Navigating Seattle’s fast-paced real estate market in 2026 takes more than timing. To succeed, you need a mortgage and financial advisor who understands local trends, lending rules, and your unique goals.

This guide gives Seattle-area buyers, homeowners, and investors a clear plan. You’ll discover evolving mortgage trends, financial advisor strategies, step-by-step home loan processes, and Seattle-specific data for Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

Seattle’s market is competitive, but with the right guidance, you can move forward with confidence. Ready to take the next step? Use this 2026 roadmap to make smart, informed decisions.

Understanding the 2026 Mortgage & Financial Landscape in Seattle

Navigating the 2026 real estate market in Seattle and its surrounding cities demands a proactive approach and reliable information. As a seasoned mortgage and financial advisor serving the region, I know firsthand how quickly market conditions can shift. Whether you are planning to buy, refinance, or invest, understanding the unique financial landscape in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett is essential for making informed decisions.

Seattle-Area Market Projections for 2026

The outlook for Seattle’s housing market in 2026 remains dynamic, shaped by both local and national forces. Median home prices are projected to rise moderately, with Seattle expected to see values approach $950,000, while Lynnwood, Everett, and Mill Creek trend closer to $700,000. In Shoreline and Lake Forest Park, competitive demand and limited new construction are likely to keep prices elevated. According to the Seattle housing market forecast 2025-2026, buyers should expect moderate appreciation and a slight increase in inventory compared to the previous year. As a mortgage and financial advisor, I recommend monitoring these forecasts closely, as city-by-city differences can impact your strategy.

Interest Rates, Inflation, and Affordability

Interest rates in 2026 are forecasted to stabilize, with 30-year fixed rates hovering between 5.5% and 6.25% in the Seattle metro area. Inflation is expected to remain moderate, but even small rate changes can influence monthly payments and overall affordability. For example, a 0.5% shift in rates could affect your buying power by tens of thousands of dollars. A mortgage and financial advisor can help you model different scenarios, ensuring you secure the most favorable terms possible.

Housing Inventory: New Construction and Demand

King and Snohomish counties are seeing a slow but steady rise in new construction, especially in Mill Creek and Lynnwood. However, resale inventory remains tight, particularly for entry-level homes. In Lake Forest Park and Shoreline, low listing volumes and high demand mean homes often sell within 10 to 14 days. Everett is experiencing increased multifamily development, creating more options for first-time buyers and investors. Staying updated on local inventory trends allows a mortgage and financial advisor to advise clients on timing and offer strategies that work in fast-moving markets.

Regulatory Changes and Lending Standards

Lending regulations in 2026 may introduce stricter credit score requirements and higher minimum down payments for some loan products. Fannie Mae and Freddie Mac are anticipated to adjust guidelines for self-employed borrowers and those using alternative income, such as RSUs or bonuses—a common scenario for tech professionals in Seattle and Redmond. Understanding these regulatory shifts is vital, and a mortgage and financial advisor ensures you are prepared for new documentation or qualification standards before you apply.

Local Expertise: Navigating Micro-Market Differences

Each Seattle-area city has its own unique dynamics. For example, Mill Creek’s surge in new construction offers opportunities for buyers able to move quickly when rates dip. In early 2026, one of my clients in Mill Creek leveraged a brief drop in interest rates to lock in a favorable mortgage and secure a property before prices climbed further. This illustrates why working with a local mortgage and financial advisor who tracks hyper-local shifts can give you a decisive edge.

Market Data at a Glance

| City | Median Price (2026) | Avg. Days on Market | Projected Rate Range |

|---|---|---|---|

| Seattle | $950,000 | 12 | 5.50% – 6.25% |

| Shoreline | $800,000 | 13 | 5.50% – 6.25% |

| Lynnwood | $700,000 | 15 | 5.625% – 6.375% |

| Lake Forest Park | $850,000 | 11 | 5.50% – 6.25% |

| Mill Creek | $720,000 | 14 | 5.625% – 6.375% |

| Everett | $650,000 | 16 | 5.75% – 6.49% |

As your trusted mortgage and financial advisor, my advice is to stay informed, seek local expertise, and be ready to act when market windows open. Seattle’s real estate landscape in 2026 will reward those who plan ahead and leverage hyper-local insights for confident, successful outcomes.

