An FHA mortgage continues to serve as one of the most accessible pathways to homeownership for buyers throughout the Seattle area. Backed by the Federal Housing Administration, this government-insured loan program enables qualified borrowers to purchase homes with down payments as low as 3.5% and more flexible credit standards than conventional financing. For first-time buyers navigating competitive markets in Seattle, Bellevue, Redmond, and Kirkland, understanding how this loan type works can make the difference between remaining on the sidelines and successfully closing on a property. Tech professionals, families, and move-up buyers across the Puget Sound region regularly use this financing option to achieve their homeownership goals.

Understanding the FHA Mortgage Framework

The FHA mortgage program was established in 1934 to expand homeownership opportunities for Americans who might not qualify for traditional bank financing. Rather than lending money directly, the Federal Housing Administration insures loans made by approved lenders, which reduces risk and allows those lenders to offer more favorable terms to borrowers.

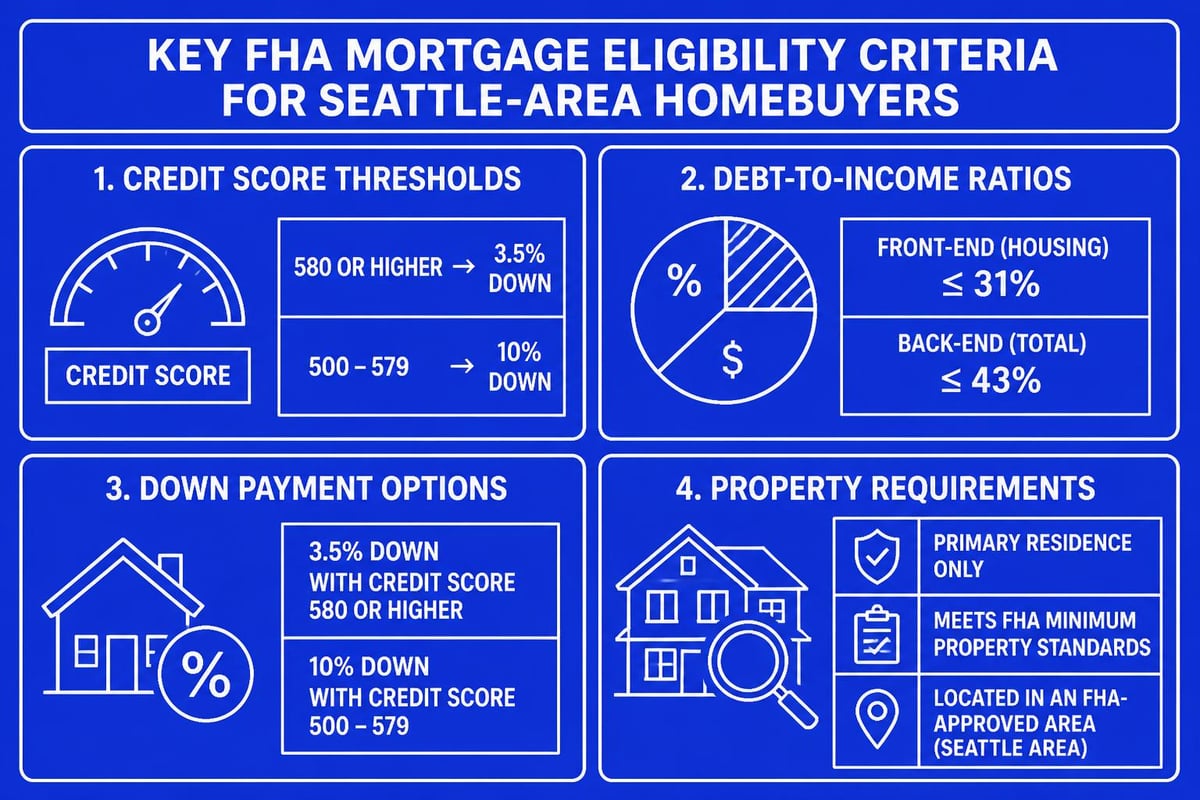

This insurance structure creates several distinct advantages for borrowers. Lenders feel protected against default, which translates into lower down payment requirements and more lenient credit score thresholds. The program accepts credit scores as low as 580 for the minimum 3.5% down payment, and borrowers with scores between 500 and 579 may still qualify with a 10% down payment.

