Finding the right mortgage lender VA specialists can make all the difference when purchasing a home in the Greater Seattle area. Veterans, active-duty service members, and eligible surviving spouses have access to one of the most powerful home financing tools available through the Department of Veterans Affairs. However, not all mortgage lenders offer VA loans, and among those that do, experience and expertise vary significantly. Understanding how to select a qualified mortgage lender VA partner in Seattle, Bellevue, Redmond, or surrounding communities ensures you maximize the benefits of your service while navigating one of the nation's most competitive housing markets with confidence.

Understanding VA Loans and Mortgage Lender VA Requirements

VA loans represent a unique benefit earned through military service, offering several advantages over conventional financing. These government-backed mortgages eliminate the need for private mortgage insurance (PMI), often require no down payment, and typically feature more flexible credit and income requirements compared to traditional loan programs.

Key VA Loan Benefits in 2026

The VA home loan program continues to evolve, offering Seattle-area veterans exceptional opportunities despite rising home prices. When working with a knowledgeable mortgage lender VA specialist, borrowers gain access to:

- Zero down payment options on purchase prices up to the county conforming loan limit

- No private mortgage insurance requirement regardless of down payment amount

- Competitive interest rates typically lower than conventional mortgages

- Flexible credit standards that consider compensating factors beyond credit scores

- Limited closing costs with specific restrictions on what veterans can be charged

- Assumption capabilities allowing qualified buyers to take over your loan terms

For homes in Seattle, where median prices exceeded $825,000 in early 2026, these benefits translate into substantial savings. A veteran purchasing a $750,000 home in Shoreline with zero down payment would save approximately $150-225 per month by avoiding PMI compared to a conventional loan with less than 20% down.