Step-by-Step Mortgage Planning for Seattle Buyers and Homeowners

Navigating the Seattle-area housing market in 2026 requires a clear, structured approach. Whether you are a first-time buyer in Everett, a homeowner in Lynnwood, or an investor in Mill Creek, a comprehensive mortgage and financial advisor plan is essential. In this section, I will guide you through each critical step, ensuring you have the tools and insights needed for a confident home loan journey.

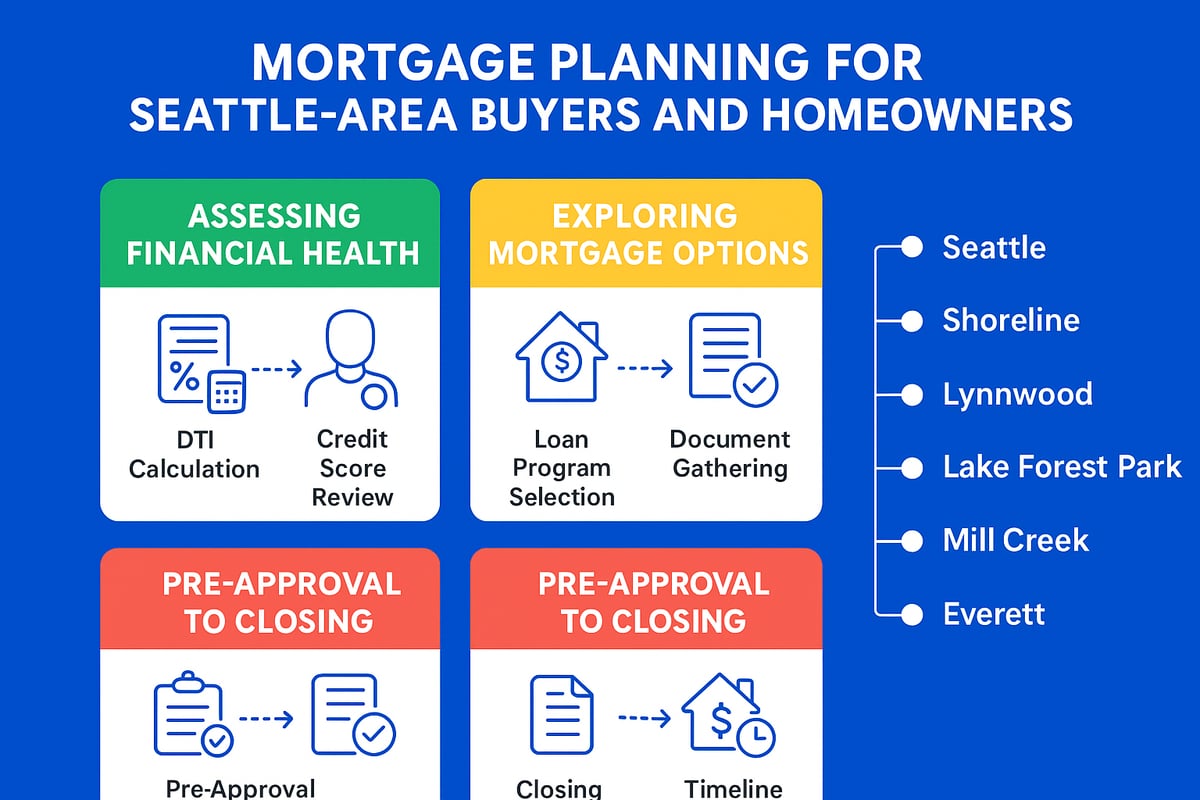

Assessing Your Financial Health

The first step in your mortgage and financial advisor plan is a thorough review of your financial foundation. Lenders in Seattle, Shoreline, and surrounding areas will closely evaluate your debt-to-income (DTI) ratio, which compares your total monthly debts to your gross monthly income. A lower DTI increases your chances of qualifying for favorable loan terms.

