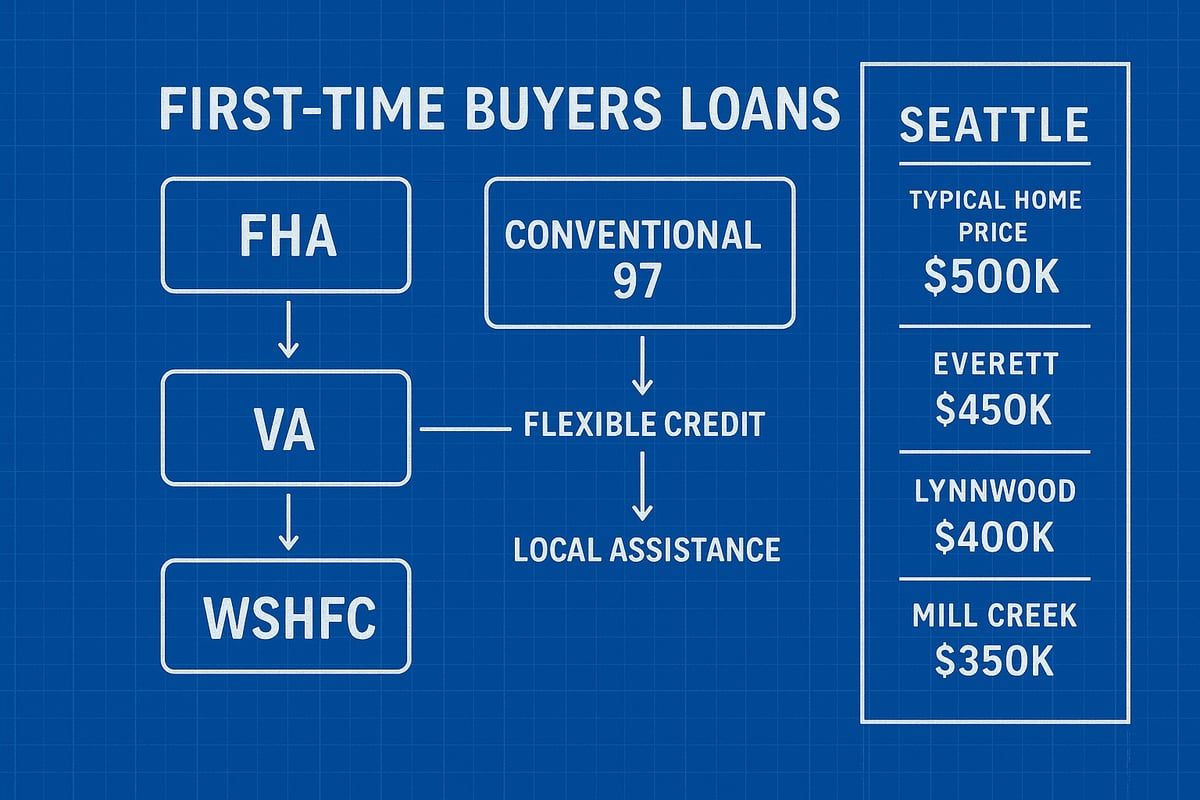

Local examples of first time buyers loan programs include FHA, Conventional 97, VA, and USDA loans. Each has distinct requirements, and some are tailored to the Seattle market or specific professions, such as veterans or public service workers.

Types of First-Time Buyer Loans Available

Seattle-area homebuyers have access to several first time buyers loan options. Here is a comparison of the most common programs:

| Loan Type | Down Payment | Credit Score | Special Features |

|---|---|---|---|

| FHA | 3.5% | 580+ | Flexible credit, higher DTI allowed |

| Conventional 97 | 3% | 620+ | Lower PMI with good credit |

| VA | 0% | Varies | For eligible veterans, no PMI |

| USDA | 0% | 640+ | Rural properties, income limits |

| WSHFC | Varies | 620+ | State programs, down payment help |

FHA loans are popular for first time buyers loan applicants due to their flexible credit standards and low down payment. Conventional 97 loans require only 3 percent down but expect higher credit. VA loans are outstanding for eligible veterans in Mill Creek and Everett, offering zero down and no mortgage insurance. USDA loans support buyers targeting rural areas north of Seattle.

Washington State Housing Finance Commission (WSHFC) programs provide additional support, including down payment assistance and educational resources. For a full overview of these options, visit First-time buyer home loans Washington to compare features and eligibility.

