Navigating the Seattle housing market in 2026 requires strategic planning, especially when competing for homes in high-demand neighborhoods across Seattle, Bellevue, Redmond, and Kirkland. Understanding mortgage broker how to strategies empowers homebuyers to make informed decisions throughout the financing process. Whether you're a first-time buyer in Lake Forest Park or a tech professional qualifying stock compensation for a jumbo loan, knowing how to effectively work with a mortgage broker can mean the difference between missing opportunities and securing your ideal home with confidence.

Understanding What a Mortgage Broker Does

A mortgage broker acts as an intermediary between borrowers and multiple lending institutions, providing access to loan programs that individual banks may not offer. Unlike loan officers who work for a single lender, mortgage brokers compare options from numerous sources to find competitive rates and terms that match your specific financial situation.

The Broker's Role in Your Home Financing Journey

Mortgage brokers perform several critical functions:

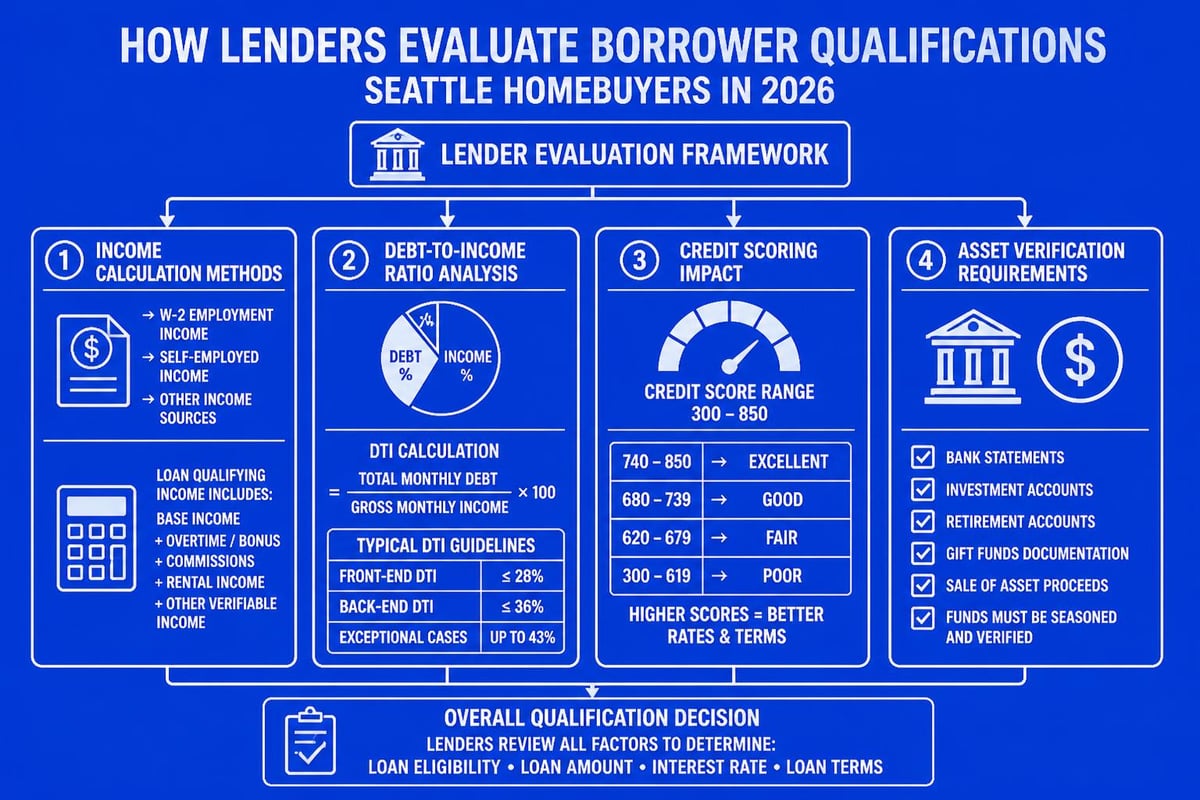

- Analyze your financial profile including income, credit, assets, and employment history

