Understanding your home mortgage options can be the difference between a confident purchase decision and years of unnecessary financial stress. For homebuyers across Seattle, Bellevue, Redmond, and Kirkland, navigating today's mortgage landscape requires more than just comparing rates. It demands a strategic approach that considers loan programs, qualification requirements, and how your unique financial profile-including RSUs, bonuses, and other compensation-impacts your buying power in a competitive housing market.

What Is a Home Mortgage and How Does It Work

A home mortgage is a secured loan used to purchase real estate, where the property itself serves as collateral. When you obtain a mortgage, you're borrowing funds from a lender and agreeing to repay that amount plus interest over a specified term, typically 15 or 30 years.

The mortgage process involves several key components that work together. Your monthly payment typically includes principal (the loan amount you borrowed), interest (the lender's fee for lending you money), property taxes, homeowners insurance, and potentially private mortgage insurance if your down payment is less than 20 percent.

The Mortgage Structure

Understanding how mortgages are structured helps you make better financial decisions:

- Principal and Interest: These comprise your base payment and determine how quickly you build equity

- Escrow Account: Most lenders collect taxes and insurance monthly, holding funds in escrow to pay annual bills

- Amortization Schedule: Your payment allocation shifts over time, with early payments weighted toward interest

- Loan-to-Value Ratio: This percentage determines your risk profile and potential PMI requirements

The Consumer Financial Protection Bureau provides comprehensive resources for understanding these mortgage fundamentals and managing your loan throughout its lifecycle.

