Seattle homeowners, are rising mortgage rates causing you concern, or are you actively seeking ways to save in 2026? The mortgage loan refinance landscape is evolving across Seattle, Lynnwood, Shoreline, Mill Creek, and Everett, presenting new opportunities for savvy homeowners.

With the right mortgage loan refinance strategy, you could lower your monthly payments, reduce total interest, or access your home’s equity for renovations or investments.

This guide is designed to walk you through every step of the process—covering refinance basics, rate trends, a step-by-step approach, local Seattle market insights, and expert tips. My goal is to help you confidently navigate mortgage loan refinance decisions and secure the best rates and terms available in 2026.

Understanding Mortgage Loan Refinancing: What It Is & Why It Matters

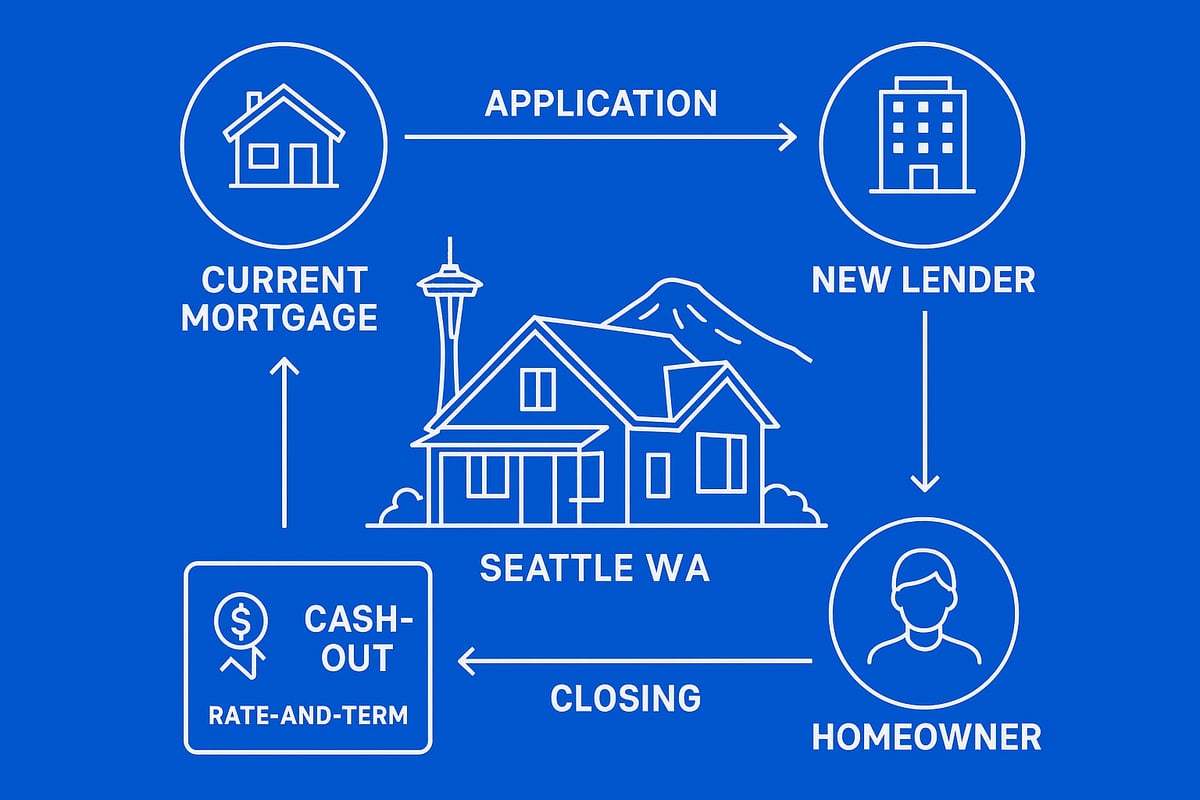

Seattle homeowners often ask, “What exactly is mortgage loan refinance, and why should I consider it?” Refinancing replaces your current mortgage with a new one, typically to secure better terms or rates. Unlike a loan modification, which changes terms on your existing loan, refinancing creates an entirely new agreement. Many in Lynnwood and Shoreline refinance for lower rates, shorter terms, or to tap home equity for projects like adding an ADU. Nationally, more than 5 million homeowners refinanced during the last major rate drop. Two main types exist: rate-and-term (changing rate or term) and cash-out (accessing equity). For more strategies tailored to Seattle, explore these Seattle mortgage refinance options.