Core Eligibility Requirements

Meeting FHA mortgage qualification standards involves several key criteria. Borrowers must demonstrate steady employment history, typically for at least two years in the same field. Income documentation requirements mirror conventional loans, though the program offers flexibility for those with non-traditional income sources.

Primary qualification factors include:

- Credit score minimum of 580 for 3.5% down payment

- Debt-to-income ratio typically not exceeding 43%

- Property must be primary residence

- Borrower must have valid Social Security number and lawful U.S. residency

- Property must meet FHA appraisal standards

The property itself must meet specific safety, security, and structural standards established by the FHA. Understanding how FHA loans work provides essential context for evaluating whether this financing matches your homebuying strategy.

Down Payment Options and Savings Strategies

One of the most compelling features of an FHA mortgage is the low down payment requirement. The standard 3.5% minimum down payment significantly reduces the cash needed to close compared to conventional financing that typically requires 5% to 20% down.

For a $600,000 home in Shoreline, the FHA down payment would be $21,000, compared to $30,000 for a conventional loan with 5% down or $120,000 for the traditional 20% down payment. This difference allows buyers to preserve cash reserves for moving expenses, home improvements, or emergency savings.

Gift Funds and Down Payment Assistance

The FHA program allows buyers to use gift funds from family members, employers, or charitable organizations to cover the entire down payment and closing costs. This flexibility proves particularly valuable for first-time buyers who may have strong income but limited savings.

Acceptable gift fund sources:

- Family members (parents, grandparents, siblings, spouse)

- Employer assistance programs

- Labor unions or close friends with demonstrated interest

- Charitable organizations

- Government agencies offering down payment assistance

Washington State and King County offer various down payment assistance programs that combine effectively with FHA financing. Many first-time buyers in Seattle utilize these layered strategies to minimize out-of-pocket costs while maintaining mortgage affordability.

