Seattle’s real estate market remains one of the most dynamic in the country, with home values in neighborhoods like Shoreline, Lynnwood, and Everett reflecting steady growth. For buyers in 2026, navigating this landscape means understanding every detail of your financing options, especially the conventional home mortgage.

This guide is designed to demystify the conventional home mortgage process for Seattle and its surrounding areas. We will cover the basics, eligibility requirements, step-by-step application process, current rates, pros and cons, and actionable strategies tailored to the local market.

Whether you are a first-time buyer in Lake Forest Park or planning to upgrade in Mill Creek, this resource will give you the knowledge and confidence you need to make informed decisions. Ready to take the next step toward homeownership in Seattle? Let’s get started.

What Is a Conventional Home Mortgage?

Understanding the conventional home mortgage is essential for Seattle buyers aiming to secure the right financing in 2026. In a market as diverse as Seattle, from bustling downtown to quiet streets in Shoreline and Mill Creek, knowing your options is the first step to homeownership. Let’s break down how these mortgages work, their types, and what’s new for this year.

Defining Conventional Mortgages

A conventional home mortgage is a loan that is not insured or guaranteed by government agencies like FHA, VA, or USDA. Instead, these loans are provided by private lenders and follow guidelines set by Fannie Mae and Freddie Mac. The two main categories are conforming loans, which meet local loan limits, and non-conforming (jumbo) loans, which exceed those limits.

