Navigating the Seattle housing market as a prospective homeowner requires more than just finding the right property-it demands strategic financial planning, market awareness, and expert guidance. Home buyers in 2026 face a unique landscape shaped by evolving interest rates, competitive neighborhoods across Seattle, Bellevue, Redmond, and Kirkland, and innovative financing options designed to maximize purchasing power. Whether you're a first-time purchaser or a seasoned investor, understanding the mortgage process and available programs can mean the difference between securing your dream home and missing out in this dynamic market.

Understanding Today's Home Buyer Landscape in Seattle

The Greater Seattle area continues to attract home buyers from diverse backgrounds, particularly tech professionals working at Amazon, Microsoft, Google, and other major employers. These buyers often possess unique compensation structures that require specialized mortgage expertise to properly qualify income from RSUs, stock options, and performance bonuses.

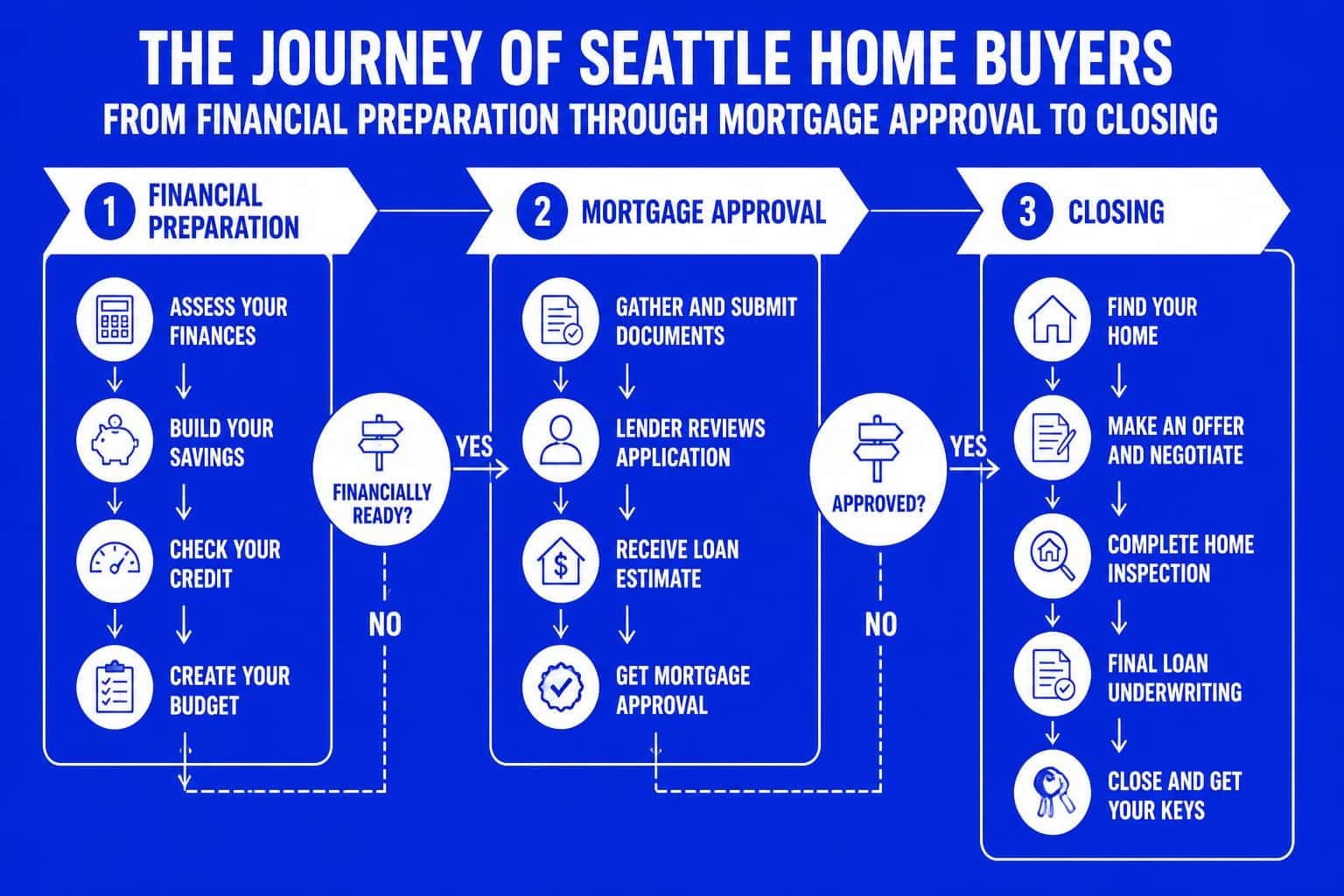

Market conditions in 2026 reflect ongoing shifts in inventory levels, pricing trends, and financing requirements. Home buyers must navigate these variables while maintaining realistic expectations about affordability and competition. The first steps every home buyer should take involve comprehensive financial assessment and pre-approval preparation.

Financial Readiness for Home Buyers

Before touring properties or submitting offers, home buyers should establish their financial foundation through several critical steps:

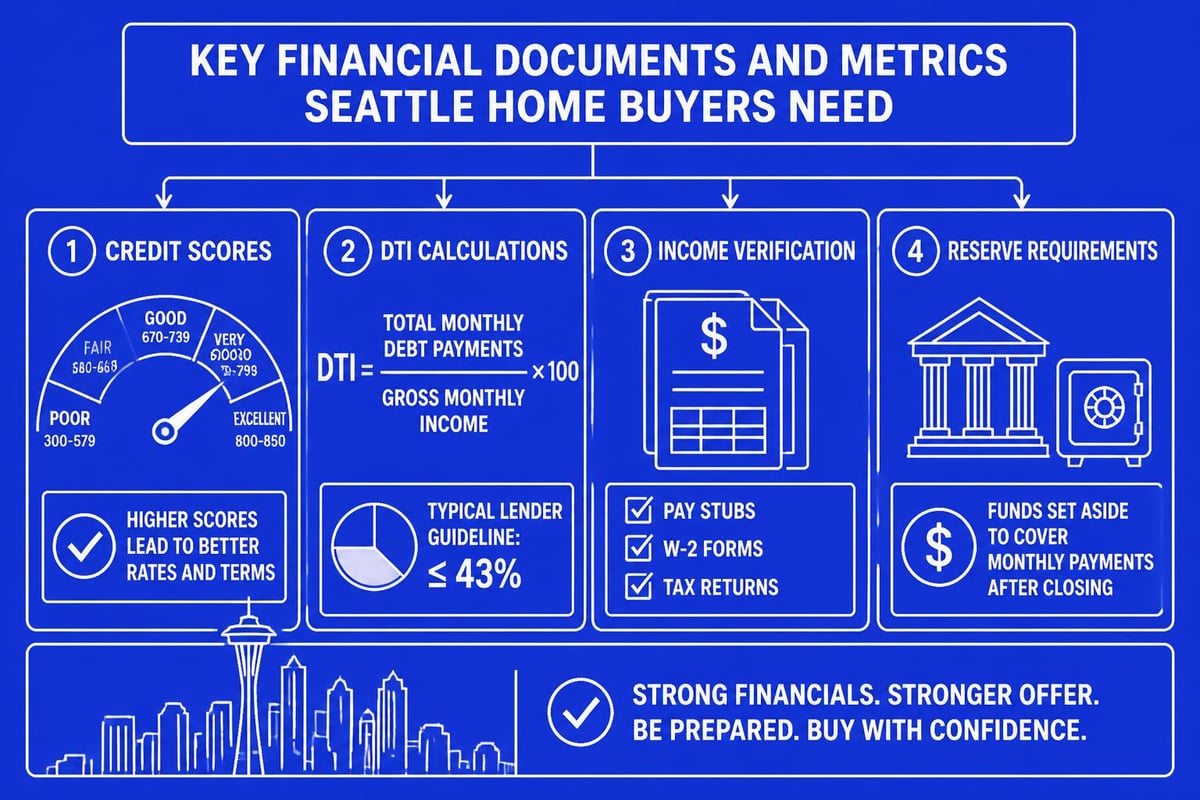

- Credit score optimization: Most conventional loans require minimum scores of 620, though competitive rates typically start at 740 or higher