Equally important is your credit score. Review your credit reports for errors and work proactively to boost your score. For instance, an Everett buyer recently improved their FICO score by 40 points, unlocking a significantly lower interest rate and better loan options. If you want detailed steps, refer to Improving your credit score for a mortgage for actionable advice.

Budgeting is essential. Prepare for your down payment, closing costs, and reserve requirements. Here is a quick look at minimum requirements for popular loan types in our region:

| Loan Type | Min. Credit Score | Max DTI | Down Payment |

|---|---|---|---|

| Conventional | 620 | 50% | 3%+ |

| FHA | 580 | 50% | 3.5%+ |

| VA | 620 | 50% | 0% |

A mortgage and financial advisor can help you interpret these numbers and craft a strategy that fits your goals in Lake Forest Park or Mill Creek.

Exploring the Right Mortgage Options

Choosing the right loan product is crucial in a fast-paced Seattle market. Your mortgage and financial advisor will help you compare fixed-rate and adjustable-rate mortgages (ARMs). Fixed-rate loans offer stability, while ARMs can provide early savings if you plan to move or refinance soon.

Explore all available programs. In King and Snohomish counties, buyers often consider:

- Conventional loans for standard purchases

- FHA loans for flexible credit and lower down payments

- VA loans for eligible veterans

- Jumbo loans for high-value properties in Bellevue or Kirkland

- First-time buyer programs with local assistance

For buyers with complex income, like RSUs, bonuses, or self-employment, documentation is key. A tech professional in Redmond recently used RSUs to maximize their buying power and secure a competitive home in Lynnwood.

2026 loan limits for King and Snohomish counties are expected to reflect rising home prices, so your mortgage and financial advisor will ensure your financing aligns with these thresholds. Together, you will find the best fit for your needs, whether you are eyeing new construction in Mill Creek or a classic home in Shoreline.

Navigating Pre-Approval to Closing

Once you have assessed your finances and selected a loan, your mortgage and financial advisor will guide you from pre-approval to closing. Start by gathering essential documents: pay stubs, W-2s, tax returns, and asset statements. In Seattle and Everett, local lenders often provide faster response times and more personalized service than national banks, giving you an edge in competitive offer situations.

When shopping for homes, move quickly. In Lake Forest Park, properties can go pending in just days. Your advisor will help you understand the appraisal, inspection, and contingency process, protecting your interests at every step.

Here is a typical timeline for the Seattle region:

- Pre-approval: 1-3 days

- Home search and offer: 7-21 days

- Underwriting and closing: 9-30 days

A recent Shoreline buyer benefited from fast-track underwriting, beating multiple offers and closing on their dream home. By following a step-by-step plan with your mortgage and financial advisor, you can confidently navigate the process in any Seattle-area city.

Financial Advisor Strategies for Building Wealth Through Real Estate

Building wealth through real estate in Seattle and the surrounding areas requires a clear partnership between your mortgage and financial advisor. In 2026, local market dynamics in places like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett create both unique opportunities and challenges. A well-structured strategy, grounded in expert guidance, can help you maximize returns, protect assets, and align property decisions with your long-term goals.

Setting Short- and Long-Term Financial Goals

Every successful real estate journey in Seattle starts with intentional goal setting. A mortgage and financial advisor helps you define objectives that fit your life stage, such as buying a first home, upgrading, or investing for retirement.

Begin by clarifying your timeline. Are you looking for a home to raise a family in Mill Creek, or do you want to build a rental portfolio in Everett? Identify how real estate fits into broader financial plans like retirement savings or funding education.

