Understanding about home loan options is essential for anyone looking to purchase property in the Seattle area. Whether you're a first-time buyer exploring neighborhoods in Lake Forest Park, a tech professional at Amazon or Microsoft considering a jumbo loan, or a veteran investigating your benefits, knowing what's available can dramatically impact your homeownership journey. The mortgage landscape in 2026 offers diverse pathways tailored to different financial situations, credit profiles, and property types across Seattle, Bellevue, Redmond, and surrounding communities.

What You Should Know About Home Loan Fundamentals

When educating yourself about home loan basics, start with the core components that define every mortgage: principal, interest, term length, and down payment requirements. These elements work together to determine your monthly payment, total interest paid over the life of the loan, and how quickly you build equity in your property.

The principal represents the actual amount you borrow to purchase your home. Interest is the cost of borrowing that money, expressed as an annual percentage rate (APR). Term length typically ranges from 15 to 30 years, with shorter terms resulting in higher monthly payments but significantly less interest paid overall. Down payment requirements vary dramatically depending on the loan type you select.

Key Mortgage Components to Understand

- Loan-to-value ratio (LTV): The percentage of the home's value you're financing

- Debt-to-income ratio (DTI): Your monthly debt obligations compared to gross income

- Private mortgage insurance (PMI): Required on conventional loans with less than 20% down

- Closing costs: Fees typically ranging from 2-5% of the purchase price

- Interest rate vs. APR: The nominal rate versus the true cost including fees

Understanding about home loan structures helps you make informed decisions when comparing offers from different lenders. The Consumer Financial Protection Bureau provides comprehensive tools to help you navigate these concepts and prepare for the homebuying process.

Types of Home Loans Available in the Seattle Market

The mortgage market offers several distinct loan categories, each designed for specific borrower profiles and property situations. Knowing about home loan types available in your area positions you to select the program that best aligns with your financial situation and homeownership goals.