- Access wholesale lending rates often unavailable directly to consumers

- Navigate complex income scenarios such as RSUs, bonuses, and commission structures

- Coordinate with underwriters, processors, and title companies throughout closing

- Provide transparency about costs, timelines, and potential obstacles

For Seattle-area tech professionals working at Amazon, Microsoft, or Google, this expertise becomes particularly valuable when qualifying RSU income for mortgage purposes. Stock compensation requires specialized knowledge of how underwriters evaluate vesting schedules, tax implications, and income stability.

Mortgage Broker How To: Finding the Right Professional

The process of selecting a qualified mortgage broker begins with research and verification. Not all brokers offer the same level of expertise, particularly in specialized markets like Seattle where jumbo loans and tech income qualification require advanced knowledge.

Key Credentials and Qualifications

| Credential | Why It Matters | How to Verify |

|---|---|---|

| NMLS License | Required federal registration | Search at nmlsconsumeraccess.org |

| State Licensing | Washington-specific authorization | Check DFI database |

| Lender Relationships | Access to diverse loan products | Ask for lender list |

| Market Experience | Local knowledge and expertise | Review client testimonials |

| Closing Speed | Competitive advantage | Request average timeline data |

When researching potential brokers, prioritize these factors:

- Years of experience in your specific market area (Seattle, Shoreline, Lynnwood)

- Volume of loans closed annually, indicating active practice

- Specialization in your loan type (conventional, jumbo, FHA, VA)

- Client reviews across multiple platforms showing consistent service quality

- Communication style that matches your preferences and needs

A Seattle mortgage broker with 750+ five-star reviews demonstrates proven reliability and client satisfaction across diverse financing scenarios.