- Debt-to-income ratio management: Lenders generally prefer DTI ratios below 43%, though some programs allow up to 50%

- Emergency fund maintenance: Beyond down payment and closing costs, maintaining 3-6 months of reserves demonstrates financial stability

- Income documentation preparation: W-2s, tax returns, pay stubs, and for self-employed buyers, detailed business financials

Understanding these fundamentals helps home buyers position themselves favorably when competing for properties in desirable neighborhoods throughout Seattle, Shoreline, and Lynnwood.

Down Payment Strategies for Different Buyer Types

Down payment requirements vary significantly based on loan type, property price, and borrower qualifications. Home buyers often assume they need 20% down, but numerous options exist with lower entry points.

| Loan Program | Minimum Down Payment | PMI Requirement | Best For |

|---|---|---|---|

| Conventional | 3% – 5% | Yes, if under 20% | Strong credit borrowers |

| FHA | 3.5% | Mandatory MIP | Lower credit scores |

| VA | 0% | None | Eligible veterans |

| Jumbo | 10% – 20% | Varies by lender | High-value properties |

For tech professionals in Seattle's competitive market, understanding how to structure down payments while preserving cash for other investments becomes crucial. A conventional loan with 5% down often provides the flexibility many buyers need without depleting liquid assets entirely.

Alternative Down Payment Approaches

Home buyers in 2026 have access to creative strategies beyond traditional savings. Gift funds from family members remain popular, provided proper documentation and sourcing requirements are met. Down payment assistance programs, though limited in higher-cost markets like Seattle, occasionally offer support for qualified buyers.

Employer-sponsored homeownership programs have expanded, particularly among tech companies seeking to retain talent. These benefits might include matching contributions, low-interest loans, or outright grants toward down payments. Home buyers should investigate whether their employer offers such programs before finalizing their financing strategy.

The debate around whether to put 10% or 20% down on jumbo loans illustrates the complexity of optimizing down payment amounts based on individual circumstances, investment opportunities, and risk tolerance.

Maximizing Buying Power with Complex Income

Seattle's concentration of high-earning tech professionals creates unique opportunities and challenges for home buyers with stock-based compensation. Traditional lending guidelines have evolved to better accommodate RSUs, stock options, and bonus income, but proper qualification requires expertise and strategic documentation.

Stock Compensation Qualification Process

Lenders evaluate equity compensation differently based on vesting schedules, grant types, and historical consistency. Home buyers with significant RSU income should understand these key factors:

- Two-year history requirement: Most lenders need at least two years of documented stock compensation to include it in qualifying income

- Vesting schedule consideration: Future vesting alone doesn't qualify-only vested or near-term vesting schedules receive full credit

- Tax impact calculations: Lenders account for withholding and marginal tax rates when determining net qualifying income

- Volatility adjustments: Some underwriters apply haircuts to stock compensation based on price volatility and market conditions

For home buyers in Bellevue, Redmond, and Kirkland with substantial equity compensation, working with a mortgage broker experienced in tech income qualification ensures maximum buying power without unnecessary income reductions.

Bonus income follows similar qualification patterns, requiring consistent year-over-year receipt and averaging calculations. Home buyers should gather comprehensive employment documentation, including offer letters, equity grant agreements, and detailed compensation breakdowns.

