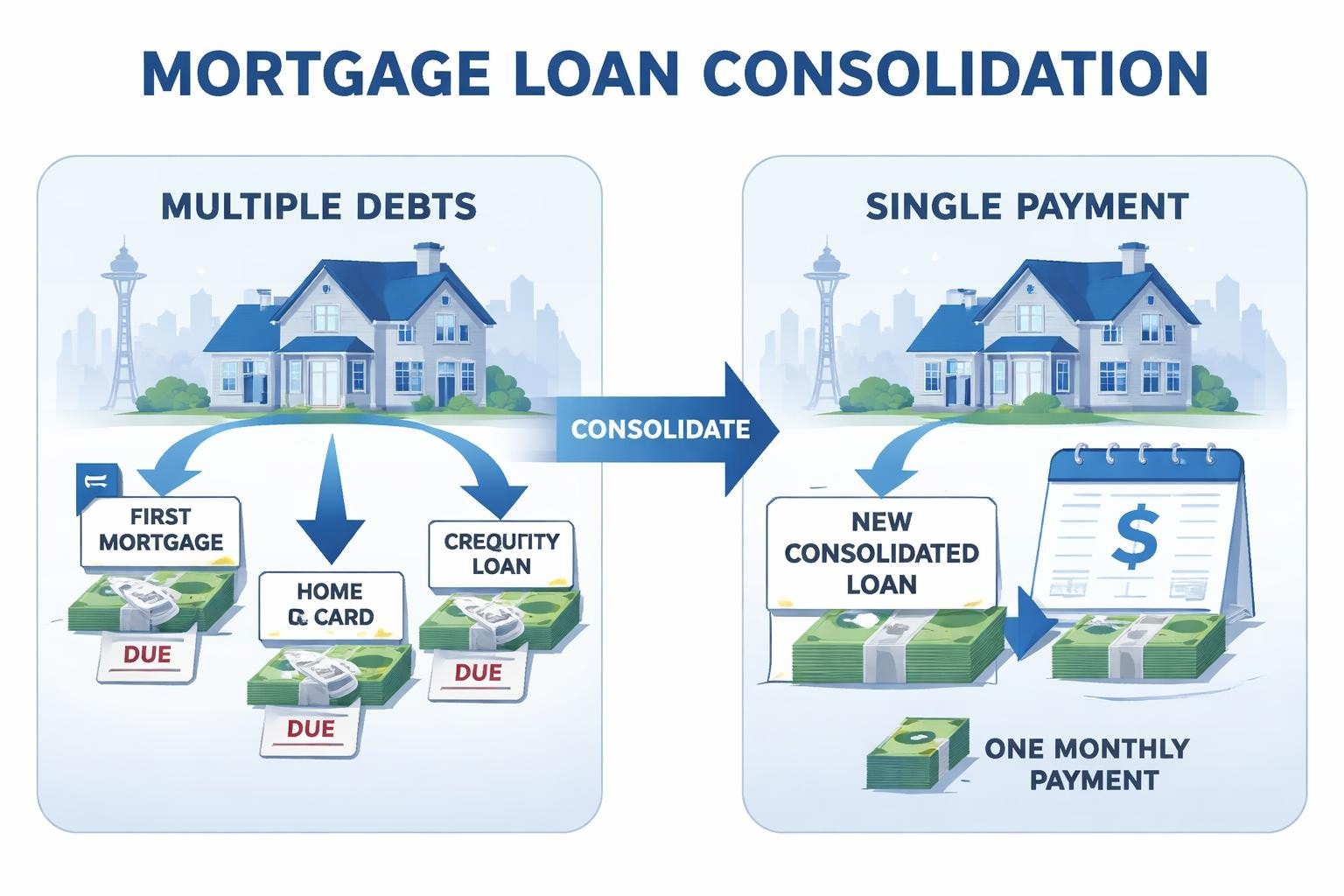

Managing multiple debts alongside your mortgage can strain even the most carefully planned household budget. For homeowners across Seattle, Bellevue, Redmond, and Kirkland, mortgage loan consolidation offers a strategic approach to simplifying monthly obligations while potentially reducing overall interest costs. This financial tool has become increasingly relevant for tech professionals and homeowners throughout the Greater Seattle area who carry various forms of debt alongside their home loans. Understanding how consolidation works, when it makes sense, and how to execute it properly can transform your financial picture and create breathing room in your monthly budget.