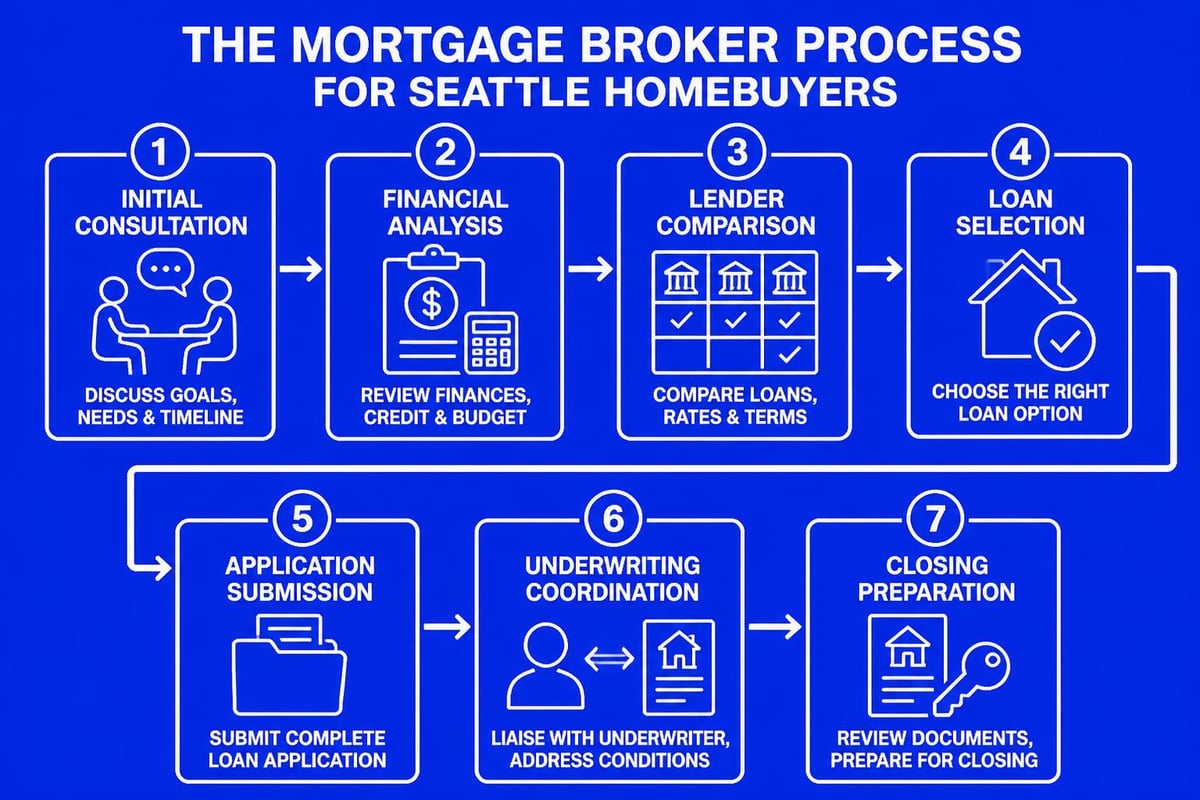

How To Prepare for Your Initial Broker Consultation

Preparation significantly impacts the quality of guidance you receive. Arriving with organized documentation allows brokers to provide accurate preliminary qualification and realistic expectations for your home search in competitive neighborhoods from Capitol Hill to Mill Creek.

Essential Documentation Checklist

Income Verification:

- Two years of W-2 forms or tax returns

- Recent pay stubs (last 30 days)

- Stock compensation statements (RSUs, options, ESPP)

- Bonus and commission history (24 months)

- Rental income documentation if applicable

Asset Documentation:

- Two months of bank statements for all accounts

- Retirement account statements (401k, IRA)

- Investment account balances and statements

- Gift letter if receiving down payment assistance

- Explanation for recent large deposits

Credit and Employment:

- Authorization for credit report pull

- Employment verification letter on company letterhead

- Business ownership documentation (if self-employed)

- Explanation letters for credit inquiries or derogatory marks

This preparation enables brokers to provide accurate pre-approval letters that strengthen your position when competing in Seattle’s housing market.

