For veterans and active-duty military members in the Greater Seattle area, the VA home loan benefit represents one of the most powerful tools for building wealth through homeownership. Yet many service members struggle to find a va loan mortgage broker who truly understands the nuances of this benefit and can navigate the competitive Seattle housing market. With median home prices in Seattle, Bellevue, and Redmond exceeding $800,000 in 2026, working with a knowledgeable broker who specializes in VA financing can mean the difference between a successful purchase and a missed opportunity. This guide explores how the right mortgage broker can help veterans leverage their earned benefits while competing effectively against conventional and cash buyers.

Understanding the VA Loan Mortgage Broker Advantage

A va loan mortgage broker serves as your dedicated advocate throughout the home financing process, representing your interests across multiple lenders rather than being tied to a single institution. This distinction matters significantly for VA borrowers, especially in markets like Mill Creek and Lynnwood where inventory remains tight and competition stays fierce.

Why Broker Experience with VA Loans Matters

Not all mortgage professionals have equal expertise with VA financing. According to industry analysis of VA loan utilization, many brokers avoid VA loans due to misconceptions about difficulty or profitability. This knowledge gap can cost veterans thousands of dollars and create unnecessary delays.

Key advantages of working with a specialized VA loan mortgage broker include:

- Access to multiple lenders with varying VA program appetites and pricing

- Deep understanding of Certificate of Eligibility requirements and restoration

- Expertise in navigating VA appraisal guidelines and property standards

- Ability to structure deals that compete against conventional and cash offers

- Knowledge of local VA underwriting overlays specific to Washington state

How Brokers Navigate Seattle's Competitive Market

The Seattle metro area presents unique challenges for homebuyers, including rapid price appreciation in neighborhoods from Shoreline to Everett and frequent multiple-offer situations. A skilled va loan mortgage broker understands how to position VA offers competitively.

In 2026, listing agents and sellers have become more educated about VA loan benefits, but misconceptions persist. Your broker should proactively address these concerns by highlighting faster closing timelines (often 9-15 business days with experienced lenders), appraisal waiver options for purchase loans, and the financial strength that zero-down financing provides.

Types of VA Loans Available Through Mortgage Brokers

Understanding the various types of VA loans helps borrowers select the right product for their specific situation. Your va loan mortgage broker should explain all available options and recommend the best fit.