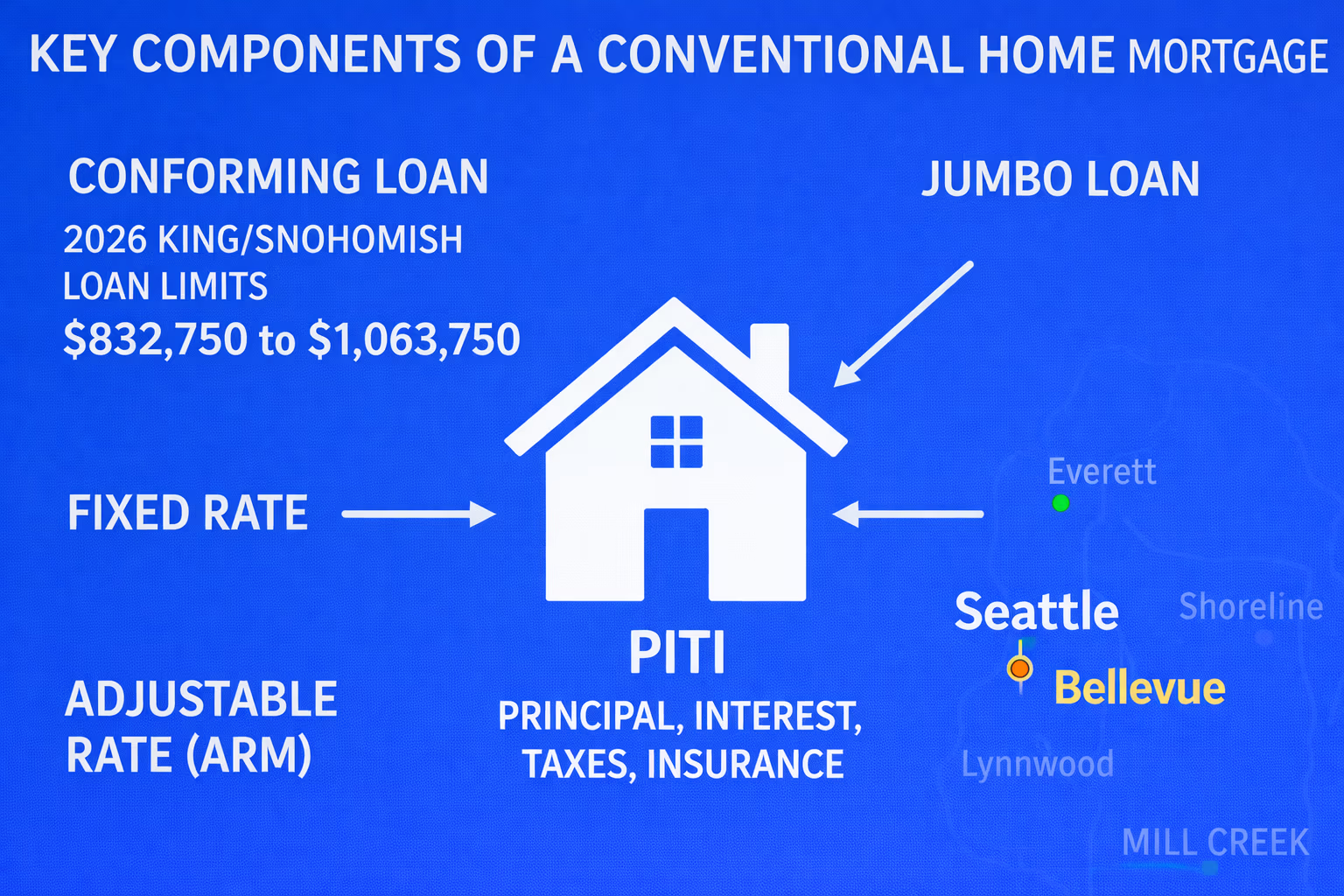

Unlike FHA or VA loans, a conventional home mortgage typically requires stronger credit and a more substantial down payment. This makes it a popular choice for buyers in Seattle, Everett, and Lynnwood who want flexibility and competitive rates. For a more detailed breakdown, see this Conventional Home Loans Overview.

Types of Conventional Loans

There are several types of conventional home mortgage options to choose from in Seattle and the surrounding region:

- Fixed-rate loans: Offer stable payments over 15, 20, or 30 years.

- Adjustable-rate mortgages (ARMs): Start with lower rates that adjust after a set period.

- Conforming loans: Stay within 2026 King and Snohomish County loan limits, which are projected to be higher to match local home values.

- Jumbo loans: Exceed conforming limits, often needed in high-priced neighborhoods.

This variety allows borrowers to tailor their conventional home mortgage to their goals and budget, whether purchasing a condo in Shoreline or a larger property in Seattle.

How Conventional Mortgages Work

Every conventional home mortgage consists of four main parts: principal, interest, taxes, and insurance (PITI). Most Seattle buyers choose 30-year terms, but 15- and 20-year options are popular for those wanting to pay off their loan sooner.

Amortization means your monthly payments gradually reduce the loan balance while paying interest. Early payments mostly cover interest, with later payments going more toward principal. This structure provides predictability for budgeting, especially in competitive markets like Seattle and the greater eastside.

Who Conventional Mortgages Are Best For

A conventional home mortgage is ideal for buyers with:

- Good to excellent credit (typically 680+)

- Stable income and employment

- Down payments of at least 3 to 5 percent for conforming, or 20 percent for jumbo loans

First-time buyers in Shoreline with solid savings, move-up buyers in Seattle, and investors in Everett often benefit most. Self-employed professionals and tech workers in may also qualify, provided they meet documentation standards, or may qualify for Non-QM financing. Loan like Bank Statement and DSCR.

Key 2026 Updates and Trends

For 2026, Seattle and King/Snohomish/Pierce Counties are seeing rising conforming loan limits, reflecting higher home prices. New guidelines may affect how lenders assess income for tech professionals and investors. Staying informed about these changes ensures your conventional home mortgage search is both efficient and successful in Seattle’s evolving market.