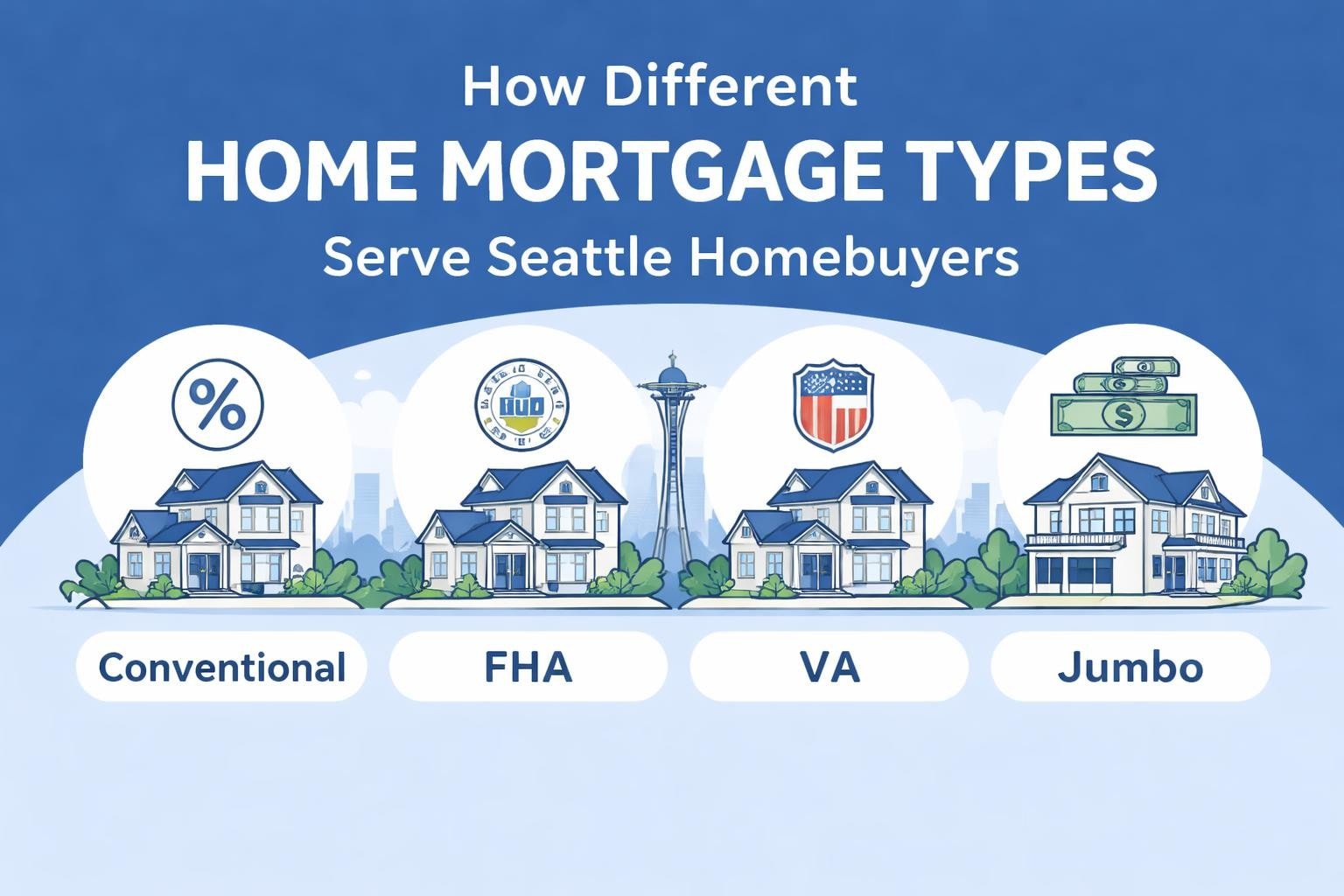

Common Home Mortgage Types in 2026

Selecting the right home mortgage product depends on your financial situation, down payment capacity, and long-term goals. Each loan type offers distinct advantages for different buyer profiles across the Greater Seattle area.

Conventional Loans

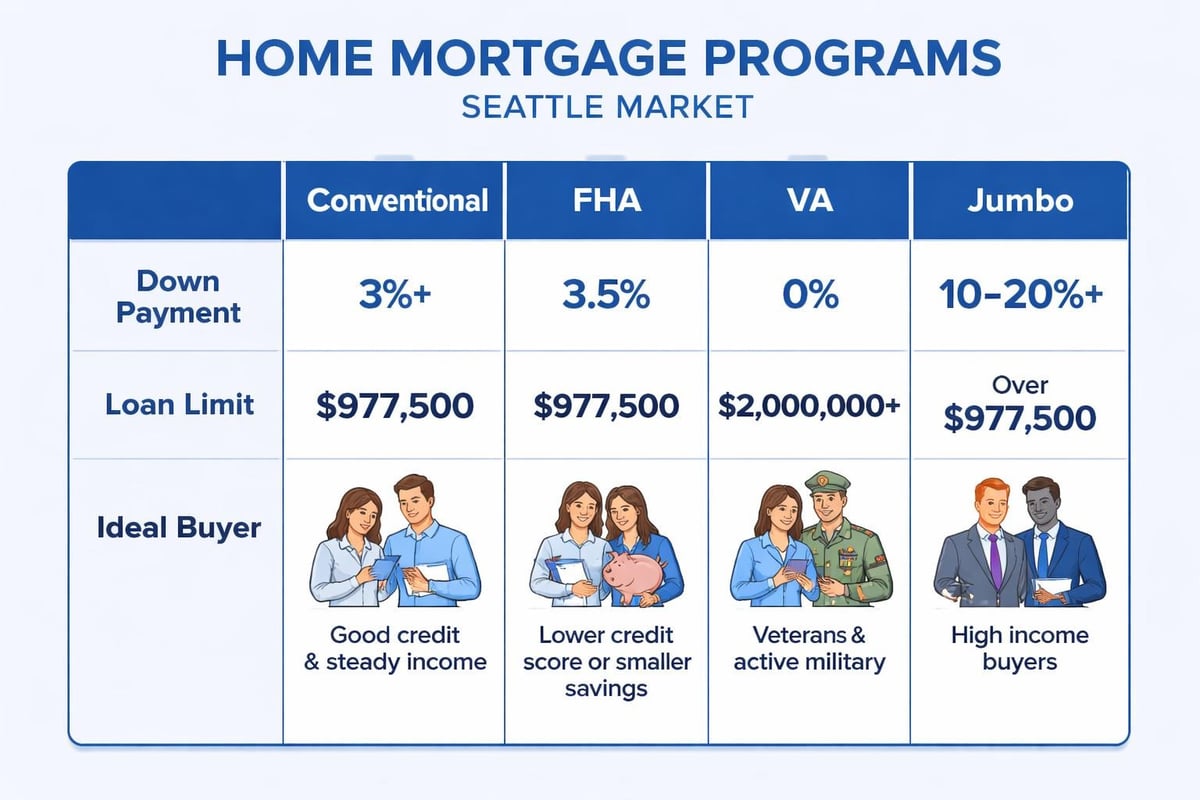

Conventional mortgages remain the most popular choice for buyers with solid credit and stable income. These loans aren't backed by government agencies and typically require:

- Minimum credit scores of 620, though 740+ secures better rates

- Down payments as low as 3% for qualified first-time buyers

- Private mortgage insurance when putting down less than 20%

- Conforming loan limits of $806,500 in King County for 2026

For tech professionals in Shoreline or Mill Creek with strong W-2 income and stock compensation, conventional loans often provide the most flexibility and competitive rates.