Local Market Considerations: Seattle and Surrounding Cities

The Seattle housing market is known for its competitive pace and high median prices. As of 2024, median home prices are approximately:

- Seattle: $850,000

- Everett: $620,000

- Lynnwood: $700,000

- Mill Creek: $740,000

Competition can influence your choice of first time buyers loan. FHA loans are sometimes less competitive in Seattle, where sellers may prefer Conventional offers. However, in Everett or Lynnwood, FHA and VA loans are commonly accepted, making them attractive for buyers with lower down payments.

Down payment assistance is available in both King and Snohomish counties, often helping buyers in Shoreline and Lake Forest Park bridge the affordability gap. For example, a Shoreline buyer might combine a Conventional 97 loan with city-specific down payment help to secure a home in a tight market.

In Seattle, the average loan amount closely tracks median prices, so understanding your local area's norms will help you select the right loan and set realistic expectations.

Pros and Cons of Each Loan Type

Each first time buyers loan program has unique benefits and trade-offs. Consider the following:

Down Payment:

- FHA: Low 3.5 percent, but upfront mortgage insurance

- Conventional 97: 3 percent, but stricter credit

- VA/USDA: Zero down, if eligible

Mortgage Insurance:

- FHA: Required for most, can be removed after refinancing

- Conventional: Private mortgage insurance (PMI) can be cancelled at 20 percent equity

- VA: No PMI, but funding fee applies

Credit Flexibility:

- FHA: Accepts lower scores, more forgiving on past credit issues

- Conventional: Rewards higher credit with better rates

- VA: Flexible, but must meet lender standards

Closing Costs and Assistance:

- All programs allow for some seller or state-paid assistance

- WSHFC and local grants can help bridge gaps

For example, an Everett buyer with a modest credit history might benefit from an FHA loan, while a Seattle buyer with strong credit could save on PMI with a Conventional 97. Always weigh the pros and cons with your lender to find the best fit for your personal situation.

