A lending officer serves as the critical bridge between homebuyers and their financing goals, guiding applicants through one of the most significant financial decisions they'll ever make. In competitive housing markets like Seattle, Bellevue, Redmond, and Kirkland, working with an experienced lending officer can mean the difference between securing your dream home or losing out to another buyer. These professionals evaluate financial profiles, recommend appropriate loan products, and shepherd applications from initial consultation through closing, all while ensuring compliance with strict regulatory requirements.

Understanding the Lending Officer Role

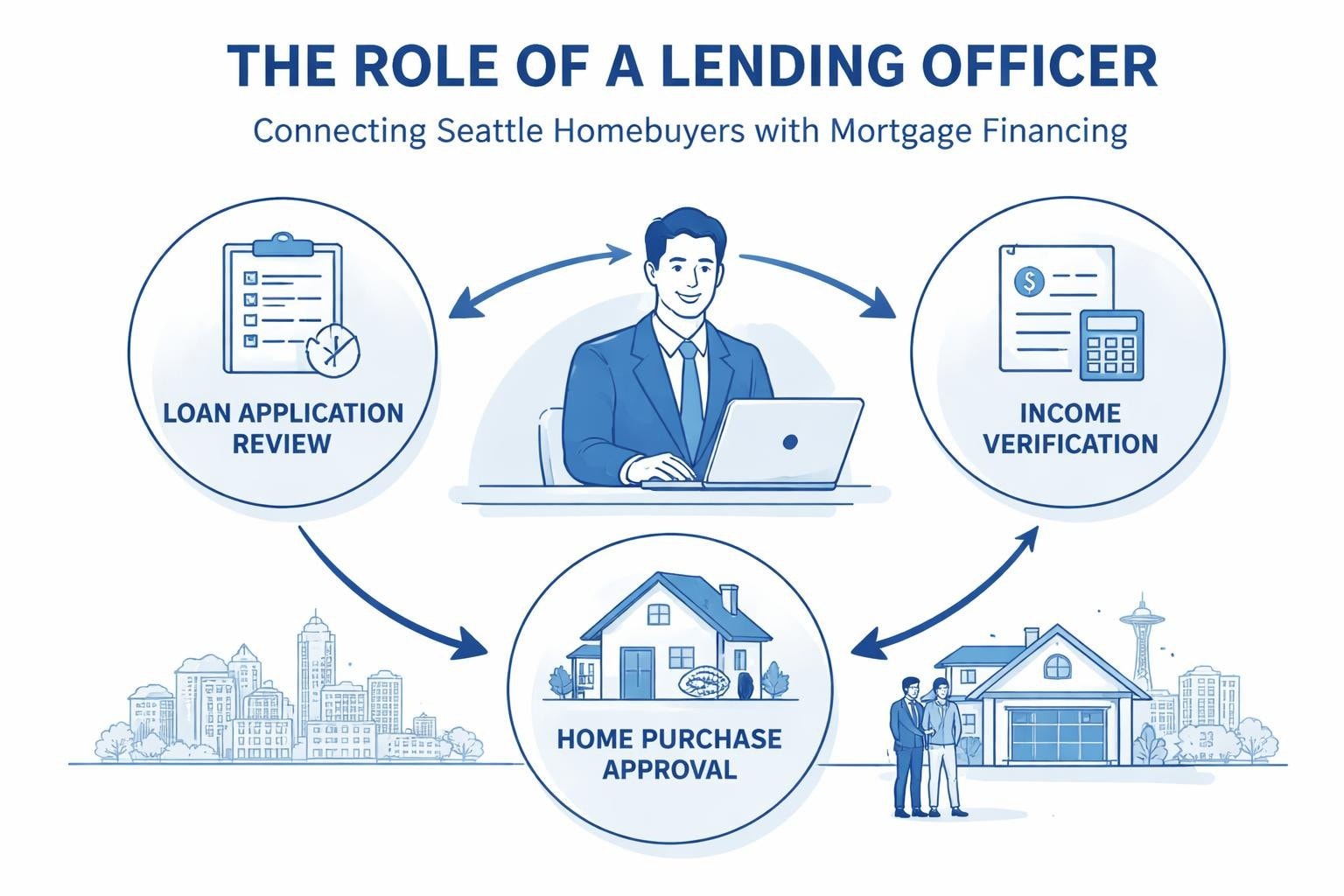

The position of a lending officer encompasses far more than simply processing paperwork. These professionals serve as financial advisors, problem-solvers, and strategic partners throughout the mortgage process.