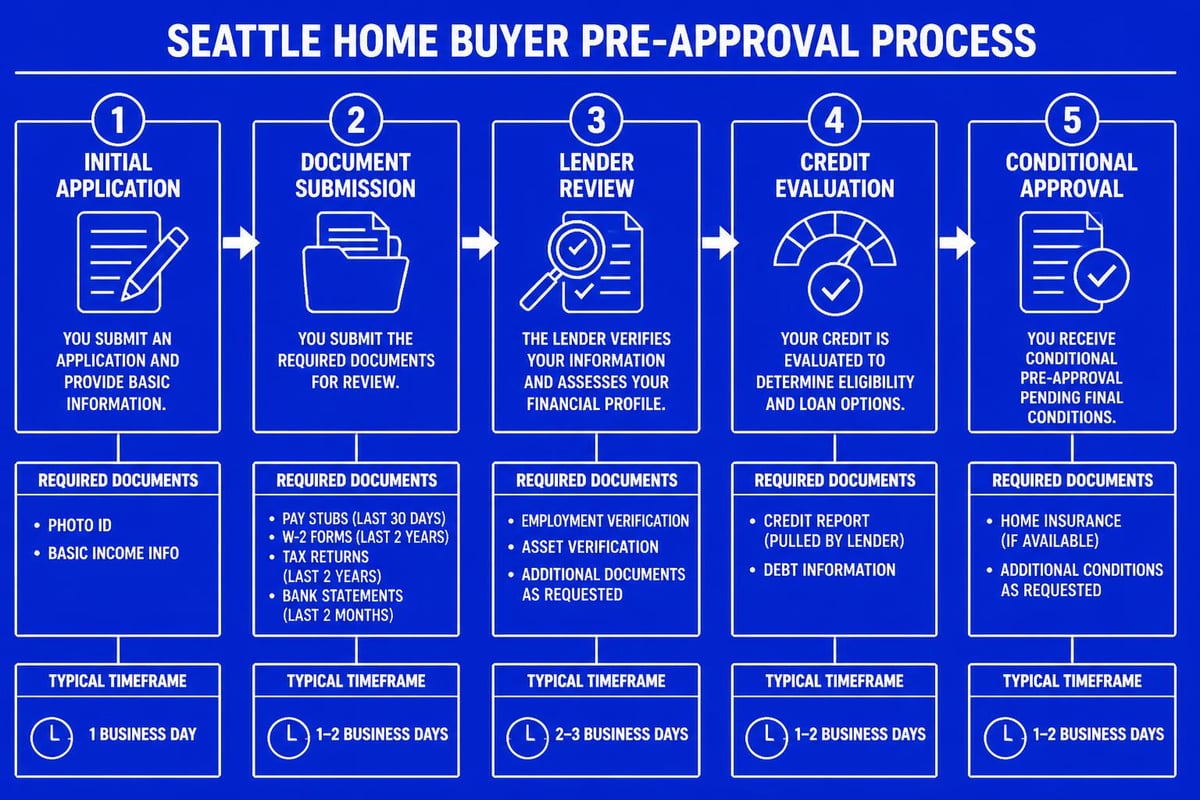

Navigating the Pre-Approval Process

Pre-approval represents one of the most critical steps for serious home buyers. In competitive Seattle neighborhoods, offers without strong pre-approval letters rarely succeed. The process involves comprehensive financial review, credit analysis, and preliminary underwriting.

Components of Strong Pre-Approval

Effective pre-approval goes beyond simple qualification. Home buyers benefit from understanding exactly what lenders review and how to present the strongest financial profile:

- Asset verification: Complete documentation of checking, savings, investment, and retirement accounts

- Income stability: Employment history showing consistent or increasing earnings in the same field

- Credit explanation: Proactive clarification of any credit issues, recent inquiries, or account changes

- Property parameters: Clear understanding of target price ranges, desired neighborhoods, and property types

The timeline for home loan approval typically spans 3-5 business days for initial pre-approval, though complex income situations may require additional review. Home buyers should initiate this process well before beginning their property search.

Strategic Offer Preparation in Competitive Markets

Once pre-approved, home buyers must develop competitive offer strategies that balance price, contingencies, and closing timelines. Seattle's market dynamics often favor buyers who can demonstrate financial strength and transaction certainty.

Crafting Compelling Offers

Beyond offering price, several factors influence seller decisions. Home buyers should consider these elements when structuring proposals:

Financial strength indicators include larger earnest money deposits, proof of substantial reserves beyond closing costs, and flexible appraisal gap coverage. Sellers gain confidence from buyers who can absorb minor valuation discrepancies without renegotiation.