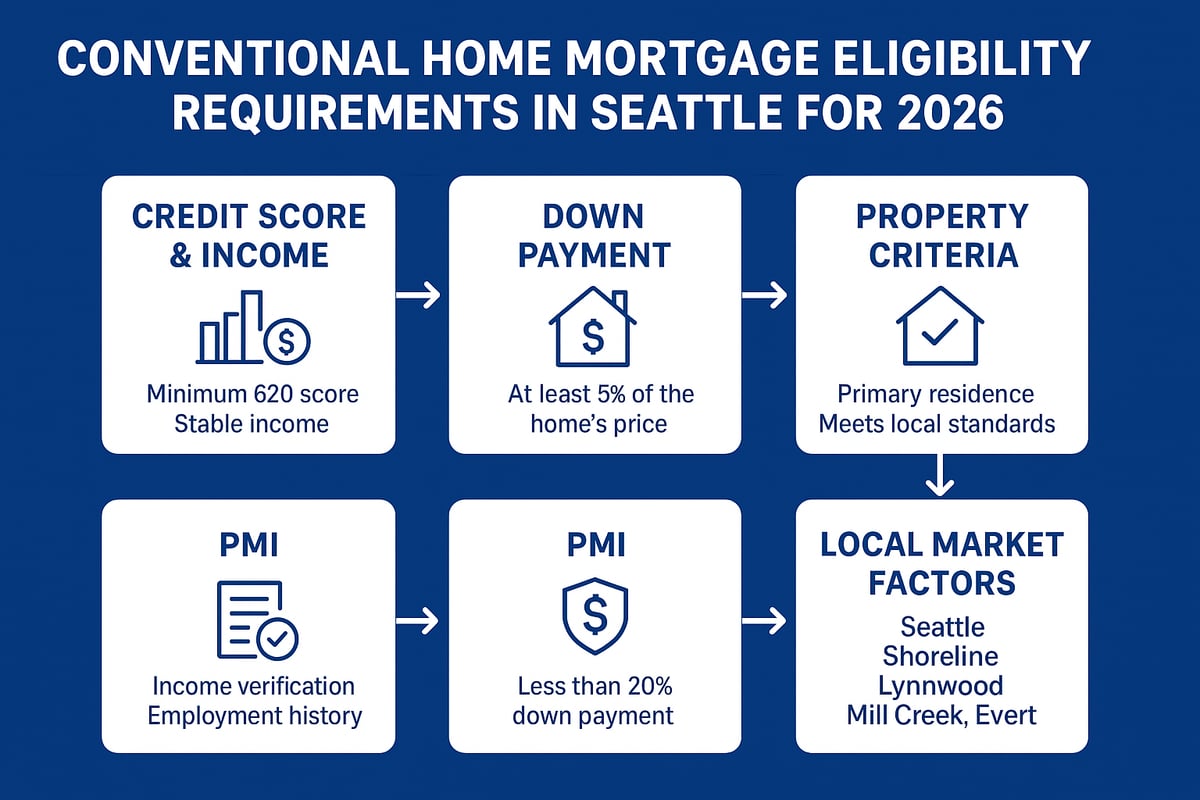

Conventional Loan Eligibility & Requirements in Seattle

Understanding the eligibility requirements for a conventional home mortgage is essential for Seattle buyers navigating the competitive 2026 market. Lenders have clear guidelines for credit, income, down payment, property type, and documentation. Here’s what you need to know to get approved for a conventional home mortgage in Seattle, Bellevue, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett.

Credit Score and Income Standards

Qualifying for a conventional home mortgage in Seattle starts with your credit and income profile. Most lenders require a minimum credit score of 620, though higher scores often lead to better rates and terms. For tech professionals in Seattle, Bellevue, Shoreline, or Lynnwood, complex income like RSUs or bonuses can be counted, but Loan Officer knowledge on calculating income and documentation needed is crucial.

Debt-to-income (DTI) ratio is another key metric. Most lenders look for a DTI under 45 percent, though some may allow up to 50 percent with strong compensating factors. Stable employment and consistent income are vital for approval. If you’re a tech worker in Seattle or Bellevue with variable pay, be prepared to provide extra documentation to provide two-year average and future projected income.

Down Payment Requirements

The down payment for a conventional home mortgage can range from 3 percent to 5 percent for conforming loans, making homeownership more accessible for first-time buyers in Seattle and Mill Creek. Jumbo loans, often needed in high-priced markets like Seattle and Bellevue, typically require at least 10 percent down.

A larger down payment can improve your approval odds and may lead to a lower interest rate. Down payment funds can come from savings, gifts, or local assistance programs. If you’re considering a low down payment, learn more about 5 Percent Down Conventional Loans to see if this flexible option fits your goals. Always check lender guidelines for acceptable sources to avoid surprises during underwriting.

Property and Occupancy Criteria

For a conventional home mortgage in Seattle, the property must meet specific guidelines. Eligible property types include single-family homes, condos, and multi-unit properties (up to four units). Each type has unique underwriting rules, especially condos in Shoreline or downtown Seattle, where HOA reviews are common.

Documentation Needed for Approval

Lenders require thorough documentation to approve a conventional home mortgage. Standard paperwork includes recent W-2s, pay stubs, bank statements, and two years of tax returns. For self-employed buyers or tech professionals in Seattle, lenders may ask for additional documents, such as profit and loss statements or detailed breakdowns of stock compensation.

The underwriting process reviews all documents for accuracy and consistency. Missing or incomplete paperwork can slow approval, so gather all materials before applying. Being proactive is especially important in competitive markets like Seattle, Bellevue or King County, where speed to close can impact your offer being accepted.

Private Mortgage Insurance (PMI)

If your down payment on a conventional home mortgage is less than 20 percent, you’ll likely need private mortgage insurance (PMI). PMI protects the lender if you default but adds to your monthly cost. In Seattle, PMI rates typically range from .12 percent to .42 percent of the loan amount annually, depending on credit and loan amount.