What Does Mortgage Refinancing Mean?

Refinancing your mortgage means replacing your existing home loan with a new one. The primary goal is often to improve your financial position. Unlike a modification, which adjusts terms on your existing loan, a mortgage loan refinance starts fresh, potentially with a new lender. Common reasons Seattle-area homeowners pursue this include lowering their interest rate, shortening the loan term, consolidating debt, or pulling out cash for renovations. For example, a Lynnwood homeowner might refinance to fund an additional dwelling unit. Nationally, over 5 million homeowners refinanced in the last big rate drop. The two main types are rate-and-term and cash-out refinancing.

Benefits of Refinancing Your Mortgage in 2026

A mortgage loan refinance in 2026 can provide several advantages for Seattle and nearby residents. Lowering your monthly payment is a major benefit, especially if rates have dropped or your credit has improved. You may also reduce the total interest paid over the life of the loan, or switch from an adjustable to a fixed rate for greater stability. Eliminating private mortgage insurance (PMI) is possible once you reach enough equity. For example, a Mill Creek resident recently saved $250 per month by refinancing. Accessing home equity for renovations or investments is another key reason homeowners in Everett and Lake Forest Park consider refinancing.

When Does Refinancing Make Sense?

Knowing when to pursue a mortgage loan refinance is crucial. Generally, if current rates are at least 0.5 to 1 percent lower than your existing rate, it might be worth exploring. Calculate your break-even point by dividing total closing costs by your projected monthly savings. If you plan to stay in your home longer than the break-even period, refinancing could be smart. Think about your remaining loan term and future plans, such as moving or staying put. In Shoreline, for instance, a homeowner with seven years left on their loan weighed the costs and benefits before choosing whether to refinance.

Risks and Considerations

Before moving forward with a mortgage loan refinance, review all the risks involved. Closing costs in Seattle typically range from $2,500 to $5,000, depending on your property and lender. Extending your loan term could mean paying more interest over time, even if your monthly payment drops. Some loans carry prepayment penalties, so check your current agreement. Your credit score might dip temporarily after applying. In Everett, one homeowner faced higher costs due to having low equity. Always review every loan disclosure carefully and compare offers to make informed decisions.

The 2026 Interest Rate Landscape: What Seattle Homeowners Need to Know

Seattle’s mortgage loan refinance environment is shifting in 2026, and understanding the rate landscape is essential. Whether you live in Lake Forest Park, Shoreline, or downtown Seattle, knowing how rates move and what drives them can help you make confident decisions. Let’s break down what you need to know about current trends, payment impacts, local market dynamics, and unique regional considerations.