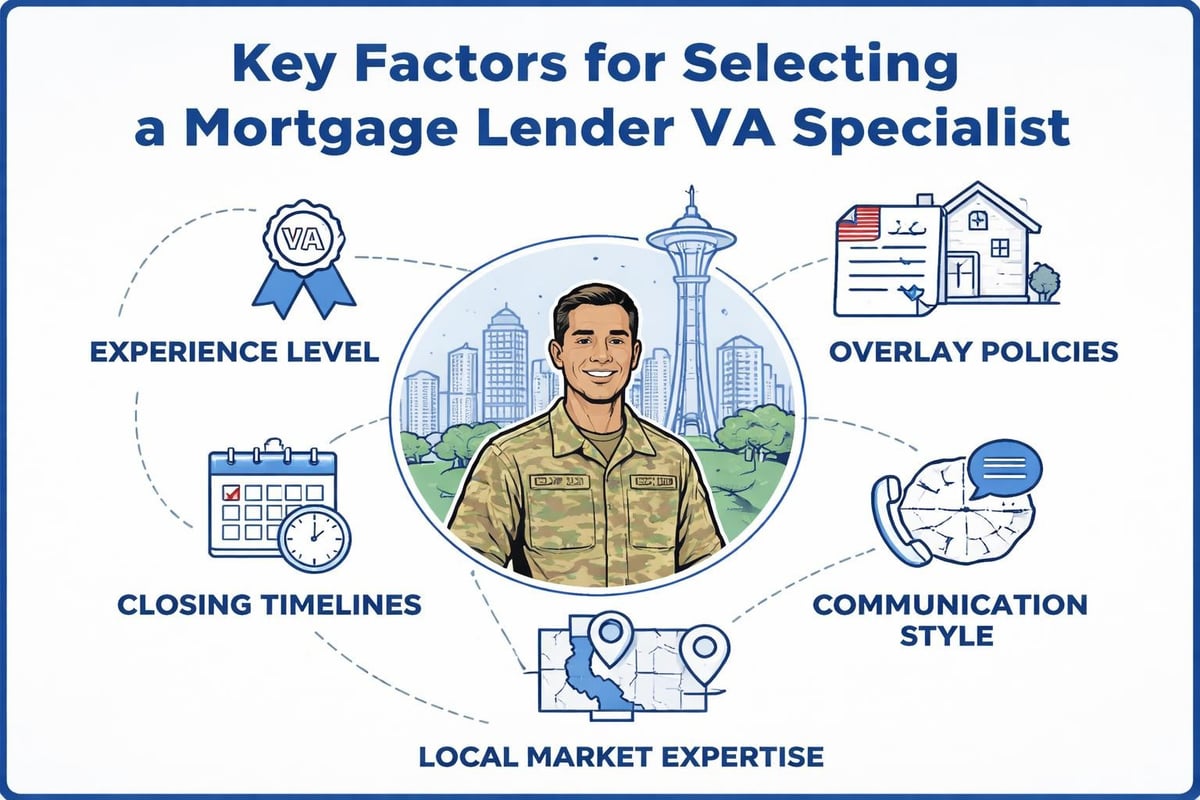

Evaluating Mortgage Lender VA Expertise and Experience

Not all lenders possess equal proficiency with VA loans. The Department of Veterans Affairs sets minimum guidelines, but each mortgage lender VA provider implements their own overlays-additional requirements beyond the VA's standards. These overlays significantly impact your approval odds and loan terms.

Critical Questions to Ask Potential Lenders

| Question | Why It Matters | What to Look For |

|---|---|---|

| What is your minimum credit score for VA loans? | VA has no minimum, but lenders impose overlays | 580-620 range indicates flexibility |

| How many VA loans do you close annually? | Experience correlates with problem-solving ability | 50+ loans shows specialization |

| What is your average closing timeline? | Speed matters in competitive Seattle markets | 21-30 days is standard, 9-14 days exceptional |

| Do you manually underwrite VA loans? | Reveals capacity to overcome automated denials | Should offer manual underwriting when beneficial |

The largest VA mortgage lenders process thousands of loans annually, providing volume-based efficiency. However, boutique lenders and experienced local mortgage brokers often deliver superior personalized service, particularly for complex income scenarios common among tech professionals in Redmond or Bellevue.

Lender Overlays and Their Impact

Understanding VA lender overlays becomes essential when comparing mortgage lender VA options. While the VA itself has no minimum credit score requirement, most lenders impose minimums ranging from 580 to 640. Some require specific debt-to-income ratios, reserve requirements, or employment history standards beyond VA guidelines.

For instance, a veteran with a 595 credit score and strong compensating factors might be declined by one mortgage lender VA provider but approved by another with more flexible overlays. This variation makes shopping multiple lenders particularly valuable in markets like Lake Forest Park or Mill Creek.

VA Loan Eligibility and Certificate of Eligibility

Before approaching any mortgage lender VA specialist, veterans must understand their eligibility status and obtain their Certificate of Eligibility (COE). The VA loan eligibility requirements outline service duration standards and discharge conditions.

Service Requirements by Military Branch

Different service categories carry distinct eligibility thresholds:

- Active-duty service members: 90 consecutive days during wartime or 181 days during peacetime

- Veterans: Generally six years in the Selected Reserve or National Guard

- Surviving spouses: Unremarried spouses of veterans who died in service or from service-connected disabilities

- Discharged service members: Must have received other than dishonorable discharge

Most mortgage lender VA professionals can help you obtain your COE electronically within minutes if you meet the basic service requirements. Veterans who served during multiple periods may have enhanced entitlement, allowing for larger loan amounts or multiple simultaneous VA loans.

Entitlement and Loan Limits in Seattle

In 2026, King County and Snohomish County have conforming loan limits of $806,500. Veterans with full entitlement can purchase homes above this amount with no down payment, though lenders may require a down payment on the portion exceeding the limit. A mortgage lender VA expert can calculate your specific entitlement and determine whether you can finance a $900,000 home in Lynnwood with zero down or need to bring additional funds.