The good news: PMI isn’t permanent. Once your equity reaches 20 to 22 percent through payments or home appreciation, you can request removal. In fast-growing areas like Seattle and King County, rising property values may help you eliminate PMI sooner. Always ask your lender about their PMI removal process and timelines.

Local Considerations for Seattle, Lynnwood, Mill Creek, Everett

Seattle’s housing market continues to evolve, and so do eligibility standards for a conventional home mortgage. High property values mean conforming loan limits are higher here than in many parts of Washington. In 2026, buyers in Seattle, Lynnwood, and Mill Creek may encounter different loan limit thresholds, impacting whether their loan is conforming or jumbo.

Competition is fierce in places like Seattle, Bellevue and King County, so being fully prepared improves your chances of success. First-time buyers often benefit from local down payment assistance, while investors in need to meet stricter criteria. Always consult with a local expert to tailor your strategy for the city and property type you’re targeting.

The Step-by-Step Process: How to Get a Conventional Home Mortgage in Seattle

Navigating the Seattle housing market in 2026 requires a clear understanding of the conventional home mortgage process. Here is a practical roadmap to securing your new home with confidence.

Step 1: Assess Your Financial Readiness

Start your journey by reviewing your finances. Check your credit score, evaluate your debt-to-income ratio, and tally your available savings. Understanding your budget will help you determine how much you can afford in Seattle or nearby cities like Lynnwood and Mill Creek.

Use local mortgage calculators to estimate payments for your target area. Consider your desired down payment—typically 3% to 5% for a conforming conventional home mortgage or 10% and up for jumbo loans. If you are unsure which down payment is right for you, review this Conventional Loan Down Payment Comparison to see how different options affect your approval and monthly costs.

Organize your finances early to build a strong foundation for the rest of the conventional home mortgage process.

Step 2: Get Pre-Approved

Pre-approval is essential in Seattle’s competitive real estate scene. Work with a local lender or mortgage broker who understands the nuances of the Seattle, Everett, and Shoreline markets. Pre-approval means a lender reviews your credit, income, employment, and assets to issue a letter showing sellers you are a serious buyer.

A pre-approval for a conventional home mortgage strengthens your offer, especially in multiple-offer situations common in most of King County. It can also highlight any potential issues with your application, giving you time to address them before making an offer and ensuring peace of mind for a successful closing.

Stay organized with your financial documents, as lenders will require them during this stage.

Step 3: Shop for Your Home

Now it is time to search for your ideal property. Work with a knowledgeable real estate agent experienced in Seattle, Lake Forest Park, and the surrounding cities. Your pre-approval for a conventional home mortgage helps you and your agent focus on homes within your budget and loan limits.

In Seattle, bidding wars and fast-moving listings are common. Be prepared to act quickly and consider making strong, clean offers. Your agent can help you navigate local trends. Speed to close, advanced underwriting can strengthen your offer to stand out to a seller.

Keep your lender updated on your search so they can adjust your pre-approval if your criteria change.

Step 5: Processing and Underwriting

Next your loan is submitted, your lender’s processing and underwriting teams review every detail. They verify your financials, employment, and property information to confirm you meet the guidelines for a conventional home mortgage.

In Seattle’s fast-paced market, the underwriting stage can reveal issues such as credit discrepancies or missing documentation. Respond to underwriter requests quickly to avoid delays, especially in competitive neighborhoods.

Your mortgage broker can help clarify any questions and guide you through additional requirements, ensuring your file stays on track for approval.

Step 6: Appraisal and Home Inspection

Every conventional home mortgage requires a property appraisal to confirm the home’s value supports the loan amount. In Seattle, Shoreline, and Everett, rapid price changes can sometimes lead to appraisal gaps. Your lender will order the appraisal, and you will get a report detailing the property’s market value.

Schedule a home inspection separately to uncover any hidden issues. Inspections are especially important for older homes in Lake Forest Park and Everett, where deferred maintenance can be a concern. Addressing problems early can save you money and stress later.

Both appraisal and inspection are critical for protecting your investment.

Step 7: Closing the Loan

You are almost home. The closing process for a conventional home mortgage in Seattle involves reviewing the closing disclosure, and signing documents. In Washington State, a neutral escrow company handles the paperwork and funds.

Expect to pay closing costs, which may include lender fees, title insurance, and escrow charges. Once your loan is funded and recorded, you will receive your keys. In cities like Seattle and Bellevue, closing timelines can be as short as nine business days if everything is in order.

Celebrate your successful journey to homeownership.

Local Mortgage Broker Support in Seattle

Working with a Seattle-based mortgage broker can make all the difference. Local experts understand the unique challenges of the conventional home mortgage process.