Current and Projected Rate Trends

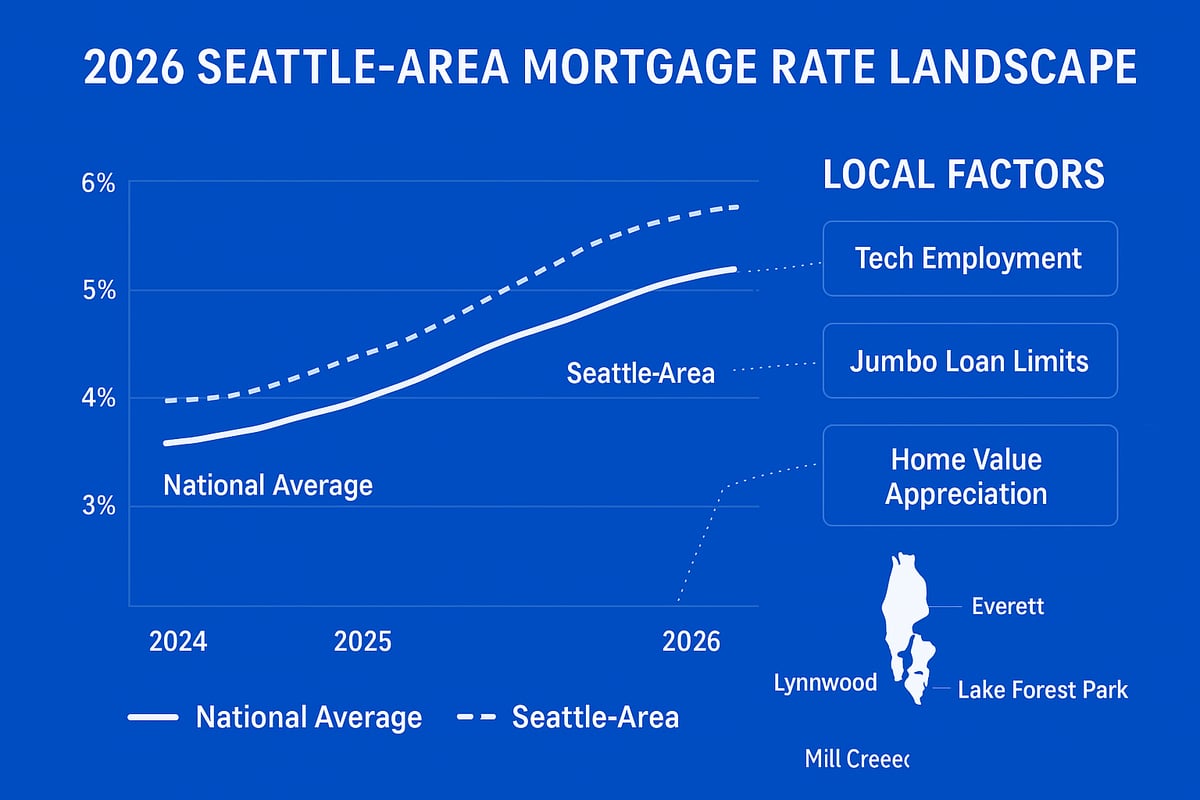

Mortgage loan refinance opportunities in Seattle depend heavily on rate trends. In 2026, experts project moderate rate fluctuations, with Seattle often tracking slightly below national averages. Local lenders in cities like Lake Forest Park are advertising rates about 0.2% lower than the U.S. average. Rates are shaped by Federal Reserve policy, inflation, and the regional economic outlook, especially in tech-heavy areas. For homeowners considering a mortgage loan refinance, staying informed on these shifts is critical. For a comprehensive look at forecasts, review the 2026 Mortgage Rates Forecast According to Experts.

How Rates Affect Your Refinance Decision

Even a small rate change can transform your mortgage loan refinance outcome. For example, if you have a $500,000 balance on a 30-year term, dropping from 6% to 5.5% could reduce your payment by about $165 per month. Here’s a quick comparison:

| Rate | Monthly Payment |

|---|---|

| 6.0% | $2,998 |

| 5.5% | $2,833 |

Rate locks let you secure today’s rate while your mortgage loan refinance is processed, protecting you from market swings. Timing your application is key—some homeowners in Mill Creek benefit by acting when rates dip, while others wait for economic signals.

Local Market Factors in Seattle & Surrounding Cities

Seattle’s mortgage loan refinance market is shaped by regional trends. Home values in Lynnwood and Everett have risen from 2024 to 2026, boosting homeowner equity and opening new refinance possibilities. Lender competition in the Puget Sound region means more loan options and competitive fees. In Shoreline, for instance, increased property values have shortened the break-even period for many refinancers. Staying aware of these local dynamics ensures you maximize your mortgage loan refinance potential.