Primary responsibilities include:

- Evaluating borrower creditworthiness and financial documentation

- Recommending appropriate loan products based on individual circumstances

- Pre-qualifying buyers to establish realistic budget parameters

- Coordinating with underwriters, processors, and closing teams

- Ensuring compliance with federal and state lending regulations

A lending officer must possess deep knowledge of various loan programs, from conventional mortgages to government-backed options like FHA, VA, and USDA loans. In the Seattle metro area, where tech professionals often have complex compensation structures including RSUs and stock options, a skilled lending officer understands how to properly qualify non-traditional income sources to maximize buying power.

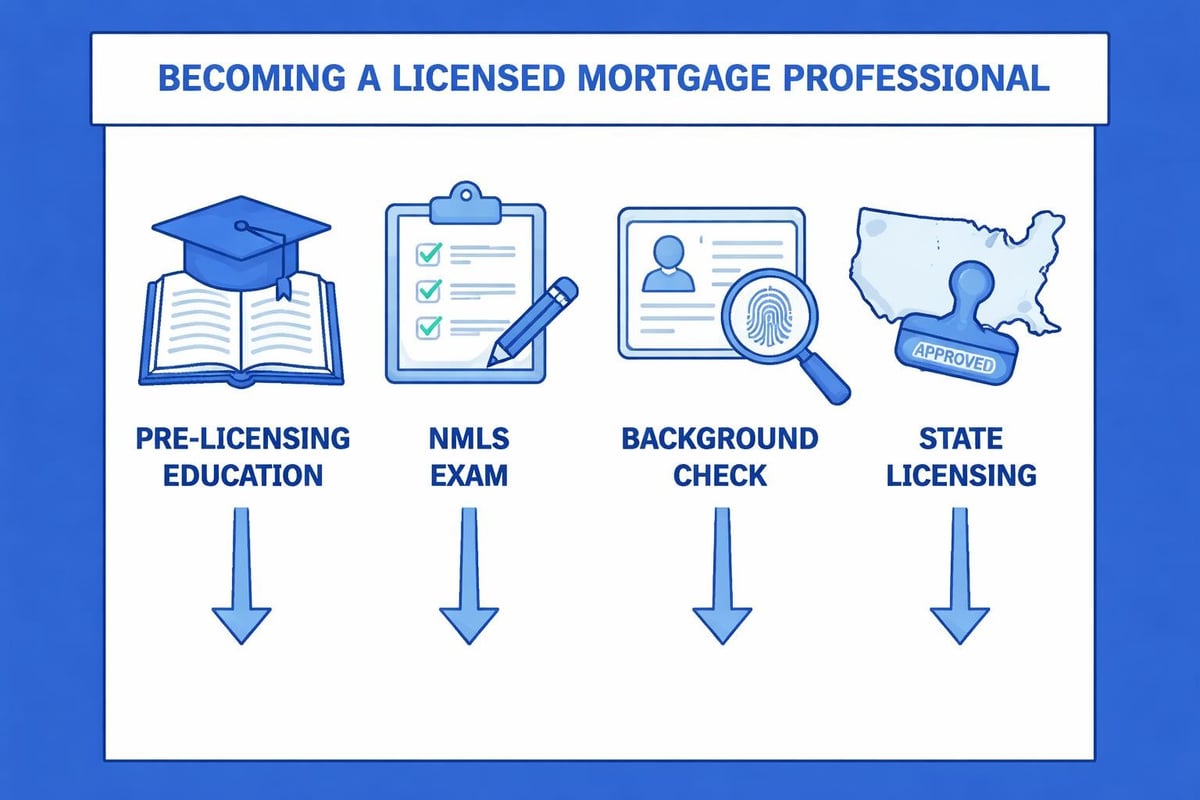

Educational Requirements and Licensing

According to detailed job descriptions from industry experts, becoming a lending officer requires specific educational credentials and licensing. Most positions require at minimum a bachelor's degree in finance, business administration, economics, or a related field. However, extensive industry experience can sometimes substitute for formal education.

The licensing process involves:

- Completing 20 hours of NMLS-approved pre-licensing education

- Passing the National SAFE MLO Test with a score of 75% or higher

- Submitting fingerprints for FBI background check

- Obtaining state-specific licensing through the NMLS

- Completing annual continuing education requirements

This regulatory framework ensures that every lending officer maintains current knowledge of lending laws, ethical standards, and industry best practices. For homebuyers in Shoreline or Lynnwood, this means working with professionals who meet rigorous qualification standards.

Compensation and Career Outlook

Understanding the financial aspects of the lending officer profession provides insight into industry dynamics and career stability. Salary data from Salary.com reveals that compensation structures vary significantly based on experience, geographic location, and employer.

| Experience Level | Base Salary Range | Commission Potential | Total Compensation |

|---|---|---|---|

| Entry-Level (0-2 years) | $40,000 – $55,000 | $10,000 – $25,000 | $50,000 – $80,000 |

| Mid-Career (3-7 years) | $55,000 – $75,000 | $25,000 – $60,000 | $80,000 – $135,000 |

| Senior (8+ years) | $70,000 – $95,000 | $50,000 – $150,000 | $120,000 – $245,000 |

