Finding the right mortgage company can determine whether your home purchase or refinance becomes a smooth, confident transaction or a stressful, confusing experience. In competitive housing markets like Seattle, Bellevue, and surrounding communities, working with an experienced mortgage company that understands local market dynamics, borrower needs, and strategic financing options makes all the difference. This guide walks you through what a mortgage company does, how to evaluate your options, and what to look for when choosing a lending partner in the Greater Seattle area.

What a Mortgage Company Actually Does

A mortgage company originates, processes, and funds home loans for borrowers purchasing or refinancing residential properties. Unlike traditional banks that primarily use their own capital and hold loans in-house, many mortgage companies operate as intermediaries, connecting borrowers with various lending sources and selling loans on the secondary market.

Core services provided by a mortgage company include:

- Pre-approval and loan qualification based on income, assets, and credit

- Loan product selection and rate comparison

- Application processing and documentation review

- Underwriting coordination and approval management

- Closing preparation and funding execution

- Post-closing servicing or servicing transfer

The structure varies significantly across the industry. Some mortgage companies function as direct lenders with their own underwriting teams and capital sources. Others operate as broker networks, accessing wholesale pricing from multiple lenders. Understanding these distinctions helps borrowers identify which model best serves their specific situation.

Mortgage Companies vs. Banks vs. Brokers

The mortgage industry includes several player types, and knowing the differences clarifies what you should expect from each relationship.

| Type | Capital Source | Product Range | Speed | Personal Service |

|---|---|---|---|---|

| Traditional Bank | Own deposits | Limited to bank products | Moderate | Variable |

| Mortgage Company | Warehouse lines, investors | Wide variety | Fast to moderate | Often high |

| Mortgage Broker | Multiple wholesale lenders | Extensive | Fast | Typically personalized |

| Credit Union | Member deposits | Moderate selection | Slower | High for members |

Traditional banks like Chase or Wells Fargo use depositor funds and typically offer their proprietary loan products. A mortgage company often has more flexibility, accessing various investors and offering specialized programs. Mortgage brokers don't lend directly but connect borrowers with wholesale lenders, often securing better rates through volume relationships.

For Seattle-area tech professionals with complex compensation structures including RSUs, stock options, and variable bonuses, working with a mortgage company that specializes in qualifying non-traditional income often proves essential. Many traditional banks struggle to properly document and underwrite equity compensation, potentially limiting buying power for employees at Amazon, Microsoft, and Google.

Key Factors When Evaluating a Mortgage Company

Choosing a mortgage company requires assessing multiple dimensions beyond just advertised rates. The right partner combines competitive pricing with execution reliability, clear communication, and market expertise.

Interest Rates and Fees

Rate competitiveness matters, but context matters more. A mortgage company advertising the lowest rate may include buydown points, restrictive lock periods, or higher closing costs that offset the initial savings.

What to compare beyond the rate:

- Annual Percentage Rate (APR), which includes fees

- Origination charges and lender fees

- Third-party closing costs the company controls

- Rate lock terms and extension policies

- Discount point options and break-even analysis

In Seattle's market, where home prices frequently exceed conforming loan limits, understanding jumbo loan pricing becomes critical. Different mortgage companies have varying jumbo rate advantages based on their investor relationships.

Service Quality and Communication

The mortgage process involves coordination across multiple parties: realtors, title companies, appraisers, and underwriters. A responsive mortgage company keeps transactions moving through proactive communication and problem-solving.

Look for these service indicators:

- Response time: How quickly does the loan officer return calls and emails?

- Transparency: Do they explain requirements clearly and set realistic expectations?

- Accessibility: Can you reach your loan officer directly, or do calls route through a call center?

- Problem resolution: How do they handle obstacles like appraisal issues or documentation requests?

In competitive markets like Shoreline and Lynnwood, where multiple offers are common, speed and reliability become competitive advantages. Sellers and listing agents favor buyers working with mortgage companies known for closing on time without complications.