Understanding Mortgage Loan Consolidation Fundamentals

Mortgage loan consolidation involves using your home's equity to pay off multiple debts, combining them into a single monthly payment through your mortgage. This strategy differs from simply refinancing your existing mortgage. Instead, you're leveraging the equity you've built in your Seattle-area property to eliminate higher-interest obligations such as credit cards, auto loans, or personal loans.

The mechanics are straightforward but require careful consideration. When you pursue consolidation loans, you're essentially replacing unsecured debt with debt secured by your home. This transfer can significantly reduce your interest rate, particularly when consolidating credit card balances that often carry rates between 18% and 25%.

How Equity Makes Consolidation Possible

Your home equity serves as the foundation for this strategy. In competitive markets like Shoreline and Lynnwood, where property values have appreciated substantially over recent years, many homeowners have accumulated considerable equity without realizing it. This equity represents the difference between your home's current market value and your remaining mortgage balance.

Key equity requirements typically include:

- Minimum 20% equity remaining after consolidation

- Strong credit profile (usually 620 or higher)

- Documented income sufficient to support the new payment

- Debt-to-income ratio within acceptable limits (typically below 43%)

For Microsoft and Amazon employees, stock compensation and RSUs can strengthen your qualification profile when pursuing mortgage loan consolidation. These income sources demonstrate stability and earning potential that lenders value when underwriting larger loan amounts.

Strategic Benefits for Seattle Homeowners

The primary advantage of mortgage loan consolidation extends beyond simple payment reduction. Homeowners in Mill Creek and Lake Forest Park often discover multiple financial benefits that compound over time. The interest on mortgage debt may be tax-deductible, unlike credit card interest, though you should always consult with a tax professional about your specific situation.

Payment simplification represents another substantial benefit. Instead of managing five or six separate creditors with different due dates, payment amounts, and interest rates, you handle one streamlined mortgage payment each month. This reduction in complexity decreases the likelihood of missed payments and the associated credit score damage.