Most lending officers earn compensation through a combination of base salary and performance-based commissions tied to loan volume and quality. This structure incentivizes professionals to provide excellent service while maintaining ethical lending practices.

Industry Trends and Job Market Dynamics

Recent analysis from HousingWire regarding loan officer mobility indicates that employment patterns shifted significantly in 2025, with professionals prioritizing stability over frequent job changes. This trend reflects broader market conditions where established lending officers with strong client relationships and proven track records command premium positions.

The Seattle mortgage market presents unique opportunities for lending officers who specialize in serving tech professionals. Understanding how to qualify employees from Amazon, Microsoft, Google, and other major employers requires expertise in evaluating:

- Restricted Stock Units (RSUs) and vesting schedules

- Annual bonus structures and consistency

- Stock option exercises and capital gains

- Relocation packages and signing bonuses

- Remote work arrangements affecting income verification

Essential Skills for Success

Technical knowledge forms only part of what makes an exceptional lending officer. The role demands a diverse skill set combining analytical abilities with interpersonal excellence.

Financial Analysis and Risk Assessment

A lending officer must quickly evaluate complex financial situations, identifying potential obstacles before they derail applications. This involves scrutinizing:

- Debt-to-income ratios and how various income sources affect qualification

- Credit report analysis, including dispute strategies for inaccuracies

- Asset verification and acceptable documentation requirements

- Employment stability indicators and income continuity

- Property appraisal reviews and value concerns

For buyers pursuing jumbo home loans in Seattle’s competitive market, lending officers must understand stricter qualification requirements and how to position applications for approval.

Communication and Client Education

Exceptional lending officers excel at translating complex mortgage concepts into understandable terms. They proactively communicate throughout the process, setting realistic expectations and preparing clients for each step. This educational approach proves particularly valuable for first-time homebuyers navigating unfamiliar territory.