Special Considerations for Seattle-Area Borrowers

Unique factors influence mortgage loan refinance decisions in the Seattle area. King and Snohomish counties have higher jumbo loan limits, which benefits homeowners with larger properties. Many tech professionals in Redmond and Bellevue use RSU or stock income to qualify for better terms. Local lenders sometimes offer exclusive programs or incentives tailored to the area’s workforce. For example, a Redmond tech employee recently leveraged RSUs to secure an advantageous mortgage loan refinance, demonstrating the value of regional expertise.

Step-by-Step Guide to Refinancing Your Mortgage in Seattle

Refinancing your mortgage in Seattle can be a smart move, but the process involves several important steps. As a local mortgage broker, I guide homeowners from Everett to Lake Forest Park through each phase with clarity and confidence. Here, I break down the seven essential steps to a successful mortgage loan refinance. Whether your goal is to lower payments, access cash, or secure a better rate, this roadmap is tailored for Seattle-area homeowners in 2026.

1. Assess Your Financial Goals

The first step in any mortgage loan refinance is to define your objectives. Are you hoping to lower your monthly payment, shorten your loan term, remove PMI, or tap into your home’s equity? For example, an Everett homeowner may choose refinance for debt consolidation, while someone in Lynnwood might aim to fund an ADU addition.

Start by calculating your current loan balance, interest rate, and remaining term. This helps you determine what makes financial sense. If your main goal is to reduce your payment, consider reviewing strategies in this how to lower your mortgage payment guide. Clear goals set the foundation for a successful mortgage loan refinance.

2. Check Your Credit and Home Equity

Lenders look closely at your credit score and home equity before approving a mortgage loan refinance. Excellent credit typically secures the best rates, while strong home equity can help you avoid PMI or qualify for cash-out options. In Seattle, average homeowner equity reached new highs in 2026, especially in Mill Creek and Shoreline.

Check your credit using a reputable service and review your home’s value through recent comparable sales or a professional appraisal. Improving your credit before applying can save you thousands over the life of your mortgage loan refinance.

3. Research Lenders and Loan Options

Next, compare lenders and loan programs available in Seattle and surrounding cities. Options include banks, credit unions, and local mortgage brokers. Each may offer different rates, fees, and loan types for your mortgage loan refinance.

Decide between fixed-rate and adjustable-rate refinance options. For example, closing costs can vary between Shoreline and downtown Seattle, so request detailed cost breakdowns. Compare at least three lenders to ensure you find the best fit for your needs and situation.

4. Gather Documentation

Gathering the right documents up front streamlines your mortgage loan refinance. Typical requirements include pay stubs, W-2s, tax returns, mortgage statements, and asset statements. Tech professionals in Redmond or Bellevue may need to provide RSU or stock grant documentation.

Self-employed or investor homeowners in Everett and Lynnwood should prepare business tax returns and profit-loss statements. Having everything organized before you apply helps avoid delays and keeps your mortgage loan refinance on track.

5. Apply and Lock Your Rate

Once you choose a lender, complete the application for your mortgage loan refinance. Be ready to provide all requested documents promptly. The lender will review your file and, if approved, offer the chance to lock your rate.

Rate locks protect you from market fluctuations during the process. For instance, a Mill Creek homeowner who locked their rate early in 2026 closed in under three weeks. Timing your rate lock can make a significant difference in the final outcome of your mortgage loan refinance.

6. Home Appraisal and Approval

After applying, most mortgage loan refinance cases require a home appraisal. The appraisal determines your property’s current value and affects your loan-to-value (LTV) ratio. In Seattle, Everett, and Lake Forest Park, appraisal timelines average 7-14 days.

If the appraisal comes in lower than expected, you may need to adjust your loan amount or provide additional documentation. A low appraisal can impact your ability to remove PMI or access cash, so it’s important to stay in close contact with your lender throughout your mortgage loan refinance.