Conventional Loans

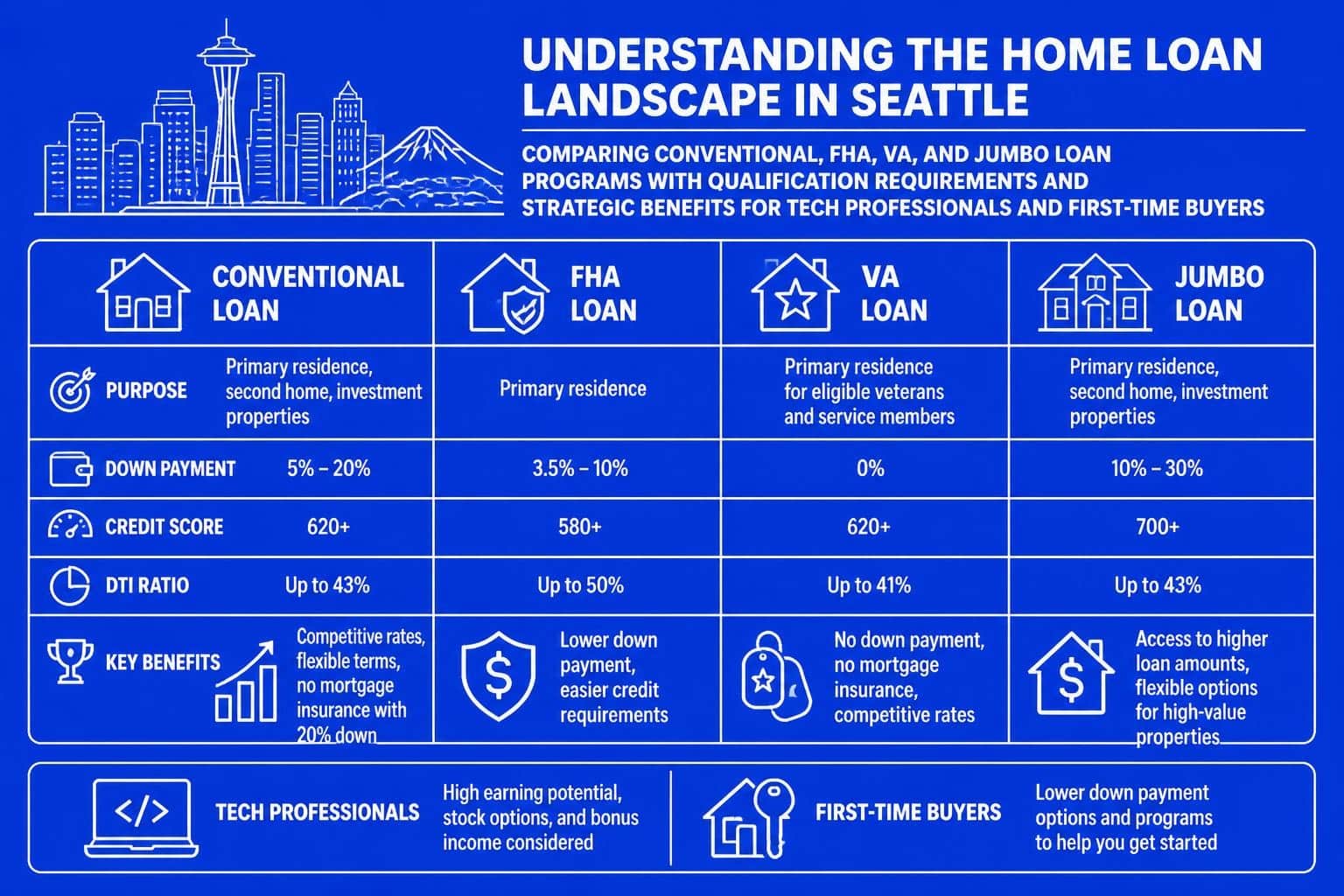

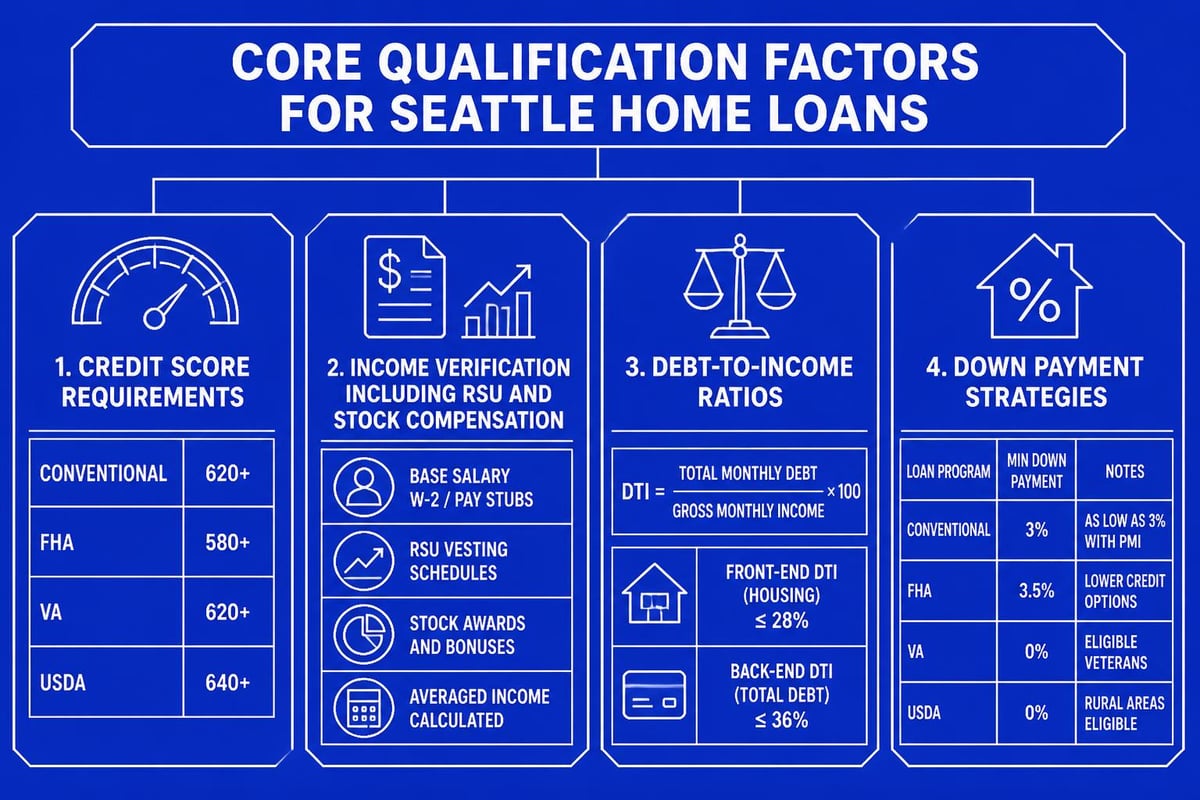

Conventional home loans represent the most common mortgage type in Seattle's competitive market. These loans aren't backed by government agencies and typically require credit scores of 620 or higher, though stronger scores unlock better rates. Down payment requirements range from 3% for first-time buyers to 20% or more for those seeking to avoid PMI.

For tech professionals in Bellevue and Redmond, conventional loans offer flexibility in qualifying alternative income sources like restricted stock units (RSUs) and performance bonuses. The key advantage lies in their adaptability and competitive rates for borrowers with strong credit profiles.

Government-Backed Programs

Government-backed loans provide accessible pathways to homeownership for specific borrower groups:

FHA Loans allow down payments as low as 3.5% with credit scores starting at 580, making them popular among first-time buyers in Shoreline and Lynnwood. These loans require both upfront and ongoing mortgage insurance premiums.

VA Loans offer zero-down financing for eligible veterans, active-duty service members, and qualifying spouses. With no PMI requirement and competitive rates, VA loans deliver substantial long-term savings for those who've served.

USDA Loans provide zero-down options for properties in eligible rural areas, though most Seattle-area properties don't qualify given the urban density.

Jumbo Loans for High-Value Properties

When property values exceed conforming loan limits-$806,500 in King County for 2026-you enter jumbo loan territory. Seattle's robust real estate market means many buyers need jumbo financing, particularly in sought-after neighborhoods throughout Seattle, Bellevue, and Kirkland.

Jumbo loans traditionally required 20% down, but innovative programs now offer 10% down jumbo options for well-qualified borrowers. These loans demand stronger credit profiles, typically 700+, and more rigorous income documentation. However, for tech professionals with substantial RSU packages, jumbo loans can unlock properties that conventional financing couldn't reach.

| Loan Type | Min. Credit Score | Min. Down Payment | PMI Required | Income Limits |