The best professionals maintain consistent contact through:

- Regular status updates via phone, email, and text

- Clear explanations of required documentation and deadlines

- Honest assessments of challenges and potential solutions

- Market insights relevant to timing and strategy

- Post-closing follow-up and refinance monitoring

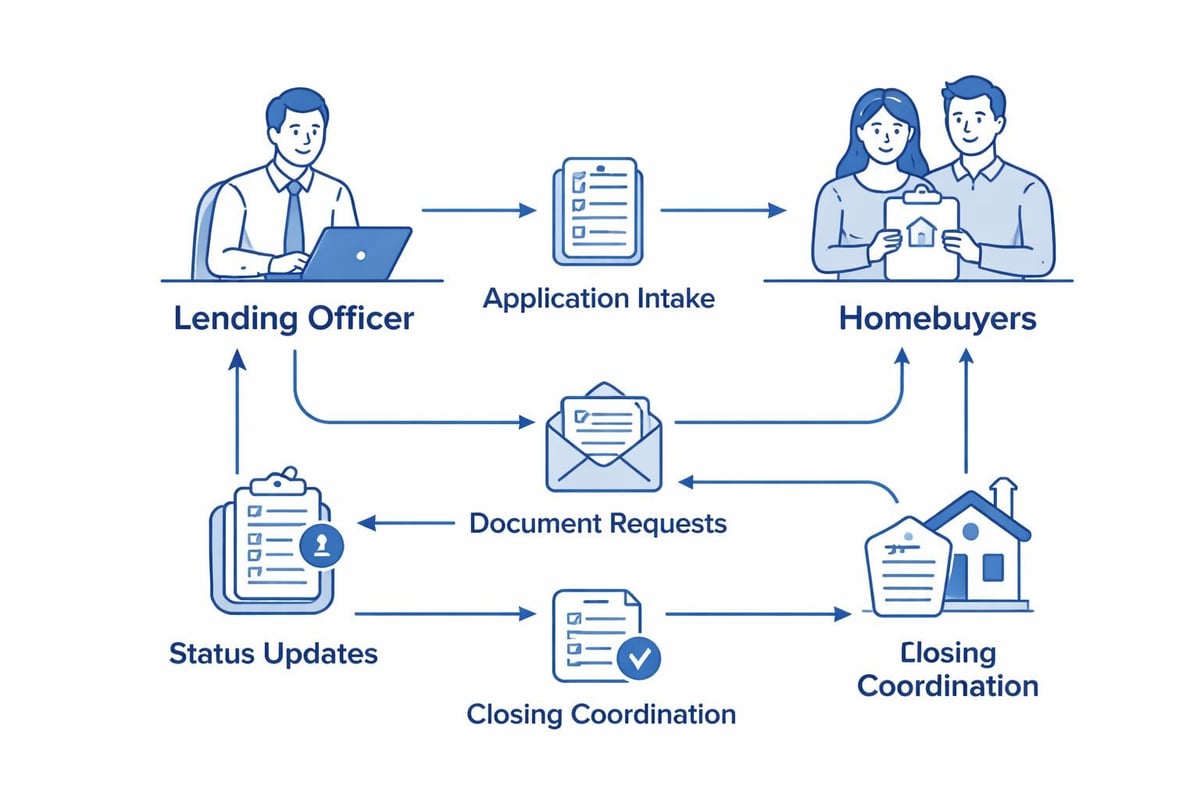

Daily Responsibilities and Workflow

Understanding the typical workday of a lending officer reveals the intensity and variety inherent in the profession. Mornings often begin reviewing new applications and prioritizing tasks based on closing timelines.

A lending officer's daily activities include:

- Conducting buyer consultations to understand financial goals and circumstances

- Reviewing credit reports and identifying improvement opportunities

- Calculating qualification amounts using various loan program guidelines

- Submitting loan applications to processing teams with complete documentation

- Responding to underwriter conditions with requested clarifications or documents

- Coordinating with real estate agents on transaction timelines and requirements

- Problem-solving obstacles that arise during underwriting or appraisal

- Attending closings to ensure smooth final execution

The role requires exceptional organizational skills and the ability to manage multiple transactions simultaneously. In fast-moving markets like Mill Creek and Lake Forest Park, lending officers often juggle 15-30 active files at various stages of completion.