7. Closing Your Refinance

The final step in a mortgage loan refinance is closing. You’ll receive closing disclosures outlining all costs, including origination, appraisal, title, and escrow fees. In Seattle and nearby cities like Lynnwood or Shoreline, average closing costs range from $2,500 to $5,000.

Review all documents carefully before signing. Once complete, your new loan funds and your updated payment schedule begins. With your mortgage loan refinance closed, you can enjoy the benefits of your new terms—whether that’s a lower payment, shorter loan, or access to home equity.

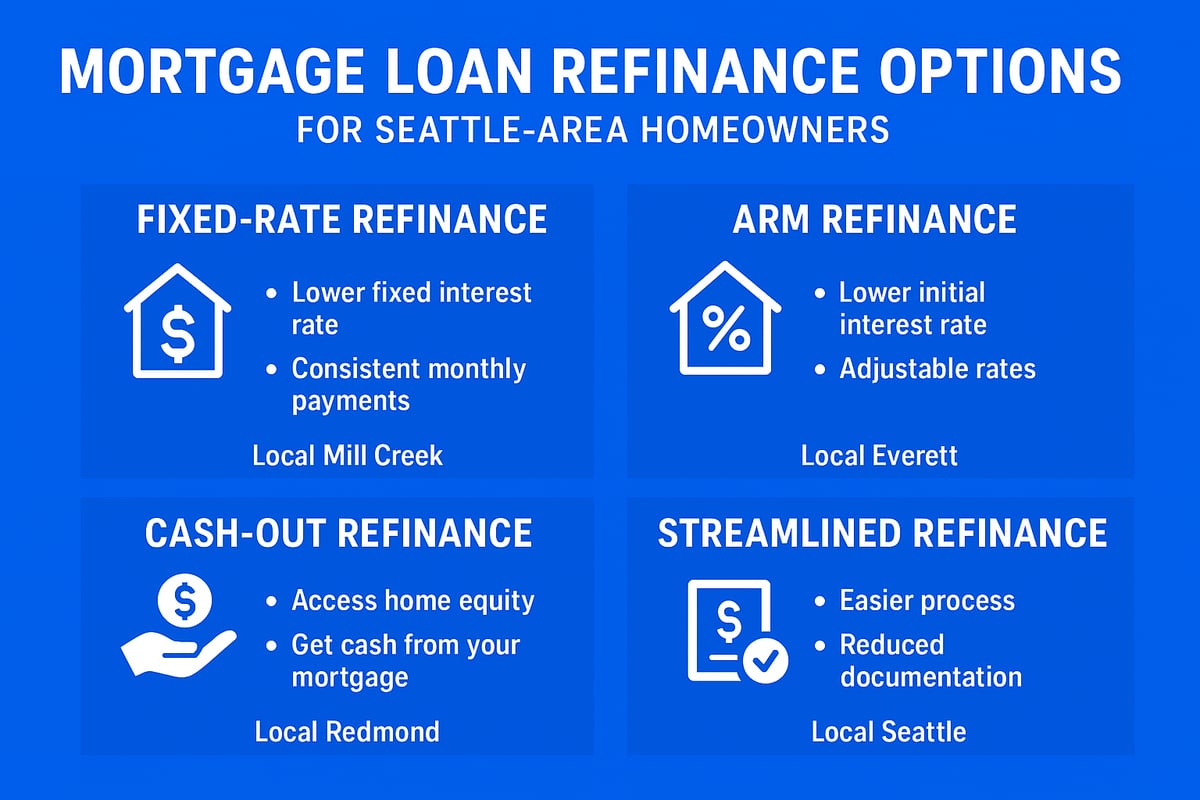

Popular Refinance Options for Seattle-Area Homeowners

When considering a mortgage loan refinance in Seattle, it is essential to understand the main options available. Each refinance type offers unique advantages and may suit different financial goals for homeowners in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Let us explore the most popular choices so you can make an informed decision for your situation.