For example, a Lynnwood homeowner may use equity from their primary residence to purchase a rental property, boosting passive income while leveraging appreciation. Your mortgage and financial advisor will evaluate your debt-to-income ratio, liquidity, and risk tolerance to ensure your property decisions are sustainable.

Establishing clear, measurable goals makes it easier to track progress and make timely adjustments as the Seattle market evolves.

Diversifying with Real Estate Investments

Diversification is key to building lasting wealth. Your mortgage and financial advisor can guide you through various real estate investment types available across Seattle, Shoreline, and other nearby cities.

Options include:

- Single-family homes, which offer stability and steady appreciation in neighborhoods like Lake Forest Park.

- Multifamily properties, providing multiple income streams, popular in Everett and Lynnwood.

- Short-term rentals, ideal for high-demand areas with tourism or tech sector growth.

Each investment type has unique pros and cons. Seattle often has higher entry costs but offers strong appreciation and robust rental demand. Surrounding cities like Mill Creek may provide better rental yields and lower upfront expenses.

Tax advantages, such as mortgage interest deductions and 1031 exchanges, can significantly impact your returns. A mortgage and financial advisor will help you compare local appreciation rates and rental yields, ensuring your portfolio is balanced and resilient.

For deeper insights on structuring investment financing, consider reviewing Seattle mortgage financing strategies to explore creative approaches tailored to today’s market.

A tech professional in Redmond, for example, may use stock compensation and RSUs to qualify for a larger loan, expanding their investment reach. By spreading assets across different property types and locations, you reduce risk and increase the potential for stable, long-term growth.

Risk Management and Asset Protection

Protecting your real estate assets is just as important as acquiring them. A mortgage and financial advisor will recommend a comprehensive risk management plan to preserve your wealth.

Start by securing robust insurance coverage for all properties, including liability and loss-of-rent protection. Consider holding investment properties in an LLC to shield personal assets from potential legal claims.

Estate planning ensures your properties transition smoothly to heirs, while tax planning strategies help minimize liabilities during market downturns. For instance, a Seattle investor with holdings in Everett and Shoreline might diversify across property types and locations, reducing exposure to localized market shifts.

Regular reviews with your mortgage and financial advisor ensure your asset protection strategies remain current. As the Seattle area market changes, proactive adjustments can safeguard your investments and provide peace of mind.

Working with Mortgage and Financial Professionals: What to Expect

Navigating the Seattle real estate market in 2026 means partnering with the right mortgage and financial advisor. In a region as dynamic as Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett, understanding exactly what these professionals do will empower you to make confident decisions.