FHA Loans

Federal Housing Administration loans serve buyers who may not qualify for conventional financing. These government-backed mortgages feature:

- Credit score minimums as low as 580 with 3.5% down

- Higher debt-to-income ratio tolerance (up to 50% in some cases)

- Upfront and annual mortgage insurance premiums

- Loan limits of $806,500 in King County

First-time buyers in Lynnwood or Lake Forest Park often benefit from FHA financing when building their credit profile or working with limited savings. Our first-time homebuyer guide covers these programs in detail.

VA Loans

Veterans, active-duty service members, and eligible spouses can access exceptional benefits through VA-backed mortgages:

- Zero down payment requirement

- No private mortgage insurance

- Competitive interest rates regardless of down payment size

- Flexible credit and income guidelines

VA loans for house purchases represent one of the most powerful financing tools available, particularly in higher-priced markets like Seattle and Bellevue.

Jumbo Loans

When purchasing property above conforming loan limits, jumbo mortgages become necessary. In 2026, these loans require:

- Excellent credit scores (typically 700+)

- Larger down payments (often 10-20%)

- Comprehensive income documentation

- Higher reserve requirements (6-12 months of payments)

Seattle's competitive real estate market frequently necessitates jumbo financing, especially for tech professionals leveraging stock compensation to purchase in Redmond or Kirkland. Specialized underwriting can qualify RSUs, bonuses, and equity grants that traditional lenders might exclude.

Home Mortgage Qualification Requirements

Understanding what lenders evaluate during the approval process helps you prepare strategically and address potential obstacles before they derail your timeline.

| Qualification Factor | Conventional | FHA | VA | Jumbo |

|---|---|---|---|---|

| Minimum Credit Score | 620-740 | 580 | 580 | 700+ |

| Maximum DTI Ratio | 43-50% | 50% | 41-50% | 43-45% |

| Minimum Down Payment | 3-5% | 3.5% | 0% | 10-20% |

| Reserves Required | 0-2 months | 0-2 months | 0 months | 6-12 months |

Credit Profile Considerations

Your credit score impacts both approval likelihood and the interest rate you'll secure. Lenders examine:

- Payment History: Late payments within the past 24 months carry significant weight

- Credit Utilization: Keeping balances below 30% of available credit demonstrates responsible management

- Recent Inquiries: Multiple credit applications within short periods can lower scores temporarily

- Account Age: Longer credit histories generally support higher scores

Before beginning your home search in Everett or other Seattle-area cities, review your credit reports for errors and address any outstanding collections or delinquencies.

Income Documentation Strategies

Lenders verify your ability to repay through comprehensive income analysis. Standard requirements include:

- Two years of W-2 forms and tax returns

- Recent pay stubs covering 30 days

- Year-to-date profit and loss statements for self-employed borrowers

- Documentation for bonuses, commissions, and stock compensation

For Seattle tech professionals, qualifying RSUs and stock grants requires specialized knowledge. Lenders can use vested equity and projected grants to increase buying power, but proper documentation and underwriting expertise are essential. According to Statista’s research on mortgage resources, homebuyers increasingly rely on specialized lenders who understand complex compensation structures.