Timeline flexibility often matters as much as price. Some sellers prioritize quick closes, while others need extended timelines for their own purchase. Home buyers working with lenders capable of closing in 9-12 business days gain significant competitive advantages.

Contingency streamlining requires careful risk assessment. While inspection contingencies protect buyers, pre-inspection strategies allow more aggressive offers. Financing contingencies remain standard, but home buyers with strong pre-approval can sometimes offer shorter review periods.

For properties in Mill Creek or Everett where competition may be less intense, home buyers might negotiate more favorable terms while maintaining standard protections. Market conditions vary significantly across the Greater Seattle area, requiring localized strategy adjustments.

Mortgage Program Selection for Different Scenarios

Home buyers face numerous loan program options, each with distinct advantages, requirements, and ideal use cases. Matching the right program to individual circumstances optimizes both short-term affordability and long-term financial outcomes.

Conventional Loans for Strong Borrowers

Conventional financing offers the most flexibility and favorable terms for home buyers with solid credit and stable income. These loans conform to Fannie Mae and Freddie Mac guidelines, providing consistent underwriting standards nationwide.

Advantages include lower overall costs compared to government-backed programs, elimination of mortgage insurance once reaching 20% equity, and higher loan limits accommodating Seattle's elevated home prices. Home buyers should explore whether conventional financing aligns with their financial profile.

Government-Backed Programs

FHA loans remain popular among home buyers with lower credit scores or limited down payment savings. The 3.5% down payment requirement and flexible credit guidelines open homeownership to broader buyer pools. However, mandatory mortgage insurance premiums persist for the loan's life on most FHA mortgages, increasing long-term costs.

VA loans offer unmatched benefits for eligible veterans and service members. Zero down payment requirements, no mortgage insurance, and competitive interest rates make VA financing highly attractive. Home buyers with military service should explore these benefits through specialized lenders familiar with VA underwriting.

Jumbo Loan Considerations

Seattle's median home prices frequently exceed conventional loan limits, pushing many home buyers into jumbo territory. These loans require more substantial down payments, stronger credit profiles, and comprehensive income documentation. Understanding jumbo loan qualification requirements helps buyers prepare appropriately.