|---|---|---|---|---|

| Conventional | 620 | 3% | Yes (if <20% down) | None |

| FHA | 580 | 3.5% | Yes | None |

| VA | No minimum | 0% | No | None |

| Jumbo | 700+ | 10-20% | Sometimes | None |

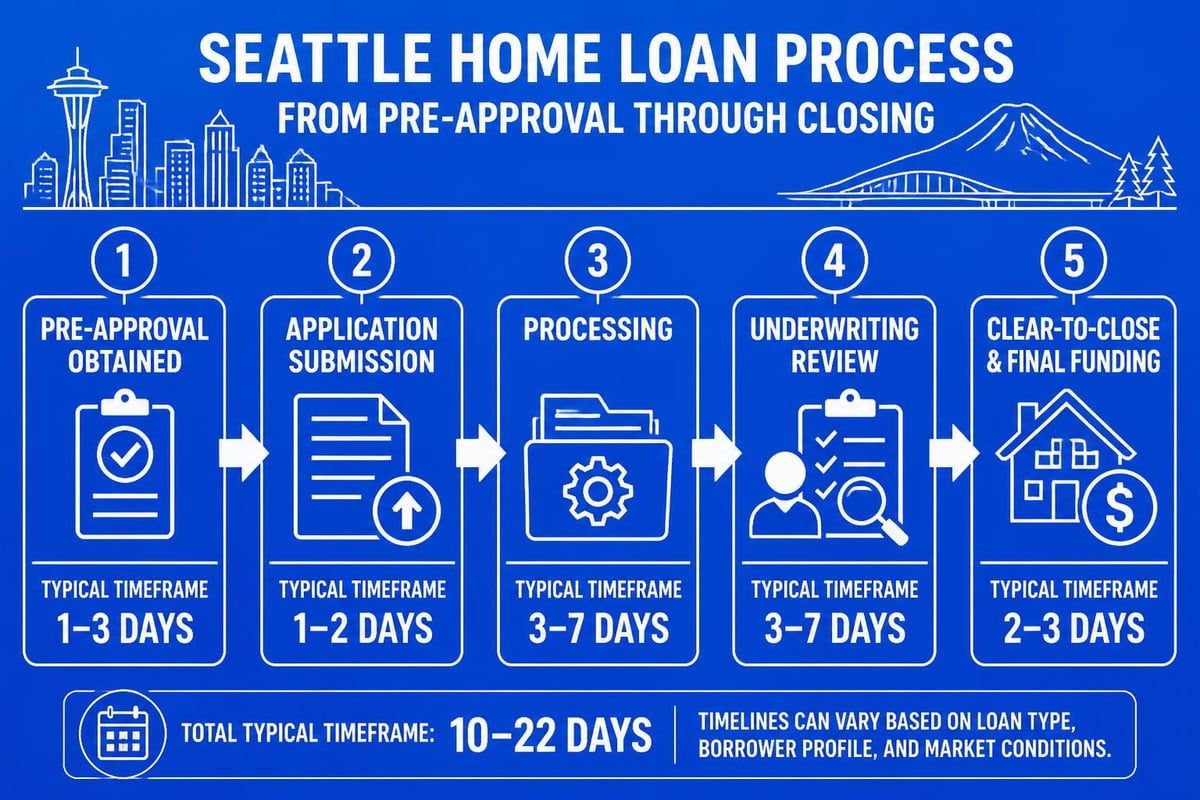

The Home Loan Application Process in Greater Seattle

Understanding about home loan application procedures helps you navigate the journey from pre-qualification to closing with confidence. The mortgage loan process involves several distinct stages, each requiring specific documentation and decision-making.

Pre-Qualification vs. Pre-Approval

Pre-qualification provides a preliminary estimate based on self-reported financial information. This informal assessment takes minutes but carries limited weight with sellers in competitive Seattle markets.

Pre-approval involves submitting documentation for verification-pay stubs, tax returns, bank statements, and credit authorization. Lenders issue a conditional commitment specifying the amount you're approved to borrow. In bidding wars common throughout Seattle neighborhoods, pre-approval letters demonstrate serious intent and financial readiness.

For tech professionals, pre-approval often requires additional documentation around RSU income qualification, including vesting schedules and historical stock performance. Working with a broker experienced in these income types streamlines the process considerably.

Documentation Requirements

- Income verification: Two years of W-2s, recent pay stubs, and tax returns

- Asset verification: Two months of bank statements for all accounts

- Credit authorization: Permission to pull your credit report

- Employment verification: Direct contact with your employer

- Additional income: Documentation for bonuses, RSUs, rental income, or side businesses

When educating yourself about home loan documentation, gather these materials early. Complete files enable faster underwriting and reduce delays that could jeopardize time-sensitive contracts in Seattle's fast-moving market.

Strategies for Seattle-Area Tech Professionals

Tech industry compensation packages present unique opportunities and challenges when learning about home loan qualification. Amazon, Microsoft, and Google employees often receive significant portions of compensation through RSUs, stock options, and performance bonuses-income sources that require specialized underwriting expertise.

Maximizing Buying Power with Stock Compensation

Restricted Stock Units (RSUs) can be used for qualification once they've vested and you have a two-year history of receiving them. Underwriters calculate a monthly average, often applying a conservative discount to account for market volatility. This means your $200,000 annual RSU package might qualify as $12,000-$15,000 in monthly income depending on vesting patterns and stock performance.

Bonus income requires a two-year history for full consideration. If you've received bonuses consistently, lenders average the amounts and include them in your qualifying income. First-year employees can't initially use bonus projections, making timing important for career transitions.

Stock options are typically not counted until exercised and sold, though some programs allow qualifying a percentage of vested options based on current market value.