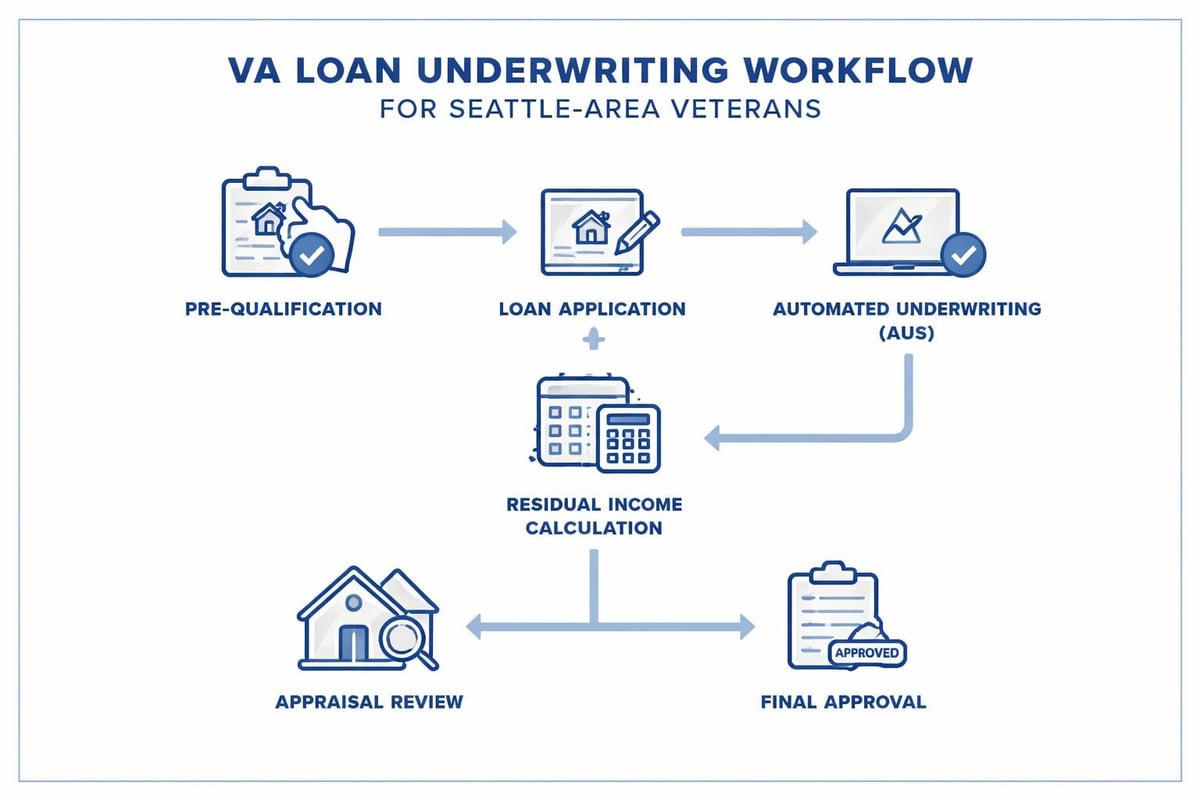

The VA Loan Underwriting Process

Understanding how mortgage lender VA underwriting works helps set realistic expectations and prepares you for documentation requirements. The VA loan underwriting process involves both automated and manual evaluation methods.

Automated Underwriting and Manual Review

Most loans first pass through automated underwriting systems that evaluate credit, income, assets, and liabilities. Veterans receive one of three findings:

- Accept/Approved: Loan meets automated guidelines with minimal documentation

- Refer/Eligible: Requires manual underwriting review but remains approvable

- Refer/Ineligible: Does not meet automated standards, needs compensating factors

A skilled mortgage lender VA partner understands how to package applications to maximize automated approval odds while successfully navigating manual underwriting when necessary. For tech professionals with stock-based compensation from Amazon or Microsoft, manual underwriting often provides better outcomes by allowing underwriters to consider RSU vesting schedules and promotion potential.