VA Purchase Loans

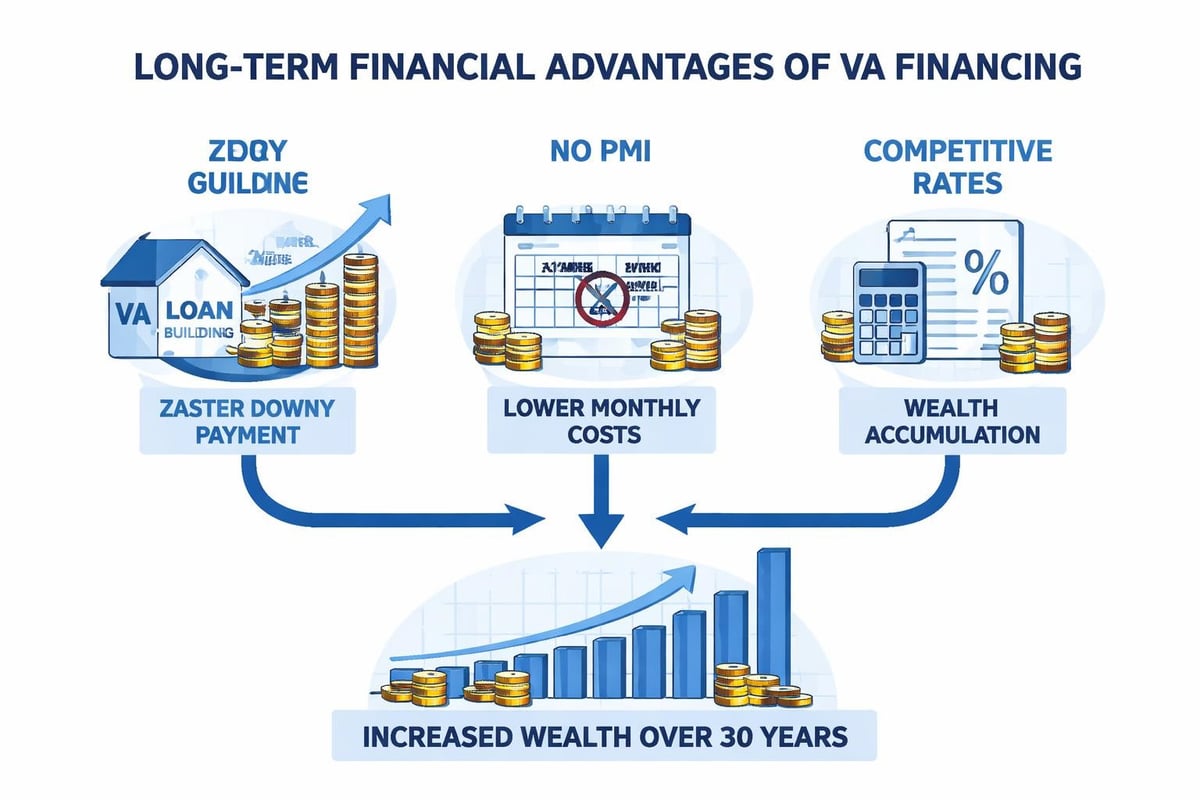

The standard VA purchase loan allows eligible veterans to buy a primary residence with zero down payment up to the conforming loan limit ($806,500 in most Washington counties for 2026, higher in King County). Above this amount, borrowers may need a down payment equal to 25% of the difference between the purchase price and the loan limit.

Key features include:

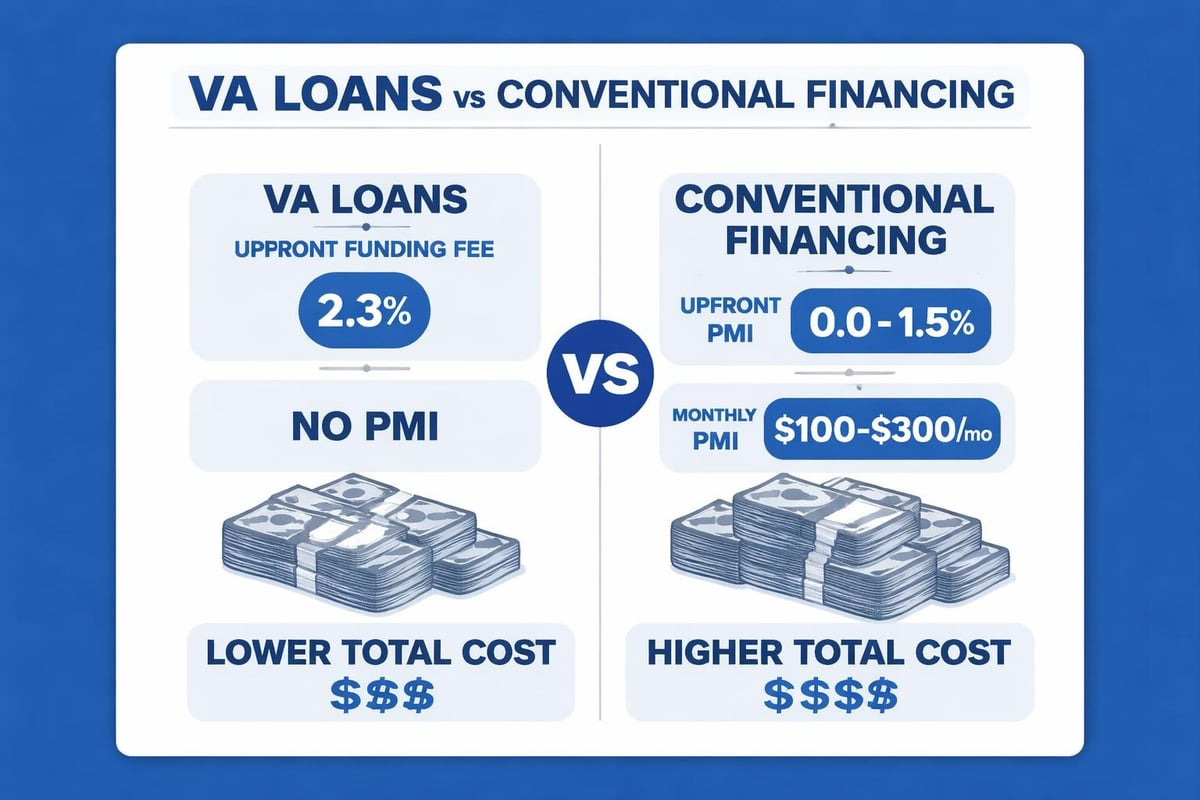

- No private mortgage insurance (PMI) required regardless of down payment

- Competitive interest rates typically lower than conventional loans

- Flexible credit requirements with manual underwriting available

- Seller can contribute up to 4% toward buyer closing costs

- Option to include VA funding fee in the loan amount

VA Cash-Out Refinance

This option allows veterans to tap into their home equity while maintaining VA loan benefits. In appreciating markets like Lake Forest Park and Bellevue, many homeowners have built substantial equity that can be accessed for debt consolidation, home improvements, or investment opportunities.