Down Payment Strategies for High Earners

Many tech professionals face a paradox: high income but limited liquid savings due to wealth concentrated in company stock. Several strategies address this challenge:

- RSU liquidation planning: Coordinate vesting events with down payment needs while managing tax implications

- Gift funds: Accept documented gifts from family members to supplement savings

- Asset depletion: Some programs allow qualifying retirement account balances as income

- Lower down payment jumbo programs: Preserve liquidity by utilizing 10% down jumbo options

Understanding about home loan flexibility for tech compensation helps you structure applications that accurately reflect your financial strength while managing stock-concentrated wealth.

First-Time Buyer Considerations in Washington State

First-time homebuyers exploring about home loan options in Washington State benefit from both federal programs and state-specific resources. The Washington State Department of Financial Institutions offers guidance specifically tailored to local buyers navigating their first purchase.

Down Payment Assistance Programs

Washington State Housing Finance Commission provides down payment assistance loans that can cover 3-5% of the purchase price. These programs target moderate-income buyers purchasing in designated areas, including portions of Shoreline, Lynnwood, and Everett.

Eligibility requirements typically include:

- First-time buyer status (or no homeownership in past three years)

- Income limits based on county median income

- Completion of homebuyer education course

- Purchase of property as primary residence

- Specific credit score minimums (usually 640+)

Education and Preparation

Successful first-time buyers invest time in education before shopping. HUD-approved counseling agencies offer courses covering budgeting, loan types, the buying process, and homeownership responsibilities. Many down payment assistance programs require course completion, but the knowledge gained benefits all buyers regardless of assistance.

The Consumer Financial Protection Bureau’s toolkit provides step-by-step guidance through each phase, helping you understand what's ahead and prepare accordingly.

Interest Rates and Market Conditions in 2026

When researching about home loan costs, interest rates represent the most significant long-term expense factor. Rates fluctuate based on Federal Reserve policy, inflation expectations, bond market performance, and your individual credit profile.

Factors Affecting Your Interest Rate

Credit score impact: The difference between a 680 and 780 credit score can mean 0.5-0.75% in rate differential-translating to tens of thousands of dollars over a 30-year term. Review your credit report months before applying to address errors and optimize your score.

Loan-to-value ratio: Higher down payments signal lower risk, earning better rates. The 20% threshold matters significantly, both for avoiding PMI and securing optimal pricing.

Loan type and term: Government-backed loans like FHA often carry slightly higher rates than conventional loans for well-qualified borrowers. Shorter terms (15-year) offer substantially lower rates than 30-year mortgages.

Property type and use: Primary residences earn better rates than investment properties or second homes. Single-family homes typically beat condos and multifamily properties.

Rate Locks and Timing

Once you've learned about home loan rates and found a property, you'll need to decide when to lock your rate. Rate locks guarantee a specific rate for a defined period, typically 30-60 days. In rising rate environments, locking early protects you. When rates are falling, float strategies with lock options preserve flexibility.