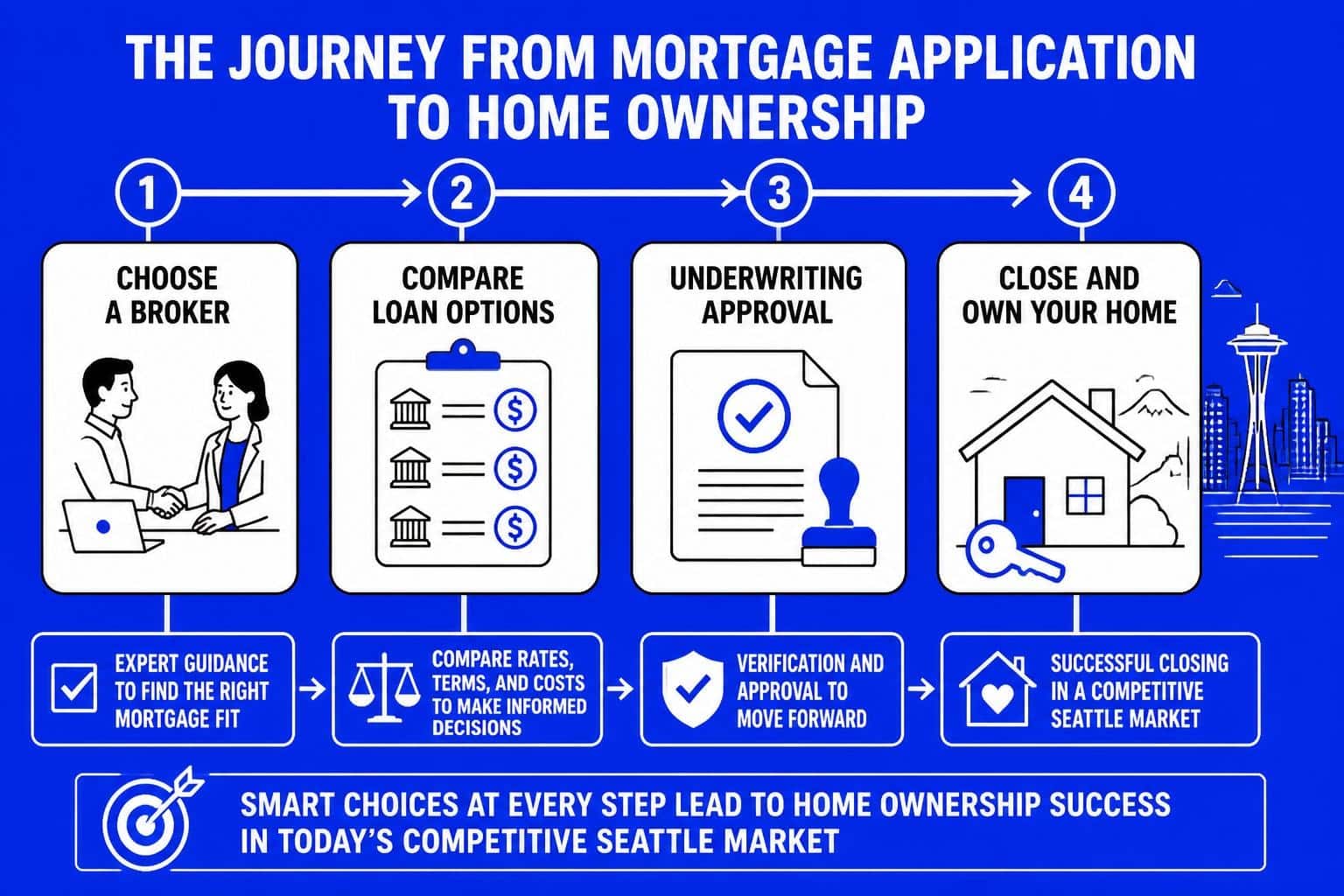

Mortgage Broker How To: Evaluating Loan Options

Once qualified, understanding how to compare loan programs prevents costly mistakes and ensures optimal financing. The mortgage broker how to process includes analyzing multiple scenarios to identify the best combination of rate, terms, and monthly payment.

Comparing Conventional vs. Jumbo Loans

For Seattle-area buyers, the distinction between conventional and jumbo loan programs matters significantly. In 2026, King County conforming loan limits affect which properties require jumbo financing.

Conventional Loan Characteristics:

- Loan amounts up to conforming limits ($766,550 in most King County areas)

- Down payment options from 3% to 20%

- Private mortgage insurance (PMI) required below 20% down

- Standardized underwriting through Fannie Mae or Freddie Mac

- Competitive rates due to government backing

Jumbo Loan Considerations:

- Required for purchase prices exceeding conforming limits

- Typically require larger down payments (10-20%)

- No PMI regardless of down payment amount

- Stricter credit and reserve requirements

- Specialized underwriting for stock compensation

Rate Comparison Strategy

| Loan Type | Typical Rate Range | Ideal Candidate | Key Benefit |

|---|---|---|---|

| 30-Year Fixed | 6.25% – 6.75% | Long-term stability seekers | Predictable payment |

| 15-Year Fixed | 5.50% – 6.00% | Equity builders | Lower total interest |

| 7/1 ARM | 5.75% – 6.25% | Short-term owners | Lower initial rate |

| Jumbo 30-Year | 6.50% – 7.25% | High-balance buyers | No PMI advantage |

Your broker should explain how different down payment amounts affect monthly payments, cash reserves, and overall purchasing power in neighborhoods like Everett or Lake Forest Park.

Working Effectively With Your Mortgage Broker

The mortgage broker how to relationship requires active participation and clear communication. Successful closings in competitive markets depend on responsiveness, transparency about changes in your financial situation, and trust in your broker's guidance.