A va loan mortgage broker can compare the VA cash-out refinance against conventional refinance options to determine which provides the best long-term value based on your equity position, credit profile, and financial goals.

VA Interest Rate Reduction Refinance Loan (IRRRL)

Also called the VA Streamline Refinance, the IRRRL allows current VA loan holders to refinance to a lower rate with minimal documentation. This program requires no appraisal, no income verification, and no credit underwriting in most cases.

| Loan Type | Down Payment | Appraisal Required | Income Documentation | Best For |

|---|---|---|---|---|

| VA Purchase | 0% (up to limit) | Yes | Yes | First-time buyers, move-up buyers |

| VA Cash-Out Refi | None | Yes | Yes | Accessing equity, debt consolidation |

| VA IRRRL | None | No | No | Lowering current VA loan rate |

| VA Jumbo | Varies | Yes | Extensive | High-value Seattle properties |

Qualifying for a VA Loan: What Brokers Evaluate

Your va loan mortgage broker will assess multiple factors to determine your qualification and maximize your approved loan amount. Understanding these criteria helps you prepare for a smooth application process.

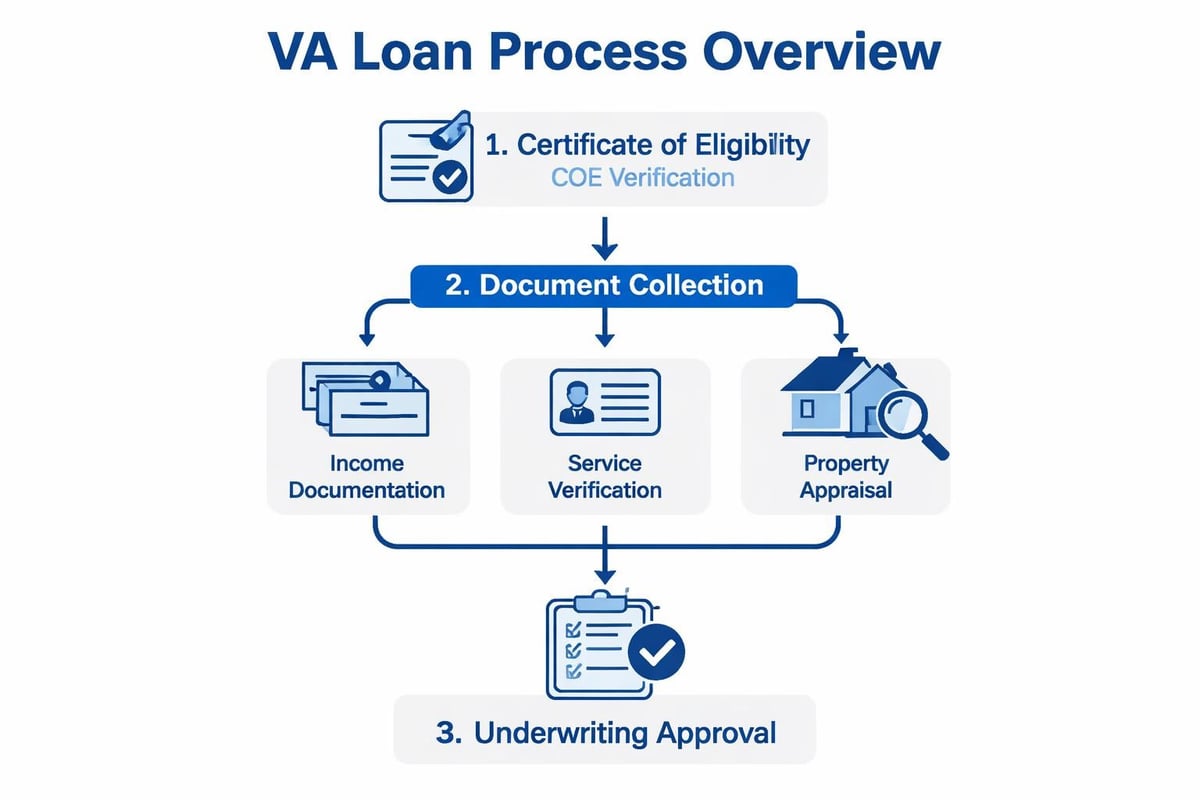

Service Requirements and Certificate of Eligibility

Eligibility starts with military service. Generally, you qualify with 90 consecutive days of active service during wartime, 181 days during peacetime, or six years in the National Guard or Reserves. Your broker can help you obtain your Certificate of Eligibility (COE) through the VA's online portal or via lender channels.

The VA home loan servicers program maintains standards that all participating lenders and brokers must follow, ensuring veterans receive consistent treatment and proper guidance regardless of location.

Income Qualification and Debt-to-Income Ratios

VA guidelines allow for higher debt-to-income (DTI) ratios than most conventional programs. While 41% DTI is the standard threshold, experienced underwriters regularly approve loans with ratios exceeding 50% when compensating factors exist.

For Seattle-area tech professionals working at Amazon, Microsoft, or Google, a knowledgeable va loan mortgage broker understands how to document and qualify:

- Restricted stock units (RSUs) using vesting schedules and historical value

- Annual bonuses with two-year history and continuation likelihood

- Stock options and equity compensation packages

- Variable income from commissions or contract work

This specialized knowledge becomes crucial when purchasing homes in the $900,000 to $1.5 million range common throughout Redmond and Kirkland.

Credit Score Considerations

While the VA itself has no minimum credit score requirement, most lenders establish overlays between 580 and 620. A va loan mortgage broker with access to multiple investors can match borrowers with lenders whose credit requirements align with their profile.