| Factor | Conventional | FHA | VA | Jumbo |

|---|---|---|---|---|

| Credit Score | 620+ | 580+ | No minimum | 700+ |

| Down Payment | 3% – 20% | 3.5% | 0% | 10% – 20% |

| Loan Limit 2026 | $806,500 | $498,257 | $806,500 | Above conforming |

| Income Documentation | Standard | Flexible | Standard | Extensive |

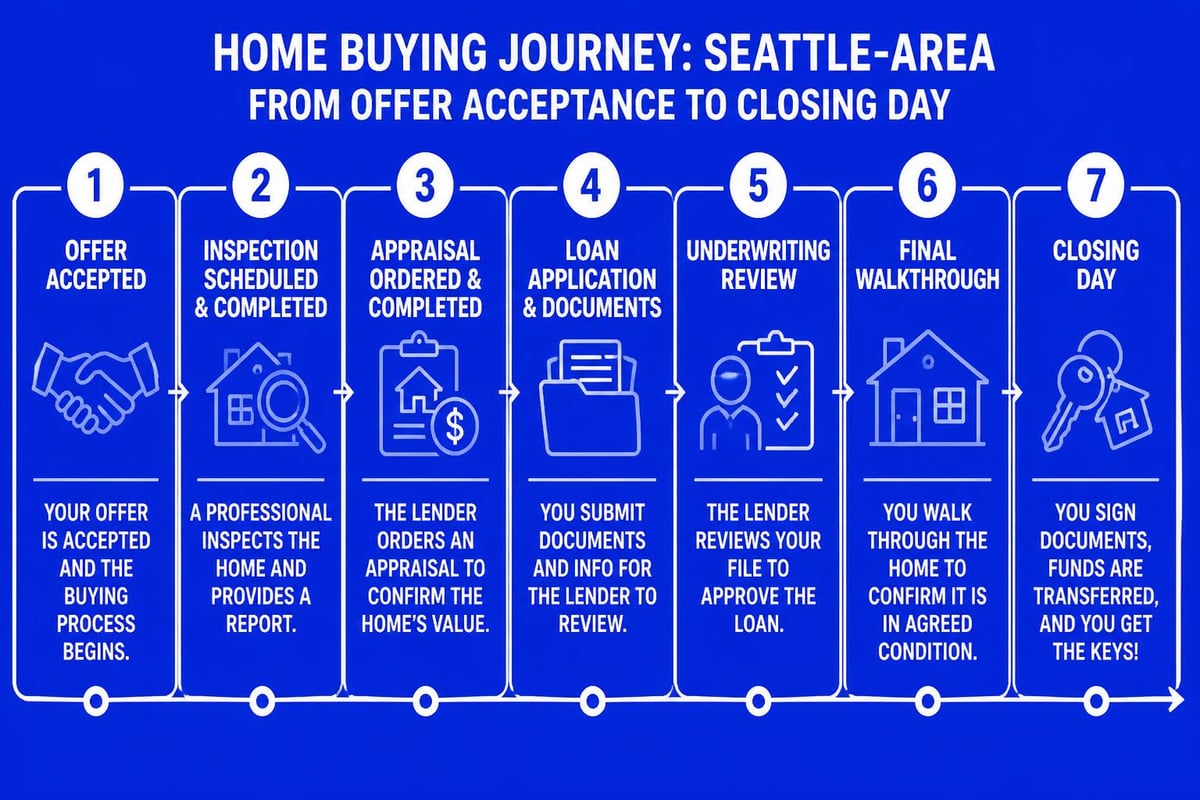

Managing the Closing Process

Once under contract, home buyers enter the closing phase involving inspections, appraisals, final underwriting, and numerous coordinating details. This period typically spans 30-45 days, though experienced lenders can compress timelines significantly.

Critical Closing Milestones

Understanding the sequence of events helps home buyers anticipate requirements and avoid delays:

- Inspection period (Days 1-10): Professional property evaluation and negotiation of repairs or credits

- Appraisal ordering (Days 3-5): Lender-required valuation to confirm purchase price aligns with market value

- Title review (Days 10-20): Examination of property ownership history and identification of potential liens

- Final underwriting (Days 20-35): Comprehensive review of all documentation and conditions clearance

- Closing preparation (Days 35-40): Final walkthrough, wire instructions, and document signing coordination

Home buyers should maintain close communication with their loan officer throughout this period. Any changes to employment, credit, or financial status must be disclosed immediately, as lenders verify conditions up until funding.

Avoiding Common Home Buyer Pitfalls

Experience reveals patterns in mistakes that cost home buyers money, time, or opportunities. Awareness of these common errors enables proactive avoidance and smoother transactions.

Financial Missteps to Prevent

Several financial errors frequently impact home buyers during the purchase process. Making large purchases on credit before closing can derail approvals, as new debt alters qualification ratios. Similarly, changing jobs-even for higher pay-can complicate income verification and delay closing.

Cash deposits without clear paper trails raise red flags during underwriting. Home buyers receiving gift funds should ensure proper documentation before depositing amounts. Large, unexplained deposits often require extensive documentation and may be excluded from qualifying assets.

According to insights shared by homeowners who learned difficult lessons, rushing into purchases without thorough due diligence commonly leads to buyer's remorse and unexpected expenses.

Market and Property Selection Errors

Overextending budgets represents perhaps the most consequential mistake. Home buyers should consider not just mortgage payments, but property taxes, insurance, maintenance, and HOA fees. Seattle's high property taxes and insurance costs can substantially increase monthly obligations beyond principal and interest.

Skipping thorough property inspections to strengthen offers occasionally backfires spectacularly. Even in competitive situations, home buyers should insist on professional inspections or accept known risks explicitly. Guidance on navigating tough housing markets emphasizes balancing competitiveness with prudent risk management.