Preparing Your Finances for a First-Time Buyers Loan

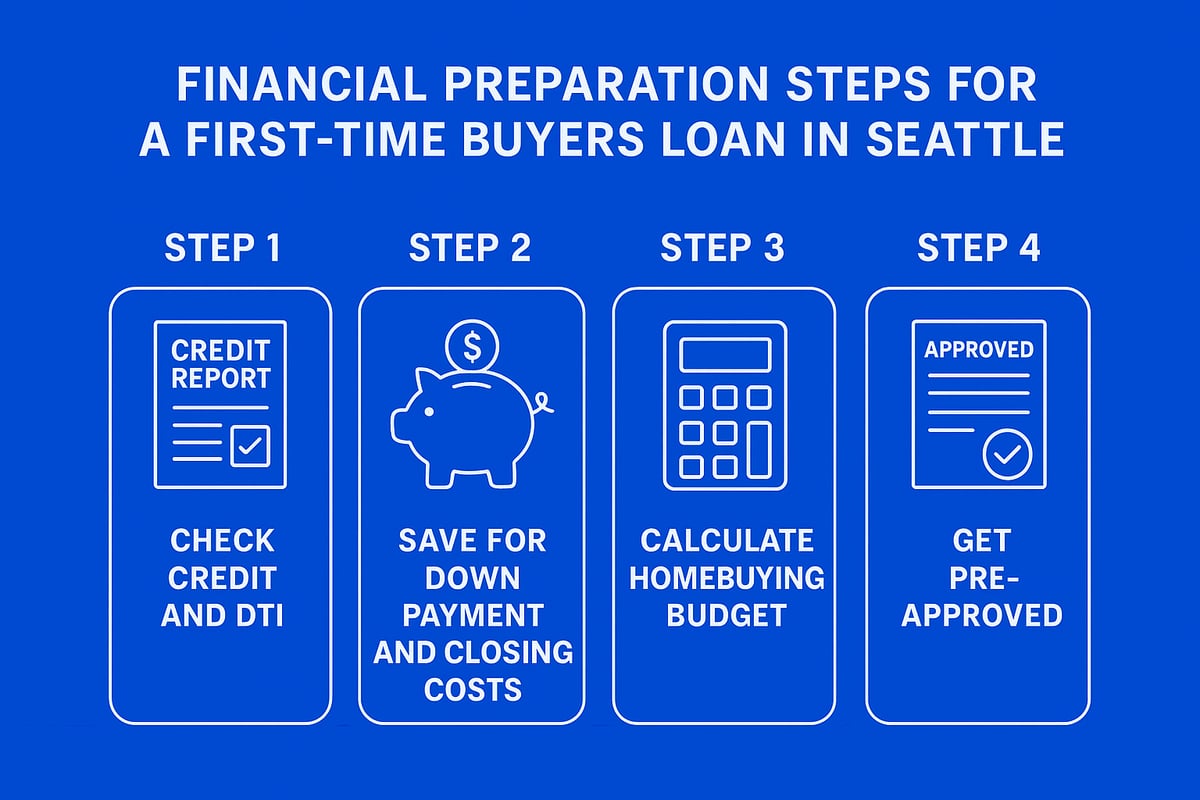

Preparing your finances is the foundation of a successful first time buyers loan journey in Seattle and the surrounding areas. By understanding your credit, planning for upfront costs, and setting a realistic budget, you can approach the homebuying process with greater confidence and clarity.

Assessing Your Credit and Financial Health

Your credit score is one of the most important factors when applying for a first time buyers loan. In Seattle, most lenders look for a minimum score of 580 for FHA loans, 620 for conventional, and 620 for VA loans. Start by checking your credit reports from all three bureaus and look for any errors that could impact your eligibility.

Improving your score before applying can save you thousands. Pay down revolving debt, avoid late payments, and do not open new accounts right before your application. Lenders will also calculate your debt-to-income (DTI) ratio, which measures your monthly debt payments against your gross income. For example, if your monthly debts (like student loans or car payments) total $2,000 and your gross income is $6,000, your DTI is 33%, which is within the preferred range for a first time buyers loan.

In the Seattle area, buyers with higher credit scores and lower DTI ratios have more loan options and better rates. Review your finances early and address any issues to maximize your approval chances.

Saving for Down Payment and Closing Costs

A key step in securing a first time buyers loan is saving enough for your down payment and closing costs. In Seattle, Lynnwood, and Mill Creek, down payments typically range from 3% to 5% of the purchase price. For a $700,000 home in Mill Creek, that means saving at least $21,000.

Closing costs usually add another 2% to 4% of the home price. In Seattle, these can range from $12,000 to $20,000 depending on the property and lender. Down payment assistance programs are available in King and Snohomish counties to help bridge the gap. Many buyers use gift funds from family, but be sure to document these according to lender guidelines.

To explore your options, consider reviewing down payment assistance programs that may be available for first time buyers loan applicants in Washington State. Planning your savings strategy early ensures you are ready to move quickly when the right home hits the market.

Calculating Your Homebuying Budget

Before you begin house hunting, it is crucial to know how much home you can afford with a first time buyers loan. Lenders determine your maximum loan amount based on your income, debts, and credit profile. Use online calculators tailored to Seattle and surrounding cities to estimate your monthly payment.

Remember to factor in property taxes, homeowners insurance, and possible HOA fees. For example, a $600,000 home in Everett with a 3% down payment could result in a monthly payment of approximately $3,400, including taxes and insurance. This breakdown helps you compare homes in Shoreline or Lake Forest Park so you can shop with confidence.

A clear budget gives you a strong foundation for negotiations and keeps your expectations realistic as you enter Seattle’s competitive market.

Getting Pre-Approved: Why It Matters

Securing a pre-approval is a vital step for anyone seeking a first time buyers loan in Seattle or nearby communities. Pre-qualification is an initial review, but pre-approval means a lender has verified your income, assets, and credit. You will need documents like pay stubs, W-2s, and bank statements.

In fast-moving markets like Seattle and Lynnwood, pre-approval letters show sellers you are a serious buyer and give you a distinct advantage. Your offer will stand out, especially when you are competing with multiple buyers in Mill Creek or Everett.

A strong pre-approval can make the difference between landing your dream home and missing out. Prepare your paperwork early and work with your lender to ensure everything is ready when you find the right property.