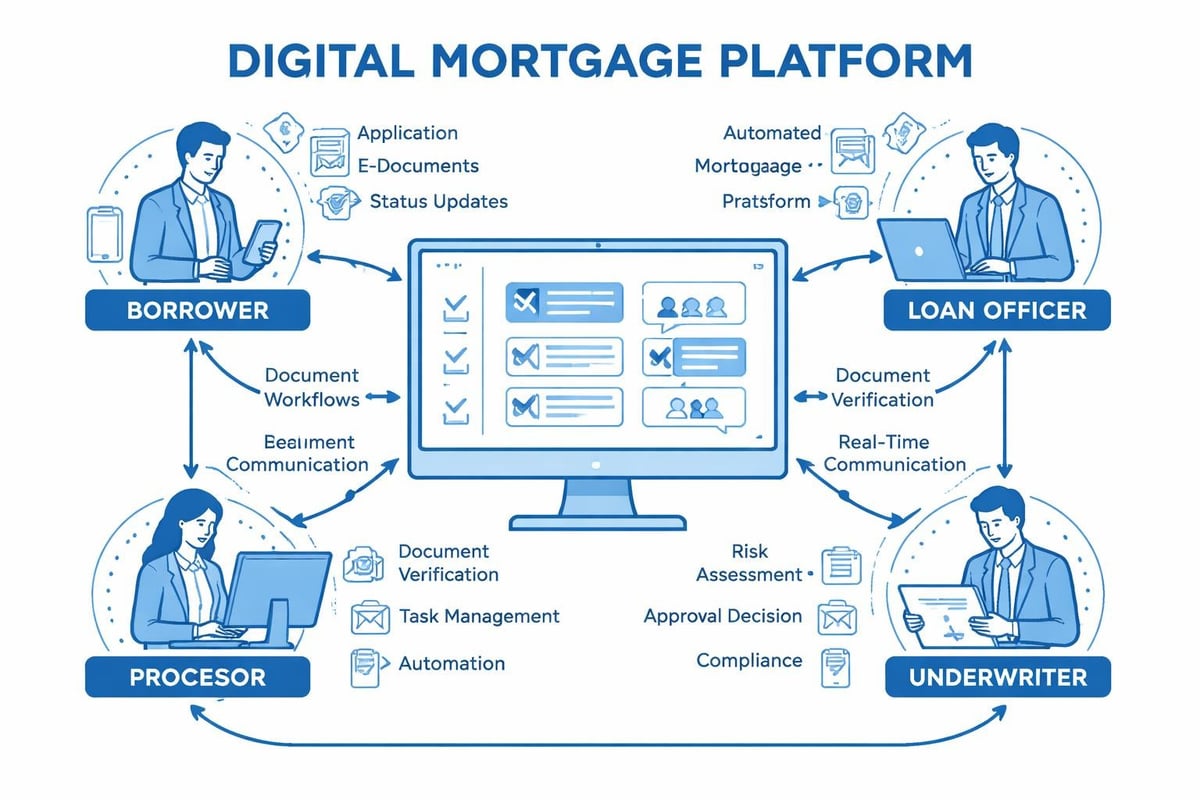

Technology and Process Efficiency

Modern mortgage companies leverage technology to streamline applications, document collection, and status updates. The best systems balance automation with human expertise, using digital tools to accelerate routine tasks while maintaining personal guidance for complex decisions.

Digital Application and Documentation

Expect a quality mortgage company to offer:

- Online application portals accessible 24/7

- Secure document upload systems

- Automated verification of income and assets when available

- Real-time status tracking and milestone updates

- E-signature capabilities for disclosures and documents

These tools matter particularly for busy professionals in Lake Forest Park or Mill Creek who need to manage the mortgage process around work schedules. The ability to upload pay stubs, review disclosures, and track progress digitally reduces friction and accelerates timelines.