Interest Rate Advantages

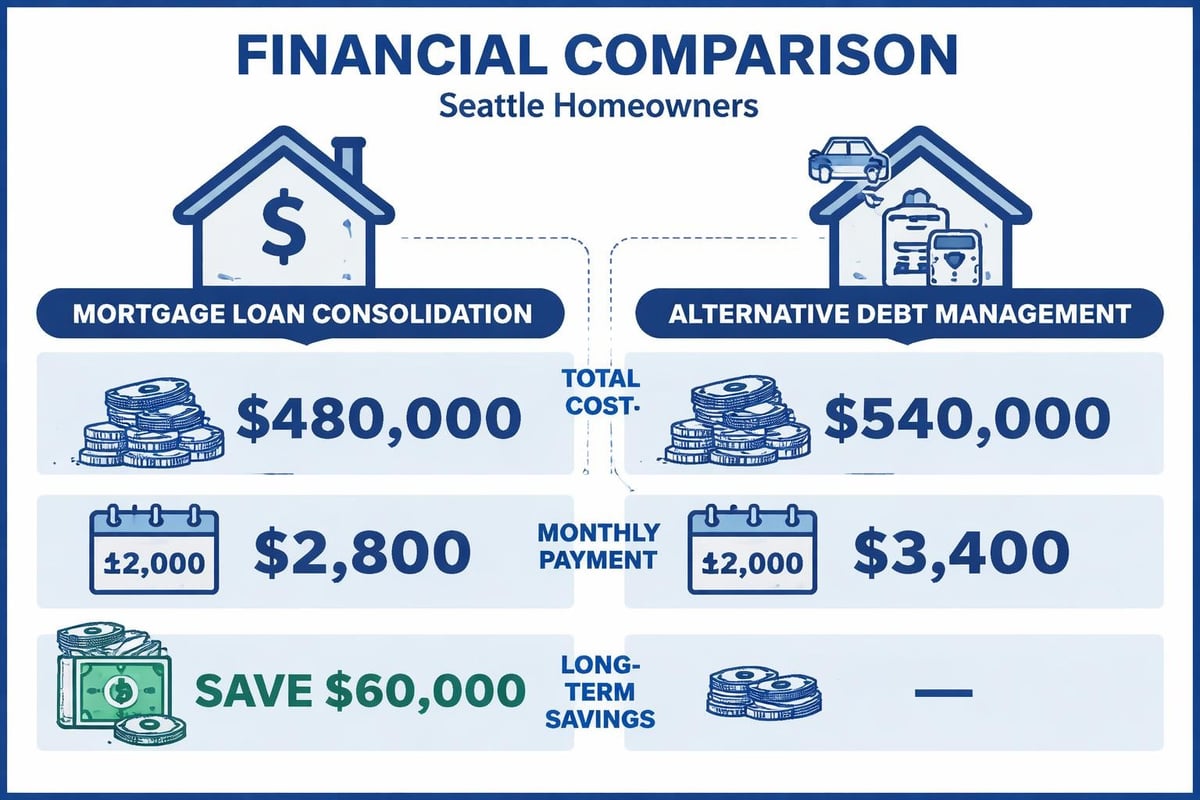

Consider the mathematical reality: mortgage rates in 2026 remain significantly lower than most consumer debt rates. When you consolidate high-interest obligations into your mortgage, you're replacing expensive debt with more affordable debt. A homeowner carrying $40,000 in credit card debt at 22% interest pays approximately $8,800 annually just in interest charges.

By incorporating that same $40,000 into a mortgage at 6.5%, the annual interest drops to roughly $2,600, creating immediate cash flow improvement. Over time, this difference can amount to tens of thousands of dollars in savings, money that can be redirected toward retirement savings, emergency funds, or investment opportunities.

| Debt Type | Typical Rate | Monthly Payment on $40K | Annual Interest |

|---|---|---|---|

| Credit Cards | 22% | $1,200+ | $8,800 |

| Personal Loans | 12% | $900 | $4,800 |

| Auto Loans | 8% | $800 | $3,200 |

| Mortgage Consolidation | 6.5% | $250 | $2,600 |

When Consolidation Makes Financial Sense

Timing plays a critical role in determining whether mortgage loan consolidation serves your best interests. Not every homeowner in every situation should pursue this strategy. The decision requires honest assessment of your financial habits, long-term goals, and current circumstances.

Ideal candidates typically carry significant high-interest debt that they can eliminate through consolidation while maintaining adequate equity cushion in their property. If you're planning to stay in your Everett or Seattle home for at least three to five years, the benefits of consolidation typically outweigh the closing costs associated with the transaction.

Warning Signs to Consider

However, certain circumstances should give you pause. If your debt accumulation stems from overspending rather than temporary circumstances, consolidation without behavioral change simply provides temporary relief. The underlying problem persists, and you risk accumulating new debt while now having less equity in your home.

Situations where consolidation may not be appropriate:

- Planning to sell your home within two years

- Unable to qualify for favorable interest rates due to credit challenges

- Insufficient equity to consolidate debts while maintaining 20% cushion

- Debt stems from ongoing overspending without budget corrections

- Closing costs exceed the interest savings you'll realize

Understanding how debt consolidation affects your mortgage helps you make informed decisions. Your debt-to-income ratio, credit utilization, and overall financial profile all shift when you pursue consolidation, impacting your ability to qualify for future financing.