Technology and Systems Proficiency

Modern lending officers leverage sophisticated technology platforms to streamline workflows and enhance client experience. Comprehensive job descriptions from Comeet emphasize the importance of technical proficiency in loan origination systems, CRM platforms, and digital document management.

| Technology Category | Common Platforms | Primary Function |

|---|---|---|

| Loan Origination System | Encompass, Calyx Point, Byte | Application processing and submission |

| Customer Relationship Management | Salesforce, Top of Mind, Surefire | Client communication and pipeline management |

| Document Management | Encompass, Docutech, Snapdocs | Secure file storage and e-signature |

| Pricing Engines | Optimal Blue, Mortech, LenderPrice | Rate quotes and product comparison |

Proficiency with these systems enables lending officers to provide rapid responses to client inquiries, generate accurate pre-approvals, and maintain compliance with documentation requirements.

Specialization Opportunities

As lending officers gain experience, many choose to specialize in specific market segments or loan types. This focused expertise allows professionals to differentiate themselves and better serve particular client demographics.

Serving Tech Professionals in Seattle

The concentration of major technology employers throughout Seattle, Bellevue, and Redmond creates demand for lending officers who understand stock-based compensation. These specialists know how underwriters evaluate RSU income, which documentation satisfies requirements, and how to structure applications for maximum approval odds.

Key considerations when working with tech employees include:

- Demonstrating two-year vesting history when possible

- Calculating average income using conservative methodologies

- Addressing volatility in stock valuations

- Timing applications around bonus payments and stock exercises

- Structuring down payments using various asset sources

When evaluating mortgage options for Seattle homebuyers, lending officers must consider how compensation structure affects both qualification and long-term affordability.

Investment Property Financing

Some lending officers specialize in serving real estate investors, requiring different analytical frameworks than owner-occupied financing. These professionals evaluate rental income potential, calculate cash flow projections, and structure portfolios across multiple properties.

Building a Successful Career Path

The trajectory from entry-level lending officer to senior professional or team leader follows predictable patterns, though individual timelines vary based on market conditions, work ethic, and skill development.

Career progression typically includes:

- Junior Loan Officer (Years 0-2): Learning systems, building initial client base, achieving first production milestones

- Loan Officer (Years 3-5): Establishing independent practice, developing referral partnerships, increasing transaction volume

- Senior Loan Officer (Years 6-10): Building team support, specializing in complex scenarios, mentoring newer professionals

- Branch Manager/Team Leader (Years 10+): Overseeing multiple loan officers, managing branch operations, strategic planning

According to HousingWire’s analysis of loan officer growth in 2025, the number of producing professionals has increased, reflecting improving market conditions and refinance opportunities. This growth creates both opportunity and competition, rewarding lending officers who differentiate through expertise and service quality.

Building Referral Partnerships

Sustainable success as a lending officer requires developing strong referral relationships with real estate agents, financial planners, attorneys, and past clients. Top mortgage brokers in Seattle understand that consistent communication and reliable execution build reputations that generate ongoing business.

Effective partnership strategies include:

- Providing educational resources agents can share with clients

- Offering rapid pre-approval turnaround to strengthen purchase offers

- Maintaining transparent communication throughout transactions

- Solving problems proactively rather than reactively

- Following up post-closing to ensure client satisfaction

Regulatory Compliance and Ethics

Operating as a lending officer demands unwavering commitment to regulatory compliance and ethical standards. The industry operates under intense oversight from multiple agencies including the Consumer Financial Protection Bureau, state banking departments, and the Federal Housing Finance Agency.

Critical compliance areas include:

- Truth in Lending Act (TILA) and RESPA disclosures

- Fair Housing Act anti-discrimination provisions

- Ability-to-Repay and Qualified Mortgage rules

- ECOA equal credit opportunity requirements

- State-specific licensing and advertising regulations

Violations of these regulations carry serious consequences including fines, license suspension, and potential criminal charges. Ethical lending officers prioritize borrower interests, recommend appropriate products rather than highest-commission options, and maintain transparency throughout the process.