Specialized Strategies for First-Time Home Buyers

First-time home buyers face unique challenges and opportunities. Lack of experience, limited savings, and uncertainty about the process can create hesitation and missed opportunities. However, numerous resources and programs specifically support this buyer segment.

Educational preparation significantly impacts outcomes. First-time home buyers benefit from understanding comprehensive buying strategies before beginning their search. This knowledge empowers confident decision-making and reduces anxiety throughout the process.

First-Time Buyer Programs and Benefits

Several advantages specifically target first-time home buyers. While down payment assistance initiatives vary by administration and local jurisdiction, investigating available programs often uncovers valuable support.

First-time buyer status also enables IRA withdrawal provisions allowing up to $10,000 in penalty-free distributions for home purchases. This provision helps buyers bridge down payment gaps without incurring early withdrawal penalties.

Working with professionals experienced in first-time buyer challenges and solutions provides valuable guidance through unfamiliar territory. These specialists understand the questions, concerns, and education needs unique to first-time purchasers.

Additional resources from established financial institutions offer valuable frameworks. Charles Schwab’s tips for first-time buyers emphasize financial preparedness and realistic expectations. Similarly, NerdWallet’s comprehensive guide covers essential steps from affordability assessment through closing.

Local Market Considerations Across Greater Seattle

Home buyers should recognize that market conditions, pricing, and competition vary significantly across Seattle neighborhoods and surrounding cities. Understanding these local nuances enables more strategic property searches and realistic expectations.

Seattle Urban Neighborhoods

Central Seattle neighborhoods like Capitol Hill, Queen Anne, and Wallingford attract home buyers seeking walkable, urban lifestyles with proximity to employment centers. These areas typically command premium prices with intense competition. Properties often receive multiple offers, requiring aggressive pricing and strong terms.

Inventory constraints in these core neighborhoods mean home buyers must act decisively when suitable properties emerge. Pre-approval, flexible timelines, and willingness to compete aggressively distinguish successful buyers from those repeatedly outbid.

Eastside Communities

Bellevue, Redmond, and Kirkland draw substantial home buyer interest due to proximity to major tech employers, highly-rated schools, and newer housing stock. These cities often see buyers from Amazon, Microsoft, and other eastside companies seeking short commutes.

Property values in these markets reflect strong demand and limited inventory. Home buyers should expect competitive bidding and premium pricing, particularly for single-family homes in desirable school districts.

North Seattle and Beyond

Shoreline, Lake Forest Park, Lynnwood, Mill Creek, and Everett offer more diverse pricing and property options. Home buyers priced out of central Seattle or eastside markets often find excellent value in these communities while maintaining reasonable commute access.

These areas attract families prioritizing larger properties, good schools, and more affordable entry points. Competition exists but often proves less intense than core Seattle markets, allowing home buyers slightly more negotiating leverage.