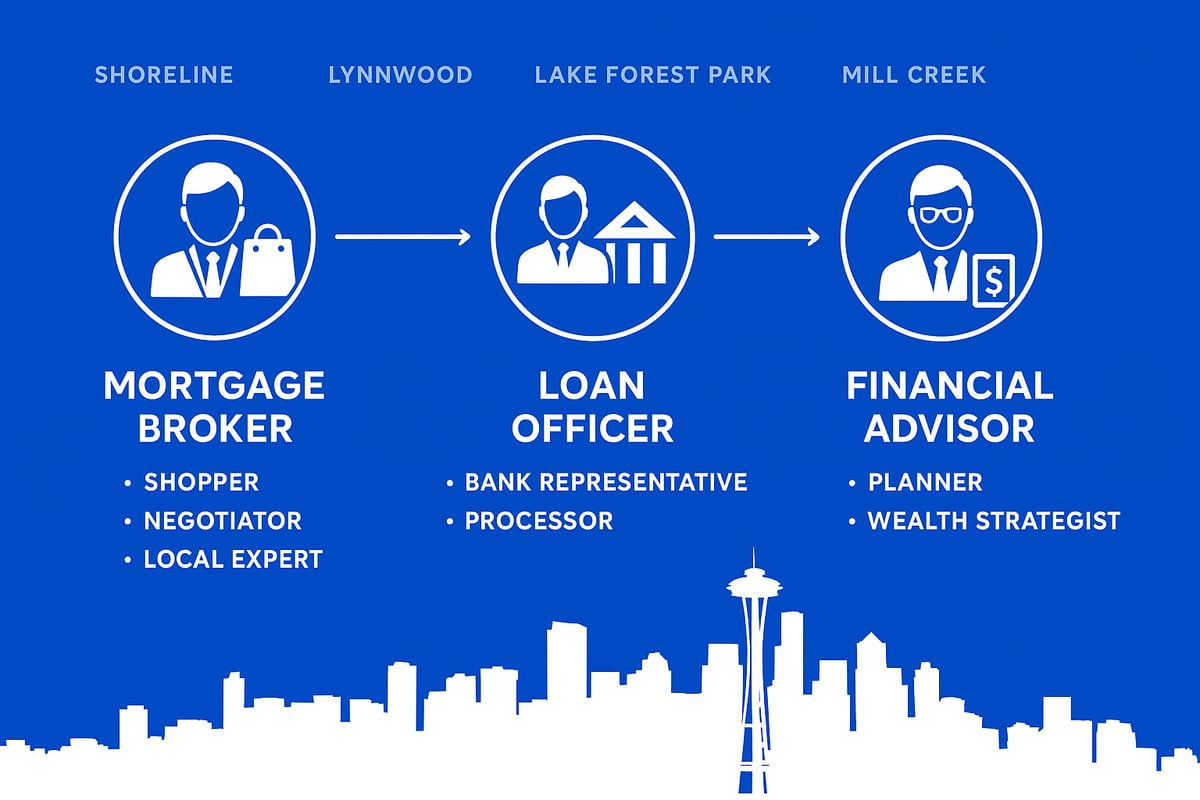

Understanding Roles and Responsibilities

The mortgage and financial advisor landscape includes several key players. Each brings specialized expertise to your home financing journey.

Here’s a comparison of their core functions:

| Professional | What They Do | Who They Represent |

|---|---|---|

| Mortgage Broker | Shops multiple lenders for best mortgage terms, provides guidance tailored to your needs, especially helpful in Seattle’s competitive market | You, the borrower |

| Loan Officer | Works for a specific bank or lender, processes your loan application, may offer limited product options | The bank or lender |

| Financial Advisor | Helps set long-term financial goals, manages assets, and offers strategies for building wealth through real estate | You, the client |

A mortgage and financial advisor can help you navigate everything from loan selection to wealth planning. If you’re unfamiliar with some terms, the Mortgage glossary and key terms resource is invaluable for clarity.

The Value of Local Expertise

Seattle’s market moves quickly, but each surrounding city has unique trends. A local mortgage and financial advisor understands micro-market differences in places like Lynnwood, Mill Creek, and Everett. They can spot opportunities—such as new construction in Mill Creek or a fast-moving resale in Lake Forest Park—that national lenders might overlook.

In Shoreline and Seattle, competitive offers and unique property types are common. Local professionals know how to structure offers and navigate city-specific challenges, giving you a decisive edge.

Choosing Your Mortgage or Financial Partner

Selecting the right mortgage and financial advisor is crucial. Start by asking:

- Are you licensed to work in Washington, and do you specialize in Seattle-area markets?

- How do you get compensated, and are there any upfront fees?

- What loan programs do you have experience with in Lynnwood, Everett, or Shoreline?

- Can you guide me on leveraging RSUs, bonuses, or self-employment income?

- How do you communicate during the process, and how often will I get updates?

A great mortgage and financial advisor will welcome these questions and provide transparent, detailed answers.

Red Flags: What to Avoid

Be cautious if a professional:

- Pushes you toward only one lender or product without explaining alternatives

- Is vague about fees or compensation

- Pressures you to move forward without full documentation

- Lacks experience in Seattle, Lake Forest Park, or nearby cities

Trust your instincts and prioritize education and transparency.