Strategies for credit-challenged borrowers include:

- Identifying lenders who accept manual underwriting for scores below 620

- Timing the loan application after recent credit improvements age appropriately

- Providing detailed written explanations for past credit issues

- Demonstrating consistent payment history over the past 12-24 months

- Leveraging compensating factors like significant cash reserves

Navigating VA Appraisal Requirements

The VA appraisal process protects both the veteran borrower and the VA's guarantee by ensuring properties meet minimum property requirements (MPRs). Your va loan mortgage broker should prepare you for this process and know how to address common issues.

Common Appraisal Challenges in Seattle-Area Properties

Older homes in established Seattle neighborhoods may present MPR concerns including outdated electrical systems, roof condition, foundation issues, or peeling paint. Your broker can coordinate with sellers on repair negotiations or explore alternative solutions.

In competitive markets, appraisal gaps (when the appraised value comes in below the purchase price) create particular challenges for zero-down VA buyers. Experienced brokers develop strategies including:

- Pre-qualifying for appraisal waivers through automated systems

- Structuring offers with escalation clauses that account for appraisal risk

- Negotiating seller price reductions when appraisals support lower values

- Helping buyers understand when bringing cash to closing makes sense

- Exploring rapid resale restriction exceptions for new construction

Working with VA Appraisers

The VA maintains a panel of approved appraisers in each region. While your broker cannot select a specific appraiser, they can ensure the appraisal order includes all necessary property information and comparable sales data to support the contract price.

In rapidly appreciating areas like Mill Creek and Lynnwood, providing recent comparable sales becomes essential for accurate valuations. Your va loan mortgage broker should work closely with your real estate agent to compile this information.

Cost Considerations: Funding Fees and Closing Costs

Understanding the true cost of VA financing helps veterans make informed decisions. A transparent va loan mortgage broker will break down all fees and explain strategies to minimize out-of-pocket expenses.

VA Funding Fee Structure

The VA funding fee helps sustain the loan program for future generations of veterans. For 2026, the fee structure includes:

| Use Type | Down Payment | Regular Military | Reserves/Guard |

|---|---|---|---|

| First Use | 0% down | 2.15% | 2.40% |

| First Use | 5-9.99% down | 1.50% | 1.75% |

| First Use | 10%+ down | 1.25% | 1.50% |

| Subsequent Use | 0% down | 3.30% | 3.30% |

Veterans receiving VA disability compensation are exempt from the funding fee entirely, creating significant savings. On a $700,000 loan in Shoreline, the exemption saves $15,050.