Mortgage Insurance Requirements

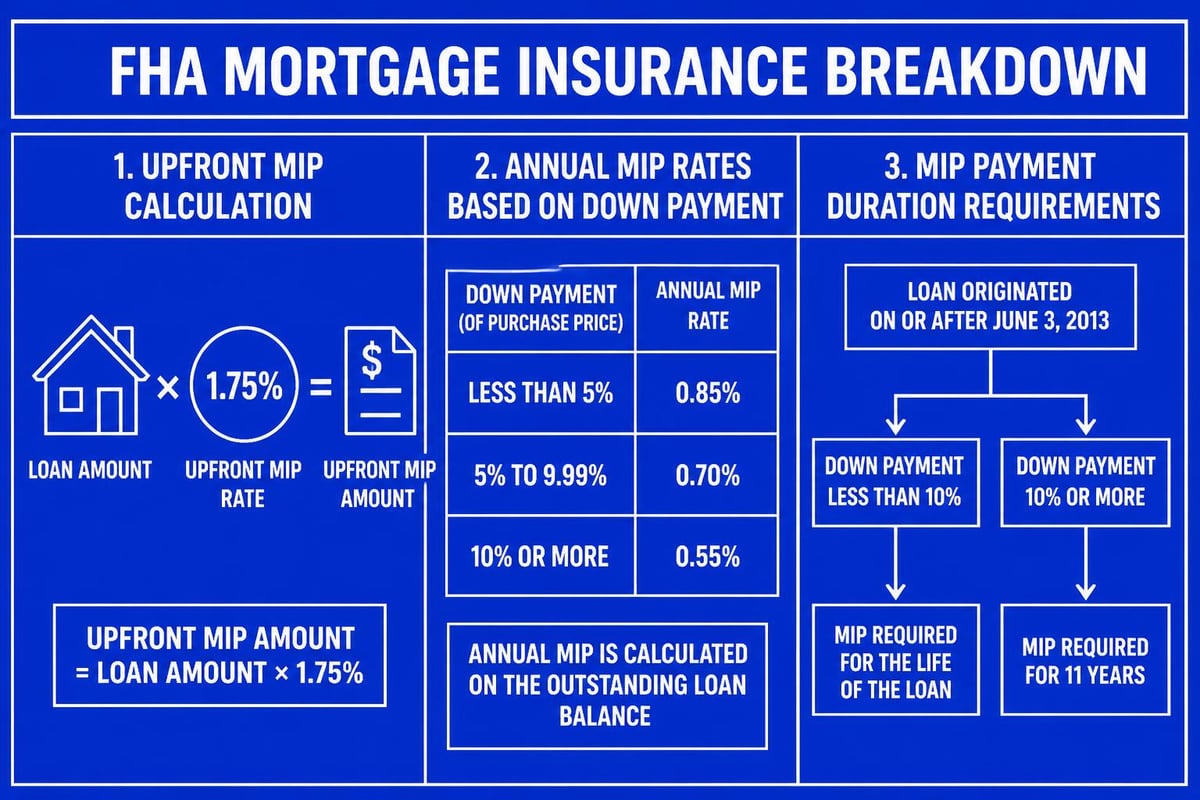

Unlike conventional loans that allow borrowers to avoid private mortgage insurance with 20% down, FHA mortgages require mortgage insurance regardless of down payment size. This insurance protects lenders against default and consists of two components: an upfront mortgage insurance premium and annual mortgage insurance.

The upfront premium equals 1.75% of the loan amount and is typically rolled into the mortgage balance rather than paid at closing. For a $575,000 loan, this amounts to approximately $10,063 added to your principal.

| Down Payment | Annual MIP Rate | MIP Duration |

|---|---|---|

| Less than 5% | 0.85% | Loan lifetime |

| 5% to 10% | 0.80% | Loan lifetime |

| 10% or more (30-year) | 0.80% | 11 years |

| 10% or more (15-year) | 0.45% | 11 years |

Annual mortgage insurance premiums are divided into monthly payments. For most buyers putting down 3.5%, the annual premium of 0.85% translates to approximately $407 per month on a $575,000 loan. This adds to the monthly housing expense but enables homeownership years earlier than saving for a larger down payment.

FHA Loan Limits in the Seattle Market

The Department of Housing and Urban Development adjusts FHA mortgage limits annually based on median home prices in each county. For 2026, King County's FHA loan limit stands at $822,375 for single-family homes, reflecting the area's high-cost housing market status.

This limit applies to most Seattle neighborhoods, Bellevue, Redmond, and Kirkland. Snohomish County carries the same limit, covering Lynnwood, Mill Creek, and Everett. These thresholds accommodate a significant portion of the local housing inventory, though buyers targeting properties above these limits must explore jumbo loan options.

Working Within Loan Limits

For properties priced above the FHA limit, buyers have several strategic options. Increasing the down payment to bring the loan amount within limits maintains FHA eligibility. Alternatively, transitioning to a conventional loan or jumbo financing may provide better overall terms for higher-priced homes.

Tech professionals with stock compensation or bonus income working at Amazon, Microsoft, or Google often benefit from conventional financing once their total compensation and savings reach certain thresholds. Evaluating conventional loan alternatives alongside FHA options ensures optimal financing for your specific situation.

Comparing FHA to Conventional Financing

Deciding between an FHA mortgage and conventional financing requires analyzing your complete financial picture, including credit profile, available savings, and long-term homeownership plans. Each loan type offers distinct advantages depending on your circumstances.