Real Example: Lake Forest Park Success

A Lake Forest Park buyer recently worked with a local mortgage and financial advisor who prioritized education. The advisor explained every step, compared loan options, and made sure the buyer understood all terms. This approach led to a smooth closing and high satisfaction—reflecting the average 4.8-star client ratings for Seattle-area mortgage professionals.

The Importance of Ongoing Communication

Your relationship with a mortgage and financial advisor should not end at closing. Annual financial reviews and clear communication ensure your mortgage and investment strategies keep pace with Seattle’s evolving market.

2026 Mortgage and Financial FAQ for Seattle-Area Homebuyers

Seattle’s real estate market is evolving rapidly. As a seasoned mortgage and financial advisor, I receive countless questions from buyers in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Here are the top questions answered for 2026.

What are the 2026 mortgage rate forecasts for Seattle and nearby cities?

Seattle buyers are keenly focused on interest rates. Projections suggest moderate fluctuations throughout 2026, with some experts predicting a slight decrease as inflation stabilizes. For granular insights, review the Mortgage rate predictions for 2026 to compare averages for Seattle, Shoreline, and Lynnwood. Staying connected with a local mortgage and financial advisor ensures you lock the best rate at the right time.

How do RSUs and stock compensation affect mortgage qualification in the tech sector?

In Seattle, Redmond, and Kirkland, many buyers rely on RSUs or bonuses. Lenders consider RSUs as qualifying income if there’s a two-year history and ongoing vesting. Your mortgage and financial advisor will guide you on documenting this income and strategizing for maximum purchasing power, especially in competitive tech-driven neighborhoods.

What down payment assistance programs are available in King and Snohomish counties?

First-time buyers in Seattle, Everett, and Mill Creek can access state-backed grants, forgivable loans, and low-down-payment options. FHA programs are especially popular. Explore FHA loan options for Seattle buyers to see how they fit your needs. A mortgage and financial advisor can help you layer these programs for the greatest benefit.

How can first-time buyers compete in a low-inventory market?

Low inventory remains a challenge in Lake Forest Park and Lynnwood. To stand out, obtain a strong pre-approval, work with a responsive agent, and consider flexible contingencies. Your mortgage and financial advisor can help you prepare fast-track documentation, giving you an edge in multiple-offer scenarios.

Are there special programs for veterans or self-employed borrowers in Seattle?

Absolutely. VA loans offer zero down for eligible veterans in Seattle and Everett. Self-employed buyers in Mill Creek and Shoreline should prepare two years of tax returns and profit-and-loss statements. A knowledgeable mortgage and financial advisor will tailor your loan strategy, ensuring you meet unique qualification standards.

What are the closing costs and average timelines for homes in Shoreline, Mill Creek, and Everett?

Expect closing costs to range from 2% to 4% of the purchase price, with timelines averaging 30 to 40 days. In fast-moving areas like Shoreline, a mortgage and financial advisor can coordinate fast-track underwriting, helping you meet tight deadlines and avoid costly delays.

How does refinancing work if rates drop after I buy?

If rates decrease after your purchase in Seattle or Lynnwood, refinancing can lower your payment or shorten your loan term. Your mortgage and financial advisor will monitor market trends, advise on timing, and ensure you understand potential costs and benefits before proceeding.

Example: Common pitfalls to avoid during the mortgage process in the Seattle area

Buyers in Everett and Lake Forest Park sometimes overlook credit report errors or underestimate closing costs. Working closely with a local mortgage and financial advisor helps you avoid these missteps. Clear communication, early document review, and proactive planning set you up for a smooth closing.

Local Market Insights: Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett

Navigating Seattle’s property market in 2026 requires more than surface-level research. As a local mortgage and financial advisor, I see daily how nuanced trends shape opportunities across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Each city offers a distinct blend of price growth, inventory, and demand, demanding a tailored approach for buyers and investors.