Residual Income Requirements

Unlike conventional loans that focus primarily on debt-to-income ratios, VA loans emphasize residual income-the amount of money left after paying all debts and estimated living expenses. This approach recognizes that a family's ability to manage a mortgage extends beyond simple ratio calculations.

For Seattle-area veterans, residual income requirements vary by family size:

| Family Size | Required Monthly Residual Income (West Region) |

|---|---|

| 1 person | $492 |

| 2 people | $823 |

| 3 people | $990 |

| 4 people | $1,117 |

| 5 people | $1,245 |

| Over 5 | Add $80 per additional person |

Your mortgage lender VA specialist should calculate residual income during pre-qualification to ensure you meet these thresholds comfortably, particularly important when stretching your budget in expensive markets like Everett or Seattle.

Credit Score Considerations for VA Loans

While the VA imposes no minimum credit score, every mortgage lender VA provider establishes their own thresholds. Understanding VA loan credit score benchmarks helps you assess your approval likelihood and identify areas for improvement.

Credit Score Tiers and Lender Requirements

Most mortgage lender VA specialists work within these general frameworks:

- 640 and above: Qualifies with most lenders, best rates available

- 620-639: Approved by many lenders, potentially higher rates

- 580-619: Limited lender options, may require compensating factors

- Below 580: Very few lenders, requires exceptional compensating factors

Veterans with credit scores below 620 benefit significantly from working with experienced mortgage brokers who maintain relationships with multiple investors. A broker can simultaneously submit your application to several mortgage lender VA sources, identifying which offers the most favorable terms for your specific situation.

Compensating Factors That Strengthen Applications

Lower credit scores don't automatically disqualify veterans. Strong compensating factors include:

- Significant cash reserves (six months or more of payments)

- Low debt-to-income ratios (below 35%)

- Stable employment history (two-plus years same employer)

- Substantial residual income exceeding minimums

- Previous successful homeownership

- Down payment (even small amounts demonstrate commitment)

A veteran purchasing in Mill Creek with a 595 credit score, 28% debt-to-income ratio, and twelve months of reserves might secure approval where someone with a 620 score but 48% debt-to-income ratio would not.

Finding the Best Mortgage Lender VA Partner in Seattle

Selecting your mortgage lender VA representative requires research beyond interest rate shopping. While rates matter, execution quality, communication consistency, and problem-solving capabilities often prove more valuable in competitive Seattle markets where offers face multiple counteroffers.

Evaluation Criteria Beyond Interest Rates

When comparing best VA loan lenders, consider these factors:

- Local market knowledge: Understanding Seattle-specific appraisal challenges, HOA requirements, and competitive bidding strategies

- Technology platform: Digital application, document upload, and status tracking capabilities

- Underwriting authority: In-house underwriting versus outsourced processing

- Closing speed: Ability to meet tight deadlines common in seller's markets

- Availability: Responsiveness during evenings and weekends when decisions happen quickly

Veterans working with Seattle real estate professionals benefit from loan officers who communicate proactively with listing agents, provide pre-approval letters that carry weight, and can adjust timelines when necessary to strengthen offers.

Questions About Stock Compensation and Tech Industry Income

Seattle's concentration of major technology employers creates unique income documentation scenarios. Veterans employed by Amazon, Microsoft, Google, or similar companies often receive substantial portions of compensation through restricted stock units (RSUs), stock options, and performance bonuses.

Traditional mortgage lender VA providers may struggle to properly qualify this income, either being overly conservative or lacking understanding of vesting schedules and grant structures. Specialists familiar with tech compensation can:

- Calculate average RSU income using vesting schedules and stock price history

- Document bonus income using historical patterns and employment agreements

- Maximize qualifying income while maintaining conservative underwriting standards

- Structure loans that account for variable income fluctuations

For a software engineer in Redmond with $140,000 base salary plus $60,000 annual RSU income, proper documentation might increase buying power by $150,000-200,000 compared to lenders who only consider base compensation.