A good broker can help you navigate complex income situations, recommend the best loan products, and expedite approvals for tech professionals and families. Their local knowledge helps you stand out in a competitive market and ensures a smooth, personalized experience from start to finish.

Leverage local expertise for the best possible results on your home purchase.

Conventional Mortgage Rates & Costs in Seattle: 2026 Outlook

Understanding the cost of a conventional home mortgage is essential for Seattle-area buyers planning their 2026 purchase. As a local mortgage broker, I see how rates, fees, and market trends shape affordability in Seattle, Shoreline, Lynnwood, Mill Creek, and Everett. Please allow me to break down how rates are determined, what to expect for costs, and how to compare your options for the best outcome.

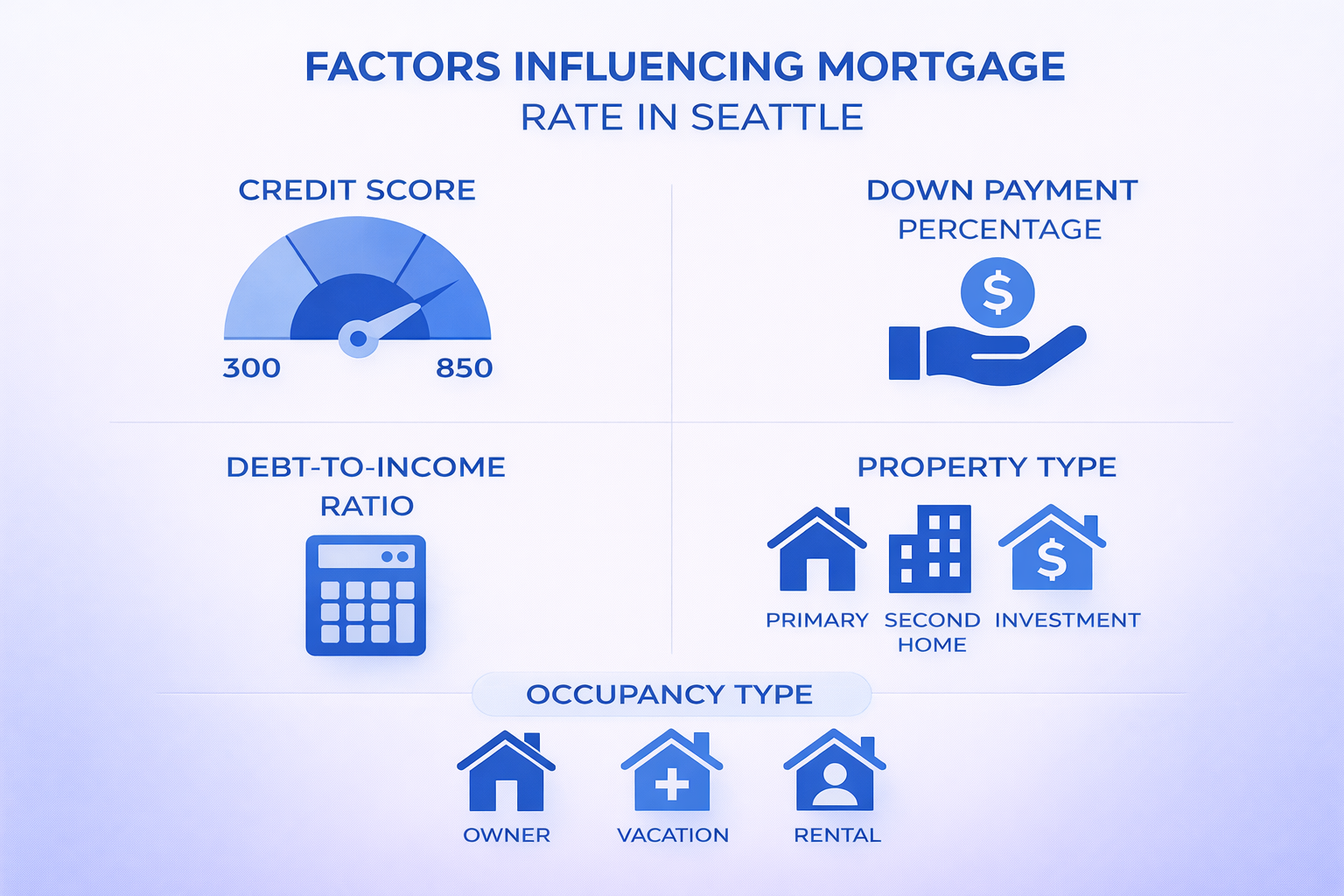

How Interest Rates Are Set

Several factors influence the interest rate you receive on a conventional home mortgage in Seattle. Your credit score remains one of the biggest drivers, with higher scores earning lower rates. Lenders also examine your down payment, loan amount, and the type of property you are buying.