FHA mortgage advantages:

- Lower down payment (3.5% vs. 5% minimum conventional)

- More flexible credit requirements

- Higher debt-to-income ratio tolerance

- Easier qualification after bankruptcy or foreclosure

- Streamlined refinance options for rate reduction

Conventional loan advantages:

- No mortgage insurance with 20% down

- Removable mortgage insurance at 20% equity

- Higher loan limits (conforming limit of $806,500 in 2026)

- Lower overall costs for borrowers with excellent credit

- More property type flexibility

The comparison between FHA and conventional mortgages highlights how borrower qualifications drive the optimal choice. Buyers with credit scores above 740 and sufficient savings for 10-20% down often find conventional financing more cost-effective long-term, while those with lower scores or limited savings benefit from FHA accessibility.

Property Requirements and Appraisal Standards

Every property financed with an FHA mortgage must meet minimum property standards established by HUD. These requirements ensure the home is safe, sound, and secure for occupancy. The FHA appraisal process examines both property value and condition.

Appraisers evaluate structural integrity, roofing condition, electrical and plumbing systems, foundation stability, and potential safety hazards. Properties must have adequate heating, functioning utilities, and safe access. Any issues affecting safety, soundness, or structural integrity must be addressed before loan approval.

Common Appraisal Issues in Seattle-Area Homes

Older homes throughout Seattle, Lake Forest Park, and surrounding neighborhoods occasionally encounter FHA appraisal challenges. Common issues include:

- Peeling exterior paint on homes built before 1978 (lead-based paint concern)

- Missing handrails on stairs or decks

- Exposed electrical wiring or outdated electrical panels

- Roof damage or insufficient remaining lifespan

- Foundation cracks or moisture intrusion

- Non-functioning major systems

Sellers must complete required repairs before closing, or buyers can negotiate repair credits and complete work post-closing when permitted. Working with experienced real estate agents familiar with FHA requirements helps identify potential issues during home search and prevents delays during the transaction.

Credit Score Considerations and Improvement Strategies

While the FHA mortgage program accepts credit scores as low as 580, higher scores unlock better interest rates and overall loan terms. Understanding how credit impacts your mortgage rate helps buyers make strategic decisions about timing their home purchase.

Borrowers with scores between 580 and 620 face higher interest rates and more stringent income verification. Those with scores above 680 typically receive pricing similar to conventional borrowers. For buyers in Bellevue or Redmond with borderline credit, dedicating several months to credit improvement can save thousands over the loan's lifetime.

Rapid Credit Improvement Techniques

Several strategies can boost credit scores relatively quickly before applying for an FHA mortgage. Paying down credit card balances below 30% utilization provides immediate benefit. Correcting errors on credit reports through disputes with bureaus removes inaccurate negative items.

Becoming an authorized user on a family member's established credit card with perfect payment history adds positive trade lines. Avoiding new credit applications during the mortgage process prevents hard inquiries that temporarily lower scores. Strategic planning with a knowledgeable Seattle mortgage broker ensures credit optimization aligns with your purchase timeline.