Communication Best Practices

Establish clear expectations early:

- Response timeframes for questions and document requests

- Preferred communication channels (text, email, phone)

- Update frequency during critical phases like underwriting

- Escalation procedures if issues arise

- Timeline milestones from application to closing

For tech professionals with variable income, maintaining open dialogue about RSU vesting schedules and bonus payments prevents surprises during underwriting. Document any changes in employment status, income, or financial obligations immediately.

Common Pitfalls to Avoid

During the mortgage process, avoid these mistakes:

- Opening new credit accounts or making large purchases

- Changing jobs or employment status without disclosure

- Making large deposits without documentation

- Missing document request deadlines

- Assuming verbal approval equals final approval

Understanding the mortgage application timeline helps you plan accordingly and avoid delays that could jeopardize rate locks or purchase agreements in fast-moving Seattle neighborhoods.

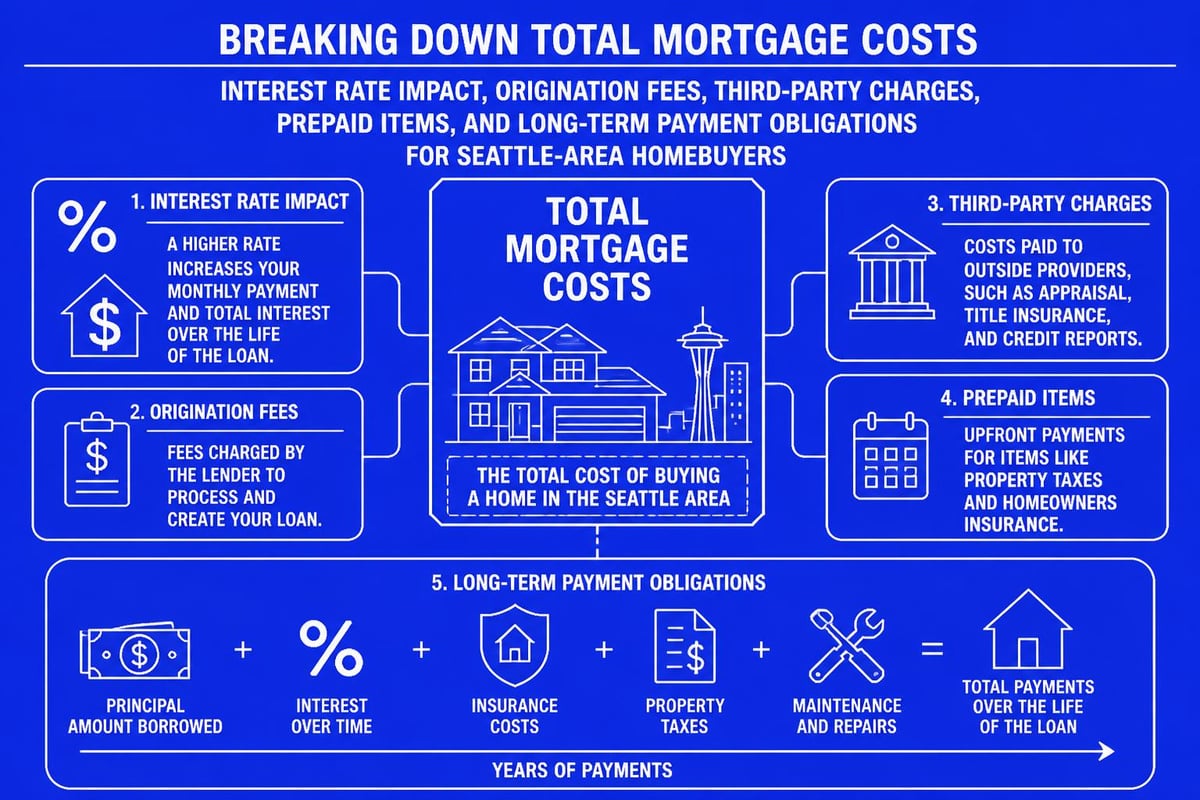

Mortgage Broker Compensation and Cost Transparency

Understanding how mortgage brokers are compensated removes mystery from the relationship and ensures you evaluate total loan costs accurately. In most cases, lenders pay broker compensation through wholesale rate pricing, meaning you're not charged separately for broker services.