VA Funding Fee and Closing Cost Considerations

Every VA loan includes a funding fee-a percentage of the loan amount that helps sustain the program for future generations. Your mortgage lender VA specialist should clearly explain this fee and available exemptions during the pre-qualification process.

Funding Fee Structure in 2026

| Service Category | First Use | Subsequent Use | With Down Payment (5-10%) |

|---|---|---|---|

| Regular Military | 2.15% | 3.30% | 1.50% |

| Reserve/Guard | 2.40% | 3.30% | 1.50% |

| Exempt (Disability) | 0% | 0% | 0% |

Veterans with service-connected disabilities rated at 10% or higher receive full funding fee exemption, potentially saving thousands of dollars. A $700,000 loan would carry a $15,050 funding fee for first-time users without disability exemption-a substantial amount that can be financed into the loan or paid at closing.

Allowable and Prohibited Closing Costs

VA regulations strictly limit what veterans can be charged. Allowable costs include:

- Appraisal and inspection fees

- Credit report charges

- Title insurance and recording fees

- Origination charges (limited to 1% of loan amount)

- Discount points (if veteran chooses to pay)

Prohibited charges that sellers or lenders must cover include:

- Loan processing or underwriting fees

- Document preparation charges

- Attorney fees (except in attorney states)

- Application fees

- Postage or courier costs

Experienced mortgage lender VA professionals structure transactions to minimize veteran out-of-pocket expenses while ensuring sellers understand their obligations under VA guidelines. In competitive Seattle markets, this knowledge prevents deals from falling apart due to closing cost disputes.

VA Appraisal Requirements and Seattle Market Challenges

The VA appraisal process serves dual purposes: establishing market value and ensuring the property meets minimum safety and habitability standards. Unlike conventional appraisals that focus solely on value, VA appraisals identify required repairs that must be completed before closing.

Common VA Appraisal Issues in Seattle-Area Homes

Older homes in neighborhoods throughout Seattle, Shoreline, or Lynnwood may encounter VA appraisal challenges:

- Peeling paint on homes built before 1978 (lead-based paint concern)

- Missing handrails on stairs with three or more steps

- Roof condition requiring certification of two years remaining useful life

- Foundation cracks or water intrusion evidence

- GFCI outlets missing in kitchens and bathrooms

- Wood-destroying organism damage or evidence

Your mortgage lender VA partner should prepare you for potential repair requirements and help negotiate who bears responsibility. In seller's markets, buyers sometimes agree to handle minor repairs to keep deals together, though the VA requires completion before funding.

Appraisal Timelines and Rush Options

Standard VA appraisals take 10-14 days from order to completion in the Seattle area. During peak spring and summer markets, this timeline can extend to three weeks. Mortgage lender VA specialists with established appraiser relationships often secure faster turnarounds, critical when competing against cash offers or conventional financing with waived appraisal contingencies.

Some lenders offer appraisal rush services for additional fees, reducing turnaround to 5-7 days. While the VA funding fee cannot be financed on refinances of non-VA loans, purchase transactions allow veterans to roll nearly all costs into the loan amount, preserving cash reserves.

Specialized VA Loan Scenarios for Seattle Veterans

Beyond standard purchase transactions, VA loans offer flexibility for various scenarios common among Greater Seattle homeowners and investors.

VA Jumbo Loans in High-Cost Seattle Markets

Properties exceeding conforming loan limits still qualify for VA financing, though down payment requirements may apply. A veteran purchasing an $1,100,000 home in Bellevue with full entitlement could finance $806,500 with zero down, requiring approximately $293,500 down payment for the remainder. Some mortgage lender VA providers offer more favorable terms by using proprietary jumbo programs that maintain VA-like benefits for the entire loan amount.

VA Renovation Loans for Fixer-Uppers

The VA renovation loan program allows veterans to purchase properties needing repairs and finance improvement costs into a single mortgage. This option works well for homes in Lake Forest Park or Everett requiring updates but offering strong value potential. Your mortgage lender VA specialist can determine whether the standard VA loan or a VA renovation product better serves your goals.