Continuing Education Requirements

Maintaining an active lending officer license requires ongoing education. Most states mandate 8 hours of NMLS-approved continuing education annually, covering topics like federal regulations, ethics, and fair lending practices.

Beyond mandatory requirements, successful professionals pursue additional education in:

- Advanced underwriting guidelines and policy updates

- Specialized loan programs and niche products

- Technology platforms and efficiency tools

- Market analysis and economic trends

- Communication and negotiation skills

This commitment to continuous improvement distinguishes exceptional lending officers from mediocre performers, particularly when navigating complex scenarios involving Seattle refinance opportunities or challenging qualification situations.

Working with a Skilled Lending Officer

For homebuyers and homeowners in Everett, Shoreline, and throughout King County, selecting the right lending officer significantly impacts both immediate transaction success and long-term financial outcomes.

When evaluating potential lending officers, consider:

| Evaluation Factor | What to Look For | Why It Matters |

|---|---|---|

| Experience Level | Years in industry, transaction volume | Seasoned professionals navigate challenges effectively |

| Reviews and Testimonials | Consistent five-star ratings, detailed feedback | Past client satisfaction predicts future service |

| Communication Style | Responsiveness, clarity, proactive updates | Reduces stress and prevents surprises |

| Product Knowledge | Understanding of multiple loan programs | Ensures optimal product selection |

| Local Market Expertise | Knowledge of Seattle-area nuances | Better positioning in competitive situations |

The distinction between an average lending officer and an exceptional one often becomes apparent during challenging situations. When appraisals come in low, when underwriters request unusual documentation, or when timing gets compressed, experienced professionals find solutions while maintaining client confidence.

The Value of Experience and Reviews

In an industry where licensing establishes minimum competency, experience and reputation separate good lending officers from great ones. Detailed job requirements from Manatal outline baseline qualifications, but exceptional service comes from years of navigating real-world scenarios.

A lending officer with 25+ years of experience brings advantages including:

- Pattern recognition from thousands of previous transactions

- Established relationships with underwriters and processors

- Deep knowledge of guideline nuances and exceptions

- Proven problem-solving frameworks for common obstacles

- Perspective on market cycles and strategic timing

Client reviews provide invaluable insight into how lending officers actually perform under pressure. While one or two testimonials might reflect isolated experiences, hundreds of five-star reviews across multiple platforms demonstrate consistent excellence. These reviews often highlight specific strengths like clear communication, creative problem-solving, or exceptional responsiveness that matter most during stressful home purchases.

Choosing Between Banks, Brokers, and Direct Lenders

Understanding organizational structures helps borrowers identify which type of lending officer best fits their needs. Each model offers distinct advantages depending on individual circumstances.

Banks employ lending officers who originate loans funded directly by the institution. These professionals access only their employer's products and rates, which may limit options but can streamline processing.

Mortgage brokers work with multiple lenders, allowing their lending officers to shop rates and programs across various institutions. This model often provides more flexibility, particularly for complex scenarios or specialized loan types.

Direct lenders combine aspects of both models, employing lending officers who originate loans their company funds while maintaining control over underwriting and processing. Organizations like Mortgage Reel powered by Fairway offer this approach, combining personalized service with robust lending capacity.

The role of a lending officer extends far beyond transaction facilitation, encompassing financial advisory, strategic guidance, and committed advocacy throughout the mortgage process. For Seattle-area homebuyers and homeowners, partnering with an experienced professional who understands local market dynamics, complex compensation structures, and sophisticated loan products can transform the home financing experience. Keith Akada brings over 25 years of expertise and 750+ five-star reviews to every client relationship at Mortgage Reel, delivering the clarity, responsiveness, and strategic guidance that empowers confident decisions in competitive housing markets from first-time purchases to complex jumbo refinances.