Market conditions matter, too. The Federal Reserve’s monetary policy and broader economic trends can move mortgage rates up or down. In 2026, Seattle’s robust real estate activity and steady demand will keep lenders attentive to local market shifts.

If you are considering a condo versus a single-family home, expect minor rate differences depending on property type and occupancy. Always review your full financial profile with your lender to understand how it impacts your rate.

Current Rate Ranges for 2026

For 2026, the projected average interest rate for a 30-year fixed conventional home mortgage in Seattle is expected to hover between 5.75% and 6.25%. Adjustable-rate mortgages (ARMs) may start slightly lower, often in the 5.00% to 5.50% range, though they can adjust after the initial period.

Conforming loans, which meet local loan limits, usually offer better rates than jumbo loans. In high-cost areas like Seattle and Shoreline, jumbos—loans above the conforming limit—carry rates about 0.00% to 0.25% higher. For the latest projections and detailed rate trends, review the Seattle Mortgage Rate Trends and Forecast 2026.

Closing Costs and Fees

When finalizing your conventional home mortgage in Seattle, plan for closing costs typically range 2% or less of the purchase price. These cover lender fees, title insurance, escrow services, appraisals, and recording charges.

To manage these costs, ask your lender for a Loan Estimate early in the process. Compare estimates from different providers, and explore options to roll certain fees into your loan amount if needed.

Comparing Lenders and Rate Lock Strategies

Shopping for your conventional home mortgage means comparing both rates and fees among Seattle-area lenders. Direct lenders, credit unions, and mortgage brokers each offer unique advantages. Brokers often provide access to multiple lenders, which is valuable for buyers in competitive markets.

When you find a rate you like, consider locking it in. Rate locks typically last 15 to 45 days. In a volatile market, locking early can protect you from sudden increases. However, if rates are trending down, a shorter lock could save money.

Ask about rate lock policies, expiration dates, and any fees for extensions. This is especially important if your purchase might involve a longer closing timeline due to appraisal or inspection contingencies.

Example Mortgage Scenarios

To put costs in perspective, here are two sample scenarios for Seattle-area buyers using a conventional home mortgage:

| Scenario | Home Price | Loan Type | Down Payment | Rate (est.) | Monthly Payment* |

|---|---|---|---|---|---|

| Seattle, Conforming Loan | $850,000 | 30-yr Fixed | 20% ($170K) | 6.00% | $4,076 |

| Seattle, Jumbo Loan | $1,500,000 | 30-yr Fixed | 20% ($300K) | 6.125% | $7,291 |

*Monthly payment includes principal and interest only. Taxes, insurance, and PMI (if required) are extra. No specific program was used, for example only.

A higher credit score or larger down payment can reduce your interest rate and monthly cost. Always calculate total costs, not just the rate, when choosing a mortgage.

Pros and Cons of Conventional Mortgages for Seattle Homebuyers

Seattle’s real estate market is dynamic, and understanding the pros and cons of a conventional home mortgage is essential for buyers in neighborhoods like Shoreline, Lynnwood, and Everett. Let’s break down the key advantages, potential drawbacks, comparisons, and ideal borrower profiles for 2026.

Advantages of Conventional Loans

A conventional home mortgage offers several benefits for Seattle-area buyers seeking flexibility and long-term value. Qualified borrowers with strong credit and stable income often secure lower overall costs compared to government-backed loans. There are no upfront mortgage insurance fees, and monthly private mortgage insurance (PMI) can be removed once you reach 20 percent equity, reducing payments over time.

Conventional home mortgage options are also versatile. Buyers can use them for primary residences, vacation homes, or investment properties, which is especially attractive for investors. For more details on using these loans for rental properties, visit this guide on Conventional Loan for Investment Property.

Additionally, these loans accommodate various property types, including single-family homes, condos in downtown Seattle, and multi-units.

Potential Drawbacks and Risks

While a conventional home mortgage can be cost-effective, it comes with stricter approval standards. Lenders require higher credit scores, typically 620 or above, and a lower debt-to-income ratio. This can create challenges for self-employed tech professionals in Seattle or those with variable income from RSUs and bonuses.

Buyers with less than 20 percent down must pay PMI, which adds to monthly costs. In high-priced markets like Seattle, conforming loan limits may not cover all homes, forcing some buyers to seek jumbo loans with even more rigorous requirements.