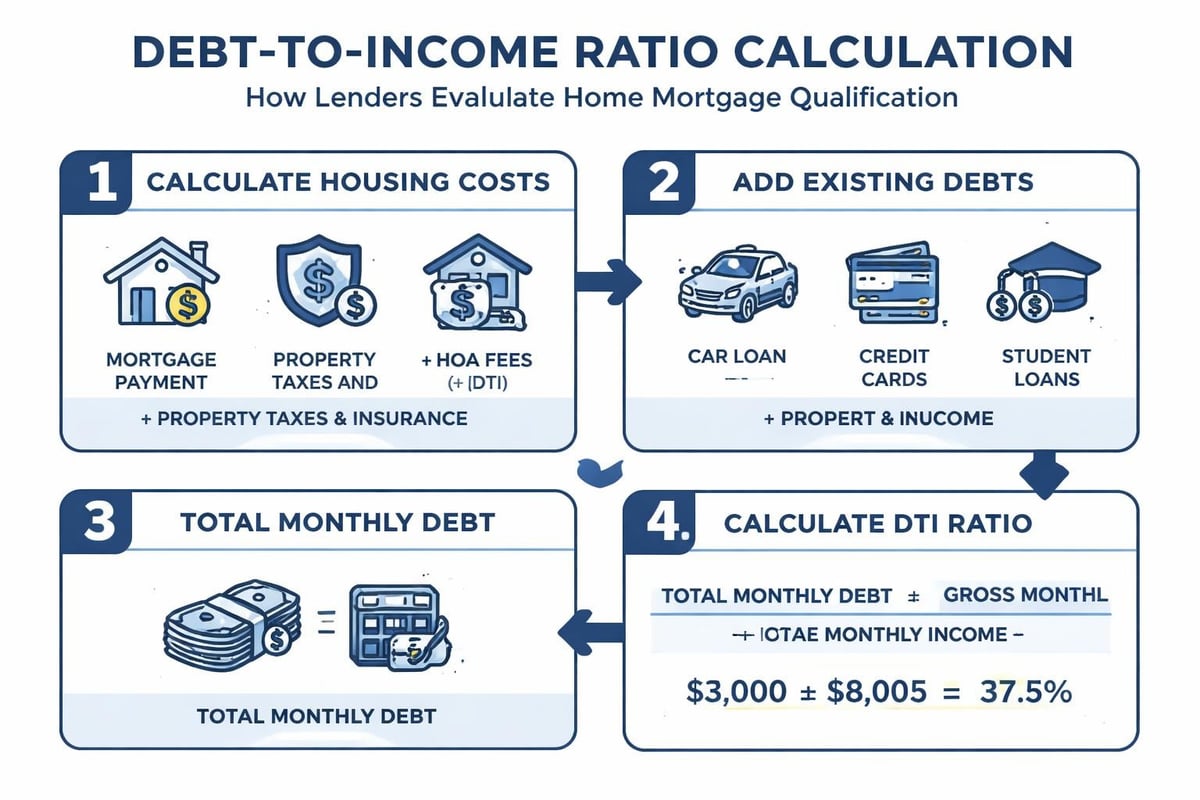

Debt-to-Income Ratio Management

Your DTI ratio compares monthly debt obligations to gross income. Lenders calculate two ratios:

- Front-End Ratio: Housing payment divided by gross monthly income

- Back-End Ratio: All monthly debts divided by gross monthly income

To improve your DTI before applying, consider paying down credit cards, postponing major purchases, or increasing income through promotions or additional compensation recognition.

Down Payment Strategies for Your Home Mortgage

The amount you put down affects your monthly payment, interest rate, mortgage insurance requirements, and overall loan costs. Understanding your options helps you make strategic decisions aligned with your financial goals.

Minimum Down Payment Requirements

Different loan programs offer varying down payment flexibility:

- Conventional 97: 3% down for first-time buyers with income limits

- Conventional 95: 5% down for repeat buyers

- FHA: 3.5% down with credit scores of 580+

- VA: 0% down for eligible veterans and service members

Many buyers assume they need 20 percent down for home loans, but numerous programs enable homeownership with significantly less. However, lower down payments typically result in higher monthly costs due to mortgage insurance.

Down Payment Sources and Documentation

Lenders scrutinize where your down payment originates. Acceptable sources include:

- Personal savings seasoned in accounts for at least 60 days

- Gift funds from immediate family members with proper documentation

- Down payment assistance programs available in King and Snohomish counties

- Proceeds from selling another property

- Retirement account withdrawals (with tax implications)

Large deposits appearing shortly before application require explanation letters and documentation showing the source. For detailed guidance on down payment planning, explore our resource on down payment on home purchases.

The 20 Percent Advantage

While not required, reaching a 20% down payment delivers multiple benefits:

- Eliminating PMI: Avoid monthly mortgage insurance premiums

- Better Rates: Lower loan-to-value ratios qualify for improved pricing

- Stronger Offers: In competitive Seattle markets, larger down payments signal buyer strength

- Lower Monthly Costs: Reduced principal means smaller payments over the loan term

Balancing down payment size with maintaining emergency reserves and investment opportunities requires careful analysis of your complete financial picture.