VA IRRRL Refinances

The Interest Rate Reduction Refinance Loan (IRRRL) streamlines refinancing existing VA loans when rates drop. These transactions require minimal documentation, no appraisal in most cases, and reduced funding fees. Veterans who financed Seattle homes when rates peaked in 2023-2024 should monitor opportunities to refinance, potentially saving hundreds monthly.

Understanding when an IRRRL makes sense requires analysis of break-even points, remaining loan terms, and future ownership plans. A knowledgeable mortgage lender VA advisor provides this analysis without pressure, ensuring refinance decisions align with your long-term financial strategy. For investors, understanding how conventional loans for investment properties compare with VA options helps optimize portfolio financing.

Pre-Approval Strategy for Competitive Seattle Markets

Obtaining pre-approval from a reputable mortgage lender VA specialist before house hunting delivers significant advantages in markets where desirable properties receive multiple offers within days.

Components of a Strong Pre-Approval

Comprehensive pre-approval includes:

- Full credit report review with score optimization recommendations

- Complete income documentation including pay stubs, W-2s, and tax returns

- Asset verification confirming down payment and reserve funds

- Certificate of Eligibility obtained and verified

- Residual income calculation ensuring comfortable qualification

- Automated underwriting approval when possible

Pre-qualification letters issued without documentation review carry minimal weight with Seattle-area listing agents. Full pre-approval from a respected mortgage lender VA source, particularly one known to local real estate professionals, strengthens your position significantly.

Waiving Financing Contingencies

In extremely competitive situations, some buyers waive financing contingencies to make offers more attractive. This strategy carries risk-if your loan doesn't fund, you potentially forfeit earnest money. Only consider contingency waivers when:

- You have full underwriting approval (not just pre-approval)

- Your mortgage lender VA specialist confirms no outstanding conditions

- The property clearly meets VA appraisal standards

- You have backup financing capability or cash to close if needed

Veterans purchasing in Everett, Mill Creek, or similar markets with moderate competition rarely need such aggressive strategies, while those targeting highly desirable Seattle neighborhoods may face pressure to remove contingencies to remain competitive.

Working with Real Estate Agents and Your Mortgage Lender VA Team

Successful transactions require coordination between your real estate agent and mortgage lender VA professional. Strong communication prevents surprises and ensures smooth progression from offer acceptance through closing.

Information Your Agent Needs from Your Lender

Effective real estate agents request specific details to properly position your offers:

- Exact pre-approval amount with confirmation of down payment funds

- Closing timeline capabilities to meet seller preferences

- Lender contact information for listing agent verification

- Potential appraisal or underwriting concerns related to property type or condition

- Flexibility for short or extended closing periods based on transaction needs

Your mortgage lender VA partner should proactively communicate with your agent, providing updates on application progress, underwriting conditions, and appraisal results. This transparency allows agents to manage seller expectations and address issues before they threaten the transaction.

Questions Your Lender Needs from Your Agent

Conversely, mortgage lender VA specialists require information from real estate agents:

- Property address and listing details for initial review

- HOA requirements, dues, and special assessments

- Known property condition issues that might affect VA appraisal

- Seller's preferred closing timeline and flexibility

- Competing offer situations requiring expedited processing

VA loans provide exceptional benefits for eligible veterans, service members, and surviving spouses navigating Seattle's dynamic housing market. Selecting an experienced mortgage lender VA specialist who understands local market conditions, technology industry compensation, and VA underwriting nuances maximizes your chances of securing favorable terms and closing successfully.

Keith Akada brings 25+ years of mortgage expertise to Seattle-area veterans, combining comprehensive VA loan knowledge with the advanced underwriting capabilities of Fairway. Whether you're purchasing your first home in Shoreline, upgrading to a larger property in Bellevue, or refinancing an existing VA loan, Mortgage Reel delivers the education, transparency, and execution excellence that has earned over 750 five-star reviews from satisfied clients throughout the Greater Seattle region.