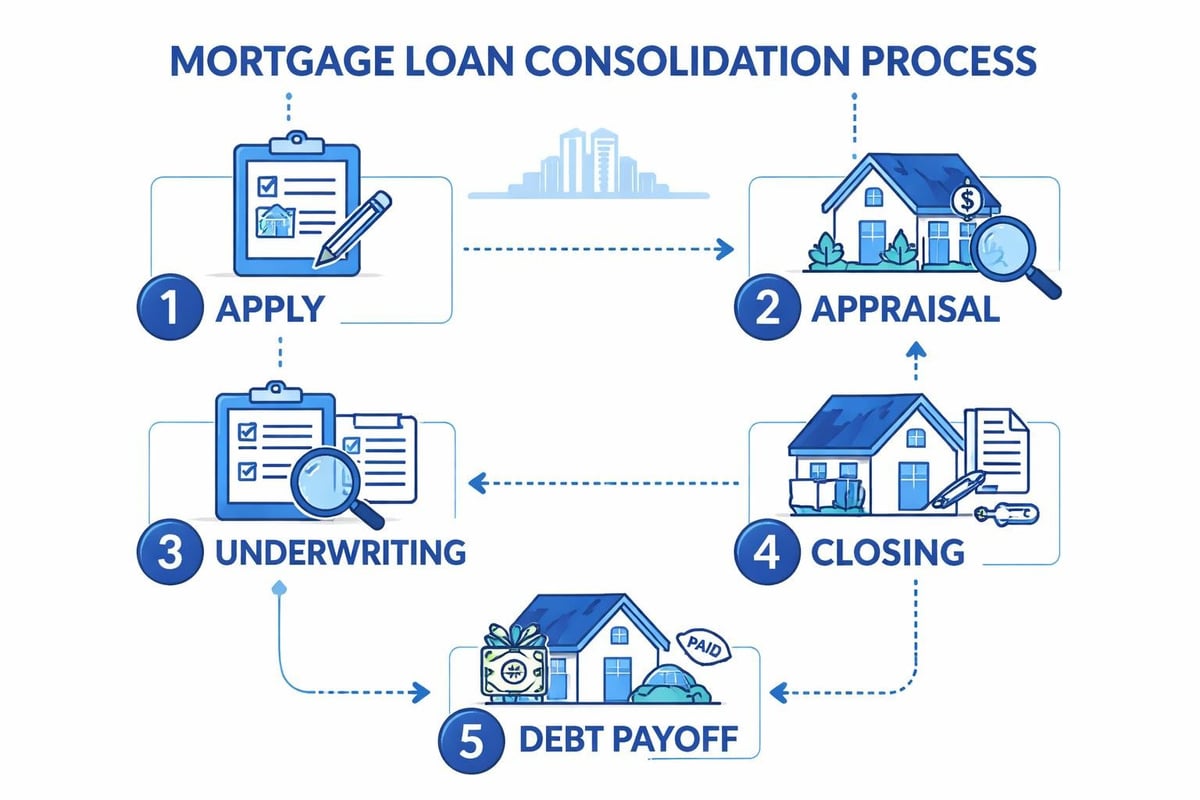

Execution Strategies for Seattle Market Conditions

Successfully implementing mortgage loan consolidation in the Seattle area requires understanding local market dynamics and working with experienced professionals who navigate these transactions regularly. The process typically takes 30 to 45 days from application to closing, though streamlined programs can reduce this timeline significantly.

Your first step involves accurate assessment of your current debts and home value. Gather statements for all obligations you want to consolidate, including current balances, interest rates, and minimum payments. In rapidly appreciating markets like Redmond and Bellevue, your home may be worth considerably more than you realize, providing additional consolidation capacity.

Working with Local Mortgage Professionals

Selecting the right mortgage broker makes a substantial difference in your consolidation outcome. Top mortgage brokers in Seattle understand how to structure these transactions to maximize benefits while minimizing costs. They can identify the optimal loan program, whether that's a cash-out refinance, home equity loan, or home equity line of credit.

Each option carries distinct advantages. Cash-out refinancing replaces your existing first mortgage with a larger loan, providing funds to pay off other debts. This approach works particularly well when current mortgage rates are favorable compared to your existing rate. Home equity loans provide a lump sum with a separate payment, while HELOCs offer revolving credit access similar to a credit card but secured by your home.

When considering refinancing options in Seattle, factor in closing costs, which typically range from 2% to 5% of the new loan amount. A $400,000 consolidation refinance might carry $8,000 to $20,000 in closing costs. These expenses can be rolled into the new loan amount, though this increases your overall debt.

Qualifying for Consolidation with Complex Income

Tech professionals throughout the Seattle area often have compensation packages that extend beyond base salary. Stock options, restricted stock units, bonuses, and equity grants complicate income qualification but shouldn't prevent you from accessing mortgage loan consolidation when it makes financial sense.

Lenders evaluate these income sources differently. Vested RSUs with a two-year history typically qualify as stable income. Unvested stock requires different treatment, though experienced underwriters understand how to incorporate this compensation appropriately. Bonus income with a consistent two-year track record can strengthen your application substantially.