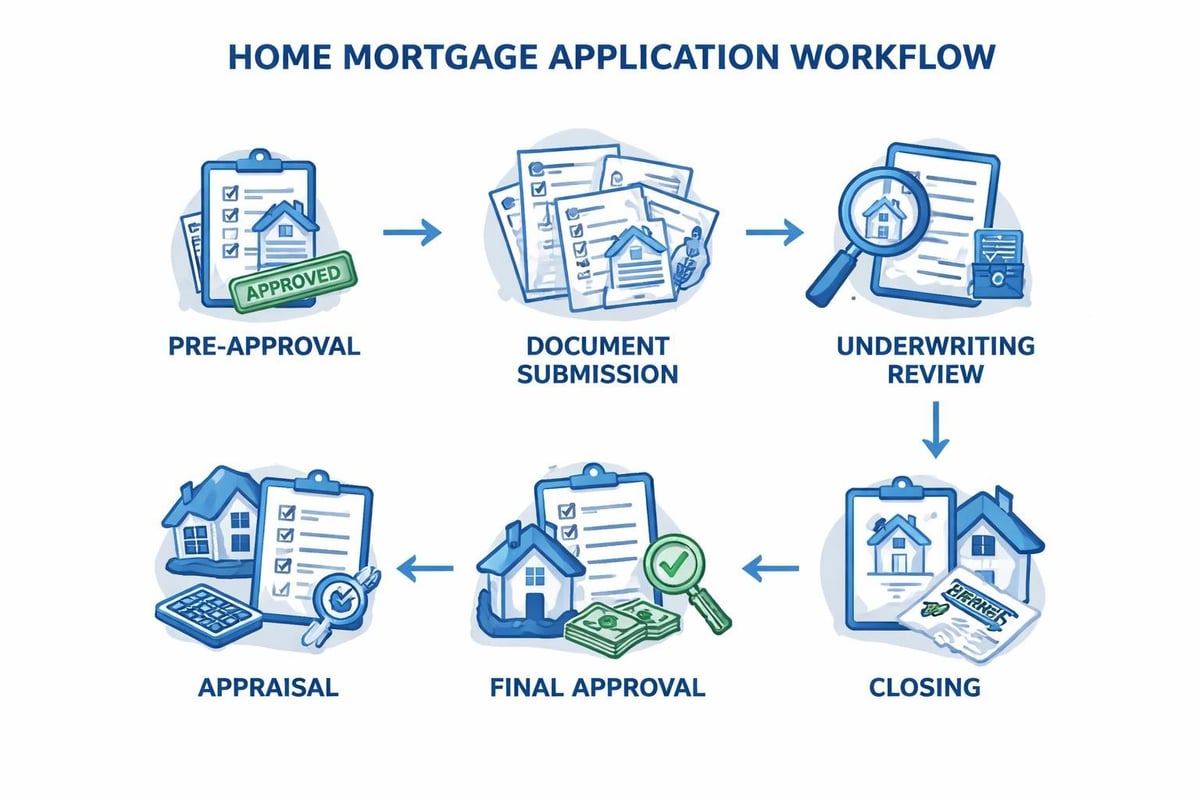

The Home Mortgage Application Process

Understanding what to expect during the mortgage process reduces stress and helps you meet critical deadlines in competitive markets where timing matters.

Pre-Approval vs. Pre-Qualification

These terms are often confused but represent different commitment levels:

Pre-Qualification provides a rough estimate based on basic financial information you provide. It requires no documentation verification and carries minimal weight with sellers.

Pre-Approval involves comprehensive document review, credit checks, and underwriter evaluation. This demonstrates serious buyer intent and provides accurate budget parameters for your home search.

In Seattle's competitive market, pre-approval is essential. Many listing agents won't accept offers without verified pre-approval letters demonstrating your financing capability.

Timeline and Key Milestones

| Phase | Duration | Key Activities |

|---|---|---|

| Pre-Approval | 1-3 days | Document submission, credit review, initial underwriting |

| Home Search | Varies | Working with agents, viewing properties, market analysis |

| Offer Acceptance | 1-7 days | Negotiation, contract execution, earnest money deposit |

| Processing | 7-14 days | Appraisal, title work, detailed underwriting review |

| Clear to Close | 2-5 days | Final conditions, funding approval, closing coordination |

With advanced underwriting capabilities, experienced brokers can compress timelines significantly. Closing in 9 business days is achievable when buyers provide complete documentation upfront and properties appraise appropriately.