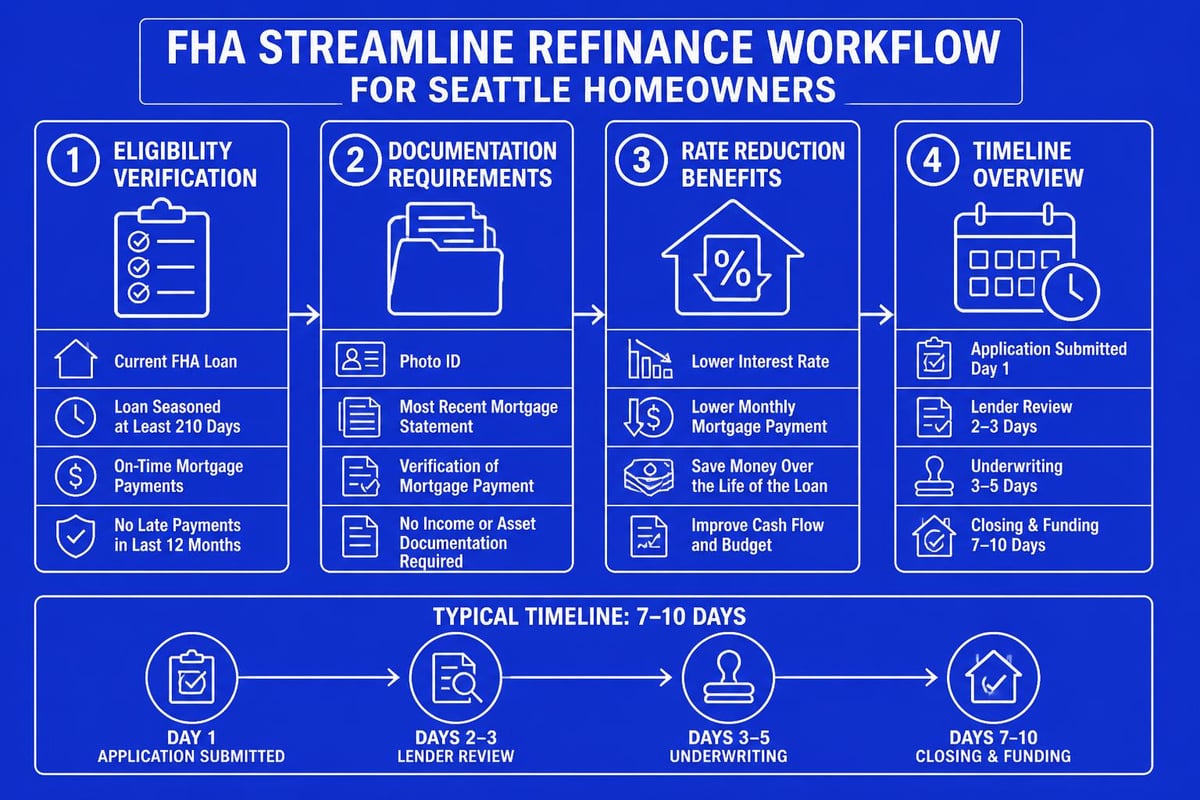

FHA Streamline Refinance Benefits

Current FHA mortgage holders gain access to the FHA Streamline Refinance program, which simplifies rate reduction without requiring full income verification or home appraisal. This program enables borrowers to lower monthly payments or switch from adjustable to fixed-rate financing with minimal documentation.

Streamline refinances require no cash out, maintain FHA insurance, and demonstrate a tangible benefit to the borrower through lower payments or increased stability. The simplified process often closes faster than traditional refinances, and reduced documentation requirements appeal to self-employed borrowers or those with variable income.

Qualification requires current FHA mortgage seasoning of at least 210 days, on-time payment history for the previous six months, and demonstration of net tangible benefit. Borrowers must have made at least six monthly payments and experienced at least six months since closing the original loan.

Closing Costs and Seller Concessions

FHA mortgages permit sellers to contribute up to 6% of the purchase price toward buyer closing costs, compared to 3% on conventional loans. This flexibility proves valuable in balanced or buyer-favorable markets where sellers accept concession requests.

Typical closing costs on an FHA mortgage include origination fees, appraisal, credit report, title insurance, escrow fees, prepaid property taxes, and homeowners insurance. Total costs typically range from 2% to 5% of the purchase price, though this varies by property location and transaction specifics.

Common closing cost components:

- Origination and processing fees: 0.5% to 1% of loan amount

- FHA appraisal: $500 to $700

- Title and escrow fees: $1,000 to $2,500

- Prepaid property taxes and insurance: varies by closing date

- Recording fees and transfer taxes: varies by county

- Upfront mortgage insurance premium: 1.75% of loan amount

Negotiating seller concessions reduces cash needed at closing, though buyers in competitive Seattle neighborhoods may encounter resistance during multiple-offer situations. Understanding standard practices helps set realistic expectations based on current market dynamics.