If your finances are complex or your credit history is limited, you may face higher interest rates or even loan denial. Always assess your readiness before applying.

Comparing Conventional to FHA, VA, and Other Options

Choosing between a conventional home mortgage and government-backed options depends on your profile and goals. Conventional loans usually offer lower overall costs for those with strong credit, while FHA loans are more forgiving of lower scores and smaller down payments. VA loans, available to veterans, often have no down payment or PMI, making them ideal for eligible buyers.

| Feature | Conventional | FHA | VA |

|---|---|---|---|

| Credit Score | 620+ | 580+ | Varies |

| Down Payment | 3%–20% | 3.5% | 0% |

| PMI/MIP | PMI <20% | MIP | None |

| Property Flexibility | High | Medium | Medium |

In Seattle, FHA loans may be preferred for first-time buyers with limited savings, while VA loans are a top choice for military families buying closed to where they are stationed.

Who Should (and Shouldn’t) Choose Conventional

A conventional home mortgage is ideal for Seattle buyers with good credit, stable income, and the ability to put down at least 3–5 percent. Move-up buyers in Shoreline or investors in Everett benefit from flexible property options and the ability to remove PMI. Tech professionals with straightforward income will find approval smoother.

However, buyers with lower credit, minimal down payment, or complex finances should consider FHA or VA loans. For example, first-time buyers with limited savings may find FHA requirements easier to meet, while veterans can leverage VA benefits with no down payment.

Evaluate your financial profile, long-term goals, and property needs to determine if a conventional loan is your best path to homeownership.

Local Insights: Navigating the Seattle-Area Mortgage Market

Seattle’s real estate landscape is as diverse as the communities it covers. Whether you are buying in bustling Seattle or the quieter suburbs like Shoreline, Lynnwood, Mill Creek, or Everett, understanding the local context is crucial for any successful conventional home mortgage journey.

Unique Challenges in Seattle, Shoreline, Lynnwood, Mill Creek, Everett

Navigating a conventional home mortgage in the Seattle region means facing several unique hurdles. Home prices in Seattle and surrounding cities often exceed national averages, which can push buyers into jumbo loan territory. For 2026, Seattle’s 2026 Conforming Loan Limits have increased, reflecting rising property values, but many homes in neighborhoods like Mill Creek or Shoreline still challenge these thresholds.

Multiple-offer situations are common where demand remains high. Appraisal gaps can also arise if bidding wars push offer prices above appraised values. Fast-moving market conditions require buyers to act decisively and have their conventional home mortgage financing in order.

Local nuances, such as varying property types and competition levels, mean that homebuyers must be well-prepared and flexible. Understanding these challenges is the first step to a successful purchase.

Strategies for Winning in a Competitive Market

To secure a conventional home mortgage in Seattle’s tight housing market, buyers must be proactive. Strengthening your pre-approval is essential, showing sellers that you are a serious contender. Working with a local lender who understands Seattle’s pace can make your offer stand out.

Consider these strategies:

- Get fully underwritten before shopping.

- Be ready to waive contingencies, but weigh risks carefully.

- Offer a larger earnest money deposit for added credibility.

- Move quickly on new listings.

- Speed to close in 10 business days or less.

- Partner with a real estate agent who specializes in your target area.

These tactics, combined with a solid conventional home mortgage plan, increase your chances of winning in a multiple-offer scenario. Preparation and local expertise are your best assets.

Down Payment Assistance & Local Programs

Even with rising home prices, down payment assistance programs can make a conventional home mortgage more accessible for buyers. Washington State offers several options, including the Home Advantage and House Key Opportunity programs, which provide grants or forgivable loans for qualified applicants.

Initiatives to help first-time buyers bridge the affordability gap. These programs often come with income limits, homebuyer education requirements, and property price caps, so it’s important to review eligibility details early.

By utilizing these resources, buyers can reduce their upfront costs and improve their chances of qualifying for a conventional home mortgage. Consult with your lender or broker to identify the best-fit program for your situation.

Special Considerations for Tech Professionals

Seattle’s booming tech sector brings unique mortgage challenges and opportunities. Many buyers from companies like Amazon, Microsoft, and Google receive compensation through RSUs, bonuses, or stock options. Properly documenting and qualifying this income is crucial for a conventional home mortgage.

Lenders evaluate tech income differently, requiring a history of payouts or vesting schedules to count RSUs as qualifying income. Self-employed tech consultants or those with variable bonuses may need additional documentation, such as multiple years of tax returns and letters from employers.