The Step-by-Step Loan Application Process

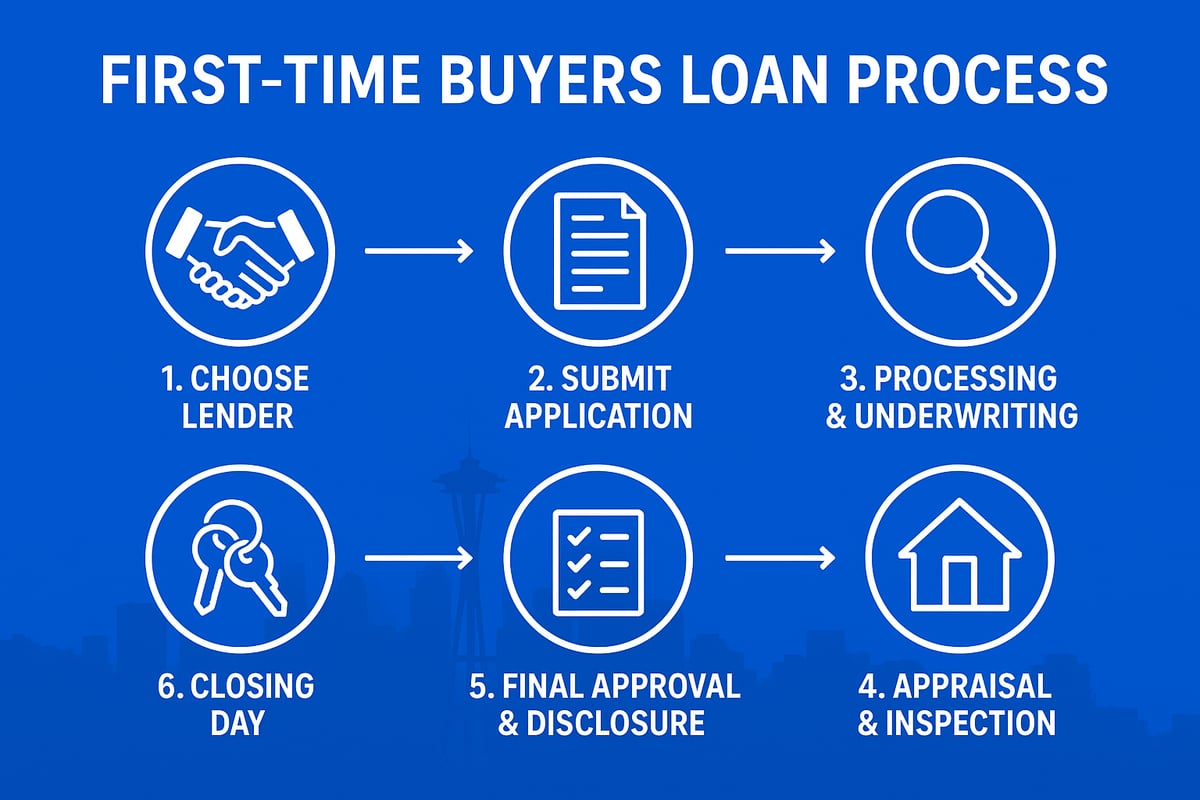

Navigating the first time buyers loan process in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett requires careful attention to every detail. Each step can influence your timeline and success, especially in a competitive market. Here’s how to move from pre-approval to holding the keys to your new home.

Step 1: Choose the Right Lender and Loan Officer

The first step to securing your first time buyers loan is selecting a lender with deep local knowledge. In Seattle and the Eastside, work with professionals who understand the nuances of King and Snohomish counties. Interview at least three lenders, asking about:

- Their experience with first time buyers loan programs

- Local approval rates and turnaround times

- Down payment assistance familiarity

For tailored advice specific to Seattle and surrounding cities, review these Seattle first-time buyer tips. Choosing the right partner sets the tone for your entire home buying journey.

Step 2: Submit Your Loan Application

After choosing a lender, your next move is to complete the first time buyers loan application. Decide whether you prefer an online or in-person experience. Both options require similar documentation:

- Recent pay stubs and W-2s

- Bank statements and asset verification

- Government-issued ID

Here’s a quick comparison:

| Application Method | Pros | Cons |

|---|---|---|

| Online | Fast, convenient | Less personal |

| In-person | Personalized help | Takes more time |

Expect your lender to outline the timeline, which usually ranges from a few days to a week for initial review.

Step 3: Loan Processing and Underwriting

Once your first time buyers loan application is submitted, the file moves to processing and underwriting. During this stage, your lender verifies:

- Credit score and credit history

- Income and employment stability

- Assets and reserves

Underwriters ensure your profile meets the loan program’s requirements and local standards. In Lynnwood and Everett, delays often occur if documentation is incomplete or if there are recent credit inquiries. Stay proactive and respond quickly to requests for additional information to keep your process on track.