Fixed-Rate Mortgage Refinance

A fixed-rate mortgage loan refinance is a top choice for Seattle homeowners seeking predictable monthly payments and long-term stability. This option lets you lock in a single interest rate for the life of your new loan, whether you choose a 30-year, 20-year, 15-year, or 10-year term. Many Lake Forest Park families opt for a 15-year fixed refinance, securing rates like 5.5 percent APR and building equity faster.

Key benefits include:

- Consistent payments that never change

- Protection from rising interest rates

- Multiple term options to fit your goals

Maximum loan amounts and loan-to-value (LTV) requirements apply, especially in King and Snohomish counties. Always compare Current Seattle mortgage rates to find the most competitive offer for your mortgage loan refinance.

Adjustable-Rate Mortgage (ARM) Refinance

With an adjustable-rate mortgage loan refinance, you can benefit from a lower initial interest rate, which adjusts after a set period. Common ARM options in Seattle include 3/1, 5/1, and 7/1 ARMs, where the first number shows the fixed period in years. Homeowners who plan to move within five to seven years, like many in Redmond, may find ARMs especially attractive.

Typical ARM features:

- Lower starting interest rates than fixed-rate loans

- Fixed-rate period before adjustments begin

- Potential savings for short-term homeowners

For example, a Redmond resident planning to relocate in five years chose a 5/1 ARM, maximizing savings during their expected timeframe. Always review how future adjustments could affect your payment before finalizing your mortgage loan refinance.

Cash-Out Refinance

A cash-out mortgage loan refinance allows you to tap into your Seattle-area home equity for renovations, debt consolidation, or investment. You replace your old mortgage with a larger one and receive the difference in cash at closing. In Everett, one homeowner used a cash-out refinance to purchase a rental property, leveraging increased home values from 2024 to 2026.

Points to consider:

- LTV limits typically cap cash-out at 80 percent of your home’s value

- Local restrictions may apply in Seattle and nearby cities

- Funds can be used for home improvements or other financial goals

Be mindful of potential tax implications when accessing equity through a mortgage loan refinance. Consult a tax professional for personalized advice.

Streamlined and Express Refinance Options

Streamlined mortgage loan refinance programs, like Refi Express, offer reduced paperwork and faster closings for well-qualified borrowers. These are ideal for Seattle-area residents with strong credit and straightforward finances. For instance, a Shoreline homeowner recently closed a streamlined refinance in just 10 days, enjoying a quick and hassle-free process.

Streamlined options typically feature:

- Fewer documentation requirements

- Lower fees and reduced approval times

- Qualification based on payment history and equity

If you have a solid payment record and sufficient equity in your home, a streamlined mortgage loan refinance can help you save time and money. Always review eligibility requirements with your lender.

Costs, Fees & Break-Even Analysis: Making the Math Work

Refinancing your home in Seattle or nearby cities like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett requires a clear understanding of the true costs involved. Before you start a mortgage loan refinance, it’s crucial to know what expenses to expect, how you can pay them, and when your investment will pay off. Let’s break down the essentials so you can make informed decisions and maximize your savings.

Typical Refinance Costs in Seattle & Surrounding Areas

When you pursue a mortgage loan refinance in Seattle, you’ll encounter a variety of closing costs. These typically include:

- Origination fees

- Appraisal fees

- Title insurance

- Escrow services

- Recording fees

- Local taxes

To give you a sense of what to expect, here’s a comparison of average total closing costs by county:

| Area | Average Closing Costs |

|---|---|

| Seattle/King | $3,800 |

| Snohomish | $3,200 |

| Everett | $2,900 |

Expect most refinance costs to fall between $2,500 and $5,000. Always review the Loan Estimate provided by your lender, as fees can vary between Shoreline, Lynnwood, and other local markets.