| Lock Period | Typical Cost | Best For |

|---|---|---|

| 30 days | Standard rate | Quick closes, cash buyers |

| 45 days | +0.125% | Standard financed purchases |

| 60 days | +0.250% | New construction, complex transactions |

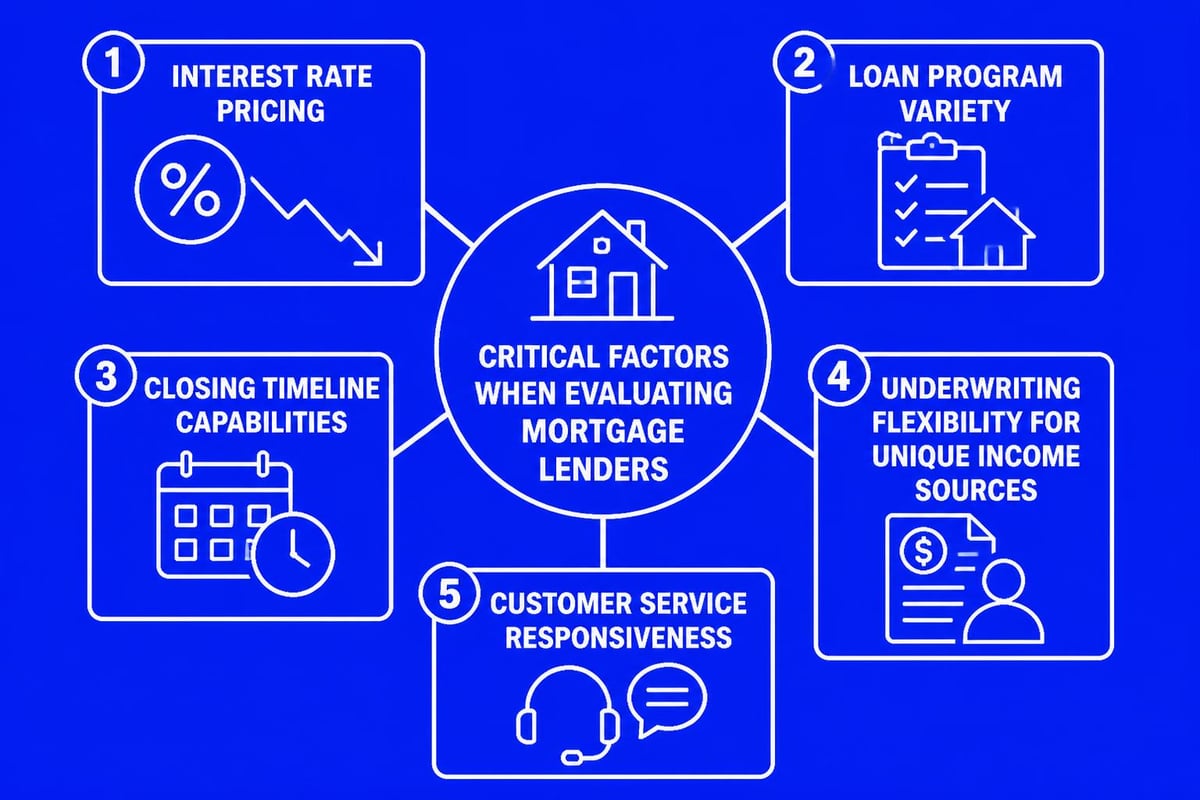

Comparing Lenders and Choosing Your Mortgage Partner

Understanding about home loan lender options helps you select a partner who'll deliver competitive terms and reliable execution. Your choices include big banks, credit unions, online lenders, and local mortgage brokers.

Benefits of Local Mortgage Brokers

Local brokers offer distinct advantages in Seattle's competitive market:

- Multiple lender access: Brokers submit your application to various lenders, finding the best fit for your specific situation

- Local market expertise: Understanding Seattle neighborhoods, appraisal challenges, and competitive offer strategies

- Specialized programs: Access to niche products like low-down jumbo loans and alternative income qualifying

- Personalized service: Direct communication with a licensed professional throughout the process

National banks provide brand recognition and potential relationship benefits, but often lack flexibility in underwriting unique income situations common among Seattle tech professionals. Choosing a local lender who understands RSU qualification and fast-close requirements can make the difference in competitive scenarios.

Special Situations and Advanced Strategies

As you expand your knowledge about home loan possibilities, several specialized scenarios and strategies merit consideration depending on your circumstances.

Mortgage Recasting for Recent Buyers

If you've recently purchased and come into additional funds-perhaps through an inheritance, RSU vesting, or bonus-mortgage recasting allows you to make a lump-sum principal payment and re-amortize your loan. This reduces your monthly payment without the cost and credit impact of refinancing.

Recasting works particularly well when:

- Current interest rates exceed your existing rate

- You want to reduce monthly obligations without extending your term

- You've received a windfall but want to maintain your current loan structure

- You're trying to improve cash flow while building equity faster

Investment Property Financing

Investment property loans require larger down payments (typically 20-25%), higher credit scores, and demonstrate rental income potential. Understanding about home loan requirements for non-owner-occupied properties helps real estate investors structure their portfolios effectively.

Bridge Loans and Contingent Offers

In scenarios where you're selling one property to purchase another, bridge loans provide short-term financing until your current home sells. These allow non-contingent offers that compete more effectively in Seattle's market, though they carry higher rates and fees due to their temporary nature.