Seller Concessions and Closing Cost Strategies

VA regulations allow sellers to pay up to 4% of the purchase price toward buyer closing costs, significantly more than the 3% typically permitted on conventional loans. Your broker should negotiate these concessions to minimize your cash requirement at closing.

Typical closing costs covered by seller concessions include:

- Lender origination and processing fees

- Title insurance and escrow fees

- Property tax and insurance reserves

- VA funding fee (can also be financed)

- Prepaid interest and recording fees

Finding the Right VA Loan Mortgage Broker in Seattle

Selecting a mortgage professional who combines VA expertise with local market knowledge ensures you receive comprehensive guidance throughout your home purchase journey.

Questions to Ask Potential Brokers

Before committing to a va loan mortgage broker, conduct thorough due diligence. Mortgage industry advocates emphasize that brokers should never let ignorance about VA loans prevent them from serving veteran clients effectively.

- How many VA loans do you close annually in the Seattle metro area?

- Which lenders in your network offer the most competitive VA pricing?

- What's your average timeline from application to closing on VA purchases?

- How do you handle appraisal issues and repair negotiations?

- Can you provide references from recent veteran clients?

- What experience do you have with jumbo VA loans above conforming limits?

- How do you stay current on VA guideline changes and local underwriting overlays?

Evaluating Broker Experience and Reviews

Online reviews provide valuable insights into a broker's service quality and VA loan expertise. Look for consistent themes around communication, problem-solving, and successful closings in competitive situations.

A va loan mortgage broker with hundreds of five-star reviews across multiple platforms demonstrates sustained excellence. Pay particular attention to feedback from veteran clients who purchased in similar neighborhoods or price ranges to your target area.

Understanding Broker Compensation and Lender Relationships

Mortgage brokers typically receive compensation from lenders in the form of yield spread premium or lender-paid compensation. This arrangement should not increase your interest rate or costs compared to working directly with a retail lender.

Your broker should disclose their lender relationships and explain how they select the best option for your specific scenario. Transparency about compensation builds trust and ensures alignment of interests throughout the transaction.

Special Considerations for Seattle-Area VA Borrowers

The unique characteristics of the Greater Seattle housing market create specific scenarios where VA loan expertise becomes particularly valuable.

Condominium Financing

Many Seattle neighborhoods feature condominium developments, particularly in urban areas and newer construction communities. VA condo financing requires the building to hold VA approval, which not all developments maintain.

Your va loan mortgage broker should verify condo approval status early in your search and understand the approval process if you find a non-approved building worth pursuing. This specialized knowledge prevents wasted time on properties you cannot finance with VA benefits.

New Construction and Builder Negotiations

Working with production builders in areas like Everett and Mill Creek requires different strategies than resale home purchases. Builders often have preferred lenders offering incentives, but these may not provide the best overall value.

A skilled broker can analyze builder incentives against open market financing to determine the most advantageous path. They can also negotiate builder contributions toward closing costs and explain how design center upgrades impact your loan amount and qualification.

Investment Property Restrictions

VA loans require owner occupancy, limiting their use for investment properties. However, multi-unit properties (2-4 units) qualify for VA financing when you occupy one unit as your primary residence.

This provision creates powerful wealth-building opportunities in Seattle's strong rental market. Your broker should understand how to underwrite rental income from non-occupied units and structure these more complex transactions for approval.

Working with Real Estate Agents on VA Purchases

The relationship between your va loan mortgage broker and your real estate agent significantly impacts your success in competitive markets. Coordinated teamwork creates stronger offers and smoother transactions.

Pre-Approval Strength and Documentation

Generic pre-approval letters carry little weight in multiple-offer situations. Your broker should provide detailed pre-approval documentation demonstrating thorough underwriting, verified income and assets, and clear path to closing.

For Bellevue and Redmond purchases where competition remains intense, some brokers offer pre-underwritten approvals with conditional loan commitments issued before you even find a property. This elevated approval status positions VA buyers as favorably as conventional and cash buyers.

Communication and Timeline Management

Your real estate agent needs confidence in your broker's ability to meet contracted deadlines. Regular communication throughout the transaction keeps all parties informed and allows proactive problem-solving when issues arise.

Experienced Seattle mortgage brokers understand local escrow timelines, title company requirements, and the importance of coordination with all transaction parties. This local knowledge prevents delays and builds trust with listing agents who may have concerns about VA financing timelines.