Rolling Costs Into Your Loan vs. Paying Upfront

One decision you’ll face during a mortgage loan refinance is whether to pay your closing costs upfront or roll them into your new loan balance. Each option has pros and cons:

- Paying upfront reduces your loan balance and total interest paid.

- Rolling costs into the loan increases your loan amount, which may raise your monthly payment and total interest over time.

For example, a Lynnwood homeowner who rolled $4,000 in costs into their refinance saw a slight increase in their monthly payment, but avoided out-of-pocket expenses at closing. Consider your cash flow needs and long-term goals when making this decision.

Calculating Your Break-Even Point

Understanding when your mortgage loan refinance will start saving you money is essential. The break-even point tells you how long it takes to recoup your closing costs through lower monthly payments. Here’s a simple formula:

Break-Even (months) = Total Closing Costs / Monthly Savings

For instance, if a Mill Creek homeowner pays $3,600 in refinance costs and saves $200 per month, the break-even point is 18 months. If you’re interested in strategies to reduce your term and interest, check out Pay off your mortgage faster for practical tips that complement refinancing.

Avoiding Common Costly Mistakes

A successful mortgage loan refinance in Seattle means steering clear of pitfalls that can erode your savings. Watch out for these common errors:

- Failing to shop multiple lenders for lower rates or credits

- Extending your loan term unnecessarily, increasing total interest

- Ignoring local grants or lender credits in cities like Everett or Lake Forest Park

- Not reviewing all closing disclosures carefully

A Seattle homeowner recently saved $1,200 by comparing three lender offers. Take time to evaluate all options, and always ask questions before you sign.

Seattle-Area Refinance FAQs: Direct Answers for Homeowners

Seattle homeowners often have pressing questions about the mortgage loan refinance process, especially as the 2026 market evolves. Below, I address the most common concerns I hear from clients in Seattle, Everett, Lynnwood, Lake Forest Park, Mill Creek, and Shoreline. Each answer is crafted to help you make informed decisions with clarity and confidence.

Can I Remove PMI By Refinancing?

Private Mortgage Insurance (PMI) can add significant costs to your monthly payment. If your home equity reaches at least 20 percent (80 percent loan-to-value), a mortgage loan refinance may allow you to remove PMI. In Washington, lenders typically require a new appraisal to confirm your property’s value. For example, an Everett homeowner who saw their property appreciate in 2025 refinanced after their equity surpassed 20 percent, eliminating PMI and saving over $150 monthly. Always check your lender’s specific requirements, as they may vary by loan type and investor.

Quick Table: PMI Removal by Refinance in WA

| Requirement | Typical Threshold |

|---|---|

| Minimum Equity | 20% (80% LTV) |

| New Appraisal Needed | Yes |

| Satisfactory Payment History | Yes |

How Fast Can I Close a Refinance in Seattle?

The average mortgage loan refinance in Seattle closes within 21 to 30 days, but several factors can speed this up or slow it down. Having all your documents ready, responding quickly to lender requests, and using streamlined programs can shorten the timeline. For instance, a Mill Creek resident who submitted complete paperwork and scheduled their appraisal promptly closed in just 18 days. On the other hand, appraisal delays or incomplete documentation can stretch the process beyond a month. If speed is critical, ask about express or streamlined refinance options.

Typical Closing Timeline

- Standard refinance: 21–30 days

- Streamlined/express: 10–18 days

- Delays: Appraisal issues, missing docs

What If My Home Appraises Low?

A low appraisal can affect your mortgage loan refinance approval by increasing your loan-to-value ratio or reducing the amount you can borrow. If your appraisal comes in lower than expected, you have options: dispute the appraisal with additional comps, bring extra cash to closing, or adjust your loan amount. One Lake Forest Park homeowner successfully negotiated a higher value by providing recent comparable sales to the appraiser. Staying informed about current market values is crucial, especially as local trends can shift quickly. For more on how rate and value trends impact refinancing, see Assessing Mortgage Rate Trends and Refinance Opportunities in 2026.