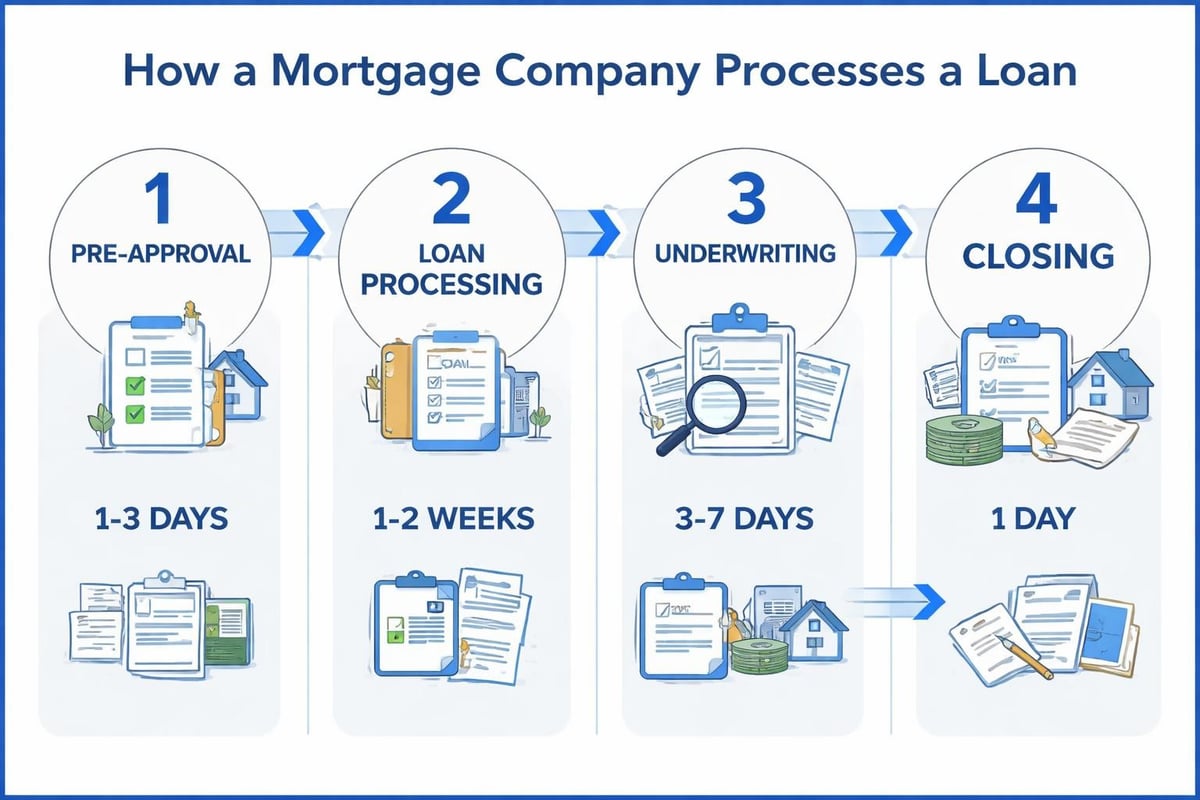

Underwriting Speed and Closing Timelines

Processing speed varies dramatically across mortgage companies based on their underwriting structure, technology systems, and workload management. Some companies maintain in-house underwriting teams with authority to make real-time decisions. Others outsource underwriting or operate with large queues that slow processing.

| Timeline Component | Efficient Company | Average Company | Slower Company |

|---|---|---|---|

| Pre-approval | Same day | 1-3 days | 3-5 days |

| Initial underwriting | 2-4 days | 5-7 days | 7-10 days |

| Conditional approval | 5-7 days | 10-14 days | 14-21 days |

| Clear to close | 9-12 days | 21-30 days | 30-45 days |

In Seattle's fast-moving market, the ability to close in 9-15 business days rather than 30-45 days creates meaningful advantages. Faster closings reduce the risk of rate changes during rate-lock periods, minimize time between contract and occupancy, and strengthen offers in competitive situations.

Regulatory Compliance and Financial Stability

The mortgage industry operates under extensive federal and state oversight designed to protect consumers and ensure responsible lending practices. Reputable mortgage companies maintain proper licensing, follow mortgage servicing regulations, and implement compliance systems.

Licensing and Regulatory Requirements

Every mortgage company must comply with state licensing requirements and federal regulations including:

- NMLS (Nationwide Multistate Licensing System) registration

- State-specific mortgage lender or broker licenses

- Individual loan officer licensing and continuing education

- Anti-money laundering programs as outlined by FinCEN requirements

- Fair lending and equal credit opportunity compliance

Before working with any mortgage company, verify their NMLS number and check for regulatory actions or complaints. The NMLS Consumer Access website provides free public records of licensing status and disciplinary history.