Using FHA Financing in Competitive Markets

While FHA mortgages offer accessibility advantages, sellers in competitive markets occasionally prefer conventional or cash offers due to perceived reliability concerns. Understanding these dynamics and implementing strategic approaches helps FHA buyers succeed.

The primary seller concern involves appraisal requirements and potential delays if property condition issues arise. Preemptive home inspections allow buyers to identify concerns before making offers, demonstrating seriousness and reducing contingency periods.

Obtaining full underwriting approval before making offers-rather than simple preapproval-strengthens your position significantly. This process verifies income, assets, and credit through complete documentation review, leaving only property appraisal and final verification before closing. Reducing approval timeline uncertainty makes FHA offers more attractive to sellers evaluating multiple bids.

Letter Strength and Communication

Including personal letters explaining your homebuying journey and connection to the neighborhood creates emotional appeal. Demonstrating financial strength through substantial reserves beyond minimum requirements reassures sellers about transaction completion.

Working with experienced buyer's agents who effectively communicate financing strength to listing agents levels the playing field. Clear explanation of FHA advantages-including higher seller concession limits and reliable closing timelines-reframes perceptions and positions offers competitively.

Tax Benefits and Long-Term Financial Planning

FHA mortgage interest remains tax-deductible for most borrowers who itemize deductions, providing annual tax savings that reduce true ownership costs. Mortgage interest deductibility combined with property tax deductions often makes homeownership more affordable than renting, particularly in high-cost areas like Seattle and surrounding communities.

Building equity through monthly principal payments creates forced savings and long-term wealth accumulation. Even with mortgage insurance costs, understanding the complete financial picture demonstrates how strategic FHA financing accelerates wealth building compared to extended renting while saving for larger down payments.

Homeowners gain stability through fixed housing costs (with fixed-rate mortgages) while rental rates continue climbing annually. The equity buildup and appreciation potential in Seattle-area markets historically outpaces mortgage costs, creating positive net worth impact over time.

Special Programs for First-Time Buyers

First-time homebuyers receive particular advantages within the FHA mortgage framework. The program defines first-time buyers as anyone who hasn't owned a primary residence within the previous three years, creating opportunities for returning buyers after life transitions.

Washington State Housing Finance Commission offers down payment assistance programs specifically designed to layer with FHA financing. These programs provide forgivable loans or deferred-payment second mortgages covering down payment and closing costs, sometimes requiring zero money down from the borrower.

Homebuyer education courses, often required for down payment assistance programs, provide valuable knowledge about budgeting, home maintenance, and avoiding foreclosure. These courses strengthen long-term success rates and empower buyers with confidence throughout the homeownership journey. Exploring options through specialized first-time buyer resources ensures access to all available programs and benefits.

Common Misconceptions About FHA Financing

Several persistent myths surround FHA mortgages that prevent qualified buyers from considering this valuable financing option. Clarifying these misconceptions helps buyers make informed decisions based on facts rather than outdated information.

Myth: FHA is only for low-income buyers

Reality: No income limits apply to FHA mortgages. High earners frequently use FHA financing strategically to minimize down payment and preserve capital for other investments or opportunities.

Myth: Sellers won't accept FHA offers

Reality: While some sellers in extremely competitive markets prefer conventional financing, most accept FHA offers, particularly when buyers demonstrate strong financial profiles and quick closing capabilities.

Myth: FHA homes must be in poor condition

Reality: FHA property standards ensure safe, sound homes. Many newer homes and well-maintained properties throughout Seattle easily meet requirements.

Myth: You can't refinance to conventional later

Reality: Homeowners can refinance from FHA to conventional financing once they reach 20% equity, eliminating mortgage insurance and potentially reducing monthly payments.