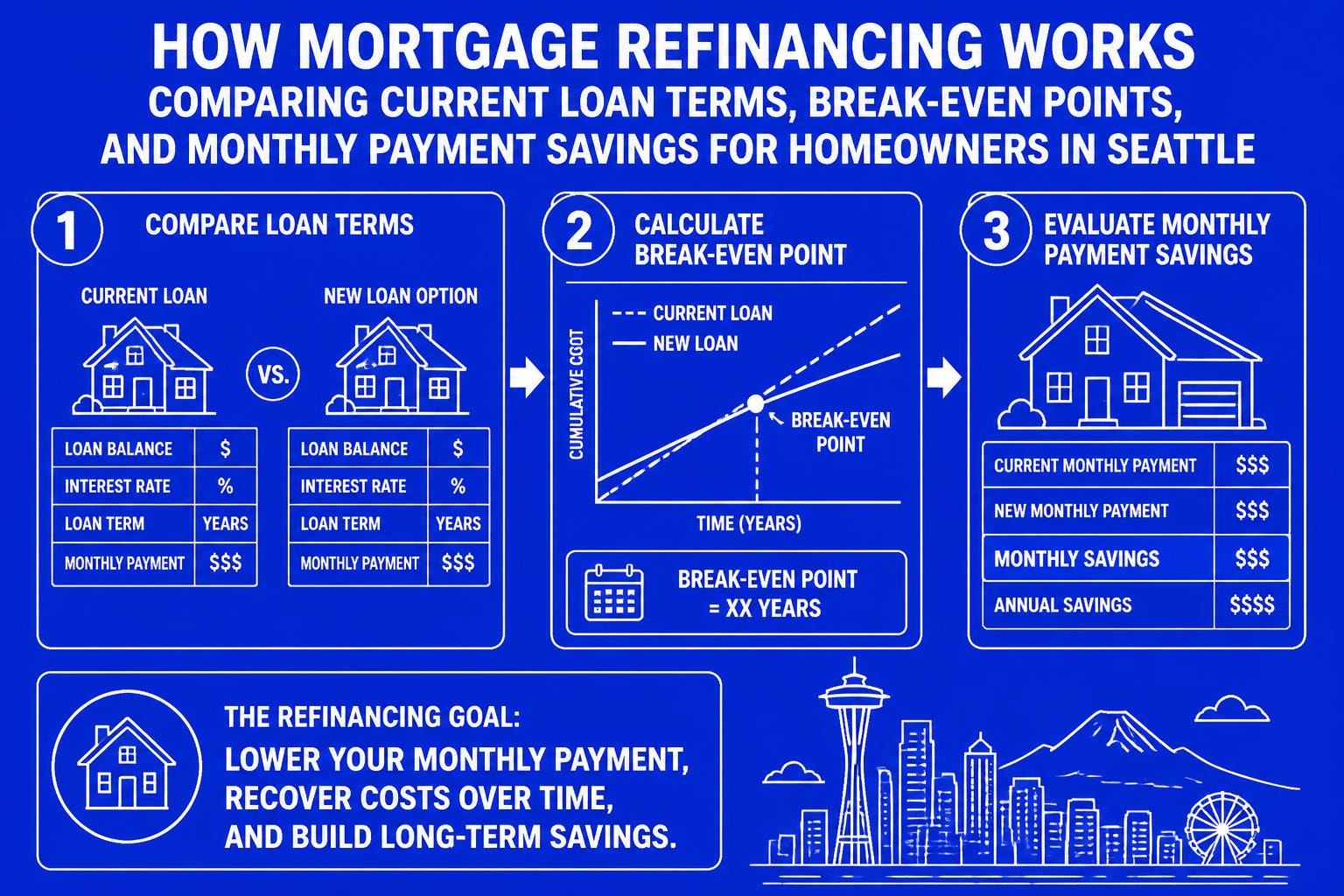

Refinancing Considerations for Future Planning

While this guide focuses primarily on purchase transactions, home buyers should understand how their initial loan selection impacts future refinancing opportunities. Market conditions, rate environments, and personal circumstances change over time, making refinancing strategy part of comprehensive homeownership planning.

When Refinancing Makes Sense

Home buyers who initially accept higher rates due to credit or financial limitations should plan to refinance once circumstances improve. Credit score increases, debt paydown, or income growth can unlock significantly better terms 12-24 months after purchase.

Similarly, home buyers utilizing FHA financing might refinance to conventional loans after reaching 20% equity, eliminating ongoing mortgage insurance premiums. This strategy reduces monthly obligations and long-term interest costs substantially.

Understanding these future possibilities helps home buyers make informed initial loan selections, balancing immediate needs against long-term optimization opportunities.

Successfully navigating the home buying journey requires financial preparation, market knowledge, and expert guidance tailored to your unique situation. Whether you're a first-time buyer, tech professional with complex compensation, or experienced investor, understanding financing strategies and local market dynamics positions you for confident decision-making. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping home buyers across Seattle, Bellevue, Redmond, and Kirkland secure optimal financing with transparent communication and proven execution. With specialized expertise in qualifying stock compensation and the ability to close in as few as 9 business days, we're ready to guide you through every step of your home purchase. Start your journey today with Mortgage Reel.