Step 4: Home Appraisal and Inspection

The home appraisal is a critical part of the first time buyers loan process in Seattle and King County. Your lender orders an independent appraisal to confirm the home’s value matches the agreed purchase price. Typical appraisal fees in the area range from $600 to $900.

If the appraisal comes in low, your options may include renegotiating with the seller or increasing your down payment. Inspections are also essential, revealing any hidden issues. Use your inspection report to negotiate repairs or credits, especially in competitive markets like Lake Forest Park and Mill Creek.

Step 5: Final Loan Approval and Closing Disclosure

Receiving final approval on your first time buyers loan means you are “clear to close.” Your lender will provide a Closing Disclosure, outlining all loan terms, closing costs, and payment details. Review it thoroughly, comparing figures to your initial Loan Estimate.

Schedule a final walkthrough of the property before closing. Check that repairs are complete and the home’s condition matches your expectations. This last step ensures a smooth transition to ownership.

Step 6: Closing Day—What to Expect

On closing day, you’ll sign the final documents for your first time buyers loan, either at a local title company or attorney’s office. Bring a government-issued ID and be prepared for a wire transfer or certified check for your closing funds.

Common closing tasks include:

- Verifying your identity and loan details

- Reviewing the settlement statement

- Receiving and signing the deed

Once the transaction is recorded, you’ll receive the keys and officially own your new home in Seattle or the surrounding area. Congratulations on reaching this milestone.

Navigating Challenges and Common Mistakes for First-Time Buyers

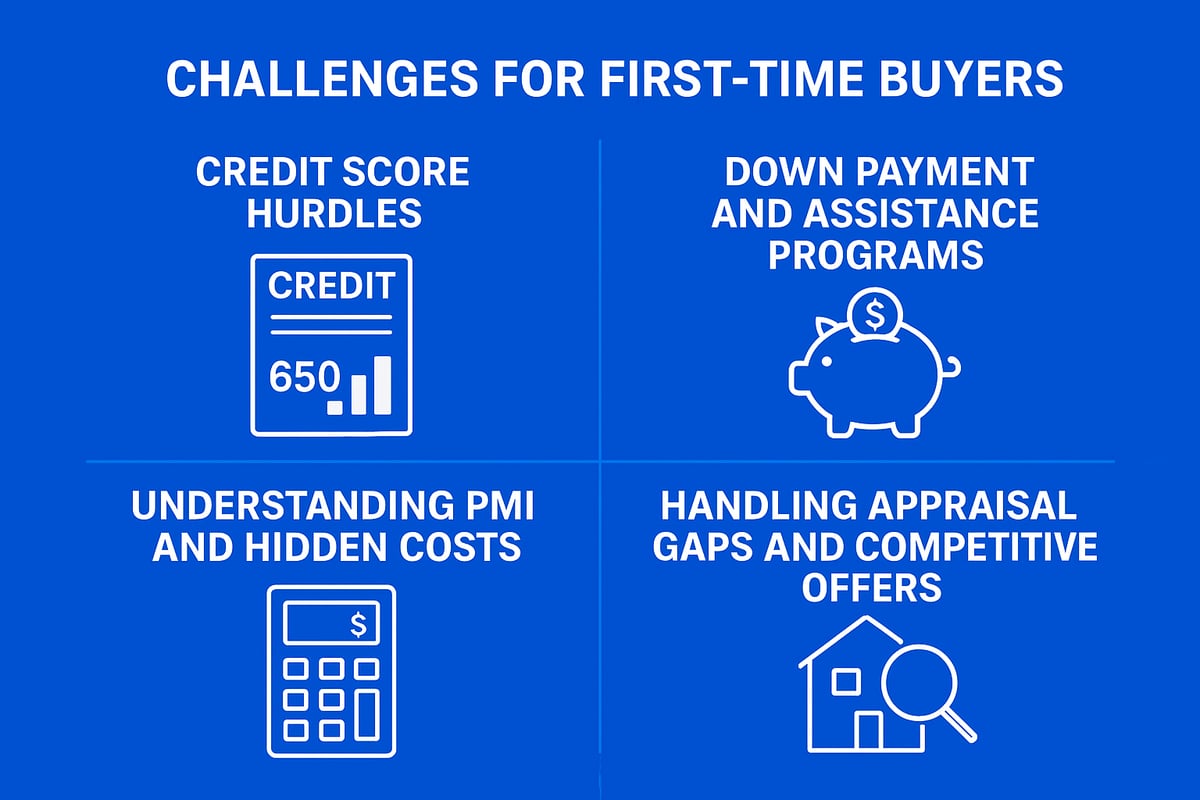

Buying your first home in Seattle, Everett, or Mill Creek is an exciting milestone, but the process can be filled with challenges. Many first time buyers loan applicants face hurdles with credit, down payments, or understanding hidden costs. By preparing for these common pitfalls, you can position yourself for success in competitive markets like Shoreline and Lynnwood.