If you are a tech professional in Seattle, working with a lender experienced in complex compensation packages is essential. This ensures your full income is considered when securing a conventional or jumbo home mortgage.

Working with a Trusted Seattle Mortgage Broker

A knowledgeable mortgage broker is invaluable for navigating the Seattle-area real estate market. Local brokers understand the nuances of each community, from Everett’s investment opportunities to Mill Creek’s family neighborhoods. They can guide you through the conventional home mortgage process, help with paperwork, and advocate for your interests during negotiations.

Key advantages of partnering with a Seattle mortgage broker include:

- Fast, accurate pre-approvals tailored to local market demands

- Access to a wide range of lenders and loan products

- Personalized advice for tech professionals and first-time buyers

- Strategic planning to support your offer

- Speed to close in 10 business days or less

Ultimately, a trusted expert helps you secure the right conventional home mortgage for your needs and ensures your experience is smooth from start to finish.

Frequently Asked Questions (FAQ) About Conventional Home Mortgages in Seattle

Navigating the Seattle-area real estate market in 2026 means understanding every detail of the conventional home mortgage process. Below, I answer the most common questions I receive from buyers in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. These insights will help you approach your next purchase with confidence.

What credit score do I need for a conventional mortgage in Seattle?

Most Seattle lenders require a minimum credit score of 620 for a conventional home mortgage, but stronger scores (740+) can help you secure better rates. If your income includes RSUs or bonuses—a common scenario for tech professionals in Seattle and Lynnwood—lenders may review your credit profile more closely. For updated eligibility details, see Conventional Loan Requirements for 2026.

What is the minimum down payment for a conventional loan in Washington State?

The minimum down payment for a conventional home mortgage is typically 3 percent for first-time buyers and 5 percent for repeat buyers. Jumbo loans, often needed in high-priced areas, usually require at least 10 percent down. Using a larger down payment can lower your interest rate and closing costs. Down payment assistance programs are available for qualifying buyers.

How does PMI work and how can I remove it?

Private mortgage insurance (PMI) is required on most conventional home mortgage loans when your down payment is less than 20 percent. In Seattle, monthly PMI costs vary based on your credit and loan size, but typically range from 0.3 percent to 1.5 percent of the loan amount. Once your loan balance reaches 78 percent of the home’s original value, lenders will automatically remove PMI. You can request early removal by refinancing or providing proof of increased home value.

Are there special programs for first-time buyers in Seattle?

Yes, several local and state programs support first-time buyers using a conventional home mortgage in Seattle, Lynnwood, and Everett. These include down payment assistance, reduced PMI options, and homebuyer education courses. Eligibility often depends on income, credit, and property location. Working with a knowledgeable mortgage broker ensures you access the best resources for your situation.

How do I qualify for a jumbo conventional loan in King/Snohomish County?

To qualify for a jumbo conventional home mortgage in King or Snohomish County, you typically need a higher credit score (700+), a larger down payment, and strong income documentation. Seattle’s loan limits increased for 2026, so some high-value homes may still fit within conforming guidelines. For the latest limits and how they impact your buying power, review Seattle’s Loan Limits Increased For 2026.

What are typical closing costs for Seattle-area homebuyers?

Closing costs for a conventional home mortgage usually range 2 percent of the purchase price. These include lender fees, title insurance, escrow, appraisal, and recording charges. For an $800,000 home in Everett, expect total closing costs around $11,000 to $15,000. Comparing lender estimates and negotiating fees can help you manage these expenses.

You’ve just explored the ins and outs of conventional home mortgages in Seattle, from understanding local loan options to navigating unique challenges for tech professionals. If you’re feeling more confident about your next steps or still have questions about your specific situation, I’m here to help you make sense of it all. Let’s take the conversation further—I’ll walk you through your options, answer all your questions, and help you craft a tailored strategy for your home goals. Ready to get started or just want to explore what’s possible? Let’s have a conversation

Key Takeaways

- The Seattle Conventional Home Mortgage Guide helps buyers navigate financing options and understand the application process for 2026.

- Conventional home mortgages are not government-insured and include fixed-rate and adjustable-rate options for various buyer needs.

- Eligibility requires good credit, stable income, and down payments ranging from 3% to 10%, depending on the loan type.

- Key trends for 2026 include rising conforming loan limits and unique challenges in Seattle’s competitive housing market.

- Potential buyers should utilize local down payment assistance programs and consult trusted mortgage brokers for tailored advice.

Estimated reading time: 22 minutes