Required Documentation Checklist

Gathering documents before starting your application accelerates the process:

- Government-issued photo identification

- Two years of federal tax returns with all schedules

- Two years of W-2 forms or 1099s

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Documentation for additional income sources (bonuses, RSUs, rental income)

- Divorce decrees or separation agreements if applicable

- Bankruptcy or foreclosure discharge papers if relevant

For self-employed borrowers in Lake Forest Park or Mill Creek, additional profit and loss statements and business tax returns are necessary.

Interest Rates and How They Impact Your Home Mortgage

Your interest rate determines how much you'll pay over the life of your loan, making it one of the most critical factors in mortgage selection. Small rate differences create substantial cost variations over 30 years.

Factors Affecting Your Interest Rate

Lenders price loans based on risk assessment. Variables influencing your rate include:

- Credit Score: Higher scores qualify for better rates, with optimal pricing typically starting at 740+

- Loan-to-Value Ratio: Larger down payments reduce lender risk and improve pricing

- Property Type: Single-family homes receive better rates than condos or multi-unit properties

- Occupancy Status: Primary residences get preferential rates compared to investment properties

- Loan Amount: Jumbo mortgages often carry slightly higher rates due to increased risk

Market conditions also influence rates. The Home Mortgage Disclosure Act data provides insights into lending patterns and rate trends across different markets.

Fixed vs. Adjustable Rate Mortgages

Fixed-Rate Mortgages maintain the same interest rate throughout the loan term, providing payment predictability. In 2026, 30-year fixed mortgages remain the most common choice, though 15-year and 20-year options exist for buyers wanting to build equity faster.

Adjustable-Rate Mortgages (ARMs) offer lower initial rates that adjust periodically based on market indices. Common structures include:

- 5/1 ARM: Fixed for 5 years, then adjusts annually

- 7/1 ARM: Fixed for 7 years, then adjusts annually

- 10/1 ARM: Fixed for 10 years, then adjusts annually

ARMs can benefit buyers planning to sell or refinance before the adjustment period begins, or those expecting significant income increases. However, they carry risk if rates rise substantially during the adjustment phase.

Rate Locks and Timing Strategies

Once you have an accepted offer, locking your interest rate protects against market increases during closing. Standard lock periods range from 30 to 60 days, with longer locks sometimes available for new construction purchases.

Deciding when to lock requires market awareness. In rising rate environments, early locks preserve favorable pricing. In declining markets, float strategies or float-down options may secure better rates.

Mortgage Insurance and How It Affects Your Payment

When putting less than 20% down on a conventional home mortgage, private mortgage insurance protects lenders against default risk. Understanding PMI costs and elimination strategies helps you manage long-term expenses.

PMI Cost Structure

Private mortgage insurance typically costs between 0.5% and 1.5% of the original loan amount annually, divided into monthly payments. A $400,000 loan might carry $200-$500 in monthly PMI depending on your credit score and down payment percentage.

Factors influencing your PMI rate include:

- Down payment size (higher down payments = lower PMI)

- Credit score (stronger credit = lower PMI)

- Loan type and term

- Property location and type

Eliminating Private Mortgage Insurance

PMI isn't permanent. You can remove it when your loan balance reaches 80% of the original purchase price through:

- Scheduled Cancellation: Making regular payments until you reach 78% loan-to-value automatically triggers removal

- Requested Cancellation: Reaching 80% LTV through extra payments and requesting removal

- Refinancing: Obtaining a new loan once you've reached 20% equity

- Property Appreciation: Some lenders permit removal based on current home value after a minimum period

For FHA loans, mortgage insurance rules differ. Loans originated after 2013 with less than 10% down carry mortgage insurance for the life of the loan, removable only through refinancing to conventional financing.

Working with Mortgage Brokers vs. Direct Lenders

Choosing where to obtain your home mortgage significantly impacts your experience, options, and potentially your costs. Understanding the differences helps you make an informed decision.

Mortgage Broker Advantages

Brokers work with multiple lenders, offering access to diverse loan products and pricing. Benefits include:

- Program Variety: Access to conventional, government, and specialty loan products from numerous lenders

- Rate Shopping: Comparing multiple lenders simultaneously without additional credit inquiries

- Complex Scenarios: Expertise in qualifying challenging situations like stock compensation, self-employment, or credit issues

- Personalized Service: Direct communication with experienced professionals throughout the process

For Seattle tech professionals with RSUs, bonuses, and complex compensation packages, working with brokers who understand these income sources is essential for maximizing buying power.