Overcoming Low Credit or Limited Down Payment

One of the most common obstacles for first time buyers loan applicants in Seattle and Snohomish County is a low credit score or a limited down payment. FHA loans are specifically designed for buyers with credit scores as low as 580, and VA loans offer flexible credit requirements for eligible veterans. These options can be a lifeline in places like Lynnwood or Everett, where median home prices are rising.

If saving for a large down payment seems daunting, explore down payment assistance programs, such as those offered by the Seattle Office of Housing Down Payment Assistance. These programs can bridge the gap for buyers with modest savings, allowing you to qualify for a first time buyers loan sooner.

Before applying, review your credit report, pay down revolving debts, and avoid new credit inquiries. Even improving your score by a few points can make a difference for loan approval in Mill Creek or Lake Forest Park.

Avoiding Costly Mistakes During the Loan Process

Navigating the first time buyers loan process requires attention to detail, especially in fast-moving markets like Seattle and Shoreline. One major mistake is failing to compare loan offers. Rates, terms, and closing costs can vary by lender, so always request multiple quotes.

Another pitfall is making large purchases or opening new credit accounts before closing. This can change your debt-to-income ratio and put your loan at risk. For example, a buyer in Lake Forest Park avoided an $8,000 increase in closing costs by waiting to buy furniture until after closing.

Timing also matters. Failing to lock in your interest rate at the right time can cost you thousands, especially if rates rise before your closing date. Stay in close contact with your loan officer and ask questions throughout the process.

Understanding Private Mortgage Insurance (PMI) and Other Costs

Many first time buyers loan options in Seattle require mortgage insurance if your down payment is less than 20 percent. PMI protects the lender, not the borrower, and can add $150–$400 per month to your payment, depending on loan size and credit score.

You can remove PMI after building enough equity, usually once your loan-to-value ratio drops below 80 percent. Other costs to plan for include appraisals, homeowners insurance, escrow setup, and property taxes. In Everett and Mill Creek, closing costs typically range from 2 to 5 percent of the purchase price.

Here is a quick breakdown:

| Cost Type | Typical Range |

|---|---|

| PMI | $150–$400/month |

| Appraisal | $650–$900 |

| Homeowners Insurance | $800–$1,200/year |

| Escrow Fees | $1,000–$2,000+ |

Understanding these expenses up front helps you budget for your first time buyers loan and avoid surprises at closing.

Handling Appraisal Gaps and Competitive Offers

In Seattle and Shoreline, homes often receive multiple offers, which can drive sale prices above appraised values. If the appraisal comes in lower than your offer, you may face an appraisal gap. Options include renegotiating with the seller, increasing your down payment, or using escalation clauses.

Waiving contingencies can make your offer more attractive, but comes with risks. Always consult with your lender and real estate agent before removing protections, especially for your first time buyers loan. In Lynnwood, buyers sometimes use escalation clauses to outbid competitors, but careful planning is essential to avoid overextending your budget.

By understanding these challenges, you can prepare, adapt, and confidently move forward on your homebuying journey in any Seattle-area market.

Maximizing Your Success: Tips, Tools, and Local Resources

Starting your journey toward a first time buyers loan in Seattle requires the right tools and support. With the right strategies, you can navigate the local market in Seattle, Shoreline, Lynnwood, Mill Creek, and Everett with confidence. Let’s explore key resources and expert tips to help you succeed as a first-time homebuyer.

Leveraging Down Payment Assistance and Grants

For many buyers in Seattle and nearby cities, the biggest hurdle to a first time buyers loan is saving for the down payment. Fortunately, Washington offers robust support through programs like the Washington State Housing Finance Commission Homebuyer Programs, which provide down payment assistance, low-interest loans, and grants.

Eligibility is usually based on income, location, and whether you are a first-time buyer. Local programs often offer additional benefits for specific communities in Everett and Lynnwood. If you or a family member has a disability, the HomeChoice Down Payment Assistance Program can be a valuable resource, offering deferred second mortgages with favorable terms.