Common VA Loan Myths and Misconceptions

Despite being one of the best mortgage products available, VA loans face persistent myths that can disadvantage veteran buyers. Your va loan mortgage broker should actively combat these misconceptions with listing agents and sellers.

Myth: VA Loans Take Longer to Close

Reality: With experienced lenders and brokers, VA loans regularly close in 15-20 days, with some completing in as few as 9 business days. The perceived delays often result from broker inexperience or borrower documentation issues, not the VA program itself.

Myth: VA Appraisals Are Overly Strict

Reality: VA appraisals focus on health and safety, ensuring the property is safe, sound, and sanitary. While MPRs exist, they protect buyers from purchasing homes with significant defects. Most properties that pass conventional appraisals also meet VA requirements.

Myth: Sellers Pay More in Fees

Reality: Sellers face the same costs regardless of buyer financing type. The VA restricts which costs buyers can pay, but this doesn't increase seller expenses. The 4% seller concession allowance actually benefits sellers by making their properties more attractive to VA buyers.

Myth: VA Buyers Are Less Qualified

Reality: VA borrowers undergo the same rigorous underwriting as conventional buyers. The zero-down payment reflects an earned benefit, not weak financial position. Many VA buyers maintain substantial reserves and strong credit profiles.

Refinancing Strategies for Current VA Loan Holders

Veterans who already own homes using VA financing have unique refinancing opportunities. Your va loan mortgage broker should monitor rates and recommend strategic refinances that improve your financial position.

When to Consider an IRRRL

The streamlined VA refinance makes sense when you can reduce your interest rate by at least 0.50% and plan to remain in the home long enough to recoup closing costs through monthly savings. With no appraisal or income verification required, the application process takes days rather than weeks.

Your broker should calculate your break-even point considering the funding fee, any rate-buy-down costs, and monthly payment reduction. In 2026's rate environment, many veterans who financed or refinanced in 2021-2023 may benefit from an IRRRL.

Cash-Out Refinancing for Home Improvements

Seattle's strong appreciation has created substantial equity for homeowners. A VA cash-out refinance allows you to access this equity while maintaining favorable VA loan terms, though current market rates should be compared against your existing rate.

Consider cash-out refinancing when:

- Your current equity exceeds 30-40%

- You need funds for significant home improvements that increase value

- You're consolidating higher-interest debt

- The new rate remains competitive with your current financing

Your broker can model various scenarios showing long-term costs and benefits of different refinancing strategies, including conventional refinance alternatives when appropriate.

Advanced Strategies for Maximizing VA Loan Benefits

Sophisticated borrowers can leverage multiple VA loan features simultaneously to build wealth and housing flexibility.

Multiple Simultaneous VA Loans

Veterans with sufficient remaining entitlement can maintain more than one VA loan simultaneously. This allows you to purchase a second primary residence without selling your current home, creating opportunities for:

- Relocation while retaining your current property as a rental

- Purchasing a multi-unit property while still owning your single-family home

- Upgrading to a larger home without contingent sale requirements

Your va loan mortgage broker should understand entitlement calculations and help determine whether you qualify for concurrent VA financing.

Entitlement Restoration After Sale

When you sell a property financed with a VA loan, you can restore your full entitlement by ensuring the loan is paid in full and submitting the appropriate paperwork to the VA. This restoration allows you to use the benefit again with first-time-use funding fee rates.

The restoration process typically takes 4-6 weeks, so plan accordingly if you're selling and purchasing simultaneously. Your broker can coordinate timing to ensure your entitlement is available when needed for your next purchase.

Combining VA Benefits with Other Programs

In some scenarios, VA borrowers can layer additional assistance programs. Washington State offers down payment assistance programs that can supplement VA financing, though this rarely makes sense given VA's zero-down capability.

More commonly, disabled veterans who are exempt from the funding fee can combine this benefit with seller concessions to achieve a truly zero-cost transaction, walking into their new home with minimal out-of-pocket expense.

Working with a specialized va loan mortgage broker transforms your home buying or refinancing experience from confusing to confident. The right professional combines deep VA program knowledge with local Seattle market expertise, ensuring you maximize your earned benefits while competing effectively in one of the nation's most dynamic real estate markets. Whether you're purchasing your first home in Lake Forest Park or refinancing your Everett property, expert guidance makes all the difference. Keith Akada and the team at Mortgage Reel bring 25+ years of experience serving veterans throughout the Greater Seattle area, backed by 750+ five-star reviews and the ability to close your VA loan in as few as 9 business days.