Documentation Requirements

Thorough documentation streamlines the qualification process. Beyond standard pay stubs and tax returns, consolidation applicants should prepare:

- Complete list of debts to be consolidated with account numbers and balances

- Two years of W-2s and complete tax returns

- Stock compensation statements showing vesting schedules

- Recent pay stubs reflecting all income sources

- Bank statements covering the most recent two months

- Homeowners insurance declarations page

- HOA documents if applicable

The underwriting process for jumbo loans and complex compensation requires additional scrutiny, but don't let this deter you. Proper preparation and experienced guidance ensure smooth processing even with non-traditional income sources.

Market-Specific Considerations Across Greater Seattle

Real estate markets vary significantly across the Greater Seattle region, impacting consolidation feasibility and strategy. Downtown Seattle condos face different appreciation patterns than single-family homes in Lake Forest Park. Understanding these nuances helps you determine realistic home values and available equity.

Shoreline properties have experienced robust appreciation, providing homeowners with substantial equity accumulation over recent years. This equity growth creates consolidation opportunities that may not have existed when these homeowners initially purchased. Similarly, Lynnwood's development boom has lifted property values, expanding consolidation possibilities for residents.

| City | Median Home Value (2026) | Typical Equity Available | Consolidation Potential |

|---|---|---|---|

| Seattle | $825,000 | 35-45% | High |

| Bellevue | $1,150,000 | 40-50% | Very High |

| Redmond | $975,000 | 38-48% | Very High |

| Kirkland | $1,050,000 | 40-48% | Very High |

| Shoreline | $775,000 | 32-42% | Moderate-High |

| Everett | $585,000 | 28-38% | Moderate |

Working with professionals like Wendy Dean, Esq. Realtor and Associate Broker provides valuable market insights when assessing your property's current value. Real estate professionals understand neighborhood-specific trends that influence appraisal outcomes and consolidation capacity.

Alternative Approaches and Comparison Options

While mortgage loan consolidation offers powerful benefits, it's not the only debt management strategy available to Seattle homeowners. Understanding general loan consolidation concepts provides context for evaluating whether mortgage-based consolidation or alternative approaches better serve your situation.

Balance transfer credit cards can work for smaller debt amounts if you have strong credit and can pay off balances during promotional periods. Personal consolidation loans don't require home equity but typically carry higher rates than mortgage-based solutions. Debt management programs through credit counseling agencies offer structured repayment without new borrowing.

Comparing True Costs

Effective comparison requires looking beyond interest rates to total cost over the life of the loan. A $30,000 credit card balance paid over 20 years as part of your mortgage costs more in total interest than the same balance paid off in five years through a personal loan, even if the mortgage rate is lower. The extended timeline changes the mathematics.

Run detailed scenarios comparing:

- Total interest paid across the full repayment period

- Monthly payment impact on cash flow

- Equity position after consolidation

- Tax implications of deductible versus non-deductible interest

- Closing costs amortized over expected ownership period

This comprehensive analysis reveals the true financial impact of each option, enabling informed decision-making rather than choices based solely on monthly payment reduction.

Building Long-Term Financial Strength

Successful mortgage loan consolidation extends beyond the transaction itself. The strategy only delivers lasting value when combined with improved financial habits and long-term planning. Seattle homeowners who consolidate debt but continue overspending find themselves in worse positions within a few years, now carrying both mortgage debt and newly accumulated consumer debt.

Create a realistic budget that accounts for your new consolidated payment while preventing debt reaccumulation. Consider automatic savings transfers that redirect the cash flow improvement toward emergency funds or retirement accounts. Many homeowners find that the discipline of understanding home ownership responsibilities extends naturally to broader financial management.

Monitoring Your Progress

Establish quarterly check-ins to review your financial position after consolidation. Track your mortgage balance reduction, ensure no new high-interest debt accumulation, and monitor your credit score improvement. Most homeowners see credit score increases within six to twelve months after consolidation as their credit utilization drops and payment history strengthens.

The psychological benefits of consolidation often exceed the mathematical advantages. Reduced financial stress, simplified money management, and clear progress toward debt freedom create momentum that supports continued financial improvement. This emotional component, while harder to quantify, substantially impacts long-term success.