Financial Strength and Reputation

A mortgage company's financial stability affects its ability to honor rate locks, fund loans at closing, and provide consistent service during market volatility. While private companies don't publish financial statements, several indicators reveal financial health:

- Years in business and market presence

- Lending volume and market share data

- Warehouse lending relationships with major banks

- Investor and agency approvals (Fannie Mae, Freddie Mac, FHA, VA)

- Industry awards and third-party recognitions

Companies with established track records, diverse investor relationships, and strong operational infrastructure weather market cycles more reliably than newer or undercapitalized competitors.

Local Market Expertise in Greater Seattle

National mortgage companies may offer competitive rates, but local market knowledge creates tangible value in regional markets with unique characteristics. Seattle's housing market presents specific challenges including high prices, competitive bidding, and specialized property types.

Understanding Seattle-Area Property Types

Experienced local mortgage companies navigate Seattle's diverse housing stock, from Capitol Hill condos to Everett single-family homes to Lake Forest Park waterfront properties. Different property types carry different lending considerations:

Condos and townhomes: Require project approval, HOA financial review, and occupancy ratio verification. Some mortgage companies maintain pre-approved condo project lists that accelerate underwriting.

Multi-family properties: Two-to-four unit properties qualify for residential financing but require additional income documentation and reserve requirements that vary by mortgage company policy.

New construction: Requires construction-to-permanent financing or coordination between builders and lenders. Companies with builder relationships often streamline this process.

A Seattle mortgage broker familiar with these property types anticipates issues and structures loans appropriately from the start, avoiding delays and surprises during underwriting.

Income Documentation for Tech Professionals

Seattle's concentration of technology employers creates unique mortgage scenarios. Compensation packages including RSUs, stock options, restricted stock, and bonus structures require specialized documentation and underwriting knowledge.

Common equity compensation challenges:

- Determining which RSU income is stable enough to qualify

- Calculating two-year average for variable stock grants

- Projecting future vesting schedules for income qualification

- Documenting option exercises and tax implications

- Handling one-time bonuses vs. recurring incentive compensation

A mortgage company experienced with Seattle tech employment understands these nuances and knows how to maximize qualifying income while meeting investor guidelines. This expertise directly impacts buying power, sometimes adding hundreds of thousands of dollars to maximum loan amounts.

Specialized Loan Programs and Products

Mortgage companies vary significantly in their product offerings. Some focus exclusively on conventional conforming loans, while others maintain approvals for specialized programs that expand borrower options.