Fee Structure Breakdown

Typical compensation models:

- Lender-paid compensation: Broker receives commission from lender (1-2% of loan amount)

- Borrower-paid fees: Origination charges added to closing costs

- Hybrid models: Combination of lender and borrower compensation

- No-cost options: Higher rate in exchange for zero origination fees

Reputable brokers provide Loan Estimates within three business days of application, clearly itemizing all costs including origination charges, discount points, third-party fees, and prepaid items. Compare these estimates across multiple scenarios to understand total cost implications.

Specialized Scenarios for Seattle Homebuyers

The mortgage broker how to approach varies based on property type, buyer profile, and financing needs. Seattle's diverse housing market from Shoreline single-family homes to Bellevue condominiums requires adaptable strategies.

First-Time Homebuyer Programs

Washington State offers several programs that experienced brokers leverage for qualified buyers:

Program Options:

- House Key Opportunity Loan: Down payment assistance up to 5% or $15,000

- House Key Home Advantage: Conventional financing with flexible terms

- FHA loans: 3.5% down payment with flexible credit requirements

- VA loans: Zero down for eligible veterans and active military

- Conventional 97: 3% down for qualified first-time buyers

These first-time buyer programs often include income limits and property price restrictions that vary by county, making local expertise essential.

Tech Professional Considerations

For employees at Seattle's major tech employers, mortgage qualification involves unique considerations:

- RSU income calculation: Typically averaged over two years of vesting history

- Bonus income verification: Requires two-year history for full consideration

- Stock volatility: Recent stock price fluctuations may affect calculated income

- Jumbo loan requirements: Higher balances require substantial liquid reserves

- Fast closing timelines: Ability to close in 9-15 business days for competitive offers

Working with a broker experienced in qualifying stock compensation ensures maximum borrowing power without documentation surprises.

Questions to Ask Your Mortgage Broker

The mortgage broker how to evaluation process includes asking specific questions that reveal expertise and service quality. These conversations should occur during initial consultations before committing to a lender.

Essential Interview Questions

Experience and Credentials:

- How many years have you been licensed in Washington State?

- What percentage of your loans are in the Seattle metro area?

- Do you specialize in any particular loan types or buyer profiles?

- How many loans did you close in 2025?

- What is your average time from application to closing?

Process and Communication:

- Who will handle my file after initial application?

- How quickly do you typically respond to questions?

- What happens if issues arise during underwriting?

- Can you provide references from recent clients?

- What makes your service different from other brokers?

Costs and Options:

- How are you compensated on this transaction?

- Can you show me multiple loan scenarios?

- What rate lock policies do your lenders offer?

- Are there options to reduce closing costs?

- How do your rates compare to direct lenders?

These questions establish baseline expectations and help you choose the right mortgage professional for your specific situation.