Seattle continues to set the pace for the region. Median home prices are forecast to approach $980,000, with inventory remaining tight. In Shoreline and Lynnwood, competitive demand has pushed prices to around $770,000 and $710,000, respectively. Lake Forest Park and Mill Creek are seeing increased new construction, which is helping moderate price acceleration. Everett, meanwhile, offers relative affordability, with projected median prices near $640,000, making it a draw for first-time buyers and investors alike.

| City | Median Sale Price (2026) | Average Rent (2BR) | Days on Market |

|---|---|---|---|

| Seattle | $980,000 | $2,650 | 26 |

| Shoreline | $770,000 | $2,350 | 23 |

| Lynnwood | $710,000 | $2,200 | 21 |

| Lake Forest Park | $755,000 | $2,400 | 24 |

| Mill Creek | $780,000 | $2,450 | 22 |

| Everett | $640,000 | $1,950 | 28 |

Buyer demand remains strong across all cities, yet the micro-markets differ. Seattle’s central neighborhoods attract tech professionals seeking short commutes and access to amenities. In Shoreline and Lynnwood, buyers prioritize family-friendly communities and proximity to new light rail stations. Lake Forest Park is valued for its quiet neighborhoods and green spaces, while Mill Creek’s planned developments are drawing both first-time buyers and move-up purchasers. Everett is increasingly popular for investors eyeing higher rental yields and lower entry costs.

For those considering investment, neighborhood selection is crucial. Up-and-coming areas in Lynnwood and Everett offer strong appreciation potential, especially near transit and tech employment centers. Mill Creek’s new construction boom means more choices for buyers, but also rising competition. Investors should pay close attention to local rental rates, as steady demand continues to support healthy yields in these markets.

When comparing cities, property taxes vary, typically ranging from 1.0% to 1.2% of assessed value. School ratings are a major consideration for families, with Lake Forest Park and Mill Creek often ranking highly in district performance. Commute times are another factor. Seattle offers the shortest routes to downtown tech campuses, while Lynnwood and Everett benefit from expanding transit infrastructure, reducing travel time for many buyers.

Local infrastructure projects, such as the Lynnwood Link light rail extension and new parks in Mill Creek, influence both home values and lifestyle. The region’s tech sector employment also plays a pivotal role, as job growth continues to fuel demand for both primary residences and rental properties. For a deeper understanding of how macroeconomic factors, such as interest rates, impact Seattle’s market, see this Federal Reserve interest rate outlook 2026 analysis.

Consider a recent example from Mill Creek: A surge in new townhome developments provided entry points for buyers priced out of Seattle, while investors capitalized on strong rental demand. This shift not only increased affordability for local buyers, but also diversified the pool of property owners.

Ultimately, success in 2026’s competitive landscape requires more than just data. Hyper-local knowledge, paired with the guidance of a mortgage and financial advisor, is the key to making confident, informed decisions. Whether buying, investing, or refinancing, working with a trusted local professional ensures you stay ahead in Seattle’s dynamic market.

As you think about navigating Seattle’s fast-changing real estate landscape in 2026, remember that the right guidance can make all the difference. Whether you’re a first-time homebuyer, a tech professional with complex income, or a seasoned investor, having a trusted partner who understands local trends and offers clear, strategic advice is invaluable. I’m here to help you build confidence, ask the right questions, and create a plan tailored to your goals. If you’re ready to discuss your next steps or want clarity on your options, Let’s have a conversation.

Key Takeaways

- Navigating Seattle’s real estate market in 2026 requires a proactive approach and expert guidance from a mortgage and financial advisor.

- Median home prices are projected to rise, with Seattle nearing $950,000 and various surrounding areas reflecting distinct trends.

- Interest rates are expected to stabilize, but small fluctuations can significantly impact affordability and purchasing power.

- A mortgage and financial advisor helps buyers assess financial health, choose the right loan products, and navigate the mortgage process efficiently.

- Stay informed about local market insights, regulatory shifts, and strategies for building wealth through real estate with the right guidance.

Estimated reading time: 18 minutes