Government-Backed Loan Programs

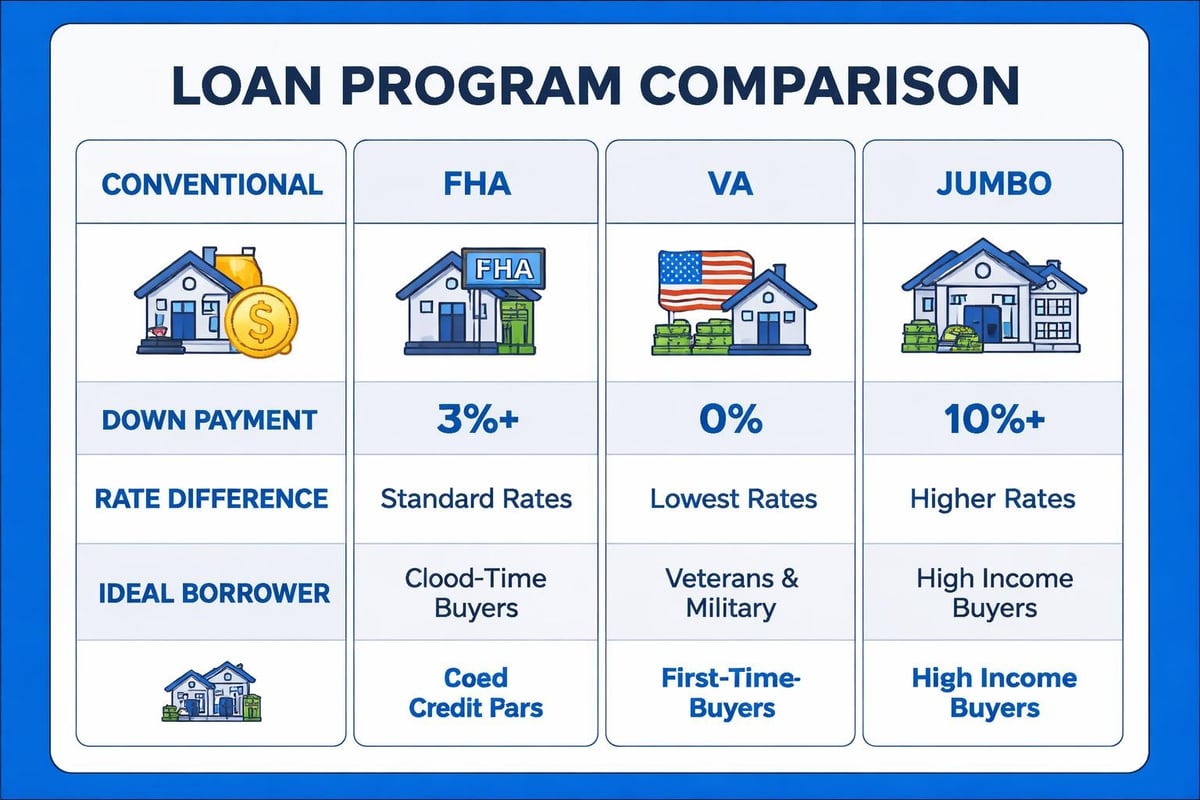

FHA, VA, and USDA loans each serve specific borrower segments with advantages like lower down payments, flexible credit requirements, or zero down payment options. Not all mortgage companies originate all government programs equally well.

- FHA loans: Ideal for first-time buyers in Shoreline or Lynnwood with limited down payment savings

- VA loans: Available to eligible veterans and service members purchasing in any Seattle-area city

- USDA loans: Applicable in eligible rural areas, though limited within central Seattle metro

- Jumbo loans: Essential for Seattle-area purchases exceeding $806,500 conforming limits in 2026

Mortgage companies maintaining strong government lending divisions typically offer better pricing, faster processing, and more expertise with these specialized products.

Down Payment Assistance and First-Time Buyer Programs

Washington State and local municipalities offer down payment assistance programs that reduce the cash required to purchase. These programs include income limits, home price caps, and specific property location requirements.

A knowledgeable mortgage company identifies which programs borrowers qualify for and layers assistance with primary financing. This requires understanding program-specific requirements and coordinating multiple funding sources at closing.

Questions to Ask Before Choosing a Mortgage Company

Smart borrowers interview potential mortgage companies just as they would any major service provider. The following questions reveal capabilities, processes, and cultural fit.

Rate and cost transparency:

- What rate can you offer today, and what assumptions does it include?

- How do your fees compare to competitor averages?

- When do you lock rates, and what happens if closing delays?

Process and communication:

- What's your typical timeline from application to closing?

- How will we communicate, and how quickly do you respond?

- Who handles my file if you're unavailable?

Experience and specialization:

- How many loans do you close monthly in Seattle?

- What experience do you have with my property type or income situation?

- Can you provide references from recent clients?

Problem-solving capability:

- What happens if the appraisal comes in low?

- How do you handle changing financial circumstances during processing?

- What's your backup plan if underwriting conditions become challenging?

The quality and confidence of responses reveal both competence and compatibility. A mortgage company that answers directly, provides specific examples, and demonstrates Seattle market knowledge earns greater trust than one offering vague assurances or avoiding difficult questions.

The Role of Reviews and Reputation

Online reviews provide valuable insight into mortgage company performance, though evaluation requires discernment. A company with 750+ five-star reviews across multiple platforms demonstrates consistent service quality more convincingly than one with 20 reviews on a single site.