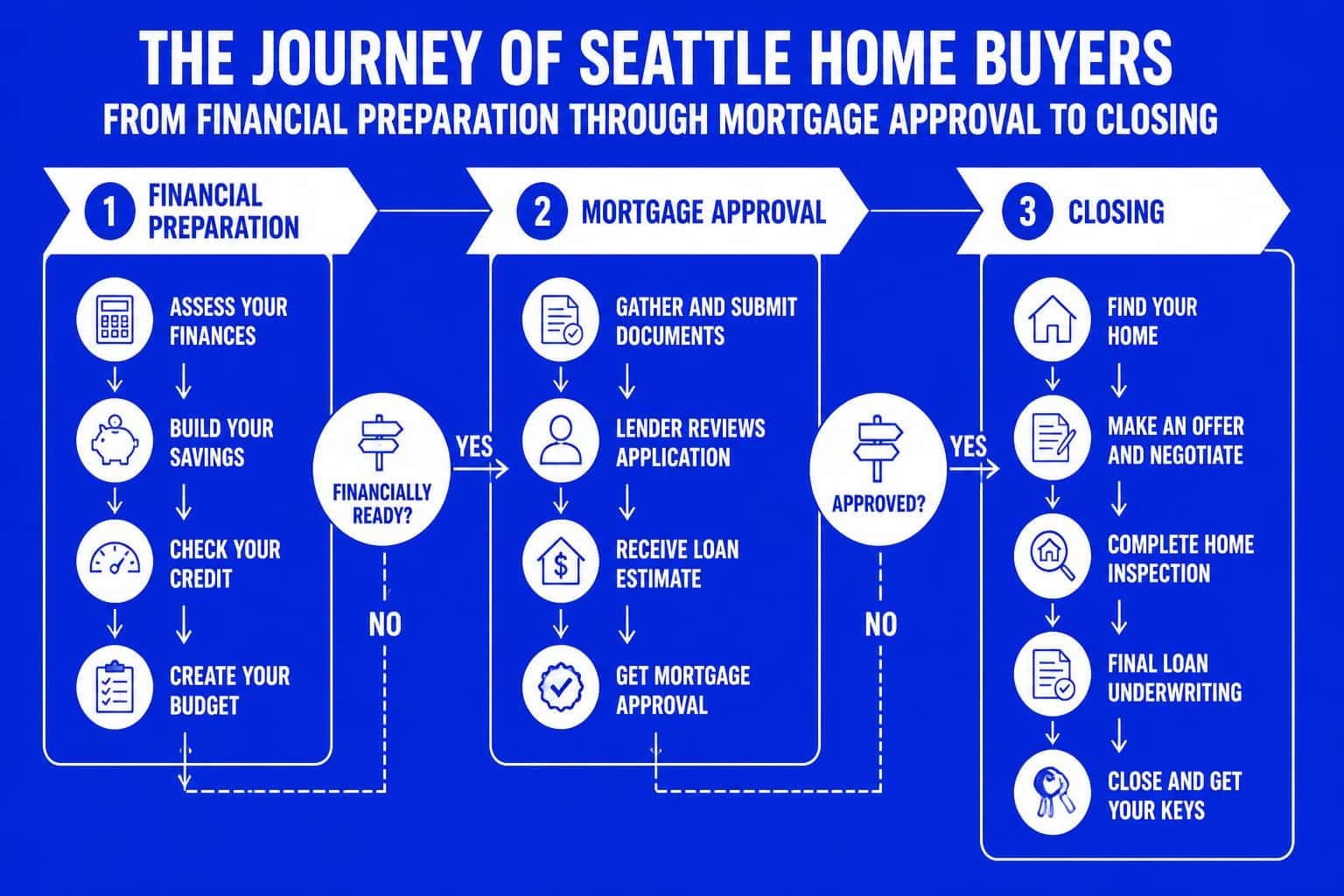

The Application to Closing Timeline

Understanding each phase of the mortgage process helps you anticipate requirements and avoid delays. In competitive markets like Redmond or Kirkland, timing often determines whether you win bidding wars or lose properties to cash offers.

Phase-by-Phase Breakdown

Pre-Approval (1-2 days):

- Submit initial documentation package

- Broker reviews credit, income, and assets

- Receive pre-approval letter with maximum loan amount

- Begin house hunting with financing confidence

Property Search and Offer (varies):

- Identify target property and negotiate terms

- Provide purchase agreement to broker

- Confirm loan amount and program selection

- Initiate formal loan application

Processing and Underwriting (7-14 days):

- Submit complete loan application with supporting documents

- Processor orders appraisal, title, and verifications

- Underwriter reviews file and issues conditions

- Respond to documentation requests promptly

- Receive conditional loan approval

Clear to Close (2-3 days):

- Satisfy all underwriting conditions

- Final verification of employment and assets

- Review Closing Disclosure for accuracy

- Schedule closing appointment with title company

Closing Day:

- Sign final loan documents and deed

- Transfer funds for down payment and closing costs

- Receive keys to your new home

Advanced underwriting capabilities enable qualified brokers to close transactions in as few as 9 business days when necessary for competitive situations.