Common Mistakes to Avoid

Learning about home loan pitfalls helps you sidestep costly errors during your homebuying journey:

- Major purchases on credit: Financing cars or furniture before closing can derail approval by changing your DTI ratio

- Job changes: Switching employers, especially to commission-based roles, complicates income verification

- Undisclosed debts: All obligations appear on your credit report-attempting to hide them damages credibility

- Minimal shopping: Comparing just one or two lenders means potentially missing better terms

- Inadequate reserves: Having only enough for down payment and closing costs leaves no cushion for unexpected expenses or appraisal gaps

Educating yourself about home loan processes includes understanding these common missteps. The important steps when buying a home cover preparation strategies that help avoid these problems.

Closing Process and Final Steps

The closing phase represents the culmination of your home loan journey. Three to five days before closing, you'll receive a Closing Disclosure detailing all final loan terms, costs, and cash requirements. Review this document carefully, comparing it to your initial Loan Estimate to identify any unexpected changes.

What Happens at Closing

During the closing appointment, you'll:

- Sign the promissory note committing you to repay the loan

- Execute the deed of trust securing the property as collateral

- Review and sign the closing disclosure acknowledging all costs

- Provide certified funds for your down payment and closing costs

- Receive keys and official ownership of your new home

In Washington State, closings typically involve a title company or escrow officer who coordinates document signing, funds disbursement, and title transfer. The entire process usually takes 60-90 minutes.

Timeline Expectations for Seattle Buyers

Working with an experienced broker and responsive lender, Seattle buyers can close in as few as 9-14 business days on straightforward purchases. More complex scenarios-new construction, multiple income sources, or unique properties-may require 30-45 days from contract to closing.

Understanding about home loan timelines helps you structure competitive offers with realistic closing dates that you can confidently meet. Sellers favor buyers who demonstrate knowledge and preparation over those requesting unnecessarily long contingency periods.

Ongoing Education and Market Awareness

The mortgage landscape evolves continuously with regulatory changes, new product offerings, and shifting market conditions. Staying informed about home loan developments helps you recognize opportunities for refinancing, accessing equity, or improving your mortgage structure as your situation changes.

Key areas to monitor include:

- Conforming loan limits: Updated annually, affecting the conventional-to-jumbo threshold

- Interest rate trends: Influencing refinance opportunities and market timing

- Program changes: New assistance programs or modified qualifying requirements

- Local market conditions: Affecting negotiating power and offer strategies

- Tax law updates: Impacting mortgage interest deductibility and property tax considerations

Resources like the types of home loans available provide updated information as programs evolve and new options emerge.

Regional Considerations Across Greater Seattle

While learning about home loan options broadly, recognize that different communities within the Seattle area present unique characteristics affecting your financing approach.

Seattle proper features higher median prices, particularly in desirable neighborhoods, often requiring jumbo financing. Competitive markets demand strong pre-approvals and quick closing capabilities.

Bellevue and Redmond concentrate tech professionals, making specialized RSU qualifying expertise essential. Properties here frequently exceed conforming limits, emphasizing jumbo loan access.

Shoreline and Lake Forest Park offer more accessible entry points for first-time buyers while maintaining excellent school access and Seattle proximity. Financing options in Lake Forest Park often include conventional programs with moderate down payments.

Lynnwood and Everett provide additional affordability while keeping commute times reasonable. These areas see strong FHA and conventional loan activity with various down payment levels.

Understanding about home loan applications across these distinct markets helps you tailor your approach to the specific community you're targeting, whether that means emphasizing quick-close capabilities in competitive Seattle neighborhoods or exploring first-time buyer programs in more accessible areas.

Making informed decisions about home loan options requires understanding the products available, qualification requirements, and strategies that align with your specific financial situation. Whether you're a first-time buyer in Shoreline, a tech professional considering a jumbo loan in Bellevue, or a veteran exploring VA benefits in Seattle, the right guidance makes all the difference. Keith Akada brings 25+ years of experience helping Greater Seattle homebuyers navigate these decisions with clarity and confidence, specializing in complex income situations and competitive market execution. Discover how Mortgage Reel can help you secure the right financing for your homeownership goals.