Where to Find Credible Reviews

Check multiple review sources to develop a comprehensive picture:

- Google Reviews: Largest volume, most public visibility

- Zillow Lender Directory: Real estate-specific context

- Redfin Partner Network: Verified transaction reviews

- Yelp: Detailed narrative feedback

- Better Business Bureau: Complaint resolution history

Look for patterns across reviews rather than individual outlier comments. Consistent praise for communication, closing speed, or problem-solving reveals strengths. Repeated complaints about responsiveness, unexpected fees, or missed deadlines signal concerning weaknesses.

Understanding Industry Benchmarks

The mortgage lending industry operates with measurable performance standards. While individual borrower circumstances vary, certain benchmarks indicate above-average versus below-average performance.

Competitive mortgage companies in 2026 typically achieve:

- Pre-approval turnaround under 24 hours

- Initial disclosures within three business days

- Conditional approval within 7-10 days of complete application

- Clear-to-close status 5-7 days before closing date

- Closing timeline of 15-21 days for purchase transactions

Companies consistently exceeding these timelines without clear justification may lack the systems, staffing, or processes necessary for efficient execution.

Mortgage Company Support Throughout the Loan Lifecycle

The relationship with a mortgage company doesn't end at closing. Quality companies provide ongoing support for questions about payments, escrow accounts, refinancing opportunities, and future financing needs.

Servicing Transitions and Long-Term Support

Many mortgage companies sell loans to servicers shortly after closing. This common practice shouldn't concern borrowers, as mortgage servicing rules protect consumers during transfers.

What matters more is whether your original loan officer remains accessible for future questions, refinance consultations, and strategy discussions. The best mortgage companies build long-term relationships, staying in touch through market updates, rate change alerts, and periodic check-ins.

For homeowners in Mill Creek or Everett planning to refinance, move up, or purchase investment properties, maintaining a relationship with a trusted mortgage company streamlines future transactions. Pre-existing knowledge of your financial profile, employment history, and homeownership goals accelerates subsequent applications.

Refinance and Equity Access Options

Homeowners work with mortgage companies not just for purchase financing but also for refinancing opportunities including:

- Rate-and-term refinancing: Lowering interest rates or adjusting loan terms

- Cash-out refinancing: Accessing equity for renovations, debt consolidation, or investments

- Streamline refinancing: FHA and VA programs with reduced documentation

- Mortgage recasting: Reducing payments without full refinancing

A relationship-focused mortgage company monitors your loan performance and market conditions, proactively identifying refinance opportunities when rate drops or equity increases justify the cost and effort.

Making Your Final Decision

Selecting a mortgage company requires balancing multiple factors: rates, service quality, technology, local expertise, and cultural fit. The lowest rate from an unresponsive company with poor reviews rarely produces the best outcome. Conversely, paying slightly higher fees for superior service, faster closing, and strategic guidance often proves worthwhile.

Create a decision framework:

- Qualify candidates: Verify licensing, check reviews, confirm product availability

- Compare costs: Request loan estimates with identical scenarios

- Assess responsiveness: Evaluate communication speed and quality during initial interactions

- Test expertise: Discuss your specific situation and gauge knowledge depth

- Check references: Contact recent clients with similar transactions

The right mortgage company combines competitive pricing with reliable execution and personalized service. For Seattle-area borrowers navigating complex compensation, competitive markets, or specialized property types, local expertise and proven track records matter as much as rate sheets.

Trust your instincts during the selection process. If a mortgage company makes unrealistic promises, avoids direct answers, or creates pressure to commit quickly, those red flags deserve attention. Professional mortgage companies earn business through demonstrated competence, transparency, and results, not sales tactics.

Choosing the right mortgage company impacts both your immediate transaction success and your long-term financial strategy. Whether you're purchasing your first home in Shoreline, upgrading to a larger property in Everett, or refinancing in Lake Forest Park, working with an experienced, responsive, and knowledgeable mortgage company makes the process smoother and the outcome more favorable. Keith Akada at Mortgage Reel brings over 25 years of Seattle-area mortgage expertise, specializing in helping tech professionals maximize buying power through strategic qualification of stock compensation and bonus income. With 750+ five-star reviews and the ability to close loans in as few as 9 business days, Mortgage Reel delivers the combination of expertise, speed, and personalized service that makes a meaningful difference in competitive markets.