Typical assistance amounts range from a few thousand dollars to over $15,000, depending on the program and your eligibility. Make sure to review the application timeline early, as funds can be limited.

Building a Strong Homebuying Team

A successful first time buyers loan experience in Seattle starts with assembling the right team. Your lender, real estate agent, and sometimes a real estate attorney play vital roles throughout the process. Local expertise is especially important in fast-moving markets like Mill Creek and Lake Forest Park.

Here’s what your team should provide:

- Clear guidance on loan options and down payment assistance.

- Deep knowledge of Seattle, Shoreline, and surrounding areas.

- Strong negotiation skills to help you compete.

Keep communication open and ask questions often. The right team will ensure you stay informed and prepared at each step.

Using Technology and Online Tools

Technology streamlines the first time buyers loan process, especially in tech-forward areas like Seattle and Bellevue. Use mortgage calculators to estimate payments for homes in Everett or Lynnwood, and explore virtual tours to preview properties safely.

Key tools include:

- Online mortgage pre-approval applications.

- Secure document uploads and e-signature platforms.

- Local listing apps for real-time property updates.

These tools give you a competitive edge, helping you act quickly when the perfect home hits the market.

Staying Informed: Education and Support

Education is your best ally when applying for a first time buyers loan. Seattle and Everett offer free homebuyer classes and seminars, often in partnership with the Washington State Housing Finance Commission. These workshops cover budgeting, loan options, and the closing process.

Stay up to date by:

- Attending webinars and in-person classes.

- Reading trusted blogs and government guides.

- Listening to local podcasts for expert advice.

For example, many buyers in Lynnwood have shared how attending a WSHFC seminar helped them understand their options and feel more confident throughout the process.

Frequently Asked Questions for First-Time Buyers in Seattle

Buying your first home in Seattle or nearby cities like Everett, Shoreline, Lynnwood, and Mill Creek often comes with many questions. As a licensed mortgage broker, I help clients every day navigate the first time buyers loan process. Below, I answer the most common questions I receive from first-time buyers in our local market.

What credit score do I need for a first-time buyer loan?

Most first time buyers loan options in Seattle require a minimum credit score. For FHA loans, you can often qualify with a score as low as 580, though some lenders may accept slightly lower. Conventional loans typically need a 620 or higher. VA loans are flexible but usually prefer scores above 620.

Review your credit before applying and consider steps to improve your score. Learn more about requirements and tips at FHA home loan basics.

How much do I need for a down payment in Seattle?

Down payments for a first time buyers loan vary by program. FHA loans start at 3.5 percent, while Conventional 97 loans require 3 percent. VA and USDA loans may offer zero down for eligible buyers.

For a $700,000 home in Mill Creek or Seattle, this means $21,000 to $24,500, plus closing costs. Many buyers use down payment assistance, such as the Covenant Homeownership Program or Washington State Housing Finance Commission grants.

Can I buy a home with student loan debt?

Yes, it is possible to qualify for a first time buyers loan even with student loan debt. Lenders look at your overall debt-to-income (DTI) ratio. If your monthly debts, including student loans, are within an acceptable range, you can still be approved.

Local buyers in Everett and Lynnwood often succeed by consolidating debts or paying down balances before applying. Ask your lender how your specific loans affect your eligibility.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate of what you might afford based on self-reported information. Pre-approval is a formal process where a lender reviews your documents and credit, giving you a specific loan amount.

In Seattle’s competitive market, a pre-approval letter carries more weight with sellers. It shows you are a serious buyer and strengthens your offer in places like Shoreline and Lake Forest Park.

Are there special loan programs for tech professionals or veterans?

Yes, several first time buyers loan programs are tailored for local buyers. VA loans offer zero down and flexible guidelines for veterans. Tech professionals may qualify for competitive rates and closing cost help, especially through employer partnerships or local credit unions.

Always ask your lender about programs available in Seattle, Everett, and surrounding areas. Each buyer’s situation is unique, so personalized guidance is key.

Now that you have a clear understanding of your first time buyer options in Seattle and how to set yourself up for success in 2026, you might still have questions about your unique situation or want help tailoring a strategy that fits your goals. I’m here to support you every step of the way—from navigating loan programs and maximizing your buying power to making confident decisions in our competitive market. If you’re ready to take the next step, let’s connect and discuss your plans together. Let’s have a conversation