Leveraging Broker Expertise in Competitive Markets

The Seattle housing market in 2026 remains highly competitive, particularly in desirable neighborhoods. Understanding how to maximize your broker's expertise provides strategic advantages when multiple offers compete for limited inventory.

Pre-Approval Strength Strategies

Strong pre-approval letters include:

- Verification that income, assets, and credit have been reviewed

- Specific loan amount rather than generic ranges

- Lender name and direct contact information

- Expiration date showing recent qualification

- Minimal contingencies or conditions

Some brokers offer underwritten pre-approvals where files receive preliminary underwriting review before offers, providing sellers with additional confidence in financing certainty.

Alternative Financing Approaches

| Strategy | Best For | Key Advantage | Consideration |

|---|---|---|---|

| Larger Down Payment | Cash-rich buyers | Lower monthly payment | Reduced liquidity |

| Rate Buydown | Long-term owners | Permanent rate reduction | Upfront cost |

| ARM Products | Short-term owners | Lower initial rate | Future adjustment risk |

| Mortgage Recast | Post-closing windfall | Lower payment, keep rate | Lump sum required |

Understanding options like mortgage recasting provides flexibility for buyers expecting bonuses, RSU vesting, or inheritance funds after closing.

Local Market Expertise Matters

Working with a broker who understands Seattle's unique neighborhoods, pricing trends, and buyer demographics ensures recommendations align with market realities. Properties in Lake Forest Park require different strategies than homes in downtown Seattle high-rises.

Neighborhood-Specific Considerations

Seattle Urban Core:

- Condo financing requires warrantability review

- HOA financial health impacts loan approval

- Parking and storage affect property value

- Rental restriction limitations for investment properties

Eastside Suburbs (Bellevue, Redmond, Kirkland):

- Higher price points often require jumbo financing

- Excellent schools drive family buyer competition

- Tech professional concentration influences buyer profiles

- New construction options with builder incentives

North End (Shoreline, Lynnwood, Mill Creek, Everett):

- More affordable entry points for first-time buyers

- Growing tech commuter population

- Mix of urban and suburban property types

- Strong appreciation potential in developing areas

A local Seattle mortgage broker brings invaluable insights about property values, neighborhood trends, and competitive positioning strategies.

Post-Closing Relationship Value

The mortgage broker how to relationship doesn't end at closing. Experienced professionals provide ongoing value through rate monitoring, refinance opportunities, and strategic financial planning as your situation evolves.

Ongoing Support Areas

Rate monitoring services:

- Notification when rates drop significantly

- Refinance analysis showing break-even calculations

- Strategy consultation for changing financial goals

- Market updates specific to Seattle-area trends

Future purchase planning:

- Investment property financing guidance

- Second home loan options

- Construction loan expertise

- Portfolio lending for multiple properties

Financial life changes:

- Divorce or separation loan modifications

- Inheritance investment strategies

- Job changes and income qualification updates

- Credit improvement programs and timeline planning

Building a long-term relationship with a trusted broker creates ongoing value beyond single transactions, particularly as you build wealth through real estate in appreciating Seattle markets.

Understanding mortgage broker how to strategies empowers you to make confident financing decisions in Seattle's competitive housing market. The right broker provides expertise in complex income qualification, access to diverse loan programs, and strategic guidance throughout the home buying process. Whether you're purchasing your first home in Lake Forest Park, upgrading to a larger property in Bellevue, or qualifying stock compensation for a jumbo loan, working with an experienced professional makes the difference between uncertainty and confidence. Keith Akada brings 25+ years of expertise helping Seattle-area homebuyers navigate every aspect of mortgage financing, from pre-approval through closing in as few as 9 business days. If you're ready to explore your financing options with a highly-reviewed local expert, connect with Mortgage Reel to start your homeownership journey today.