Direct Lender Considerations

Banks and credit unions offer loans directly, maintaining control over the entire process. Potential advantages include:

- Relationship benefits for existing customers

- Potentially streamlined processes for simple scenarios

- In-house decision-making on some loan aspects

However, product selection is limited to that institution's offerings, and pricing may not be competitive across all scenarios.

Questions to Ask Your Mortgage Professional

Regardless of whom you work with, ask these critical questions:

- What loan programs am I qualified for based on my complete financial profile?

- How do you qualify complex income like RSUs, bonuses, or self-employment?

- What are all the costs associated with my loan, including lender fees and third-party charges?

- What is your average timeline from application to closing?

- Can you provide references from recent clients in similar situations?

The OCC provides guidance on understanding loan terms and working effectively with mortgage professionals.

Common Home Mortgage Mistakes to Avoid

Even experienced buyers make errors during the mortgage process that cost money or jeopardize transactions. Awareness of these pitfalls helps you navigate successfully.

Financial Missteps During the Process

Once pre-approved, maintain financial stability until closing:

- Avoid Large Purchases: New cars, furniture, or appliances increase debt ratios and may disqualify you

- Don't Change Jobs: Employment changes, even for higher pay, can delay or derail closing

- Preserve Cash Reserves: Don't deplete accounts needed for down payment and closing costs

- Skip New Credit Applications: Hard inquiries and new accounts impact qualification

- Maintain Bill Payments: Late payments during the process can cause rate increases or denials

Lenders re-verify employment and credit immediately before closing. Changes discovered at this stage can have serious consequences.

Overlooking Total Cost of Homeownership

Your home mortgage payment is just one component of ownership costs. Budget for:

- Property taxes (which can be substantial in Seattle and surrounding areas)

- Homeowners insurance and potentially flood or earthquake coverage

- HOA fees for condos or certain communities

- Maintenance and repairs (typically 1-2% of home value annually)

- Utilities and services

Understanding complete monthly costs prevents financial strain after purchase.

Focusing Solely on Interest Rates

While important, interest rates aren't the only consideration. Evaluate:

- Total closing costs and lender fees

- Loan features like prepayment penalties or adjustable rate caps

- Lender reputation and service quality

- Processing timelines and closing reliability

The lowest rate means nothing if the lender can't close on time or charges excessive fees that offset the savings.

Refinancing Your Existing Home Mortgage

Refinancing replaces your current loan with a new mortgage, potentially lowering your rate, changing your term, or accessing equity. Understanding when refinancing makes sense protects you from costly mistakes.

Reasons to Refinance

Strategic refinancing serves multiple purposes:

- Rate and Term Refinance: Lower your interest rate or change your loan term to save money or pay off your home faster

- Cash-Out Refinance: Access equity for home improvements, debt consolidation, or investment opportunities

- PMI Removal: Refinance to eliminate mortgage insurance once you've reached 20% equity

- Loan Type Change: Convert from adjustable to fixed rates for payment stability

Break-Even Analysis

Refinancing involves costs-typically 2-5% of the loan amount. Calculate your break-even point by dividing total refinancing costs by monthly savings. If you break even in 24-36 months and plan to keep the property longer, refinancing likely makes financial sense.

For example, if refinancing costs $6,000 and saves $200 monthly, you break even in 30 months. Staying beyond that point generates savings.

Current Market Considerations for 2026

Interest rate environments shift over time. According to Consumer Financial Protection Bureau mortgage trend data, understanding market patterns helps time refinancing decisions effectively.

In 2026, evaluate refinancing when rates drop at least 0.75-1% below your current rate, or when your financial situation has improved significantly, potentially qualifying you for better terms than when you originally purchased.

Securing the right home mortgage requires strategic planning, comprehensive documentation, and expert guidance through complex qualification scenarios. From understanding loan program options to navigating Seattle's competitive market with confidence, the decisions you make today impact your financial future for decades. Whether you're a first-time buyer in Lake Forest Park, a tech professional leveraging stock compensation for a jumbo loan in Bellevue, or a veteran exploring VA benefits in Everett, working with an experienced mortgage professional who understands your unique situation is essential. Keith Akada at Mortgage Reel brings over 25 years of expertise helping Seattle-area buyers and homeowners make confident financing decisions, with the ability to close in as few as 9 business days and proven success qualifying complex compensation for Amazon, Microsoft, and Google employees.