Understanding the real advantages and limitations of FHA financing enables objective evaluation rather than decisions based on misinformation.

Timeline Expectations for FHA Purchase

The FHA mortgage process typically requires 30 to 45 days from application to closing, though expedited timelines are possible with experienced lenders and cooperative parties. Understanding each phase helps buyers set realistic expectations and plan accordingly.

Initial preapproval takes 24 to 48 hours with complete documentation. Once under contract, the formal application triggers underwriting, which reviews income, assets, credit, and property details. FHA appraisal scheduling and completion requires seven to fourteen days depending on appraiser availability.

Underwriting review and conditional approval typically occurs within five to seven business days after receiving the complete application and appraisal. Clearing conditions-providing additional documentation or explanations-requires two to five days depending on complexity and borrower responsiveness.

Final approval and clear-to-close status arrives three to five days before scheduled closing. This timeline allows title company preparation, final verification, and coordination of all closing participants. Experienced lenders with efficient processing systems sometimes achieve faster timelines while maintaining quality and accuracy.

Working with Stock Compensation and Variable Income

Tech professionals throughout Seattle working at Amazon, Microsoft, Google, and other major employers often receive significant compensation through restricted stock units, stock options, and performance bonuses. Qualifying this income for FHA mortgages requires specific documentation and calculation methodologies.

Lenders typically average two years of bonus and stock compensation to establish reliable income figures for qualifying purposes. Recent grants with vesting schedules require careful analysis to determine usable income. The consistent receipt history and likelihood of continuation influence how much income underwriters count toward qualification.

For buyers with substantial stock compensation, the FHA loan limit sometimes constrains purchase power despite strong income. In these situations, transitioning to conventional or jumbo financing may unlock higher borrowing capacity. Evaluating multiple scenarios ensures optimal financing structure aligned with your complete compensation package and homeownership goals.

Portfolio Strategy and Investment Property Considerations

While FHA mortgages require borrowers to occupy the property as their primary residence, strategic buyers use this financing to enter real estate investment. Purchasing a multi-unit property (duplex, triplex, or fourplex) with FHA financing allows owner-occupancy of one unit while renting others.

Rental income from non-occupied units can count toward qualifying income, increasing overall buying power. This strategy, called "house hacking," enables buyers to build equity, generate rental income, and establish real estate investment portfolios with minimal down payment.

After occupying an FHA-financed property for at least one year, borrowers can rent it out and purchase another primary residence with new FHA financing. This allows portfolio building while maintaining FHA accessibility, though buyers should consult with tax professionals about investment property implications and reporting requirements.

Regional Market Considerations Across Greater Seattle

FHA mortgage utilization varies across Seattle-area submarkets based on price points, inventory characteristics, and buyer demographics. Understanding these patterns helps set realistic expectations for different neighborhoods and communities.

Mill Creek and Lynnwood feature more homes within FHA loan limits compared to downtown Seattle or Bellevue's Bridle Trails neighborhood. First-time buyers often target these areas for better affordability while maintaining access to employment centers and quality schools.

Everett and Lake Forest Park present strong opportunities for FHA buyers seeking single-family homes with yards and community amenities. These markets typically see less intense competition than Seattle proper, allowing buyers more time for due diligence and negotiation flexibility.

Working with professionals who understand neighborhood-specific dynamics and local market conditions optimizes strategy development and successful outcomes across diverse Greater Seattle communities.

An FHA mortgage provides accessible, flexible financing that helps qualified buyers achieve homeownership throughout the Seattle area despite challenging affordability and competitive market conditions. Understanding program requirements, strategic advantages, and proper implementation ensures optimal outcomes aligned with your financial goals. Whether you're a first-time buyer in Shoreline, a tech professional in Bellevue, or a move-up buyer in Kirkland, Keith Akada brings 25+ years of expertise and 750+ five-star reviews to guide your financing strategy with transparency and proven execution-connect with Mortgage Reel to explore your FHA mortgage options today.