Navigating Industry Trends and Changes

The mortgage industry continues evolving, with consolidation trends affecting lenders and borrowers alike. Understanding these broader market dynamics helps you anticipate changes in available programs, qualification requirements, and pricing.

Technology has streamlined the consolidation process significantly compared to previous years. Digital documentation, automated underwriting systems, and improved communication tools reduce the time from application to closing. Some lenders now offer consolidation refinances with closing timelines as short as nine business days for well-qualified borrowers with complete documentation.

Regulatory changes also impact the consolidation landscape. Ability-to-repay requirements, debt-to-income ratio standards, and appraisal guidelines all influence who qualifies and under what terms. Staying informed about these shifts helps you time your consolidation strategy optimally.

Current market advantages in 2026 include:

- Competitive refinance rates incentivizing consolidation

- Increased home values providing equity access

- Streamlined underwriting reducing processing time

- Expanded income qualification for tech professionals

- Enhanced digital processes improving borrower experience

Smart Implementation for Seattle Tech Professionals

Amazon, Microsoft, Google, and other major Seattle employers offer compensation packages that create unique consolidation opportunities. Stock-based compensation that vests over time provides increasing earning power that traditional underwriting sometimes undervalues. Working with mortgage professionals experienced in tech industry compensation ensures you receive full credit for your actual earning capacity.

Timing consolidation around vesting schedules can strengthen your application. Major vesting events improve your debt-to-income ratio and demonstrate income stability. Some tech professionals strategically consolidate debt immediately after significant stock vesting, using a portion of the vested equity for down payment assistance on upgrades while consolidating remaining debts.

The jumbo loan expertise required for Seattle's high-value market directly applies to consolidation scenarios. Properties exceeding conforming loan limits require lenders comfortable with larger loan amounts and more complex underwriting. This expertise becomes essential when consolidating substantial debt against high-value Kirkland or Bellevue properties.

Risk Management and Protection Strategies

While mortgage loan consolidation offers significant benefits, it does convert unsecured debt into secured debt. This fundamental shift means your home now secures obligations that previously couldn't trigger foreclosure. Understanding and managing this risk requires honest assessment and protective strategies.

Never consolidate more debt than absolutely necessary. Maintaining the largest possible equity cushion provides financial flexibility and protection against market downturns. Seattle's real estate market has shown remarkable resilience, but no market appreciates indefinitely. Protecting your equity position ensures you can weather temporary value fluctuations.

Consider these protective measures:

- Maintain emergency fund covering six months of expenses

- Secure adequate disability and life insurance

- Avoid accumulating new consumer debt post-consolidation

- Build additional equity through extra principal payments when possible

- Monitor property values and refinance opportunities

Professional Guidance Through Complex Decisions

The complexity of mortgage loan consolidation, particularly in high-value Seattle markets with tech industry compensation, makes professional guidance valuable. Experienced mortgage brokers provide analysis comparing your options, projection of long-term costs and benefits, and execution support ensuring smooth transactions.

Mortgage professionals serving Seattle understand local market conditions, property value trends, and the specific challenges facing area homeowners. This localized expertise complements broader mortgage knowledge, delivering better outcomes than generic online lenders unfamiliar with Pacific Northwest markets.

Questions to ask potential mortgage advisors include:

- How many consolidation transactions have you completed in the past year?

- What percentage of your clients have tech industry compensation?

- How do you structure deals to minimize closing costs?

- What are the qualification requirements for my specific situation?

- How does consolidation impact my ability to access equity in the future?

Comprehensive answers demonstrating deep experience and transparent communication indicate professionals worth trusting with significant financial decisions.

Mortgage loan consolidation offers Seattle homeowners a powerful strategy for reducing interest costs, simplifying payments, and building long-term financial strength. Success requires careful analysis, proper execution, and ongoing discipline to maintain the benefits you achieve. Whether you're managing credit card debt, auto loans, or other obligations alongside your mortgage, consolidation may provide the financial breathing room you need. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area homeowners navigate complex financial decisions with transparency and strategic guidance. From initial analysis through closing and beyond, we're here to help you make confident decisions about consolidation and every aspect of your mortgage journey.