Can I Refinance If I Have a Second Mortgage or HELOC?

Yes, you can complete a mortgage loan refinance even if you have a second mortgage or a home equity line of credit (HELOC), but the process requires extra coordination. The second lender must agree to subordinate their lien, meaning your new first mortgage takes priority. This often involves paperwork and may add a few days to the process. In Lynnwood, a homeowner with a HELOC worked closely with both lenders and successfully refinanced, improving their overall interest rate. Make sure to discuss all existing liens with your mortgage professional upfront to avoid surprises.

Steps for Refinancing with a Second Mortgage

- Notify both lenders early

- Request subordination from the second lender

- Prepare additional documentation

- Confirm updated title report

Are There Special Programs for Tech Professionals or Investors?

Seattle’s unique employment landscape means many clients have income from RSUs, bonuses, or investments. Several lenders offer mortgage loan refinance programs that recognize these income sources, especially in tech hubs like Redmond and Kirkland. For example, a Kirkland tech employee used vested RSUs as qualifying income for a jumbo refinance, securing a better rate and loan amount. Investors can access programs tailored to rental property owners, with flexible guidelines. Always ask potential lenders about their experience with complex financial profiles and local incentives for tech professionals.

Pro Tips for Getting the Best Refinance Rate & Experience in 2026

Seattle homeowners, navigating the mortgage loan refinance process in 2026 requires more than just rate shopping. With local trends shifting in Shoreline, Lynnwood, and Mill Creek, a strategic approach can help you secure the best terms while avoiding costly mistakes. Below, I share expert strategies to help you maximize savings and streamline your experience.

Timing Your Refinance for Maximum Savings

Timing is everything when it comes to mortgage loan refinance. Seattle’s rates often move quickly, so keeping an eye on market forecasts is essential. As projected in the MBA Forecast: Mortgage Originations to Increase 8% in 2026, increased activity signals competitive options for borrowers.

To maximize your savings:

- Watch rate trends in Everett and Lake Forest Park, as local fluctuations can create unique windows for action.

- Consider locking your rate when you see a dip, especially if you’re targeting a specific payment.

- Evaluate your break-even point by comparing potential monthly savings to closing costs.

Even a 0.25% rate change can impact your long-term savings, so act decisively when the opportunity arises.

Improving Your Approval Odds

Strong financials are the foundation of a successful mortgage loan refinance. Start by checking your credit score and reviewing your debt-to-income ratio. In Mill Creek and Lynnwood, borrowers with scores above 740 often access the best rates and lender incentives.

Boost your approval chances by:

- Paying down high-interest debt before applying.

- Gathering all required documents, such as W-2s, pay stubs, and asset statements.

- Addressing any credit report errors well in advance.

For tech professionals in Seattle or Redmond, include documentation of RSU or stock income to strengthen your application. Being proactive shortens the process and improves your negotiating position with lenders.

Choosing the Right Local Lender or Mortgage Broker

Selecting the right partner for your mortgage loan refinance can directly affect your experience and outcome. Seattle-area lenders understand local market nuances, including appraisal timelines and regional programs.

Consider these tips:

- Compare rates and closing costs from at least three local sources, including credit unions in Everett and brokers serving Lake Forest Park.

- Look for transparent communication and a track record with complex or jumbo loans.

- Prioritize lenders who offer educational support, especially if your profile includes self-employment or investment properties.

A trusted Seattle-based expert can guide you through every step, ensuring your refinance aligns with your financial goals.

As you’ve seen throughout this guide, refinancing in 2026 is about more than just chasing lower rates—it’s about making smart, strategic decisions for your future. Whether you’re aiming to lower your monthly payment, tap into your home equity, or simply want clarity on the best path forward, you deserve personalized advice from someone who truly listens. I’m here to help you navigate Seattle’s evolving mortgage landscape with confidence and transparency. If you’re ready to explore your options or just want to discuss your goals, let’s connect and chart the right course together. Let’s have a conversation